Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 5.25 Billion |

| Market Size (2031) | USD 7.39 Billion |

| Growth Rate (2026 - 2031) | 7.08% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | High |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Pancreatic Cancer Therapeutics And Diagnostics Market Analysis by Mordor Intelligence

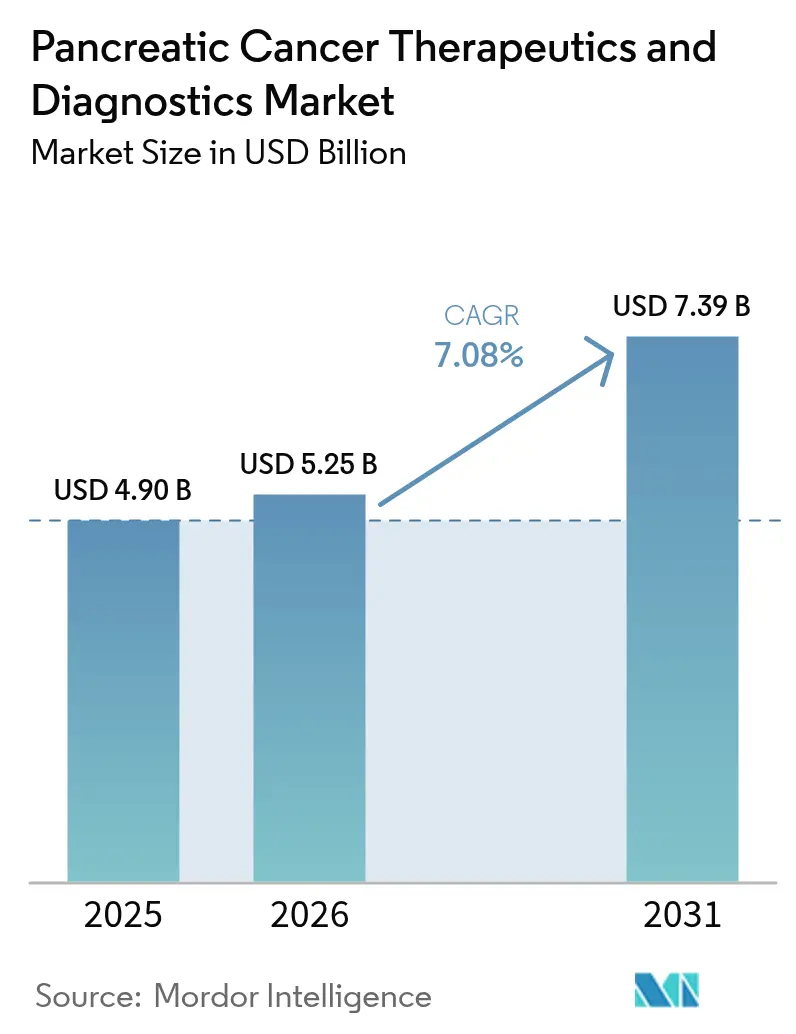

The Pancreatic Cancer Therapeutics And Diagnostics market size is expected to grow from USD 4.90 billion in 2025 to USD 5.25 billion in 2026 and is forecast to reach USD 7.39 billion by 2031 at 7.08% CAGR over 2026-2031.

Robust demand is fueled by accelerated U.S. FDA breakthrough designations; the rapid uptake of biomarker-guided precision therapies; and artificial-intelligence imaging platforms that narrow time to diagnosis. Venture-capital inflows into liquid-biopsy start-ups, combined with expanding reimbursement for next-generation sequencing panels in North America and Europe, add structural tailwinds. Meanwhile, Asia-Pacific records the sharpest incidence growth, compelling health systems to invest in early-detection infrastructure and combination-therapy capacity. Competitive intensity rises as large biopharma incumbents pursue pipeline co-development deals with niche biotechnology firms to capture white-space mechanisms such as focal-adhesion-kinase inhibition. Supply-chain pressures in radiopharmaceutical isotopes and historically high Phase III attrition rates temper the outlook but have not derailed capital formation.

Key Report Takeaways

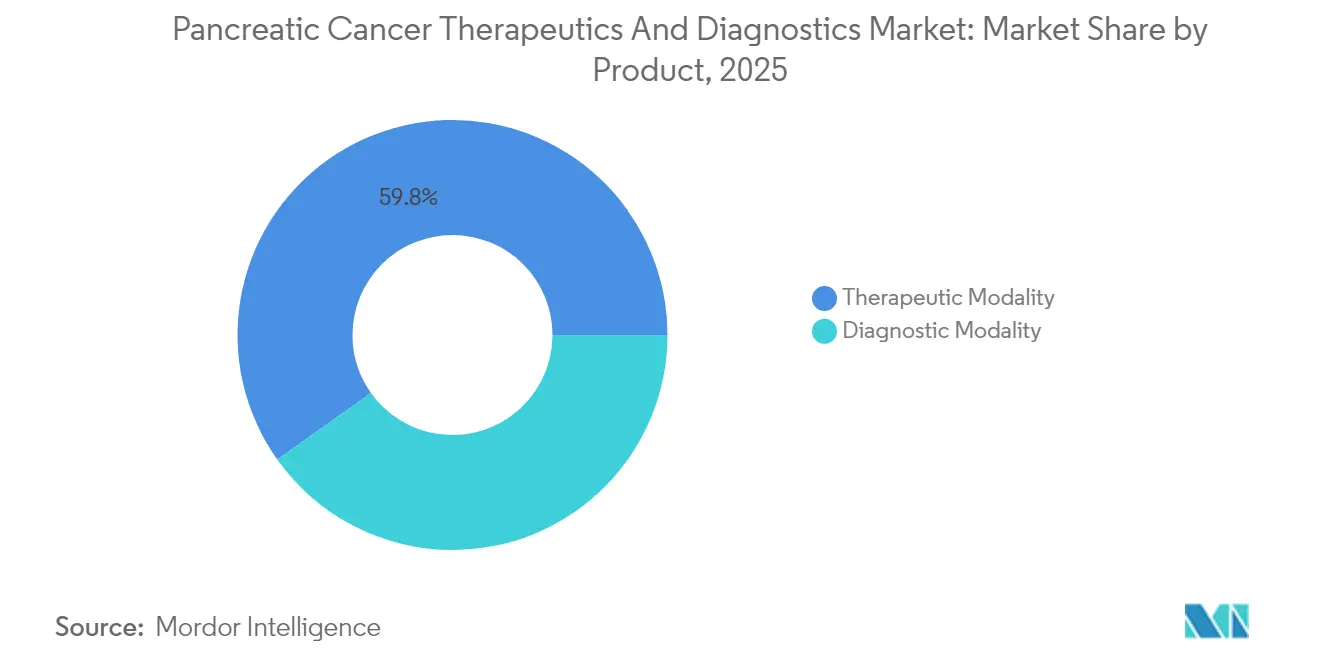

- By product, therapeutic modalities held 59.84% of pancreatic cancer therapeutics and diagnostics market share in 2025, while diagnostic modalities post the highest 7.55% CAGR to 2031 .

- By end user, hospitals and academic medical centers accounted for 51.62% of the pancreatic cancer therapeutics and diagnostics market size in 2025; diagnostic laboratories are projected to expand at a 7.31% CAGR through 2031.

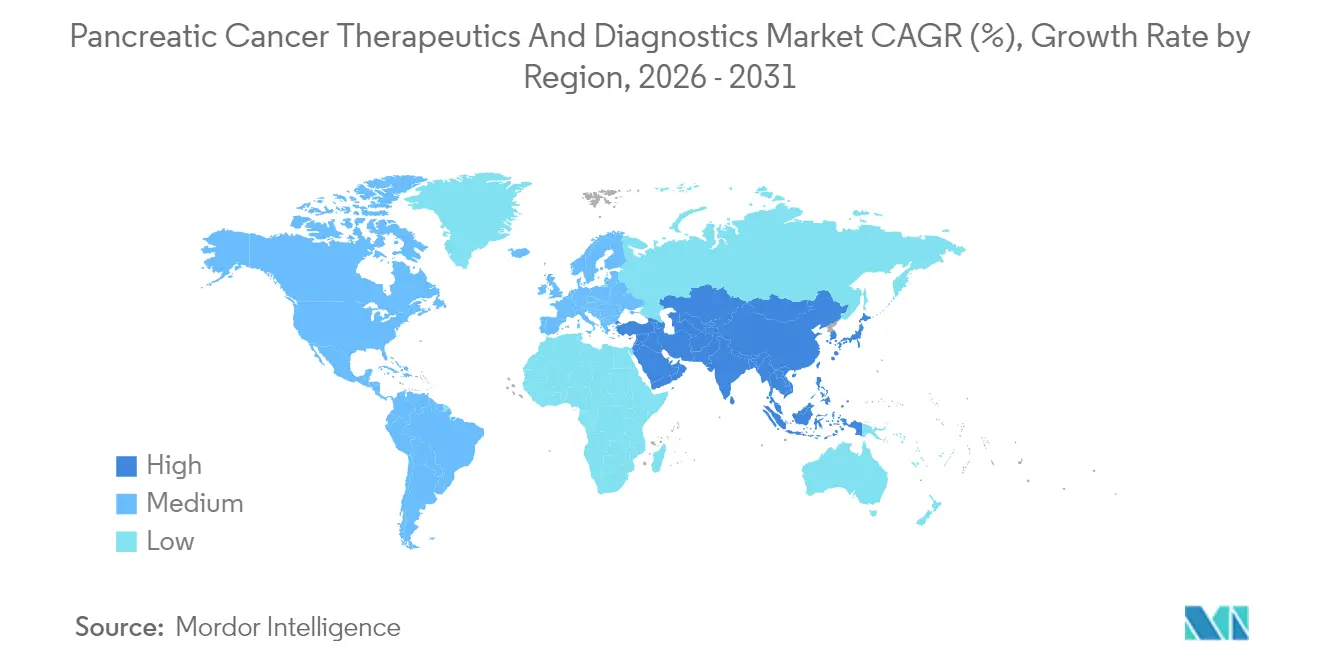

- By geography, North America led with 43.92% revenue share in 2025; Asia-Pacific is anticipated to register the fastest 7.86% CAGR between 2026 and 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Pancreatic Cancer Therapeutics And Diagnostics Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising incidence & earlier-stage detection rates | +1.2% | Global, with highest impact in Asia-Pacific and North America | Medium term (2-4 years) |

| Accelerated FDA fast-track designations for novel therapies | +1.8% | North America primary, spillover to Europe and Asia-Pacific | Short term (≤ 2 years) |

| Surge in biomarker-guided precision medicine trials | +1.5% | Global, concentrated in developed markets | Medium term (2-4 years) |

| Growing reimbursement for next-generation sequencing panels | +0.9% | North America and Europe primary | Medium term (2-4 years) |

| Venture-capital inflow into liquid-biopsy start-ups | +0.7% | Global, with concentration in North America and Europe | Long term (≥ 4 years) |

| AI-driven imaging algorithms improving diagnostic accuracy | +1.1% | Global, with early adoption in developed markets | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising incidence & earlier-stage detection rates

Population aging and lifestyle shifts are sending pancreatic adenocarcinoma incidence climbing, especially in China and the United States. Surveillance programs that monitor familial and genetic high-risk cohorts now report 50% five-year survival for screen-detected cases versus 9% for symptomatic presentations[1]Source: National Cancer Institute, “Surveillance for People at High Risk of Pancreatic Cancer,” cancer.gov . High-resolution MRI coupled with liquid-biopsy assays capable of 95% sensitivity are detecting pre-malignant lesions, moving treatment intent from palliation to cure. Surgical centers are expanding robotics suites to meet early-stage resection demand, while neoadjuvant chemotherapy protocols such as PAXG deliver 31% three-year event-free survival, more than doubling historical outcomes . The combined epidemiologic and diagnostic momentum materially lifts procedure volumes and systemic-therapy utilization across the pancreatic cancer therapeutics and diagnostics market.

Accelerated FDA fast-track designations for novel therapies

The U.S. FDA has labeled multiple pancreatic cancer assets—Daraxonrasib for KRAS mutations, EBC-129 ADC, and the DAMO PANDA AI diagnostic tool—as breakthrough products, trimming typical timelines by nearly two years. Parallel companion-diagnostic reviews streamline synchronized market entry for test-and-treat bundles. Such regulatory velocity incentivizes investors, boosting valuations and expediting Phase II/III financing rounds for start-ups positioned inside the pancreatic cancer therapeutics and diagnostics market. European and Asian regulators frequently reciprocate accelerated reviews, amplifying global spillover.

Surge in biomarker-guided precision medicine trials

KRAS-targeted compounds like Zoldonrasib record 30% overall response in G12D-mutated cases, redefining expectations for a once-undruggable lesion. Multi-omics enrollment algorithms cut screen-failure rates and drive smaller, faster studies. Circulating-tumor-DNA decline now functions as an early surrogate for overall survival, allowing adaptive trial designs that recycle non-responders into alternative arms. These efficiencies are shrinking capital burn and elevating approval probabilities inside the pancreatic cancer therapeutics and diagnostics industry.

Growing reimbursement for next-generation sequencing panels

Medicare’s fixed USD 1,160 code for the Avantect 20-gene panel signposts payers’ recognition that comprehensive genomic insights lower downstream costs through optimized therapy alignment . German and Japanese insurers are following suit. Hospital networks have begun embedding sequencing into standard care pathways, ensuring every resected pancreatic tumor receives actionable profiling. Reimbursement security anchors sustainable volumes for specialized molecular labs, propelling the pancreatic cancer therapeutics and diagnostics market.

Restraints Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High attrition rates in late-stage clinical trials | -1.4% | Global, with highest impact in North America and Europe | Medium term (2-4 years) |

| Limited patient pools constrain trial enrollment | -0.8% | Global, with particular challenges in rare mutation subsets | Long term (≥ 4 years) |

| Complex supply chain for radiopharmaceutical tracers | -0.9% | Global, with acute shortages in Europe and North America | Short term (≤ 2 years) |

| Rising pricing pressure from payers & HTA bodies | -1.1% | North America and Europe primary, expanding to Asia-Pacific | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High attrition rates in late-stage clinical trials

Pancreatic tumors’ dense stroma and immunosuppressive microenvironment render many promising agents ineffective in Phase III. Recent high-profile immunotherapy combinations failed to demonstrate significant survival benefit, triggering portfolio reshuffles and depressing follow-on funding. Regulators now mandate larger cohorts and longer follow-up, pushing development costs above USD 450 million per asset. These setbacks delay the flow of new treatments into the pancreatic cancer therapeutics and diagnostics market and heighten investors’ risk perception.

Limited patient pools constrain trial enrollment

Biomarker-defined subsets, such as NRG1 fusion carriers, represent <1% of pancreatic cases, making multi-arm studies logistically complex and expensive. Geographic concentration of high-volume centers forces patients to travel long distances, and rapid clinical decline between screening and randomization disqualifies many candidates. Sponsors increasingly launch umbrella protocols across 12-15 countries to aggregate sufficient numbers, escalating administrative overhead and stretching timelines inside the pancreatic cancer therapeutics and diagnostics market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product: Therapeutic Dominance Meets Diagnostic Innovation

Therapeutic modalities captured 59.84% of pancreatic cancer therapeutics and diagnostics market share in 2025, underpinned by combination regimens like NALIRIFOX that extend median overall survival beyond 12 months. Chemotherapy remains the foundation, yet targeted KRAS-blocking agents and subcutaneous checkpoint inhibitors add differentiated options. Radiopharmaceutical advances and stereotactic ablative radiotherapy further diversify the therapeutic armamentarium. Manufacturers pair new drugs with companion diagnostics to ensure precise patient selection, driving bundled revenue streams. Competitive rivalry centers on pipeline depth and speed to secure additional breakthrough designations that can convert into first-mover advantage.

Diagnostic modalities expand at a 7.55% CAGR, the fastest within the pancreatic cancer therapeutics and diagnostics market. Liquid-biopsy platforms integrating exosomal microRNA panels now achieve 97% accuracy when combined with CA19-9, enabling stage I detection. AI-enhanced endoscopic ultrasound improves lesion delineation, shortening procedure time and minimizing false negatives. Multi-omics assays that merge genomics, proteomics, and metabolomics shape next-generation companion diagnostics. Vendor differentiat ion hinges on analytical sensitivity and frictionless integration into oncologists’ ordering systems, fostering high switching costs.

By End User: Hospital Consolidation Drives Laboratory Growth

Hospitals and academic medical centers held 51.62% of the pancreatic cancer therapeutics and diagnostics market size in 2025, leveraging multidisciplinary teams and high-volume surgery programs. Vertical integration allows on-site infusion, advanced imaging, and clinical-trial enrollment, anchoring referral networks. Capital expenditures focus on proton-therapy bays and robotic-assisted surgery suites, positioning these centers as regional hubs for complex pancreatic procedures. Their purchasing scale secures favorable drug pricing and sequencing-platform discounts, defending share.

Diagnostic laboratories, though smaller today, are projected to grow 7.31% annually, the fastest among end users. Specialized labs deploy 600-gene panels and high-throughput ctDNA platforms that exceed hospital lab capabilities. Oncology clinics outsource complex testing to these centers, benefiting from rapid, standardized reports that drive therapy alignment. As liquid-biopsy adoption widens, reference labs integrate phlebotomy networks to simplify specimen logistics, solidifying their role within the pancreatic cancer therapeutics and diagnostics market.

Geography Analysis

North America generated 43.92% of 2025 revenue. Accelerated FDA reviews and Medicare reimbursement for next-generation sequencing underpin high adoption levels. Yet cost-effectiveness scrutiny intensifies; analyses peg NALIRIFOX at USD 206,341 per QALY, pushing payers toward value-based contracting . Academic expansions, such as the approved 300-bed Dana-Farber hospital, deepen regional expertise and clinical-trial throughput.

Asia-Pacific is forecast to post an 7.86% CAGR, the strongest globally. China’s aging population, rising obesity, and smoking prevalence propel incidence, while public-private partnerships finance molecular-testing labs and precision-oncology parks. Japan’s regulatory harmonization with U.S. breakthrough-therapy policies shortens drug-approval lags to under six months, facilitating swift diffusion of innovative regimens. Governments allocate funds for surgeon-training programs in robotic resection, elevating curative-intent procedure volumes.

Europe maintains moderate growth as the European Medicines Agency approved 28 oncology therapies in 2024, including NALIRIFOX. Health-technology assessments by NICE increasingly factor pharmacogenomics, incentivizing payers to reimburse sequencing. Cross-border clinical-trial consortia streamline enrollment for rare biomarker cohorts, while EU investments in isotope-production facilities mitigate sporadic shortages that hamper diagnostic imaging. Still, stringent price negotiations curb immediate revenue upside for manufacturers within the pancreatic cancer therapeutics and diagnostics market.

Regulatory Landscape

Regulation in the pancreatic cancer therapeutics and diagnostics market is shaped by accelerated oncology pathways and increasing scrutiny of combination regimens and device-drug products. In February 2026, the US FDA approved Novocure's Optune Pax as a first-of-its-kind device to treat pancreatic cancer, reinforcing the role of device-led modalities alongside systemic therapy and tightening expectations around evidence generation, labeling, and postmarket controls for novel platforms.

For combination therapy development, the FDA released guidance in July 2025 on developing cancer drugs for use in novel combinations. It emphasizes the need to determine the contribution of individual drugs to observed effects, a key issue for multi-agent pancreatic regimens. In parallel, the FDA issued proposals in June 2025 affecting diagnostics and combination-product compliance, including a proposed reclassification of certain oncology therapeutic ISH test systems toward Class II (special controls) and draft direction on Unique Device Identifier application for combination products. In Europe, EMA actions support faster access while maintaining structured evidence standards, including a July 2026 fast-track review initiation for a medicine in metastatic pancreatic cancer and established scientific guidelines for anticancer medicinal product evaluation and fixed-combination clinical development.

Value Chain Analysis

The value chain spans discovery and translational biology through clinical development, regulated manufacturing, and delivery via specialty oncology networks. On the therapeutics side, core inputs include active pharmaceutical ingredients for chemotherapy backbones (for example, irinotecan liposome and nab-paclitaxel), biologics and targeted agents progressing through biomarker-driven trials, and enabling technologies for localized or device-based delivery. Clinical development and evidence generation concentrate in high-volume academic centers and global trial networks, reflecting complex eligibility tied to molecular profiling (KRAS subtypes, BRCA1/2, PALB2, ATM, MSI) and the need to aggregate rare biomarker subsets across multiple countries.

Manufacturing and commercialization diverge by modality. Established small-molecule and liposomal products rely on scaled pharmaceutical supply chains, while device-drug combinations add medical-device quality systems, labeling, and traceability requirements. Optune Pax is an anchor example, having received FDA PMA (P250034) in February 2026 for use with gemcitabine and nab-paclitaxel in locally advanced pancreatic cancer, creating an integrated chain from device production to oncology clinic deployment. Diagnostics and patient selection depend on tissue workflows (biopsy, pathology) and expanding liquid-biopsy and molecular testing capacity, with distribution routed through hospitals, academic medical centers, and reference laboratories that return actionable reports to guide test-and-treat pathways.

Competitive Landscape

The pancreatic cancer therapeutics and diagnostics market remains moderately fragmented. Bristol Myers Squibb advanced a subcutaneous nivolumab formulation, easing infusion-center burden while sustaining PD-1 inhibitor growth. Roche expanded its oncology assay portfolio, integrating liquid-biopsy tests with sequencing systems and dedicating CHF 13 billion to R&D in 2025. Novocure’s Tumor Treating Fields therapy achieved 16.2-month median overall survival in PANOVA-3 and is slated for FDA submission, introducing a non-systemic modality that may complement chemotherapy.

Strategic collaborations define the competitive narrative. Mainz Biomed partnered with Liquid Biosciences to co-develop mRNA biomarker assays boasting 95% sensitivity to stage I disease, underscoring diagnostics’ convergence with therapeutics. Arrivent joined forces with Alphamab to build antibody-drug conjugates leveraging proprietary linker technology, targeting multi-antigen payload delivery. RenovoRx’s Phase III chemo-infusion platform demonstrates the appeal of device-drug synergies to circumvent systemic toxicity. Emergent players exploit niche mechanisms—focal-adhesion-kinase blockade and stromal-digesting enzymes—to challenge incumbents, while AI vendors embed imaging analytics into hospital PACS to lock in radiology workflows.

Regulatory compliance increasingly necessitates co-development of companion diagnostics, compelling drug developers to either build in-house assays or secure exclusive partnerships. As integrated solutions proliferate, competitive advantage tilts toward companies capable of delivering end-to-end diagnostic-therapeutic ecosystems within the pancreatic cancer therapeutics and diagnostics market.

Pancreatic Cancer Therapeutics And Diagnostics Industry Leaders

Myriad Genetics, Inc.

Pfizer, Inc

Novartis AG

AstraZeneca plc

Immunovia AB

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

Earlier detection and repeatable monitoring create whitespace for diagnostics that improve sensitivity and operational turnaround beyond conventional tissue biopsy and standard NGS panels. In 2026, academic and clinical innovation highlights multiple routes to higher-performance testing, including a Mayo Clinic AI model that identifies pancreatic cancer risk signatures up to three years before clinical diagnosis and ddPCR-based approaches reported by Northwestern Medicine for higher-sensitivity detection of circulating KRAS mutations. Peer-reviewed advances in multi-marker platforms, such as signal-enhanced lateral flow immunoassays (SELFI) and enzymatic colorimetric encoding-based digital risk scoring (EnCODE), support productization opportunities for screening high-risk cohorts, differentiating benign pancreatic disease from malignancy, and enabling longitudinal surveillance.

On the therapeutics side, opportunities concentrate in biomarker-defined and combination strategies that tighten linkage between diagnostics and regimen selection, supported by regulatory willingness to act in narrowly defined populations. FDA approvals such as NALIRIFOX (irinotecan liposome combination) for first-line metastatic pancreatic adenocarcinoma and BIZENGRI (zenocutuzumab-zbco) for NRG1-fusion positive advanced pancreatic adenocarcinoma reinforce the commercial importance of identifying actionable subsets and embedding companion testing into care pathways. Device-enabled and localized modalities also expand the addressable opportunity set, with the February 2026 FDA approval of Optune Pax showing how non-systemic adjuncts can be integrated into established chemotherapy backbones and hospital delivery infrastructure.

Recent Industry Developments

- June 2026: Myriad Genetics announced expanded availability of its Precise MRD assay for patients undergoing treatment and surveillance in breast, colorectal, and renal cancers. Broadening access and publication support strengthens the company's ctDNA-based monitoring footprint, a capability that can extend into high-need solid tumors where longitudinal molecular tracking is increasingly used to guide escalation or de-escalation decisions.

- May 2026: Pfizer and Innovent Biologics entered a global strategic licensing and collaboration agreement to research and develop 12 early-stage and de novo oncology medicines, including antibody-drug conjugates and multi-specific antibodies. The deal adds breadth across modalities commonly evaluated in pancreatic oncology combination strategies and signals continued large-pharma sourcing of external innovation to accelerate pipeline build-out.

- February 2024: Johns Hopkins Medicine initiated patient enrollment for RenovoRxs Phase III TIGeR-PaC trial evaluating localized drug-delivery technology for pancreatic cancer. Progression into pivotal-stage evaluation supports continued investment in device-drug approaches aimed at increasing intratumoral exposure while limiting systemic toxicity.

Research Methodology Framework and Report Scope

Market Definition and Coverage

This market is defined as the revenues generated from products and procedures used to diagnose pancreatic cancer and to treat it, across routine care settings, and tracked in USD at current prices.

Scope exclusions: General oncology platform research tools, broad hospital services, and non-pancreatic cancer indications are excluded from the totals.

Segmentation Overview

- By Product

- Therapeutic Modality

- Chemotherapy

- Targeted Therapy

- Immunotherapy

- Radiotherapy

- Combination Therapy

- Diagnostic Modality

- Imaging (CT, MRI, PET)

- Endoscopic Ultrasound (EUS)

- Biomarker Tests

- Liquid Biopsy

- Molecular Diagnostics

- Therapeutic Modality

- By End User

- Hospitals & Academic Medical Centers

- Oncology Specialty Clinics

- Diagnostic Laboratories

- Research Institutes

- By Geography

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Rest of Europe

- Asia-Pacific

- China

- India

- Japan

- South Korea

- Australia

- Rest of Asia-Pacific

- South America

- Brazil

- Argentina

- Rest of South America

- Middle East and Africa

- GCC

- South Africa

- Rest of Middle East and Africa

- North America

Data Sources, Market Sizing, and Validation

Desk Research

Desk research was used to set the pancreatic cancer disease context and build a clean demand pool before numbers were modeled. We reviewed public sources such as the World Health Organization, the US CDC, the US National Cancer Institute, and Globocan-style cancer incidence and mortality releases to understand country-level patient burden and trends.

To translate burden into addressable demand, we also referred to sources such as clinical guidelines and evidence reviews from peer-reviewed journals (to map typical diagnostic pathways and lines of therapy), along with health agency publications and reimbursement notes where available. Company annual reports, investor presentations, and press releases were used for product timelines and geography exposure, and a paid subscription for company financials and patent intelligence was used selectively to sanity-check pipeline intensity and revenue mix. These sources are illustrative only, and many additional public references were used to collect, validate, and clarify inputs during the study.

Primary Interviews and Surveys

Primary work focused on interviews and structured questionnaires with oncologists, gastroenterologists, radiologists, pathologists, hospital procurement teams, and diagnostic lab stakeholders across major regions, so the model could reflect real-world testing and treatment patterns. Inputs were used to validate adoption by stage, how often specific imaging and biopsy routes are chosen, typical therapy sequencing, and how pricing tends to shift over time, and then to close data gaps left by public sources.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 27% | CXOs: 13% | APAC: 41% |

| Mid tier: 56% | Functional/Unit leaders: 28% | EMEA: 33% |

| Smaller Players: 17% | Managers: 59% | Americas: 26% |

Market-Sizing & Forecasting

Sizing was built using a top-down demand reconstruction that starts from pancreatic cancer incidence, then narrows into the diagnosed and treated population by region, and finally applies utilization rates for key diagnostic steps and therapy classes. Once that backbone was established, selective bottom-up checks were used to corroborate totals, such as sampling price per test or per course of therapy and multiplying by estimated volumes from channel checks and supplier mix discussions.

Key inputs used in the model included incidence and mortality trend direction, diagnostic pathway mix (imaging, endoscopic ultrasound, and biopsy rates), stage-at-diagnosis split and treatment eligibility, therapy utilization by line of therapy (for example chemotherapy versus targeted options), and average selling price progression by geography and setting. Where country-level inputs were thin, gaps were handled through proxies from clinically comparable markets and then adjusted using expert feedback on access, reimbursement, and capacity constraints.

For forecasting, scenario analysis was applied around patient diagnosis rates, adoption of newer modalities, and pricing pressure, and then the selected case was aligned to the most common expectations heard in interviews. Assumptions were documented at the variable level so the forecast can be recreated and stress-tested with simple updates as new data appears.

Data Validation & Update Cycle

Outputs were checked through multiple passes so the final totals match real-world clinical flow and spending signals. We cross-verified country rollups against independent indicators like procedure intensity, oncology drug spending direction, and reported diagnostic capacity where those metrics were available, and then investigated outliers rather than averaging them away.

Before sign-off, the model is reviewed by another analyst to confirm that definitions, arithmetic, and assumptions are consistent across regions and years. If a major variance is flagged, experts are re-contacted to confirm whether it reflects a real shift (for example, guideline changes or access expansion) or a modeling issue. The report is refreshed annually, with interim updates when material events occur, and a final pre-delivery review is completed so clients receive the latest updated view.

Mordor Intelligence's Pancreatic Cancer Therapeutics Diagnostics Market Size Measured Against Other Published Estimates

Published market sizes for this space often differ even when the titles look similar, because the included clinical pathways, the way diagnostics are valued, and the base-year refresh timing are not handled the same way across sources.

Biomarker discovery research tools and broad oncology screening panels sit outside Mordor Intelligence's scope, which keeps the 2025 total tied to pancreatic cancer specific diagnosis and treatment spending rather than adjacent research and multi-cancer testing revenues.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 4.90 B (2025) | |

| Global Consultancy A | USD 4.53 B (2025) | Often applies a more conservative testing intensity assumption by region, which can reduce diagnostic procedure volumes per patient and pull down the same-year total. |

| Industry Publisher B | USD 4.72 B (2025) | Tends to emphasize drug-only spend signals and uses a narrower pricing pathway for diagnostics, which can undercount the full set of imaging and endoscopic ultrasound related revenues. |

Overall, the spread is mainly explained by what gets counted inside diagnostics, plus how utilization and price are projected in the base year. Using explicit patient flow variables and then cross-checking sampled price times volume logic helps keep the number traceable and easier to replicate when assumptions are updated.

Key Questions Answered in the Report

What is the projected value of the pancreatic cancer therapeutics and diagnostics market in 2031?

It is expected to reach USD 7.39 billion, expanding at a 7.08% CAGR from 2026.

Which product segment grows fastest over the forecast horizon?

Diagnostic modalities, led by liquid-biopsy and AI imaging, post a 7.55% CAGR through 2031.

Which region shows the highest growth rate?

Asia-Pacific records the fastest 7.86% CAGR, driven by rising incidence and expanding precision-oncology infrastructure.

Why are liquid-biopsy platforms attracting significant investment?

Exosome-based assays now demonstrate up to 97% accuracy, enabling earlier detection and repeat-testing revenue streams.

How do FDA fast-track designations influence market dynamics?

They shorten development timelines by up to two years, accelerating product launches and raising company valuations.

What challenges most constrain late-stage clinical success?

High Phase III attrition stems from pancreatic cancers aggressive biology and limited trial-enrollment pools, inflating development costs.

Page last updated on: