Amphoteric Surfactant Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 3.87 Billion |

| Market Size (2031) | USD 4.73 Billion |

| Growth Rate (2026 - 2031) | 4.08% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Amphoteric Surfactant Market Analysis by Mordor Intelligence

The Amphoteric Surfactant market size is expected to grow from USD 3.72 billion in 2025 to USD 3.87 billion in 2026 and is forecast to reach USD 4.73 billion by 2031 at 4.08% CAGR over 2026-2031. Steady expansion rests on the dual-charge chemistry of amphoteric molecules, which supports broad pH stability, synergizes with anionic and cationic ingredients, and allows formulators to reduce overall surfactant loads without sacrificing performance. Rising regulatory scrutiny has elevated biodegradability and toxicity compliance to board-level priorities, steering procurement toward bio-based supply chains and boosting innovation in fermentation-derived betaines and rhamnolipids. Asia-Pacific contributes the highest consumption volume, with continued investment in large-scale plants across China, Japan, and India that capitalize on proximity to oleochemical feedstocks and fast-growing personal-care markets. Parallel momentum is visible in oilfield chemicals, where amphoteric surfactants lower interfacial tension in harsh reservoir environments, supporting energy-sector resilience amid increasingly complex drilling programs. As end users pivot away from per- and polyfluoroalkyl substances (PFAS)-laden foams and high-sulfate blends, amphoteric variants are positioned as compliance-ready backbones for next-generation detergents, agrochemicals, and institutional cleaners.

Key Report Takeaways

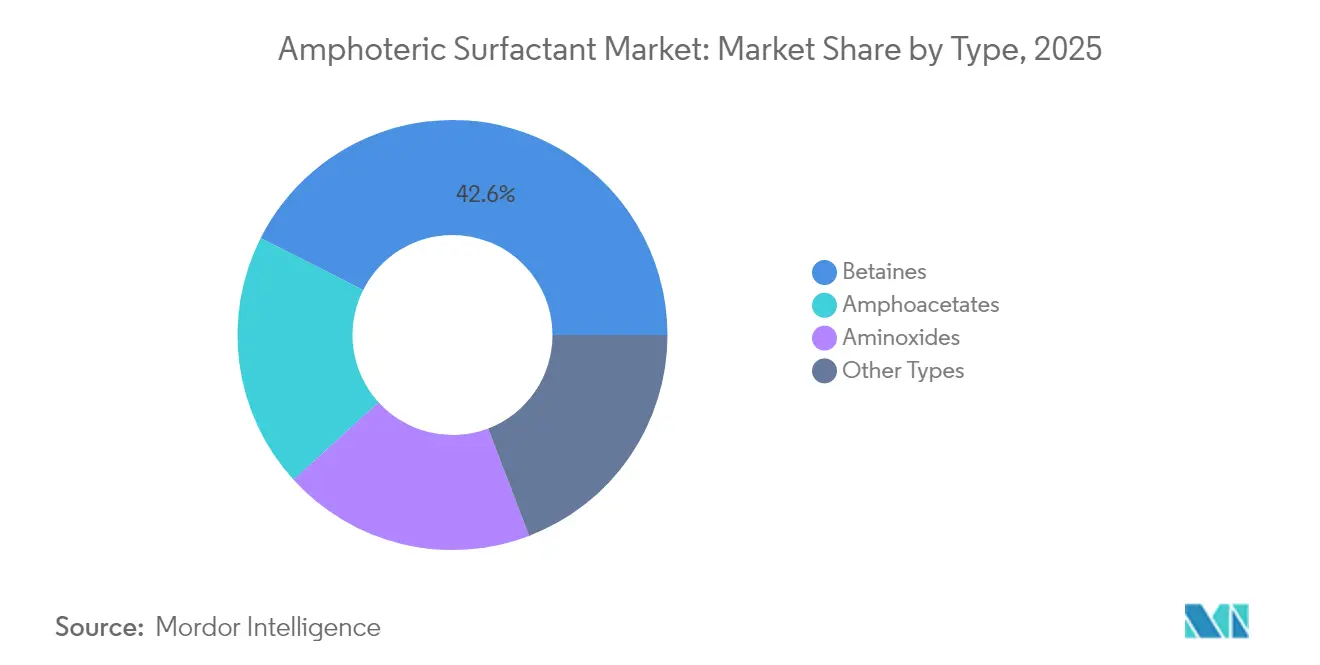

- By type, betaines led with 42.55% of the Amphoteric Surfactant market share in 2025, while amphoacetates are forecast to grow at a 4.92% CAGR through 2031.

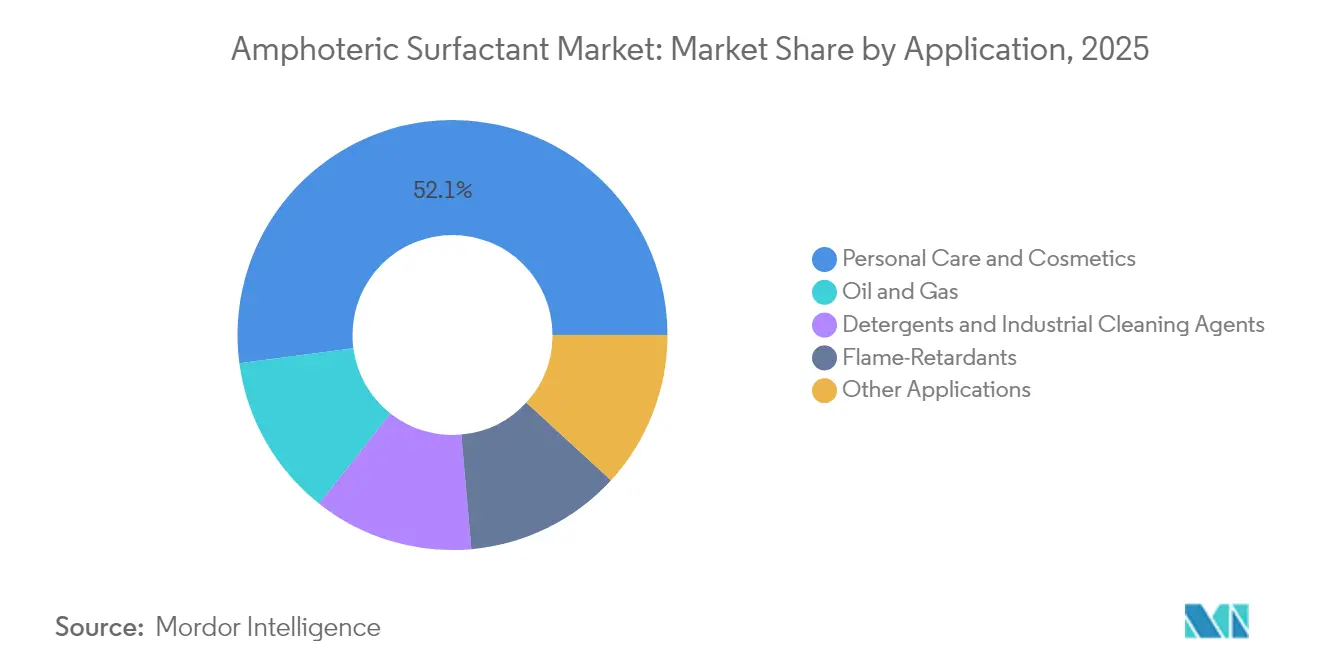

- By application, personal care and cosmetics accounted for 52.10% of the Amphoteric Surfactant market size in 2025; the oil and gas segment is advancing at a 5.01% CAGR through 2031.

- By origin, synthetic variants held 70.60% share of the Amphoteric Surfactant market size in 2025, whereas bio-based alternatives are expanding at a 5.12% CAGR to 2031.

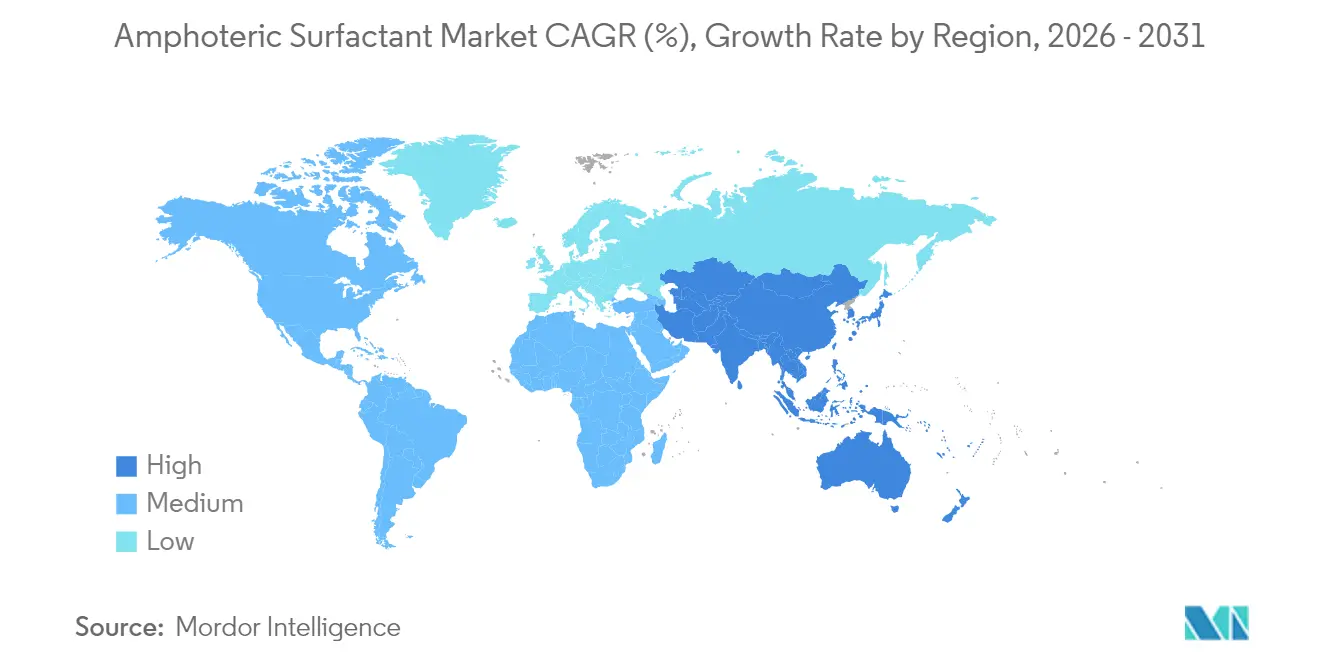

- By geography, Asia-Pacific dominated with a 41.10% share of the Amphoteric Surfactants market size in 2025 and is expected to log a 4.88% CAGR during the forecast horizon.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Amphoteric Surfactant Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growing Demand from Personal Care and Cosmetics | +1.2% | Global, with concentration in APAC and North America | Medium term (2-4 years) |

| Shift Toward Bio-based and Sulfate-free Formulations | +0.9% | North America & EU, expanding to APAC | Long term (≥ 4 years) |

| Expansion of Industrial and Institutional Cleaning Sector | +0.8% | Global, post-COVID recovery driven | Short term (≤ 2 years) |

| Growing Utilization as an Adjuvant in Pesticide Formulations | +0.5% | APAC core, spill-over to Latin America | Medium term (2-4 years) |

| PFAS-free High-performance Firefighting Foams Requiring Amphoteric Blends | +0.6% | North America & EU, with regulatory spillover globally | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Growing Demand from Personal Care and Cosmetics

Premium skin-cleansing lines now require ultra-mild surfactant systems that pair strong foaming with low irritation potential, and amphoteric chemistries satisfy both checkpoints. BASF’s Dehyton PK45 GA/RA, sourced from Rainforest Alliance-certified coconut oil, exemplifies how traceability and performance converge in brand storytelling [1]“Dehyton PK45 GA/RA Launches at in-cosmetics Global,” BASF, basf.com. Global bar-soap consumption is declining, but liquid formats, micellar waters, and scalp scrubs are rising, each leveraging betaines as viscosity builders and foam stabilizers. Emerging middle-class consumers in India, Indonesia, and Vietnam are upgrading to sulfate-free shampoos, adding volume to the amphoteric surfactants market. Regulatory convergence, such as Japan’s quasi-drug alignment on maximum allowable nitrogen content, reduces formulation redundancy and speeds regional launch cycles. Ingredient-transparency apps compel marketers to replace Drug Enforcement Administration (DEA)-derived amphoterics with Roundtable on Sustainable Palm Oil (RSPO)-certified, 1,4-dioxane-free variants, reinforcing demand diversity across mid-price and prestige tiers.

Shift Toward Bio-based and Sulfate-free Formulations

Locus Ingredients secured Environmental Protection Agency (EPA)-TSCA (Toxic Substances Control Act) registration for its sophorolipid portfolio, demonstrating commercial-scale fermentation at International Organization for Standardization (ISO)-certified Ohio facilities. This milestone legitimizes home-grown biosurfactants in a space dominated by Asian oleochemical supply. BASF’s EcoBalanced approach, verified under REDcert², swaps fossil carbon for waste-based feedstocks without changing International Nomenclature of Cosmetic Ingredients (INCI) names, giving brand owners a drop-in route to Scope 3 reduction. European Union (EU) detergent revisions now mandate digital product passports, allowing end users to trace carbon intensity to the batch level, an incentive that heightens competitive stakes among suppliers. Evonik’s first rhamnolipid plant in Slovenská Ľupča leverages European corn glucose, cutting dependence on palm derivatives and avoiding deforestation risks. Economies of scale are narrowing the price delta between synthetic and bio-based amphoterics, and life-cycle-assessment data reveal double-digit reductions in global-warming potential, tipping purchasing decisions in favor of bio-routes.

Expansion of Industrial and Institutional Cleaning Sector

Tighter disinfection requirements in airports, schools, and food-processing plants have moved amphoteric surfactants from “nice-to-have” to core ingredient status in multi-surface cleaners. Plant-derived betaines formulated at neutral pH show fungicidal boosts when paired with quaternary ammonium compounds, reducing overall active-load thresholds and decreasing worker exposure. European Biocide Regulation tiers raise the cost of re-registering legacy solvent systems, pushing contract formulators toward amphoteric solutions that already possess favorable ecolabel dossiers. The cleaning market’s shift from powder to liquid concentrates and on-site dilution stations increases the need for stable surfactants under varied water hardness and temperature. Facility managers rely on automatic dosing compressors, demanding consistent viscosity; amphoteric blends help maintain Newtonian flow at low shear. Corporate procurement policies now include cradle-to-gate greenhouse-gas scoring, and bio-based amphoterics cut Scope 1 data by double-digit percentages, strengthening their value proposition in tender bids.

Growing Utilization as an Adjuvant in Pesticide Formulations

Farm-gate economics favor adjuvants that improve spray efficiency, and amphoteric molecules excel by modulating charge as tank-mix pH shifts, ensuring active ingredients adhere to hydrophobic leaf cuticles. Under precision-farming regimes, every droplet counts, and amphoteric adjuvants curb drift by tightening droplet-size distribution while lowering dynamic surface tension. Trials at the University of Georgia show yield improvements in greenhouse peppers when herbicides are paired with amphoteric surfactants that penetrate waxy layers at lower application rates. Latin American soybean growers increasingly adopt these systems to boost glyphosate efficacy against resistant weeds, creating a sizeable regional pull. Regulatory bodies prefer adjuvants with rapid biodegradation profiles; amphoterics meet Organization for Economic Cooperation and Development (OECD) 301 standards, easing dossier compilation. As global acreage for high-value crops expands, agro-input players integrate tailor-made amphoterics into one-pack solutions that simplify farmer handling and storage.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Stringent Environmental and Tox-substance Regulations | -0.7% | Global, with EU and North America leading | Long term (≥ 4 years) |

| Volatility in Fatty Alcohol and Petro Feedstock Prices | -0.5% | Global, with higher impact in cost-sensitive markets | Short term (≤ 2 years) |

| Enzyme-based Cleaners Cannibalising Surfactant Volumes | -0.4% | North America & EU, with gradual APAC adoption | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Stringent Environmental and Tox-substance Regulations

The European Chemicals Strategy for Sustainability introduces a Generic Risk Assessment model that may classify entire surfactant families as substances of concern if aquatic-tox or endocrine-disruption flags rise, irrespective of actual exposure scenarios. US EPA strengthens Significant New Use Rules (SNUR) review timelines under Toxic Substances Control Act (TSCA), raising pre-manufacture notification costs, particularly for novel amphoacetates lacking read-across data [2]“TSCA New Chemical Review Statistics,” United States Environmental Protection Agency, epa.gov. China’s detergent standard GB/T 42072 -2022 now requires 90% biodegradation within 28 days, forcing testing expenditures that lengthen time-to-market for small producers. Fragmented definitions of “natural” across ASEAN jurisdictions demand multiple eco-cert audits, siphoning research and development (R&D) budgets into compliance rather than application development. As regulators pivot toward hazard-based rules, formulators hedge by adopting by-product-free synthetic routes, but the capex burden narrows margins, tempering the overall amphoteric surfactants market growth trajectory.

Volatility in Fatty Alcohol and Petro Feedstock Prices

Palm-kernel-oil futures climbed nearly 30% in 2024 after weather-linked yield declines in Malaysia, while coconut-oil output faced shipping bottlenecks in the Philippines, jointly inflating lauryl betaine costs. Simultaneously, n-dodecylamine prices tracked crude-oil spikes following geopolitical flare-ups in the Middle East, constraining cash flow for contract manufacturers tied to fixed-price agreements. Stepan Company reported a year-end gross-margin squeeze despite revenue upticks, attributing the erosion to freight surcharges and tight fatty-alcohol supply. These oscillations complicate production-planning algorithms and limit long-term contracting visibility. The bio-based hedge introduces its volatility, maize-derived glucose correlates with ethanol demand, making dual-feedstock strategies essential yet capital-intensive. Consequently, mid-tier formulators lacking integrated upstream assets experience the sharpest EBITDA impact, dampening their ability to scale with demand surges in the amphoteric surfactants market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Type: Performance-driven Shifts within a Mature Mix

Betaines anchored 42.55% of the Amphoteric Surfactant market share in 2025 and continued to post stable single-digit volume gains during 2025. Consumer trust in cocamidopropyl betaine’s mildness and well-documented toxicology history underpins its popularity in shampoos, facial washes, and baby cleansers. The Amphoteric Surfactant market size attached to betaines has broadened beyond toiletries, with foam-firefighting foams and oilfield friction-reducers relying on their zwitterionic nature for viscosity control. Pipeline operators appreciate betaine additives because they remain effective even when salt concentrations fluctuate across the wellbore, reducing downtime for additive recalibration.

Amphoteric amidopropyl hydroxysultaines address stringent viscosity demands in professional kitchen degreasers, preserving gel structure across temperature swings. Aminoxides, though niche, provide oxidative stability in chlorine-enhanced cleaners used in dairy and brewery sanitation lines, carving a resilient revenue stream shielded from retail-price pressures. Innovators like Daicel blend polyglycerin backbones with amphoteric heads to create transparent, low-foam surfactants tailored for water-based metal-working fluids, opening fresh industrial corridors. These developments suggest that the amphoteric surfactants market will increasingly segment along functionality rather than raw molecule class, with tailored derivatives carrying premium price tags.

By Origin: Bio-based Adoption Gains Structural Momentum

Synthetic variants delivered 70.60% of the Amphoteric Surfactant market size in 2025, anchored by cost-efficient refinery streams producing fatty-amine and chloroacetic acid intermediates. Established global networks ensure consistent specification and facilitate multi-year procurement contracts critical for large fast-moving consumer goods (FMCG) rollouts. Yet, bio-based alternatives, growing at 5.12% CAGR, are pushing into mainstream status as carbon-pricing schemes raise the true cost of fossil-sourced chemicals. Evonik’s Slovakian rhamnolipid plant validates fermentation economics on European soil, shifting the risk calculus for multinationals debating import-versus-local sourcing.

Supply-chain resilience arguments also favor diversified feedstocks: if palm plantations encounter El Niño-linked stress, synthetic routes using ethylene oxide back integrate to shale gas streams, bridging supply gaps. Conversely, when crude spikes, sugar-cane-derived surfactants insulate finished-goods margins. Brand owners use on-pack QR codes to showcase cradle-to-gate CO₂ savings of bio-routes, reinforcing consumer perception and encouraging repeat purchase. Over the forecast horizon, analysts expect the amphoteric surfactants market to operate a dual-feedstock model, where procurement will balance cost and carbon attributes quarter-by-quarter.

By Application: Consumer Staples Remain Core as Oilfield Demand Accelerates

Personal-care accounted for 52.10% of the Amphoteric Surfactant market size in 2025, anchored by the unstoppable rise of liquid formats. The ever-tightening irritancy benchmarks for leave-on products keep amphoteric surfactants in the reformulation spotlight because they enable sulfate-free claims while sustaining dense, elastic foam. E-commerce has amplified ingredient transparency, and influencer culture now scrutinizes every INCI deck, pressuring brands to adopt multifunctional amphoterics that reduce total component count and simplify clean-beauty narratives. Regional players in Indonesia and Brazil are adding coconut-sourced betaines to prestige hair-care lines to claim both natural origin and performance parity with imported brands, supporting volume uplift in emerging economies.

Oil and gas posted the fastest 5.01% CAGR, energized by national oil companies stepping up enhanced-oil-recovery projects to meet energy-security objectives. Lab findings published in Nature reported ultra-low interfacial tension down to 10⁻³ m N/m when amphoteric–anionic blends were injected into tight carbonate reservoirs, boosting displacement efficiency beyond 15% over waterflood baselines. Downstream, flame-retardant firefighting foams shift away from per- and polyfluoroalkyl substances (PFAS) and adopt amphoteric foam boosters that remain fluid at sub-zero runway conditions, a vital requirement for NORDIC and Canadian airports. Institutional cleaning, though mature, benefits from global pathogen-awareness that sustains higher cleaning frequencies and drives demand for low-rinse amphoterics compatible with electrostatic sprayers used in hospitals.

Geography Analysis

Asia-Pacific delivered 41.10% of the Amphoteric Surfactants market share in 2025 and is expected to advance at a 4.88% CAGR to 2031, buoyed by domestic downstream demand and aggressive capacity build-outs in Jiangsu, Maharashtra, and Chiba clusters. Local governments support bio-route expansions through soft-loan programs and expedited permitting for projects that displace petrochemical imports. High urbanization rates translate into sustained growth for liquid cleansers and hand hygiene products, which lift discretionary spending on mild amphoteric systems. Indian personal-care startups source semi-refined coconut-oil betaines directly from southern plantations, trimming logistics costs and reinforcing supply-chain transparency.

North America’s Amphoteric Surfactants market exhibits maturity yet continues to push the innovation envelope. EPA-certified sophorolipid lines enter mass-market household-cleaning aisles, signaling bio-based viability at scale. The United States oilfield chemical suppliers integrate amphoteric friction reducers to maintain drilling efficiency in shale operations characterized by variable salinity and temperature. The region also acts as a patent hotbed for multifunctional blends that marry amphoteric backbones with cationic polymers to form hybrid conditioning agents for hair-care lines positioned at premium price points.

Europe remains at the forefront of regulatory sculpting and life-cycle transparency, making the region an incubator for high-purity grades. REACH registration portfolios increasingly include amphoteric-based “drop-in” replacements for legacy ethoxylated amines, reflecting tighter chronic-toxicity thresholds]. Detergent brands advertise 100% renewable-carbon surfactant systems, capitalizing on the EU digital product passport that communicates cradle-to-grave environmental metrics to consumers with smartphone scans. Eastern European facilities supply Western brand owners under tolling agreements, offsetting higher energy costs through proximity to sugar-beet feedstocks used in biotechnological routes.

South America and the Middle East & Africa represent fast-emerging but fragmented demand pockets. Brazilian soy growers adopt amphoteric adjuvants in line with sustainable-farming certification, while Gulf Cooperation Council (GCC) countries leverage desalination plants’ brine streams to produce feedstocks for betaine synthesis, reducing dependence on imported raw materials. Although absolute volume remains modest, high growth rates mean these regions will contribute incremental tonnage that sustains global demand equilibrium.

Competitive Landscape

The Amphoteric Surfactant market is moderately consolidated with major players, such as BASF, Evonik Industries AG, Clariant, Croda International Plc, and Kao Corporation. BASF expands its EcoBalanced portfolio alongside renewed supply deals with multinational personal-care brands, enabling it to lock in long-term contracts for bio-based grades. Evonik’s Slovakian fermentation hub reflects its strategy to align specialty chemicals with circular-economy objectives, offering European customers short supply lines and a reduced carbon footprint. Mid-tier firms like Aarti Surfactants and Enaspol pursue regional nimbleness, providing custom toll-blending and quicker sample-turnaround times, a service advantage when global majors prioritize volume orders. Supply-chain security remains a strategic imperative. Major players integrate backward into fatty-alcohol production or sign long-term sugar contracts to hedge price volatility.

Amphoteric Surfactant Industry Leaders

Clariant

Kao Corporation

Evonik Industries AG

Croda International Plc

BASF

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2025: BASF launched natural-based innovations, including Dehyton PK45 GA/RA amphoteric surfactant derived from Rainforest Alliance Certified coconut oil, at in-cosmetics Global 2025. The product targets sustainable personal care formulations with foaming properties and biodegradability.

- August 2022: Kensing, LLC, announced a definitive agreement to acquire the Hopewell, Virginia, amphoteric surfactants and specialty esters manufacturing business from Evonik Industries AG. The business primarily serves the personal care market, focusing on skin, hair, and oral care applications.

Global Amphoteric Surfactant Market Report Scope

Amphoteric surfactant refers to the surfactant that has both anionic and cationic hydrophilic groups and a structure that contains hermaphroditic ions that can form cation or anion depending on the ambient conditions such as pH changes. The amphoteric surfactant market is segmented by type, application, and geography. By type, the market is segmented into betaines, amphoacetates, aminoxides, and other types. By application, the market is segmented into personal care and cosmetics, detergents and industrial cleaning agents, oil and gas, flame retardants, and other applications. The report also covers the market size and forecasts for the Amphoteric Surfactant Market in 15 countries across major regions. For each segment, the market sizing and forecasts have been done on the basis of value (USD Million).

| Betaines |

| Amphoacetates |

| Aminoxides |

| Other Types (Imidazoline-based Amphoterics, etc.) |

| Personal Care and Cosmetics |

| Detergents and Industrial Cleaning Agents |

| Oil and Gas |

| Flame-Retardants |

| Other Applications (Agricultural Chemicals and Adjuvants, etc.) |

| Synthetic |

| Bio-based / Natural |

| Asia-Pacific | China |

| Japan | |

| India | |

| South Korea | |

| ASEAN Countries | |

| Rest of Asia-Pacific | |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Russia | |

| NORDIC Countries | |

| Rest of Europe | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Middle East and Africa | Saudi Arabia |

| South Africa | |

| Rest of Middle East and Africa |

| By Type | Betaines | |

| Amphoacetates | ||

| Aminoxides | ||

| Other Types (Imidazoline-based Amphoterics, etc.) | ||

| By Application | Personal Care and Cosmetics | |

| Detergents and Industrial Cleaning Agents | ||

| Oil and Gas | ||

| Flame-Retardants | ||

| Other Applications (Agricultural Chemicals and Adjuvants, etc.) | ||

| By Origin | Synthetic | |

| Bio-based / Natural | ||

| By Geography | Asia-Pacific | China |

| Japan | ||

| India | ||

| South Korea | ||

| ASEAN Countries | ||

| Rest of Asia-Pacific | ||

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Russia | ||

| NORDIC Countries | ||

| Rest of Europe | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Middle East and Africa | Saudi Arabia | |

| South Africa | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

What is the current size of the Amphoteric Surfactant market?

The Amphoteric Surfactant market size is valued at USD 3.87 Billion in 2026 and is projected to reach USD 4.73 Billion by 2031.

Which region leads global consumption of amphoteric surfactants?

Asia-Pacific holds the top position with a 41.10% share in 2025 and is forecast to grow at a 4.88% CAGR through 2031.

Why are betaines important in personal-care formulations?

Betaines combine mildness, foam stability, and broad regulatory acceptance, giving them 42.55% of amphoteric surfactants market share in 2025.

How fast are bio-based amphoteric surfactants growing?

Bio-based variants are advancing at a 5.12% CAGR to 2031 as brands and regulators favor renewable raw materials.

Which application segment is expanding the quickest?

Oil and gas applications lead growth with a 5.01% CAGR, driven by enhanced-oil-recovery projects that need pH-adaptive surfactants.

Page last updated on: