Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

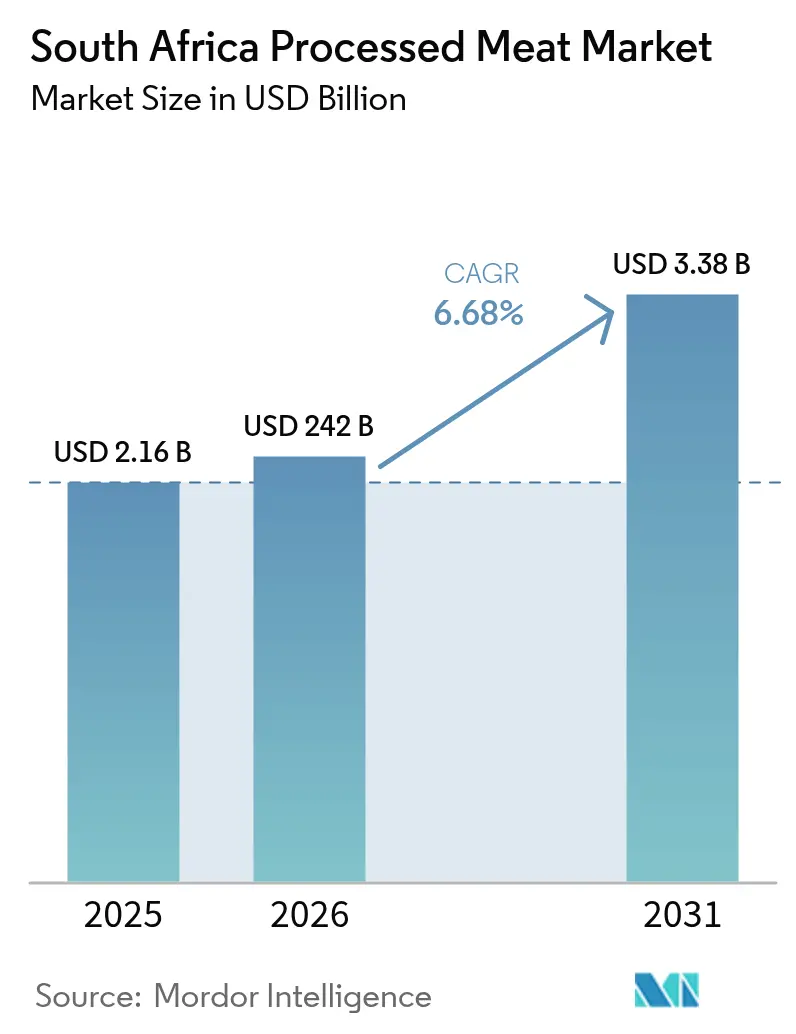

| Base Year Market Size (2025) | USD 2.16 Billion |

| Market Size (2026) | USD 242 Billion |

| Market Size (2031) | USD 3.38 Billion |

| Growth Rate (2026 - 2031) | 6.68% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

South Africa Processed Meat Market Analysis by Mordor Intelligence

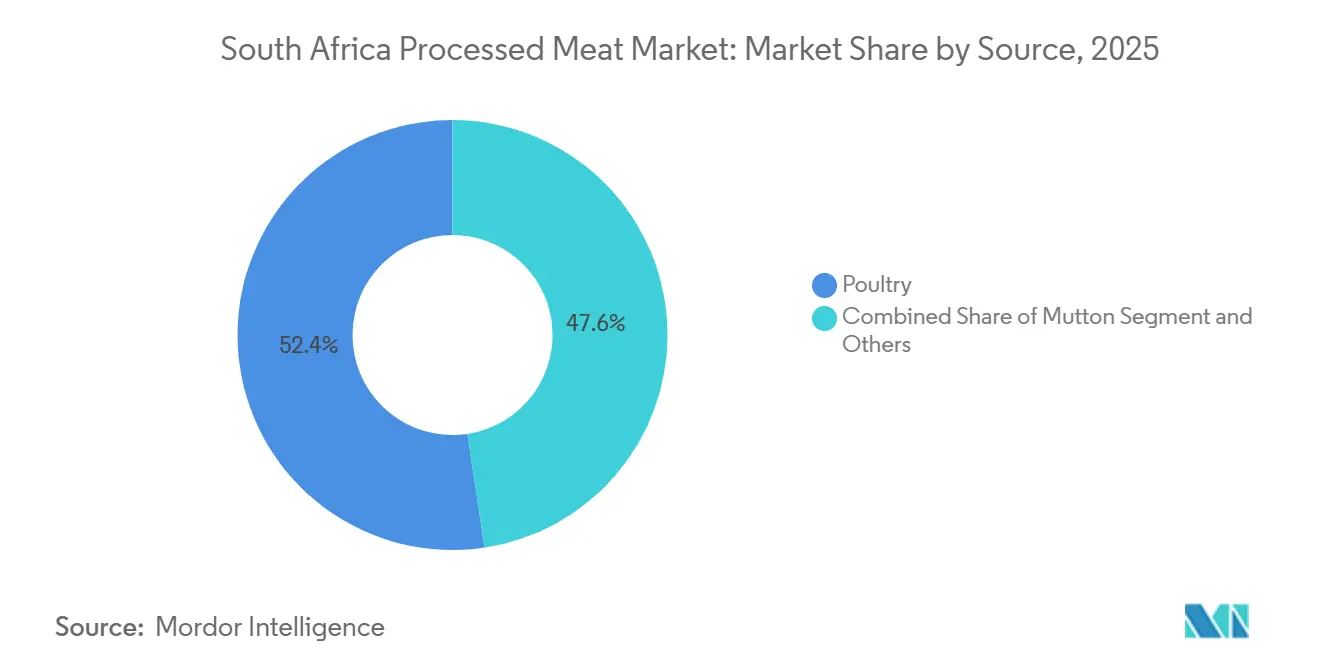

The South Africa processed meat market size was valued at USD 2.16 billion in 2025 and is estimated to grow from USD 2.42 billion in 2026 to reach USD 3.38 billion by 2031, at a CAGR of 6.68% during the forecast period (2026-2031). Demand tracks rapid urbanization, expanding cold-chain capacity, and certified halal exports, while public health concerns and the spread of plant-based analogues temper volume growth. Poultry leads with 52.38% of 2025 source-based volume on the back of integrated operations and price advantages over beef and pork. Chilled items dominate almost half of retail value because consumers equate refrigeration with freshness, yet frozen lines are expanding fastest, owing to load-shedding-resilient cold stores. Supermarkets and hypermarkets maintain buying power through national distribution centers, although online platforms such as Checkers Sixty60 lift e-commerce penetration and spur last-mile refrigerated logistics.

Key Report Takeaways

- By source, poultry secured 52.38% of the South Africa processed meat market share in 2025, while mutton is projected to advance at a 7.85% CAGR through 2031.

- By product type, meatballs led with 78.11% revenue share in 2025; sausages are forecast to expand at an 8.05% CAGR to 2031.

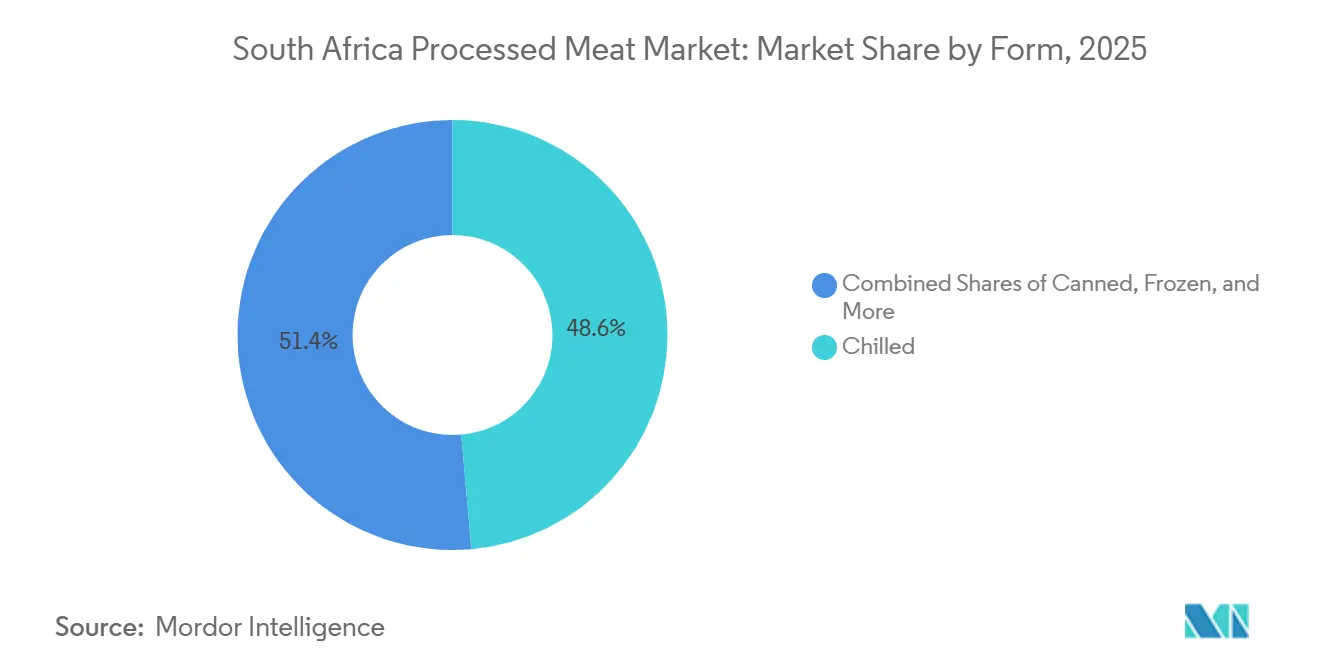

- By form, chilled formats accounted for 48.59% of value in 2025, whereas frozen offerings are growing at an 8.28% CAGR between 2026 and 2031.

- By distribution channel, supermarkets and hypermarkets captured 56.85% of 2025 sales, but online retail registers the highest forecast CAGR at 8.95% through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

South Africa Processed Meat Market Trends and Insights

Drivers Impact Analysis*

| Driver | % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rise of Urban Lifestyles and Convenience Food Demand | +1.2% | National, with concentration in Gauteng, Western Cape, KwaZulu-Natal metros | Medium term (2-4 years) |

| Growth in Chilled Meat-Snack Product Formats | +0.8% | National, with early gains in urban retail clusters | Short term (≤ 2 years) |

| Expansion of Modern Retail and Cold-Chain Infrastructure | +1.5% | National, led by Gauteng and Western Cape distribution hubs | Long term (≥ 4 years) |

| Improvements in Cold Chain Logistics | +1.0% | National, with spillover to SADC export corridors | Medium term (2-4 years) |

| Scaling of Halal-Certified SADC Exports Boosting Local Supply | +0.9% | National production, with export focus on Mozambique, Zimbabwe, Botswana | Medium term (2-4 years) |

| Adoption of High-Pressure Processing to Extend Shelf Life | +0.6% | National, concentrated among premium brands in Western Cape and Gauteng | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising Urban Lifestyles and Demand for Convenience Foods

Urbanization reached 65.78% by 2017 and continues to climb, concentrating purchasing power in Gauteng, Western Cape, and KwaZulu-Natal metros, where dual-income households prioritize time-saving meal solutions. This demographic shift underpins demand for pre-marinated, portion-controlled, and ready-to-cook processed meat formats that align with 30-minute meal preparation windows. McKinsey's 2024 State of Grocery Retail report noted that 42% of South African shoppers increased spending on convenience foods post-pandemic, a behavior sustained into 2025 as hybrid work models persist. Processors responded by launching single-serve meatball packs and microwave-ready sausage trays, capturing incremental margin from format premiums. The Food and Agriculture Organization's 2022 South Africa Food Systems Profile highlighted that meat products supply 11% of daily caloric intake, with poultry consumption tripling over two decades as affordability and convenience converged. Urban density also enables cold-chain efficiency, reducing last-mile spoilage and supporting chilled-product penetration in township retail networks where informal traders historically dominated.

Growth in Chilled Meat-Snack Product Formats

Chilled biltong, droëwors, and pre-sliced cold cuts are migrating from specialty butcheries into mainstream supermarket chillers, leveraging consumer perception that refrigerated products are fresher and less processed than shelf-stable alternatives. This category benefits from South Africa's indigenous meat-snacking culture, yet modern packaging, vacuum-sealed, resealable pouches with transparent windows, positions these items as premium grab-and-go options rather than bulk commodities. Retailers reported double-digit growth in chilled snack sales during 2025, driven by protein-focused diets and the portability required by mobile workforces, according to the USDA Foreign Agricultural Service[1]Source: USDA Foreign Agricultural Service, “Retail Foods Annual 2025,” usda.gov. The Perishable Products Export Control Board's 2024/25 annual report emphasized that digital cold-chain certification, mandated by 2025, ensures traceability from abattoir to retail, reducing contamination risk and extending chilled-product shelf life to 21-28 days. Artisanal producers, previously confined to farm stalls, now access national distribution through partnerships with Woolworths and Spar, fragmenting the category and elevating quality benchmarks. The shift also reflects health-conscious consumers seeking minimally processed snacks, a paradox given that biltong and droëwors undergo curing and drying, yet their "natural" positioning resonates more than emulsified sausages.

Expansion of Modern Retail and Cold-Chain Infrastructure

Five retail chains, Shoprite, Pick n Pay, Spar, Woolworths, and Massmart, controlled over 60% of South Africa's USD 50 billion retail food market in 2025, a concentration that drives cold-chain standardization and economies of scale. These chains invested in automated distribution centers equipped with blast freezers and temperature-monitored reefer trucks, reducing spoilage rates and enabling longer supply chains from rural abattoirs to urban stores. The Global Cold Chain Alliance documented that South Africa's cold-storage sector added over 50 million cubic feet of capacity between 2020 and 2024, with facilities incorporating backup generators and solar arrays to mitigate load-shedding disruptions. This resilience is critical for processed meat, where temperature excursions compromise safety and shelf life. Maersk's September 2025 insights noted that South Africa exported USD 13.7 billion in perishable goods, underscoring the infrastructure's dual role in domestic distribution and export competitiveness. Modern retail also enforces HACCP and ISO 22000 compliance, raising barriers for informal processors and consolidating share among certified players. The Department of Transport's February 2024 Freight Logistics Roadmap prioritized rail and port upgrades, which will further reduce logistics costs and enable processors to serve inland provinces more economically[2]Source: Department of Transport, “Freight Logistics Roadmap 2024,” transport.gov.za.

Improvements in Cold Chain Logistics

Load-shedding, South Africa's term for rolling blackouts, historically disrupted cold chains, causing an estimated 10 million tons of food waste annually. However, investments in diesel generators, lithium-ion battery storage, and solar-hybrid systems transformed the sector's resilience by 2024. Freight News reported in July 2024 that 85% of refrigerated containers returned empty from export shipments, prompting logistics providers to backhaul chilled imports and optimize asset utilization. The Perishable Products Export Control Board's digital certification platform, operational since 2025, integrates IoT sensors that transmit real-time temperature data, enabling proactive intervention before spoilage occurs[3]Source: Perishable Products Export Control Board, “Annual Report 2024/25,” ppecb.com. This transparency reassures retailers and consumers, supporting premium pricing for verified cold-chain products. Third-party logistics providers such as Imperial Logistics and Bidvest expanded reefer fleets, offering processors flexible capacity without capital expenditure. The Department of Transport's roadmap also targets intermodal rail-road solutions, which could reduce diesel dependency and carbon footprint, a consideration as European export markets tighten sustainability requirements. Improved logistics enable processors to source livestock from lower-cost rural regions while maintaining product integrity, compressing farm-to-fork timelines and enhancing margin.

Restraints Impact Analysis*

| Restraint | % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Health Concerns and Negative Consumer Perceptions | -0.8% | National, with higher impact in urban, educated demographics | Medium term (2-4 years) |

| Volatile Feed and Livestock Input Costs | -0.5% | National, concentrated among vertically integrated poultry and pork producers | Short term (≤ 2 years) |

| Intense Competition from Alternative Protein Sources | -0.7% | National, led by Western Cape and Gauteng retail innovation | Medium term (2-4 years) |

| Increasing Flexitarian and Plant-Protein Substitution Trends | -0.4% | National, with early adoption among millennials and Gen Z | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Health Concerns and Negative Consumer Perceptions

The World Health Organization's International Agency for Research on Cancer classified processed meat as a Group 1 carcinogen in 2015, concluding that each 50-gram daily serving increases colorectal cancer risk by 18%. This classification, reinforced in WHO's 2024 Healthy Diet fact sheet, permeates South African public-health messaging and media coverage, particularly as non-communicable diseases account for a rising share of the disease burden. Deloitte's January 2025 Consumer Tracker found that 37% of South African respondents reduced meat consumption over the prior year, citing health and environmental motivations. Younger, urban, and higher-income cohorts are disproportionately represented in this shift, the same demographics that drive premium-product adoption and influence broader consumption norms. Processors face a strategic dilemma: reformulating to reduce sodium, nitrites, and saturated fat can compromise taste and shelf life, yet failing to address health concerns risks long-term volume erosion. Some brands introduced "better-for-you" lines featuring organic meat, reduced additives, and transparent sourcing, yet these command price premiums that limit mass-market penetration. The Competition Commission's June 2024 Fresh Produce Market Inquiry highlighted that input-cost inflation constrains processors' ability to invest in reformulation without passing costs to price-sensitive consumers.

Volatile Feed and Livestock Input Costs

Yellow maize, the primary poultry and pork feed ingredient, exhibited price swings of 16% between November 2024 and January 2025, with the South African Grain Information Service reporting ZAR 4,111 per ton in November 2024 and ZAR 3,542 per ton by January 2025. Such volatility compresses margins for vertically integrated producers like Astral Foods and RCL Foods, which operate feed mills, farms, and processing plants. The Bureau for Food and Agricultural Policy's 2024 Baseline Report projected maize production of 16.8 million tons for the 2024/25 season, yet drought risk and input-cost inflation, fertilizer prices rose 12% year-on-year in 2024, introducing uncertainty. Processors lacking vertical integration face even sharper margin pressure, as they purchase livestock at spot prices that reflect feed-cost spikes. Statistics South Africa's December 2024 Consumer Price Index showed meat prices declining 0.4% year-on-year, indicating that processors absorbed input-cost increases rather than passing them to consumers, a strategy that erodes profitability. The Competition Commission's inquiry into input costs revealed that concentration among feed suppliers and livestock genetics providers limits processors' negotiating power, a structural constraint that periodic price relief cannot resolve. Climate variability, exacerbated by El Niño cycles, adds further unpredictability, compelling processors to hedge via futures contracts or diversify sourcing—both of which carry financial and operational complexity.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Source: Poultry Anchors Volume, Mutton Targets Premium

In 2025, poultry accounted for a dominant 52.38% of the market volume, underscoring its cost efficiency. Chicken requires only 1.7 kg of feed to produce 1 kg of meat, significantly outperforming beef, which needs 6-8 kg of feed for the same output. Imports from Brazil and the EU have been instrumental in maintaining competitive domestic prices, although these imports have occasionally triggered the imposition of anti-dumping duties. Mutton, while representing a smaller segment, is anticipated to grow at a robust 7.85% CAGR through 2031. This growth is fueled by strong halal demand during religious festivals and limited domestic flock numbers, which constrain supply. Beef and pork occupy a mid-tier position in the market. Beef faces restrictions due to export bans linked to foot-and-mouth disease outbreaks, while pork consumption is limited by religious and cultural preferences.

Market processors are adopting innovative strategies by blending proteins to reduce costs and cater to diverse consumer preferences. Products such as poultry-pork sausages and beef-mutton patties are gaining traction among mixed-income households. Leading players like Astral Foods, RCL Foods, and Country Bird dominate the poultry processing segment, leveraging economies of scale in feed milling and hatchery operations. Meanwhile, farmer-owned Eskort secures stable pork input prices, ensuring consistent supply. By 2025, the South African processed meat market for poultry reached a valuation of USD 1.13 billion, representing 52.38% of the total market value. This dominance underscores the efficiency of poultry production and its critical role in the market. Mutton processors are increasingly investing in traceability systems and upgrading cold storage facilities to capitalize on export premiums and meet international standards.

By Product Type: Meatballs Dominate, Sausages Innovate

In 2025, meatballs dominated South Africa's processed meat market, contributing 78.11% of total sales and generating USD 1.69 billion in revenue. This strong performance is primarily driven by their versatility in various dishes, including pasta, rice-based meals, and school feeding programs, where their standardized spherical shapes and cost-effective pricing make them a preferred choice. Looking ahead, sausages are projected to achieve the highest growth, with a robust 8.05% CAGR through 2031. This growth is fueled by the cultural significance of boerewors and continuous flavor innovations, such as peri-peri and cheese-infused options. Patties, while serving the quick-service restaurant (QSR) and retail burger segments, face increasing competition from plant-based alternatives that replicate their texture and mouthfeel.

To reduce production costs, processors are increasingly utilizing mechanically deboned meat in meatball production and adopting automated forming technologies to lower labor expenses. Sausages benefit significantly from South Africa's braai culture, particularly during public holidays when demand peaks. To further expand their market presence, processors are focusing on breakfast-link formats to capture a share of the morning meal segment. On the other hand, cured meats are experiencing slower growth due to rising health concerns among consumers, who associate nitrites with cancer risks. In response, manufacturers are reformulating products to be nitrite-free, although this shift has led to increased production costs.

By Form: Chilled Freshness Meets Frozen Convenience

In 2025, chilled lines accounted for 48.59% of the market value, driven by consumer preferences for refrigeration, which is perceived as a marker of freshness and minimal processing. The introduction of digital cold-chain certification has further enhanced product reliability, ensuring a shelf stability of 21-28 days. This advancement has significantly reduced product returns and enabled manufacturers to command premium pricing. On the other hand, frozen products are anticipated to grow at a robust CAGR of 8.28%. This growth is supported by the adoption of backup power solutions and solar systems, which effectively mitigate the risks associated with load-shedding. These developments have expanded the distribution network, allowing frozen products to reach remote provinces where delivery frequency is lower.

Processors are increasingly viewing frozen outputs as a strategic measure to address seasonal demand fluctuations and as an opportunity to export surplus products to SADC markets. By 2031, the processed meat market in South Africa for frozen formats is expected to reach USD 1.75 billion. This growth reflects the sector's resilience to load-shedding challenges and the rising trend of household bulk purchasing. As electrification continues to improve, the relevance of canned meats is diminishing, with consumers shifting toward products that offer better taste and texture.

By Distribution Channels: Supermarkets Reign, Online Accelerates

Supermarkets and hypermarkets captured 56.85% of the distribution share in 2025, anchored by Shoprite, Pick n Pay, Spar, Woolworths, and Massmart, which collectively control over 60% of South Africa's retail food market. Online retail is surging at 8.95% CAGR, led by Checkers Sixty60's rapid delivery, Woolworths' e-commerce platform, and third-party aggregators such as Takealot and Mr D Food. Convenience stores, including franchises like Engen and Shell forecourts, serve impulse purchases and top-up shopping, yet their limited chiller space constrains processed-meat assortments. Specialty stores, butcheries, and delicatessens retain loyal customers seeking artisanal products and personalized service, though their collective share erodes as supermarkets expand premium private-label ranges.

Other channels, including informal traders and spaza shops, persist in townships but face formalization pressure as municipalities enforce health and licensing regulations. In response, the South African processed meat industry has adopted dark-store models to reduce pick-and-pack times, while leveraging dynamic routing software to optimize delivery routes and lower mileage. Specialty butcheries continue to attract affluent urban customers by offering premium services such as dry-aged beef and custom slicing. However, their ability to scale operations is constrained by rising rental and labor expenses. On the other hand, convenience stores are focusing on catering to forecourt shoppers by stocking shelf-stable sausages that align with their needs for quick and portable food options.

Geography Analysis

Gauteng dominates regional demand, driven by its high urban density, well-established cold-storage infrastructure, and higher disposable incomes among its population. Retail audit data highlights that chilled chicken meatballs and boerewors sell 30% faster in Johannesburg and Pretoria compared to the national average, showcasing the region's strong consumer preference for processed meat products. The Western Cape follows as the second-largest market, supported by Cape Town's thriving tourism industry and premium retail environment, which cater to a demand for high-quality, HPP-treated sausages with clean labels. KwaZulu-Natal rounds out the top three urban markets, leveraging the logistical advantages of Durban's port, which significantly reduces inbound feed and packaging costs, further enhancing the region's competitiveness.

Secondary provinces, including Eastern Cape and Mpumalanga, lag behind due to cold-chain penetration levels that remain below the national average. However, the installation of solar micro-grids at regional distribution centers is gradually improving the distribution and availability of frozen SKUs in these areas. Limpopo and North West, on the other hand, demonstrate above-average growth potential. This growth is fueled by increasing employment in the mining sector, which raises household incomes and drives demand for bulk frozen purchases, particularly through discount retail chains. Northern Cape, the smallest province due to its sparse population, relies on processors shipping shelf-stable products such as droëwors and canned corned beef. These products are distributed through wholesaler networks, effectively bypassing the limitations posed by inadequate cold-chain infrastructure.

Exports are routed through Gauteng's distribution centers to land ports and Durban's reefer terminals, with key destinations including Mozambique, Zimbabwe, and Botswana. Halal-certified poultry from KwaZulu-Natal benefits from shorter transit times to Maputo via the N2 corridor, which strengthens the supply of mutton and chicken in Muslim-majority sub-markets. By 2025, the processed meat market size for SADC exports from South Africa reached USD 215 million, supported by harmonized halal protocols that streamline trade and ensure compliance with regional standards.

Competitive Landscape

In South Africa's processed meat market, established players maintain a dominant position. However, competitive dynamics continue to drive innovation and exert pricing pressures, as reflected in a moderate concentration score. Companies such as Astral Foods, which reported ZAR 20.5 billion in revenue in 2024, highlight the growing trend of vertical integration. These firms oversee the entire value chain, from poultry production to feed manufacturing and processing, ensuring greater control over operations. To address labor constraints, many companies, including key industry leaders, are increasingly adopting advanced technologies. Investments in automation, robotics, and high-pressure processing are becoming pivotal strategies to enhance operational efficiency and improve product quality.

Tiger Brands exemplifies the benefits of strategic partnerships by employing an aggregator model to integrate black wheat and oat farmers into its supply chain. This approach not only ensures a consistent supply of raw materials but also contributes to community development. While established players proceed cautiously, significant opportunities exist in untapped areas such as alternative protein segments, premium convenience products, and export markets. Companies like AVI Ltd. and Mogale Meat are leading the charge in exploring cultivated meat technologies, which have the potential to disrupt traditional meat processing methods.

At the same time, plant-based alternatives are steadily gaining popularity, with 67% of South Africans expressing a willingness to try these products. However, compliance with the Meat Safety Act and adherence to global food safety standards present significant challenges. These regulatory requirements create entry barriers that favor established players while necessitating continuous investments in quality assurance systems. Additionally, as the industry contends with infrastructure challenges, many companies are proactively investing in backup power and water systems. These measures underscore the importance of operational excellence as a key competitive advantage in the market.

South Africa Processed Meat Industry Leaders

RCL Foods

BRF SA

Astral Foods (Pty) Ltd

Eskort Bacon Co-Operative Ltd

Tiger Brands Ltd

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2025: Under its Earlybird Farm brand, Astral Foods has launched a new range of Southern Style Crumbed Chicken, conveniently packaged in resealable packs. This new line features pre-cooked crumbed chicken thighs and strips, tailored for oven baking or air frying, targeting consumers desiring quick, high-quality meals.

- July 2024: Eskort, South Africa's leading pork manufacturer, officially launched a 10,000m² factory extension in Heidelberg, Gauteng, boosting weekly pig processing capacity from 6,000 to 9,000.

- November 2024: JBS is investing USD 2.5 billion into six meat-processing plants across Nigeria. In a recent statement, JBS revealed its plans: three facilities will focus on poultry, two on beef, and one on pork. These initiatives, underscored by a memorandum of understanding with the Nigerian government, aim to foster "sustainable production chains for food production" in Nigeria.

South Africa Processed Meat Market Report Scope

Processed meat is considered to be any meat that has been modified to either improve its taste or extend its shelf life. Methods of processing meat include salting, curing, fermentation, smoking, and adding chemical preservatives. The South African processed meat market is segmented by source, by product, and by distribution channel. Based on source, the market is segmented into poultry, pork, beef, lamb, and mutton. Based on product type, the market is segmented into chilled, frozen, and shelf-stable. Based on distribution channel, the market is segmented into online retail stores and offline retail stores. For each segment, the market sizing and forecasts have been done on the basis of value (in USD million).

By Source

| Poultry |

| Pork |

| Beef |

| Mutton |

| Other Meat Type |

By Product Type

| Sausages |

| Meatballs |

| Patties |

| Cured Meat |

| Other Processed Meat |

By Form

| Chilled |

| Frozen |

| Canned |

| Others |

By Distribution Channels

| Supermarkets/Hypermarkets |

| Convenience Stores |

| Specialty Stores |

| Online Retailers |

| Other Distribution Channels |

| By Source | Poultry |

| Pork | |

| Beef | |

| Mutton | |

| Other Meat Type | |

| By Product Type | Sausages |

| Meatballs | |

| Patties | |

| Cured Meat | |

| Other Processed Meat | |

| By Form | Chilled |

| Frozen | |

| Canned | |

| Others | |

| By Distribution Channels | Supermarkets/Hypermarkets |

| Convenience Stores | |

| Specialty Stores | |

| Online Retailers | |

| Other Distribution Channels |

Key Questions Answered in the Report

How fast will processed meat demand grow in South Africa through 2031?

Aggregate value is forecast to rise at a 6.68% CAGR from 2026-2031, reaching USD 3.38 billion by the end of the period.

Which protein dominates the national processed portfolio?

Poultry accounts for 52.38% of 2025 volume, supported by integrated supply chains and lower retail pricing.

What retail format captures the largest share of sales?

Supermarkets and hypermarkets held 56.85% of 2025 revenue, thanks to nationwide distribution centers and private-label ranges.

Which product type shows the strongest growth momentum?

Sausages are projected to expand at an 8.05% CAGR to 2031, powered by boerewors heritage and flavor innovation.

Page last updated on: