Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 24.58 Billion |

| Market Size (2031) | USD 32.39 Billion |

| Growth Rate (2026 - 2031) | 5.63% CAGR |

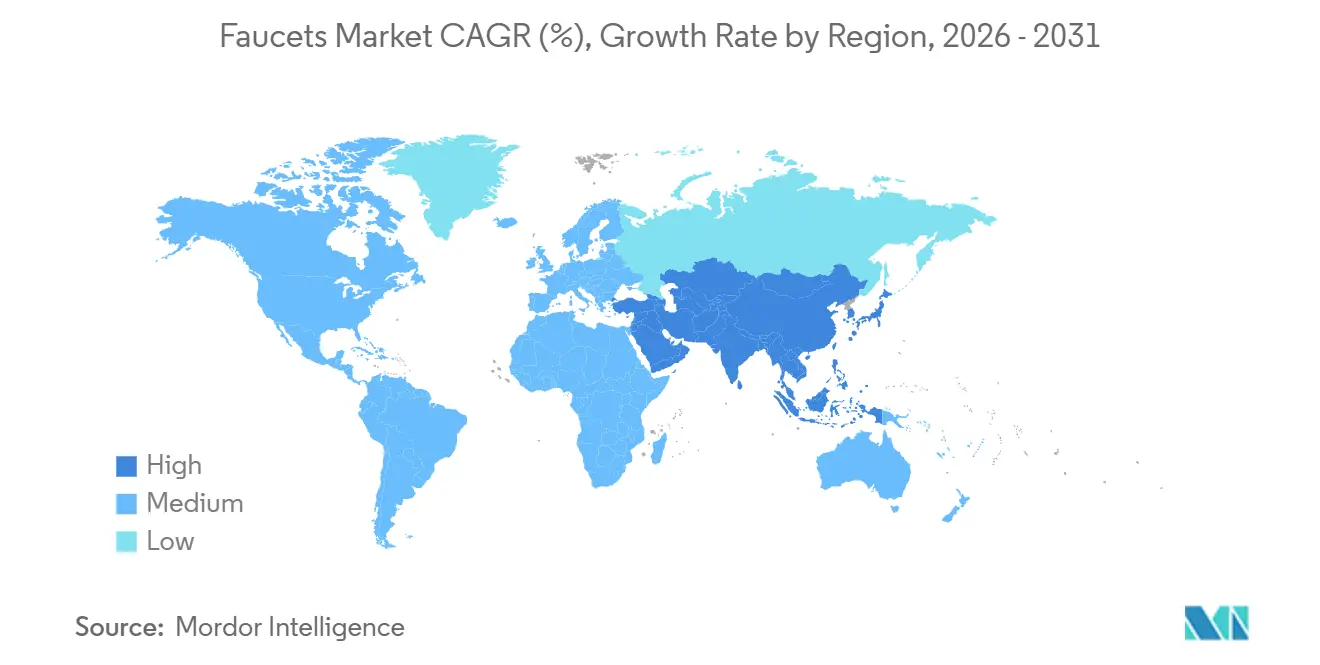

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

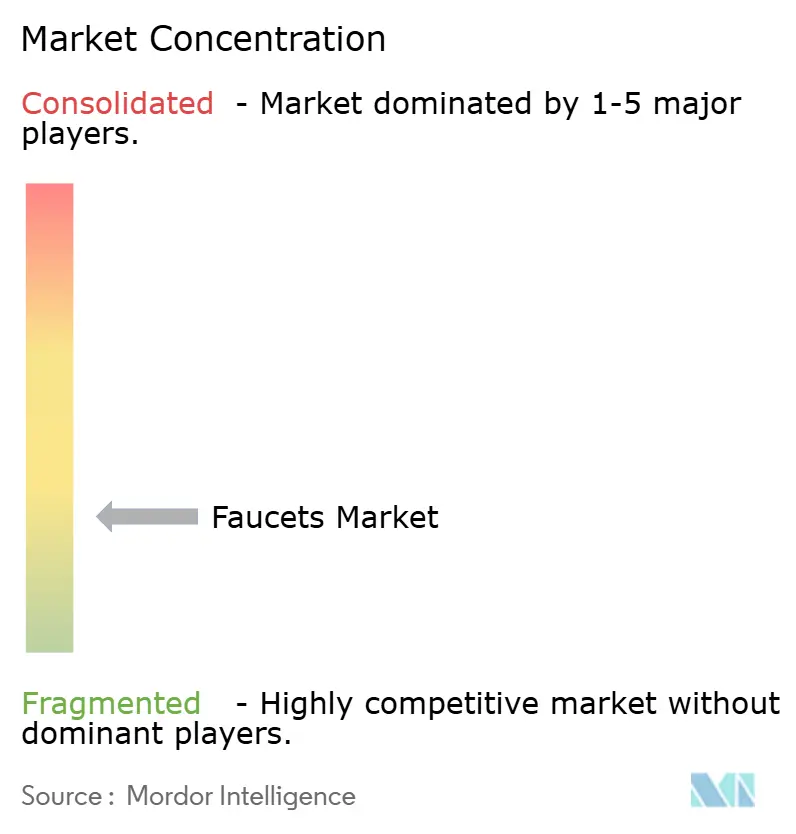

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Faucets Market Analysis by Mordor Intelligence

The faucet market size is USD 23.27 billion in 2025, expected to reach USD 24.58 billion in 2026, and is projected to reach USD 32.39 billion by 2031 at a 5.63% CAGR. Momentum reflects steady replacement activity in residential remodeling, stable project activity in hospitality and healthcare, and product refresh cycles linked to water-efficiency and drinking-water-contact rules that tighten material controls. Suppliers are using finish innovations and modular platforms to differentiate while streamlining SKUs that span both new-build and repair-and-remodel channels. Procurement behavior favors reliable brands with compliant materials and documented endurance testing, which supports premium positioning where audit trails matter. Distribution remains anchored in project channels, yet direct-to-consumer models expand options in mid to premium price bands, reshaping price discovery and brand loyalty dynamics in the faucet market.

Key Report Takeaways

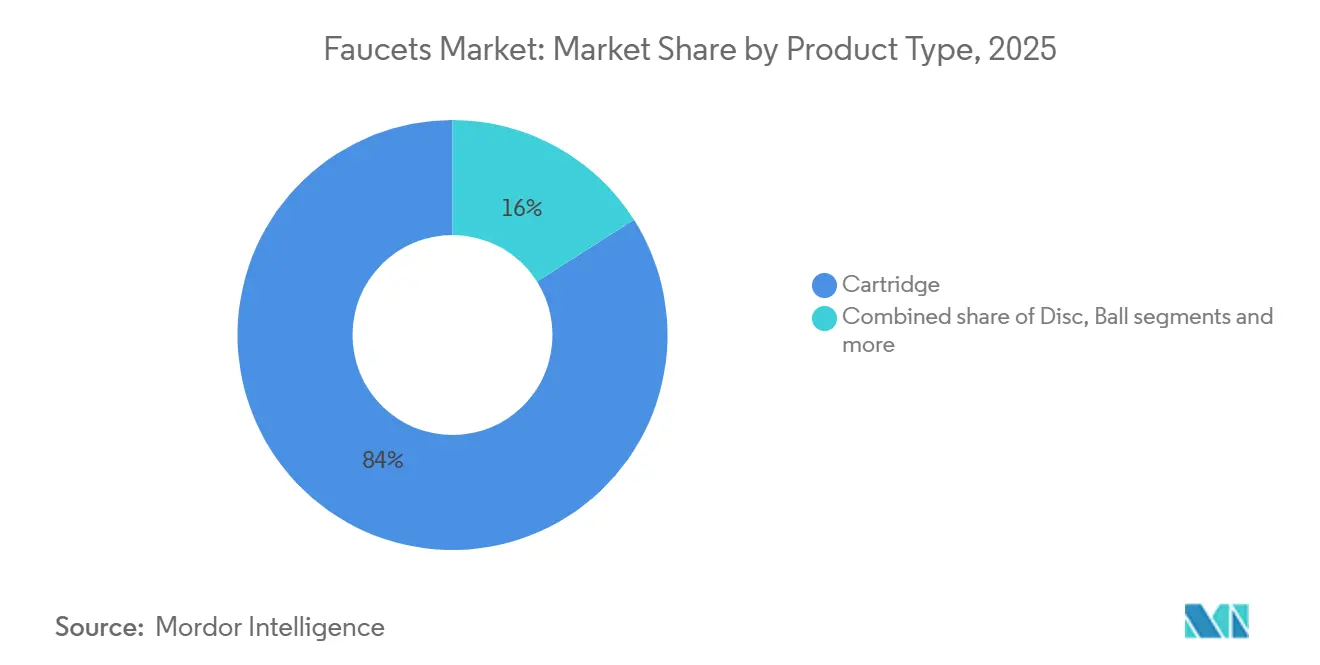

- By product type, cartridge mechanisms led with 84.05% revenue share in 2025 in the faucet market; disc valves are projected to post a 6.20% CAGR through 2031.

- By material, brass captured 44.80% of revenue in 2025; stainless steel is set to expand at a 6.45% CAGR through 2031.

- By technology, manual systems held 71.90% share in 2025 in the faucet market; automatic touchless systems are forecast to grow at a 6.75% CAGR to 2031.

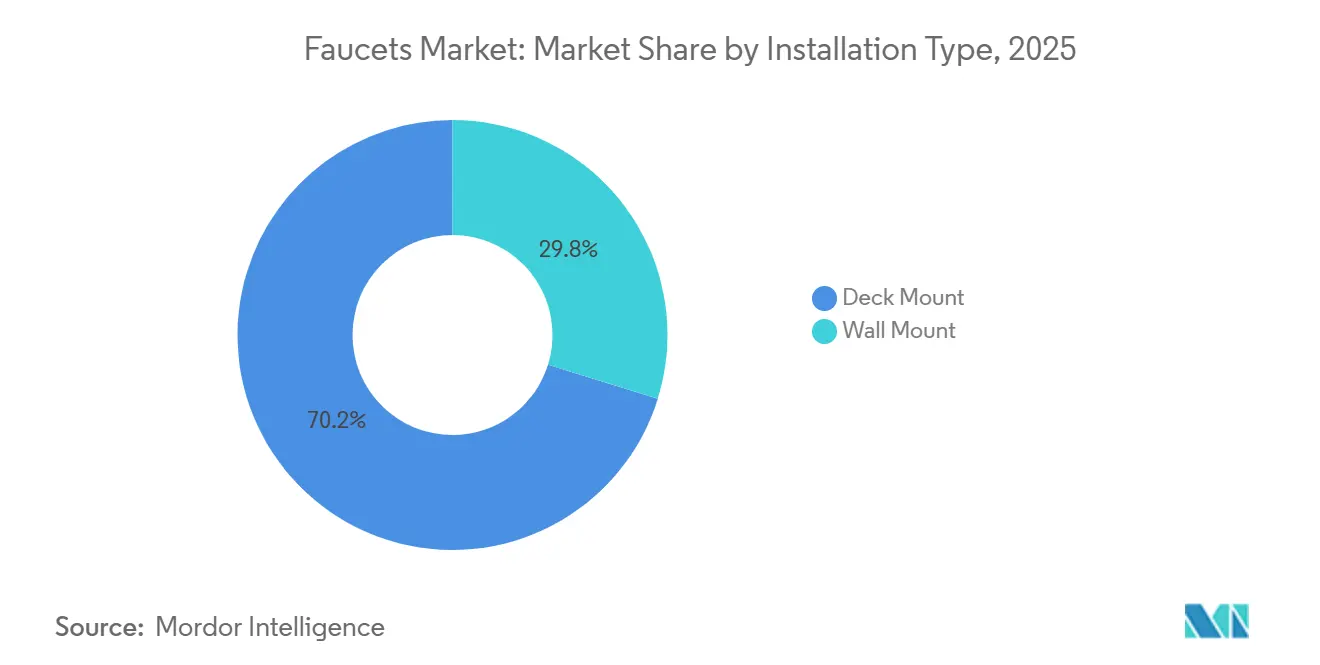

- By installation type, deck-mount faucets accounted for a 70.20% share in 2025 and are projected to advance at a 5.90% CAGR through 2031.

- By application, bathroom sink faucets represented 71.85% of the 2025 volume; kitchen sink faucets are expected to grow at a 6.30% CAGR through 2031.

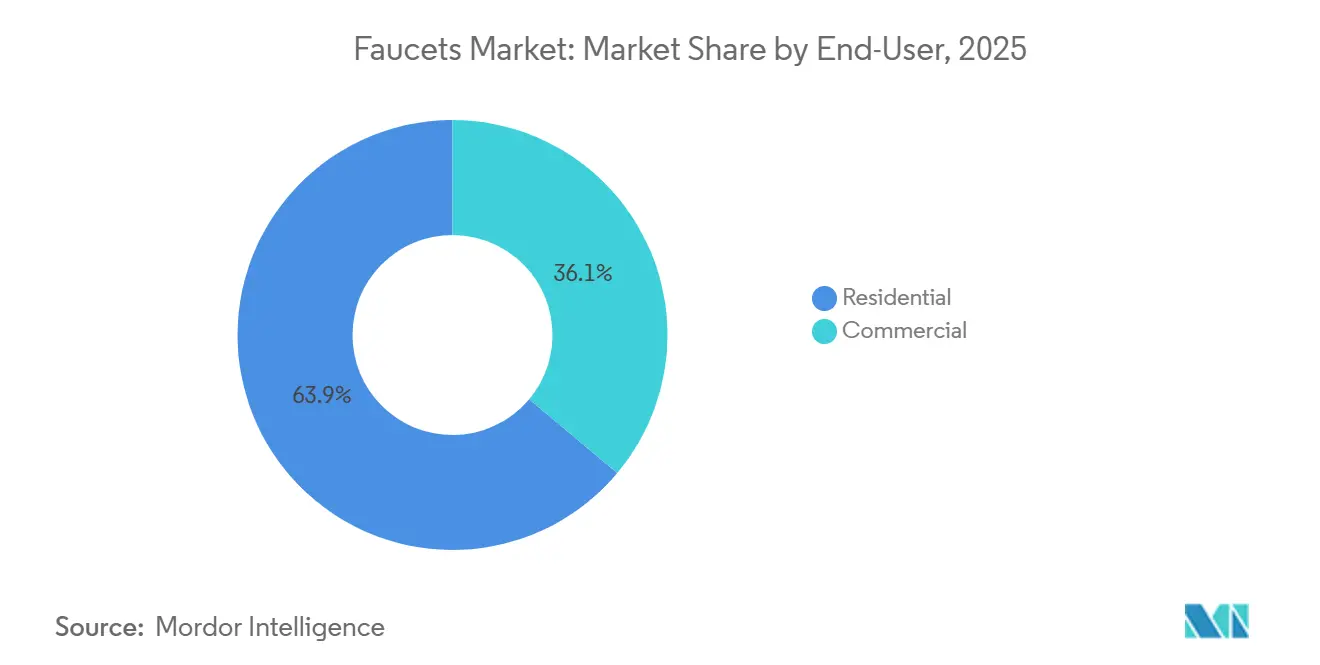

- By end-user, residential held a 63.90% share in 2025 in the faucet market, while commercial is projected to record the highest CAGR at 7.05% through 2031.

- By distribution channel, B2B and project channels held 66.20% of 2025 revenue, while B2C and retail are projected to expand at a 6.90% CAGR through 2031.

- By region, North America led with a 29.70% share in 2025, while Asia-Pacific is projected as the fastest-growing region at a 7.20% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Faucets Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Residential Remodeling and Aging Housing Stock Drive Replacement Cycles | +1.8% | Global, with early gains in North America and Asia-Pacific urban corridors | Medium term (2-4 years) |

| WaterSense v2.0 and Global Low-Flow Mandates Accelerate Product Refreshes | +1.4% | North America, Europe, pockets of Australia, and California leadership | Short term (≤ 2 years) |

| Touchless and IoT-Enabled Faucets Reshape Hygiene and Usage Monitoring | +1.2% | Global, concentrated on healthcare and hospitality | Medium term (2-4 years) |

| Hospitality and Healthcare Specify Premium, Durable, Certified Fixtures | +0.9% | Asia-Pacific, Middle East, and selective North America markets | Long term (≥ 4 years) |

| European Union drinking-water-contact material standards (2026) spur compliant product refreshes | +1.1% | Europe, with spillovers to exporters into the European Union | Short term (≤ 2 years) |

| WaterSense v2.0 (1.2 gpm, cold-start) catalyzes lavatory faucet redesigns | +0.7% | The United States, with early gains in leading states | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Residential Remodeling and Aging Housing Stock Drive Replacement Cycles

Home improvement remains a stable seam of demand for the faucet market because owners choose to upgrade kitchens and baths when moving is less attractive and equity is sufficient to fund projects. Aging housing across North America steadily adds replacement opportunities as installed fixtures reach the end of their service life, and this pattern also appears in urban Asia-Pacific, where multifamily stock matures. The mix skews to repair-and-remodel, which is less cyclical than new construction and gives brands recurring volume tied to homeowner refresh cycles. Contractors and designers favor proven cartridge platforms with ready parts availability that minimize service calls and keep schedules predictable. Premium collections that pair aesthetic updates with practical features such as temperature indicators and leak alerts create trade-up paths for equity-rich renovators in the faucet industry. Multifamily development cycles generate first-fit volume even when single-family slows, which helps stabilize factory utilization for mainstream SKUs.

WaterSense v2.0 and Global Low-Flow Mandates Accelerate Product Refreshes

The United States Environmental Protection Agency’s Draft WaterSense Version 2.0 specification for private lavatory faucets introduces a 1.2 gpm maximum and optional cold-start criteria, prompting OEMs to redesign aerators, cartridges, and flow paths ahead of a 2026 effective date[1]U.S. Environmental Protection Agency Staff, “WaterSense Program Specifications and Technical Information,” U.S. Environmental Protection Agency, epa.gov . Leading states already enforce 1.2 gpm limits for lavatory faucets, which means distributors are cycling inventory toward lower-flow SKUs in advance of nationwide changes. Local utilities and multi-housing programs use targeted rebates to speed up the adoption of WaterSense-labeled fixtures, bringing forward purchases in budget cycles and shaping assortment choices in the faucet market. In Europe, the Drinking Water Directive applies by December 31, 2026, and requires hygiene-compliant materials from a positive list for pipes, valves, and taps, pushing manufacturers to update brass alloys and validate stainless steel options that meet the new framework. German and other European Union producers have accelerated launches of low-leach materials in anticipation of national transpositions, which pulls forward portfolio refreshes and drives early mover advantages in tenders that reference the Directive. Australia’s WELS labeling influences consumer choice by linking star ratings to flow performance, reinforcing a long-term trend to lower-flow taps within building codes and retail merchandising in the faucet market.

Touchless and IoT-Enabled Faucets Reshape Hygiene and Usage Monitoring

Hands-free operation that rose during the pandemic has become standard in many healthcare and transport settings and is steadily moving into high-traffic commercial locations in the faucet market. Facility teams value touchless systems that integrate with building platforms to monitor usage, schedule purge cycles, and flag abnormal flow events for maintenance. Health agencies and accreditation bodies emphasize water management plans, which favor faucets that support routine flushing and temperature control to help reduce colonization risks in healthcare environments[2]Centers for Disease Control and Prevention Staff, “Developing a Water Management Program to Reduce Legionella Growth and Spread in Buildings,” Centers for Disease Control and Prevention, cdc.gov. Residential adoption of smart functions is growing, where users want to dispense exact volumes by voice and to track consumption in companion apps, and large brands now position these features as part of connected kitchen suites. Insurers and property managers show interest in leak detection tied to automatic shutoff because it can reduce water-damage losses and drive maintenance efficiencies at scale, which unlocks new business models around telemetry in the faucet market. Sensor and power innovations continue to improve reliability and reduce false activations, which lowers the total cost of ownership for operators that run large fleets of fixtures.

Hospitality and Healthcare Specify Premium, Durable, Certified Fixtures

Global hospitality pipelines in select corridors support orders for certified, durable faucets that can withstand frequent use and rigorous cleaning, which is a clear driver for premium lines with documented cycle life and finish durability in the faucet market. Operators lean toward PVD finishes to resist chemicals and abrasion, while value-engineered chrome remains in standardized mid-scale rooms where consistency and cost discipline matter. Healthcare specifications often call for thermostatic mixing at the point of use and programmable auto-flush features that fit within water management protocols, which directs demand toward electronic models with compliance features. Commercial kitchens and food-service operations adopt low-flow pre-rinse technologies to reduce operating costs, and municipal programs that distribute compliant devices help set new baselines in local codes. In branded hotels, common-area restrooms and back-of-house sinks increasingly use touchless fixtures to support hygiene narratives and to ease maintenance planning, while top-tier suites still use bespoke designs to align with design signatures from luxury partners in the faucet market. Portfolios that share rough-in platforms and interchangeable parts lower downtime and parts inventory for operators who manage fleets across properties.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Copper and Brass Price Volatility Compresses Margins and Delays Capex | -0.8% | Nationwide and global; pronounced in import-reliant markets | Short term (≤ 2 years) |

| Long replacement cycles and repair-first behavior dampen unit turnover | -0.5% | Global; most acute in price-sensitive markets | Long term (≥ 4 years) |

| European Union Hexavalent Chromium Restrictions Threaten Chrome-Plating Ecosystems | -0.6% | Europe, with spillovers to exporters into the European Union | Medium term (2-4 years) |

| Skilled-plumber shortages and retrofit complexity slow advanced faucet adoption | -0.4% | North America, Western Europe, Australia | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Copper and Brass Price Volatility Compresses Margins and Delays Capex

Input metal swings complicate pricing and budgeting for manufacturers, which pass some costs to channels but still see near-term margin pressure in the faucet market. Larger brands diversify sourcing geographies and qualify new foundries to stabilize supply, yet these shifts require time to pass certification and endurance testing before volume moves. Stainless steel producers watch nickel and stainless surcharge dynamics that ripple into billet costs, which can tighten spreads against brass depending on the quarter. In response, some suppliers delay discretionary capital investments in polishing and finishing lines until visibility improves, which can slow efficiency gains that matter over multi-year planning horizons. Public companies have disclosed commodity headwinds on earnings calls and described mitigation, such as product mix management and operational savings, to protect margins through volatility. Portfolio strategies that add higher-value smart or touchless SKUs can cushion gross margins, but adoption still depends on installer availability and buyer education in the faucet industry.

European Union Hexavalent Chromium Restrictions Threaten Chrome-Plating Ecosystems

The European Chemicals Agency’s restriction proposal on hexavalent chromium creates a defined transition for decorative chrome plating and sets exposure thresholds that would force process changes or investments at many European Union finishing shops. Even where Cr (III) alternatives are viable, higher cycle times and material considerations raise finish costs, and some durability tradeoffs remain part of technical discussions in industry working groups. PVD technologies provide Cr (VI)-free options with strong abrasion resistance, yet vacuum-chamber investments and volume thresholds constrain economics for mid-market SKUs. Smaller electroplaters in European clusters face capital hurdles to retrofit systems to meet proposed thresholds, which risks capacity exits and longer lead times as work consolidates to better-capitalized providers. Divergent regulatory paths between the European Union and the United Kingdom complicate supply chains as companies weigh plating locations, tariffs, and logistics when routing volume to sustain chrome-like aesthetics in the faucet market. Exporters into the European Union that rely on external finishing partners are also planning for compliance documentation and supplier audits to maintain market access under REACH[3]European Chemicals Agency Secretariat, “Annex XV Restriction Report for Chromium (VI) Substances in Decorative Plating,” European Chemicals Agency, echa.europa.eu .

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Ceramic Disc Valves Challenge Cartridge Dominance

Cartridge mechanisms held the largest share in 2025 and anchor the faucet market through broad retrofit compatibility and reliable single-lever operation, while disc valves are positioned as the fastest-growing subsegment through 2031 on durability claims and lower service frequency in high-traffic settings. Many commercial operators emphasize lifecycle economics as opposed to first cost, which supports premium ceramic-disc adoption in places like airports, hospitals, and malls where downtime is disruptive. Portfolio strategies from leading brands preserve cartridge lines for mass-market channels even as disc-valve options expand within project specifications. Universal cartridge availability at major retailers keeps the installed base serviceable, which extends useful life and sustains brand satisfaction. Disc-valve designs that allow hot-swap maintenance improve turnaround time for in-house staff, which can reduce contractor callouts for large property portfolios in the faucet market.

As catalogs evolve, compression and ball faucets retain specialty roles where budget constraints or traditional aesthetics guide specification. Design-focused programs in luxury and heritage renovations sustain compression units with period-correct hardware, while ball faucets now track niche, value-driven applications. Regional preferences also shape product-mix differences, with markets that prize longevity more likely to move toward ceramic-disc solutions and markets that favor simplicity staying with cartridge mechanisms. Rough-in and finish ecosystems remain the main levers for differentiation, and brands that extend disc-valve offerings across coordinated suites gain share in higher specification tiers. This gradual pivot gives the faucet market a balanced mix that satisfies pro channels and design centers while keeping entry points open for DIY and light commercial.

By Material: Stainless Steel Gains as Lead-Free Rules Tighten

Brass remains the revenue anchor in 2025, given mature machining knowledge and robust recycling streams, while stainless steel is the fastest-growing material category due to its inherent lead-free composition that aligns with tightening drinking-water-contact requirements. The European Union Drinking Water Directive’s materials framework accelerates shifts to dezincification-resistant, lower-leach alloys and stainless grades that clear new hygiene criteria, and producers have brought forward compliant SKUs to lock in early contracting wins[4]European Commission Services, “Directive (EU) 2020/2184 Materials Compliance and Positive List,” European Commission, ec.europa.eu . Stainless steel also benefits from finish options that skip electroplating, mitigating exposure to Cr (VI) constraints while enabling brushed and satin looks that resonate in mid to premium kitchens. Finish mix is evolving as PVD colorways widen choice at higher ASPs and as chrome alternatives progress in sheen consistency under production conditions. Investments in alloy testing and certification speed are now strategic, since faster compliance cycles help brands refresh assortments in time for regulatory milestones in the faucet market.

Material selection blends lifecycle economics and regulatory compliance, which keeps brass relevant where machining speed and scrap value remain compelling. Stainless adoption expands as production lines adapt to different tooling loads and as upstream billet costs normalize after recent surcharges. Specialized polymers and niche metals continue to serve cost-sensitive and specialty applications, yet the center of gravity in regulated markets now tilts toward alloys and steels validated under positive lists. European producers that publish third-party environmental product declarations and recycling rates also gain traction with project specifiers who weigh circularity signals in tenders. Over the next planning cycle, material mix is likely to track local compliance deadlines and channel positioning as brands target specific buyer personas in the faucet market.

By Technology: Touchless Systems Surge in Institutional Settings

Manual faucets held the clear majority in 2025, reflecting entrenched use in residential and cost-conscious renovations, while touchless systems are upshifting fastest on hygiene and maintenance advantages in public and institutional settings. Health guidance that emphasizes water safety plans and routine flushing gives weight to electronic models that support these features with programmable purge and temperature controls. Commercial adoption also benefits from hardwired power options that eliminate battery logistics, BMS integration that captures usage data, and ecosystems that include matching dispensers and sensors. Residential demand for smart functions clusters in premium kitchens where voice dispensing, presets, and app telemetry align with broader smart-home purchases in the faucet market. Dual-mode designs with manual override provide operational redundancy that facilities and homeowners value during power or sensor service events.

Touchless portfolios are moving into more finish and spout geometries so designers can maintain visual continuity in mixed-technology restrooms. OEMs refine sensor algorithms to reduce false activations on reflective surfaces and under varying ambient light. Serviceability is a rising factor, as operators look for accessible valves, quick-swap solenoids, and common cartridge families across multiple series to standardize maintenance. In parallel, manual lines defend their position through long-life ceramic discs and tactile handle designs that convey quality at mid-market price points. The result is a technology spectrum that lets channels tailor assortments by venue and budget, which is how the faucet market supports both high-volume renovations and feature-driven upgrades.

By Installation Type: Deck Mount Sustains Dominance

Deck-Mount configurations held the largest share in 2025 and are projected to maintain leadership, given widespread compatibility with existing sinks and straightforward install steps that keep labor predictable in both retail and project channels. Builders and renovators favor deck-mount to minimize wall modifications in retrofit scenarios, and the format aligns with common three-hole and single-hole sink layouts across regions. Wall-mount use concentrates in premium baths and select commercial kitchens where counter space is at a premium and where concealed rough-ins are coordinated during framing or gut renovations. Accessibility compliance and handle-force requirements also guide layout decisions in public facilities, which often favor deck-mount geometries for ergonomics and reach.

As design tastes drift toward minimalist, wall-mount grows in higher-end segments where tile and stone backdrops serve as visual anchors and where buyers accept higher installed costs. Deck-mount benefits from accessory ecosystems that add side-sprayers, soap dispensers, and filtered taps using extra sink holes, which boost basket size and attachment rates. Online listening continues to reinforce deck-mount dominance because DIY-friendly installation reduces return risk and enables fast project turnover. Pro showrooms still lead wall-mount specifications, where designers create looks and coordinate rough-in heights and tolerances. Over time, installation mix will keep mapping to labor realities and design intent in the faucet market, with deck-mount sustaining the broad base and wall-mount defining premium statements.

By Application Type: Kitchen Gains on Integrated Filtration

Bathroom sink faucets accounted for the majority of the 2025 volume due to higher fixture counts per home and shorter replacement cycles, while kitchen faucets are expanding faster as integrated filtration and multi-function sprayers elevate their role in the home. Kitchen buyers are adopting beverage faucets and under-counter systems that deliver filtered still and sparkling water at the sink, which reframes the faucet as an appliance rather than a basic fixture. In remodel budgets, kitchens command larger allocations, which support premium features like voice control and pull-down sprayers with advanced spray patterns. Bathrooms remain a steady volume engine with a strong center set and widespread adoption, and a wide finish mix that lets homeowners coordinate with mirrors and accessories.

Flow ceilings diverge by use case, with lavatory faucets tightening to a 1.2 gpm target under WaterSense v2.0 while kitchens retain higher allowances to support pot filling and dish tasks. This difference keeps product design optimized by room, with bathroom lines focused on compliance and aesthetics, and kitchen lines focused on function and integration. The beverage and filtration category is also expanding as health and taste preferences drive point-of-use investments, and branded ecosystems that pair faucets with filtration systems simplify choices. Application mix will keep reflecting domestic spatial priorities and code settings, and the faucet market will mirror these patterns through assortments that fit the specific tasks and expectations in each room.

By End-User: Commercial Outpaces Residential on Hygiene Mandates

Residential buyers represented the larger share of demand in 2025 on the strength of the installed base of households and steady replacement cycles, while commercial buyers are projected to grow faster through 2031 as institutions invest in hygiene, telemetry, and durability. Commercial specifications elevate vandal resistance, electronic controls, and extended warranties, which raise ASPs and formalize vendor evaluation against compliance and endurance standards. Hospitality and healthcare add volume with touchless requirements in public areas and with thermostatic controls in patient or prep zones that align with water management goals. Residential continues to modernize through finish trends and selective adoption of smart functions that integrate with voice assistants and home platforms. The end-user split leads vendors to manage separate value propositions and service models that address installer support for pro jobs and education for DIY channels in the faucet market.

Bulk purchasing and project logistics also define commercial procurement, which emphasizes total lifecycle cost and serviceability over ornamental variation. Residential e-commerce adds momentum to direct sales for premium and configurable models, while commercial continues to rely on authorized distributors for submittals, compliance documentation, and job-site delivery. As more commercial operators trial telemetry and leak detection to reduce maintenance calls, IoT penetration is likely to widen in multi-site portfolios. Residential remains the volume floor, yet commercial growth will lean into platform features and certification portfolios that pass institutional due diligence. Together, these patterns shape roadmap decisions and channel priorities across the faucet market.

By Distribution Channel: E-Commerce Disrupts Project Channels

B2B and project distribution controlled the larger revenue share in 2025, powered by contractor procurement, pro credit terms, and job-site services, while B2C and retail are growing faster as e-commerce compresses the path from research to purchase and delivery. Manufacturer-direct stores and partner showrooms curate high-ASP assortments and offer installation coordination for affluent buyers, while marketplaces and brand websites lean on fast shipping, AR visualization, and liberal returns to convert DIY projects. Big-box retailers maintain high-velocity ranges that focus on ease of installation and replacement-part availability, reinforcing brand familiarity in the faucet market. Direct-to-consumer growth helps brands test finishes and configurations while capturing data that informs product decisions and service offers.

On the B2B side, architects and MEP engineers anchor specifications that route fulfillment to authorized distributors with the certifications and warranty support needed for submittals and inspections. Distributors and reps also support code questions and ensure compliant substitutions, which protect the integrity of project documents. Cross-border e-commerce opens option sets for enthusiasts, but warranty logistics and returns still push most professional buyers to domestic channels with responsive service. Over time, channel mix will reflect the balance of institutional rigor and consumer convenience, and vendors will continue to diversify go-to-market approaches in the faucet market to capture both flows.

Geography Analysis

North America held 29.70% of global revenue in 2025, powered by a large and aging housing stock, steady remodel activity, and state-level water-efficiency rules that have already tightened lavatory flows ahead of national updates. WaterSense v2.0, which introduces a 1.2 gpm cap for private lavatory faucets, shapes OEM roadmaps and distributor assortments and is slated to drive national alignment as implementation begins, with several states already set to benefit first from compliant lines in the market. Municipal and utility rebate programs add local pull by offsetting upgrade costs, which encourages early replacements in multi-family and campus properties. North American production footprints that serve the region also benefit from trade frameworks that support nearshoring strategies and reduce tariff exposure, which helps stabilize lead times and landed costs in the faucet market. Together, these structural factors underpin resilient regional demand that is supported by pro distribution and a deep repair-and-remodel base.

Asia-Pacific is projected as the fastest-growing region through 2031 on urbanization, healthcare and hospitality investments, and a widening middle class that prioritizes modern fixtures in new builds and renovations. Hospitals, airports, and shopping centers in major metros are specifying touchless technologies to support hygiene and maintenance productivity, and this in turn fuels local assembly and component ecosystems for sensors and valves. Governments in Australia and New Zealand maintain WELS-driven labeling regimes that clearly signpost water performance, which steers assortments toward lower-flow taps and influences consumer choices in the faucet market. Regional players and global brands mix factory footprints to serve domestic codes and tastes, and that mix is evolving as compliance frameworks tighten in export markets. Over time, specification standards in major hospitality chains also spread requirements across countries as regional development pipelines advance.

Europe moves on a parallel path that tightly integrates regulation with market behavior, anchored by the European Union Drinking Water Directive’s December 31, 2026, application date for material hygiene compliance in contact with drinking water. The region’s producers have accelerated launches of positive-list materials and aligned internal testing to prepare for member-state transpositions, while project specifiers increasingly cite DWD readiness in procurement documents. Chrome plating changes under the proposed REACH restriction on hexavalent chromium are reshaping finishing strategies as firms validate Cr (III) and PVD alternatives and assess capital requirements and supplier viability. Divergent regulatory choices between the European Union and the United Kingdom on authorizations lead companies to balance final sourcing and logistics as they maintain appearance standards and warranty claims across markets. This regulatory cadence, paired with premium product mixes and strong installer networks, sustains a steady, compliance-oriented growth pattern in the faucet market.

Competitive Landscape

Market concentration is fragmented, with the top five players, LIXIL, Masco, Kohler, Fortune Brands, and TOTO, anchor portfolios that span cartridges, smart technologies, and finish platforms, while regional specialists target local codes and tastes. Competitive dynamics in the mid-price band remain intense as private labels and challenger brands compress pricing, which motivates leading brands to compete on finish breadth, serviceability, and smart features that justify premiums in the faucet market. Project channels value documented endurance and certification libraries, which gives incumbents with deep compliance infrastructure an advantage in public and regulated segments.

Recent corporate moves show targeted expansion and ecosystem building. Fortune Brands’ acquisition of SpringWell Water Filtration extends kitchen-system bundles that combine faucets with under-sink filtration, supporting a higher attachment model and expanding the water solutions narrative in residential channels. Roca Group’s acquisitions of Antonio Lupi and Phoenix broadened its footprint in luxury bath and Oceania tapware, while adding design and finishing depth that supports premium positioning in showrooms and design-build firms. On the product side, Kohler’s Aquifer 4-in-1 Beverage Faucet positions the kitchen faucet as an integrated beverage station with filtered ambient, chilled, sparkling, and boiling water from a single spout, signaling how functional integration can shift category expectations in the faucet market.

Brands also increase emphasis on smart functions that deliver convenience and measurable value. Delta’s touch activation, paired with hands-free mode, responds to buyer concerns about redundancy and reliability while preserving intuitive manual control for daily use. Hansgrohe’s award-winning shower platform demonstrates how water-saving recirculation and adaptive flow logic can transfer across mixing and control philosophies that affect faucets, which points to the convergence of categories within bathroom ecosystems. As telemetry and integration rise in relevance for operators and homeowners, vendors refine app experiences and service models that can drive ongoing engagement and lock-in, and this is likely to reshape differentiation and pricing strategies across the faucet market.

Faucets Industry Leaders

LIXIL Corp.

Kohler Co.

Masco Corp. (Delta, Hansgrohe)

TOTO Ltd.

Fortune Brands Innovations (Moen, Pfister)

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2026: Kohler Co. introduced the Aquifer 4-in-1 Beverage Faucet at KBIS 2026, delivering filtered ambient, chilled, sparkling, and boiling water from a single spout via an under-counter system retailing for USD 3,375 (system) plus USD 600+ (faucet); the launch targets affluent renovators (household income greater than USD 200,000) seeking appliance consolidation and is positioned to compete with Zip Water and Grohe Blue systems in the USD 850-million North American beverage-faucet segment.

- November 2025: VitrA (Eczacıbaşı Group) launched Root Sensor Faucets with advanced infrared technology for hands-free operation, targeting healthcare and hospitality sectors in Europe and the Middle East; the product line, priced at EUR 280–650, features adjustable sensor range (2–20 cm) and anti-vandal solenoid valves rated for 1 million cycles, positioning VitrA to capture share from incumbent Grohe and Hansgrohe in commercial touchless segments.

- July 2025: Roca Group acquired Phoenix, an Australian tapware manufacturer known for mid-to-high-end design leadership, to strengthen its Asia-Pacific footprint; the acquisition provides Roca with Phoenix's WELS-certified product portfolio and relationships with GWA Group and Reece Group, Australia's dominant plumbing distributors, facilitating penetration into the AUD 630-million (USD 420-million) Oceania faucet market.

Global Faucets Market Report Scope

In a plumbing system, faucets are objects that are used to regulate the water flow. These faucets are mostly utilised in bathrooms, kitchens, and other spaces where water is needed on a daily basis. Faucets come in a vast array of designs, hues, and finishes to accommodate a variety of consumer needs. Faucet market is segmented By Product Type (Ball, Disc, Cartridge and Compression), By Technology (Manual, Automatic), By Material Used (Stainless Steel, Chrome, Bronze Plastic, Others), By Application (Bathroom, Kitchen, Others), By End Use (Residential, Commercial, Industrial), and By Geography (North America, Europe, Asia-Pacific, South America and Middle East).

By Product Type

| Ball |

| Disc |

| Cartridge |

| Compression |

By Material

| Chrome |

| Stainless Steel |

| Brass |

| Polytetra Methylene Terephthalate (PTMT) Plastic |

| Other Materials |

By Technology

| Manual |

| Automatic |

By Installation Type

| Deck Mount |

| Wall Mount |

By Application Type

| Kitchen Sink Faucets |

| Bathroom Sink Faucets |

By End-User

| Residential |

| Commercial |

By Distribution Channel

| B2C/Retail Distribution Channel | Multi-Brand Stores |

| Exclusive Brand Outlets | |

| Online | |

| Local Hardware Stores | |

| B2B/Project |

By Geography

| North America | Canada |

| United States | |

| Mexico | |

| South America | Brazil |

| Peru | |

| Chile | |

| Argentina | |

| Rest of South America | |

| Europe | United Kingdom |

| Germany | |

| France | |

| Spain | |

| Italy | |

| BENELUX (Belgium, Netherlands, Luxembourg) | |

| NORDICS (Denmark, Finland, Iceland, Norway, Sweden) | |

| Rest of Europe | |

| Asia-Pacific | India |

| China | |

| Japan | |

| Australia | |

| South Korea | |

| South-East Asia | |

| Rest of Asia-Pacific | |

| Middle East & Africa | United Arab Emirates |

| Saudi Arabia | |

| South Africa | |

| Nigeria | |

| Rest of Middle East & Africa |

| By Product Type | Ball | |

| Disc | ||

| Cartridge | ||

| Compression | ||

| By Material | Chrome | |

| Stainless Steel | ||

| Brass | ||

| Polytetra Methylene Terephthalate (PTMT) Plastic | ||

| Other Materials | ||

| By Technology | Manual | |

| Automatic | ||

| By Installation Type | Deck Mount | |

| Wall Mount | ||

| By Application Type | Kitchen Sink Faucets | |

| Bathroom Sink Faucets | ||

| By End-User | Residential | |

| Commercial | ||

| By Distribution Channel | B2C/Retail Distribution Channel | Multi-Brand Stores |

| Exclusive Brand Outlets | ||

| Online | ||

| Local Hardware Stores | ||

| B2B/Project | ||

| By Geography | North America | Canada |

| United States | ||

| Mexico | ||

| South America | Brazil | |

| Peru | ||

| Chile | ||

| Argentina | ||

| Rest of South America | ||

| Europe | United Kingdom | |

| Germany | ||

| France | ||

| Spain | ||

| Italy | ||

| BENELUX (Belgium, Netherlands, Luxembourg) | ||

| NORDICS (Denmark, Finland, Iceland, Norway, Sweden) | ||

| Rest of Europe | ||

| Asia-Pacific | India | |

| China | ||

| Japan | ||

| Australia | ||

| South Korea | ||

| South-East Asia | ||

| Rest of Asia-Pacific | ||

| Middle East & Africa | United Arab Emirates | |

| Saudi Arabia | ||

| South Africa | ||

| Nigeria | ||

| Rest of Middle East & Africa | ||

Key Questions Answered in the Report

What is the faucets market size in 2026, and how fast is it growing?

The faucets market size is USD 24.58 billion in 2026 and is projected to reach USD 32.39 billion by 2031 at a 5.63% CAGR.

Which region leads the faucets market, and which grows fastest?

North America leads with 29.70% of 2025 revenue, while Asia-Pacific is projected to be the fastest-growing region through 2031.

Which product and technology segments are most important for growth?

Cartridge mechanisms hold the largest share in 2025, while touchless systems are the fastest-growing technology on hygiene and maintenance benefits.

How are regulations shaping new faucet launches in 2026?

WaterSense v2.0 in the United States pushes 1.2 gpm lavatory designs, and the European Union Drinking Water Directive requires compliant contact materials by December 31, 2026, accelerating product refreshes.

Which end-users are driving premium features and why?

Healthcare, hospitality, and other commercial operators are adopting touchless, thermostatic, and telemetry-enabled faucets to support hygiene programs and maintenance efficiency.

What risks could affect faucet market growth through 2031?

Metal price volatility and European Union finish-process restrictions on hexavalent chromium can compress margins and add transition costs for finishing, influencing pricing and availability.

Page last updated on: