United Kingdom Home Equity Lending Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

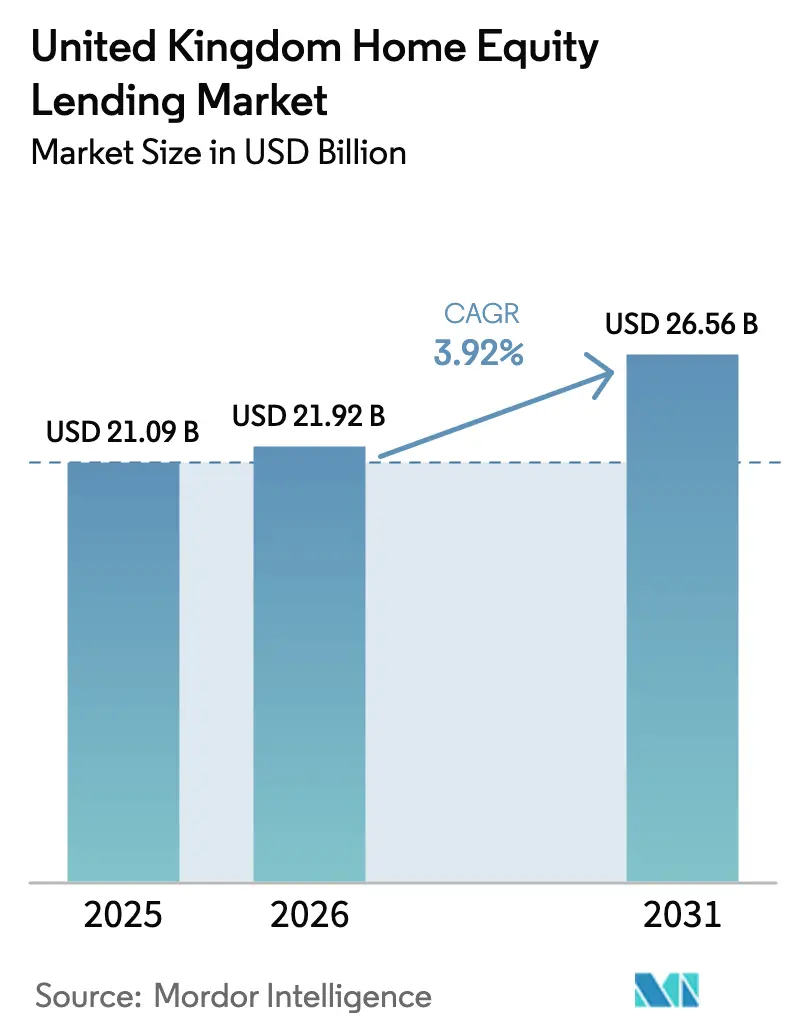

| Base Year Market Size (2025) | USD 21.09 Billion |

| Market Size (2026) | USD 21.92 Billion |

| Market Size (2031) | USD 26.56 Billion |

| Growth Rate (2026 - 2031) | 3.92% CAGR |

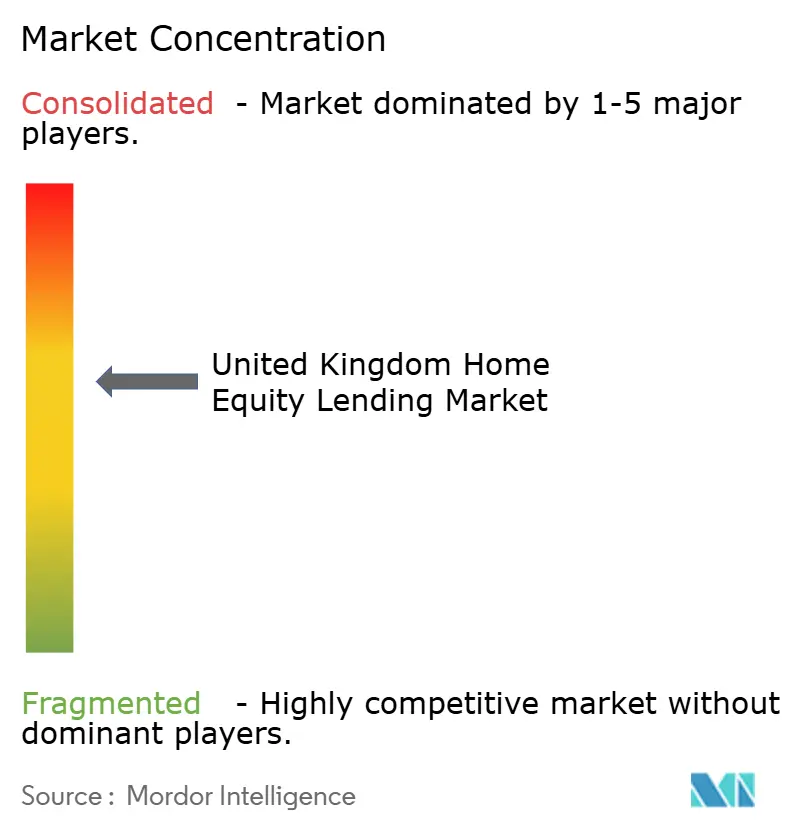

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

United Kingdom Home Equity Lending Market Analysis by Mordor Intelligence

The United Kingdom home equity lending market size in 2026 is estimated at USD 21.92 billion, growing from 2025 value of USD 21.09 billion with 2031 projections showing USD 26.56 billion, growing at 3.92% CAGR over 2026-2031. The measured expansion of the United Kingdom home equity lending market is supported by an ageing population that views housing wealth as a retirement income source, steady property price appreciation that enlarges tappable equity, and Financial Conduct Authority (FCA) rules that strengthen borrower confidence. Successive Bank of England rate cuts from 5.25% to 4.5% in 2024 intensified rate competition, rewarding lenders able to combine scale with digital efficiency. While cultural resistance to drawing down wealth persists, the sustained appetite for flexible retirement funding options continues to underpin growth in the United Kingdom's home equity lending market.

Key Report Takeaways

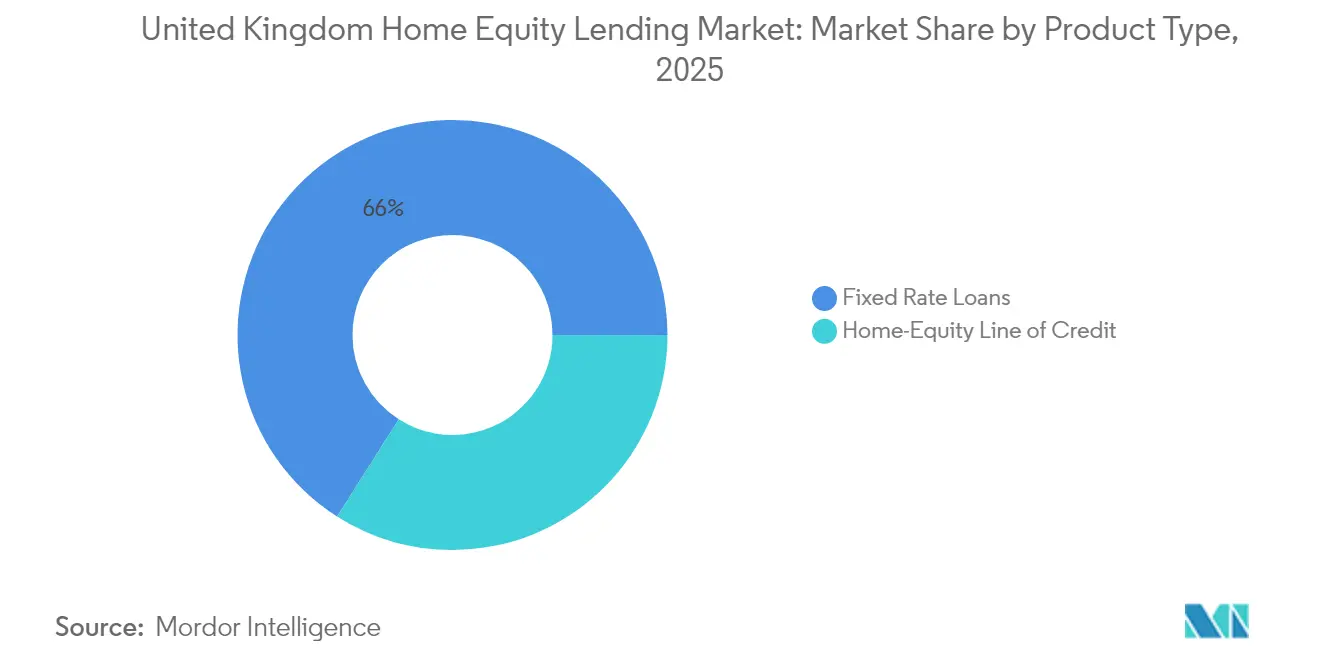

- By product type, fixed-rate loans held 65.98% of the UK home equity lending market share in 2025, while home equity lines of credit (HELOCs) are projected to expand at a 5.38% CAGR through 2031.

- By provider, banks commanded 56.15% of the UK home equity lending market share in 2025; fintech and alternative lenders are forecasted to grow at 7.12% CAGR through 2031.

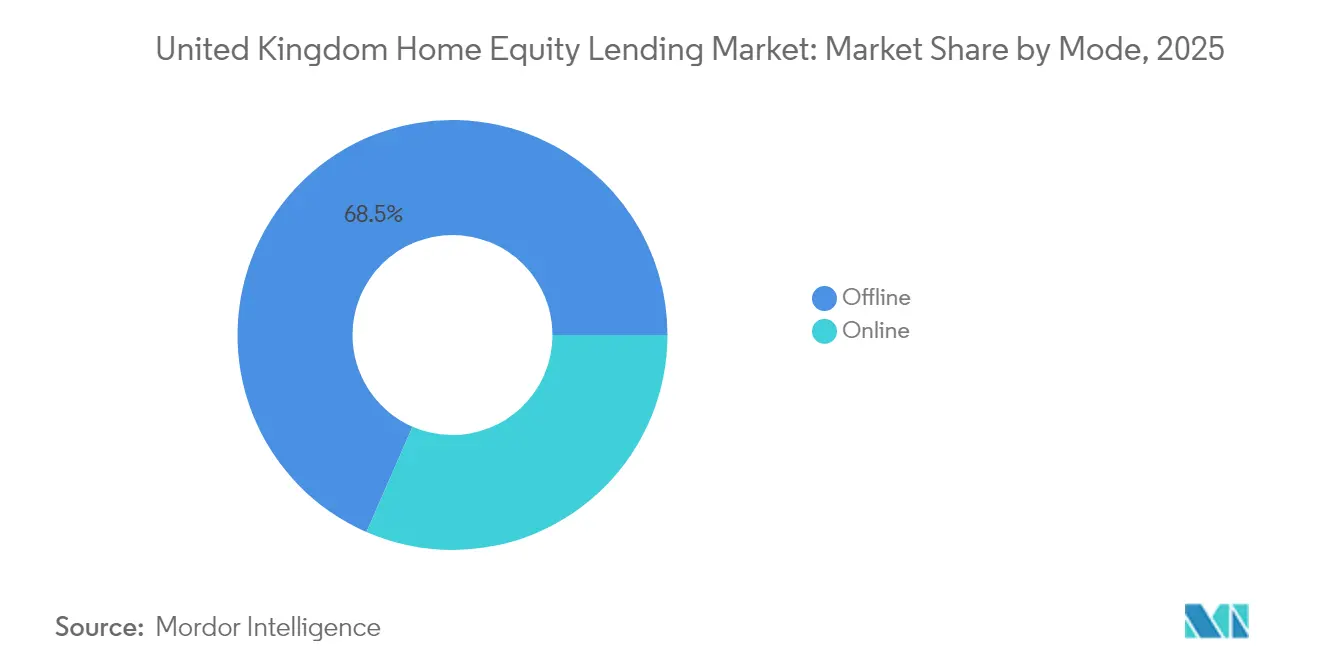

- By mode, offline distribution accounted for 68.45% of the UK home equity lending market in 2025, whereas online channels are advancing at a 7.41% CAGR to 2031.

- The United Kingdom home equity market is moderately concentrated. Major players such as Barclays Bank, Lloyds Banking Group, Nationwide Building Society, and Natwest Group dominate the market.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

United Kingdom Home Equity Lending Market Trends and Insights

Drivers Impact Analysis*

| Driver | ( ~ ) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Ageing population driving retirement-funded borrowing | +1.5% | Nationwide, strongest in South East and South West | Long term (≥ 4 years) |

| Rising UK house prices expanding tappable equity | +0.8% | Nationwide, strongest in London and South East | Medium term (2-4 years) |

| Lenders diversifying mortgage books amid margin squeeze | +0.6% | Nationwide, concentrated in major banking centres | Short term (≤ 2 years) |

| FCA-backed consumer-protection rules boosting confidence | +0.4% | Nationwide | Medium term (2-4 years) |

| Fintech-enabled open-banking underwriting cuts approval times | +0.3% | UK-wide, early adoption in urban areas | Short term (≤ 2 years) |

| HELOC draw-down flexibility attracting portfolio landlords | +0.2% | UK-wide, concentrated in high-yield rental markets | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Ageing Population Driving Retirement-Funded Borrowing

The UK home equity lending market benefits from a structural rise in borrowers aged 55 plus who increasingly tap housing wealth to supplement pensions. By 2040, more than half of homeowners over 60 are expected to access equity. This shift reflects both rising home values and stagnating annuity yields, which make property a more attractive source of retirement liquidity. Housing wealth now accounts for 40% of retirement assets for this cohort, surpassing defined-contribution pensions. The FCA’s 2024 Consumer Duty obliges lenders to offer fair value and clearer disclosures, encouraging cautious retirees to consider lifetime mortgages [1]Financial Conduct Authority, “Consumer Duty Policy Statement,” fca.org.uk . This regulatory emphasis on transparency and suitability has led to wider product diversification, including flexible drawdown features and interest-serviced options. Record volumes were evident in early 2025 when Key Later Life Finance reported 25% up in new lending compared to the previous year. This growth signals increasing borrower confidence, aided by improved adviser support and evolving perceptions around intergenerational wealth planning.

Rising UK House Prices Expanding Tappable Equity

Rising UK house prices are significantly expanding tappable equity, serving as a key driver for the growth of the UK home equity lending market. Property prices continued their upward trend, lifting aggregate homeowner equity to a record USD 7.1 trillion in 2024 and widening the addressable base for the UK home equity lending market[2] Equity Release Council, “Spring 2025 Market Outlook,” equityreleasecouncil.com . This increase in property values boosts loan-to-value headroom, allowing more homeowners to qualify for equity release without refinancing their primary mortgage. Nationwide’s House Price Review projects 2–4% growth for 2025, supported by earnings growth that exceeds price rises. London and the South East hold the largest equity pools, creating higher-value lending opportunities. These regions also attract wealthier, older homeowners who are more likely to engage in lifetime mortgages or drawdown products. Many borrowers locked into low-rate first mortgages, therefore, view second-lien products as a cost-effective way to release capital while rates remain below historical averages. This trend is also prompting lenders to launch more competitive HELOC and equity loan products targeted at prime urban markets.

Lenders Diversifying Mortgage Books Amid Margin Squeeze

Margin compression in conventional mortgages is prompting banks and building societies to pivot toward equity-based products. Building Societies Association data show that higher deposit costs eroded net interest margins in 2024, encouraging greater focus on specialist lending. Paragon Bank, for example, introduced buy-to-let HELOCs starting at 3.34% to capture landlord demand. Aldermore expanded criteria for self-employed borrowers, demonstrating how lenders use home-equity solutions to deepen relationships in underserved niches.

FCA-Backed Consumer-Protection Rules Boosting Confidence

FCA-backed consumer-protection rules are boosting confidence and acting as a strong driver for the UK home equity lending market. The FCA strengthened consumer safeguards in 2024 by embedding tailored support guidance and no-negative-equity guarantees within its handbook. These measures provide greater reassurance for older homeowners, especially those considering lifetime mortgages, that they will not owe more than their property’s value. Clearer disclosures, compulsory advice, and proposed 2025 mortgage-rule simplification aim to cut application times and reduce costs, making the UK home equity lending market more accessible. As a result, more cautious or first-time equity borrowers are entering the market, supported by regulated financial advice and standardized suitability assessments. Lenders that align product design with the FCA’s Consumer Duty gain a competitive advantage as borrower trust improves. This regulatory clarity is also encouraging institutional capital to flow into the sector, further improving product innovation and pricing stability.

Restraints Impact Analysis*

| Restraint | ( ~ ) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Successive Bank of England rate hikes eroding affordability | -0.7% | Nationwide | Short term (≤ 2 years) |

| Property-price volatility raising negative-equity risk | -0.5% | Nationwide, highest in London and South East | Medium term (2-4 years) |

| Cultural reluctance linked to inheritance considerations | -0.30% | UK-wide, stronger in traditional communities | Long term (≥ 4 years) |

| Compliance burden of evolving FCA rules for small lenders | -0.20% | UK-wide, concentrated among smaller providers | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Successive Bank of England Rate Hikes Eroding Affordability

Successive Bank of England rate hikes are eroding affordability and acting as a restraint on home equity lending. The base-rate climb from 0.1% in 2021 to a peak of 5.25% in 2024 materially lifted lifetime-mortgage and HELOC pricing[3]Bank of England, “Financial Stability Report 2024,” bankofengland.co.uk . Although cuts to 4.5% offer relief, monthly refinancing costs rose for many households, curbing the appetite for additional borrowing. These higher debt-servicing burdens make homeowners more cautious about leveraging property equity, especially for non-essential expenditures. Average lifetime-mortgage coupons briefly exceeded 6%, testing affordability buffers set by the FCA. While easing monetary policy should gradually restore capacity, affordability headwinds are expected to temper near-term loan growth. This environment is also prompting lenders to tighten underwriting criteria and limit higher-LTV offers, further restricting market access.

Property-Price Volatility Raising Negative-Equity Risk

Property-price volatility is raising negative-equity risk, acting as a restraint on the UK home equity lending market. After two consecutive annual declines, UK house prices stabilised in late 2024 but pockets of softness persist, particularly in high-value London boroughs. Lenders responded by tightening loan-to-value ceilings and applying conservative automated valuations. This has reduced the amount of tappable equity available to borrowers, particularly in regions where price recovery remains uncertain. Negative-equity fears remain a deterrent for risk-averse borrowers and a capital-allocation concern for lenders, slowing origination volumes until sustained price stability is evident. As a result, some lenders are also pausing product rollouts or re-pricing offers to reflect increased downside risk.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Fixed-Rate Leadership with HELOC Momentum

Fixed-rate lifetime mortgages dominated the UK home equity lending market with a 65.98% share in 2025, underscoring homeowners’ preference for payment certainty during a volatile rate cycle. Average releases of GBP 90,000 (USD 113,000) and loan-to-value ceilings near 60% illustrate sizable transaction values that reinforce lender profitability even as margins tighten. These products provide stability for both borrowers and lenders, especially in an environment where rising interest rates have increased the appeal of locking in costs. The flexibility of interest-roll-up structures appeals to retirees seeking liquidity without servicing payments. This structure allows older homeowners to unlock wealth without impacting monthly cash flow, which is particularly attractive for those relying primarily on pensions or fixed income.

HELOCs recorded a 5.38% CAGR outlook to 2031 as portfolio landlords leverage revolving facilities for acquisition and refurbishment projects. This product's flexibility allows repeat borrowing without reapplying, making it ideal for property investors needing short-term capital access. Open-banking analytics accelerate approvals and improve risk-based pricing, drawing interest from self-employed and limited-company borrowers. Real-time income verification and dynamic credit scoring have significantly shortened application timelines, enhancing user experience. Although fixed-rate products will likely remain dominant, HELOC adoption is poised to rise as digital platforms demystify line-of-credit utilisation and as FCA proposals streamline underwriting. Enhanced borrower education and fintech-led transparency are expected to gradually normalize HELOC usage among mainstream owner-occupiers

By Provider: Banks Hold Scale Advantage; Fintech Gains Share

Banks possessed 56.15% of the UK home equity lending market size in 2025 due to large customer bases, low-cost funding, and cross-sell synergies. Barclays and HSBC trimmed pricing by up to 0.31 percentage points following the 2024 rate cut to protect franchise strength. These institutions leverage their deposit base and established distribution networks to maintain competitive pricing while offering bundled financial services. Additionally, they benefit from high brand trust and regulatory alignment, enabling them to scale lifetime mortgages and HELOCs across both urban and regional markets. Challenger banks and building societies pursue acquisition strategies, evidenced by Coventry Building Society’s purchase of Co-operative Bank. This consolidation trend allows smaller players to expand balance sheets, diversify loan portfolios, and compete more effectively with major incumbents.

Fintech and alternative lenders are forecast to expand at 7.12% CAGR through 2031, propelled by modern cloud-native cores and data-driven risk scoring that compress approval cycles to days. Their platforms often offer fully digital onboarding, document uploads, and real-time income verification, which attract tech-savvy and underserved borrowers. Partnerships with technology vendors such as Tata Consultancy Services demonstrate the push to digitize end-to-end origination. These collaborations also help fintechs comply with evolving FCA guidelines by embedding regulatory frameworks directly into the application workflow. Niche players like Gatehouse Bank further diversify the landscape through Shariah-compliant structures, highlighting how specialism can unlock untapped borrower segments. Such targeted offerings are particularly appealing in multicultural regions and among faith-based investors, creating new growth avenues beyond the conventional lending base.

By Mode: Hybrid Distribution Bridges Offline Trust and Digital Speed

The advice-centric nature of equity-release transactions kept offline channels at 68.45% of the UK home equity lending market in 2025. FCA rules require qualified advisers to confirm suitability, reinforcing the role of branch networks and telephone advice. Nevertheless, cost pressures encourage lenders to streamline manual processes, prompting the adoption of video advice sessions and e-signatures within traditional journeys. These hybrid formats preserve regulatory integrity while reducing overhead and increasing convenience for less digitally fluent borrowers.

Online channels are set for a 7.41% CAGR through 2031 as borrowers embrace digital front-ends that simplify data capture and documentation upload. The FCA’s 2025 consultation to simplify mortgage rules is expected to reduce regulatory friction, accelerating the take-up of fully online or hybrid journeys. Challenger banks such as Starling exemplify how digital self-service complements mandatory advice to deliver faster decisions without compromising compliance standards. Growing familiarity with digital financial tools among older age groups is also expected to widen adoption and support long-term market scalability.

Geography Analysis

The United Kingdom home equity lending market shows pronounced regional variation anchored in property price disparities and demographic distribution. London and the South East command the largest aggregate equity pools, translating into elevated penetration rates for lifetime mortgage products. High average loan sizes in these regions support lender income even at compressed spreads. At the same time, price volatility in prime postcodes prompts lenders to adopt lower advance rates to mitigate downside risk.

Southern coastal counties such as Dorset and Devon exhibit an above-average concentration of retirees, combining equity richness with lifestyle migration that sustains demand for draw-down products. Local planners’ restrictive housing supply policies maintain upward pressure on prices, reinforcing equity accumulation. The Equity Release Council notes that borrowers in these counties tend to extract a higher proportional share of property value than the national mean.

Northern England and Scotland present the fastest volume growth as lower property prices expand accessibility for middle-income households. Buy-to-let investors active in cities such as Manchester and Glasgow use HELOCs to finance energy-efficiency upgrades that enhance rental yields. Wales is also emerging as an opportunity zone after academic studies showed that equity release could boost local consumption and raise private-pension wealth. Government initiatives, including an extended Mortgage Guarantee Scheme, provide additional tailwinds across regions with historically lower ownership rates.

Competitive Landscape

Competition in the UK home equity lending market intensified after the Bank of England’s 2024 rate cuts triggered a wave of repricing. Nationwide, Santander UK, and Halifax successively announced rate reductions to defend market share, with Santander introducing the first sub-4% residential fixes of 2025. Pricing pressure favors lenders with scalable funding platforms and advanced risk analytics.

Technology investment is a critical differentiator. Major banks deploy open-banking data feeds and cloud-based decision engines to lower origination costs. TCS’s Digital Mortgage Lending Solution has been adopted by multiple mid-tier lenders seeking progressive system renovation rather than wholesale core replacement. Specialist player Aldermore uses automated income verification to serve self-employed borrowers who fall outside mainstream credit models.

Strategic consolidation is reshaping the provider map. Coventry Building Society’s acquisition of Co-operative Bank added 2.5 million retail customers and 94,000 SMEs, broadening cross-selling opportunities and enhancing funding diversity. Partnerships also feature prominently: Gatehouse Bank signed a GBP 550 (USD 691) million sharia-compliant origination deal with ColCap UK, signalling appetite for niche segments that larger lenders have yet to prioritise. Despite regulatory barriers to fully digital distribution, hybrids that blend human advice with digital efficiency seem best positioned for sustained share gains.

United Kingdom Home Equity Lending Industry Leaders

Barclays Bank

Nationwide Building Society

Lloyds Banking Group

NatWest Group

Santander UK

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2025: Nationwide Building Society raised maximum LTV on new-build houses to 95% within its Helping Hand program and extended offer validity on new-build purchases to nine months.

- May 2025: The Financial Conduct Authority opened consultation CP25/7 to simplify mortgage rules, targeting faster approvals and reduced costs without diluting consumer protection.

- February 2025: Santander UK introduced two- and five-year fixed residential mortgages at 3.99% for 60% LTV after a 0.75% cut to affordability rates, extending borrowing capacity for new and existing customers.

- January 2025: Coventry Building Society completed its acquisition of Co-operative Bank Holdings, creating an institution with GBP 50.3 (USD 63.2) billion in mortgage balances while retaining separate banking licenses during integration.

United Kingdom Home Equity Lending Market Report Scope

Home equity lending allows homeowners to get credit based on how much equity they have in their homes. Lenders normally allow homeowners to borrow up to 80 percent of their home equity in a lump sum, which may be a big figure for those who have paid off a major portion of their mortgage or who own their property outright. This report aims to provide a detailed analysis of Home equity lending in the United Kingdom. It focuses on the market dynamics, emerging trends in the segments, the future of markets, and insights on various drivers and restraints. Also, it analyses the key players and the competitive landscape in the market. The UK Home Equity Lending Market can be segmented by Types, (Fixed Rate Loans, Home Equity Line of Credit (HELOC)), By Service Provider, (Banks, Building Societies, Online, Credit Unions and Others), and by Mode (Online and Offline).

| Fixed Rate Loans |

| Home Equity Line of Credit |

| Banks |

| Credit Unions |

| Non-Banking Financial Institutions |

| Others (Fintech, Brokers, etc.) |

| Online |

| Offline |

| By Product Type | Fixed Rate Loans |

| Home Equity Line of Credit | |

| By Provider | Banks |

| Credit Unions | |

| Non-Banking Financial Institutions | |

| Others (Fintech, Brokers, etc.) | |

| By Mode | Online |

| Offline |

Key Questions Answered in the Report

What is the current size of the United Kingdom home equity lending market?

The United Kingdom home equity lending market size was USD 21.92 billion in 2026 and is projected to reach USD 26.56 billion by 2031 at a 3.92% CAGR.

Which product dominates this market?

Fixed-rate lifetime mortgages led with 65.98% share in 2025, reflecting borrower preference for payment certainty in a volatile rate environment.

How fast are online channels growing?

Online distribution in the UK home equity lending market is forecasted to expand at a 7.41% CAGR as simplified FCA rules accelerate digital adoption.

Why are HELOCs becoming popular among landlords?

Portfolio landlords favour HELOCs for flexible draw-down that finances acquisitions and renovations, with specialist lenders offering rates starting at 3.34%.

Page last updated on: