Hydrogel Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

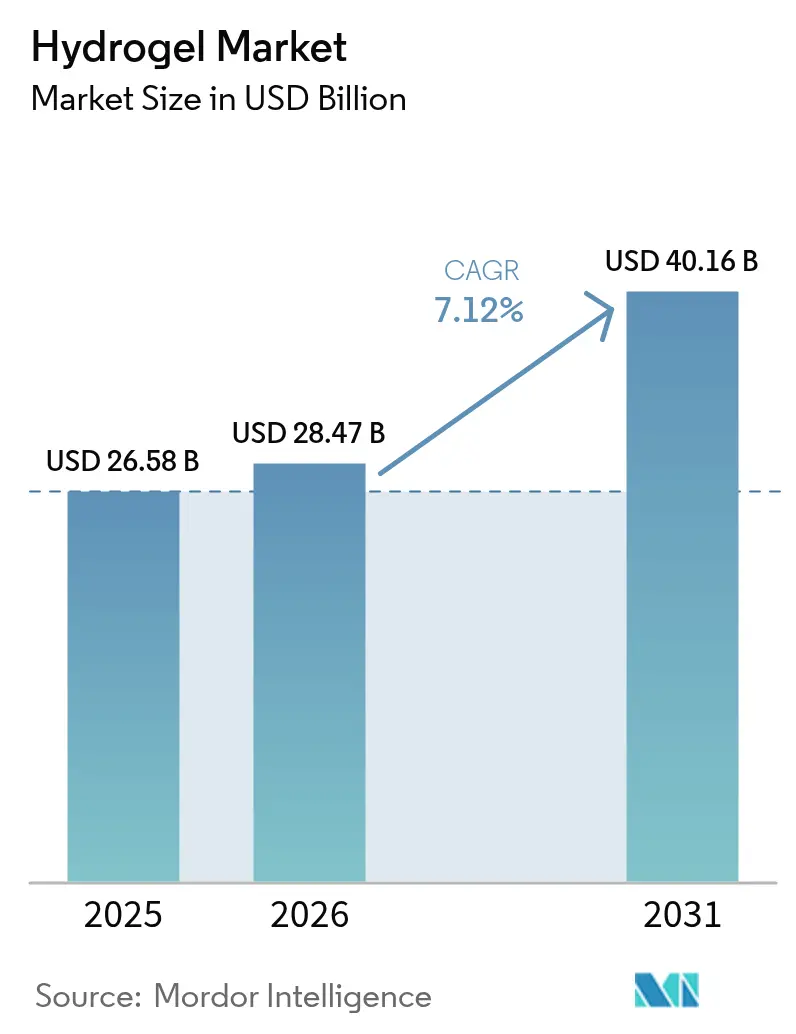

| Market Size (2026) | USD 28.47 Billion |

| Market Size (2031) | USD 40.16 Billion |

| Growth Rate (2026 - 2031) | 7.12% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Hydrogel Market Analysis by Mordor Intelligence

The Hydrogel Market size is projected to be USD 26.58 billion in 2025, USD 28.47 billion in 2026, and reach USD 40.16 billion by 2031, growing at a CAGR of 7.12% from 2026 to 2031. End-use demand is pivoting from commodity absorbents toward precision-engineered matrices that merge sensing, drug release, and biodegradability. Semi-crystalline grades hold dominant revenue because tunable mechanical strength secures hospital formulary preference in wound care. Amorphous formulations are expanding fastest as pharmaceutical developers seek rapid-dissolution patches and injectable depots that accelerate therapeutic onset. Polyacrylate remains the incumbent in hygiene products, yet polyacrylamide is gaining traction among water-stressed agricultural economies where 400-fold water uptake offers a lifeline for drip-irrigation systems. Regionally, Asia-Pacific leads the hydrogel market thanks to capacity additions in China and policy-linked subsidies in India that embed hydrogels into soil-moisture mandates.

Key Report Takeaways

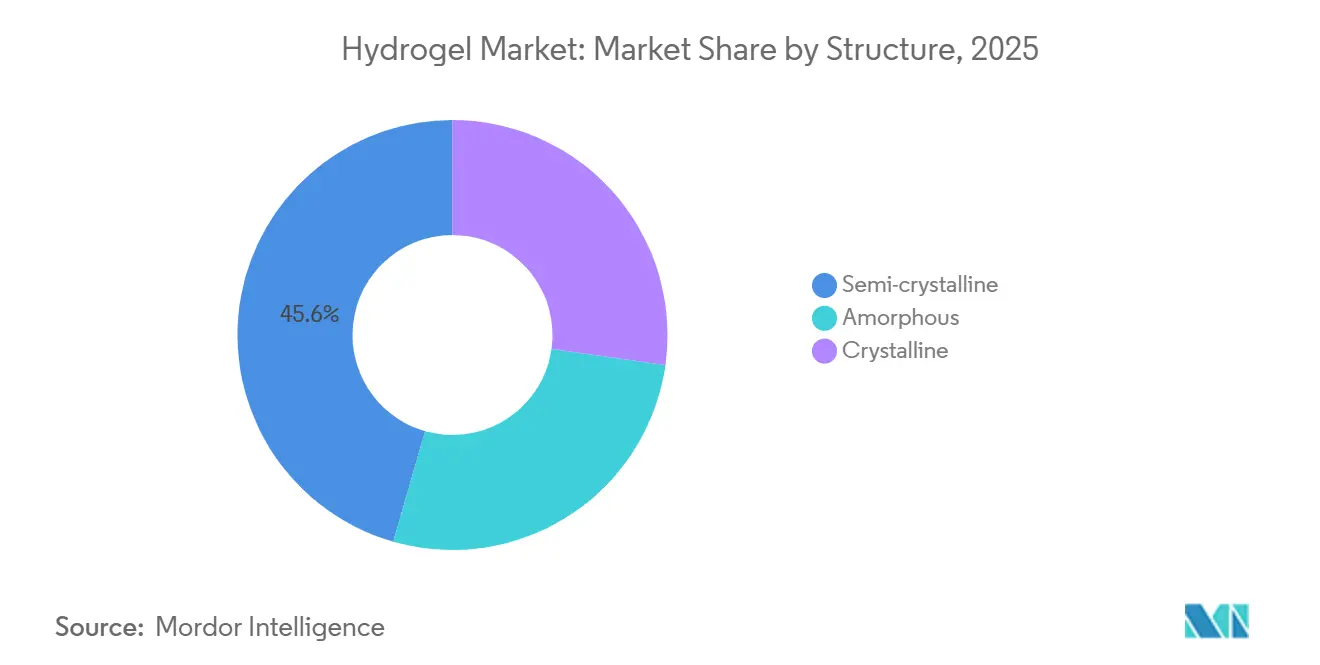

- By structure, semi-crystalline grades held 45.56% of the hydrogel market share in 2025, while amorphous grades are tracking an 8.01% CAGR through 2031.

- By material, polyacrylate captured 25.33% revenue in 2025, whereas polyacrylamide is forecast to expand at a 7.58% CAGR to 2031.

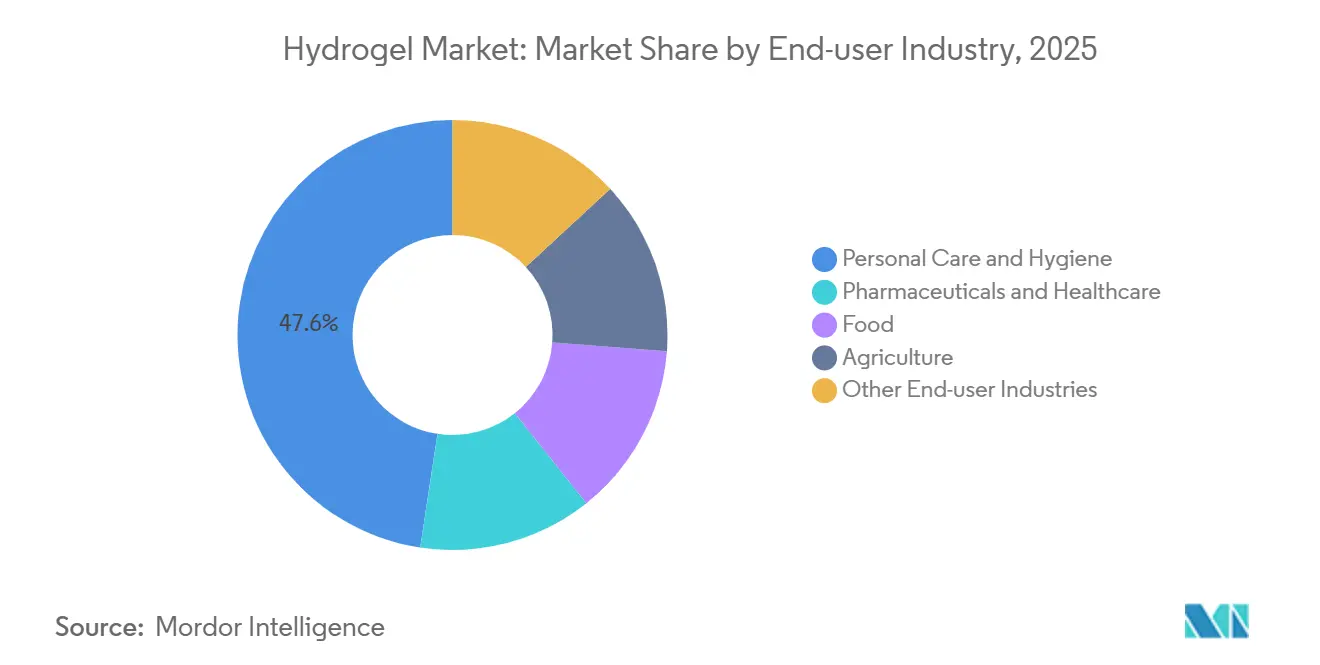

- By end-user industry, personal care and hygiene commanded 47.61% of the hydrogel market size in 2025, and pharmaceuticals and health care are advancing at a 7.79% CAGR through 2031.

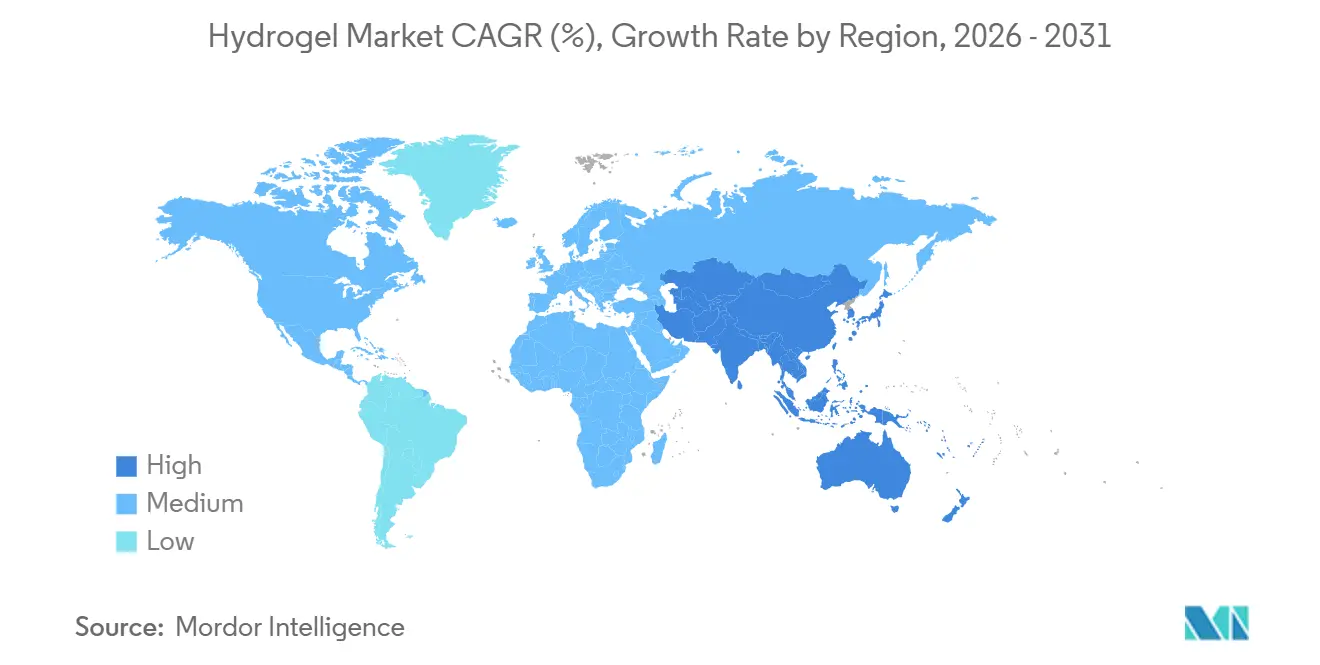

- By geography, Asia-Pacific contributed 41.10% revenue in 2025 and is projected to climb at an 8.02% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Hydrogel Market Trends and Insights

Drivers Impact Analysis*

| Drivers | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Expanding use in disposable hygiene products | +1.8% | Global, with concentration in Asia-Pacific (China, India) and Latin America | Medium term (2-4 years) |

| Growing demand for silicone-hydrogel contact lenses | +1.5% | North America, Europe, Japan, South Korea | Short term (≤ 2 years) |

| Regulatory push for water-saving agricultural inputs | +1.3% | Asia-Pacific (India, ASEAN), Middle East and Africa, South America (Brazil) | Long term (≥ 4 years) |

| Proliferation of conductive hydrogel sensors for wearable electronics | +1.2% | North America, Europe, Japan | Medium term (2-4 years) |

| 4D-printed smart hydrogel implants for minimally-invasive therapies | +1.0% | North America, Europe | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Expanding Use in Disposable Hygiene Products

Global consumption of hydrogels was primarily driven by diaper and feminine-care products. Notably, the Asia-Pacific region accounted for a significant portion of this volume, fueled by rising incomes and a shift towards premium ultra-thin formats. In a strategic move, Chinese manufacturers achieved a reduction in basis weight by increasing crosslink density. This innovation led to thinner cores, resulting in reduced packaging costs and enhanced comfort. Under Beijing's Healthy China 2030 initiative, a target has been set for rural households to have access to hygienic menstrual products. To support this goal, significant investments are being funneled into new polyacrylate production lines. Meanwhile, Europe's Extended Producer Responsibility regulations are accelerating a shift towards cellulose-hydrogel blends. These blends, which decompose within 90 days, position bio-based suppliers advantageously for future gains. As a result of these dynamics, the demand for hygiene-grade hydrogels is witnessing robust growth. This growth persists despite a slip in unit prices, a consequence of overcapacity in China.

Growing Demand for Silicone-Hydrogel Contact Lenses

Silicone-hydrogel designs represented a significant portion of the soft lenses dispensed in 2025, reflecting prescriber preference for oxygen transmissibility over 100 Dk/t[1]American Optometric Association, “2025 Contact Lens Report,” aoa.org. Revenue momentum rests on water-gradient technology that preserves surface water content while embedding silicone channels to maintain comfort during extended wear. Japan cleared two UV-blocking silicone-hydrogel disposables in 2025, tapping pediatric and myopia-control niches that grow steadily. ISO 18369 now requires public disclosure of oxygen permeability, modulus, and lipid-deposition metrics, accelerating the retirement of legacy hydrogels. China is simultaneously expanding orthokeratology for children; silicone-hydrogel ortho-k lenses already own a notable share of pediatric prescriptions, underlining cross-regional adoption potential.

Regulatory Push for Water-Saving Agricultural Inputs

India’s flagship irrigation program allocates significant funding in 2025-26, covering a portion of spending only when farmers deploy hydrogel soil conditioners that cut irrigation cycles. Rajasthan field trials showed cotton yields climb while water use fell per hectare. Brazil’s water authority made hydrogel use mandatory in drought-prone sugarcane zones, creating a guaranteed domestic market. FAO’s climate-smart guidelines list hydrogels as a Tier 1 adaptation tool, unlocking multilaterals’ funding. Certification under ISO 17556 for biodegradability is fast becoming a license to operate, especially as African regulators curb imports of non-degradable polyacrylamide.

Proliferation of Conductive Hydrogel Sensors for Wearable Electronics

In 2025, conductive hydrogel electrodes made their mark by being integrated into millions of wearables, surpassing the performance of traditional rigid Ag/AgCl contacts. This advancement achieved a significant reduction in skin-electrode impedance. Highlighting the efficacy of these innovations, a monitor showcased its durability with an impressive mean absolute relative difference over a span of days, all without the need for recalibration. In a move that underscores the industry's momentum, a recent draft FDA guidance has streamlined biocompatibility data requirements, effectively slashing months off start-up launch timelines. Meanwhile, patent filings for stretchable circuits surged, with tech giants fortifying their portfolios, particularly in the realms of flexible displays and haptic layers. Such advancements not only enhance the hydrogel market's appeal, extending its reach beyond traditional fitness trackers, but also revolutionize monitoring for neonates and the elderly, areas previously hindered by rigid devices that caused pressure ulcers.

Restraints Impact Analysis*

| Restraints | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Competition from foam and alginate dressings | -0.9% | Global, particularly North America and Europe | Short term (≤ 2 years) |

| Regulatory scrutiny on micro-plastic shedding and landfill impact | -0.7% | Europe, North America, with spillover to APAC | Medium term (2-4 years) |

| ESG pressure over high energy-intensity hydrogel manufacturing | -0.5% | Global, strongest in Europe and North America | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Competition from Foam and Alginate Dressings

In 2025, polyurethane foams secured a significant share of the advanced wound-care market, surpassing hydrogels. Clinicians leaned towards foams for treating heavily exuding ulcers. Meanwhile, calcium alginates gained traction in hemostasis, benefiting from faster clotting times that influenced operating-room practices. A review highlighted comparable healing rates between foams and hydrogels, diminishing the latter's price advantage. Silicone-border foams, requiring nursing attention only once every five days, offered a significant edge amid prevalent staffing shortages. Hydrogel manufacturers, incorporating silver or iodine for enhanced infection control, face a tighter competitive margin, especially outside burn centers and oncology wards, due to the added costs.

Regulatory Scrutiny on Micro-Plastic Shedding and Landfill Impact

Europe’s chemical watchdog estimates that each diaper releases microplastic particles, with a significant portion of these particles escaping treatment plants and entering waterways[2]European Chemicals Agency, “Risk Assessment of Microplastics,” echa.europa.eu. France has proposed a mandate to label microplastic content on hygiene products by 2027, a move that could provoke a backlash from consumers. In California, a ban is already in place for agricultural hydrogels that don't achieve sufficient mineralization within a specified timeframe. This effectively sidelines conventional polyacrylamide in the state's soil-amendment market. Reformulating to starch-grafted copolymers incurs additional raw material costs and requires certification under ISO 17556. Furthermore, fragmented national definitions of “biodegradable hydrogel” complicate compliance for multinational corporations.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Structure: Mechanical Tunability Anchors Semi-Crystalline Dominance

Semi-crystalline grades generated 45.56% of 2025 revenue, leveraging tensile moduli ranging from low values in wound dressings to higher values in cartilage scaffolds. These advantages stemmed from precise adjustments in crosslink density and crystalline domain size. Meanwhile, amorphous variants clock an 8.01% CAGR, as drug-delivery experts pursue the rapid diffusion rates that semi-crystalline matrices hinder. The hydrogel market is set to see a significant uptick for amorphous formulations in transdermal patches. At the same time, semi-crystalline compositions maintain their foothold in agriculture, where they outperform their amorphous counterparts by releasing water over a span of several days. Crystalline hydrogels remain a niche player, as their brittleness leads to high rejection rates, limiting their market share. Regulatory endorsements are boosting the adoption of amorphous variants, spurring investments in non-invasive therapeutic pipelines.

On the commercial front, suppliers are strategically blending structures, merging amorphous domains for enhanced permeability with micro-crystalline regions for superior load-bearing capabilities. This blend commands a premium in the orthopedic implant market. Asian suppliers are ramping up capacity, recognizing the paramount importance of mechanical performance in the burgeoning wound-care sector. In contrast, African agronomists favor semi-crystalline powders for drip irrigation, valuing their extended field life. This diverse structural landscape creates distinct value pools, allowing vendors to safeguard their margins even amidst commodity price fluctuations.

By Material: Polyacrylate Incumbency Confronts Polyacrylamide in Water-Stressed Regions

In China, polyacrylate accounted for 25.33% of the 2025 market value, solidifying its position as the cost leader. Yet polyacrylamide’s 7.58% growth aligns with water scarcity policies, especially given its impressive absorption capacity. Although silicone chemistry constitutes a small percentage of the hydrogel market by volume, it commands a substantial share of the market's value. This premium is largely due to oxygen-permeable lenses, underscoring the industry's tilt towards lucrative medical applications. In Europe, bio-derived cellulose and chitosan are steadily gaining traction in the biodegradable diaper market, bolstered by the introduction of a wood-pulp hydrogel. However, heightened purification costs, necessary to ensure residual acrylamide stays within FDA thresholds, are squeezing margins, particularly for non-integrated polyacrylamide suppliers.

Looking ahead, the hydrogel industry is poised for a split: while cost-effective polyacrylate will gravitate towards mega-plants with large capacities, high-performance silicone and bio-based variants will flourish, bolstered by strong intellectual property protections. Meanwhile, mid-tier polyacrylamide producers, lacking breakthroughs in biodegradability, face the dual threats of shrinking margins and potential buyouts.

By End-User Industry: Personal-Care Volume Versus Pharmaceutical Value

In 2025, personal care and hygiene accounted for a 47.61% share of tonnage, driven by a growing infant population in the Asia-Pacific and Africa regions, where diaper usage remains relatively low. Meanwhile, pharmaceuticals and healthcare, leveraging the high prices of implantable devices and antimicrobial dressings, are growing at a 7.79% CAGR with a smaller share of the volume. While agricultural soil conditioners made up a considerable part of the hydrogel market's tonnage, their value remained subdued due to subsidies that keep farm-gate prices low. However, food applications, like hydrogel coatings used on fruits, contribute to steady growth.

As the margin gap widens, suppliers are adjusting their strategies: Ashland and DSM are moving away from bulk hygiene, focusing instead on ISO 13485-certified medical-grade lines that boast higher gross margins. In contrast, Chinese producers are opting for mergers, aiming for feedstock integration to safeguard their commodity share. With a rising demand for premium healthcare, the divergence among end-users is set to shape the hydrogel market's strategy.

Geography Analysis

Asia-Pacific anchored 41.10% of global demand in 2025 and is projected to expand at an 8.02% CAGR through 2031. China invests heavily in polyacrylate and silicone-hydrogel clusters in Jiangsu and Guangdong, bolstering supply security and asserting cost leadership. India witnesses a diaper boom, attracting substantial plant investments from major companies, effectively sidestepping import duties. Japan's contact-lens sector pivots to daily disposable silicone-hydrogels in light of new health guidelines. Meanwhile, South Korea advances conductive hydrogel electrodes for smartwatch ECG functionalities. ASEAN initiatives are subsidizing hydrogels in drought-stricken rice regions, boosting regional market adoption.

North America accounted for a significant share of revenue in 2025, driven by the FDA's nod to multiple hydrogel devices leveraging the expedited 510(k) pathway. Medicare's reimbursement for advanced dressings spurs hospital uptake. However, Canada introduces value-based tenders emphasizing cost-per-healed-wound, steering suppliers towards clinical outcome validation. In Mexico, state tax credits for avocado producers using hydrogels not only conserve stressed aquifers but also carve out an agri-hydrogel niche in the NAFTA region.

Europe, holding a notable share of demand, is characterized by stringent biodegradability standards, pushing purchases towards cellulose and starch-grafted chemistries. The EU's Medical Device Regulation eases compliance hurdles, favoring established players with regulatory acumen in wound care. Post-Brexit, companies face dual filings under MHRA, elongating market entry for newcomers. In the Nordics, utilities are testing hydrogel-based phase-change systems for district heating, hinting at a broader thermal-storage potential.

South America, with a modest share, sees Brazil's sugarcane initiative conserving significant volumes of water annually. While Argentina grapples with higher unsubsidized prices dampening uptake, government-led pilots might tap into this dormant demand. The Middle East and Africa, together contributing a small share, spotlight Saudi Arabia's boost to hydrogel-driven greenhouse projects and South Africa's distribution of conditioners to drought-stricken maize farmers, albeit with logistical challenges.

Competitive Landscape

The hydrogel market remains moderately fragmented. Compliance with ISO 10993 and ISO 13485 becomes table stakes for hospital tenders, advantaging multinational incumbents over cash-constrained start-ups. Emerging university spin-outs feed the pipeline. Bulk hygiene players in China backward-integrate into acrylic acid to buffer feedstock volatility, whereas Western specialists forward-integrate into finished devices to capture value from proprietary coatings. This bifurcation suggests mid-tier formulators lacking either scale or IP will face consolidation pressures before 2030.

Hydrogel Industry Leaders

3M

Smith+Nephew

Johnson and Johnson

Coloplast Ltd

Convatec

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- July 2025: Hannox International Corp. introduced Hannox Wound Hydrogel, a sterile dressing for managing various wounds, including chronic, post-operative, bedsores, and ulcers. The dressing's key features include exudate absorption, bacterial protection, and moisture maintenance for enhanced healing.

- November 2024: Alcon released PRECISION7, a weekly replacement silicone hydrogel contact lens featuring the ACTIV-FLO System. The lens provides 16-hour comfort and clear vision, offering a cost-effective alternative to daily disposables.

Global Hydrogel Market Report Scope

Hydrogel is defined as a three-dimensional network of hydrophilic polymers capable of retaining significant amounts of water. It can be derived from synthetic or natural polymers and is responsive to external stimuli, such as temperature and pH, enabling it to adapt its function and structure based on environmental changes.

The hydrogel market is segmented by structure, material, end-user industry, and geography. By structure, the market is segmented into semi-crystalline, amorphous, and crystalline. By material, the market is segmented into polyacrylate, polyacrylamide, silicone, and other materials. By end-user industry, the market is segmented into personal care and hygiene, pharmaceuticals and healthcare, food, agriculture, and other end-user industries. The report also covers the market size and forecasts for the hydrogel market in 16 countries across major regions. The market sizing and forecasts have been done for each segment based on revenue (USD).

| Semi-crystalline |

| Amorphous |

| Crystalline |

| Polyacrylate |

| Polyacrylamide |

| Silicone |

| Other Materials |

| Personal Care and Hygiene |

| Pharmaceuticals and Healthcare |

| Food |

| Agriculture |

| Other End-user Industries |

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| ASEAN Countries | |

| Rest of Asia-Pacific | |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Russia | |

| NORDIC Countries | |

| Rest of Europe | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Middle East and Africa | Saudi Arabia |

| South Africa | |

| Rest of Middle East and Africa |

| By Structure | Semi-crystalline | |

| Amorphous | ||

| Crystalline | ||

| By Material | Polyacrylate | |

| Polyacrylamide | ||

| Silicone | ||

| Other Materials | ||

| By End-user Industry | Personal Care and Hygiene | |

| Pharmaceuticals and Healthcare | ||

| Food | ||

| Agriculture | ||

| Other End-user Industries | ||

| By Geography | Asia-Pacific | China |

| India | ||

| Japan | ||

| South Korea | ||

| ASEAN Countries | ||

| Rest of Asia-Pacific | ||

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Russia | ||

| NORDIC Countries | ||

| Rest of Europe | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Middle East and Africa | Saudi Arabia | |

| South Africa | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

What is the projected value of the hydrogel market in 2031?

It is forecast to reach USD 40.16 billion by 2031, from USD 28.47 billion, registering a 7.12% CAGR.

Which segment currently leads hydrogel demand by structure?

Semi-crystalline grades led with 45.56% revenue share in 2025.

How do hydrogels support water-saving agriculture?

Polyacrylamide conditioners absorb up to 500 times their weight, cutting irrigation frequency.

What regulatory challenge faces hygiene-grade polyacrylates in Europe?

Proposed microplastic-content labeling and biodegradability mandates could force reformulation by 2028.

Page last updated on: