Smart Speaker Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

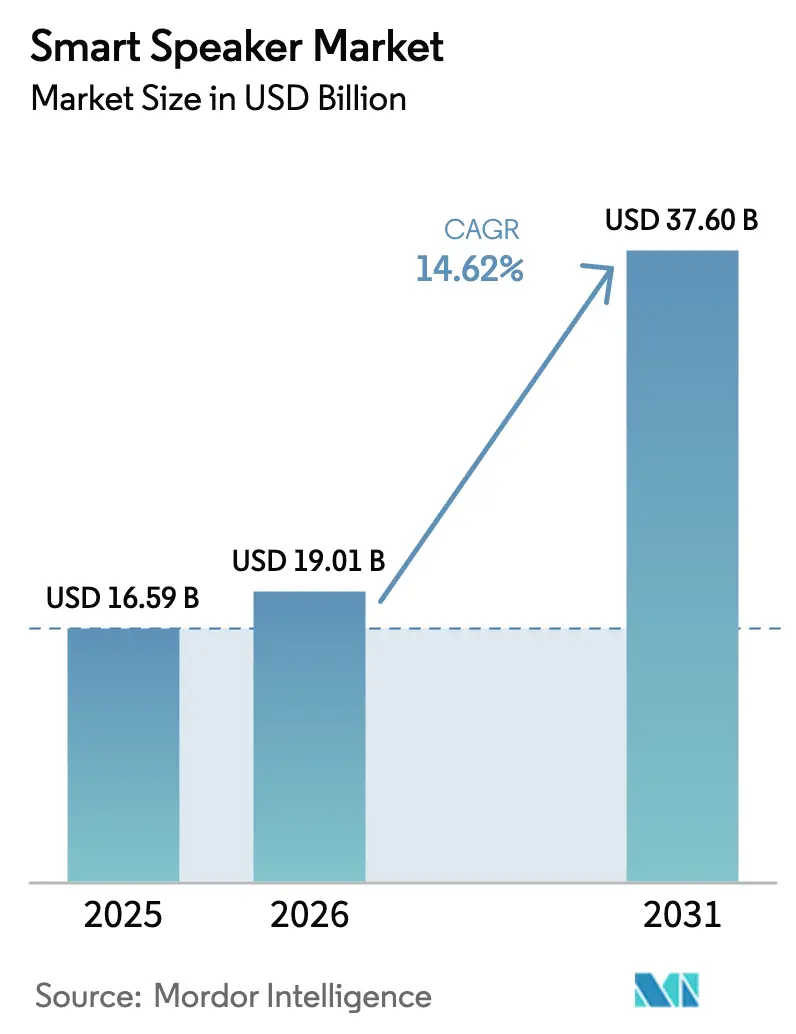

| Market Size (2026) | USD 19.01 Billion |

| Market Size (2031) | USD 37.6 Billion |

| Growth Rate (2026 - 2031) | 14.62% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

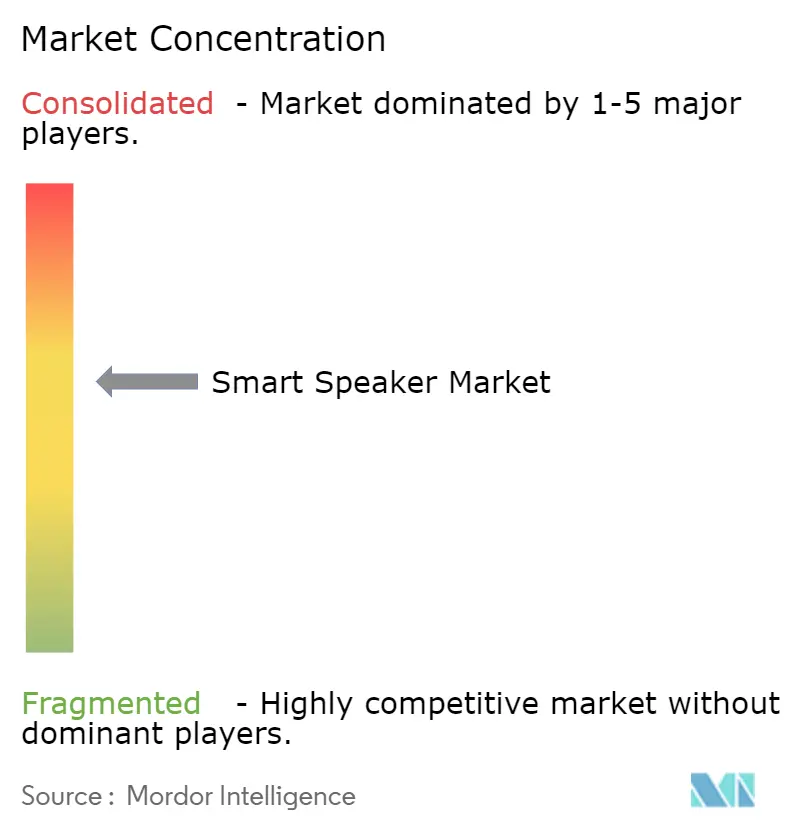

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Smart Speaker Market Analysis by Mordor Intelligence

The smart speaker market size was valued at USD 16.59 billion in 2025 and estimated to grow from USD 19.01 billion in 2026 to reach USD 37.6 billion by 2031, at a CAGR of 14.62% during the forecast period (2026-2031). Solid uptake of generative-AI features, subscription service layers, and Matter-enabled interoperability standards are redefining consumer expectations and sustaining double-digit growth momentum. Platform vendors are layering premium services-Amazon’s Alexa+ at USD 19.99 per month being the most visible example-to move the revenue focus beyond hardware.[1]Amazon News, “Introducing Alexa+, the Next Generation of Alexa,” aboutamazon.com Asia-Pacific leads both volume and velocity, powered by Chinese subsidy programs and 5G home-hub bundles that keep entry prices low while raising functionality. Competitive intensity is accelerating as Google shifts from Assistant to Gemini and Apple deepens on-device processing, while component suppliers consolidate to secure MEMS microphones and edge-AI chips for premium acoustic performance. Rising bill-of-materials costs, fragmented privacy rules, and gaps in multilingual training data temper the outlook but do not derail the overall upward trajectory.

Key Report Takeaways

- By intelligent virtual assistant, Amazon Alexa retained 36.12% of smart speaker market share in 2025; Apple Siri is projected to expand at a 16.56% CAGR through 2031.

- By component, hardware accounted for 80.55% of the smart speaker market size in 2025, whereas software is set to rise at a 20.92% CAGR to 2031.

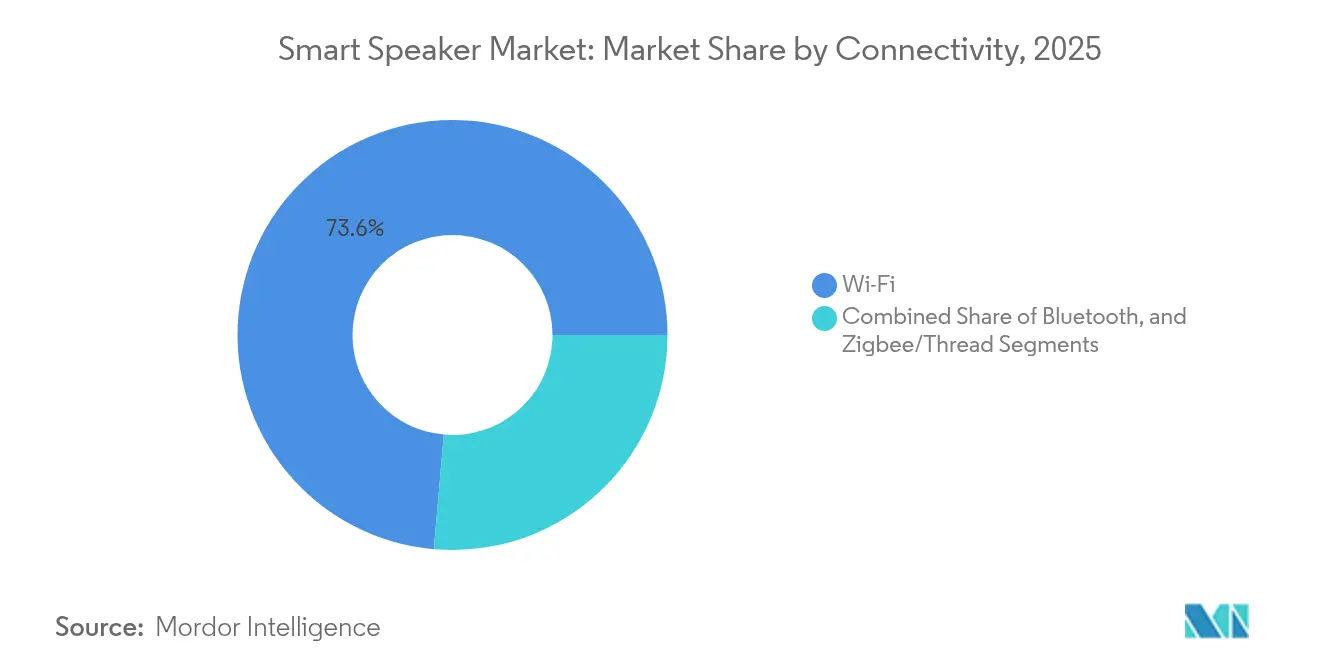

- By connectivity, Wi-Fi led with 73.62% revenue share in 2025; Bluetooth is the fastest mover at an 17.96% CAGR.

- By price band, the low-price segment (< USD 50) commanded 47.88% share of the smart speaker market size in 2025; the premium band (> USD 150) is forecast to grow at 18.58% CAGR.

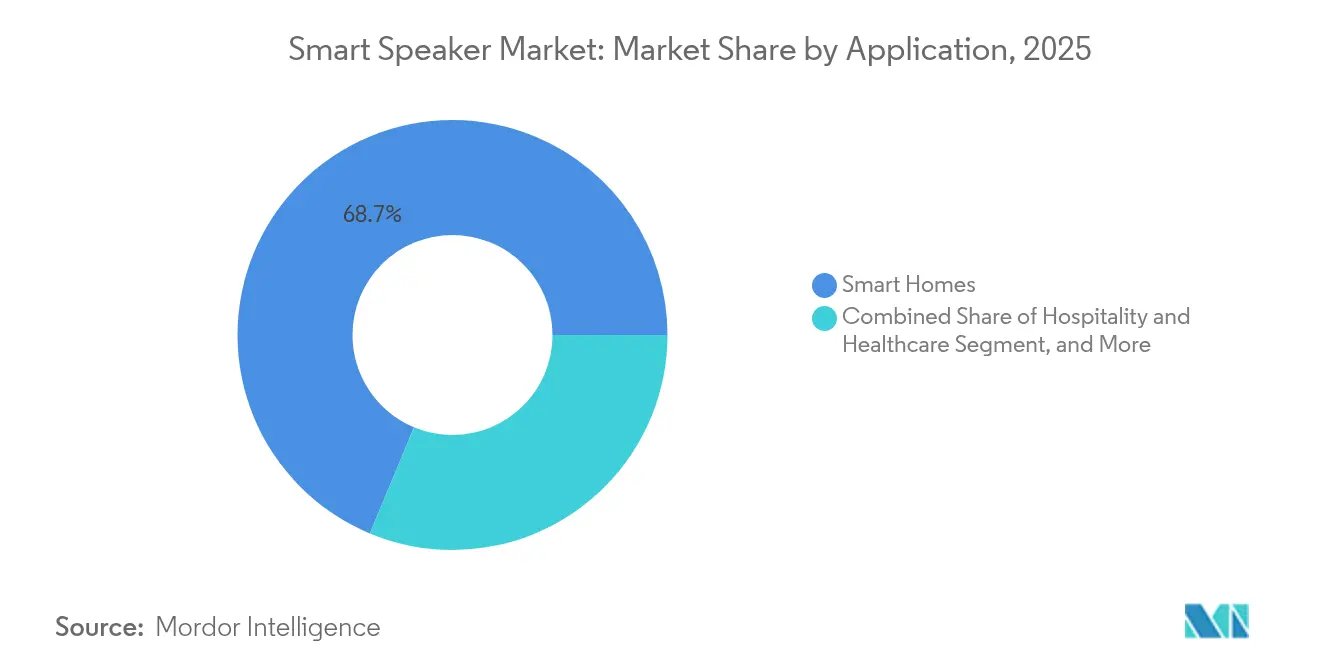

- By application, smart home use captured 68.72% of smart speaker market share in 2025, while hospitality and healthcare applications will climb at 16.68% CAGR.

- By end-user, residential users held 87.95% of market revenue in 2025; commercial deployments are poised for the quickest expansion at 21.96% CAGR

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Smart Speaker Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| AI-driven language localisation in Asia-Pacific | +3.2% | Asia-Pacific core, spill-over to MEA | Medium term (2-4 years) |

| Matter-ready smart-home integration in North America | +2.8% | North America & EU | Short term (≤ 2 years) |

| Subsidised price bundling by Chinese e-commerce giants | +2.1% | China; Southeast Asia follow-on | Short term (≤ 2 years) |

| Enterprise voice-commerce pilots in Europe | +1.9% | UK & Germany lead | Medium term (2-4 years) |

| Telco-led 5G home-hub programs | +1.6% | Japan & South Korea | Long term (≥ 4 years) |

| Automotive OEM partnerships for in-vehicle speakers | +1.4% | US & Germany | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

AI-driven Language Localisation Accelerating Adoption in Asia-Pacific

Region-specific large language models such as SEA-LION and SeaLLM close critical gaps in dialect support, letting smart speakers understand local idioms and code-switching that once stifled uptake. Vendors now treat multilingual capability as a market-entry prerequisite rather than a premium differentiator. The localisation wave lets devices double as educational aides in Indonesia, Thailand, and Vietnam where first-time digital users adopt voice interfaces before keyboards. Competitive advantage increasingly shifts to platforms willing to invest in regional data sets instead of chasing share solely in English-speaking territories. Government funding for indigenous AI research further cements localisation as a durable growth lever.

Integration of Smart Speakers with Matter-Ready Ecosystems in North America

Matter 1.4’s multi-admin feature eliminates the need for separate setup procedures, letting a single device join Amazon, Google, and Apple networks in one step. Apple, Google, and Samsung now accept Matter certification across their Works With badges, stripping months from product launches and lowering testing costs. With 45% of US homes already owning at least one smart-home gadget, simplified interoperability reduces customer friction and unlocks cross-brand automation use cases such as unified energy monitoring. The outcome positions the smart speaker as the orchestration hub for evolving home-energy programs tied to utility demand-response incentives.

Subsidised Price Bundling by Chinese E-commerce Giants Driving Unit Shipments

China’s 15% consumer-electronics subsidy on devices priced below CNY 6,000 keeps retail tags flat even as component costs climb. Xiaomi leveraged the program for its February 2025 Smart Speaker Pro launch, maintaining margins while reaching mass-market volumes. Subsidy-fuelled production scale drives global cost curves down, allowing aggressive pricing in export markets until the scheme sunsets in 2026. The initiative dovetails with Beijing’s goal of building domestic AI competencies, as larger in-market user bases supply rich voice data to train home-grown models.

Enterprise Voice-Commerce Pilots in Europe Boosting B2B Demand

European corporates are scripting full procurement workflows via voice, slashing routine admin time by as much as 40%. Early pilots in the UK and Germany show voice-activated order placement integrating directly with ERP back-ends, signalling a pivot from consumer convenience toward enterprise efficiency. With 97% of firms already experimenting with voice technology and 84% planning budget increases, dedicated commercial-grade speakers with hardened security firmware are entering the European channel.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising on-device BOM costs for premium acoustics | -2.3% | Global; higher pain in value tiers | Short term (≤ 2 years) |

| Fragmented regional data-privacy mandates | -1.8% | EU, China, California | Medium term (2-4 years) |

| Limited multilingual training data for emerging dialects | -1.5% | Africa, LatAm, Southeast Asia | Long term (≥ 4 years) |

| Saturation of early-adopter households | -1.2% | US & Western Europe | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rising On-Device BOM Costs Due to Premium Acoustic Components

High-fidelity MEMS microphones, spatial-audio transducers, and AI-enabled DSPs now account for up to 40% of total device cost, pressuring entry-level pricing strategies. Syntiant’s acquisition of Knowles’ MEMS microphone unit underscores the strategic value of owning the acoustic stack.[2]Syntiant, “Syntiant Closes Acquisition of Knowles Consumer MEMS Microphones,” syntiant.com Manufacturers targeting the sub-USD 50 bracket face the toughest squeeze, balancing minimal margins against user expectations for features like adaptive noise cancellation. Supply-chain constraints add volatility, forcing smaller brands to either migrate up-market or exit.

Fragmented Regional Data-Privacy Mandates

GDPR’s consent rules, China’s data-localisation under PIPL, and California’s CCPA compel vendors to maintain separate firmware builds and data architectures. Compliance overhead raises development cost and complicates cloud-based model training that thrives on pooled datasets. The requirement for regional data enclaves reduces algorithm accuracy gains achievable through global learning loops, nudging companies toward heavier on-device processing that in turn worsens BOM economics.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Intelligent Virtual Assistant: Alexa Leads Despite Siri’s AI Surge

Amazon Alexa captured 36.12% of the smart speaker market share in 2025. The launch of Alexa+ layers multitier AI capabilities, shielding the platform from churn even as Google transitions to Gemini and Apple amplifies Siri’s on-device model. Apple’s privacy-centric stance is fuelling a 16.56% CAGR, appealing to users wary of cloud logging. Meanwhile, Baidu DuerOS and Alibaba AliGenie dominate Chinese install bases via e-commerce tie-ins yet remain geographically bounded. The landscape is tilting toward subscription-based value, shifting competitive vectors away from sheer device counts.

Apple’s accelerated edge-AI rollout reduces latency and lifts user satisfaction scores, pressuring rivals to match on-device inference to avoid bandwidth costs. Samsung’s generative-AI-augmented Bixby demonstrates strategic hedging against dependence on third-party assistants but lacks cross-vendor traction. Emerging contenders such as SK Telecom’s Aster test proactive agent capabilities in North America, signalling an evolution from reactive commands to predictive task management. Over the forecast horizon, convergence in core voice recognition highlights differentiation through ecosystem depth and verticalised services.

By Component: Software Growth Outpaces Hardware Dominance

Hardware still represents 80.55% of 2025 revenue, but software is set to climb 20.92% CAGR as generative-AI orchestration becomes the main value lever. Continuous over-the-air updates give vendors a pathway to monetize post-sale via new skills and premium subscriptions. Chipmakers are baking inference accelerators into connectivity SoCs to offset cloud costs, blending hardware and software roadmaps.

Firmware complexity rises with features such as emotion detection and contextual memory, demanding more robust operating environments. The pivot to software-defined upgrades shortens replacement cycles, with users opting for periodic feature unlocks instead of new hardware. This shift reallocates R&D budgets toward ML engineering and cloud orchestration while nudging OEMs to partner closely with silicon vendors for co-optimised stacks.

By Connectivity: Wi-Fi Dominance Challenged by Bluetooth Innovation

Wi-Fi held 73.62% revenue in 2025 by supporting bandwidth-hungry voice-cloud interactions and multi-room audio. Yet Bluetooth LE Audio and Auracast spark an 17.96% CAGR for Bluetooth by enabling broadcast mode and personal-audio sharing in public venues. Thread and Zigbee adoption rises as Matter mandates multi-protocol hubs, turning premium speakers into interoperability anchors.

Thread 1.4, expected to reach mass rollout in 2026, resolves cross-vendor border-router issues, boosting user confidence in large-scale device pairing. Early 5G integration in Japanese and Korean home hubs proves the appetite for cellular redundancy, albeit at premium pricing tiers. Vendors increasingly pack tri-radio designs (Wi-Fi, Bluetooth, Thread) to future-proof SKUs and avoid channel fragmentation.

By Price Range: Premium Segment Drives Value Innovation

Devices under USD 50 remain volume kingpins at 47.88% share, courtesy of subsidy amplification and stripped-down feature sets. However, premium units above USD 150 outpace all tiers at 18.58% CAGR as households upgrade for spatial audio and multi-model AI. Subscription-bundled hardware eases sticker shock, with Alexa+ effectively subsidising upfront costs through lifetime value calculus.

Component inflation challenges the low-tier economics, compelling OEMs to push mid-range SKUs between USD 51–150 where feature-cost balance resonates with mainstream buyers. Chinese brands exploit scale to undercut rivals while matching spec sheets, forcing incumbents to justify premiums via ecosystem tightness and service integration

By Distribution Channel: Online Retail Maintains Digital Advantage

Online outlets delivered 62.45% of 2025 unit sales, leveraging search optimisation and instant comparison features that suit tech-savvy shoppers. Offline growth at 14.74% CAGR stems from experiential zones in electronics chains where acoustic demos sway premium purchases. Brands blend click-and-collect with showrooming, reflecting an omnichannel norm rather than a binary choice.

Amazon’s own marketplace dominance grants Echo devices prime visibility, prompting competitors to forge exclusive bundles with brick-and-mortar retailers. Hands-on demos mitigate the intangible nature of voice UX, especially for first-time buyers of high-ticket models. Retailers reciprocate by integrating smart-home vignettes that showcase end-to-end automation to spur cross-category sales.

By Application: Smart Homes Lead While Healthcare Accelerates

Smart homes controlled 68.72% revenue in 2025, anchoring the smart speaker market around lighting, security, and entertainment orchestration. Hospitality and healthcare rollouts, expanding 16.68% CAGR, reveal the technology’s migration into professional environments. Hospitals exploit ambient voice capture for electronic health-record updates, trimming clinicians’ documentation time by up to five-fold.

Hotels deploy voice-managed room controls and concierge queries, lifting guest satisfaction while enabling labour cost containment. Smart offices adopt voice-activated AV and facility management that trim meeting setup times. As use cases widen, data-privacy assurances and vertical certifications grow pivotal for supplier selection.

By End-User: Commercial Segment Accelerates Despite Residential Dominance

Residential households delivered 87.95% of 2025 revenue, reflecting early adoption cycles and Prime-led bundling strategies. Commercial demand surges at 21.96% CAGR as enterprises embed voice agents into customer service and supply-chain workflows. Hotel chains forecast 71% growth in room-installed speakers over five years, seeing voice as a differentiator in guest experience.

Enterprise adoption requires specialised APIs, audit logging, and local processing to meet compliance mandates. Vendors respond with ruggedised hardware and enterprise dashboards that manage fleets across sites. Residential replacement cycles now hinge on feature upsells such as spatial audio and proactive task agents, confirming the pivot from penetration to value extraction.

Geography Analysis

Asia-Pacific accounted for 32.48% of 2025 revenue and is on track for a 16.98% CAGR through 2031, powered by China’s subsidy-fuelled volumes and the emergence of regional language models that dismantle linguistic barriers. Xiaomi’s Smart Speaker Pro benefited directly from the 15% subsidy, while Japanese and Korean telcos bundle 5G hubs with speakers to upsell premium connectivity. Southeast Asia’s adoption curve steepens as SEA-LION and SeaLLM enable natural interaction in Bahasa Indonesia, Thai, and Vietnamese.

North America remains the crucible for premium feature testing. Amazon’s February 2025 launch of Alexa+ targets monetisation of a mature user base that already enjoys high smart-home penetration. Matter adoption alleviates long-running compatibility headaches, fostering multi-vendor setups and encouraging replacement purchases focused on added value rather than first-time ownership. Canada and Mexico echo US trends, albeit from lower baselines, helped by shared language support and contiguous retail channels.

Europe posts steady but less explosive gains. Enterprise voice-commerce pilots anchor growth, especially in Germany and the UK, where GDPR drives demand for on-device inference solutions. Nordic buyers demand privacy-first devices, nudging vendors to ship models with local processing defaults. Southern European markets engage via multilingual AI that respects regional dialects, while EU energy-efficiency directives spur interest in speakers that act as energy-management nodes.

Competitive Landscape

The smart speaker market exhibits moderate concentration. Amazon, Google, and Apple leverage deep ecosystems and cloud heft, but share gains are no longer guaranteed as smaller players exploit niches. Syntiant’s acquisition of Knowles’ MEMS microphone division highlights upstream consolidation aimed at de-risking supply and tailoring silicon to AI workloads. Apple’s privacy posture and vertical integration grant differentiation in secure local processing, while Google bets on Gemini’s multimodal finesse.

Regional challengers bolster competitiveness. Baidu and Alibaba rule mainland China through e-commerce integration and Mandarin proficiency, yet struggle abroad. SK Telecom’s Aster agent arrives in North America with proactive task execution, seeking whitespace between consumer-grade assistants and enterprise RPA tools.[4]OpenTools, “SK Telecom’s AI Agent ‘Aster’ Prepares for North American Debut,” opentools.ai Component vendors court OEMs with reference designs that embed Wi-Fi 7, LE Audio, and edge-AI cores, lowering the barrier for new entrants to deliver highly specified devices.

Subscription economics reshape rivalry. Alexa+ introduces a two-sided model where hardware margins can shrink if lifetime service revenue compensates. Apple may replicate the template via bundled services, and Google could fold Gemini Premium tiers into Nest hardware. The field thus tilts toward platforms capable of continuous AI improvement and cross-device synergy rather than single-product leadership.

Smart Speaker Industry Leaders

-

Apple Inc.

-

Amazon.com, Inc.

-

Bose Corporation

-

Sonos, Inc.

-

Google LLC (Alphabet Inc.)

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2025: SK Telecom introduced its proactive AI assistant “Aster” in North America, enabling autonomous task execution across calendars, shopping lists, and IoT routines.

- February 2025: Amazon rolled out Alexa+, a generative-AI upgrade priced at USD 19.99 per month for non-Prime users and complimentary for Prime members, integrating multiple large language models for complex task handling.

- February 2025: Xiaomi unveiled the Smart Speaker Pro featuring upgraded AI and enhanced acoustics, buoyed by China’s 15% subsidy on electronics priced below CNY 6,000.

- January 2025: Apple, Google, and Samsung agreed to accept Matter certification across their Works With programs, streamlining multi-platform smart-home approvals.

- January 2025: Google commenced migration from Assistant to Gemini on smart-home devices, with full phase-out of classic Assistant on most mobiles expected by late 2025.

Global Smart Speaker Market Report Scope

A smart speaker is a wireless electronic device typically equipped with Wi-Fi connectivity and integrated voice assistants such as Amazon Alexa, Google Assistant, and Siri. These convenient devices can be operated remotely through voice commands, also allowing users to manage other smart home gadgets.

The smart speaker market is segmented by intelligent virtual assistance (Amazon Alexa, Google Assistance, Apple Siri, and DuerOS), component (hardware and software), application (smart home, smart office, and consumer), and geography (North America, Europe, Asia-Pacific, Latin America, and Middle East and Africa). The report offers market size and forecast for all the above segments in value (USD).

| Amazon Alexa |

| Google Assistant |

| Apple Siri |

| Baidu DuerOS |

| Alibaba AliGenie |

| Hardware | Transducers and Microphones |

| Connectivity ICs | |

| Power and Amplifier Modules | |

| Software | Firmware/OS |

| NLP and AI Engines |

| Wi-Fi |

| Bluetooth |

| Zigbee/Thread |

| Low (Upto USD 50) |

| Mid (USD 51-150) |

| Premium ( Above USD 150) |

| Online Retail |

| Offline Retail |

| Smart Homes |

| Smart Offices |

| Hospitality and Healthcare |

| Consumer Entertainment (Personal Use) |

| Residential |

| Commercial |

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Nordics | ||

| Rest of Europe | ||

| South America | Brazil | |

| Rest of South America | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South-East Asia | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | Middle East | Gulf Cooperation Council Countries |

| Turkey | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Rest of Africa | ||

| By Intelligent Virtual Assistant | Amazon Alexa | ||

| Google Assistant | |||

| Apple Siri | |||

| Baidu DuerOS | |||

| Alibaba AliGenie | |||

| By Component | Hardware | Transducers and Microphones | |

| Connectivity ICs | |||

| Power and Amplifier Modules | |||

| Software | Firmware/OS | ||

| NLP and AI Engines | |||

| By Connectivity | Wi-Fi | ||

| Bluetooth | |||

| Zigbee/Thread | |||

| By Price Range | Low (Upto USD 50) | ||

| Mid (USD 51-150) | |||

| Premium ( Above USD 150) | |||

| By Distribution Channel | Online Retail | ||

| Offline Retail | |||

| By Application | Smart Homes | ||

| Smart Offices | |||

| Hospitality and Healthcare | |||

| Consumer Entertainment (Personal Use) | |||

| By End-User | Residential | ||

| Commercial | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| Europe | Germany | ||

| United Kingdom | |||

| France | |||

| Nordics | |||

| Rest of Europe | |||

| South America | Brazil | ||

| Rest of South America | |||

| Asia-Pacific | China | ||

| Japan | |||

| India | |||

| South-East Asia | |||

| Rest of Asia-Pacific | |||

| Middle East and Africa | Middle East | Gulf Cooperation Council Countries | |

| Turkey | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Rest of Africa | |||

Key Questions Answered in the Report

What is the current size of the smart speaker market?

The smart speaker market reached USD 19.01 billion in 2026 and is projected to grow to USD 37.6 billion by 2031.

Which region is growing fastest for smart speakers?

Asia-Pacific is the growth leader with a forecast 16.98% CAGR, helped by Chinese subsidies and 5G home-hub bundles.

How are companies monetizing smart speakers beyond hardware sales?

Firms are introducing subscription layers such as Amazon’s Alexa+, which charges USD 19.99 per month for advanced generative-AI capabilities bundled with existing devices.

Why is Matter important for the smart speaker industry?

Matter certification simplifies interoperability across Amazon, Google, and Apple ecosystems, removing setup friction and driving multi-device smart-home adoption.

What is the biggest restraint to smart speaker growth?

Rising bill-of-materials costs for premium acoustic components and fragmented data-privacy regulations increase product costs and complexity, particularly for value-tier devices.

Which application segment outside smart homes is expanding fastest?

Healthcare and hospitality deployments are climbing at a 16.68% CAGR as hospitals and hotels use voice AI to streamline workflows and enhance user experiences.

Page last updated on: