Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

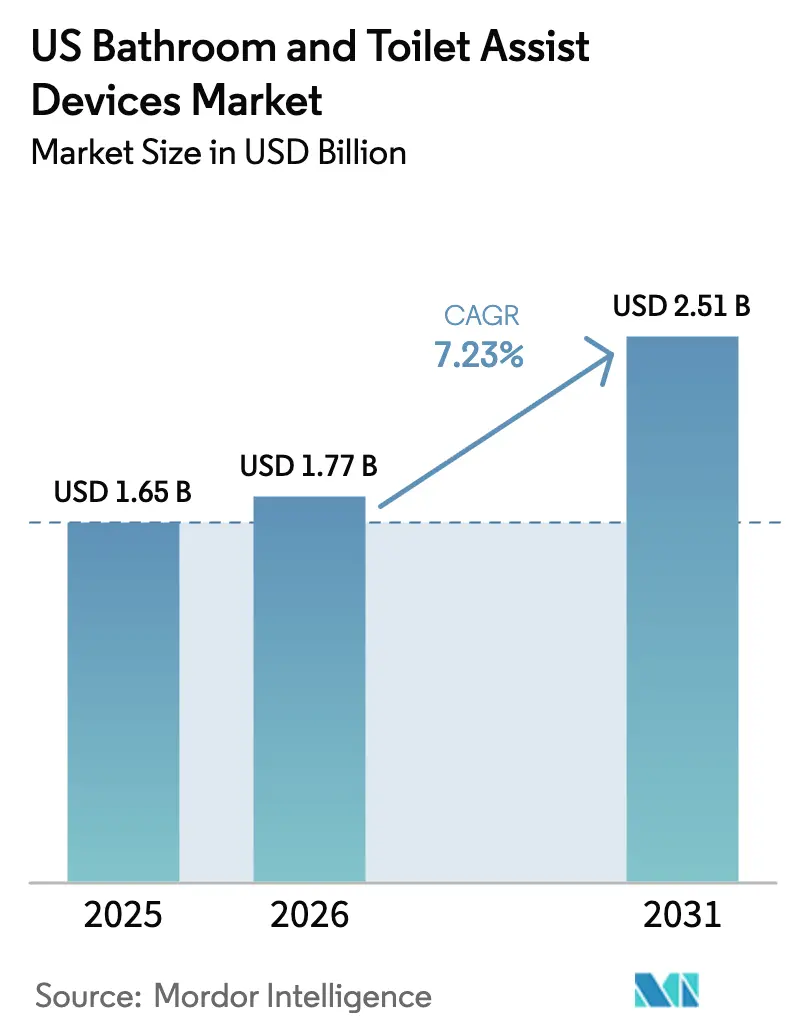

| Base Year Market Size (2025) | USD 1.65 Billion |

| Market Size (2026) | USD 1.77 Billion |

| Market Size (2031) | USD 2.51 Billion |

| Growth Rate (2026 - 2031) | 7.23% CAGR |

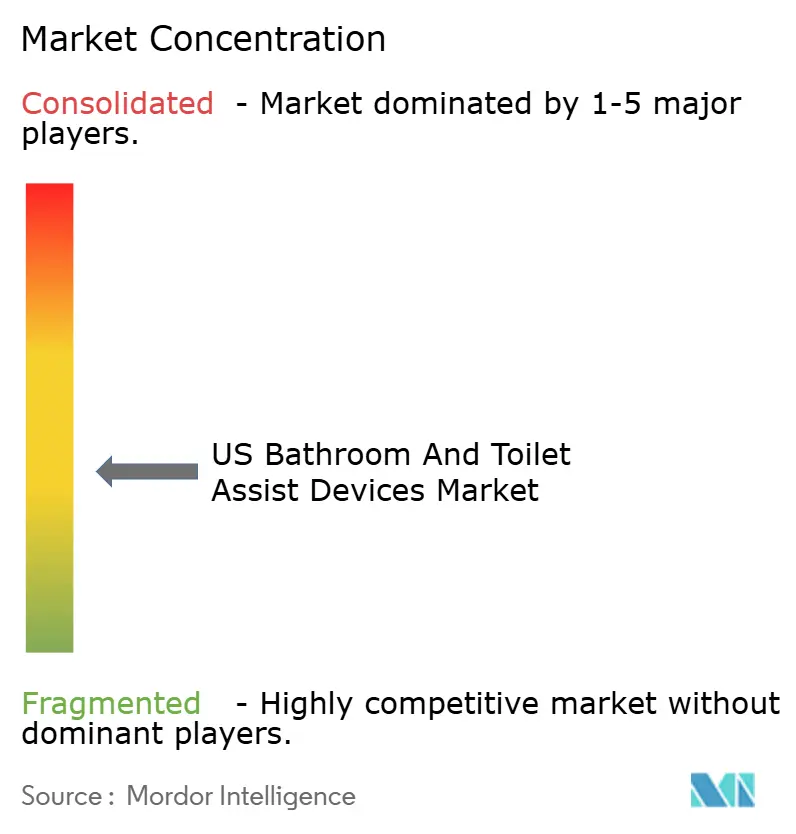

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

US Bathroom And Toilet Assist Devices Market Analysis by Mordor Intelligence

The bathroom assist devices market size in the United States market size in 2026 is estimated at USD 1.77 billion, growing from 2025 value of USD 1.65 billion with 2031 projections showing USD 2.51 billion, growing at 7.23% CAGR over 2026-2031. This expansion is propelled by rapid population aging, the shift toward home-based care, and targeted federal funding that offsets out-of-pocket costs for safety modifications. Medicaid Home and Community-Based Services (HCBS) waivers, the Department of Veterans Affairs’ adaptive-housing grants, and expanding Medicare Advantage benefits are funneling capital directly into residential retrofits. Manufacturers are responding with lightweight aluminum frames that comply with new weight-bearing tests, antimicrobial surface treatments that satisfy infection-control policies, and digitally connected devices that support remote monitoring. The bathroom assist devices market is also benefiting from value-based reimbursement models that reward hospitals and payers for preventing fall-related readmissions.

Key Report Takeaways

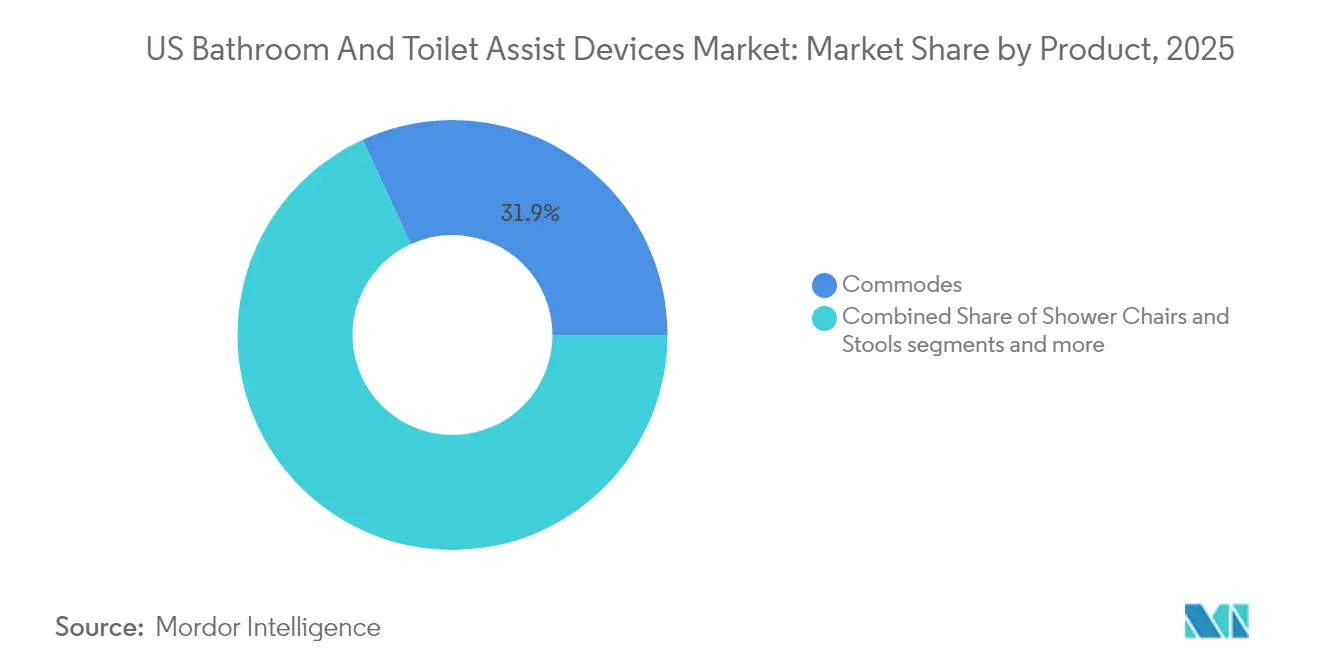

- By product type, commodes led with 31.86% of bathroom assist devices market share in 2025, while bath lifts are projected to post the fastest 9.46% CAGR through 2031.

- By end use, the residential segment held 65.58% of the bathroom assist devices market size in 2025 and is set to grow at an 8.63% CAGR to 2031.

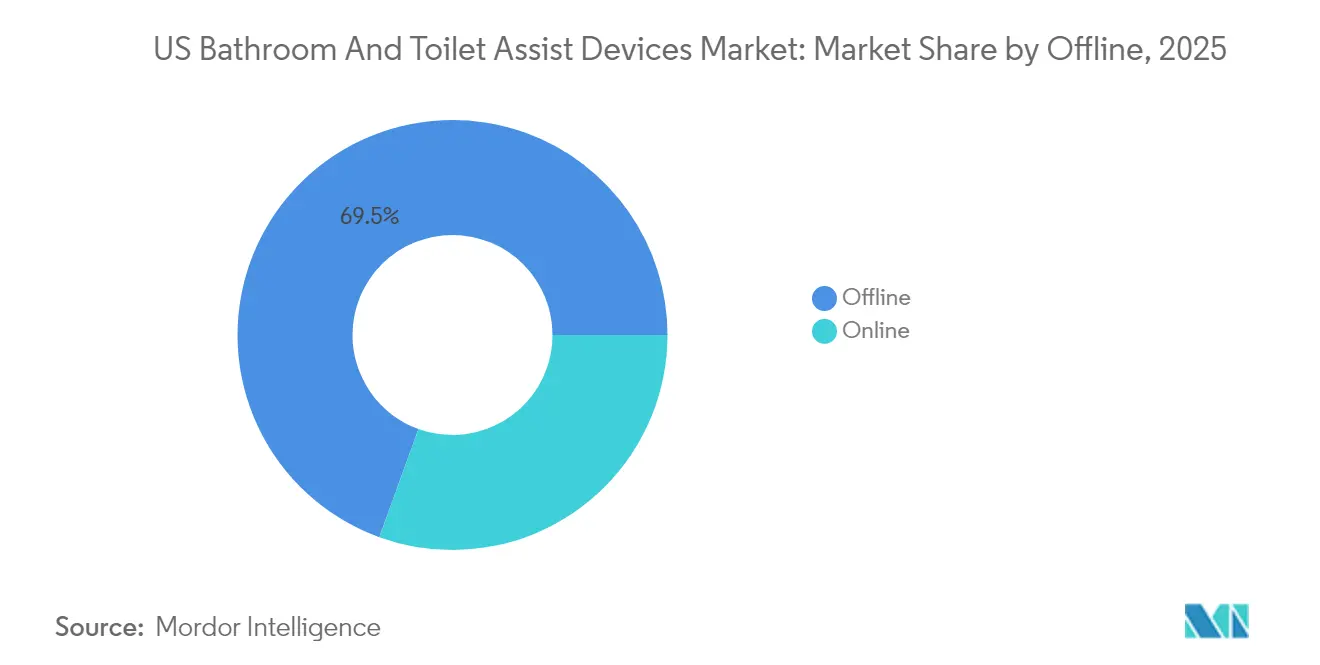

- By distribution channel, offline outlets retained 69.47% revenue share in 2025, whereas online sales are forecast to expand at an 10.72% CAGR through 2031.

- By material composition, plastic accounted for 47.62% of revenue in 2025; aluminum is the fastest-growing material at 9.18% CAGR to 2031.

- By region, the Northeast commanded 32.21% revenue in 2025 and is projected to accelerate at 10.94% CAGR, the highest among all regions.

- Drive DeVilbiss Healthcare, Etac AB, Invacare Corporation, and ArjoHuntleigh together represented the bulk of branded volume in 2024, with Invacare’s North American sale to MIGA Holdings LLC signaling further consolidation.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

US Bathroom And Toilet Assist Devices Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising Prevalence of Mobility-Related Conditions | +1.8% | National, concentrated in Northeast and Southeast | Long term (≥ 4 years) |

| Government Initiatives and Regulations Promoting Adoption | +1.5% | National, with state-level variations | Medium term (2-4 years) |

| Home-Based Care and Aging in Place | +1.2% | National, stronger in suburban areas | Long term (≥ 4 years) |

| Insurance Reimbursement via Medicaid HCBS Waivers | +0.9% | State-dependent, strongest in expansion states | Medium term (2-4 years) |

| Surge in VA Adaptive-Housing Grants | +0.6% | National, concentrated near military installations | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Rising Prevalence of Mobility-Related Conditions

One-third of households with older adults reported an accessibility need in 2024, reflecting the growing burden of chronic disease and post-surgical rehabilitation. Sixty percent of seniors live with two or more chronic conditions that often impair activities of daily living. The Food and Drug Administration classifies many mechanical supports, including transfer chairs, as Class I devices exempt from pre-market notification, ensuring a streamlined supply pathway. Hospitals operating under value-based payment contracts increasingly prescribe bathroom safety equipment to avoid costly readmissions. The bathroom assist devices market therefore receives stable demand from both clinical and consumer channels as clinicians integrate assist devices into discharge plans.

Government Initiatives and Regulations Promoting Adoption

Federal and state programs have elevated accessibility from a consumer option to a compliance mandate. The Specially Adapted Housing Assistive Technology Grant Program can now disburse up to USD 200,000 annually to qualifying innovators. Alaska’s Medicaid waiver funds environmental modifications up to USD 18,500 every three years. Americans with Disabilities Act audits continue to drive institutional retrofits. At the payer level, Medicare Advantage plans expand coverage for home safety products deemed medically necessary, lowering direct costs for older adults. As states add environmental-modification benefits to HCBS waivers, the bathroom assist devices market experiences a direct infusion of reimbursable demand.

Home-Based Care and Aging in Place

Aging-in-place has shifted from personal preference to national policy priority. Only 10% of U.S. homes are currently age-friendly, triggering a surge of retrofit projects[1]Administration for Community Living, “2022 Profile of Older Americans,” acl.gov . Smart sensors integrated into bath lifts and grab bars support remote monitoring, allowing caregivers to verify safe usage without intrusive supervision. Fall-related injuries cost the healthcare system billions each year, so payers view proactive bathroom modifications as essential. Consequently, the bathroom assist devices market aligns closely with broader home-health strategies focused on cost containment and patient autonomy.

Insurance Reimbursement via Medicaid HCBS Waivers

State Medicaid programs now allocate meaningful budget lines for environmental adaptations. Minnesota’s Environmental Accessibility Adaptations benefit extends up to USD 40,000 annually for specific waivers[2]Minnesota Department of Human Services, “Environmental Accessibility Adaptations Policy,” mn.gov. Applications typically move through a 6-to-12-month cycle, creating predictable production windows for manufacturers. Managed care organizations standardize product specifications, favoring vendors with proven quality histories. Because waivers explicitly reference bathroom safety products, the bathroom assist devices market enjoys recurring, policy-driven purchasing momentum in waiver-expansion states.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Tightening FDA Weight-Bearing Certification Tests | -0.8% | National, affecting all manufacturers | Short term (≤ 2 years) |

| Raw-Material Price Volatility (Aluminum and Plastics) | -0.6% | National, concentrated in manufacturing regions | Medium term (2-4 years) |

| Low Consumer Awareness Beyond Grab Bars and Risers | -0.5% | National, stronger in rural areas | Medium term (2-4 years) |

| Competitive Gray-Market Imports (Non-ANSI/RESNA) | -0.4% | National, concentrated in price-sensitive segments | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Tightening FDA Weight-Bearing Certification Tests

The FDA has intensified scrutiny of third-party laboratories after uncovering data-integrity lapses, subjecting non-compliant shipments to detention without physical examination. New guidance on biocompatibility and static-load testing requires extensive documentation under 21 CFR Part 880, escalating compliance costs. Established manufacturers with ISO-certified quality systems can absorb these expenses, while new entrants face higher barriers. As a result, the bathroom assist devices market may experience slower product introductions until suppliers recalibrate their testing pipelines.

Raw-Material Price Volatility (Aluminum and Plastics)

Polyethylene prices climbed 3 cents per pound in 2024, while polypropylene retreated by 2 cents, exemplifying the uncertainty facing device makers. Supply-chain realignments designed to shorten lead times have pushed labor costs upward. Because medical-grade resins and aircraft-grade aluminum have few viable substitutes, sudden price swings directly compress margins. Some manufacturers hedge with long-term supply contracts, but smaller firms may respond by passing costs to end customers, tempering adoption among price-sensitive buyers.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Mechanized Aids Outpace Static Fixtures

In revenue terms, commodes captured 31.86% of bathroom assist devices market share in 2025, anchoring the category through brand familiarity and prescriber confidence. Enhanced anti-microbial coatings and tool-free height adjustments have expanded commode adoption beyond institutional settings. Bath lifts, although inherently higher in price, are expanding at a 9.46% CAGR, reflecting rising bariatric demand and safer lithium-ion battery systems. Drive DeVilbiss Healthcare’s Bellavita Nova illustrates how regional manufacturing and 30-minute installation appeal to contractors and caregivers alike. Grab bars and handgrips remain volume staples, but heightened commoditization encourages vendors to bundle them with sensors that detect abnormal traction forces.

Toilet seats incorporating bidet functionality respond to hygiene concerns, bridging traditional assist devices with smart bathroom ecosystems. Collectively, these innovations signal that the bathroom assist devices market is pivoting from mechanical aids to integrated safety solutions. Second-generation products emphasize remote diagnostics, enabling clinicians to adjust lift speeds or lock commode casters through mobile apps. The bathroom assist devices market size for bath lifts is projected to expand steadily as veterans receive higher grant ceilings for lift installations. Meanwhile, shower chairs add quick-drain seat perforations that reduce water pooling and infection risk.

By End Use: Residential Installations Sustain Growth Momentum

Residential applications controlled 65.58% of revenue in 2025, underpinned by the nation’s aging-in-place movement. Homeowners favor low-profile, tool-free designs that blend with contemporary décor. Many manufacturers now offer color-matched grab bars that complement faucet finishes, solving historical stigma barriers. Institutional buyers—hospitals, skilled-nursing facilities, and veteran centers—procure through three-to-five-year capital cycles, emphasizing durability and infection control. Under CMS Minimum Data Set 3.0, facilities must document individualized toileting plans, guaranteeing baseline demand for transfer benches and bariatric commodes.

Telehealth expansion allows therapists to prescribe bathroom safety products remotely, accelerating residential throughput. The bathroom assist devices market size allocated to direct-pay consumers is set to grow as Medicare Advantage and Medicaid waivers broaden eligibility for in-home modifications. Conversely, institutional budgets remain relatively flat, prompting suppliers to offer rental programs that convert capital expenses into operating expenditures. As a result, the bathroom assist devices market continues to segment along functionality lines: aesthetic flexibility for homes versus industrial specification for care facilities.

By Distribution Channel: Digital Acceleration Redefines Consultation

Offline distributors maintained 69.47% of revenue in 2025 by coupling product selection with professional installation. However, online platforms grew at double-digit rates, aided by e-commerce portals that verify Medicare numbers during checkout. Amazon’s accredited DME storefront illustrates how frictionless reimbursement boosts conversion among older adults. Some manufacturers pilot “click-to-contractor” models in which customers purchase online and schedule certified installers within 48 hours.

Hybrid fulfillment now dominates big-ticket items: consumers research bath lifts online, but final purchase occurs through local dealers who manage in-home fitting. The bathroom assist devices market benefits from this omnichannel integration, which blends digital convenience with clinical oversight. Suppliers that invest in augmented-reality apps enabling customers to visualize grab-bar placement on a smartphone screen are achieving higher close rates. Consequently, logistics partners that can deliver bulky products within narrow time windows gain competitive leverage as last-mile experience becomes part of brand value.

By Material Composition: Aluminum Innovation Gains Ground

Plastic retained 47.62% revenue in 2025, buoyed by cost advantages and color versatility. Yet the FDA’s weight-bearing focus elevates aluminum, which is advancing at 9.18% CAGR thanks to superior structural integrity. Hospital purchasing teams also favor aluminum for its recyclability, aligning with internal carbon-reduction targets advocated by the Georgetown Climate Center. Composite materials marry carbon-fiber stiffness with polymer flexibility, targeting high-end residential users, although regulatory validation costs remain high.

Aluminum’s momentum is further reinforced by high-capacity lifts designed for bariatric patients. The bathroom assist devices market size tied to aluminum framed commodes could grow faster if commodity spot prices stabilize. Some vendors anodize aluminum frames in matte black to match modern fixtures, demonstrating how aesthetics now complement safety. Resin suppliers, meanwhile, develop anti-yellowing additives to extend plastic product lifespans, maintaining relevance in price-sensitive segments.

Geography Analysis

The Northeast remains the focal point for the bathroom assist devices market, commanding 32.21% revenue in 2025 and outpacing all regions at 10.94% CAGR through 2031. High urban density, aging infrastructure, and generous state-level waivers amplify retrofit demand, especially for multistory brownstones lacking ground-floor bathrooms. Maryland’s Environmental Modification program funds grab bars, roll-in showers, and alarm systems, sustaining contractor pipelines. Institutional demand concentrates around teaching hospitals and rehabilitation centers, which upgrade transfer benches and lift systems to comply with evolving CMS safety metrics.

Sunbelt states in the Southeast and Southwest exhibit rising potential as retirement inflows swell senior populations. Florida’s condominium associations increasingly mandate universal-design elements in renovation bylaws, bolstering premium shower seat installations. Texas combines extensive veterans’ facilities with sprawling suburban housing, generating hybrid demand that spans residential and institutional procurement. Rapid housing starts allow builders to integrate blocking for future grab-bar placement, embedding bathroom assist devices market opportunities into new construction cycles.

The Midwest and West reveal contrasting drivers. In the Midwest, local fabrication shortens lead times for aluminum frames and custom-cut rails, appealing to hospital systems pressed for capital project deadlines. The West Coast prioritizes sustainability; healthcare alliances use ecolabel purchasing criteria that reward recyclable materials. California’s CalAIM waiver finances accessibility modifications up to USD 7,500, seeding a substantial baseline of funded projects even within a lifetime cap context. Tech adoption also runs higher, with Silicon Valley start-ups co-designing sensor-equipped shower stools, reinforcing the bathroom assist devices market’s convergence with digital health.

Competitive Landscape

The bathroom assist devices market exhibits moderate concentration. Drive Medical, Etac AB, Invacare Corporation, and Arjo dominate through broad catalogs and deep distribution. Drive Medical offers more than 200 SKUs spanning raised toilet seats, bath benches, and bariatric commodes, enabling cross-selling to group-purchasing organizations. Etac leverages Scandinavian ergonomics to differentiate its Molift transfer solutions. Arjo’s 2024 European acquisitions added rental diagnostics units, allowing U.S. customers to trial products before capital purchase.

Technology integration now defines competitive edges. Leading manufacturers embed Bluetooth modules that transmit lift-cycle counts, guiding preventive maintenance scheduling for long-term care operators. Veterans Affairs grants increasingly favor bids that include remote-monitoring features, steering procurement toward tech-enabled incumbents. Smaller niche players emphasize bespoke aesthetics for high-end residential bathrooms, but stringent FDA documentation may limit scale. Suppliers with vertically integrated U.S. plants mitigate tariff exposure, appealing to distributors wary of gray-market imports that lack ANSI/RESNA certification.

Regulatory compliance functions as a strategic moat. The FDA’s heightened oversight strains firms lacking ISO 13485 accreditation. Companies investing in automated tensile-test rigs and digital traceability secure smoother 510(k) submissions, reducing time-to-market. Consequently, the bathroom assist devices market tilts toward players with both engineering depth and policy fluency, even as e-commerce opens front-end channels for smaller brands.

US Bathroom And Toilet Assist Devices Industry Leaders

Drive DeVilbiss / Drive Medical

Etac AB

Invacare Corporation

ArjoHuntleigh

EZ-ACCESS

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2025: TOTO USA unveiled the WASHLET S5 and S2 bidet seats that cut energy consumption by 38%; commercial launch is slated for summer 2025.

- May 2025: Midmark introduced a procedure chair compliant with United States Access Board guidelines, improving exam-room accessibility.

- February 2025: Drive Medical launched the Nitro Sprint rollator, rated for a 350-pound capacity and equipped with enhanced braking.

US Bathroom And Toilet Assist Devices Market Report Scope

There are numerous varieties of toilet-assisting equipment. Toilet rails that can be mounted to a wall or the toilet are among the most basic aids. The conventional toilet can be placed with these toilet rails, which provide support for both sitting and standing.

The US Bathroom and Toilet Assist Devices Market are Segmented by Product Type (Shower Chairs and Stools, Bath Lifts, Toilet Seats, Raisers, Commodes, Handgrips and Grab Bars, Bath-aids, and Other Product Types), End Use (Residential and Commercial), and Distribution (Online and Offline). The market sizes and forecasts are provided in value terms in USD Million for all the above segments.

By Product Type

| Shower Chairs and Stools |

| Bath Lifts |

| Toilet Seats |

| Raisers |

| Commodes |

| Handgrips and Grab Bars |

| Bath Aids |

| Others |

By End Use

| Residential |

| Commercial (Hospitals, LTC, Hotels, Airports) |

| Other Institutional (VA, Rehab Centers) |

By Distribution Channel

| Offline |

| Online |

By Material Composition

| Plastic |

| Aluminum |

| Steel |

| Composite and Others |

By Region

| Northeast |

| Southeast |

| Midwest |

| Southwest |

| West |

| By Product Type | Shower Chairs and Stools |

| Bath Lifts | |

| Toilet Seats | |

| Raisers | |

| Commodes | |

| Handgrips and Grab Bars | |

| Bath Aids | |

| Others | |

| By End Use | Residential |

| Commercial (Hospitals, LTC, Hotels, Airports) | |

| Other Institutional (VA, Rehab Centers) | |

| By Distribution Channel | Offline |

| Online | |

| By Material Composition | Plastic |

| Aluminum | |

| Steel | |

| Composite and Others | |

| By Region | Northeast |

| Southeast | |

| Midwest | |

| Southwest | |

| West |

Key Questions Answered in the Report

What is the current size of the US bathroom assist devices market?

The market is valued at USD 1.77 billion in 2026.

How fast is the market expected to grow?

It is projected to expand at a 7.23% CAGR, reaching USD 2.51 billion by 2031.

Which product category holds the largest market share?

Commodes lead with 31.86% of revenue in 2025.

Which US region shows the strongest growth outlook?

The Northeast is forecast to advance at an 10.94% CAGR through 2031.

How significant is the residential end-use segment?

Residential applications accounted for 65.58% of revenue in 2025 and are growing at an 8.63% CAGR.

Page last updated on: