Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Market Size (2026) | USD 43.26 Billion |

| Market Size (2031) | USD 61.03 Billion |

| Growth Rate (2026 - 2031) | 7.13% CAGR |

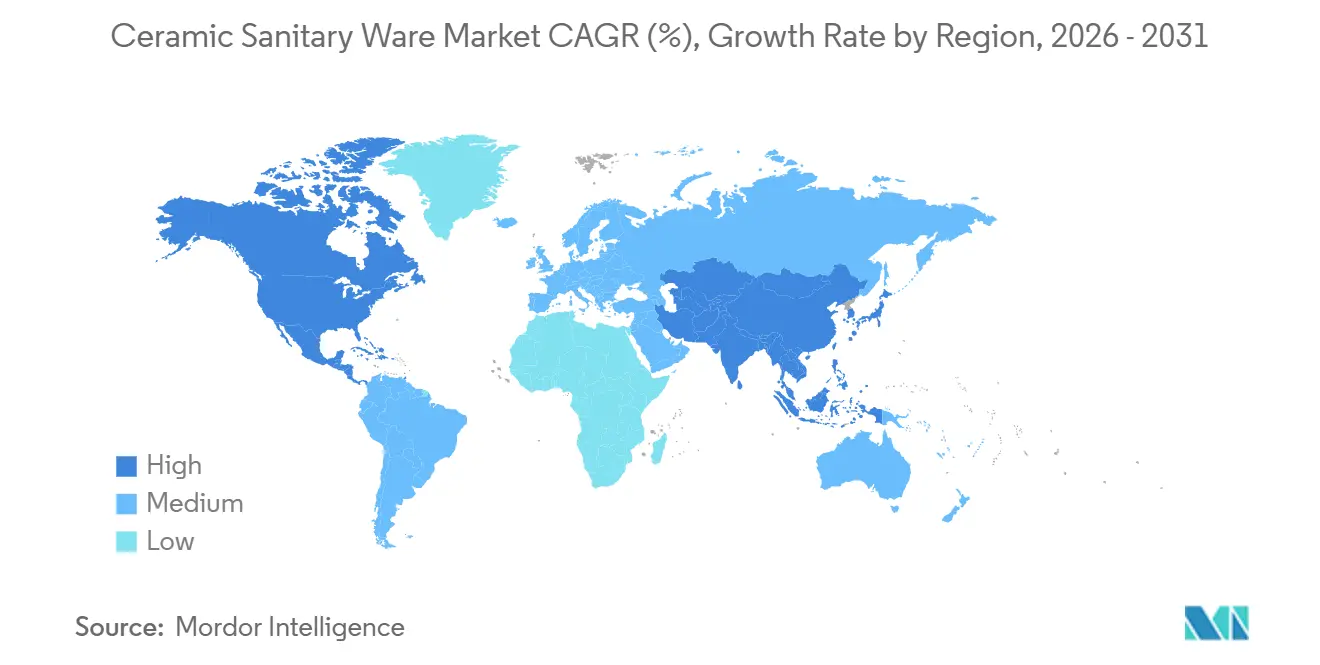

| Fastest Growing Market | North America |

| Largest Market | Asia Pacific |

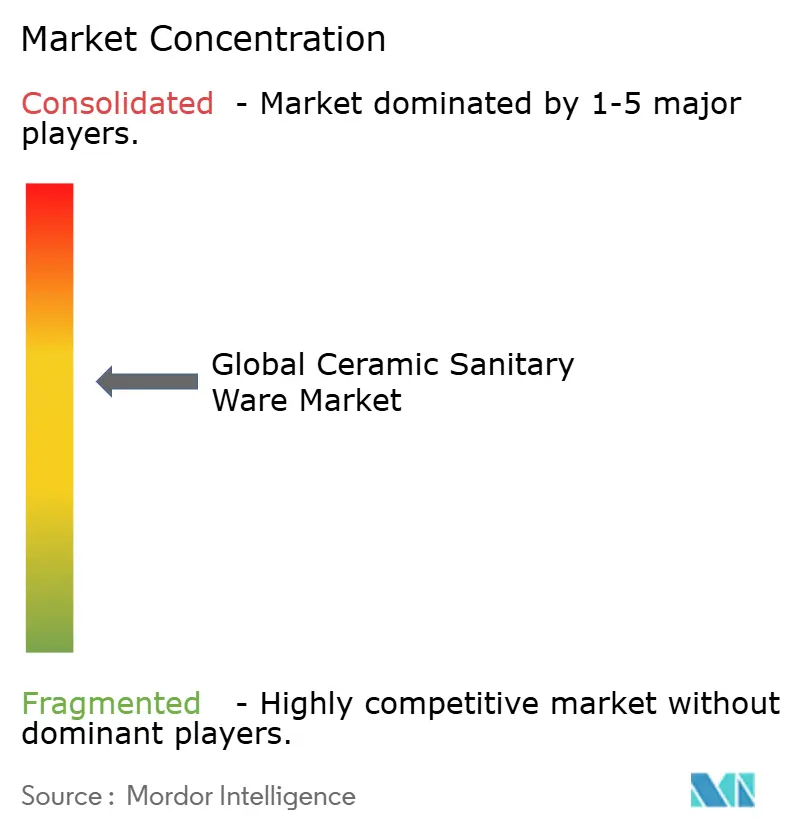

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Ceramic Sanitary Ware Market Analysis by Mordor Intelligence

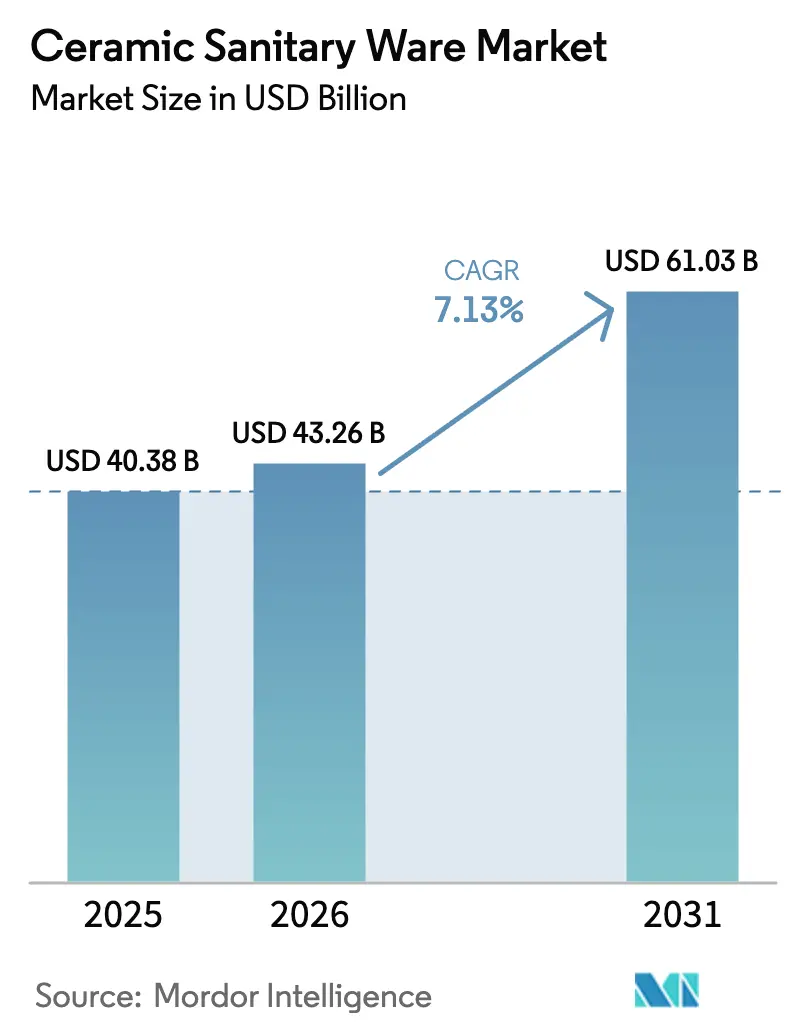

The Ceramic Sanitary Ware Market size is projected to be USD 40.38 billion in 2025, USD 43.26 billion in 2026, and reach USD 61.03 billion by 2031, growing at a CAGR of 7.13% from 2026 to 2031.

Momentum continues to build around the decarbonization of kilns and process heat, shaping capital expenditure priorities and influencing sourcing and site selection in the ceramic sanitaryware market. Manufacturers that pair energy-efficient firing with digital design and rapid prototyping are carving out lead-time and sustainability advantages that resonate with institutional buyers in healthcare and hospitality within the ceramic sanitaryware market. Regional performance remains uneven, with Asia-Pacific driving scale while North America leads growth, which in turn encourages flexible product portfolios and segmented go-to-market strategies across the ceramic sanitaryware market.

Key Report Takeaways

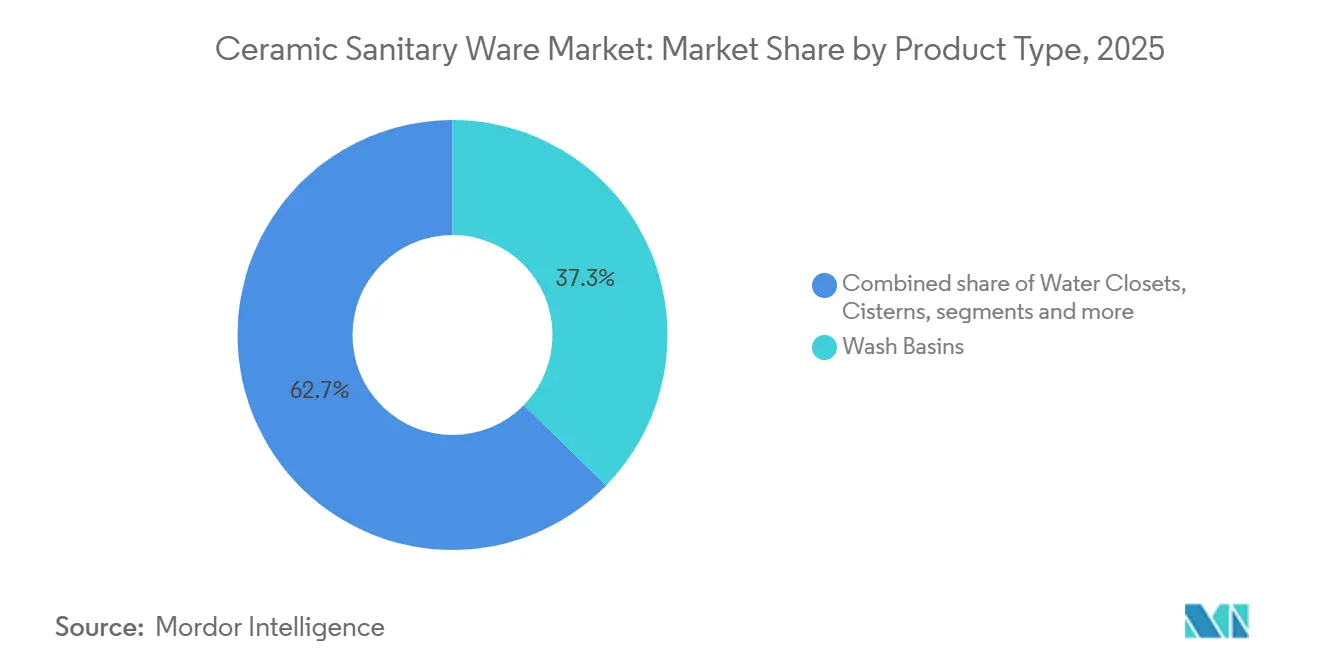

- By product type, wash basins led with 37.33% market share of the ceramic sanitary ware market in 2025, while water closets are forecast to expand at a 7.67% CAGR to 2031.

- By end-user, residential accounted for 62.74% of the ceramic sanitary ware market size in 2025, while commercial is projected to grow at a 5.87% CAGR through 2031.

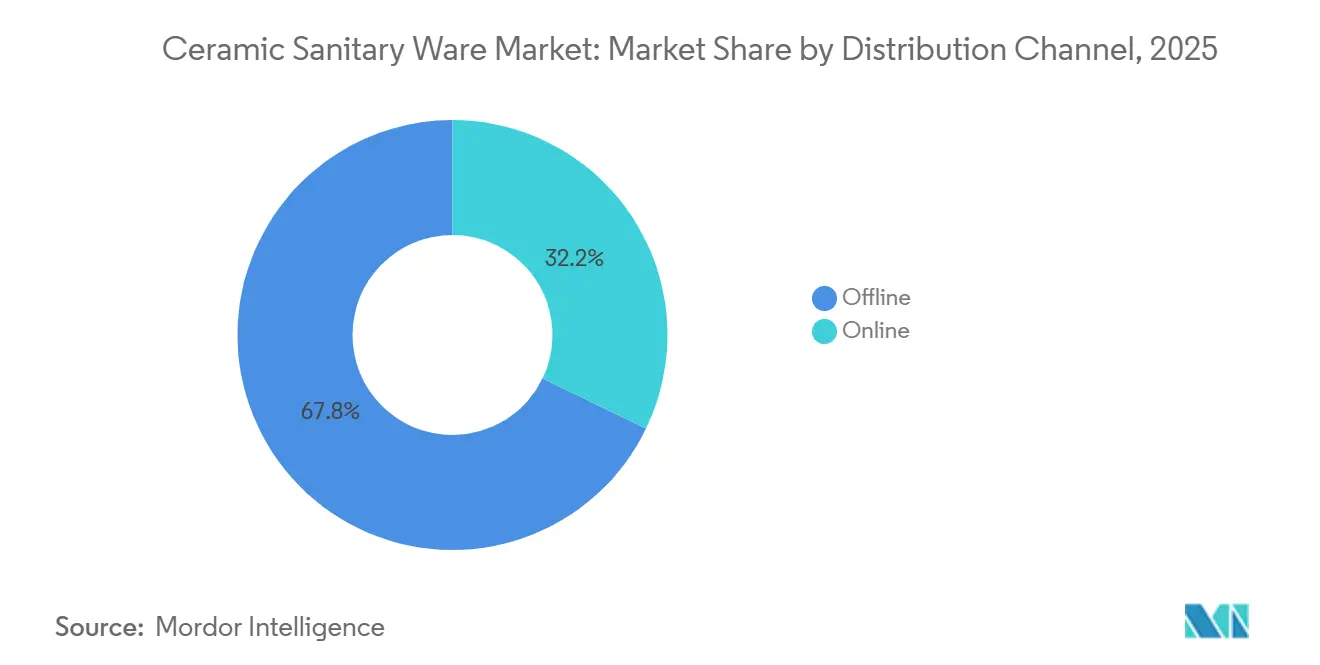

- By distribution channel, offline retained a 67.84% share of the ceramic sanitary ware market size in 2025, while online is expected to rise at an 8.98% CAGR through 2031.

- By geography, Asia-Pacific held 43.39% of the ceramic sanitary ware market share in 2025, while North America is set to record the highest regional CAGR at 7.67% through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Ceramic Sanitary Ware Market Trends and Insights

Drivers Impact Analysis*

| Driver | % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Urban Housing and Renovation Boom | +1.8% | Asia-Pacific core, secondary gains in MEA & South America | Medium term (2–4 years) |

| Sanitation Subsidies in Emerging Markets | +1.3% | India, Bangladesh, Sub-Saharan Africa, Latin America | Short term (≤ 2 years) |

| Shift Toward Water-Efficient Smart Sanitary Ware | +2.1% | North America & EU lead, rapid uptake in urban China & India | Medium term (2–4 years) |

| Growth of Organized Home-Improvement Retail & E-Commerce | +0.9% | Global, strongest in North America, Europe, and urban Asia | Short term (≤ 2 years) |

| Uptake of Prefabricated Bathroom Pods in Commercial Builds | +0.6% | Europe, North America, Middle East hospitality/healthcare | Long term (≥ 4 years) |

| Demand for Antimicrobial-Glazed Ceramics Post-Pandemic | +0.5% | Global, concentrated in Europe, North America, and high-end Asia projects | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Urban Housing and Renovation Boom

Urban migration is expanding municipal sanitation buildouts and mobilizing household renovation cycles that sustain the ceramic sanitaryware market across residential and mixed-use projects. In Japan, renovation accounted for 51% of Water Technology revenue at LIXIL in fiscal 2024, and that pivot underscores how mature markets balance new-build softness with upgrades in the ceramic sanitaryware market.[1]Source: LIXIL Corporation, “LIXIL Revenue and Profit Decrease in FYE 2024 Due to Sluggish Demand in International Markets,” LIXIL Newsroom, newsroom.lixil.com Developer-led activity in the United Arab Emirates continued through 2025, with RAK Ceramics reporting a 26.4% year-on-year domestic revenue rise in Q2 2025, which supported scale utilization and mix improvements in sanitaryware.[2]Source: RAK Ceramics, “Annual Report 2024,” RAK Ceramics, corporate.rakceramics.com In Europe, Geberit’s business mix reflected steady renovation demand that cushioned the trough in new residential starts, which disciplines product development toward retrofit-friendly systems in the ceramic sanitaryware market. At the same time, a drop in global project finance for water and sanitation in developing regions during 2024 signaled near-term constraints in public-sector upgrades, which can temper unit growth until financing normalizes.

Sanitation Subsidies in Emerging Markets

Policy support in large emerging economies sustains baseline demand for durable fixtures, and procurement rules increasingly reward certified water efficiency in the ceramic sanitaryware market. TOTO targets 3.50 million overseas WASHLET unit shipments by fiscal 2026, up from 3.06 million in fiscal 2024, aligning product penetration goals with government-backed sanitation programs and hygiene campaigns. In Bangladesh, new showrooms and capacity actions by multinational and regional players signal latent urban demand that could be unlocked as energy supply stabilizes, which keeps the ceramic sanitaryware market engaged in local buildouts. In the European Union, the European Water Label registry has expanded across brands and SKUs and is increasingly used to screen products in public tenders, which aligns subsidies and specifications with conservation outcomes in the ceramic sanitaryware market.

Growth of Organized Home-Improvement Retail & E-Commerce

Omnichannel distribution is compressing discovery-to-purchase cycles for bathroom upgrades and is nudging brands to blend showroom curation with direct digital tools in the ceramic sanitaryware market. Kohler’s network reached 53 U.S. stores by late 2025 after 10 additions in the prior year, and that footprint helps engage designers and homeowners with premium sanitaryware lines in the ceramic sanitaryware market. Forecasts to 2031 show online channels outpacing physical retail growth from a smaller base, which sets expectations for richer product visualization, installation guides, and configurable bundles in the ceramic sanitaryware market. RAK Ceramics invested in new showrooms in Bangladesh in 2024 that integrate digital order capture, which illustrates how display spaces can channel demand toward higher-margin assortments in the ceramic sanitaryware market. As logistics and last-mile partners improve heavy-goods delivery capabilities and returns handling, more categories of ceramic sanitaryware become viable for e-commerce, provided packaging and damage claims are tightly managed in the ceramic sanitaryware market.

Uptake of Prefabricated Bathroom Pods in Commercial Builds

Commercial developers are using prefabricated bathroom pods to shorten installation cycles and reduce on-site complexity, which is reshaping B2B procurement pathways in the ceramic sanitaryware market. The shift places more influence with pod fabricators and system integrators who prefer standardized fixture dimensions and just-in-time deliveries for predictable fit-out schedules in the ceramic sanitaryware market. Geberit’s planned logistics center in North Rhine-Westphalia, slated for commissioning in 2029–2030, is designed for high-volume shipping of concealed systems and components that feed prefabricated solutions, which reflects this structural channel shift in the ceramic sanitaryware market. The approach resonates in healthcare and hospitality projects that require consistent quality and faster room turnover, which widens the addressable pool for project-based sanitaryware bundles in the ceramic sanitaryware market. As pod adoption scales, manufacturers will benefit from modular design libraries and co-engineering programs with pod specialists to lock in multi-year volume in the ceramic sanitaryware market.

Restraints Impact Analysis*

| Restraint | % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Volatile Prices of Feldspar, Clay, Silica, and Natural-Gas/LNG Power | -1.4% | Bangladesh, Pakistan, energy-import-dependent South Asia; EU gas-reliant ceramics clusters | Short term (≤ 2 years) |

| Rising Carbon Costs and Tight Emission Caps on Ceramic Firing Lines (EU ETS, UK CBAM 2027, China Pilot ETS) | -0.8% | EU ETS jurisdictions, United Kingdom, Guangdong–Fujian–Hubei pilot provinces in China | Medium term (2–4 years) |

| Persistent Shortage of Trained Kiln Operators and Maintenance Technicians Slowing Modernization | -0.4% | Bangladesh, Sub-Saharan Africa, parts of Southeast Asia | Long term (≥ 4 years) |

| Share Capture by Lightweight Polymer-Composite and Brushed Stainless-Steel Sanitary Fixtures in Premium Segments | -0.7% | North America, Northern Europe designer bathroom segment, selected Asia luxury projects | Medium term (2–4 years) |

| Source: Mordor Intelligence | |||

Volatile Prices of Feldspar, Clay, Silica, and Natural-Gas/LNG Power

Producers are exposed to energy price volatility because firing cycles depend on uninterrupted high-temperature processes, which pushes energy efficiency to the top of plant-upgrade agendas in the ceramic sanitaryware market. In Europe, ceramics are largely gas reliant and are simultaneously subject to carbon-pricing signals that can raise operating costs, which create strong incentives to electrify kilns and implement heat recovery solutions. On the materials side, feldspar logistics and mining bottlenecks in key exporting countries trigger price spikes and scheduling delays, and those shocks can cascade into delivery lead times for sanitaryware lines in the ceramic sanitaryware market. Manufacturers with diversified sourcing, larger safety stocks, and closer collaboration with mines and processors are better placed to sustain service levels in the ceramic sanitaryware market. As more suppliers switch to hydrogen-ready or fully electric tunnels, the sensitivity to gas supply volatility should ease, but transition costs will remain a near-term margin headwind in the ceramic sanitaryware market.

Rising Carbon Costs and Tight Emission Caps on Ceramic Firing Lines (EU ETS, UK CBAM 2027, China Pilot ETS)

Regulatory instruments that price carbon or cap plant-level emissions are changing cost curves and investment timing across the ceramic sanitaryware market. The European Union Emissions Trading System has covered ceramics since its early phases and recorded an average allowance price near USD 92.1 (EUR 83.47) per tCO2e in 2023, which raised the cost of carbon-intensive firing and aligned returns on electrification projects in the ceramic sanitaryware market[3]Source: International Carbon Action Partnership, “Emissions Trading Worldwide: Status Report 2024,” ICAP, icapcarbonaction.com. The United Kingdom’s Carbon Border Adjustment Mechanism is expected to include ceramics from 2027, which will expose imports to border levies if exporters operate in regions without equivalent pricing, and that will accelerate decarbonization plans among international suppliers serving the UK in the ceramic sanitaryware market. China’s provincial ETS pilots began covering ceramic building and hygiene products, using intensity-based allocations and credit purchases, which adds a compliance layer for manufacturers in Guangdong, Fujian, and Hubei that sell into domestic and export channels in the ceramic sanitaryware market. Emission factors reported in the literature for ceramic production highlight CO2 and acidifying gases that can be mitigated through kiln electrification, green electricity sourcing, and glaze reformulation, which will continue to shape products and process innovation in the ceramic sanitaryware market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Water Closets Lead Growth Through Smart Integration

Wash basins captured 37.33% of the 2025 product-type market size, while water closets are projected to post the fastest advance at a 7.67% CAGR to 2031, setting the tone for premium performance and hygiene features in the ceramic sanitaryware market. Expanded feature sets, such as electrolyzed-water sanitization and integrated bidet functions, support price realization as brands elevate perceived value in water closets within the ceramic sanitaryware market. Kohler’s design-led connected bathing systems, including Anthem+, show how controls and experiences in adjacent categories influence expectations for coordinated bathroom suites in the ceramic sanitaryware market. Additive manufacturing demonstrations, such as Kohler’s 3D-printed vitreous china concepts, spotlight a pathway to rapid iteration and potential scrap reduction, which could compress lead times for select basin formats in the ceramic sanitaryware market. Emerging industrial research suggests that ceramic 3D printing can reduce waste and improve energy footprints under certain geometries, which strengthens the case for targeted deployment in complex sanitaryware parts over the planning horizon.

Urinals and cisterns are advancing more steadily where public and commercial projects move in line with broader construction cycles, which directs emphasis to reliability and maintenance ease in the ceramic sanitaryware market. Bathtubs and shower trays face design shifts toward walk-in configurations in aging-in-place renovations, which favors a subset of SKUs aligned with ease of entry and cleaning. In Europe, renovation continues to anchor demand, and that tilt supports retrofit-friendly product families and concealed systems that integrate smoothly into existing footprints in the ceramic sanitaryware market. As brands coordinate finishes and accessories across collections, the aesthetic coherence of basins, water closets, and fittings helps pull through premium combinations, which can raise average selling prices in the ceramic sanitaryware market. Over the forecast window, the mix of smart-ready and antimicrobial finishes in top-selling categories should deepen differentiation without compromising production efficiency in core lines of the ceramic sanitaryware market.

By End-User: Commercial Hospitality Retrofits Accelerate Antimicrobial Adoption

Residential applications accounted for 62.74% of 2025 demand, and that share reflects stable household formation and renovation cycles that continue to anchor the ceramic sanitaryware market size across key regions. Large urban projects and private household remodels set the cadence for favored SKUs, and that drives scale in basins and water closets that balance performance, cleanability, and style in the ceramic sanitaryware market. Developers in the United Arab Emirates supported solid order flow in 2025, with RAK Ceramics’ domestic revenue up 26.4% in Q2 2025, which reinforced momentum in multi-unit residential and mixed-use complexes in the ceramic sanitaryware market. On the commercial side, hospitality and healthcare operators are upgrading to higher-spec fixtures and flush systems that combine hygiene features with durable glazes, a combination that aligns with brand standards and procurement priorities in the ceramic sanitaryware market. As these upgrades proliferate, suppliers with robust project service teams and modular specification guides will capture more repeat business among institutional owners in the ceramic sanitaryware market.

Commercial applications are expected to expand at a 5.87% CAGR through 2031, supported by retrofit programs, pod-based buildouts, and expanding chains in hospitality and care delivery that require standardized bathrooms across properties in the ceramic sanitaryware market. Product development is converging around touch-free actuation, improved antimicrobial properties, and low-consumption flush solutions, which blend compliance and user experience goals in commercial projects. European bathroom system leaders continue to invest in concealed cisterns and flush plates with slim profiles that ease installation and add aesthetic appeal in renovations in the ceramic sanitaryware market. In emerging markets, the long-term commercial opportunity also depends on reliable energy and water infrastructure, and that sets the context for local partnerships and service models that support uptime across facilities in the ceramic sanitaryware market. Across both residential and commercial uses, brands that align specifications, installation support, and after-sales service are building stickier relationships with channel partners in the ceramic sanitaryware market.

By Distribution Channel: E-Commerce Surge Challenges Showroom Incumbents

Offline channels retained 67.84% of the 2025 distribution, while online is forecast to grow at an 8.98% CAGR through 2031, which will shift customer acquisition dynamics in the ceramic sanitaryware market and raise expectations for digital content and delivery reliability. Showrooms remain pivotal for tactile evaluation and design consultations, and that is why leading brands continue to expand curated spaces that showcase full bathroom solutions within the ceramic sanitaryware market. Kohler added 10 U.S. stores in the year heading into late 2025, and that presence helps seed premium lines and integrated suites in local markets within the ceramic sanitaryware market. RAK Ceramics’ showroom investments in Bangladesh include digital order capture that routes shoppers to broader assortments, which demonstrates how physical footprints can catalyze omnichannel growth in the ceramic sanitaryware market. Over the forecast period, marketplace selling will continue to open entry points for mid-tier brands, while direct-to-consumer channels invest in visualization and installation support tools to reduce returns in the ceramic sanitaryware market.

Trade distribution remains central for large-scale and project work, and that underscores the importance of predictable fulfillment and jobsite-ready packaging in the ceramic sanitaryware market. Logistics investments that stage high-volume components closer to demand centers are becoming more common as suppliers support prefabrication and tight construction schedules in the ceramic sanitaryware market. The rise of pods and standardized room kits is encouraging supply agreements that bundle fixtures, cisterns, and flush controls with installation guidance, which creates a more integrated proposition for contractors in the ceramic sanitaryware market. As brands integrate sustainability metrics like embodied carbon and recycled content into digital product passports, online and offline channels will both play a role in compliance documentation and procurement workflows in the ceramic sanitaryware market. The interplay between showrooms, marketplaces, and direct channels will keep rewarding SKUs with strong content, clear specifications, and reliable last-mile experiences in the ceramic sanitaryware market.

Geography Analysis

Asia-Pacific held 43.39% of the 2025 market size, while North America is set to chart the highest regional advance at a 7.67% CAGR through 2031, which frames the growth map for the ceramic sanitaryware market share and supplier deployment plans. China’s provincial emissions trading pilots have extended coverage to ceramics, where intensity-based allocations and provincial credit purchases now apply in Guangdong, Fujian, and Hubei, and these rules are influencing kiln modernization choices in the ceramic sanitaryware market. In Japan, LIXIL’s revenue mix in fiscal 2024 emphasized the importance of renovations, and that pattern supports a steady pull for concealed systems and retrofit-friendly SKUs across urban housing stock in the ceramic sanitaryware market. Southeast Asian markets continue to expand sanitaryware penetration through private development and improving retail channels, where showroom investments by multinationals are pairing with e-commerce to raise assortment breadth in the ceramic sanitaryware market. As energy system reliability improves and credit conditions normalize, the addressable base for mid-tier products will broaden in key metropolitan corridors in the ceramic sanitaryware market.

Europe remains anchored by renovation activity and compliance-driven upgrades, which reinforce demand for water-efficient flush systems, low-noise concealed cisterns, and durable glazes in the ceramic sanitaryware market. Carbon costs under the EU ETS continue to support returns on electric tunnel kilns and heat recovery deployments, and that is reshaping capex priorities across European production hubs in the ceramic sanitaryware market. The European Water Label registry is a growing procurement reference that helps public agencies and large property owners screen products on performance and conservation, which aligns brand portfolios with subsidy criteria in the ceramic sanitaryware market. Logistical constraints in feldspar supply routes periodically influence cost baselines, and diversification of sources and recycled inputs is becoming part of resilience strategies in the ceramic sanitaryware market. As manufacturers weigh plant electrification and hydrogen-ready conversions, financing terms and green electricity access will be decisive for European cost competitiveness in the ceramic sanitaryware market.

North America is forecast to post a 7.67% CAGR through 2031, with growth supported by smart-ready upgrades, aging-in-place renovations, and strong brand investments in network and production technology within the ceramic sanitaryware market. Kohler’s U.S. expansion in retail and its Casa Grande, Arizona, facility’s focus on energy and water efficiency illustrate how brands are integrating sustainability and operational performance in their strategies for the ceramic sanitaryware market. Canada’s push toward low-emission manufacturing, including electric kilns powered by low-carbon electricity, positions select facilities to supply premium decarbonized lines to the region’s retrofit-heavy channels in the ceramic sanitaryware market. In the Middle East, strong residential and mixed-use pipelines in the United Arab Emirates supported revenue gains for local producers in 2025, and tariff adjustments in Saudi Arabia in late 2024 aided cross-border flows into the ceramic sanitaryware market. Sub-Saharan African markets face skills and energy constraints that slow modernization, which sustains import reliance and shapes mid-tier assortments in the ceramic sanitaryware market.

Competitive Landscape

Competition remains active across multinational leaders and regionally strong brands, and differentiation increasingly rests on decarbonization progress, product system integration, and omnichannel reach in the ceramic sanitaryware market. Roca presented zero-emission sanitary ceramics production capability powered by electric tunnel kilns, signaling a decisive move to eliminate fossil combustion from firing in its showcased lines and setting a sustainability benchmark in the ceramic sanitaryware market. RAK Ceramics commissioned a 162-meter kiln designed for future hydrogen conversion and documented 715 Kcal/kg fuel consumption, which is materially below legacy tunnels and supports cost and emissions objectives in the ceramic sanitaryware market. Carbon-pricing exposure across the EU and border-adjustment signals in the UK are pushing more suppliers to advance electrification and waste-heat recovery at scale in the ceramic sanitaryware market.

Strategic moves also cluster around logistics and channel capabilities that bring full bathroom systems closer to demand in the ceramic sanitaryware market. Geberit’s planned logistics center in North Rhine-Westphalia targets high-volume flows of concealed systems and components to serve prefabricated and renovation projects with shorter lead times in the ceramic sanitaryware market. Kohler continued to scale curated brand showrooms to connect with design professionals and discerning homeowners, while pairing that presence with product platforms that integrate digital controls and water efficiency across categories in the ceramic sanitaryware market. RAK Ceramics expanded retail points in South Asia with digital ordering support, which demonstrates how in-store experience can drive premium upsell and specification wins for project buyers in the ceramic sanitaryware market.

Product and process innovation continue to track toward rapid design iteration and sustainable manufacturing in the ceramic sanitaryware market. Kohler highlighted Anthem+ at KBIS 2025 as part of a connected ecosystem, and that activity aligns with the shift to experiential bathrooms that integrate touchless operation and personalized settings in the ceramic sanitaryware market. Research and pilot programs on ceramic additive manufacturing point to waste and cycle-time advantages for suitable designs, which could be leveraged first in basins and specialty pieces in the ceramic sanitaryware market. Industry associations and company disclosures indicate continuing investment in electric kilns and hydrogen-ready tunnels, and that wave will influence cost structures and product positioning through the decade in the ceramic sanitaryware market.

Ceramic Sanitary Ware Industry Leaders

Roca Sanitario S.A.

Kohler Co.

Toto Ltd.

LIXIL Corporation (INAX, American Standard)

Geberit AG

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2025: Roca Sanitario S.A. launched the world's first zero-emission sanitary ceramics production facility at ISH Frankfurt 2025 using electric tunnel kilns, positioning the brand to avoid combustion emissions and align with carbon-pricing regimes.

- February 2025: Kohler Co. introduced the Anthem+ digital showering valve at KBIS 2025 that enables orchestration of water, light, sound, and steam via the Konnect app, targeting premium renovation demand.

- May 2024: RAK Ceramics unveiled an 8,500 sq. ft. Experience Centre in Bengaluru to showcase sanitaryware, tiles, faucets, and sinks, including premium signature installations.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study defines the ceramic sanitary ware market as all finished bathroom fixtures produced from vitreous china or fire-clay that are permanently plumbed into residential or commercial premises, covering wash basins, water closets, cisterns, bidets, urinals, bathtubs, and related accessories. We exclude loose OEM pieces, refurbished units, and items made from acrylic, stainless steel, or composite stone, so the baseline stays strictly ceramic.

Scope Exclusions: Decorative countertop bowls sold without plumbing fittings and portable chemical toilets remain out of scope.

Segmentation Overview

- By Product Type

- Wash Basins

- Water Closets

- Cisterns

- Bidets

- Urinals

- Bathtubs & Shower Trays

- Accessories (Soap Holders, Shelves, etc.)

- By End-user

- Residential

- Commercial

- Hospitality

- Healthcare

- Institutional & Educational

- Offices

- Retail & Other Commercial

- By Distribution Channel

- Offline

- Sanitary Ware Showrooms & Specialty Stores

- Home Improvement & DIY Chains

- Builders & Contractor Sales

- Online

- Company-Owned E-stores

- Third-Party Marketplaces

- Offline

- By Geography

- North America

- United States

- Canada

- Mexico

- South America

- Brazil

- Peru

- Chile

- Argentina

- Rest of South America

- Europe

- United Kingdom

- Germany

- France

- Spain

- Italy

- BENELUX (Belgium, Netherlands, Luxembourg)

- NORDICS (Denmark, Finland, Iceland, Norway, Sweden)

- Rest of Europe

- Asia-Pacific

- India

- China

- Japan

- Australia

- South Korea

- South East Asia (Singapore, Malaysia, Thailand, Indonesia, Vietnam, Philippines)

- Rest of Asia-Pacific

- Middle East and Africa

- United Arab Emirates

- Saudi Arabia

- South Africa

- Nigeria

- Rest of Middle East and Africa

- North America

Detailed Research Methodology and Data Validation

Primary Research

Mordor analysts spoke with sanitary ware distributors, building contractors, home-improvement retailers, and municipal procurement officers across Asia-Pacific, North America, Europe, the Middle East, and Africa. These conversations clarified average selling prices, uptake of rimless bowls or sensor urinals, and delivery lead-times, allowing us to reconcile desk estimates and close information gaps.

Desk Research

We gathered baseline numbers from public datasets such as UN Comtrade HS 6910 trade flows, Eurostat building permits, US Census housing starts, and India's Swachh Bharat mission dashboards. Insights from the European Bathroom Forum, Plumbing Manufacturers International, and the World Plumbing Council enriched regulatory and efficiency benchmarks. Company 10Ks, IPO filings, and D&B Hoovers profiles provided revenue splits, while shipment trends were cross-checked through Volza customs intelligence and Dow Jones Factiva archives. The sources listed are illustrative, and many additional open feeds were tapped for data collection and validation.

Market-Sizing & Forecasting

We begin with a top-down reconstruction of demand from national production plus net imports, then adjust for inventory swings and the typical 12-15 year replacement cycle. We next cross-check with selective bottom-up samples such as factory output rolls and retailer sell-through ratios to fine-tune totals. Housing completion counts, commercial floor-space additions, unit price inflation, sanitation subsidy beneficiaries, and urban population growth form core model variables. Forecasts are generated via multivariate regression blended with scenario analysis whenever water-saving mandates or construction cycles deviate from trend, and any data gaps are bridged using price proxies vetted during expert calls.

Data Validation & Update Cycle

We pass every iteration through variance dashboards that flag anomalies beyond two standard deviations, followed by peer review. Reports refresh annually, with interim updates if major policy shifts or large project cancellations occur, and before release, an analyst reruns key indicators so clients receive the latest view.

Why Mordor's Ceramic Sanitary Ware Baseline Inspires Reliance

We observe that published estimates often diverge, driven by unequal product mixes, pricing ladders, and refresh cadences.

We find key gap drivers include some publishers bundling composite or plastic fixtures, using list prices instead of weighted transactions, or modeling infrequent updates that miss fast subsidy-led installations in Asia.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 40.38 B (2025) | Mordor Intelligence | |

| USD 47.27 B (2024) | Global Consultancy A | counts acrylic fixtures and applies constant 2020 price deck |

| USD 34.36 B (2024) | Industry Analyst B | excludes bathtubs and shower trays and models only residential demand |

| USD 38.99 B (2025) | Trade Journal C | projects straight-line growth from 2023 without fresh primary validation |

We believe Mordor's disciplined scope selection, live pricing surveys, and annual refresh cycle give decision-makers a balanced and transparent baseline that can be traced to explicit variables and repeatable steps.

Key Questions Answered in the Report

What is the current size and growth outlook for the global ceramic sanitaryware market?

In 2026, the ceramic sanitaryware market size is USD 43.26 billion, and it is projected to reach USD 61.03 billion by 2031 at a 7.13% CAGR.

Which region leads demand, and which will grow fastest through 2031 in ceramic sanitaryware?

Asia-Pacific held 43.39% of 2025 revenues, while North America is expected to grow fastest at a 7.67% CAGR through 2031.

Which product categories are setting the pace in ceramic sanitaryware upgrades?

Water closets are the fastest growing category at a 7.67% CAGR, while wash basins remain the largest by revenue share due to their universal installation footprint.

How are regulations influencing investments in ceramic sanitaryware manufacturing?

EU ETS carbon pricing and UK CBAM signals are accelerating electric kiln adoption and hydrogen-ready conversions, influencing cost structures and plant siting.

What distribution shifts matter most for ceramic sanitaryware through 2031?

Offline showrooms still dominate with 67.84% share, but online is forecast to grow at 8.98% CAGR as richer visualization and delivery solutions expand the addressable set.

Which strategic themes define competition in ceramic sanitaryware today?

Decarbonization of kilns, logistics proximity for prefabrication channels, and integrated digital experiences are key themes shaping competitive advantage.

Page last updated on: