Market Overview

| Study Period | 2021 - 2031 |

|---|---|

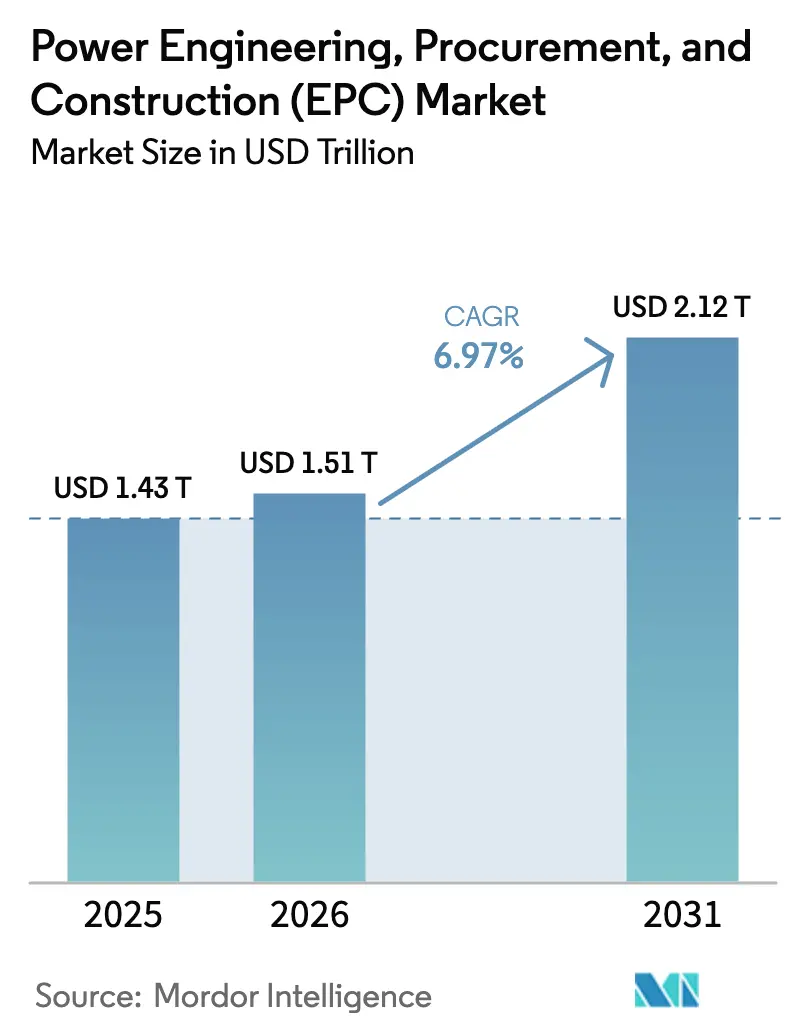

| Market Size (2026) | USD 1.51 Trillion |

| Market Size (2031) | USD 2.12 Trillion |

| Growth Rate (2026 - 2031) | 6.97% CAGR |

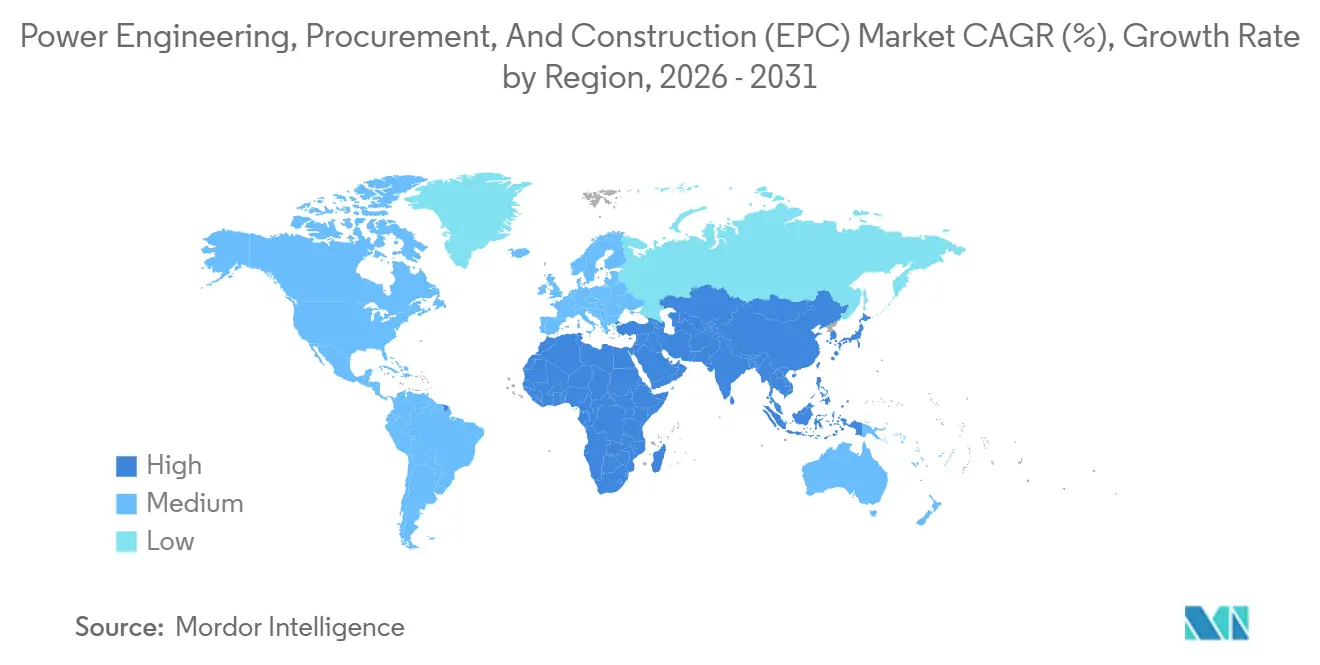

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia-Pacific |

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Power Engineering, Procurement, And Construction (EPC) Market Analysis by Mordor Intelligence

The Power Engineering, Procurement, And Construction Market size is expected to grow from USD 1.43 trillion in 2025 to USD 1.51 trillion in 2026 and is forecast to reach USD 2.12 trillion by 2031 at 6.97% CAGR over 2026-2031.

Rising national net-zero mandates, accelerated renewable additions, and an upsurge in captive micro-grids for hyperscale data centers are widening the project pipeline while diversifying the risk profile across geographies.[1]United Nations Framework Convention on Climate Change, “Net Zero Tracker,” unfccc.int Asia-Pacific dominates current activity, but South America is registering the fastest growth as Brazil’s auctions and Chile’s hydrogen plans scale up grid-connected and behind-the-meter installations. Competitive dynamics remain fluid: Chinese and Indian conglomerates win volume on cost, yet HVDC specialists and offshore-wind integrators earn premium margins on complex scopes. Two structural brakes, high up-front capex and a shortage of HVDC/offshore personnel, continue to stretch commissioning timelines in North America and Europe.

Key Report Takeaways

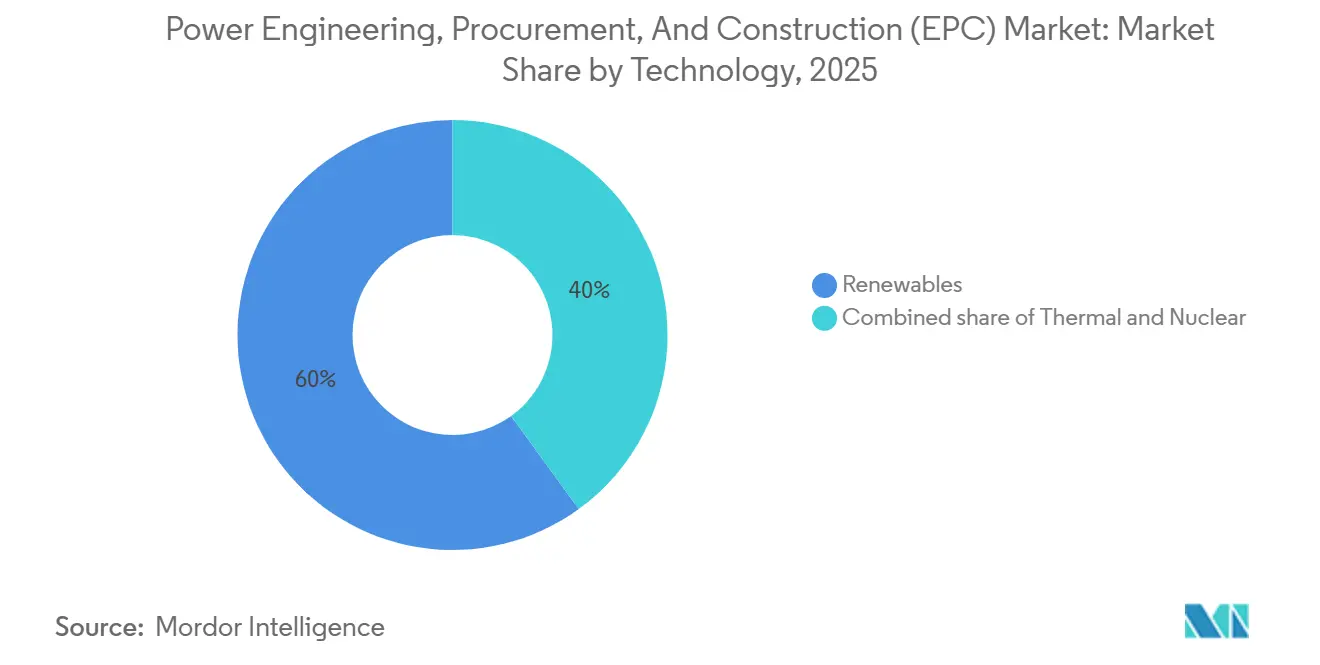

- The global power EPC market is segmented into power generation EPC and power transmission and distribution (T&D) EPC. Power generation EPC accounted for 50.98% of the market in 2025, while power transmission and distribution (T&D) EPC is projected to grow at a 7.39% CAGR through 2031, outpacing generation EPC.

- By technology, renewables commanded 60% of the 2025 power generation EPC market and are advancing at a 7.8% CAGR through 2031.

- By capacity band, the above 500 MW range captured 51.5% of the global power generation EPC market size in 2025, while the up to 100 MW distributed-energy-resource segment is poised to grow at an 8.1% CAGR to 2031.

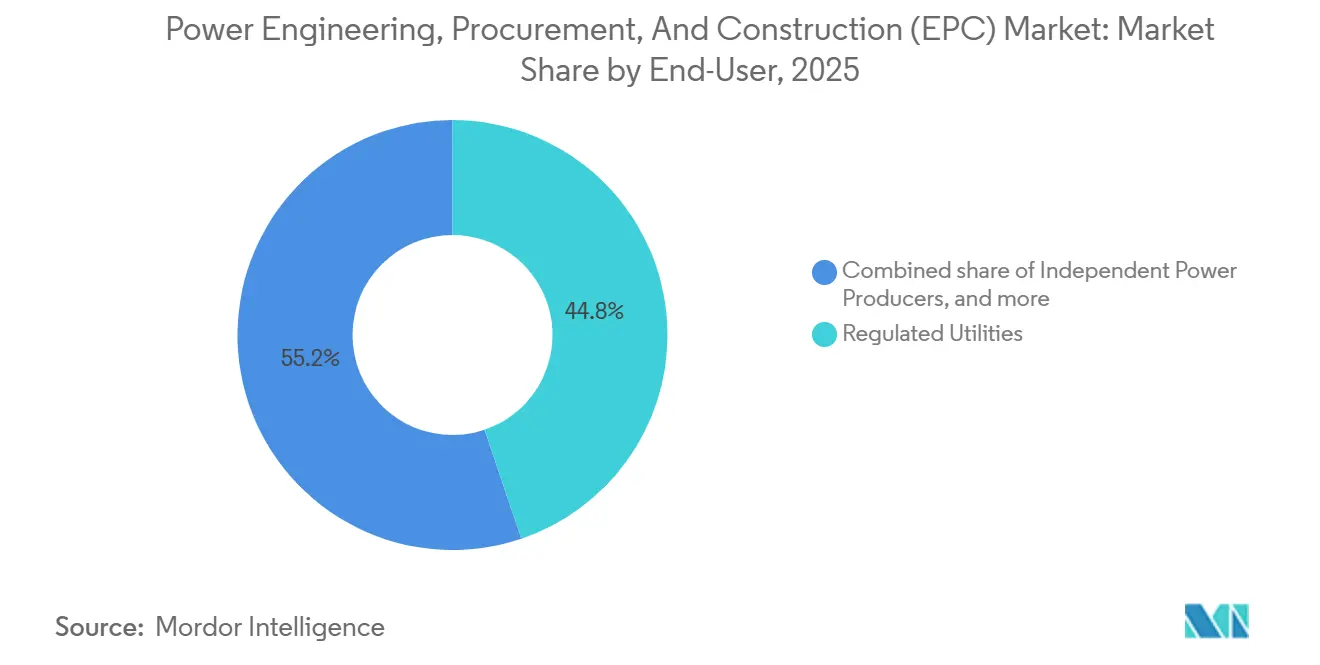

- By end user, regulated utilities held 44.8% of the 2025 power generation EPC market; independent power producers are growing fastest at 7.7% to 2031.

- By geography, Asia-Pacific led with a 59.4% share of the power generation EPC market in 2025, while South America is expected to expand at a 7.5% CAGR through 2031.

- The power transmission and distribution (T&D) EPC market is segmented by geography: Asia-Pacific accounted for the largest share of 48.1% in 2025, and is also projected to lead the market growth with a CAGR of 8.6% through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Power Engineering, Procurement, And Construction (EPC) Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growing power demand in emerging economies | +1.2% | APAC core, spill-over to Middle East and Africa | Medium term (2-4 years) |

| Accelerated renewable-energy build-out | +1.8% | Global, with concentration in APAC, Europe, North America | Short term (≤ 2 years) |

| Aging grid and generation asset replacements | +0.9% | North America, Europe, select APAC markets | Long term (≥ 4 years) |

| National net-zero mandates unlocking EPC pipelines | +1.5% | Global, led by EU, North America, China, India | Medium term (2-4 years) |

| Hyperscale data-center micro-grids | +0.7% | North America, Europe, APAC hubs (Singapore, Tokyo) | Short term (≤ 2 years) |

| GW-scale green-hydrogen projects | +0.6% | Middle East, Europe, Australia | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Growing Power Demand in Emerging Economies

Electricity use in emerging markets is increasing at 5-7% annually, pushing utilities to accelerate EPC tenders for gas turbines and utility-scale solar assets that close supply gaps.[2]United Nations Framework Convention on Climate Change, “Net Zero Tracker,” unfccc.int India added 24 GW of renewables in 2024, yet industrial states still record peak shortages that channel USD 8 billion each year into captive EPC contracts.[3] International Energy Agency, “World Energy Outlook 2025,” iea.org Sub-Saharan Africa’s electrification hit 54% in 2025, but grid-extension costs of USD 3,000 per rural connection steer donor programs toward mini-grid EPC packages bundling solar, storage, and prepaid metering. Local fabrication yards and vendor networks gain an advantage because transformer import duties can swell project costs by up to 20%. The contract model is shifting from turnkey lump-sum to EPCM frameworks that leave schedule risk with owners yet preserve contractor equipment margins.[4]Central Electricity Authority of India, “Monthly Generation Report,” cea.nic.in

Accelerated Renewable-Energy Build-Out

Global renewable additions hit 507 GW in 2024, but EPC execution trails equipment availability by 12-18 months due to land and grid connection delays. The 3.5 GW Terra Solar complex in the Philippines demonstrates scale changes; prefabricated racking slashes on-site installation to 14 months on a USD 3.5 billion contract. Offshore wind is spreading into the Atlantic seaboard, yet limited Jones Act vessels move first-turbine dates into late 2026, leaving a USD 12 billion backlog for marine EPC firms. Floating offshore wind below 1 GW today requires niche mooring know-how possessed by fewer than a dozen contractors. Tighter rules, such as the EU’s one-year window for environmental assessments, compel EPC bidders to front-load ecological studies, balancing risk and speed.

National Net-Zero Mandates Unlocking EPC Pipelines

More than 140 countries have set net-zero targets, translating into 1,200 GW of planned generation and 400,000 circuit-km of transmission upgrades by 2035. U.S. tax credits now require 40% domestic steel and 55% domestic labor, reshaping bid teams and excluding foreign contractors from bonus rates. India’s Green Hydrogen Mission calls for 5 million t/year of output, driving 60 GW of renewables and USD 25 billion in EPC contracts. Saudi Arabia’s NEOM green-hydrogen facility broke ground in 2024 with the largest single EPC contract to date at 4 GW of hybrid capacity. Procurement cycles compress from 24 to 12 months, rewarding contractors with modular supply lines.

Hyperscale Data-Center Micro-Grids

Hyperscale data centers consumed 460 TWh in 2024 and may hit 1,000 TWh by 2030 as AI workloads multiply. Operators sidestep 3.7-year grid queues by signing 20-year PPAs linked to co-located generation, such as Microsoft’s 500 MW nuclear offtake in 2024. Black & Veatch and Kiewit launched divisions that bundle substation design, diesel backup, and batteries under a single point of responsibility. Micro-grid EPC margins run 12-15%, almost double utility projects because of condensed schedules and bespoke guarantees. Digital-twin commissioning validates islanding and black-start functions before handover, meeting IEEE 1547 and IEC 62933 standards.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High upfront capex and financing risk | -0.8% | Global, acute in emerging markets | Medium term (2-4 years) |

| Global supply-chain volatility | -0.5% | Global, with acute pressure in North America, Europe | Short term (≤ 2 years) |

| Shortage of HVDC/offshore EPC talent | -0.4% | North America, Europe, select APAC markets | Medium term (2-4 years) |

| Permitting delays for large infrastructure | -0.6% | North America, Europe, Latin America | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High Upfront Capex and Financing Risk

Utility-scale projects demand USD 1-4 billion in capital, yet emerging-market debt spreads hover 450-650 basis points over U.S. Treasuries, curbing bank appetite. Currency devaluation of 10% can shave 200-300 basis points off returns when equipment is dollar-denominated. Contractors increasingly structure build-own-operate-transfer deals that defer payment until COD, although balance-sheet exposure limits the number of parallel jobs. Inflation in steel, copper, and cement, up 12-18% between 2023 and 2025, triggers force-majeure claims on fixed-price contracts, steering owners toward cost-plus-fee models.

Permitting Delays for Large Infrastructure

The U.S. average from environmental review to notice to proceed rose to 4.2 years for transmission projects in 2024, up from 2.8 years in 2019. Similar patterns appear in the EU, where cross-border HVDC links require 36-48 months of multi-state approvals. Developers now front-load community engagement and route flexibility, adding 3-5% to soft-cost budgets yet avoiding multi-year litigation. Contractor holding costs rise as equipment sits idle; transformer lead times of 18 months exacerbate delay penalties. These bottlenecks cap the attainable growth rate below component manufacturing levels despite strong demand pull.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Technology: Renewables Extend Lead

Renewables accounted for 60% of the Power generation EPC market share in generation spending during 2025 and are tracking a 7.8% CAGR to 2031. Utility-scale solar EPC costs have fallen to USD 850 per kW for fixed-tilt arrays, but bifacial modules and trackers add USD 100-150 per kW, compressing contractor margins to 6-8%. Offshore wind maintains gross margins above 12% as unit costs sit near USD 4,000 per kW due to marine logistics. Hybrid solar-storage projects already represent 18% of renewable awards, driven by grid operators mandating 2-4 hours of dispatchable capacity.

Second-order dynamics underpin this lead. Renewable debt lines price at 4-6% in OECD markets compared with 8-12% for coal and nuclear, and lenders prefer the shorter build cycles of solar and onshore wind. Contractors with digital-twin workflows cut commissioning errors by 20%, shortening time to revenue. Stranded-asset concerns degrade new-build coal awards, now just 8 GW, concentrated in a handful of emerging economies. Thermal repowering into gas or biomass offers a niche for brownfield specialists. Nuclear EPC firms bank on small modular reactors, yet first-mover risk and supply-chain depth remain constraints.

By Capacity Band: Distributed Resources Gain Headroom

Projects above 500 MW controlled 51.5% of 2025 spend, leveraging economies of scale that pull EPC cost below USD 1 million per MW for solar and USD 1.5 million for onshore wind. Distributed energy resources under 100 MW, however, are registering the fastest 8.1% CAGR to 2031, riding hyperscale data-center and remote-mining demand for resilience. The mid-tier 100-499 MW band captured 28% share as IPPs and municipal utilities pursue manageable ticket sizes.

Contractors are reorganizing to match this split. Large EPC firms are purchasing micro-grid integrators to tap sub-100 MW work, while pure-play renewable builders form consortia to meet bonding requirements on gigawatt-scale bids. Modular factory pre-assembly trims on-site labor by 30% and compresses schedules by up to three months. Micro-grids under 10 MW grew 11% in 2024, especially among Australian and Chilean mines that cut diesel costs 40-60% with solar-battery hybrids. Data-center solutions in the 50-150 MW range blend gas engines for black start with lithium-ion storage to meet IEEE 1547 compliance.

By End User: IPPs Close Ground

Regulated utilities held 44.8% of 2025 generation spend, yet independent power producers are advancing at a 7.7% CAGR as merchant renewables win corporate PPAs outside utility procurement. Industrial captive power captured 22% by installing 50-200 MW solar-storage hybrids that hedge outage risk in Asia and Africa. Public-sector entities in China and the Middle East issued 18% worth of EPC, backed by sovereign guarantees that lower financing costs.

Corporate PPAs totaling 48 GW in 2024, led by Amazon, Microsoft, and Google, bypass utilities and feed IPP pipelines. Merchant generators undercut regulated tariffs by 10-15% in deregulated markets, pressuring utility EPC backlogs. Smaller manufacturers cluster rooftop solar via virtual power plants, pooling 5-10 MW of capacity to improve creditworthiness. Utilities retain advantages in rate-based financing but increasingly outsource riskier builds through EPCM arrangements that swap fixed-price certainty for schedule agility.

Geography Analysis

Asia-Pacific controlled 59.4% of the power generation EPC value in 2025, fueled by China’s 120 GW annual renewable build and India’s 24 GW addition. China’s coal EPC slipped to 8 GW in 2024 as policy pivots to wind, solar, and nuclear for its 2060 neutrality pledge. India preserved 12 GW of thermal EPC for reliability, but now layers 60% domestic-content rules on solar projects above 500 MW.

South America is the fastest-growing region (power generation EPC) at a 7.5% CAGR through 2031, anchored in Brazil’s 15 GW of 2024 auction wins at sub-USD 30 per MWh rates and Chile’s 25 GW hydrogen-linked pipeline. Argentina and Colombia add niche gas and offshore wind jobs, although currency controls and differing vessel laws adjust cost structures.

North America and Europe share bottlenecks. Interconnection queues defer 60 GW of shovel-ready assets into 2027-2028 and elevate the role of behind-the-meter builds. The Inflation Reduction Act’s domestic-content rules push Fluor and Bechtel to onshore transformers, adding 8-12 months to procurement but unlocking 30% tax credits. Europe’s next growth spurt rests on floating offshore wind platforms where EPC costs sit 40% above fixed-bottom solutions.

Regulatory Landscape

Power EPC execution is being shaped by permitting and grid-connection policy, where environmental review timelines and interconnection rules determine notice-to-proceed dates. In the United States, 2026 policy actions and active legislation around federal permitting, including NEPA-related reforms highlighted by the White House and bills progressing in the 119th Congress such as S.4475 and the American Energy and Mineral Infrastructure Act text released in June 2026, indicate a push to streamline approvals for major energy infrastructure, with direct implications for transmission and generation EPC schedules.

In Europe, accelerated renewable deployment is being supported by streamlined permitting frameworks under RED III, including the designation of renewable "go-to" areas and compressed permitting timelines that are often referenced as a 12-month pathway in targeted zones. Across markets, grid constraints remain a regulatory focus as connection queues and system planning requirements drive more detailed studies, staged interconnection, and stricter technical compliance for storage and large loads. This increases the value of EPC contractors that can support early-stage permitting, interconnection, and standards integration.

Competitive Landscape

The Power EPC Market demonstrates moderate fragmentation: the top 10 contractors capture around 35-40% of global value, yet regional champions enjoy home-market shelter through policy and local-content mandates. Chinese SOEs undercut Western peers by up to 20% but face OECD scrutiny that narrows addressable projects. Indian firms such as Larsen & Toubro and Adani Infrastructure vertically integrate into modules and development, blurring EPC and IPP boundaries.

Western multinationals pursue higher-margin engineering-only roles that earn 10-12% fees while dropping construction risk. Technology is the next moat: Hitachi Energy’s HVDC Light and ABB’s modular multilevel converters enable bidirectional flow and black-start, prized for offshore wind connections. Siemens Energy and GE Vernova embed digital twins to shave 15-20% off commissioning schedules. Disruptors such as Fluence and Wartsila back-integrate into solar EPC, while Autodesk and Bentley Systems license project-management software that captures 2-3% of contract value without balance-sheet exposure.

Power Engineering, Procurement, And Construction (EPC) Industry Leaders

Bechtel Corporation

PowerChina

Larsen & Toubro

Fluor Corporation

Siemens Energy AG (EPC Services)

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

Co-located solar-plus-storage and utility-scale storage integration is expanding the addressable EPC scope as grid operators and offtakers look for firmed output and faster delivery rather than waiting for transmission upgrades. This shift is reflected in 2026 project financing and construction starts, including Masdar reaching financial close on a 5.2 GW solar project paired with a 19 GWh BESS in Abu Dhabi (USD 6.1 billion investment), and Cypress Creek Energy breaking ground on the USD 4.5 billion Steel River Energy Center in Arkansas (2.5 GW solar and 2.9 GWh storage) backed by a 20-year Google PPA. Both cases broaden EPC demand for integrated civil works, high-voltage balance-of-plant, and storage commissioning.

Firm-capacity and system-adequacy mechanisms are also creating design-driven whitespace for EPC contractors as technical requirements evolve. Germany's StromVKG, passed July 2026, introduces a centralized, auction-based capacity market with defined delivery rules that affect technology selection and plant configurations. In North America, FERC actions in 2026 targeting large-load interconnection and reliability standards for computational loads highlight data center-driven grid upgrades as a near-term source of substation, interconnection, and behind-the-meter microgrid EPC work. Conventional generation continues to anchor large-ticket awards for stability, including Energy China receiving a USD 1.69 billion EPC contract in June 2026 for the 2.6 GW Taweelah C CCGT plant in Abu Dhabi.

Recent Industry Developments

- May 2026: Bechtel entered into a USD 4.69 billion lump-sum turnkey EPC contract with Sabine Pass Liquefaction Stage V, LLC (Cheniere Energy Partners, L.P.) for Phase 1 of the Sabine Pass Expansion Project in Louisiana, including Train 7 and a boil-off gas re-liquefaction unit. A limited notice to proceed was issued on May 22, 2026, shifting from planning into field-executable scope. The award highlights ongoing demand for mega-project EPC capacity and risk-bearing delivery models in large energy infrastructure.

- November 2025: HyperStrong International (Germany) GmbH partnered with LEAG Clean Power GmbH under an EPC contract to deliver a 1.6 GWh utility-scale BESS project in Germany. The project scale elevates storage from an ancillary add-on to a primary EPC scope, covering grid-connection, controls, and commissioning complexity. It also indicates that European utility-scale storage is increasingly being packaged through EPC structures rather than fragmented multi-vendor arrangements.

- January 2024: Microsoft signed a 500 MW nuclear offtake arrangement tied to long-tenor power procurement for large loads, reinforcing the role of corporate offtakers in shaping generation pipelines. For EPC contractors, these offtake structures support bankability for complex projects and can pull forward engineering and interconnection work. The arrangement also aligns with the broader move toward behind-the-meter and dedicated-supply solutions where grid queues are long.

Research Methodology Framework and Report Scope

Market Definition and Coverage

For this study, the market means revenue earned from engineering, procurement, and construction services delivered to power generation projects and to transmission and distribution build-outs, from design through commissioning.

Scope exclusions: We exclude pure operation and maintenance, standalone equipment manufacturing revenue, and owner-side internal project management that is not contracted as EPC.

Segmentation Overview

- Power Generation EPC

- By Technology

- Thermal

- Nuclear

- Renewables

- By Capacity Band

- Up to 100 MW (DER, micro-grid)

- 100 to 499 MW

- Above 500 MW

- By End-User

- Regulated Utilities

- Independent Power Producers

- Industrial Captive Power

- Public Sector and SOE

- By Geography

- North America

- Europe

- Asia-Pacific

- South America

- Middle East and Africa

- By Technology

- Power Transmission and Distribution (T&D) EPC

- By Geography

- North America

- Europe

- Asia-Pacific

- South America

- Middle East and Africa

- By Geography

Data Sources, Market Sizing, and Validation

Desk Research

Desk work was used to set the demand context and to keep the model tied to real build cycles. We referred to public energy and construction statistics and policy signals, such as IEA power investment and capacity data, IRENA renewable capacity additions, U.S. EIA generation and capacity series, World Bank infrastructure indicators, and UN Comtrade trade flows for power equipment.

We then connected those signals to EPC revenue formation using public project pipelines, utility and developer disclosures, and contractor annual reports and investor presentations. Academic and technical papers were checked for typical construction timelines, procurement splits, and commissioning patterns that affect revenue recognition. For company financials, we also used news, patent checks, and contract announcements, along with paid subscriptions for company intelligence and global contracts and tenders tracking. The sources named above are illustrative, and we also reviewed other public and paid references to collect data, validate assumptions, and clarify open questions.

Primary Interviews and Surveys

Primary work focused on validating how EPC value is booked across engineering, procurement, construction, and commissioning, and how scope changes show up in contract values. We spoke with EPC contractors, utilities and IPPs, equipment and balance-of-plant suppliers, and project consultants across APAC, EMEA, and the Americas, which helped us pressure-test pipeline conversion, typical cost splits, and pricing moves that were not clear from public disclosures alone.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 36% | CXOs: 12% | APAC: 47% |

| Mid tier: 48% | Functional/Unit leaders: 39% | EMEA: 29% |

| Smaller Players: 16% | Managers: 49% | Americas: 24% |

Market-Sizing & Forecasting

The main model uses a top-down and bottom-up approach, where installed and planned capacity additions, grid expansion needs, and project pipeline visibility are translated into addressable EPC spending by region and project type. In practice, we use inputs such as annual capacity additions by technology, transmission line and substation build programs, average EPC cost per MW, the typical procurement share inside EPC, and construction duration (which shifts revenue across years) to reconstruct yearly revenue.

To keep totals realistic, we corroborated model outputs with selective bottom-up checks, including sampling disclosed contract wins, typical project ticket sizes, and a supplier and contractor revenue sanity check by geography. Where contract values were not publicly disclosed, we used range-based assumptions from interviews and then narrowed them using comparable project benchmarks and local cost indices. For forecasting, scenario analysis was applied because policy, interest rates, and permitting timelines can shift project start dates, and then expert feedback was used to choose a base case with realistic conversion of announced projects into executed EPC work.

Data Validation & Update Cycle

Validation happens in layers so the story and the math stay aligned. We compare results with independent signals such as capacity commissioning trends, grid capex plans, tender intensity, and contractor backlog direction, and then investigate any large swings that do not match these checks.

Before sign-off, assumptions are reviewed by another analyst, followed by a final consistency pass across regions and sub-markets so totals reconcile. The report is refreshed annually, and interim updates are triggered when material events occur, such as major policy changes, large project cancellations, or sharp input cost moves. Right before delivery, we recheck key inputs and adjust the model if new public releases or interview feedback change the near-term outlook.

Mordor Intelligence's Power Engineering Procurement Construction Epc Market Size Compared With Other Published Estimates

Published numbers for power EPC can look far apart because firms do not always measure the same work, and they also choose different timing for revenue recognition and currency conversions. We keep the model readable by linking it to a small set of observable build indicators, and then cross-checking those totals with contract and backlog signals gathered in interviews.

Some published figures focus only on power plant EPC, and they also roll up different project stages into a single bucket. In Mordor Intelligence's model, transmission and distribution EPC is included alongside generation EPC, and pure O&M and equipment-only sales are kept out so totals reflect contracted EPC services only.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 1.43 T (2025) | |

| Global Consultancy A | USD 0.78 T (2025) | Often uses a narrower inclusion set that can undercount full EPC value in large projects, and assumptions for T&D and commissioning scope are not clearly separated from equipment spend. |

| Trade Journal B | USD 0.25 T (2024) | Typically tracks only power generation EPC and reflects a mix of announced and commissioned activity, which can shift the year and exclude grid build-outs that drive meaningful EPC revenue. |

The spread mainly comes from what is counted and the year it is tied to, not from arithmetic errors. When scope is kept consistent across generation and grid EPC and revenue timing is aligned to project execution, the market size becomes easier to reproduce and to use for planning.

Key Questions Answered in the Report

What is the forecast value of the Power EPC Market by 2031?

The Power EPC Market is projected to reach USD 2,120.01 billion by 2031, sustaining a 6.97% CAGR between 2026 and 2031.

Which technology leads current Power EPC spending?

Renewables account for 60% of 2025 generation EPC value and are growing at 7.8% annually through 2031.

Which region is growing fastest for Power Generation EPC contracts?

South America is the fastest-expanding region, advancing at a 7.5% CAGR on the back of Brazilian auctions and Chilean hydrogen projects.

Why are hyperscale data centers important to Power EPC growth?

Data centers bypass grid queues by funding on-site micro-grids, a segment that carries 12-15% EPC margins and is scaling rapidly.

What restrains faster Power EPC deployment in mature markets?

Extended permitting cycles, averaging 4.2 years in the United States, and talent shortages in HVDC and offshore wind delay project starts.

How concentrated is the competitive landscape?

Global market concentration sits at 3 on a 1-10 scale, with the ten largest contractors holding about 35-40% of total revenue but facing strong regional competition.

Page last updated on: