Smart Toilet Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

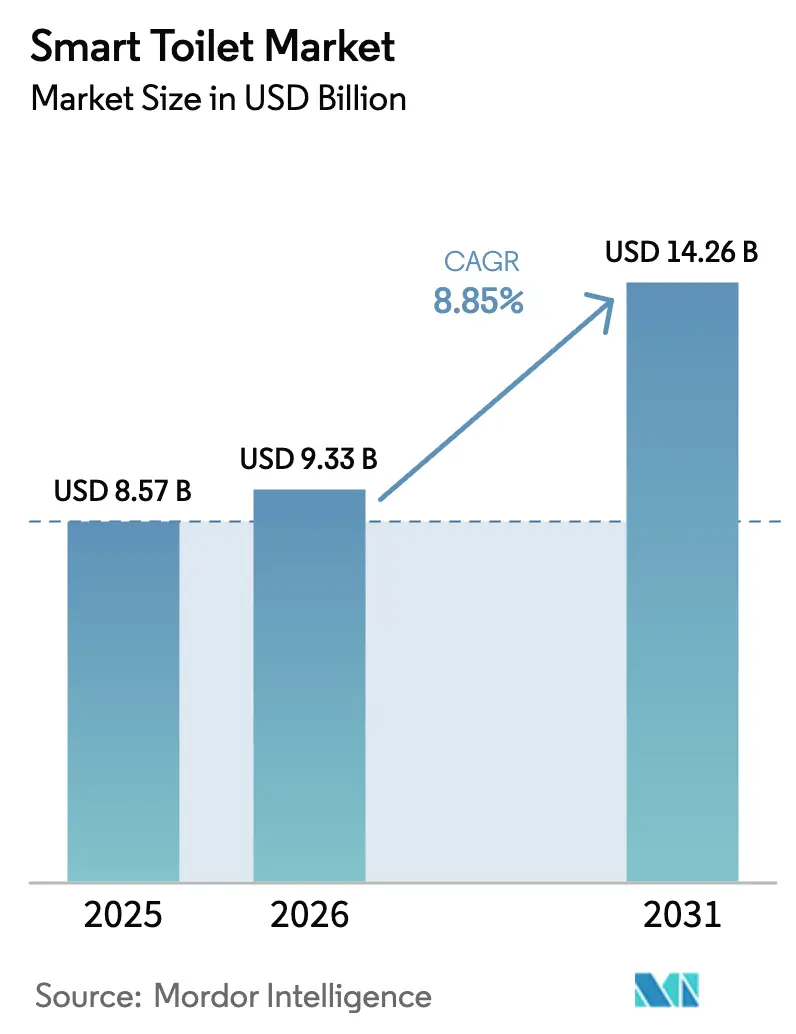

| Market Size (2026) | USD 9.33 Billion |

| Market Size (2031) | USD 14.26 Billion |

| Growth Rate (2026 - 2031) | 8.85% CAGR |

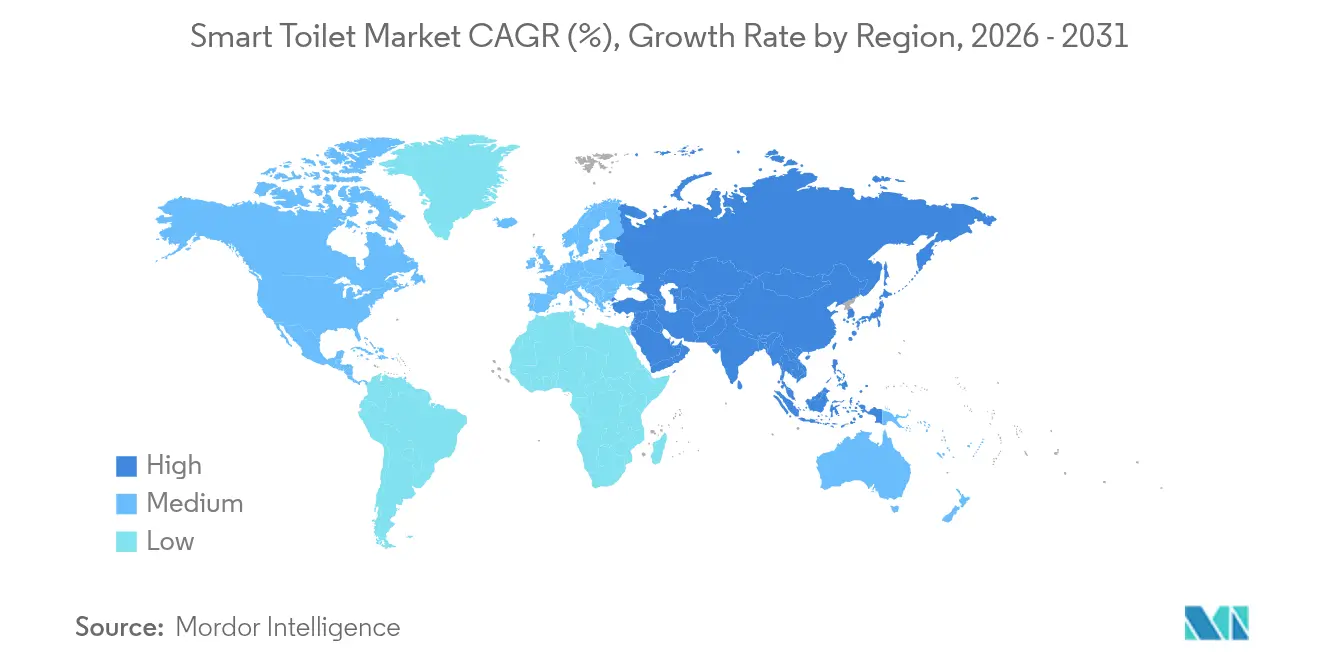

| Fastest Growing Market | Asia Pacific |

| Largest Market | Europe |

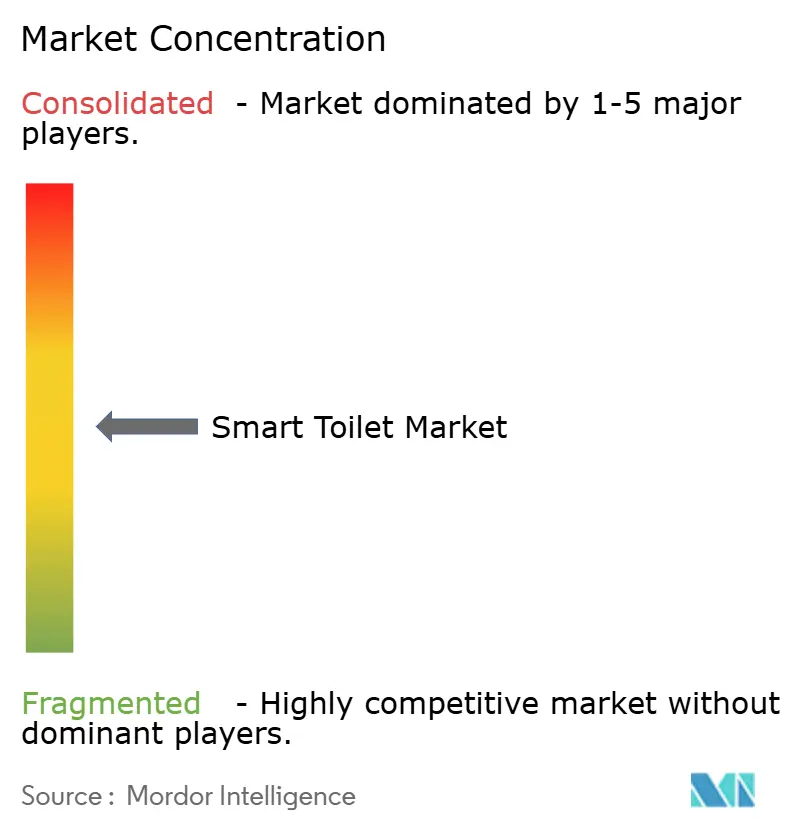

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Smart Toilet Market Analysis by Mordor Intelligence

The smart toilet market size was valued at USD 8.57 billion in 2025 and estimated to grow from USD 9.33 billion in 2026 to reach USD 14.26 billion by 2031, at a CAGR of 8.85% during the forecast period (2026-2031). Persistent post-pandemic hygiene priorities, rapid smart-home ecosystem penetration, and aging demographics are shifting toilets from basic fixtures toward connected health platforms. European consumers lead adoption of water-efficiency regulations and premium bathroom culture, while Asia-Pacific is urbanization and income growth that fuel the fastest regional expansion. Product demand skews toward all-in-one systems, yet retrofit kits are rising quickly as cost-effective upgrades. Healthcare facilities, hotels, and elder-care providers are accelerating deployments to reduce caregiver burden and enhance patient safety. Digital retail keeps gaining traction, but in-store showrooms remain indispensable for high-involvement purchases.

key Report Takeaways

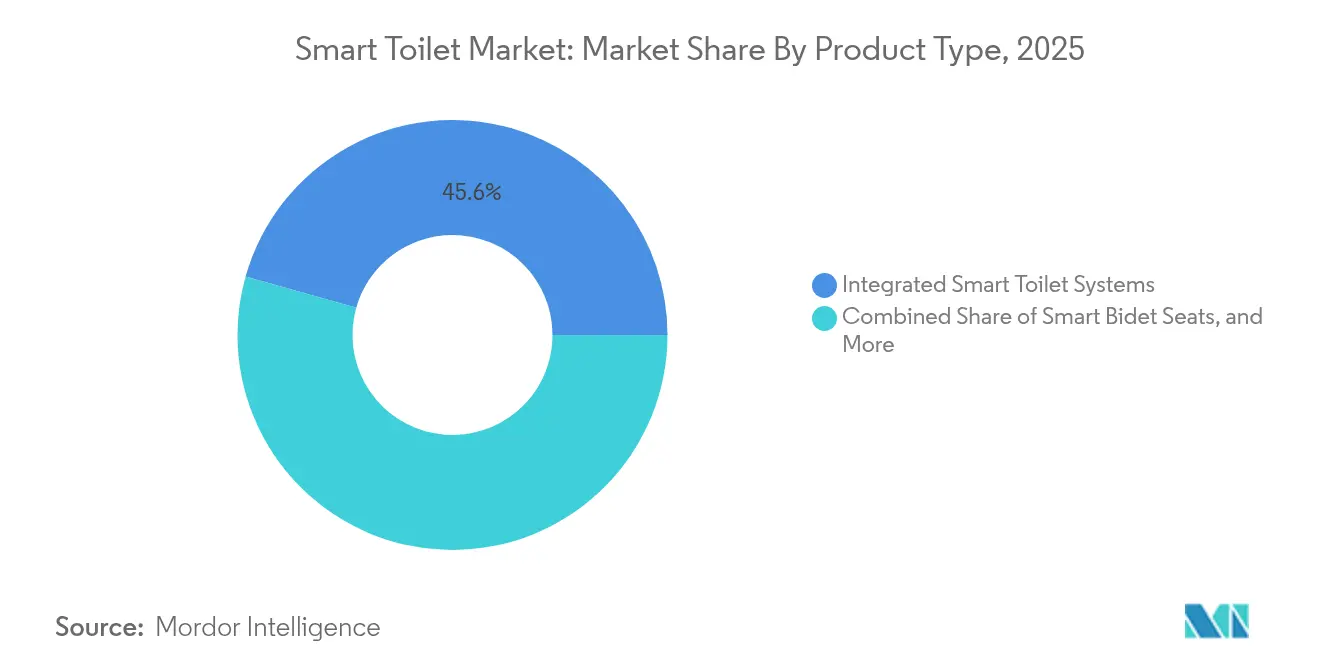

- By product type, all-in-one smart toilets commanded 45.62% of the smart toilet market share in 2025, whereas retrofit conversion kits post a 12.05% CAGR through 2031.

- By connectivity, remote-control units held 46.88% of 2025 revenue, but Wi-Fi/app-connected models expand at 14.02% CAGR to 2031 in the smart toilets market.

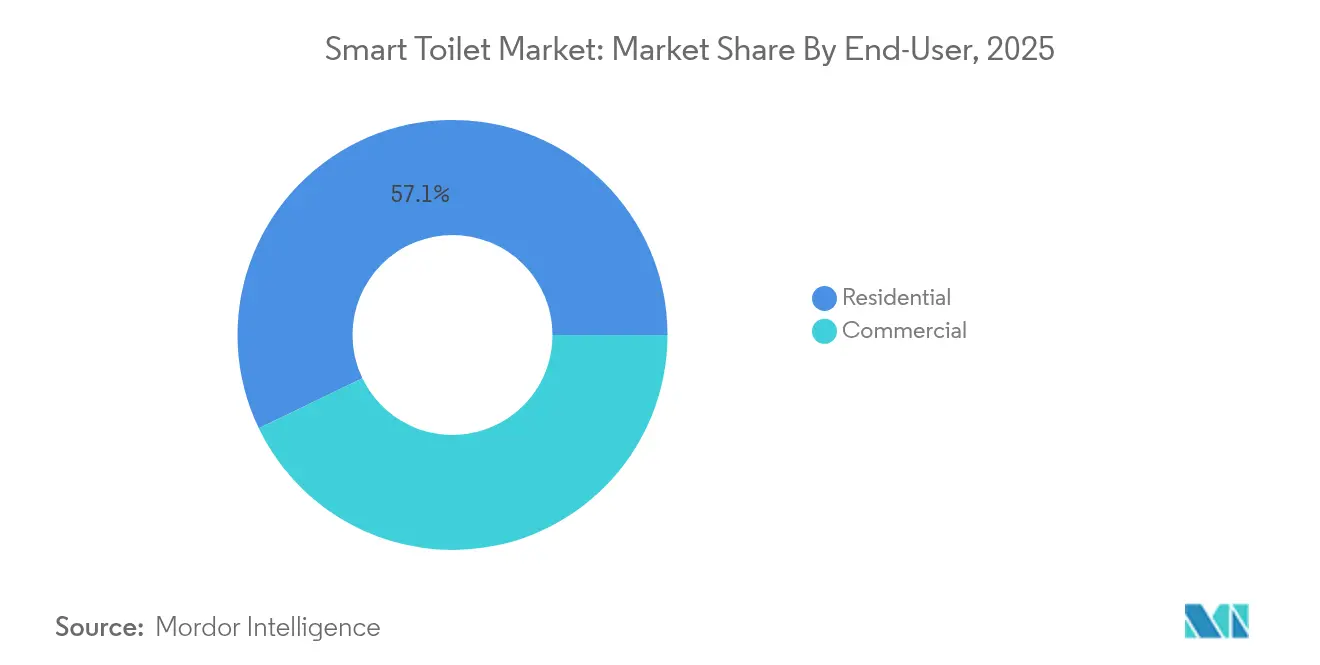

- By end user, residential settings captured 57.14% of the smart toilet market size in 2025; healthcare facilities are growing fastest at 12.74% CAGR.

- By distribution channel, offline retail retained 66.41% share of the smart toilet market size in 2025, while online retail scales at 17.12% CAGR.

- By geography, Europe led with 35.12% revenue in 2025; Asia-Pacific advances at a 12.51% CAGR, the highest among all regions.

- Market leaders like TOTO, LIXIL Corporation, Kohler Co., Villeroy & Boch AG, and Roca Sanitario benefit from brand recognition, distribution networks, and manufacturing scale that create barriers for pure-play technology companies attempting to enter the market.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Smart Toilet Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising hygiene and sanitation awareness post-COVID-19 | +2.1% | Global, with strongest impact in North America & Europe | Short term (≤ 2 years) |

| Aging population driving demand for elderly-friendly bathroom solutions | +1.8% | APAC core, spill-over to North America and Europe | Long term (≥ 4 years) |

| Integration with smart-home ecosystems and voice assistants | +1.4% | North America and EU, expanding to APAC urban centers | Medium term (2-4 years) |

| Government incentives for water-efficient fixtures | +1.2% | North America with state-level programs, EU regulatory framework | Medium term (2-4 years) |

| Insurance discounts for fall-detection and health-monitoring toilets | +0.8% | North America and Japan, pilot programs in EU | Long term (≥ 4 years) |

| Hotel ESG commitments accelerating premium restroom retrofits | +0.6% | Global hospitality hubs, luxury segment focus | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rising Hygiene and Sanitation Awareness Post-COVID-19

Touch-free flushing, bidet cleansing, and UV self-sterilization have become mainstream expectations as consumers continue prioritizing household hygiene. U.S. surveys show more than 50% of homeowners now express purchase intent for smart toilets, with Gen Z and millennials leading interest. Many European and Japanese households already treat smart toilets as essential wellness infrastructure. Product development now centers on antimicrobial coatings and automated bowl-cleaning cycles that align toilets with medical-grade sanitation standards.

Aging Population Driving Demand for Elderly-Friendly Bathroom Solutions

Global seniors will exceed 1.4 billion by 2030, prompting caregivers and facility managers to adopt fall-detection seats, automated emergency alerts, and in-bowl health sensors. Hospitals and long-term-care centers cite reduced caregiver workload and faster response times as justification for premium pricing. Academic pilots such as iRestroom demonstrate low-cost sensor arrays that transmit real-time data to family dashboards, underscoring the technology is potential to enable aging-in-place without compromising privacy.

Integration with Smart-Home Ecosystems and Voice Assistants

Bathroom fixtures are merging into unified IoT networks alongside lighting, HVAC, and security systems. Diurnal traffic analysis shows connected appliances generate predictable data spikes that mirror daily routines, positioning smart toilets as valuable nodes for whole-home analytics. Voice-controlled flushing and personalized user profiles improve accessibility, yet cybersecurity remains a pain point as many IoT devices still launch without encryption or multi-factor authentication.

Government Incentives for Water-Efficient Fixtures

Rebate schemes and efficiency mandates reduce payback periods for high-efficiency smart toilets. Utah’s 2025 program covers up to USD 200 per unit for ultra-low-flush models [1]Source: Utah Division of Water Resources, “Utah Water Conservation Rebate Program,” water.utah.gov. . Florida’s WISE initiative and EU ecodesign rules likewise accelerate conversion by linking conservation goals to consumer savings.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High upfront cost versus conventional toilets | -1.9% | Global, particularly price-sensitive emerging markets | Short term (≤ 2 years) |

| Cyber-security and data-privacy concerns | -1.3% | North America and EU with strict data protection regulations | Medium term (2-4 years) |

| Plumbing compatibility and retrofit complexity in older buildings | -1.1% | North America and Europe with aging infrastructure | Medium term (2-4 years) |

| Supply-chain volatility for MEMS sensors and heating elements | -0.8% | Global, with Asia-Pacific manufacturing concentration | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

High Upfront Cost Versus Conventional Toilets

Smart models can cost 3-4 times more than standard bowls, slowing adoption among budget-constrained homeowners and cash-strapped institutions. Hotels and hospitals often require documented ROI from reduced water use or lower infection-control costs before approving capital outlays. Retrofit kits, typically priced under USD 500, help bridge this gap by allowing stepwise upgrades.

Cyber-Security and Data-Privacy Concerns

Advanced units that analyze biomarkers must meet stringent data-protection standards. Academic reviews warn that unpatched IoT firmware, weak default passwords, and unclear data-ownership clauses expose users to surveillance and potential discrimination. Privacy-by-design engineering and optional offline modes are emerging as selling points in Europe GDPR environment.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: All-in-One Systems Lead Innovation

All-in-one designs captured 45.62% smart toilet market share in 2025, with seamless integration of bidet sprays, heated seats, and air purifiers. Flagship lines such as TOTO NEOREST combine EWATER+ disinfection with automatic lid lift, appealing to hygiene-focused consumers. Up-market demand anchors a premium price tier that shields margins even as component costs ease.

Retrofit smart conversion kits, however, post the highest 12.05% CAGR, signaling a strong value proposition for households unwilling to overhaul plumbing. Brands are bundling universal mounting plates and app-based tutorials to simplify do-it-yourself installation. Smart bidet seats continue steady growth in countries that have already normalized cleansing sprays, while wall-hung bowls address small urban bathrooms. Portable camping variants remain niche but showcase battery-powered flush pumps and composting features relevant to disaster relief agencies.

By Connectivity: Remote-Control Dominance Faces Digital Disruption

Infra-red handsets kept 46.88% of 2025 revenue, reflecting user confidence in proven technology and zero-latency operation. Elderly residents appreciate tactile buttons that bypass smartphone dependencies. Yet Wi-Fi modules are scaling at 14.02% CAGR as consumers seek push notifications on water usage and predictive maintenance. This shift enlarges the smart toilet market by tapping into existing smart-home hubs.

Bluetooth bridges offline reliability with app-level customization, whereas voice-assistant models offer hands-free controls key for limited-mobility users. Manufacturers now embed over-the-air firmware updates to patch vulnerabilities and release new health features, underscoring the sector is migration from hardware-centricity toward service-oriented software lifecycles.

By End-User: Healthcare Facilities Drive Growth

Residential bathrooms delivered 57.14% of the smart toilet market size in 2025, buoyed by home renovation cycles and smart-home bundle discounts. Multigenerational households value automatic cleaning and adjustable spray positioning that accommodate varied mobility needs.

Healthcare installations are expanding at a 12.74% CAGR as hospitals quantify fewer slips and faster pathogen mitigation. A Japanese study linked 86.9% of electric bidet bowls to residual bacterial loads, galvanized design tweaks such as instant electrolyzed-water rinses . Commercial subsegments including hospitality and corporate offices follow closely, integrating odor management and usage analytics to elevate guest satisfaction and facility benchmarking.

By Distribution Channel: Digital Transformation Accelerates

Showrooms and specialty dealers still account for 66.41% of 2025 revenue, providing live demos and plumbing consultations essential for first-time buyers. Retailers curate mock-up bathrooms where shoppers test heated seats and ambient night lights, reinforcing perceived value.

Online sales, however, record a 17.12% CAGR as immersive 3D configurators and virtual-reality room planners build confidence to complete high-ticket checkout. Brand websites dominate direct-to-consumer volume, while marketplaces attract comparison shoppers through bundled installation services. Successful sellers meld click-and-collect models that let customers research online, then verify fitment in-store before scheduling delivery.

Geography Analysis

Europe is 35.12% revenue share reflects decades of water-efficiency rules, mature distribution, and design-forward consumer preferences. German and Dutch codes favor dual-flush volumes, prompting early embrace of electronic valves. LIXIL’s local subsidiary markets WaterSense-certified bowls that reduce water use by more than 20%. In the UK, 2024 Washlet sales climbed 50% as households retrofit loft conversions for multi-generational living.

Asia-Pacific represents the growth engine, registering a 12.51% CAGR on the back of Japan's cultural leadership and China's rising middle class. TOTO has shipped more than 60 million WASHLET units worldwide, with household penetration above 80% in major Japanese cities. Indian manufacturers now bundle sensor seats with government sanitation drives targeting urban apartments. Regional supply-chain depth for MEMS sensors and heating elements also compresses costs, reinforcing local adoption advantages.

North America is catching up, evidenced by a 19.7% 2025 sales surge for TOTO in the Americas. State-level rebates and insurance discounts for fall-detection toilets further widen the addressable smart toilet market. Yet legacy plumbing layouts and cultural familiarity with toilet paper still temper velocity. Ongoing education campaigns underscore water savings and hands-free hygiene to convert skeptics.

Competitive Landscape

Established ceramic specialists maintain brand trust, global footprints, and vertically integrated production scale. TOTO, LIXIL, and Roca collectively exert technology leadership by coupling proprietary glazing with sensor advancements. TOTO alone has surpassed 60 million smart-capable shipments, reflecting deep R&D pipelines and disciplined channel partnerships.

Mid-tier challengers chase whitespace by offering Wi-Fi upgrade modules and AI-driven health analytics that interpret urine and stool markers. Partnerships with med-tech startups yield intellectual-property cross-licensing while sharing compliance costs for medical-device registration. Some HVAC vendors are bundling toilets with shower decalcification systems to capture larger bathroom-suite contracts.

Price-focused entrants exploit e-commerce to launch retrofit sprays under USD 150, driving entry-level awareness and seeding future upgrades. Component suppliers of seat heaters, nozzles, and methylacrylate panels benefit from rising volume orders. Overall, competition is moderate; deep expertise in ceramics and water-routing still protects incumbents even as software layers add room for differentiation.

Smart Toilet Industry Leaders

TOTO Ltd.

Kohler Co.

LIXIL Corporation (incl. American Standard)

Roca Sanitario, S.A.

Villeroy and Boch AG

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- October 2024: TOTO Vietnam launched the upgraded NEOREST NX smart toilet. Celebrating TOTO’s 100th anniversary, it features a refined ceramic design and advanced technologies like EWATER+ for seat hygiene, automatic functions, and deodorization. The product emphasizes luxury, health, and sustainability for a next-generation bathroom experience.

- July 2024: At India Design Week 2024, Kohler unveiled its Numi 2.0 Intelligent Toilet, showcasing advanced features like KOHLER® Konnect, motion-sensing functions, UV sanitization, and ambient settings. Alongside, Kohler presented smart bathroom innovations, digital showers, and artist edition collections, highlighting a fusion of technology, design, and artistic heritage in bath spaces.

- February 2024: Brondell launched its Sutro Integrated Smart Bidet Toilet, combining hands-free automation, advanced hygiene features, and WaterSense-certified dual jet and siphon flushing. Priced at USD 2,499.99, Sutro offers a sustainable, high-tech bathroom experience with features like heated seating, endless warm water, UV nozzle cleaning, and a powerful 1.28-gallon flush system.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study defines the smart toilet market as the worldwide sales value of factory-built toilet fixtures that integrate electronic or sensor-based features such as heated bidet wash, automatic flush, deodorization, app or voice connectivity, and basic health monitoring.

This review excludes stand-alone electronic bidet lids sold without a matching ceramic pan.

Segmentation Overview

- By Product Type

- Integrated Smart Toilet Systems

- Tankless Design

- Tank-type Design

- Smart Bidet Seats

- Electric Bidet Seats

- Hybrid-heating Bidet Seats

- Wall-Hung Smart Toilets

- Floor-Mounted Smart Toilets

- Retrofit Smart Conversion Kits

- Portable & Camping Smart Toilets

- Integrated Smart Toilet Systems

- By Connectivity

- Remote-Control (Infrared)

- Wi-Fi / App-Connected

- Bluetooth

- Voice-Assistant Enabled

- By End-User

- Residential

- Commercial

- Hospitality

- Healthcare Facilities

- Corporate Offices

- Public Utilities & Transport Hubs

- By Distribution Channel

- Offline Retail

- Showrooms & Specialty Stores

- Home-Improvement Centers

- Online Retail

- Brand Websites

- E-Commerce Marketplaces

- Offline Retail

- By Region

- North America

- Canada

- United States

- Mexico

- South America

- Brazil

- Peru

- Chile

- Argentina

- Rest of South America

- Asia-Pacific

- India

- China

- Japan

- Australia

- South Korea

- South East Asia (Singapore, Malaysia, Thailand, Indonesia, Vietnam, and Philippines)

- Rest of Asia-Pacific

- Europe

- United Kingdom

- Germany

- France

- Spain

- Italy

- BENELUX (Belgium, Netherlands, Luxembourg)

- NORDICS (Denmark, Finland, Iceland, Norway, Sweden)

- Rest of Europe

- Middle East and Africa

- United Arab Emirates

- Saudi Arabia

- South Africa

- Nigeria

- Rest of Middle East and Africa

- North America

Detailed Research Methodology and Data Validation

Primary Research

Mordor analysts interviewed plumbing wholesalers, hospital and airport facility managers, home-builder procurement heads, and R&D engineers across North America, Europe, and Asia. The conversations verified unit prices, retrofit rates, and connectivity preferences that statistics alone could not surface, letting us align regional elasticity assumptions.

Desk Research

We began with public datasets from the World Bank, UN DESA, Eurostat, and national building-permit portals, because population aging, urban housing starts, and water-use regulations shape adoption. Trade flows drawn from UN Comtrade, Japanese and German customs dashboards, and Volza shipment records clarified origin-destination patterns for smart ceramics and control valves. Investor presentations, 10-Ks, and Plumbing Manufacturers International papers fleshed out pricing corridors and capacity additions. D&B Hoovers, Dow Jones Factiva, and Questel patents then helped us map competitive intensity and technology pivots. Please note that these references only illustrate our desk work, and many other open and paid sources contributed to data collection and validation.

Market-Sizing & Forecasting

We applied a top-down model that reconstructs demand from new housing completions, commercial floor-space additions, and premium-sanitary-ware penetration, then cross-checked results with sampled average selling price × volume roll-ups from key suppliers. Urban household formation, wellness-oriented remodeling spend, sensor cost decline, regulatory flush limits, and connected-home device ownership are the main drivers feeding the multivariate regression that underpins the 2025-2030 outlook. Bottom-up channel checks fine-tune anomalies where distributor mark-ups distort headline values.

Data Validation & Update Cycle

Our team triangulates every revision against independent signals, runs variance tests, and submits the workbook to senior peer review before sign-off. Reports refresh every year, with interim updates triggered by material events such as code changes or major product recalls.

Why Mordor's Smart Toilet Market Baseline Stands Reliable

Published estimates often diverge because firms choose different product mixes, price points, and refresh cadences. Gaps typically arise from whether aftermarket seats are counted, how currencies are converted, and whether institutional retrofits are annualized or recorded in lump sums.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 8.57 B | Mordor Intelligence | - |

| USD 10.60 B (2024) | Global Consultancy A | Counts bidet seats and applies straight-line growth without retrofit discount |

| USD 10.70 B | Trade Journal B | Uses single global ASP, ignores wide regional price spread |

Taken together, our disciplined scope selection, variable-driven modeling, and yearly refresh give decision-makers a balanced, transparent baseline they can readily trace and replicate when stress-testing strategies.

Key Questions Answered in the Report

How big is the Smart Toilet Market?

The Smart Toilet Market size is expected to reach USD 9.33 billion in 2026 and grow at a CAGR of 8.85% to reach USD 14.26 billion by 2031.

Which region holds the largest smart toilet market share today?

Europe commands 35.12% of global revenue, bolstered by strict water-efficiency regulations and premium bathroom culture.

Which segment is expanding fastest within the smart toilet industry?

Retrofit smart conversion kits show the quickest pace at a 12.05% CAGR because they offer affordable upgrades without full bathroom renovation.

Why are healthcare facilities adopting smart toilets?

Hospitals and elder-care centers leverage fall-detection, infection-control, and patient-monitoring features to improve safety and reduce caregiver workload.

How are government incentives influencing growth?

State rebates and efficiency mandates lower acquisition costs, accelerating consumer acceptance while advancing water-conservation objectives.

What are the key barriers to wider adoption?

High upfront prices and unresolved data-privacy concerns remain the principal obstacles, especially in price-sensitive and highly regulated markets.

Page last updated on: