Methane Sulfonic Acid Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

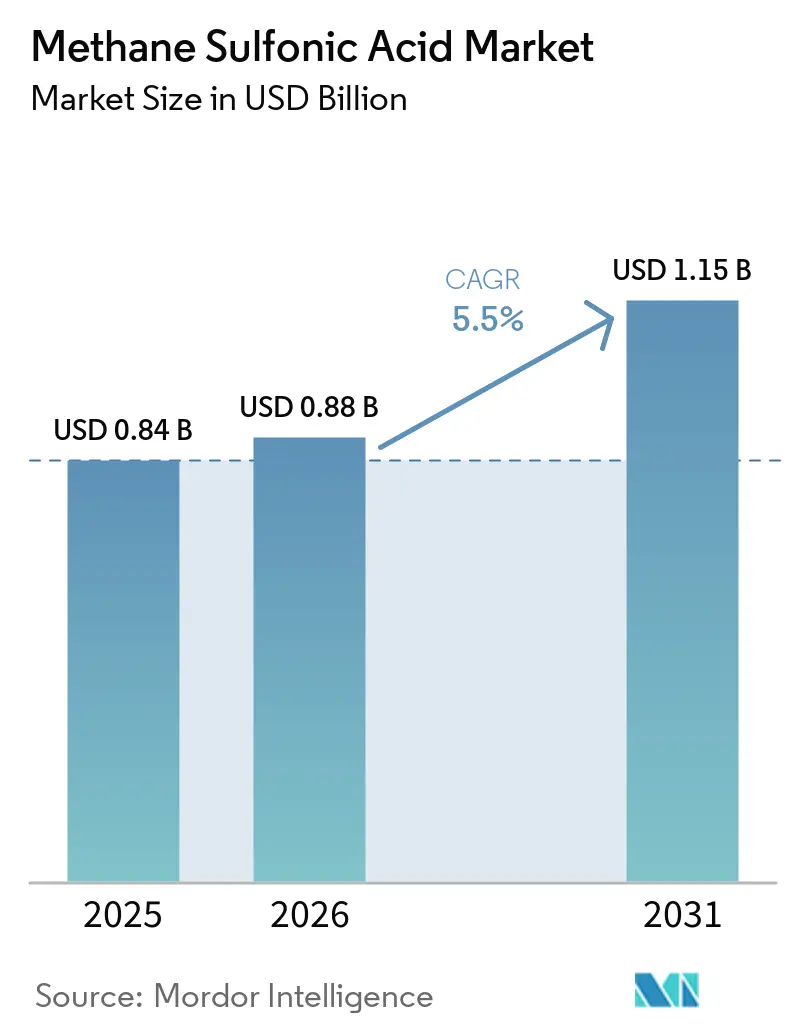

| Market Size (2026) | USD 0.88 Billion |

| Market Size (2031) | USD 1.15 Billion |

| Growth Rate (2026 - 2031) | 5.50% CAGR |

| Fastest Growing Market | Middle East and Africa |

| Largest Market | Asia-Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Methane Sulfonic Acid Market Analysis by Mordor Intelligence

The Methane Sulfonic Acid Market size is expected to grow from USD 0.84 billion in 2025 to USD 0.88 billion in 2026 and is forecast to reach USD 1.15 billion by 2031 at 5.5% CAGR over 2026-2031. Flow-battery electrolytes, peptide active pharmaceutical ingredient (API) synthesis and semiconductor plating are replacing legacy mineral acids because methanesulfonate salts deliver high metal solubility, low volatility and rapid biodegradability. Asia-Pacific holds more than half of global demand, fueled by Chinese electroplating clusters and India’s peptide manufacturing, while utility-scale batteries and green hydrogen projects accelerate uptake in North America and Europe. The Middle East and Africa lead future growth as petrochemical downstream integration and battery corridors emerge around the Gulf Cooperation Council. Producers differentiate through ultra-high-purity grades, technical service, and cradle-to-gate carbon footprints to justify premiums over sulfuric and p-toluenesulfonic acids.

Key Report Takeaways

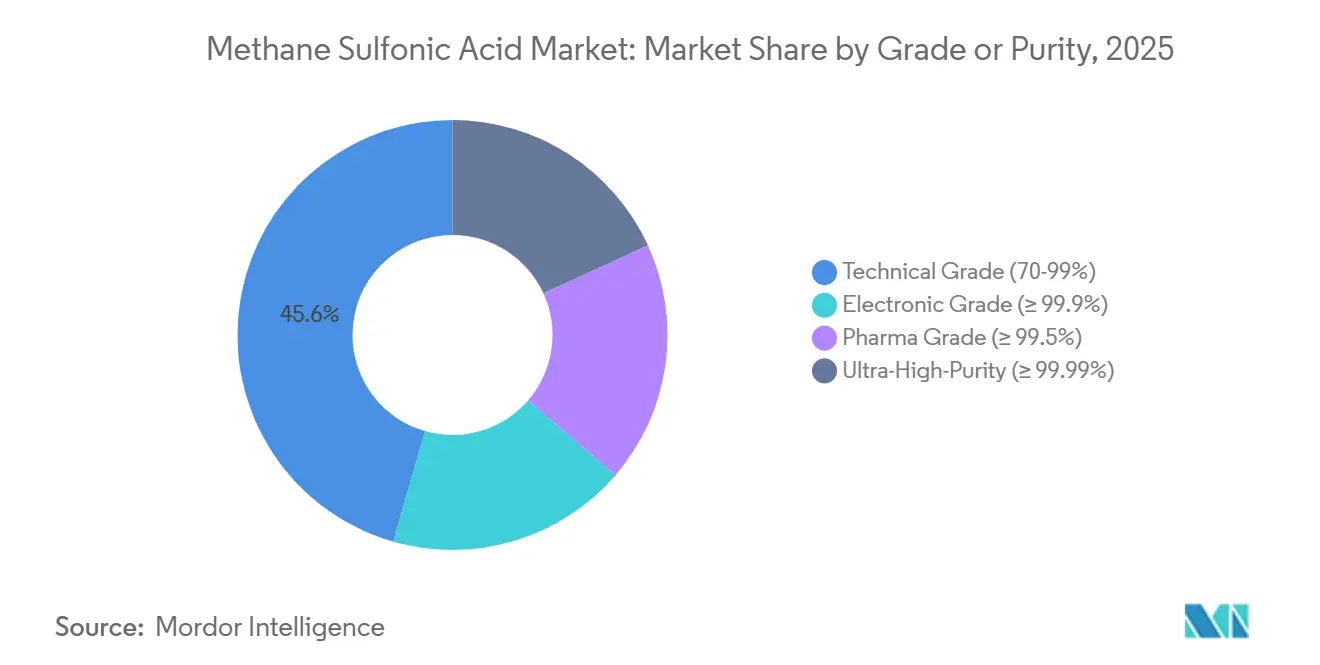

- By grade, technical grade captured 45.55% of 2025 revenue, and ultra-high-purity is advancing at a 6.56% CAGR through 2031.

- By form, Liquid held 82.43% of 2025 volume, whereas solid/flakes is forecast to expand at a 6.41% CAGR by 2031.

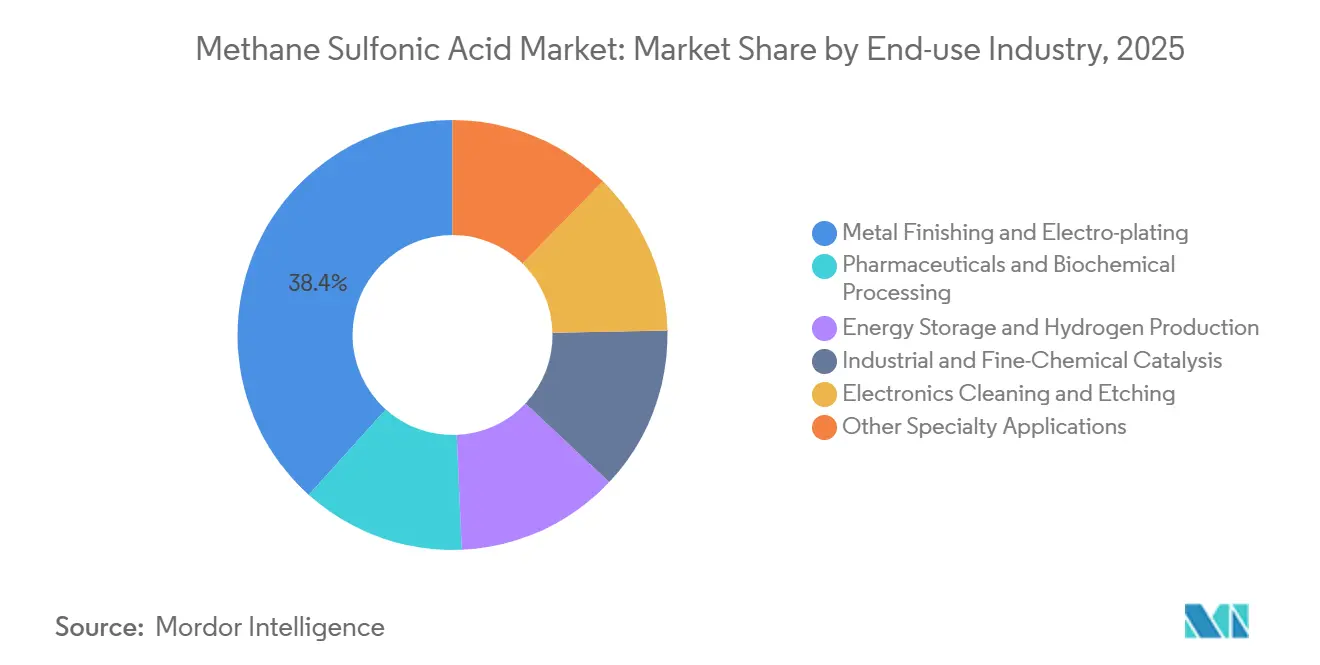

- By end-use, metal finishing commanded 38.35% of 2025 revenue, while energy storage and hydrogen production is rising at a 6.74% CAGR to 2031.

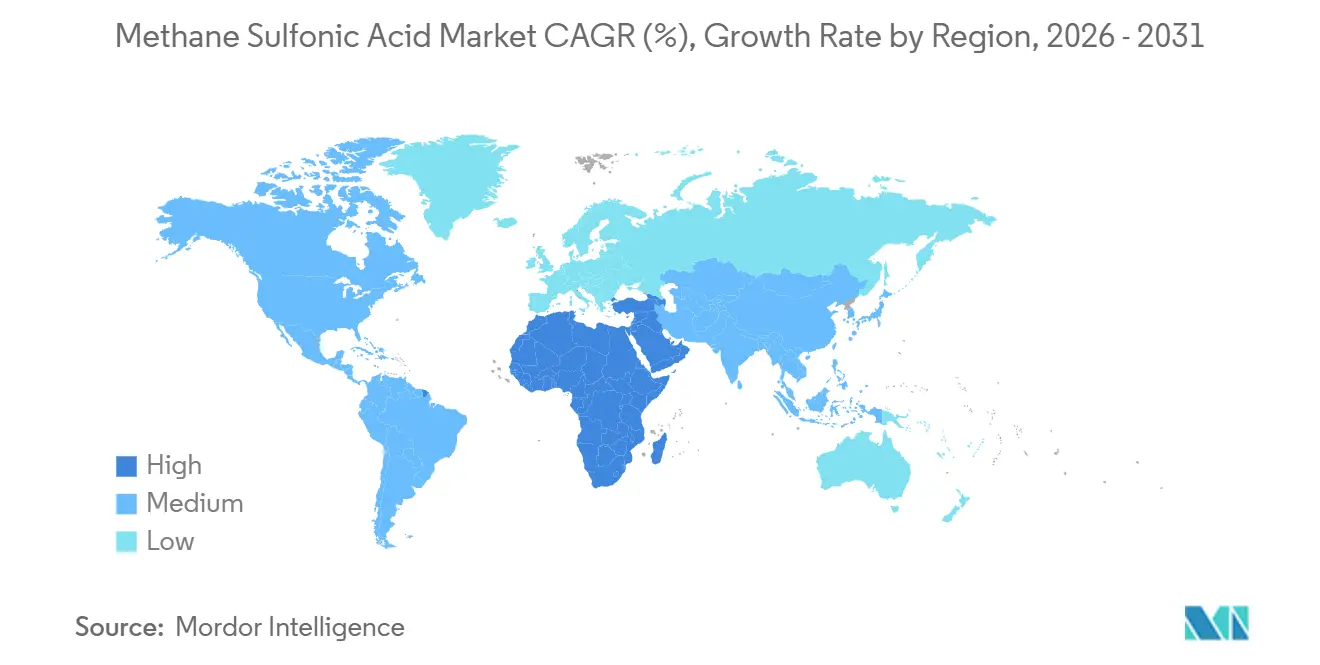

- By geography, Asia-Pacific led with 54.25% revenue share in 2025, yet Middle East and Africa is poised for a 6.66% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Methane Sulfonic Acid Market Trends and Insights

Driver Impact Analysis*

| Drivers | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growing demand in electro-plating and metal finishing | +1.2% | APAC core (China, Japan, South Korea), spill-over to North America automotive corridors | Medium term (2-4 years) |

| Expanding use in pharmaceutical and specialty synthesis | +0.9% | North America and EU pharmaceutical hubs, India API manufacturing clusters | Long term (≥4 years) |

| Adoption in flow-battery and hydrogen fuel-cell electrolytes | +1.5% | Global, with early concentration in China, EU, and North America grid-scale storage projects | Long term (≥4 years) |

| Catalyst role in biomass-derived fuel refining | +0.6% | North America, EU (cellulosic ethanol mandates), Brazil (sugarcane bagasse) | Long term (≥4 years) |

| Circular economy push for electrolyte recycling | +0.4% | EU (Circular Economy Action Plan), China (dual-carbon goals), selective North America utilities | Long term (≥4 years) |

| Source: Mordor Intelligence | |||

Growing Demand in Electroplating and Metal Finishing

Automotive lightweighting and electronics miniaturization lift tin and precious-metal plating volumes, and methanesulfonic acid baths deliver higher throwing power alongside lower hydrogen evolution than sulfuric systems. Printed-circuit board fabricators in Guangdong and Taiwan maintain fine-pitch deposits because methanesulfonate salts stay soluble at elevated tin concentrations, extending bath life. Tier-1 automotive suppliers coat aluminum battery enclosures to reach ISO 9227 salt-spray durability without chromate layers, and MSA’s non-oxidizing nature minimizes substrate attack. These performance gains reduce reject rates in volume production, broadening the methane sulfonic acid market across both decorative and functional coatings.

Expanding Use in Pharmaceutical and Specialty Synthesis

Peptide API producers have validated a PFAS-free global deprotection cocktail containing 2% methanesulfonic acid in formic acid, cutting strong-acid use 98% versus trifluoroacetic acid and yielding 99% cleavage for model sequences. Full-length tirzepatide achieved comparable purity to TFA workflows, positioning MSA for ton-scale GLP-1 agonist manufacture as global output climbs. Reversible formylation side reactions are cleared by mild ammonium hydroxide washes, and vacuum distillation recovers 88% of MSA for circular reuse, strengthening environmental and economic cases[1]Royal Society of Chemistry, Fidha et al., “PFAS-Free Peptide Deprotection Using MSA,” rsc.org.

Adoption in Flow-Battery and Hydrogen Fuel-Cell Electrolytes

Vanadium-cerium redox flow batteries using methanesulfonic acid deliver around 30% higher practical volumetric capacity and maintain near-100% coulombic efficiency over 100 cycles, while mixed-acid electrolytes reach 39.87 Wh/L energy density. Hydrocarbon sulfonic-acid ionomers in proton-exchange-membrane fuel cells reach mass activities of 180 A/g platinum and surpass perfluorosulfonic acid membranes in gas barrier performance, reducing PFAS exposure and stack degradation (ECS). These gains anchor the methane sulfonic acid market within long-duration storage and heavy-duty mobility

Catalyst Role in Biomass-Derived Fuel Refining

MSA selectively cleaves glycosidic bonds in lignocellulose, lowering char formation versus sulfuric acid and enabling catalyst recovery through methanesulfonate precipitation. U.S. Renewable Fuel Standard and EU biofuel mandates create a pull for higher yields and cleaner wastewater, where methanesulfonic acid’s biodegradability simplifies compliance. Process-intensified reactors shorten residence time, helping offset MSA’s price premium and supporting broader adoption in cellulosic ethanol and sugar-derived chemical plants[2]U.S. Department of Energy, “Cellulosic Ethanol Targets,” energy.gov.

Restraint Impact Analysis*

| Restraints | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Corrosiveness and occupational handling risks | -0.8% | Global, acute in regions with stringent OSHA/HSE enforcement (North America, EU) | Short term (≤2 years) |

| Price competition from sulfuric and p-toluenesulfonic acids | -1.1% | Global, most intense in cost-sensitive industrial cleaning and catalysis segments | Medium term (2-4 years) |

| Regulatory classification gaps for battery-grade MSA | -0.5% | North America, EU (IEC/ISO standards development lag commercial deployment) | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Corrosiveness and Occupational Handling Risks

MSA carries H314 hazard classification and requires acid-resistant gloves, goggles, and enclosed transfer systems. Standard stainless grades corrode above 80 °C, pushing users toward duplex steels or exotic alloys that raise capital outlays. Absence of substance-specific OSHA limits complicates compliance documentation, particularly for small platers and job shops that lack dedicated industrial hygiene staff.

Price Competition from Sulfuric and P-Toluenesulfonic Acids

Bulk sulfuric acid sells at USD 50-150/ton, and p-toluenesulfonic acid runs USD 1,500-2,500/ton, leaving MSA at a 10-40 times disadvantage absent lifecycle savings. Only applications requiring high metal-salt solubility, low oxidation potential, or reduced wastewater load can absorb the premium, restricting near-term substitution in commodity catalysis and cleaning.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Grade/Purity: Ultra-High-Purity Uptake in Advanced Electronics

Technical grade commanded 45.55% revenue in 2025 as legacy electroplating and cleaning continued to dominate volumes. Electronic and pharma grades together held around 35% share, serving PCB plating and peptide APIs that demand low chloride and transition-metal levels. Ultra-high-purity is projected to record the fastest advance at 6.56% CAGR because next-generation semiconductor nodes tighten contaminant limits to below 1 ppm for iron and copper. Supplier investments in distillation and ion-exchange polishing raise availability, enlarging the methane sulfonic acid market among fab operators.

Rising chip demand for artificial intelligence accelerators and automotive power modules boosts tin and tin-silver deposition, reinforcing pull for electronic-grade MSA. Pharma Grade receives additional lift as regulators tighten PFAS limits, encouraging manufacturers to switch from trifluoroacetic acid. Technical Grade faces margin pressure where sulfuric acid remains adequate, but hydrometallurgy and rare-earth recycling still value high metal-methanesulfonate solubility.

By Form: Solid/Flakes Benefit Pharmaceutical Logistics

Liquid presentations retained 82.43% of 2025 consumption owing to established pumping infrastructure in plating lines and battery plants. Still, solid/flakes are expected to grow 6.41% CAGR through 2031 as peptide houses favor reduced shipping mass and precise stoichiometry. Flakes melt near room temperature, lowering vapor exposure during weighing and easing compliance with hazardous-material codes.

Exporters from Europe to the Middle East cut freight cost 15-20% by eliminating dilution water, bolstering the methane sulfonic acid market size for solid form. Liquid grades, however, remain indispensable in high-throughput plating where automated dosing keeps tin concentration and free acid within narrow ranges. Dissolution time limits solid uptake in bulk industrial cleaning.

By End-use Industry: Energy Storage Surges

Metal Finishing led revenue at 38.35% in 2025, anchored by tin, zinc and precious-metal coatings on electronic connectors and EV battery housings. High throwing power and low hydrogen evolution deliver uniform films on high-aspect parts, sustaining demand in automotive and consumer electronics.

Energy storage and hydrogen production are forecast to be the fastest-growing segments at 6.74% CAGR, reflecting the scale-up of vanadium redox flow batteries and PFAS-free PEM fuel cells. A single 200 MWh installation can raise regional MSA demand by several thousand tons, and utility pipelines in China, California, and Germany suggest rising orders through the decade. Methane sulfonic acid market share in pharmaceuticals is also expanding as GLP-1 peptide capacity climbs, while biomass refining and electronics cleaning add incremental volume.

Geography Analysis

Asia-Pacific controlled 54.25% of 2025 revenue, led by Chinese electroplating hubs in Guangdong and Jiangsu, India’s peptide corridors around Hyderabad and Ahmedabad, and Korean semiconductor investments. China’s dual-carbon roadmap favors biodegradable specialty acids and closed-loop battery electrolytes, reinforcing structural demand.

North America accounted for significant market share in 2025, underpinned by Boston-area peptide CDMOs, Midwestern automotive platers and early flow-battery deployments in California and Texas. Hydrite Chemical’s USD 63 million plant in South Carolina, announced in 2026, promises local supply for Southeast vehicle and electronics clusters. Europe held roughly 18%, anchored by Germany’s chemical complex at Ludwigshafen and Scandinavia’s green hydrogen projects, while pharmaceutical hubs in France and Belgium adopt MSA to exit PFAS.

The Middle East and Africa is projected to clock the fastest regional CAGR at 6.66% as Saudi and Emirati downstream expansions integrate specialty acids into diversified petrochemical chains. Al-Jubail and Abu Dhabi investments improve feedstock security and draw plating and battery makers to the Gulf. South America’s 8% slice is stable, with Brazil’s sugarcane refineries using MSA in lignocellulosic pretreatment and Argentina piloting methanesulfonate-based lithium extraction.

Competitive Landscape

The methane sulfonic acid market is moderately consolidated. Arkema is steering half its research spend toward green mobility and electronics; its 2024 buyout of ionic-liquid specialist Proionic signals intent to widen electrolyte offerings. Regional Chinese firms such as Shandong Xinhua Pharma and Zibo DeHong Chemical price aggressively in technical grades but struggle to match impurity specs demanded by fabs and peptide API houses. North American distributors like Hydrite Chemical are moving into custom blending and just-in-time deliveries, serving fragmented job shops that larger producers overlook. Process analytics, including inline Raman and ion chromatography, now trim MSA consumption up to 15% per bath, giving service-oriented suppliers a value-added proposition.

White-space opportunities include bio-methane feedstocks that cut Scope 3 emissions, flow-chemistry deprotection platforms for continuous peptide synthesis, and battery-grade formulations for zinc-cerium and soluble-lead redox couples. Pilot electrolyzer projects demonstrate methanesulfonic acid recovery and rebatching, tightening producer–end user collaboration through closed-loop contracts and reinforcing the methane sulfonic acid market across energy, pharma, and electronics.

Methane Sulfonic Acid Industry Leaders

Arkema

BASF

Sipcam Oxon Spa

Shandong Xinhua Pharma

Varsal

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2025: Arkema's Thiochemicals business unit presented a comprehensive portfolio of high-performance intermediates and additives, including sulfonyls. Arkema offers the industry's most extensive range of sulfonyls, featuring methane sulfonic acid.

- June 2024: Sipcam Oxon Spa VAT, through its newly formed subsidiary Sipcam France SA, has completed the acquisition of all distribution assets of the French company Phyteurop SA. This move is anticipated to bolster Sipcam Oxon's presence in the methane sulfonic acid market by improving its distribution network and solidifying its foothold in the French market.

Global Methane Sulfonic Acid Market Report Scope

Methane sulfonic acid is a strong, biodegradable organic acid used as an eco-friendly catalyst in organic synthesis, electroplating, and industrial cleaning, offering a sustainable alternative to sulfuric or hydrochloric acid.

The methane sulfonic acid market is segmented by grade/purity, form, end-use industry, and geography. By grade/purity, the market is segmented into technical grade, electronic grade, pharma grade, and ultra-high-purity. By form, the market is segmented into liquid and solid/flakes. By end-use, the market is segmented into metal finishing and electroplating (precious-metal plating, printed-circuit-board plating, and automotive components), pharmaceuticals and biochemical processing, energy storage and hydrogen production (vanadium-redox flow batteries and PEM fuel cells), industrial and fine-chemical catalysis, electronics cleaning and etching, and other specialty applications. The report also covers the market size and forecasts for the methane sulfonic acid market in 16 countries across major regions. For each segment, the market sizing and forecasts have been done based on revenue (USD).

| Technical Grade (70-99%) |

| Electronic Grade (≥ 99.9%) |

| Pharma Grade (≥ 99.5%) |

| Ultra-High-Purity (≥ 99.99%) |

| Liquid |

| Solid/Flakes |

| Metal Finishing and Electro-plating | Precious-metal plating |

| Printed-circuit-board plating | |

| Automotive components | |

| Pharmaceuticals and Biochemical Processing | |

| Energy Storage and Hydrogen Production | Vanadium-redox flow batteries |

| PEM fuel cells | |

| Industrial and Fine-Chemical Catalysis | |

| Electronics Cleaning and Etching | |

| Other Specialty Applications |

| North America | United States |

| Canada | |

| Mexico | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Russia | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle-East and Africa | United Arab Emirates |

| Saudi Arabia | |

| Rest of Middle-East and Africa |

| By Grade/Purity | Technical Grade (70-99%) | |

| Electronic Grade (≥ 99.9%) | ||

| Pharma Grade (≥ 99.5%) | ||

| Ultra-High-Purity (≥ 99.99%) | ||

| By Form | Liquid | |

| Solid/Flakes | ||

| By End-use Industry | Metal Finishing and Electro-plating | Precious-metal plating |

| Printed-circuit-board plating | ||

| Automotive components | ||

| Pharmaceuticals and Biochemical Processing | ||

| Energy Storage and Hydrogen Production | Vanadium-redox flow batteries | |

| PEM fuel cells | ||

| Industrial and Fine-Chemical Catalysis | ||

| Electronics Cleaning and Etching | ||

| Other Specialty Applications | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle-East and Africa | United Arab Emirates | |

| Saudi Arabia | ||

| Rest of Middle-East and Africa | ||

Key Questions Answered in the Report

What will be the market size for methane sulfonic acid by 2031?

By 2031, the methane sulfonic acid will value USD 1.15 billion, growing with a CAGR of 5.50% during 2026-2031.

What are methane sulfonic acid advantages over sulfuric acid in plating?

Higher throwing power, minimal hydrogen evolution and lower wastewater load reduce reject rates and treatment cost.

What is expected demand growth for battery-grade methane sulfonic acid

The energy-storage segment is set to post a 6.74% CAGR to 2031 as flow batteries and PFAS-free fuel cells commercialize.

Which is a key region driving methane sulfonic acid adoption

Asia-Pacific held 54.25% of 2025 revenue, supported by Chinese plating and Indian peptide manufacturing clusters.

What are the typical materials of construction for MSA handling?

Duplex stainless, Hastelloy, and lined carbon steel provide corrosion resistance above 80 °C service temperatures.

What is outlook for ultra-high-purity grade supply?

Capacity additions at BASF and other majors support a 6.56% CAGR through 2031 to meet advanced semiconductor demand.

Page last updated on: