SME Lending Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 13.34 Trillion |

| Market Size (2031) | USD 16.71 Trillion |

| Growth Rate (2026 - 2031) | 4.61% CAGR |

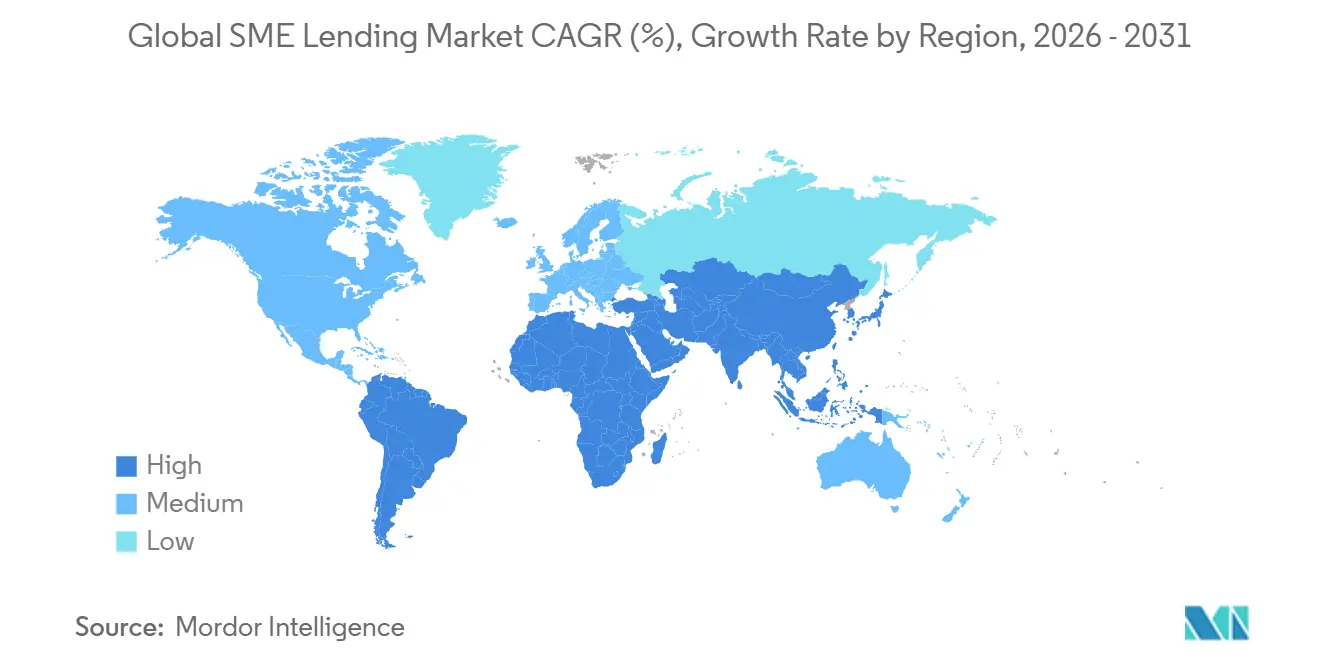

| Fastest Growing Market | Asia-Pacific |

| Largest Market | Asia-Pacific |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

SME Lending Market Analysis by Mordor Intelligence

The SME Lending Market size is expected to grow from USD 12.82 trillion in 2025 to USD 13.34 trillion in 2026 and is forecast to reach USD 16.71 trillion by 2031 at 4.61% CAGR over 2026-2031.

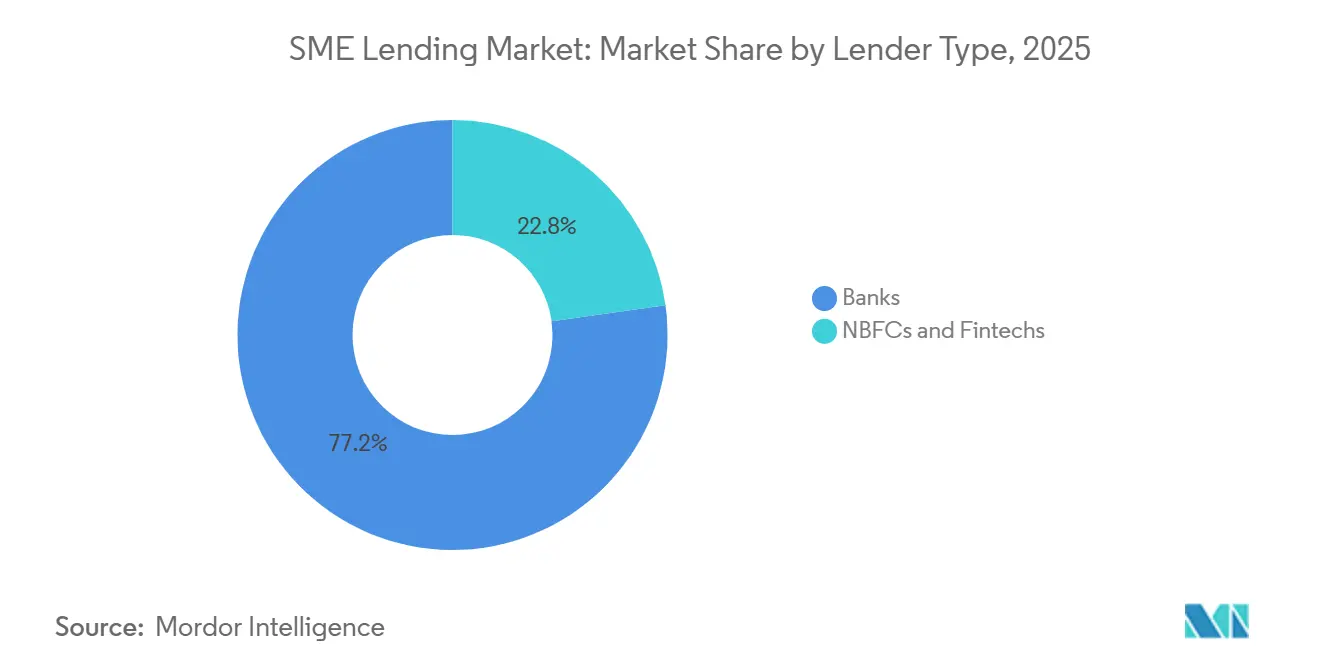

The SME lending market is moving away from branch-led, collateral-heavy processes toward data-led, multi-channel origination, helping lenders convert unmet demand into active loan books faster. Banks still accounted for the core of the SME lending market in 2025, with 77.21% of total volumes, but the faster expansion of NBFCs and fintechs suggests that origination speed, workflow integration, and credit analytics are becoming increasingly important for future competition. Product mix in the SME lending market also reflects near-term operating pressure on businesses, with working capital loans holding 42.97% of originations in 2025 and short-term credit rising as invoice finance and revolving facilities spread across more lender channels. Asia-Pacific led the SME lending market with 43.23% of global volumes in 2025 and is also the fastest-growing regional block, pointing to the combined effects of scale, digital financial infrastructure, and policy-backed credit support. The main brake on the SME lending market remains the aftereffect of tighter rate cycles, as OECD economies saw the stock of SME loans fall by 4.7% in 2023, and restrictive credit conditions persisted through 2025.

Key Report Takeaways

- By lender type, banks held 77.21% of total lending volume in the SME lending market share in 2025, while NBFCs and fintechs are projected to grow at 9.02% CAGR through 2031.

- By loan type, working capital loans accounted for 42.97% of total originations in the SME lending market share in 2025, while invoice financing is projected to grow at an 8.29% CAGR through 2031.

- By collateral, secured lending accounted for 64.07% of total volume in the SME lending market share in 2025, while unsecured lending is projected to grow at 7.13% CAGR through 2031.

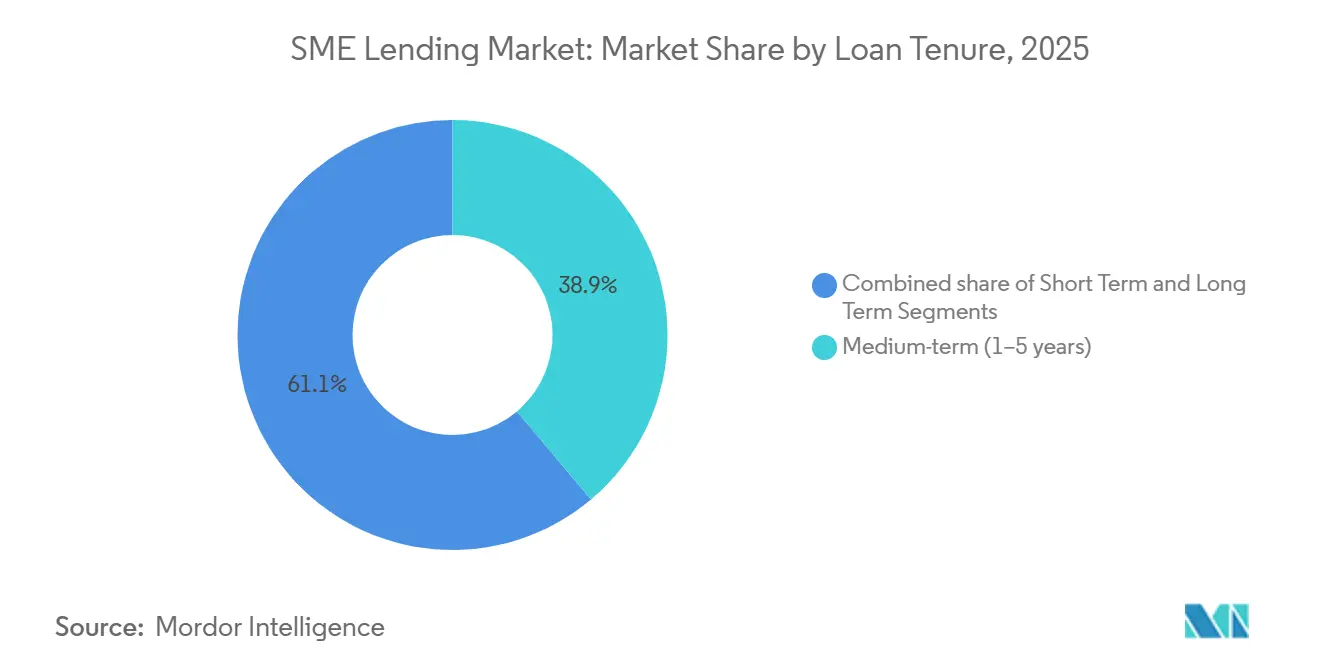

- By loan tenure, medium-term loans held a 38.86% of the SME lending market share in 2025, while short-term loans are projected to grow at a 5.86% CAGR through 2031.

- By borrower size, small enterprises accounted for 36.67% of lending volumes in the SME lending market share in 2025, while micro enterprises are projected to grow at 7.21% CAGR through 2031.

- By geography, Asia-Pacific captured 43.23% of global volume in the SME lending market share in 2025, while the region is projected to grow at 5.74% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global SME Lending Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Digitization of SME underwriting and loan origination | +1.2% | Global, concentrated gains in Asia-Pacific and North America | Short term (≤ 2 years) |

| Rising working capital demand from volatile cash conversion cycles | +0.9% | Asia-Pacific core, spill-over to the Middle East and Africa, and South America | Medium term (2-4 years) |

| Growth of non-bank and embedded finance channels | +0.8% | North America and Europe, expanding into the Asia-Pacific | Medium term (2-4 years) |

| Policy-backed credit guarantees and direct lending programs | +0.6% | Global, strongest near-term impact in Asia-Pacific and Europe | Long term (≥ 4 years) |

| Alternative data and cash-flow analytics improving approval rates | +0.5% | Asia-Pacific, the Middle East and Africa, and South America | Short term (≤ 2 years) |

| International trade and supply-chain financing needs among SMEs | +0.4% | Asia-Pacific core, Europe with spill-over to the Middle East and Africa | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Digitization of SME Underwriting Compresses Credit Cycles

The SME lending market is seeing faster approval and disbursement cycles as underwriting moves from document-heavy review to automated decisioning based on cash flow and transaction data. Funding Circle stated in its full-year 2025 results that its AI credit models are 3x better at discriminating risk than traditional bureau scores, drawing on 10 billion proprietary data points built over 15 years[1]Funding Circle Holdings plc, “Full Year 2025 Results,” Funding Circle Corporate, fundingcircle.com. FinRegLab also found that cash-flow variables from bank transaction data offer predictive power comparable to credit history in small-business underwriting. The combined models perform better than either source alone. Mastercard is extending open-finance credit analytics that combine payment network sales data with open banking cash-flow signals, supporting a move toward near-real-time monitoring rather than a static annual review. These changes reduce processing friction across the SME lending market and make smaller ticket loans more viable for both banks and non-bank lenders. As this model scales, the cost gap between large and small lenders narrows, which can support new regional entry into the SME lending market.

Working Capital Demand Driven by Cash Conversion Cycle Volatility

Working capital demand remains the clearest volume anchor in the SME lending market because operating cash needs have stayed elevated across supply chains, payment cycles, and procurement networks. Working capital loans accounted for 42.97% of total SME loan originations in 2025, indicating that liquidity support still matters more than long-duration investment credit across most borrower segments. Short-term loans are also the fastest-growing tenure band, with a 5.86% CAGR through 2031, which aligns with a broader shift toward revolving facilities, invoice-backed borrowing, and shorter repayment terms. Citi noted in its 2026 supply chain financing outlook that SMEs remain the most underserved group in trade finance and that AI is beginning to lower underwriting costs for these exposures at scale[2]Citigroup, “Supply Chain Financing 2026,” Citi Global Insights, citigroup.com. This favors lenders that can see live business cash positions and receivable flows rather than relying only on annual statements. The result is a SME lending market expanding around recurring working capital needs, not just traditional term lending demand.

Embedded And Non-Bank Channels Redefine Origination Economics

The SME lending market is also being reshaped by lenders that reach borrowers within accounting, payments, commerce, and treasury workflows rather than through branch or broker channels. NBFCs and fintechs are projected to grow at a 9.02% CAGR from 2026 to 2031, nearly double the pace of the total SME lending market. Funding Circle’s 2025 results show that credit extended rose 29% to GBP 2,453 million (USD 3.1 billion), and profit before tax increased 6x to GBP 20.3 million (USD 25.7 million), indicating that digital origination models are moving beyond scale-building and into sustained profitability. SmartBiz completed the acquisition of Centrust Bank in March 2025 and began operating as SmartBiz Bank, N.A., which shows how platform-led lenders are pairing software-driven origination with regulated funding capacity. In this setting, the most valuable edge is not the cost of funds alone, but the ability to source, assess, and renew credit faster than traditional channels. That is why the next stage of competition in the SME lending market is likely to be concentrated around distribution partnerships, embedded integrations, and approval accuracy rather than pricing alone.

Policy-Backed Guarantees Unlock Credit Supply In Underserved Segments

Public credit support remains a structural driver of the SME lending market because guarantees help lenders expand their risk appetite in segments that lack collateral or long-formal records. The World Bank reported that outstanding SME loan guarantees averaged 2% of GDP across surveyed countries in 2024 and exceeded 5% of GDP in East Asia and the Pacific. In the United States, the SBA launched the Made in America Loan Guarantee in March 2026 with 90% coverage for manufacturing SME loans, up from the standard 75%, and waived loan fees for small manufacturers in FY2026[3]U.S. Small Business Administration, “SBA Announces New Made in America Loan Guarantee to Restore Manufacturing Dominance,” SBA, sba.gov. In India, the Mutual Credit Guarantee Scheme for MSMEs provides 60% guarantee coverage for facilities up to INR 100 crore (USD 12 million) for machinery purchases by small and medium manufacturers. The European Investment Fund has made cumulative guarantee commitments of more than EUR 77 billion and is deploying an additional EUR 10 billion under InvestEU for higher-risk SME credit. These programs widen the addressable borrower base inside the SME lending market and support lending in segments where risk pricing alone would otherwise block formal credit access.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Elevated SME default risk during policy tightening cycles | -0.8% | Global, concentrated in Europe and South America | Short term (≤ 2 years) |

| Limited financial transparency and sparse formal records for smaller firms | -0.7% | Asia-Pacific, the Middle East and Africa, and South America | Long term (≥ 4 years) |

| Higher compliance burden in KYC, AML, and model governance | -0.5% | Global | Medium term (2-4 years) |

| Collateral scarcity and weak asset coverage for unsecured lending | -0.4% | The Middle East and Africa, South America, and the Asia-Pacific core | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

SME Default Risk Intensifies Under Prolonged Rate Pressure

The SME lending market continues to feel the effects of the tightening cycle that began in 2022, as credit stress typically emerges after rates have remained high for a sustained period. OECD data showed that SME bankruptcies rose by 11% in 2023 across the median tracked economy, and 25 of 32 countries reported increases. In Germany, the KfW-ifo Credit Barrier survey for Q4 2025 found that more than 40% of SMEs in retail and services reported credit access difficulties, which marked a record high for those sectors[4]KfW Research, “KfW-ifo Credit Barrier Q4 2025 English Edition,” KfW, kfw.de. The ECB also noted in May 2026 that insolvency trends and credit loss exposure remain uneven across countries, especially where SME lending is concentrated in local banking systems. The Bank of England added that SME lending remains costlier to serve than large corporate lending because of smaller ticket sizes and information asymmetry, leaving lenders more inclined to tighten supply when stress rises. This creates a difficult pattern in the SME lending market because lenders often cut off access before defaults actually peak, deepening liquidity strain for weaker borrowers.

Formal Record Gaps Constrain Credit Decisioning For Micro Enterprises

The SME lending market still faces a basic infrastructure problem at the smallest end of the borrower base, as many micro firms do not maintain the consistent digital records lenders need for low-cost verification. The World Bank’s B-READY work found that customer due diligence requirements impose disproportionate costs on SMEs in developing economies, which reduces effective access even where formal lending channels exist. India’s SIDBI MSME Pulse showed that serious delinquencies improved to a 5-year low of 1.79% in March 2025. Still, the improvement was concentrated among borrowers with exposures above INR 50 lakh, while credit quality weakened in the sub-INR 50 lakh band. That pattern matters for the SME lending market because the fastest-growing borrower cohort is microenterprises, meaning the hardest-to-verify firms are also becoming more important to growth. FinRegLab’s findings on cash-flow underwriting show that better use of transaction data can improve decision quality. Still, those benefits depend on the availability of clean, accessible financial records in the first place. Until digital identity, eKYC, and open-finance tools reach smaller firms at scale, record gaps will remain a core friction point across the SME lending market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Lender Type: Incumbents Hold Volume, Fintechs Drive Growth

Banks held 77.21% of the SME lending market share in 2025, while NBFCs and fintechs are projected to expand at 9.02% CAGR through 2031. This split shows that the largest balance sheets still dominate formal credit delivery, especially in larger ticket sizes and longer-duration lending. At the same time, the fastest-growing segment of new business formation in the SME lending market is moving toward lenders that can approve and disburse smaller loans at lower processing costs. Funding Circle reported that credit extended rose 29% to GBP 2,453 million (USD 3.1 billion) in 2025, and profit before tax increased 6x to GBP 20.3 million (USD 25.7 million).

OakNorth also reported pre-tax profit of GBP 222.5 million (USD 289 million) in 2025, with gross originations growing 33% to GBP 2.8 billion (USD 3.7 billion) and cumulative lending facilities exceeding GBP 15.1 billion (USD 20 billion). These results indicate that digital and specialist lenders are now proving durable economics rather than relying solely on volume growth. For the SME lending industry, the main threat to incumbent banks is not a loss of funding scale, but a loss of customer access points and underwriting speed. That is why distribution partnerships, embedded channel access, and selective acquisitions look more rational than broad rate competition for many established lenders. The SME lending market is therefore developing into a two-speed structure, with banks retaining the largest loan books while non-bank players capture a larger share of the incremental flow.

By Loan Type: Working Capital Anchors Volume As Invoice Financing Scales

Working capital loans accounted for 42.97% of the SME lending market in 2025, making them the largest loan category by volume. Invoice financing is the fastest-growing loan type, with a 8.29% CAGR from 2026 to 2031, indicating that receivables-led borrowing is moving closer to the center of the SME lending market. The shift is being reinforced by formal policy action, including the Reserve Bank of India’s draft TReDS Directions 2026, which aims to streamline invoice financing rules, permit guarantee cover on TReDS exposures, and simplify onboarding for financiers. This matters because invoice products work well when borrowers need recurring liquidity but cannot offer fixed assets as security.

Term loans remain the second-largest category by volume in the SME lending market and continue to play a central role in funding equipment, expansion, and medium-term investment. Funding Circle said term loan originations increased 16% to GBP 1,638 million (USD 2.1 billion) in 2025. Equipment finance and trade finance serve distinct needs: the former is tied to productive asset purchases, while the latter is tied to supplier and buyer cycles. Citi’s 2026 supply chain financing report noted that SMEs remain the most underserved group in trade finance, leaving room for specialized lenders and digital platforms to expand their product reach. As a result, the SME lending market is broadening not by replacing working capital loans, but by building more precise products around cash-flow timing, invoices, and supply-chain activity.

By Collateral: Secured Lending Dominates, Unsecured Reshapes Credit Architecture

Secured lending accounted for 64.07% of total volume in 2025, confirming that collateral still anchors most of the SME lending market. Unsecured lending is forecast to grow at a 7.13% CAGR through 2031, well above the overall market pace, indicating that underwriting architecture is shifting. This change is being supported by better use of behavioral and transaction data rather than by a sudden improvement in borrower asset coverage. FinRegLab found in June 2025 that cash-flow variables derived from bank transaction data have predictive power comparable to credit history for small-business underwriting, and that combined models outperform either data source alone.

That evidence supports a broader shift across the SME lending market toward lending decisions based on business performance rather than on pledged assets alone. It is especially important for micro and small firms, where land, machinery, and formally documented fixed assets are often limited. For the SME lending industry, this opens a larger borrower pool but also raises the bar on model quality, fraud controls, and ongoing monitoring. Secured products will remain central because they still offer lower loss severity and easier risk pricing. Even so, the direction of the SME lending market points toward hybrid structures that combine partial security, guarantees, and cash-flow analytics within a single credit product.

By Loan Tenure: Short-Term Credit Gains As Working Capital Demand Fragments

Medium-term loans accounted for 38.86% of total volume in 2025, making them the largest tenure band in the SME lending market. Short-term loans are projected to grow at a 5.86% CAGR through 2031, reflecting the spread of revolving facilities, invoice-based borrowing, and shorter draw-and-repay structures. This does not mean SMEs have reduced their investment needs. It shows that more lenders are packaging liquidity around recurring operating cycles rather than around fixed multi-year amortization schedules.

OECD data have already pointed to a wider shift toward shorter maturities in Europe during the recent tightening period, as lenders reduced duration risk under uncertain rate conditions. Iwoca committed GBP 1.5 billion (USD 1.9 billion) in SME lending for 2026, including GBP 300 million for construction firms, demonstrating continued lender appetite for revolving and shorter-cycle products. Long-term loans still matter for asset-heavy businesses in manufacturing, construction, and equipment services, but those products remain more concentrated among banks and specialist institutional lenders. An important product evolution is the use of evergreen short-term facilities that renew based on repayment behavior and live trading data. This gives the SME lending market a way to mimic longer capital access while keeping flexibility for repricing and risk management.

By Borrower Size: Micro Enterprises Drive Volume Growth Despite Higher Risk

Small enterprises accounted for 36.67% of total lending volume in 2025, while micro enterprises are expected to expand at a 7.21% CAGR through 2031. This is one of the clearest signs that the SME lending market is becoming more accessible at the lower end of the business spectrum. Growth is strongest where automated underwriting can reduce the cost of serving very small loans that were previously uneconomic in formal channels. CRIF High Mark reported that micro enterprises accounted for 37% of the outstanding MSME credit portfolio and 85.8% of active loans in India as of April 2026, underscoring the segment's scale despite modest average ticket sizes.

That same segment also carries the greatest verification burden inside the SME lending market because formal records, tax trails, and audited statements are often weak or incomplete. Medium enterprises form a smaller borrower group in terms of count. Still, they command far larger average loan volumes and remain attractive to specialist lenders focused on entrepreneur-led lower mid-market businesses. Guarantee structures are therefore becoming essential for bridging the gap between high borrower need and limited conventional security. India’s guarantee programs, the EIF’s InvestEU platform, and related regional schemes show how public support can expand risk appetite for smaller firms that banks would otherwise price out. The SME lending market will continue to expand into micro business segments. Still, the quality of digital records and verification tools will determine how much of that demand becomes sustainable formal credit.

Geography Analysis

Asia-Pacific accounted for 43.23% of the SME lending market share in 2025 and is projected to grow at a 5.74% CAGR through 2031, keeping the region in a rare position as both the largest and fastest-growing geography. India remains a major driver of that profile, with the MSME credit portfolio crossing INR 46 lakh crore (USD 553 billion) in April 2026. Bank credit to MSMEs in India also rose 24.6% year on year as of November 2025, lifting the segment’s share of total bank credit to 18.5%. Policy support remains important across Asia-Pacific, including India’s Mutual Credit Guarantee Scheme and the RBI’s effort to formalize invoice financing rules. The region’s position in the SME lending market reflects a mix of borrower scale, rapid digitization, and widening policy intervention rather than a single-country effect.

North America remains a high-volume part of the SME lending market because bank penetration is deep, but competitive pressure is shifting toward technology-enabled origination. JPMorgan Chase announced in March 2026 that it would commit USD 80 billion to small-business lending over 10 years and expand its client base from 7 million to 10 million businesses. The SBA’s Made in America Loan Guarantee raised guarantee coverage to 90% for manufacturing SME loans and removed loan fees for small manufacturers in FY2026. SmartBiz’s move into a bank charter in 2025 showed how platform lenders in the region are combining digital acquisition with stable balance-sheet funding. Mastercard’s open-finance credit analytics also point to a broader North American shift from periodic review toward live transaction-led surveillance.

Europe remains one of the tighter parts of the SME lending market, with OECD data showing a 12% decline in new SME lending across the European Union in 2023 and restrictive conditions continuing into 2024. The European Investment Fund continues to provide the region’s key de-risking platform, with cumulative guarantee commitments exceeding EUR 77 billion and another EUR 10 billion deployed under InvestEU. Germany’s Q4 2025 KfW-ifo survey showed that more than 40% of SMEs in retail and services are facing difficulties accessing credit, underscoring the gap between demand and available supply. South America and Middle East, and Africa remain smaller in volume. Still, Brazil’s rise in higher-risk MSME loans from 8.2% in January 2025 to 8.9% in September 2025 shows how sensitive these regions are to policy rates and credit-cycle stress.

Competitive Landscape

The SME lending market remains moderately fragmented at the top and highly dispersed below the first tier, because no single lender or small cluster controls global credit flow across all borrower classes and geographies. Large banks still anchor the SME lending market through branch networks, deposit funding, and long-standing client relationships, but the basis of competition is changing. JPMorgan Chase’s USD 80 billion commitment over 10 years shows that leading banks are treating small business lending as a major growth priority rather than a peripheral segment. At the same time, digital specialists are proving that superior approval speed and better model performance can create a durable edge. Funding Circle’s 2025 results and OakNorth’s low cumulative principal loss record of 0.1% over 10 years show that data-rich lenders can scale without relying on the largest balance sheets.

Strategic moves in the SME lending market increasingly revolve around combining origination software with regulated funding. SmartBiz’s acquisition of Centrust Bank is a clear example, because it joined a digital lending platform with bank status and stable funding access. The same pattern is visible in product partnerships and technology deployment, where lenders are buying or integrating underwriting capability faster than they are building it internally. Funding Circle’s institutional forward-flow commitments of GBP 2.2 billion as of end-2025 also show that strong data performance can attract capital partners on favorable terms. This leaves the SME lending market with a clear divide between lenders that can continuously feed better transaction data into pricing models and those that still depend on slower, document-based credit review.

The main white spaces in the SME lending market remain microenterprise lending below formal bank thresholds, supply-chain finance for deeper supplier tiers, and unsecured medium-term credit supported by open finance data. OECD’s 2026 Scoreboard noted that governments are advancing digital infrastructure for invoice discounting and centralized credit registries, which support lenders with stronger compliance and workflow integration. That favors firms that can combine underwriting, monitoring, and reporting inside a single operating stack. It also means the next wave of winners in the SME lending market will likely be defined less by size alone and more by who can turn fragmented SME data into repeatable, low-friction credit decisions.

SME Lending Industry Leaders

-

JPMorgan Chase and Co.

-

Bank of America Corporation

-

Wells Fargo and Company

-

Industrial and Commercial Bank of China Limited

-

HDFC Bank Limited

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2026: GCash (Philippines) expanded MSME financing through a PHP 1.75 billion (USD 30 million) credit facility from the Asian Development Bank, targeting women-led and rural MSMEs with collateral-free, AI-underwritten loans. This positions GCash as a critical channel for last-mile credit access in Southeast Asia

- March 2026: The United States Small Business Administration launched the Made in America Loan Guarantee, offering a 90% guarantee for small manufacturing loans, up from the standard 75%, and waived all loan fees for small manufacturers in FY2026, directly expanding SME credit access in domestic production.

- March 2026: Funding Circle reported full-year 2025 results, with revenue growing 28% to GBP 204.3 million (USD 259 million), credit extended increasing 29% to GBP 2,453 million (USD 3.1 billion), and profit before tax rising 6x to GBP 20.3 million (USD 25.7 million). The company also upgraded its FY2026 revenue guidance to GBP 235 million.

- January 2026: The Reserve Bank of India published draft TReDS Directions 2026, consolidating MSME invoice financing regulations into a unified master direction, permitting credit guarantee cover on TReDS exposures, and simplifying financier onboarding to scale invoice discounting volumes.

Global SME Lending Market Report Scope

| Banks |

| NBFCs and Fintechs |

| Working Capital Loans |

| Term Loans |

| Equipment Financing |

| Trade Finance Loans |

| Invoice Financing |

| Other Loan Types |

| Secured Lending |

| Unsecured Lending |

| Short-term (<1 year) |

| Medium-term (1–5 years) |

| Long-term (>5 years) |

| Micro Enterprises |

| Small Enterprises |

| Medium Enterprises |

| North America | United States |

| Canada | |

| Mexico | |

| South America | Brazil |

| Argentina | |

| Chile | |

| Peru | |

| Rest of South America | |

| Europe | United Kingdom |

| Germany | |

| France | |

| Italy | |

| Spain | |

| BENELUX (Belgium, Netherlands, and Luxembourg) | |

| NORDICS (Denmark, Finland, Iceland, Norway, and Sweden) | |

| Rest of Europe | |

| Asia-Pacific | India |

| China | |

| Japan | |

| Australia | |

| South Korea | |

| South East Asia (Singapore, Malaysia, Thailand, Indonesia, Vietnam, and Philippines) | |

| Rest of Asia-Pacific | |

| Middle East and Africa | United Arab Emirates |

| Saudi Arabia | |

| South Africa | |

| Nigeria | |

| Rest of Middle East and Africa |

| By Lender Type | Banks | |

| NBFCs and Fintechs | ||

| By Loan Type | Working Capital Loans | |

| Term Loans | ||

| Equipment Financing | ||

| Trade Finance Loans | ||

| Invoice Financing | ||

| Other Loan Types | ||

| By Collateral | Secured Lending | |

| Unsecured Lending | ||

| By Loan Tenure | Short-term (<1 year) | |

| Medium-term (1–5 years) | ||

| Long-term (>5 years) | ||

| By Borrower Size | Micro Enterprises | |

| Small Enterprises | ||

| Medium Enterprises | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Chile | ||

| Peru | ||

| Rest of South America | ||

| Europe | United Kingdom | |

| Germany | ||

| France | ||

| Italy | ||

| Spain | ||

| BENELUX (Belgium, Netherlands, and Luxembourg) | ||

| NORDICS (Denmark, Finland, Iceland, Norway, and Sweden) | ||

| Rest of Europe | ||

| Asia-Pacific | India | |

| China | ||

| Japan | ||

| Australia | ||

| South Korea | ||

| South East Asia (Singapore, Malaysia, Thailand, Indonesia, Vietnam, and Philippines) | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | United Arab Emirates | |

| Saudi Arabia | ||

| South Africa | ||

| Nigeria | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

What is the current size of SME lending and how fast is it growing?

The SME lending market stood at USD 12.82 trillion in 2025 and is projected to reach USD 16.71 trillion by 2031, growing at a CAGR of 4.61% over 2026-2031.

Which lender group currently leads SME credit volumes?

Banks led in 2025 with 77.21% of total lending volume, showing that institutional credit infrastructure still dominates even as fintech channels expand.

Which loan category is most important for small business borrowing today?

Working capital loans held 42.97% of originations in 2025, which reflects the continued importance of liquidity support for operating cycles and payment timing.

What is the fastest-growing area within SME credit products?

Invoice financing is projected to grow at 8.29% CAGR through 2031, supported by tighter receivables management and more formal digital invoice-finance frameworks.

Which region offers the strongest growth outlook through 2031?

Asia-Pacific held 43.23% of global volume in 2025 and is also expected to post the fastest regional growth at 5.74% CAGR through 2031.

Why are micro enterprises becoming more important to lenders?

Micro enterprises are forecast to grow at 7.21% CAGR through 2031 as automated underwriting lowers servicing cost, even though record gaps and verification challenges remain significant.

Page last updated on: