Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

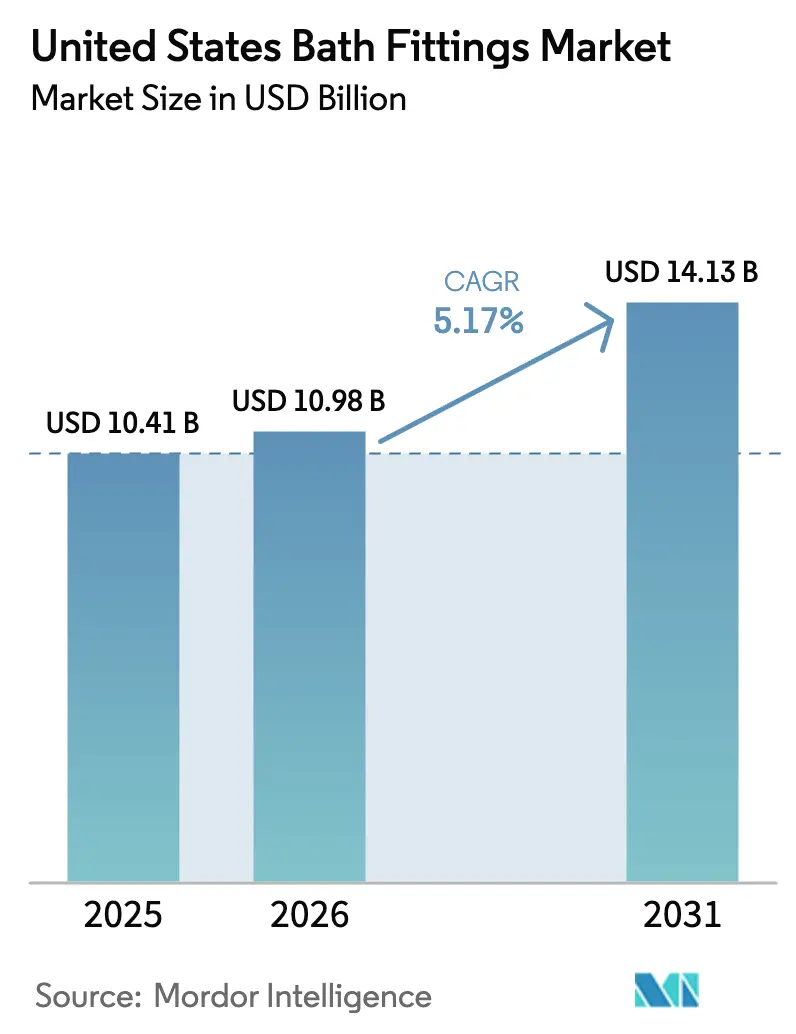

| Base Year Market Size (2025) | USD 10.41 Billion |

| Market Size (2026) | USD 10.98 Billion |

| Market Size (2031) | USD 14.13 Billion |

| Growth Rate (2026 - 2031) | 5.17% CAGR |

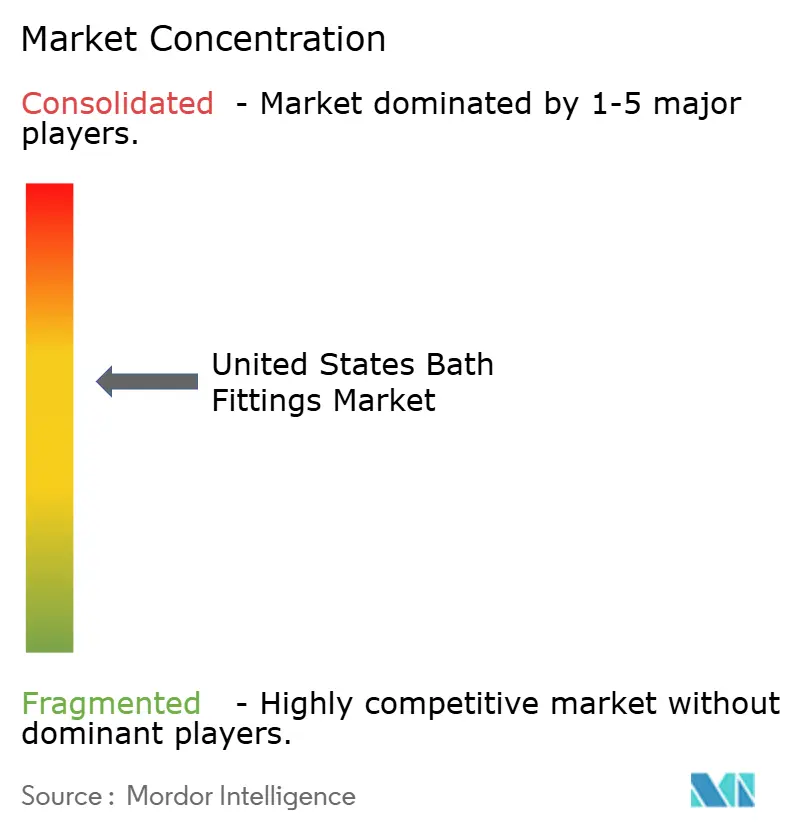

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

United States Bath Fittings Market Analysis by Mordor Intelligence

The United States bath fitting market size was valued at USD 10.41 billion in 2025 and estimated to grow from USD 10.98 billion in 2026 to reach USD 14.13 billion by 2031, at a CAGR of 5.17% during the forecast period 2026-2031. The United States bath fitting market is supported by an aging housing stock that requires systematic fixture replacement, which keeps demand resilient even when construction cycles soften. Regulatory scrutiny also matters, as the EPA’s draft WaterSense 2.0 specification proposed in December 2024 to lower lavatory faucet maximums from 1.5 to 1.2 GPM was paused in February 2025 for a consumer-choice review, adding uncertainty to product roadmaps while signaling further tightening ahead [1]U.S. Environmental Protection Agency, “WaterSense Program and Specifications,” U.S. EPA, epa.gov. State-level standards remain active, with California enforcing 1.8 GPM shower limits that catalyze early adopter replacement cycles and create product differentiation for adaptable flow configurations. Construction activity continues to shape installation volume, as 2025 housing starts of 1.36 million units and completions of 1.50 million units influence specification timing and the mix of fittings specified for multifamily and single-family deliveries [2]U.S. Census Bureau, “New Residential Construction,” U.S. Census Bureau, census.gov.

Key Report Takeaways

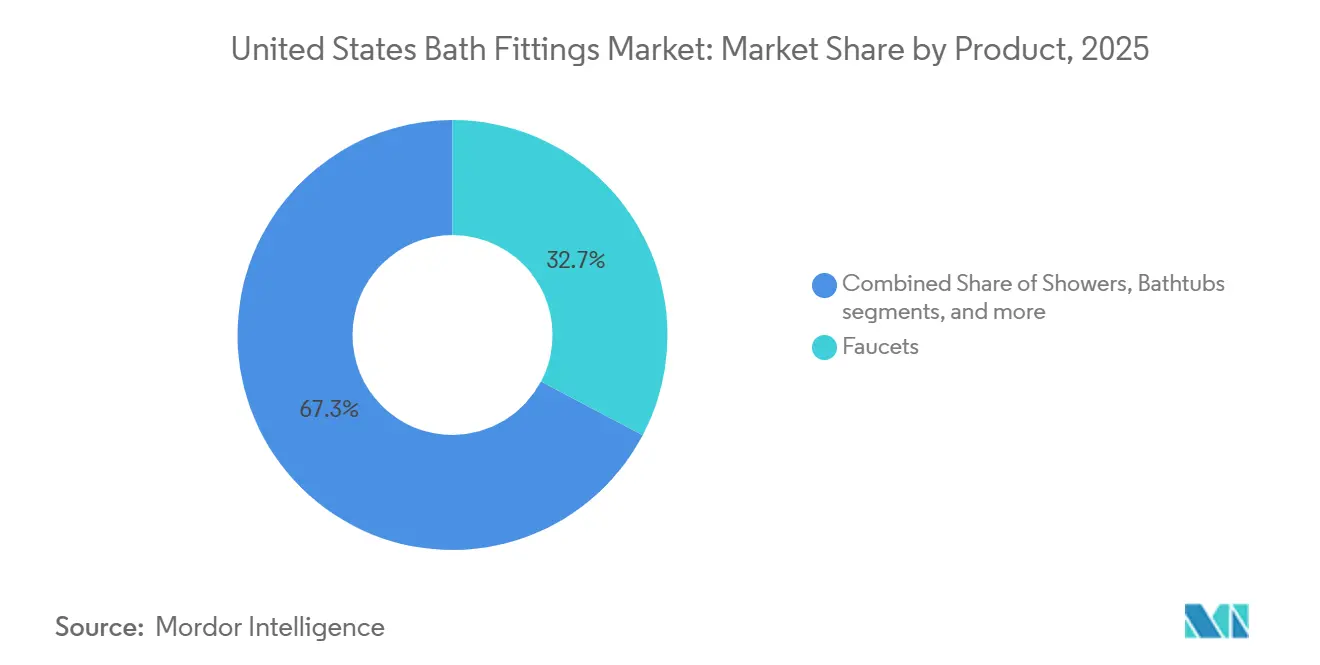

- By product type, faucets led with 32.71% revenue share in 2025 in the United States bath fitting market, while showerheads and systems are forecast to expand at a 6.54% CAGR through 2031.

- By material, chrome-plated brass accounted for a 41.94% share in 2025 in the United States bath fitting market, as stainless steel records the highest projected CAGR at 6.21% to 2031.

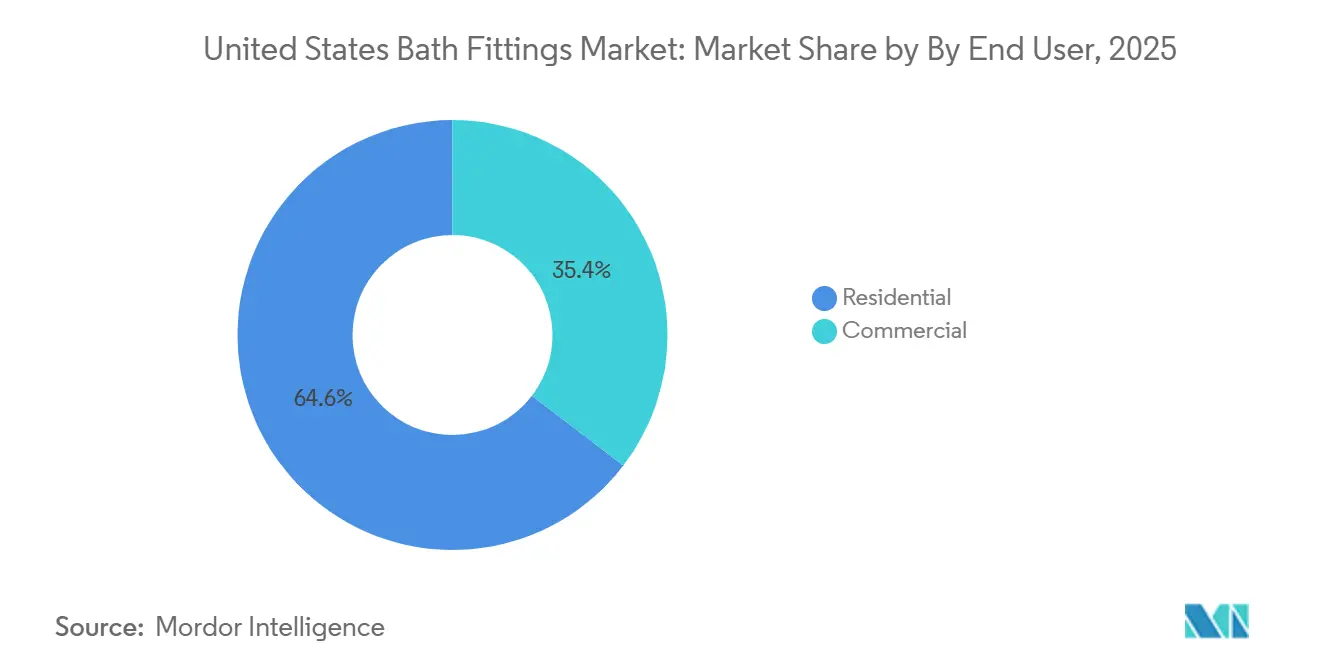

- By end user, residential represented 64.62% of volume in 2025 in the United States bath fitting market, while commercial is projected to grow at a 6.39% CAGR through 2031.

- By distribution channel, B2C captured 58.93% of 2025 sales in the United States bath fitting market, and is advancing at a 5.94% CAGR to 2031.

- By geography, the West region held 41.64% of national revenue in 2025 in the United States bath fitting market, while the South posted the fastest projected growth at a 6.03% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

United States Bath Fittings Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Remodeling and replacement cycle sustains faucet, shower, and fitting upgrades | +1.4% | National, with early gains in Northeast aging-home corridors | Medium term (2-4 years) |

| New residential construction and household formation bolster bath fitting demand | +0.9% | South (Texas, Florida metros), West (Arizona, Nevada) | Short term (≤ 2 years) |

| WaterSense and state flow standards accelerate efficient retrofits | +1.2% | California, Colorado, Oregon; spillover to municipal utilities nationwide | Long term (≥ 4 years) |

| Offline retail and showroom coverage supports premium upselling | +0.7% | West, South urban clusters | Medium term (2-4 years) |

| Legionella/scald risk management drives thermostatic mixing valves in institutions | +0.6% | National, concentrated in healthcare and K-12 retrofits | Long term (≥ 4 years) |

| Insurer-led leak-detection incentives expand smart shutoff adoption | +0.4% | High-loss ZIP codes (Bay Area, coastal Florida, Northeast metros) | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Remodeling and Replacement Cycle Sustains Faucet, Shower, and Fitting Upgrades

A large share of United States owner-occupied homes predates 1980, which means plumbing systems often face age-related leaks, corrosion, and compliance gaps that trigger steady replacement demand independent of new construction cycles. Even when interest rates were elevated in 2025, leading building-product manufacturers reported only a minor moderation in home improvement activity, which underscores the stickiness of functional bath upgrades anchored in safety, compliance, and water savings. EPA’s 2014 lead-free thresholds and ongoing WaterSense labeling discipline have set clearer compliance baselines, nudging homeowners and contractors to prioritize certified fittings when tackling replacements. Local code enforcement at point-of-sale inspections, especially in jurisdictions emphasizing flow and backflow standards, further channels upgrade toward compliant faucet, shower, and valve assemblies. Utilities that combine leak notifications with rebates for efficient fixtures also shorten decision cycles for households sitting on aging plumbing, which supports a durable aftermarket for the United States bath fitting market across economic conditions. Together, these structural factors keep the United States bath fitting market well supplied with replacement-driven opportunities that are less sensitive to short-term changes in building permits.

New Residential Construction and Household Formation Bolster Bath Fitting Demand

United States housing starts totaled 1.36 million units in 2025, and completions reached 1.50 million, which supported a steady cadence of fixture installations across single-family and multifamily projects despite a mixed permitting backdrop. Within the mix, multifamily starts rose 16.6% year over year, while single-family starts contracted by 7.0% in 2025, which guided specification patterns toward mid-tier and code-forward products that are common in higher-density housing. Household formation momentum added 1.2 million net new households in 2024, which sustained baseline bath fitting requirements per unit across the new supply pipeline. Builders and developers increasingly specify WaterSense-labeled faucets and low-flow showerheads to meet certification objectives and unlock utility incentives, tightening the feedback loop between code ambition, rebate programs, and product selection in the United States bath fitting market. Category leaders also report growing sales of sustainable offerings that align with conservation codes and design expectations, which indicates that efficient fixtures continue to capture wallet share even when budgets are guarded. These dynamics, combined with localized distribution and inventory strategies, concentrate near-term upside in metro corridors with active multifamily pipelines and certification-linked project playbooks.

WaterSense and State Flow Standards Accelerate Efficient Retrofits

The EPA’s WaterSense program has delivered cumulative water savings measured in the trillions of gallons since launch, and its December 2024 draft proposal to lower lavatory faucet maximums from 1.5 to 1.2 GPM, though paused in February 2025 for consumer-choice review, continues to shape specification planning among brands and builders. State action proceeds alongside federal deliberations, with California’s 1.8 GPM shower limit and faucet efficiency requirements reinforcing a policy posture that favors early adoption of low-flow fittings and accelerates replacement of still-functional legacy fixtures in regulated metros. Municipal utilities amplify the shift through targeted programs; San Francisco Public Utilities Commission recorded thousands of leak notifications using automated meter data and reinforced conservation with rebates for high-efficiency fixtures and controllers, which nudges households and property managers toward code-aligned retrofits. California’s energy and building code updates require better insulation and durability in exposed piping and outdoor installations, which modestly raise upfront costs while improving life-cycle performance and operational reliability for compliant bath fittings. Drought contingency planning at city utilities, such as staged water shortage protocols, normalizes low-flow selections as a prudent hedge against future restrictions, which increases the speed and breadth of retrofit activity in the United States bath fitting market. As a result, manufacturers with agile portfolios that cover 1.2, 1.8, and 2.5 GPM regimes without retooling delays are better positioned to capture share in policy-forward regions.

Offline Retail and Showroom Coverage Supports Premium Upselling

Showrooms continue to influence mid-to-premium bath fitting purchases by offering working displays, finish comparisons, and technical consultations that help architects, designers, and contractors validate code, accessibility, and integration details before specification. The tactile experience of testing spray patterns and evaluating PVD finishes provides assurance that is hard to replicate online, which helps preserve conversion and margins for coordinated suites in the United States bath fitting market. Regional wholesalers that pair extensive plumbing line cards with operating vignettes give trade professionals a one-stop specification workflow that reduces job-site risk and lead time, which strengthens channel stickiness. Because complex projects rely on correct clearances, mixing valve standards, and backflow integration, showrooms often function as technical clearinghouses as much as sales floors, which supports attachment of higher-value thermostatic controls and accessories in the United States bath fitting market. The ability to deliver next-day from regional distribution centers limits schedule slippage on commercial jobs that carry penalty clauses, which further incentivizes contractors to source through full-service branches and showrooms.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Skilled labor shortages and installer capacity bottlenecks delay projects | -0.7% | National, acute in the Midwest and rural South | Medium term (2-4 years) |

| Strict flow caps constrain high-flow/wellness products in drought states | -0.4% | California, Colorado, Hawaii | Long term (≥ 4 years) |

| Patchwork compliance (federal, state, and standards) raises cost-to-serve | -0.3% | National, with heightened complexity in multi-state distribution territories | Medium term (2-4 years) |

| Weak existing-home sales and financing costs temper mid-market R&R | -0.5% | National, concentrated in price-sensitive suburban markets | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Skilled Labor Shortages and Installer Capacity Bottlenecks Delay Projects

Installer availability remains a pinch point across many metro areas, which stretches project timelines and pushes contractors to triage higher-margin jobs first. Capacity gaps delay discretionary upgrades and slow throughput in complex retrofits that require coordination among plumbers, electricians, and inspectors, which tempers the pace of premium fitting adoption in the United States bath fitting market. Manufacturers are engineering products to reduce install time and maintenance burden, such as self-powered faucets and flush platforms paired with gear-driven ceramic cartridges that outlast conventional solenoids in high-traffic settings. Brands are also investing in trade training and loyalty programs to increase installer proficiency and reduce callbacks, which helps with the smooth adoption of connected and code-intensive categories. As new product platforms integrate electronics and mixing technologies, field training and simplified connection architecture remain critical to overcoming labor bottlenecks and sustaining category growth.

Strict Flow Caps Constrain High-Flow/Wellness Products in Drought States

State-level caps on shower flow rates, such as California’s 1.8 GPM limit, set a regulatory ceiling that curtails wellness-positioned high-flow experiences and forces design compromises in hospitality and luxury residential projects. This constraint compels manufacturers to advance dual-mode and recirculation designs that deliver a satisfying experience while meeting code, which requires more R&D and raises bill-of-materials costs relative to single-mode options [3]Kohler Co., “KBIS 2026 Press Materials,” Kohler Co., kohlercompany.com. Industry associations are investing in nozzle and spray innovation to maintain perceived performance within lower flow envelopes, which, over time, can ease the compliance-experience tradeoff in the United States bath fitting market. In the near term, distributors that operate across multiple states must manage parallel SKUs to align with local codes, which complicates inventory and working capital. These operational and engineering realities temper the near-term upside of premium, high-flow configurations in drought-exposed markets while incentivizing a pipeline of water-saving innovation.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Shower Systems Outpace Faucets in Growth

Faucets dominated with 32.71% of 2025 revenue, yet they are projected to grow at only 4.9% CAGR through 2031, while showerheads and systems are expected to advance at 6.54% CAGR over the same period. This mix reflects how the United States bath fitting market has pivoted toward wellness-oriented remodels and specification-grade commercial upgrades that favor multi-function showers and integrated valve controls. Homeowners and facility managers value digital presets, thermostatic safety, and consistent temperature delivery, which support upgrades beyond commodity faucet swaps in the United States bath fitting market. Smart shower controllers and water-saving modes are gaining visibility through design showcases and trade events, and the feature sets cater to both performance and conservation tendencies in water-stressed regions. Drainage and waste fittings are also part of the conversation as local codes encourage gray water readiness in some jurisdictions, which increases interest in compliant assemblies and installation practices for system-level efficiency.

System-level orchestration is reshaping how buyers evaluate bath solutions since coordinated suites across faucets, showers, and valves command higher attachment and streamline maintenance. Leading brands are extending ecosystem approaches to unify control, conserve water, and simplify installation, which helps differentiate offerings in mid-to-premium price bands in the United States bath fitting market. In commercial projects with strict hygiene and uptime requirements, touchless activation paired with thermostatic mixing creates safety and operational benefits that align with facility protocols. Because building owners often prefer predictable service intervals and standardized parts across floors or properties, comprehensive shower systems and matched faucet lines help compress service complexity and reduce stock-keeping units. As multi-function showers gain traction, faucet categories continue to refresh with sensor and voice-enabled options, but relative growth tilts toward configurations that deliver an integrated experience.

By Material: Stainless Steel Gains on Lead-Free Compliance Tailwinds

Chrome-plated brass captured 41.94% of the share in 2025, and while it remains cost-advantaged and familiar with installers, it is projected to trail stainless steel's 6.21% CAGR through 2031 as stainless gains from compliance and corrosion resistance advantages. Tighter enforcement of lead content thresholds under standards such as NSF/ANSI 372 has made stainless steel attractive for public projects and coastal installations, since it avoids dezincification concerns associated with some brass alloys in aggressive water conditions. In marine air or high-chloride municipal water, 316-grade stainless resists pitting and stress corrosion, which reduces warranty exposure and lifecycle costs for owners and operators. This performance edge aligns with the United States bath fitting market’s drift toward durable, code-forward materials that satisfy both environmental and safety criteria under city and state rules.

Coating technologies are also advancing the appeal of premium metals, with PVD finishes extending scratch and tarnish resistance beyond standard electroplated chrome. That durability helps justify higher price points in commercial venues and upscale residential projects, where abrasion and cleaning chemicals can degrade lesser finishes. As fixture lifespans stretch under stricter water treatment and maintenance regimens, owners value material and finish integrity that preserves appearance and performance. Stainless steel’s ability to bridge cost of ownership, compliance comfort, and aesthetic versatility positions it to keep taking incremental share within the United States bath fitting market over the forecast period [4]Plumbing Manufacturers International, “Lead Content Compliance and Standards,” Plumbing Manufacturers International, safeplumbing.org.

By End User: Commercial Installations Outgrow Residential on Code-Driven Retrofits

Residential applications represented 64.62% of volume in 2025 and are projected to grow at a 5.0% CAGR to 2031, while commercial installations are expected to expand at a 6.39% CAGR over the same period, supported by code-mandated hygiene and safety retrofits. Public washrooms, hospitals, and elder-care facilities emphasize touchless activation and thermostatic mixing to meet scald prevention and infection control standards, which tilts specifications to certified valves and sensor faucets. State-level requirements for touchless operations in specific applications further reinforce this direction and expand the installed base of compliant fittings. In that context, new product families that blend sensor activation, onboard temperature control, and connected diagnostics are building share due to facility demands for compliance visibility and lower maintenance effort.

The residential segment remains the larger volume base, but the commercial pipeline delivers steadier, mandate-driven demand that is less tied to consumer confidence. Code alignment often unlocks capital budgets for public and private institutions, which sustains recurring replacement cycles at multi-year intervals. As landlords and operators pursue certification and rebate pathways, their procurement teams prioritize proven performance and documentation, which supports brand incumbency in the United States bath fitting market. Residential upgrades continue to integrate touchless and water-saving features as homeowners adopt best practices from commercial venues, yet price bands and installation needs vary widely. Over time, commercial specifications tend to seed design and technology roadmaps for residential lines, which helps elevate baseline performance and spreads cost improvements across portfolios.

By Distribution Channel: Online Retail Erodes Showroom Share but Not Premium Conversion

B2C channels, including retail and online, captured 58.93% of 2025 sales and are forecast to grow at a 5.94% CAGR through 2031; B2B distribution holds the remaining 41.07%. Digital discovery and configurators have improved finish and feature selection for consumers and pros, which increases the credibility of online transactions for commodity faucet and accessory categories in the United States bath fitting market. At the upper end of the price spectrum, showrooms remain central because working displays and technical consultations reduce mis-specification risk and support bundled purchases with thermostatic valves and accessories. This channel split creates an omnichannel imperative for brands to synchronize assortments and pricing across online and offline partners to avoid cannibalization while protecting premium conversion.

Manufacturers are also using direct programs and owner communities to nurture post-purchase engagement and education, which increases satisfaction and eases future upgrade paths. For complex systems, contractors and designers still prefer showrooms and trade counters that can provide immediate parts, service guidance, and code confirmation. That hybrid approach gives distributors the ability to support project timelines while retaining margin on consultative selling, which keeps the United States bath fitting market balanced between convenience-led online growth and expertise-driven offline conversion. As connected fixtures scale, service expectations rise in tandem, and channels that can deliver both product and support remain the most defensible.

Geography Analysis

The West region held 41.64% of national revenue in 2025, reflecting the combined effect of stringent water-efficiency codes, higher median home values, and active municipal rebate programs that quicken retrofit cycles. California’s 1.8 GPM shower standard and related faucet requirements have set early benchmarks that translate into brisk replacement of legacy fixtures that exceed current thresholds. Cities such as San Francisco reinforce these standards through water-use monitoring and rebates for high-efficiency fixtures, which increases the pace of upgrades in older housing stock and larger commercial properties. Coastal code practices also influence material specifications near seawater, where 316-grade stainless steel improves durability against corrosion and reduces lifecycle maintenance in exposed installations. The region’s regulatory posture and premium housing mix sustain strong penetration for low-flow and specification-grade fittings in the United States bath fitting market.

The South is the fastest-growing region with a projected 6.03% CAGR through 2031, buoyed by sustained in-migration and active multifamily development across major Texas and Florida metros. That density favors mid-tier faucet and shower system specifications where balance among cost, performance, and code compliance is essential. As developers move to standardize product families across communities and floor plans, the region benefits from reliable volume for builders’ grade and mid-premium lines in the United States bath fitting market. While insurance dynamics can slow certain coastal high-rise projects, broad single-family and garden-style multifamily activity supports ongoing demand for efficient and durable bath fittings. Builder preferences for simplified installation and reliable service partners also strengthen ties to established distributors with strong logistics footprints.

The Midwest and Northeast together accounted for about one-third of 2025 sales, and both regions lean on replacement cycles tied to older housing stock that still dominates many markets. The Northeast’s aging homes concentrate opportunity in lead-compliant, corrosion-resistant fixtures, while heating-dominated climates make durability and maintenance access central to product choice. Institutional retrofits in education, healthcare, and government are important to both regions due to well-established public building inventories that must meet scald prevention and hygiene management standards. Distributors with showrooms and regional distribution centers that can meet stringent schedule and specification needs maintain an edge, which underscores the importance of omnichannel support in the United States bath fitting market.

Competitive Landscape

The United States bath fitting market features several national brand families with deep distribution and specification footprints, which creates a moderate concentration profile across residential and commercial channels. Strategic updates in 2025 and 2026 highlight how leading brands are consolidating portfolios and scaling platforms to serve code-driven demand and connected product adoption. Masco integrated Liberty Hardware into Delta Faucet Company under a group leadership structure to leverage shared strengths across decorative and functional categories, which signals tighter brand alignment for kitchen and bath remodels. LIXIL Americas formed a strategic partnership with American Bath Group to manufacture and distribute bathing products under American Standard, DXV, and Eljer, which reorients production and distribution capacity for core brands while sharpening the focus on high-performance toilets and fittings. These moves reinforce brand presence where code compliance, durability, and after-sales support determine the short list in the United States bath fitting market.

Suppliers serving institutional and non-residential end uses also pressed their advantage with platform expansions and acquisitions that deepen code-forward portfolios. Watts Water Technologies reported record 2025 results and completed acquisitions of Haws Corporation, Superior Boiler, and Saudi Cast in November 2025, which broadened its reach in specified, safety-critical products. Zurn Elkay reported progress against sustainability commitments and advanced connected water solutions across flush and faucet platforms, which are aligned with facility demands for reliability and lower maintenance. Chicago Faucets showcased a pipeline of touchless, thermostatic, and turbine-powered solutions with options tuned to low-flow requirements, which map directly to institutional usage and conservation targets. Kohler continued to emphasize sustainable design and WaterSense leadership in 2024 and 2026 showcases, which boost appeal for projects that weigh environmental credentials alongside performance. Together, these strategies reinforce the hold that established manufacturers have in the most code-sensitive portions of the United States bath fitting market.

Channel execution remains a competitive lever as brands balance online assortment reach with showroom and trade-counter strength. Regional wholesalers with broad line cards and operating vignettes help contractors and designers validate fit, finishes, and standards compliance before specification, which protects premium conversion where working displays and advice matter. Showrooms’ role as technical intermediaries between product engineering and job-site realities keeps them central for complex projects with ADA and ASSE requirements. At the same time, brand-owned programs and communities foster owner education and loyalty, which supports future upgrade cycles for connected and sustainable fixtures. Against this backdrop, innovation cadence, code fluency, and after-sales support remain core differentiators in the United States bath fitting market, especially in institutional retrofits and high-spec residential projects.

United States Bath Fittings Industry Leaders

Fortune Brands Innovations (Moen, House of Rohl)

Masco Corporation (Delta, Brizo, Peerless)

Kohler Co.

LIXIL (American Standard, Grohe)

Pfister (ASSA ABLOY)

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2026: Kohler showcased its "Step into Possibility" exhibition at KBIS 2026, unveiling the Claude smart toilet with furniture-inspired form, the Anthem EvoCycle Smart Shower delivering up to 80% water savings in recirculating Cycle Mode, and the industry-first Dekoda toilet-attached health-sensing system tracking hydration and gut health markers. The WasteLAB Vox sink, now available in Eggshell finish and fabricated from over 70% recycled materials, reinforces Kohler's circular-economy positioning.

- November 2025: Watts Water Technologies completed acquisitions of Haws Corporation (November 4), Superior Boiler (November 14), and Industrial Company for Castings and Sanitary Fittings ("Saudi Cast," November 29), collectively expanding product portfolio and geographic reach in institutional plumbing.

- April 2025: LIXIL Americas formed a strategic partnership with American Bath Group, granting exclusive rights to manufacture and distribute bathing products under the American Standard, DXV, and Eljer brands across North America. The agreement included the transfer of LIXIL's Ohio manufacturing facility and assets from Monterrey, Mexico, and Mansfield, Ohio, locations, refining LIXIL's portfolio to prioritize high-performance toilets and fittings.

- October 2024: Chicago Faucets showcased its 2024 ASPE Innovations at the ASPE Expo in Columbus, Ohio, including the EQ Arc water-turbine powered touchless faucet with Econo-Flo options (0.35, 0.50, 1.0 GPM), the E-Tronic 80 Series touchless faucet with Bluetooth and ASSE 1070 thermostatic protection, and the EVR Series vandal-resistant touchless faucet with integrated long-term power supply.

United States Bath Fittings Market Report Scope

Bath fittings are one of the most widely demanded products as people are adopting urbanization. A complete background analysis of the United States Bath Fitting Market includes an assessment of the economy, market overview, market size estimation for key segments, emerging trends in the market, market dynamics, and key company profiles covered in the report. The United States Bath Fitting Market Report is Segmented by Product Type (Faucets, Showerheads & Systems, Bathtub & Spa Fittings, Toilet Fittings, and Drainage Fittings), Material (Chrome-Plated Brass, Stainless Steel, Plastic, and Other Metals), End User (Residential, Commercial, and Institutional), Distribution Channel (B2C and B2B), and Geography (Northeast, Midwest, South, and West). The Market Forecasts are Provided in Terms of Value (USD).

By Product Type

| Faucets |

| Showerheads & Systems |

| Bathtub & Spa Fittings |

| Toilet Fittings & Accessories |

| Drainage & Waste Fittings |

By Material

| Chrome-Plated Brass |

| Stainless Steel |

| Plastic (ABS, PVC) |

| Other Metals (Bronze, Copper) |

By End User

| Residential |

| Commercial |

| Institutional (Education, Government) |

By Distribution Channel

| B2C | Multibrand Stores |

| Exclusive Stores | |

| Online | |

| Other Distribution Channels | |

| B2B (Direct & Project Sales) |

By Geography

| Northeast |

| Midwest |

| South |

| West |

| By Product Type | Faucets | |

| Showerheads & Systems | ||

| Bathtub & Spa Fittings | ||

| Toilet Fittings & Accessories | ||

| Drainage & Waste Fittings | ||

| By Material | Chrome-Plated Brass | |

| Stainless Steel | ||

| Plastic (ABS, PVC) | ||

| Other Metals (Bronze, Copper) | ||

| By End User | Residential | |

| Commercial | ||

| Institutional (Education, Government) | ||

| By Distribution Channel | B2C | Multibrand Stores |

| Exclusive Stores | ||

| Online | ||

| Other Distribution Channels | ||

| B2B (Direct & Project Sales) | ||

| By Geography | Northeast | |

| Midwest | ||

| South | ||

| West | ||

Key Questions Answered in the Report

What is the current size and projected growth of the United States bath fitting market?

The United States bath fitting market size was valued at USD 10.41 billion in 2025 and estimated to grow from USD 10.98 billion in 2026 to reach USD 14.13 billion by 2031, at a CAGR of 5.17% during the forecast period 2026-2031.

Which product categories are growing fastest in the United States bath fitting market?

Showerheads and systems are projected to expand at a 6.54% CAGR through 2031, outpacing faucets that grow at 4.9% over the same period.

Which regions lead demand in the United States bath fitting market?

The West led with 41.64% of 2025 revenue, while the South is the fastest-growing region with a projected 6.03% CAGR through 2031.

How are regulations influencing the United States bath fitting market?

EPA WaterSense proposals and state codes like California’s 1.8 GPM shower limit are prompting efficient retrofits and accelerating replacement of legacy fixtures that exceed thresholds.

What end users are driving upgrades in the United States bath fitting market?

Institutional and commercial settings emphasize touchless operation and thermostatic mixing for hygiene and scald control, which supports higher-spec fittings, while residential remains the larger volume base.

Which materials are gaining share in the United States bath fitting market and why?

Stainless steel is gaining on chrome-plated brass due to lead-free compliance, comfort, and corrosion resistance advantages, especially in coastal and high-chloride environments.

Page last updated on: