Fertilizer Spreader Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Market Size (2026) | USD 4.33 Billion |

| Market Size (2031) | USD 5.72 Billion |

| Growth Rate (2026 - 2031) | 5.72% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | Europe |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Fertilizer Spreader Market Analysis by Mordor Intelligence

The fertilizer spreader market size was valued at USD 4.1 billion in 2025 and estimated to grow from USD 4.33 billion in 2026 to reach USD 5.72 billion by 2031, at a CAGR of 5.72% during the forecast period (2026-2031). Evolving precision-farming practices, acute labor shortages, and tightening environmental regulations are compelling growers to replace or upgrade conventional equipment with GPS-enabled variable-rate machines. Rotary spinner designs still dominate large-acreage grain production because of their wide swath coverage, yet pneumatic airflow systems are gaining traction where uniformity and multi-nutrient accuracy drive yield. Subsidy programs in North America and Europe are shortening payback cycles for high-specification spreaders, and digital sales channels are unlocking new routes to market for smaller brands. Meanwhile, rising demand for granular micronutrient blends and in-season liquid fertilization is widening the product mix that manufacturers must support.

Key Report Takeaways

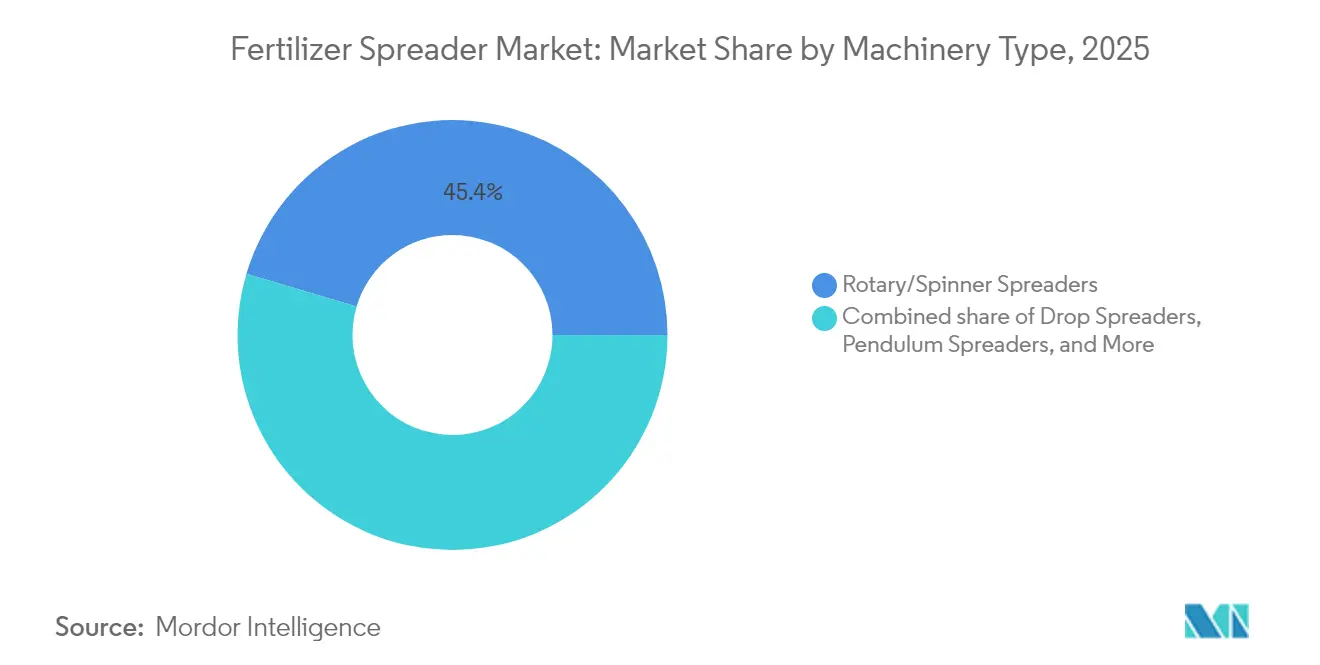

- By machinery type, rotary/spinner equipment led with 45.40% revenue share in 2025, while pneumatic airflow systems are projected to expand at a 9.18% CAGR through 2031.

- By 2025, conventional non-GPS configurations held a 71.20% market share of the fertilizer spreader market, whereas precision/GPS-guided variants were growing at a 10.52% CAGR to 2031.

- By drive mechanism, PTO-driven mounted spreaders accounted for 37.50% of the fertilizer spreader market size in 2025, while self-propelled units registered the fastest pace at 9.92% CAGR.

- By fertilizer form, granular products captured 77.40% of demand in 2025, with liquid formulations advancing at an 7.88% CAGR.

- By end-use application, row-crop farms accounted for a 66.20% share of the fertilizer spreader market size in 2025, while the specialty/horticulture segment is projected to rise at a 7.55% CAGR.

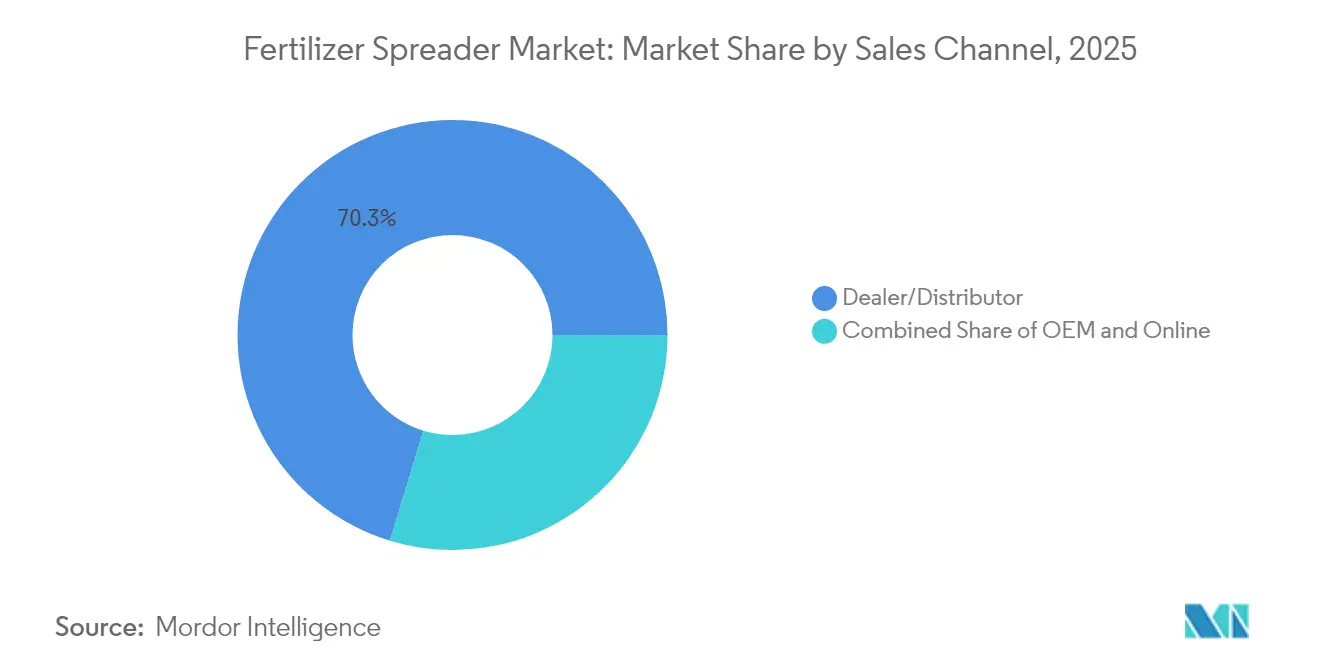

- By sales channel, dealer/distributor storefronts retained a 70.30% share in 2025, yet the online segment is accelerating at a 10.78% CAGR.

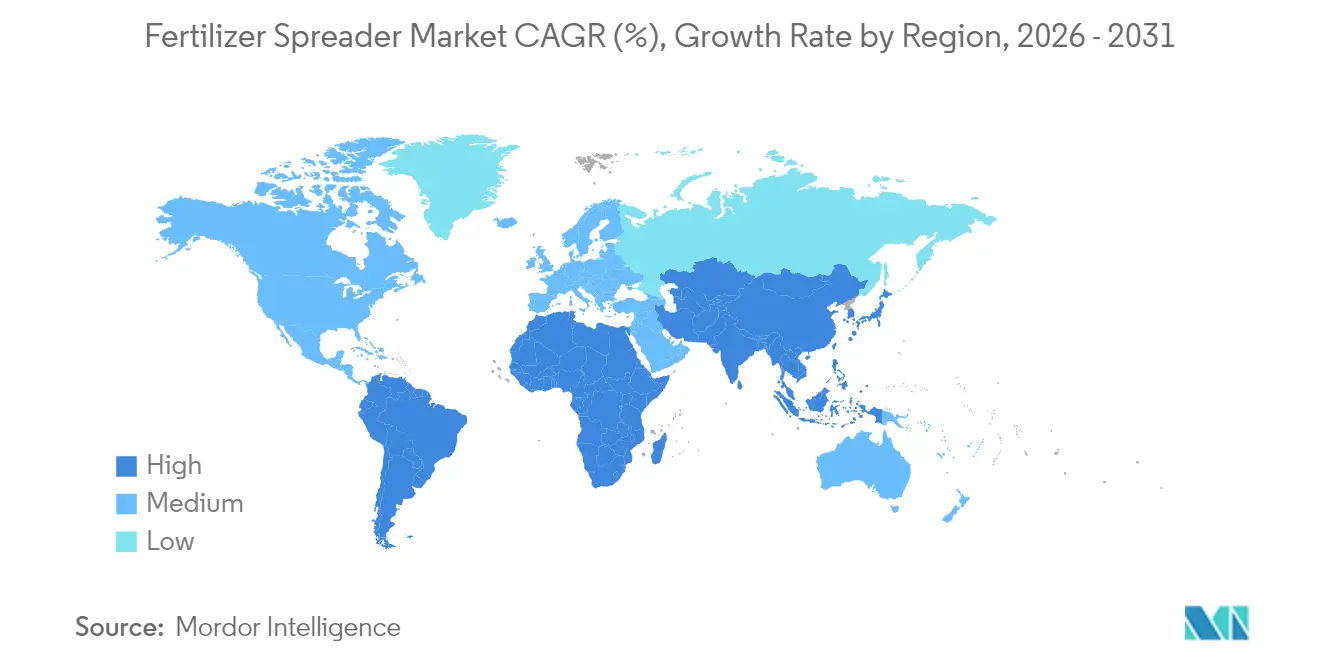

- By region, Europe commanded 28.70% revenue share during 2025, whereas Asia-Pacific shows the steepest climb at 7.45% CAGR.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Fertilizer Spreader Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising global calorie demand and arable-land scarcity | +1.2% | Global, Asia-Pacific, Sub-Saharan Africa | Long term (≥ 4 years) |

| Shortage and the rising cost of agricultural labor stimulate mechanization | +1.8% | North America and Europe core, South America | Medium term (2-4 years) |

| Subsidy programmes for precision-fertilizer equipment | +0.9% | Europe, North America, select Asia-Pacific markets | Short term (≤ 2 years) |

| Adoption of variable-rate technology (VRT) for fertilizer | +1.4% | Global, led by developed markets | Medium term (2-4 years) |

| Shift to granular micronutrient blends requiring high-accuracy spread | +0.7% | Global, high-value crop regions | Long term (≥ 4 years) |

| The surge of carbon credit schemes rewarding optimized nutrient use | +0.5% | North America, Europe, emerging Asia-Pacific | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising Global Calorie Demand and Arable-Land Scarcity

Steady population growth and changing diets are driving the rising expectations for increased yield per acre. Due to the limited land expansion potential, uniform nutrient placement through advanced airflow machines is becoming increasingly critical for high-value crops. Variable-rate spreaders that sync with soil-mapping platforms enable growers to fine-tune applications, maximizing output from existing hectares. These capabilities support export-oriented producers in the Asia-Pacific and Africa, trying to lift productivity without aggravating soil degradation. Manufacturers that can prove a aiming to boost productivity without exacerbating field-level return on investment are well-positioned to ride this secular demand wave.

Shortage and the Rising Cost of Agricultural Labour Stimulate Mechanization

Farm operations in North America and Western Europe are facing double-digit wage inflation and persistent labor shortages. Self-propelled spreaders reduce crew requirements and can finish multi-field routes before weather windows close, turning labor scarcity into a catalyst for adoption. GPS autosteer and blockage sensors enable less-experienced drivers to achieve overlap accuracy comparable to that of skilled operators, thereby mitigating the talent bottleneck. South American growers confronting seasonal labor migration trends are also adopting higher-capacity PTO units to maintain throughput. Equipment suppliers that bundle remote diagnostics and operator training stand to capture additional service revenue.

Subsidy Programmes for Precision-Fertilizer Equipment

Canadian, British, and European Union grant schemes cover 30-50% of the purchase costs for variable-rate spreaders, rapidly tipping the cost-benefit analysis in favor of higher-spec models. Canada’s Agricultural Clean Technology program offers non-repayable contributions of up to CAD 2 million (USD 1.4 million) for greenhouse-gas-reducing machinery, explicitly listing precision fertilizer applicators as eligible[1]Source: "Agricultural Clean Technology Program," Agriculture and Agri-Food Canada, agriculture.canada.ca. In the United Kingdom, DEFRA’s Technology Fund earmarked £31 million (approximately USD 40 million) in 2024 for equipment that reduces nutrient and pesticide losses. Early farm-gate data indicate that grantees shorten spreader payback periods by 18-24 months compared to non-supported purchases[2]Source: "Farming Equipment and Technology Fund," Department for Environment, Food & Rural Affairs, gov.uk .

Adoption of Variable-Rate Technology (VRT) for Fertilizer

As sensor prices fall and agronomic data proliferate, growers are shifting from simple sectional control to zone-specific nutrient scripts generated from yield maps and soil conductivity scans. Purdue University field trials show VRT cuts fertilizer use by 7-12% while sustaining yields, improving gross margins on both arable and specialty crops. Cloud connectivity lets operators upload as-applied maps that satisfy regulatory audits and carbon credit verification. Dealers report retrofit VRT controllers as a high-growth aftermarket niche because they upgrade legacy spreaders at a modest cost[3]Source: "Precision Agriculture and Fertilizer Efficiency," Purdue University, docs.lib.purdue.edu.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High upfront cost vs. conventional broadcast methods | -1.6% | Global, acute in developing markets | Short term (≤ 2 years) |

| Low farmer awareness in smallholder economies | -0.8% | Sub-Saharan Africa, South Asia, and parts of South America | Medium term (2-4 years) |

| Fragmented after-sales and calibration service networks | -0.6% | Rural areas globally, pronounced in emerging markets | Medium term (2-4 years) |

| Sensitivity to fertilizer price volatility and farm income swings | -0.9% | Global, particularly commodity-dependent regions | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

High Upfront Cost vs. Conventional Broadcast Methods

Price tags on advanced spreaders range from USD 25,000 to USD 200,000, a hurdle for small and medium farms operating on thin margins. Credit access is uneven across emerging economies, so growers prioritize near-term liquidity over multi-year efficiency gains. Equipment-as-a-service models that charge per-hectare usage and retrofit VRT kits targeting legacy spinners are gaining popularity as bridge solutions. OEMs are experimenting with subscription packages bundling hardware, software updates, and agronomic advice to flatten capital spikes and widen market reach.

Low Farmer Awareness in Smallholder Economies

Information gaps on calibration, data interpretation, and economic payback slow precision spreader uptake across smallholder regions. Limited extension capacity and scant local demonstrations leave growers unconvinced that digital prescriptions will work on variable tropical soils. Studies show that peer-to-peer trial plots and mobile-based advisory services sharply improve adoption intent among smallholders once yield benefits are visualized. Dealer networks partnering with NGOs and agritech start-ups are piloting group-purchase schemes and shared-ownership models to mitigate financial and knowledge barriers.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Machinery Type: Pneumatic Systems Gain Traction

The fertilizer spreader market size for rotary/spinner units reached a substantial scale in 2025, accounting for 45.40% of global sales, as large-acreage grain farms value wide coverage and low operating costs. Pneumatic airflow designs, although currently smaller in volume, are expanding at a 9.18% CAGR because airflow paths deliver an even distribution of multi-density blends, which are critical for vegetables, orchards, and seed crops.

Airflow spreaders also support controlled-release pellets and coated nutrients, preventing particle segregation and positioning them as the technology of choice for premium-priced input programs. In regions with frequent wind events, their enclosed boom design minimizes drift, aligning with tightening buffer-zone regulations. Manufacturers investing in boom length optimization and hydraulic fan drive efficiency anticipate a continued share gain as input suppliers broaden granular micronutrient offerings. Activated-carbon-lined drop hoppers and corrosion-resistant alloys are being introduced to extend machine life, a key purchasing consideration given the rising capital costs in the fertilizer spreader market.

By Technology: Precision Systems Drive Innovation

Conventional non-GPS spreaders still occupy 71.20% of the fertilizer spreader market share, reflecting the sheer installed base and the appeal of lower ticket prices in cost-sensitive geographies. Precision/GPS-guided platforms, however, are registering 10.52% CAGR backed by quantifiable input savings and environmental-compliance mandates that require digital record keeping.

VRT prescriptions transmitted over cellular networks let operators alter rates on the go, ensuring nutrient applications match high-resolution soil layers. Leading OEMs are integrating ISOBUS-compatible controllers so that mixed-brand fleets can share maps and machine health data, a capability prized by custom-applicator service providers managing multi-client routes. Augmented-reality calibration tools accessed via smartphones reduce set-up errors, lowering the learning curve that historically deterred upgrades within the fertilizer spreader market.

By Drive Mechanism: Self-Propelled Units Accelerate

PTO-driven mounted designs accounted for 37.50% of the fertilizer spreader market size in 2025 as they allow growers to leverage existing tractors and minimize incremental investment. Yet self-propelled rigs, once perceived as a niche, now post the fastest 9.92% CAGR because they free tractors for other fieldwork and carry larger hoppers that cut refill downtime.

Cab suspension, multi-camera visibility, and 50+ km/h road speeds make these machines attractive for contractors covering dispersed plots. Auto-boom height control maintains uniform throw distance on undulating terrain, a common challenge in South American soy regions. As Tier-4-final engine regulations spread globally, self-propelled OEMs are offering methane-capable or hybrid drivelines to future-proof fleets against evolving emission norms in the fertilizer spreader market.

By Sales Channel: Digital Transformation Accelerates

Legacy dealer storefronts retained a 70.30% channel share in 2025, largely due to their established parts distribution and financing desks, which facilitate the smooth purchase of capital equipment. Yet, online portals are growing at a robust 10.78% CAGR as farmers increasingly compare specs, watch calibration tutorials, and secure quotes online before attending in-person demos.

OEMs are piloting virtual-reality walkarounds and 3D configurators that enable customers to remotely visualize boom options and hopper capacities, thereby shrinking the decision timeline. Manufacturers that integrate their e-commerce platforms with dealer service scheduling are seeing higher customer satisfaction scores than those relying solely on traditional sales processes in the fertilizer spreader market.

By End-Use Application: Specialty Crops Drive Growth

Row-crop growers accounted for 66.20% of 2025 unit demand, anchoring the market with high-volume purchases timed to tight planting calendars. In contrast, specialty/horticulture operations covering vegetables, berries, and protected-culture crops are climbing a 7.55% CAGR curve by adopting high-accuracy pneumatic or drop technologies that validate premium produce claims.

Specialty producers want sub-5% CV to avoid cosmetic damage and nutrient hotspots that trigger tip burn or blossom-end rot. Many integrate spreader data with greenhouse climate software or irrigation controllers, evidencing how digital ecosystems extend machinery value. This diversification beyond broad access has prompted OEMs to customize smaller hopper sizes and lower-clearance chassis inside the fertilizer spreader market.

By Fertilizer Form: Liquid Applications Expand

Granular products long dominated due to storage stability and compatibility with legacy machines, owning a 77.40% share in 2025. Liquid formulations are surging at 7.88% CAGR on the back of split-application strategies that sync nutrient delivery with crop demand stages, especially in maize and oilseed rape.

Liquid systems equipped with high-capacity pumps and variable-orifice nozzles apply nitrogen-sulfur blends precisely at tasseling or flowering, boosting uptake while curbing leaching. Tank agitation, corrosion-resistant plumbing, and in-line flow meters are key engineering differentiators as manufacturers chase this opportunity. Extension research in the United States shows that properly calibrated liquid rigs can cut nitrogen loss by 15%, an economic and environmental win that resonates in the fertilizer spreader market.

Geography Analysis

Europe leads the fertilizer spreader market with a 28.70% share in 2025, reflecting mature precision-agriculture infrastructure and Common Agricultural Policy incentives that subsidize technology adoption. Stringent nitrate directives and watershed protection regulations make variable-rate application a near-requirement for large arable operations. The region's strong dealer networks and established financing channels smooth the path to high-specification machines. Manufacturers targeting this market emphasize software integration with farm management platforms and compatibility with European satellite correction signals that enable sub-meter accuracy.

The Asia-Pacific region is advancing at a 7.45% CAGR through 2031, the fastest regional growth rate globally. China's policy shift toward reduced fertilizer intensity while maintaining yields creates demand for spreaders that optimize placement efficiency. The government's agricultural modernization program subsidizes mechanization, particularly for cooperatives serving multiple smallholders. India's expanding agrochemical sector, valued at USD 32.4 billion in 2024, signals growing investment capacity for application equipment. Manufacturers are adapting designs for Asian conditions by offering narrower working widths for paddy fields and simplified controls for operators with limited technical training.

North America maintains a significant fertilizer spreader market size despite recent headwinds from commodity price volatility and rising equipment costs. Large-scale grain operations value precision technology integration and data management capabilities that align with established digital farming practices. However, AGCO's 15.1% sales decline in Q2 2024 reflects cautious capital spending as farmers prioritize equipment longevity over replacement. Manufacturers are responding with retrofit packages that add variable-rate capability to existing spreaders at lower entry points. South American growth is uneven due to currency fluctuations, though Brazil's expanding soybean acreage drives demand for high-capacity machines that can cover vast plantations during narrow application windows.

Competitive Landscape

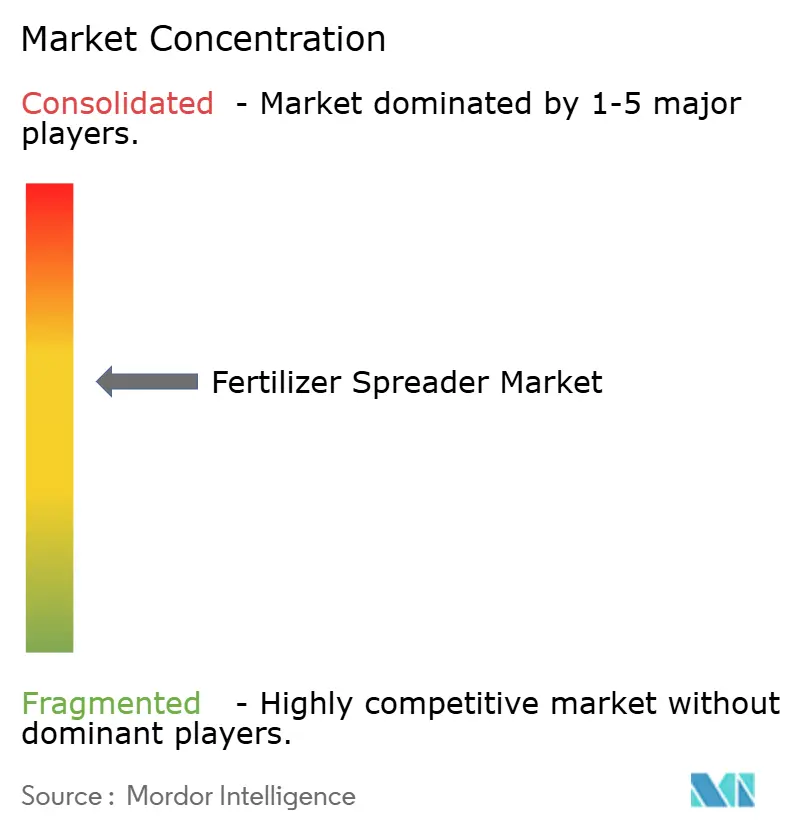

The fertilizer spreader market exhibits moderate concentration, with the top five manufacturers controlling 61% share in 2025, leaving a sizeable 39% tail served by regional specialists and niche innovators. Deere & Company leads, followed by CNH Industrial and AGCO. Kubota and Rauch round out the top bracket. Scale affords these leaders global dealer coverage and research and development resources. Still, no single brand dominates outright, enabling agile entrants to win market share by solving localized pain points.

Strategic differentiation now hinges on software integration and data connectivity rather than purely mechanical specifications. CNH Industrial’s automated control suite showcased at FIRA USA 2024 reduces fertilizer overlap by up to 10% by adjusting shutter positions in real-time, exemplifying how algorithms deliver tangible input savings. Deere’s Operations Center synchronizes as-applied maps from spreaders with planter prescription files, creating a closed agronomic loop. AGCO’s retrofit kits extend VRT capability to older Rogator platforms, monetizing installed-base relationships while lowering farmer CapEx thresholds.

White-space opportunities cluster in three areas. First, retrofit precision modules for legacy spinner frames answer cost-sensitive grower segments. Second, autonomous spreaders address acute labor shortages in vineyards and specialty crop fields. Third, pared-down precision features priced for emerging economies promise volume gains where full-spec machines remain unaffordable. Because service responsiveness ranks high in buyer surveys, regional manufacturers that bundle fast-moving parts hubs with app-based maintenance scheduling can punch above their weight despite smaller R&D budgets. As the fertilizer spreader market evolves, innovation velocity and post-sale support are poised to shift share faster than the manufacturing scale alone.

Fertilizer Spreader Industry Leaders

-

Deere & Company

-

AGCO Corporation

-

Kubota Corporation

-

Kuhn Group (Bucher Industries)

-

CNH Industrial N.V. (Exor N.V.)

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2025: Farm Credit Canada announced a CAD 2 billion investment by 2030 to enhance agtech innovation across Canada's agriculture and food sector, targeting efficiency improvements and sustainability enhancements that will drive demand for precision fertilizer application equipment.

- March 2025: AgroPages reported significant merger and acquisition activity in the agricultural biological industry, including Huma Inc.'s acquisition of Gro-Power to enhance soil fertility and crop health capabilities and Israel Chemical's acquisition of Nitro 1000 to strengthen its market position in South America.

- October 2024: CNH Industrial's New Holland brand showcased precision farming advancements at FIRA USA 2024, featuring the Precision Fan Sprayer for specialty tractors that reduces crop protection inputs by up to 10% through automated control systems.

- July 2024: AGCO Corporation reported Q2 2024 net sales of USD 2.9 billion, representing a 12.1% decrease compared to Q2 2023, reflecting challenging market conditions with declining commodity prices and reduced farm income affecting global equipment demand.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study defines the fertilizer spreader market as all new machinery designed to meter and distribute solid or liquid fertilizers over agricultural fields, turf, orchards, or specialty crops. Equipment in scope spans tractor-mounted, towed, self-propelled, and walk-behind configurations that employ broadcast, drop, pendulum, pneumatic, or drip application systems.

Scope Exclusions: This assessment omits aerial or drone application services, stand-alone rate-control electronics, and spare parts sold separately.

Segmentation Overview

-

By Machinery Type

- Drop Spreaders

- Rotary/Spinner Spreaders

- Pendulum Spreaders

- Air-Flo/Pneumatic Spreaders

- Liquid Fertilizer Sprayers

-

By Technology

- Conventional

- Precision/GPS-guided

- Autonomous/Robotics-enabled

-

By Drive Mechanism

- PTO-driven Mounted

- Trailed

- Self-propelled

- Walk-behind/Manual

-

By Fertilizer Form

- Granular

- Powdered

- Liquid

-

By End-use Application

- Row-crop Farms

- Specialty/Horticulture

- Turf and Landscaping

- Orchard and Vineyard

-

By Sales Channel

- OEM

- Dealer/Distributor

- Online

-

Geography

-

North America

- United States

- Canada

- Mexico

- Rest of North America

-

South America

- Brazil

- Argentina

- Rest of South America

-

Europe

- Germany

- United Kingdom

- France

- Spain

- Russia

- Rest of Europe

-

Asia-Pacific

- China

- India

- Japan

- South Korea

- Rest of Asia-Pacific

-

Middle East

- Saudi Arabia

- Turkey

- UAE

- Rest of Middle East

-

Africa

- South Africa

- Egypt

- Rest of Africa

-

North America

Detailed Research Methodology and Data Validation

Primary Research

We interviewed machinery dealers, agronomists, and cooperative managers across North America, Europe, Brazil, India, and China. These conversations clarified local replacement cycles, precision guidance penetration, dealer margin structures, and seasonal purchase patterns, closing gaps detected during desk work.

Desk Research

We began by mapping potential demand using public datasets such as FAOSTAT land use statistics, USDA NASS machinery surveys, Eurostat equipment registrations, and UN Comtrade HS-843240 trade flows to capture cross-border unit movements. Government subsidy guidelines, peer-reviewed agronomy papers on nutrient losses, and regional mechanization programs further refined adoption assumptions.

Our team mined OEM filings, investor decks, and product catalogs through D&B Hoovers and Dow Jones Factiva to extract selling prices, model launches, and production footprints, while Volza shipment logs validated import volumes. The sources noted above are illustrative, and many additional references supported data collection, triangulation, and clarification.

Market-Sizing & Forecasting

Current demand is modeled with a top-down cultivated-area pool layered with mechanization rate, spreader penetration by farm size, and a five-year replacement interval. Results are cross-checked through selective bottom-up supplier revenue roll-ups and channel checks that align unit volumes and average selling prices. Key variables powering the model include fertilizer consumption per hectare, average farm size, precision farming subsidy outlays, import share of mounted units, and commodity price trends. A multivariate regression, combined with exponential smoothing, projects these drivers to 2030 and produces three scenario bands. The mid case is published.

Data Validation & Update Cycle

Outputs move through anomaly scans, senior review, and a last-mile check against independent price trackers before sign-off. We refresh the model each year and trigger interim updates whenever policy, macro, or weather shocks materially shift demand.

Why Mordor's Fertilizer Spreader Baseline Commands Reliability

Published market values often diverge because firms choose different product baskets, price points, and refresh cadences. Some track only broadcast units, others fold in allied seeding tools, while a few apply retail list prices without discounting.

Key gap drivers include scope creep into planting machinery, exclusion of self-propelled rigs, inconsistent currency conversions, and forecast horizons that skip mid-cycle downswings. Our disciplined scope and annual refresh guard against these pitfalls.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 4.1 Billion (2025) | Mordor Intelligence | |

| USD 0.79 Billion (2024) | Global Consultancy A | Tracks only broadcast and drop spreaders sold through retail channels and ignores farm-dealer transactions |

| USD 1.97 Billion (2024) | Industry Journal B | Omits self-propelled rigs and relies on three-region coverage with static price assumptions |

| USD 6.65 Billion (2024) | Research Firm C | Aggregates spreaders with planters and lawn-care tools and applies list prices instead of realized sales |

These contrasts show that Mordor's clear scope, transparent variables, and blended approach create a balanced baseline that decision makers can trace to verifiable data points and reproduce with confidence.

Key Questions Answered in the Report

What CAGR is forecast for the fertilizer spreader market to 2031?

The fertilizer spreader market is projected to grow at a 5.72% CAGR, rising from USD 4.1 billion in 2025 to USD 5.72 billion by 2031.

Which technology segment is expanding the fastest?

Precision/GPS-guided spreaders lead in growth at an 10.52% CAGR because they deliver 12–18% per-hectare cost savings while meeting compliance documentation needs.

Why are pneumatic airflow spreaders gaining popularity?

Airflow machines provide superior distribution uniformity for micronutrient blends and controlled-release pellets, helping high-value crops meet tight coefficient-of-variation targets even under windy conditions.

How concentrated is the competitive landscape?

The top five manufacturers capture 61% share, with Deere & Company, CNH Industrial, and AGCO leading and leaving remaining market for regional and specialized suppliers.

What role do subsidy programs play in adoption?

Grants from Canada, the United Kingdom, and EU member states cover 30–50% of purchase costs, cutting payback periods to about three seasons and accelerating precision-equipment uptake.

Which region holds the highest growth potential?

Asia-Pacific posts the steepest 7.45% CAGR as China and India subsidize mechanization and precision fertilizer practices to boost yields while capping nutrient overuse.

Page last updated on: