Market Overview

| Study Period | 2020 - 2031 |

|---|---|

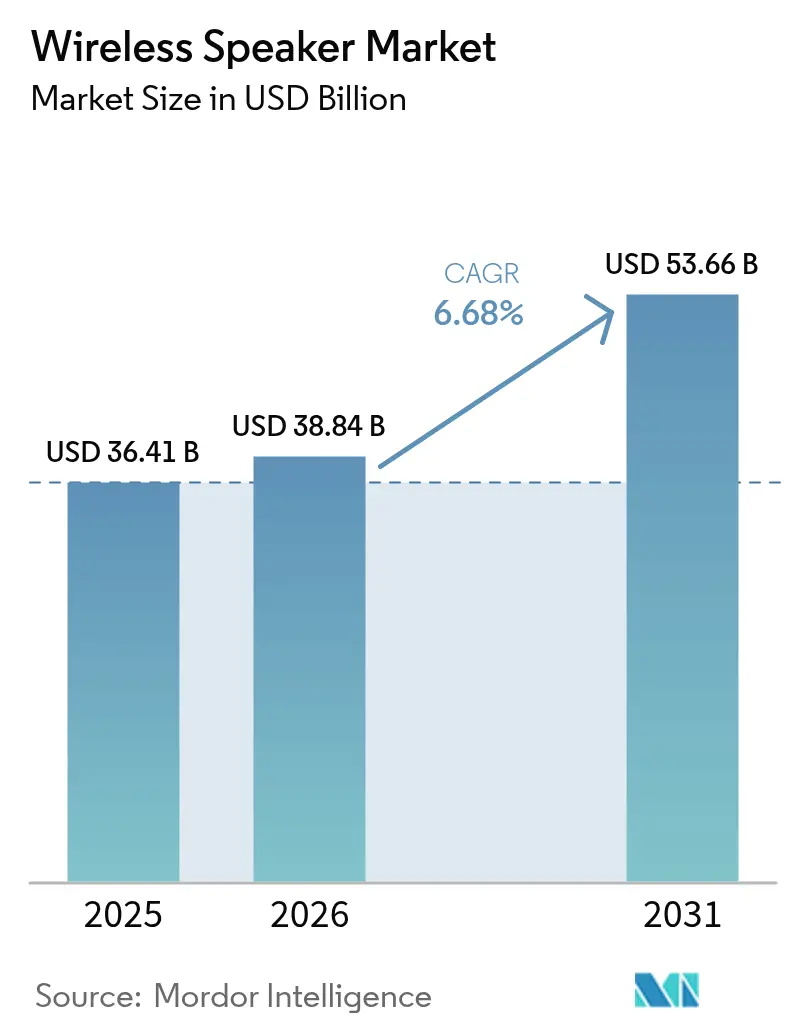

| Market Size (2026) | USD 38.84 Billion |

| Market Size (2031) | USD 53.66 Billion |

| Growth Rate (2026 - 2031) | 6.68% CAGR |

| Fastest Growing Market | Asia |

| Largest Market | Asia |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Wireless Speaker Market Analysis by Mordor Intelligence

The global wireless speaker market size size in 2026 is estimated at USD 38.84 billion, growing from 2025 value of USD 36.41 billion with 2031 projections showing USD 53.66 billion, growing at 6.68% CAGR over 2026-2031. Escalating demand for always-connected audio, the spread of spatial-sound formats and tighter links between voice assistants and smart-home platforms continue to push volume as well as average selling prices. Asia-Pacific leads both size and growth thanks to smartphone ubiquity and competitive local brands, while North America sustains premium demand through content-centric ecosystems. Supply-chain visibility on Class-D amplifier ICs remains a differentiator, helping well-capitalised brands secure production slots. At the same time, automotive OEMs, enterprise hybrid-work tools and social-video-driven, ultra-portable devices create fresh use-case clusters that lift incremental revenue across the value chain. Competitive dynamics now revolve less around raw acoustic wattage and more around AI features, subscription hooks and cross-category integration.

Key Report Takeaways

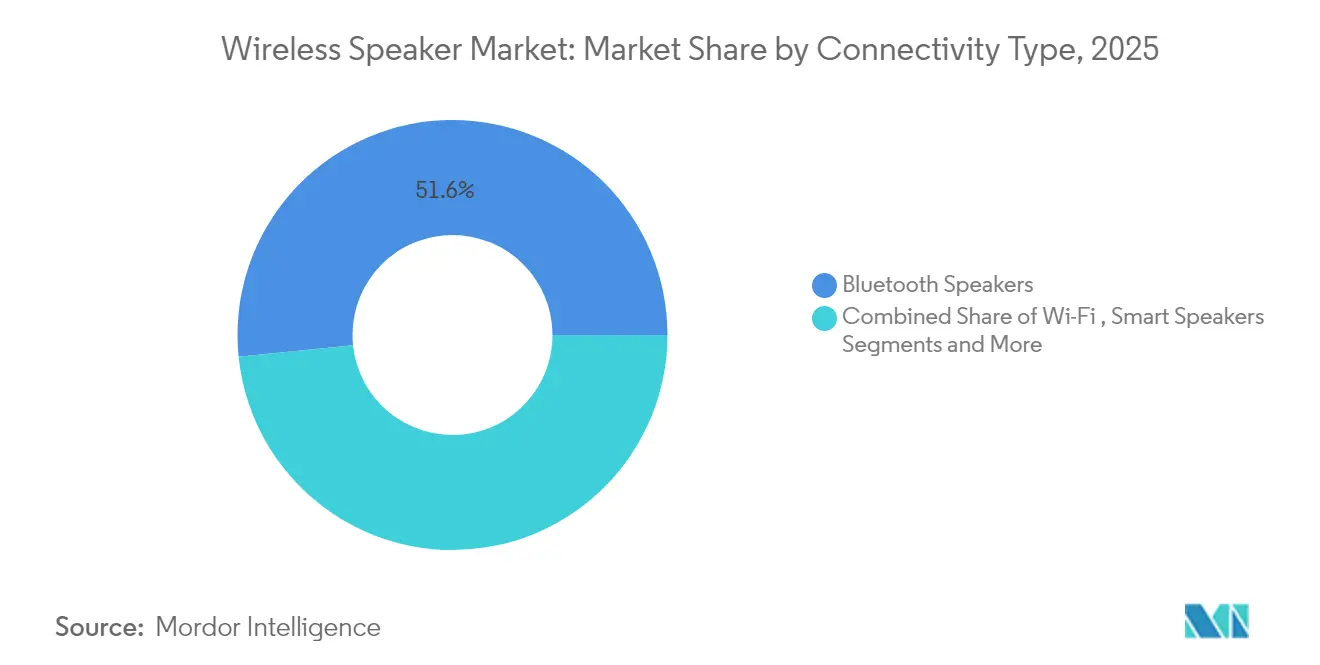

- By connectivity type, Bluetooth commanded 51.62% wireless speaker market share in 2025, while smart speakers are forecast to expand at an 8.12% CAGR through 2031.

- By form factor, portable mini speakers accounted for 40.55% of the wireless speaker market size in 2025, whereas soundbars are projected to grow fastest at a 8.95% CAGR.

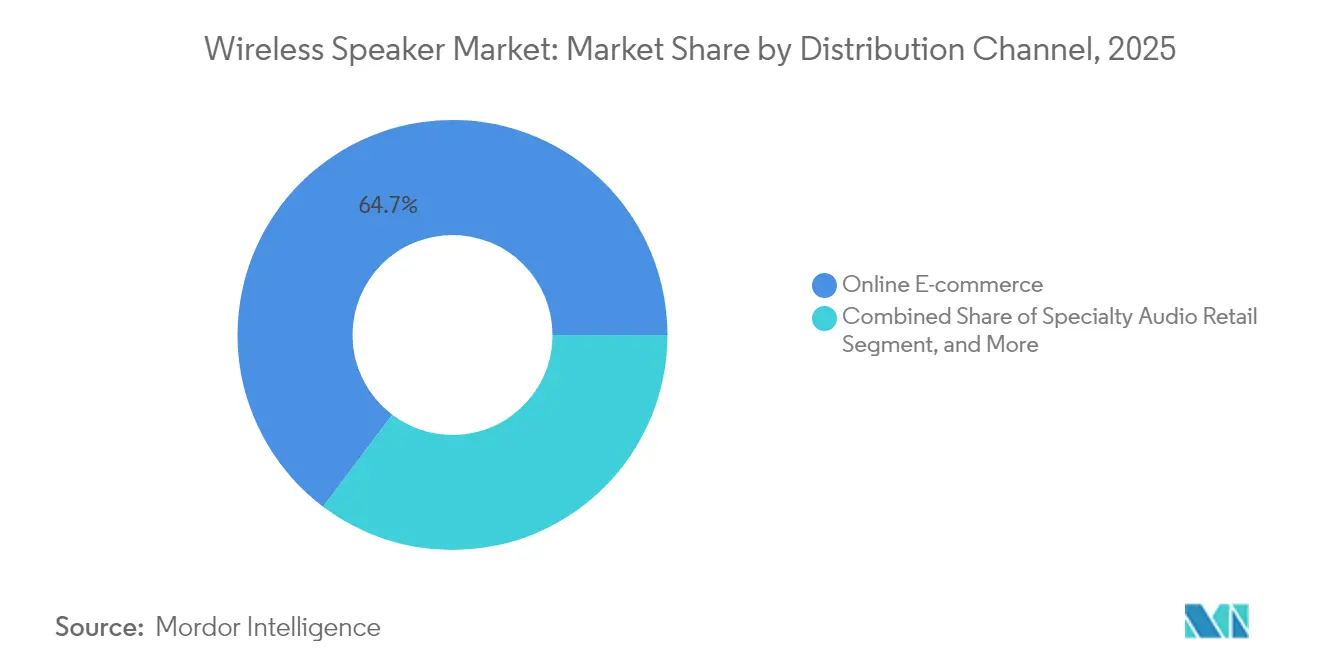

- By distribution channel, e-commerce captured 64.72% of the wireless speaker market size in 2025 and is advancing at a 7.08% CAGR to 2031.

- By end-user, residential use held 77.45% wireless speaker market share in 2025, while automotive OEM integration is rising at a 9.62% CAGR over the forecast period.

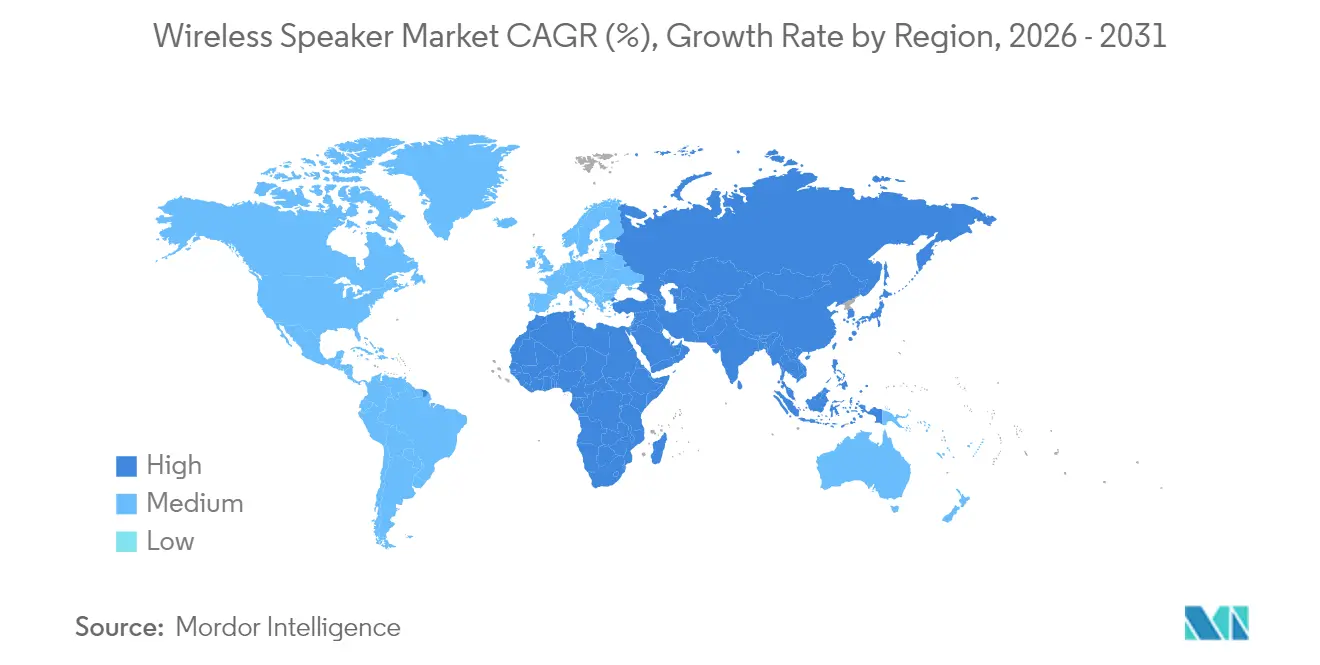

- By geography, Asia-Pacific led with 34.42% revenue share of the wireless speaker market in 2025 and is projected to expand at a 6.78% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Wireless Speaker Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Multi-room audio ecosystems adoption | +1.2% | North America & Western Europe | Medium term (2-4 years) |

| Voice-assistant integration in emerging Asia | +1.8% | China & India | Short term (≤ 2 years) |

| Dolby Atmos soundbar upgrades | +0.9% | Urban China & South Korea | Medium term (2-4 years) |

| Gen-Z short-video-led ultra-portable demand | +0.7% | Brazil & neighbouring markets | Short term (≤ 2 years) |

| Detachable speakers in premium EVs | +0.8% | Early adoption in North America & Europe | Long term (≥ 4 years) |

| Enterprise Bluetooth conference devices | +0.6% | Europe, spill-over to North America | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Voice-assistant Integration Accelerating Smart-speaker Uptake in Emerging Asia

Smart-speaker adoption in China and India jumped when vendors embedded local-language, conversational AI and kept entry prices below USD 40. Amazon’s February 2025 launch of Alexa+, a generative-AI overlay that works on 600 million existing Echo devices, extended hardware life and introduced a USD 19.99 monthly revenue stream. Google’s pivot to Gemini AI for ambient computing signals a broader architectural shift toward cloud-native, multimodal voice experiences. Asian OEMs gain fast-follower advantage because they can license mature voice stacks instead of building proprietary solutions, cutting bill-of-material costs while raising perceived intelligence. Network effects from existing smart-home assets such as bulbs or cameras further lower adoption friction for first-time buyers.

Dolby Atmos Soundbar Upgrades Fueling ASP Growth in Urban China and South Korea

City-dwelling consumers in these markets are moving away from legacy 2.1-channel bars toward Dolby Atmos-enabled bundles that include wireless surrounds. MediaTek and Dolby unveiled FlexConnect in January 2025, allowing soundbars to auto-calibrate with any compatible speaker in the room, removing HDMI-cable constraints.[1]MediaTek Inc., “MediaTek and Dolby Atmos FlexConnect,” MediaTek, mediatek.com Sony’s BRAVIA Theatre line uses 360 Spatial Sound Mapping to simulate multi-speaker environments without ceiling drivers. Higher audio immersion supports USD 300-plus price points, lifting overall wireless speaker market average-selling-price even as unit volumes stay flat.

Automotive OEM Detachable-speaker Partnerships in Premium EVs

Electric-vehicle makers treat differentiated cabin sound as a selling point equal to range or acceleration. Cadillac’s OPTIQ and VISTIQ ship with 19- and 23-speaker Dolby Atmos packages able to detach for tail-gate scenarios, turning the vehicle into a mobile jukebox.[2]General Motors, “GM Brings Dolby Atmos with Amazon Music to Cadillac EV Lineup,” General Motors, news.gm.com McIntosh’s 19-speaker array in the Jeep Wagoneer S applies a similar strategy for lifestyle positioning. Meanwhile, HARMAN’s SeatSonic shifts loudspeakers into headrests, saving weight and energy while enabling driver-specific sound zones. These integrations open OEM revenue pools beyond traditional aftermarket upgrades and feed secondary demand for over-the-air EQ presets.

Hybrid Workspaces Driving Enterprise Bluetooth Conference Speakers in Europe

Return-to-office policies are fluid, so companies equip hot desks and huddle rooms with plug-and-play audio. The EPOS EXPAND 80 covers 16-person spaces through beamforming microphones and Teams certification.[3]EPOS, “EXPAND 80,” EPOS, eposaudio.com Jabra’s Speak 510 offers sub-USD 130 portability for remote staff, and beyerdynamic’s IP64-rated SPACE MAX provides 25-hour battery life for outdoor workshops. Enterprises prefer Bluetooth plus USB-C connectivity for frictionless switching between laptops and phones, underpinning double-digit shipment growth in Western Europe since 2024.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Bluetooth codec fragmentation | -0.40% | Japan & Germany | Medium term (2-4 years) |

| High import tariffs on finished devices | -0.60% | Brazil & India | Short term (≤ 2 years) |

| Privacy concerns around smart speakers | -0.50% | France & Canada | Long term (≥ 4 years) |

| Class-D amplifier IC shortages | -0.80% | Asian manufacturing hubs | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Smart-speaker Privacy Concerns Limiting Household Adoption in France and Canada

Supervisory authorities such as France’s CNIL remind users that voice data may feed undisclosed algorithm training, prompting stricter consent settings.[4]CNIL, “Assistants vocaux : les conseils,” CNIL, cnil.fr Surveys show over half of French and Canadian households fear unintentional eavesdropping despite appreciating convenience. Vendors respond with local-processing modes and physical mute toggles, yet scepticism slows replacement cycles and keeps the addressable base below neighbouring markets.

Class-D Amplifier IC Shortages Delaying Mid-tier ODM Production in Asia

Global chip turbulence pushed some audio-grade IC lead-times above 60 weeks in 2024, forcing contract manufacturers to redesign boards or accept lower margins. Texas Instruments introduced 1-inductor Class-D reference designs at CES 2025 to trim component counts. Brands with forward-buy agreements or multi-sourcing secure launch windows, while smaller ODMs risk missing peak holiday demand, tempering overall wireless speaker market expansion in the short term.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Connectivity Type: Smart-speaker Growth Outpaces Bluetooth Leadership

Bluetooth held 51.62% of the wireless speaker market share in 2025, anchoring its dominance on ubiquity and pairing simplicity. Smart-speaker connectivity, helped by Wi-Fi dual-band chips and edge-AI advances, is forecast to rise at an 8.12% CAGR, gradually eating into basic Bluetooth volumes. The wireless speaker market size for cellular-enabled units remains low-single-digit, but satellite connectivity proofs-of-concept targeting RVs and maritime users hint at new price tiers. Emerging Bluetooth LE Audio with Auracast narrows latency, offering broadcast mode that can stream a concert feed to hundreds of personal speakers, reinforcing relevance for public venues. Legacy AirPlay-only devices continue to shrink as consumers request cross-platform support.

Wi-Fi-centric speakers outside the smart category sustain interest among audiophiles who prioritise lossless playback. Multi-room platforms now expose Matter-compatible schemas, easing interoperability pains. As chipset prices fall below USD 8, several tier-two Asian makers plan to upgrade entry-level models to Wi-Fi-plus-Bluetooth, balancing cost and ecosystem access.

By Form Factor: Soundbars Capture Value While Minis Command Units

Portable minis contributed the largest shipment volume, translating into 40.55% of the wireless speaker market size in 2025. Nevertheless, soundbars delivered superior revenue growth, advancing at a 8.95% CAGR, because cinema-grade Atmos decoding lifts average prices. Party speakers add light shows and microphone inputs, tapping Gen-Z social-video behaviour. Rugged clip-on variants meet demand for biking and hiking audio, featuring IP67 ratings and 12-hour batteries. Floor-standing wireless towers occupy a high-margin niche serving living-room audiophiles unwilling to route speaker cables.

Smart-display speakers remain a hybrid segment merging voice, touch and video chat, finding adoption in kitchens for recipe walkthroughs or surveillance camera feeds. As mini-LED costs fall, manufacturers experiment with eight-inch panels on swivel mounts, preserving compact footprints.

By Distribution Channel: E-commerce Extends Its Lead

Online platforms represented 64.72% of the wireless speaker market size in 2025 and post the fastest 7.08% CAGR because comparison shopping and flash deals align with tech-savvy buyers. Brand-owned web-stores deepen margins by bundling extended warranties and music-service trials. Specialist audio retail still matters for USD 1,000-plus models where live demos influence perceptions of soundstage. Mass-merchandisers handle impulse purchases under USD 50, especially during holiday promotions.

Automotive dealerships increasingly bundle detachable cabin speakers, capturing yet another non-traditional channel. Commercial installers focus on hospitality and education, integrating ceiling speakers with BYOD wireless hubs to reduce wiring costs.

By End-User: Automotive OEM Uptick Amid Residential Dominance

Residential applications commanded 77.45% of the wireless speaker market size in 2025, confirming that multi-room audio and smart-home hubs remain core purchase drivers. Families increasingly position compact speakers in kitchens, bathrooms and outdoor spaces, turning voice control into a default household interface. Streaming-service bundles and seasonal discounting keep replacement cycles brisk as consumers upgrade to spatial-audio-ready models. Hotel chains and cafés add background-music speakers with Wi-Fi mesh support to elevate guest experience, though these commercial installs still trail the large residential base. Conference-room upgrades in hybrid workplaces contribute incremental demand, but enterprise volumes only nibble at overall wireless speaker market share when compared with home use [eposaudio.com].

Automotive OEM integration is the fastest mover, projected to expand at a 9.62% CAGR as electric-vehicle launches showcase detachable cabin speakers and Dolby Atmos arrays. Cadillac’s OPTIQ and VISTIQ EVs, for example, ship with 19- and 23-speaker packages that double as tail-gate sound systems, underscoring how premium audio now bolsters vehicle pricing power [news.gm.com]. Partnerships between audio specialists and carmakers also create recurring revenue via over-the-air EQ updates that refresh in-car sound without new hardware. Corporate fleets begin specifying portable conference speaker kits for mobile offices, further stretching the end-user mix. While residential units will keep leading absolute volumes, automotive deployments and niche professional uses together form the next growth leg for the wireless speaker market.

Geography Analysis

Asia-Pacific contributed 34.42% of 2025 revenue and is projected to rise at a 6.78% CAGR thanks to scale manufacturing, cost-competitive brands and rapid 5G handset take-up. China anchors volume, combining local AI platforms with sub-USD 25 entry devices. South Korea and Japan chase premium niches, though codec fragmentation postpones audiophile upgrades. India’s import-tariff hikes encourage domestic assembly, with several handset brands diversifying into speakers to capture accessory spend.

North America retains a sizeable premium segment, driven by subscription ecosystems linking smart speakers to home-security and media bundles. United States consumers show willingness to pay for AI enhancements such as Amazon Alexa+, whereas Canada’s adoption curve flattens because privacy concerns curb living-room placement. Mexico benefits from cross-border fulfilment centres that cut delivery times for mid-range products.

Europe remains a mixed picture. Western Europe outperforms on multi-room adoption, with Scandinavian markets favouring sustainable materials and repairability. France’s cautious stance on always-listening devices slows smart-speaker uptake, while Germany’s hi-fi enthusiasts wait for unified lossless Bluetooth before replacing wired rigs. Central and Eastern Europe expand entry-level Bluetooth sales via e-commerce, offsetting weaker retail networks.

South America sees brisk demand for ultra-portable speakers that double as content-creation props for short-video platforms. Brazil’s high duties push brands to move final assembly onshore or consider MicroSD-equipped models that sidestep streaming data costs. Chile and Colombia import mid-priced soundbars as fibre broadband coverage widens.

Regulatory Landscape

Wireless speakers sold in the United States typically require U.S. Federal Communications Commission (FCC) equipment authorization processes for radio-enabled electronics under 47 CFR Part 2 (Subpart J), which affects product testing, labeling, and time-to-market for Bluetooth and Wi-Fi models. In the European Union, wireless speakers fall under the Radio Equipment Directive (RED) 2014/53/EU, and the cybersecurity requirements for internet-connected radio equipment under RED Article 3(3) became mandatory from 1 August 2025. This has prompted brands to build security-by-design into products and to demonstrate conformity against relevant harmonized standards when placing smart speakers and connected soundbars on the Union market.

Trade and tariff exposure continues to depend on tariff classification for cross-border shipments of speakers and smart speakers. U.S. Customs and Border Protection (CBP) rulings and the U.S. International Trade Commission (USITC) Harmonized Tariff Schedule (HTS) framework often differentiate loudspeakers, commonly under HTS heading 8518, from certain multifunction smart speakers with bidirectional communications that may be treated under 8517, which can change duty outcomes and compliance documentation requirements. This classification sensitivity is especially relevant for global brands using multi-country assembly and direct-to-consumer e-commerce fulfillment models, where landed-cost control and correct declarations influence channel pricing and margin protection.

Value Chain Analysis

The wireless speaker value chain begins with upstream electronic and acoustic components, including wireless chipsets, Class-D amplifier stages, drivers, microphones, and lithium-ion batteries, and then moves through ODM/OEM design, assembly, certification, and distribution. Component availability remains a key constraint, since long-lead-time parts such as audio-grade amplification and connectivity silicon can delay launch schedules, while speaker performance differentiation increasingly depends on firmware, microphone arrays, and streaming and voice integration stacks above commodity hardware. For smart speakers and premium soundbars, platform and ecosystem layers, such as voice assistants, multi-room protocols, and streaming services, shape BOM choices and also drive ongoing software maintenance costs.

Manufacturing and final assembly are concentrated in Asia, with China central to the specialized supplier ecosystem for acoustics, plastics, and electronics sub-assemblies, while secondary locations such as Vietnam are used for diversification and final-stage processes in some supply chains. The chain is exposed to geopolitics and material dependencies, including China export controls on certain rare earth materials used in high-performance magnets in April 2025, which tightened availability and pushed sourcing teams toward multi-supplier qualification. Downstream, online channels dominate go-to-market for many brands, while specialty audio retail and OEM-fitted or integrator networks remain important for premium demos, soundbar bundles, and automotive OEM programs where installation and tuning are part of the customer experience.

Competitive Landscape

Competition intensifies as platform owners leverage AI and subscription economics. Amazon, Google and Apple commanded roughly 45% of 2024 global shipments, bundling voice assistants and multi-room protocols to lock users in. Sonos, Bose and JBL defend share with acoustic engineering and brand equity, but face margin pressure as entry-level smart speakers close the perceived audio-quality gap. Samsung’s Harman subsidiary blends consumer, professional and automotive capabilities, fielding models that cross-sell to its TV and smartphone bases.

Emerging Chinese vendors such as Xiaomi and Anker grow rapidly on low-cost, feature-rich launches, often first to adopt new Bluetooth or battery chemistries. European specialists including Devialet position on design and patent-protected acoustic architecture, targeting luxury segments. Semiconductor shortages encourage vertical integration; Apple’s in-house silicon cuts reliance on merchant chips, while Sony and LG co-design Class-D stages with fab partners to secure allocations.

Strategic moves reveal two axes: ecosystem-centric expansion and niche-use-case specialisation. Amazon’s Alexa+ subscription illustrates the former, converting hardware users into recurring subscribers. At the other end, brands like EPOS capitalise on enterprise hybrid-work budgets by tailoring firmware for conferencing platforms. Automotive alliances, visible in GM-Dolby and Jeep-McIntosh tie-ups, signal a new battleground where cabin acoustics influence vehicle differentiation.

Wireless Speaker Industry Leaders

Bose Corporation

Samsung Electronics Co. Ltd. (Harman International Industries Inc.)

Sony Corporation

Amazon.com Inc

Sonos Inc.

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

Standards-driven interoperability and broadcast audio create whitespace across consumer, venue, and enterprise use cases. Bluetooth LE Audio with Auracast is shifting from device-level features to platform-level behavior, and the Bluetooth SIG has highlighted Auracast support at the operating-system layer in Android 16, improving discovery and control for multi-device listening in public and shared environments. That reduces friction for adjacent categories such as venue-friendly portable systems, assistive listening deployments, and multi-speaker party setups that do not depend on a single-brand app ecosystem.

Home audio ecosystems are also moving beyond proprietary walled gardens, which supports modular upgrades and cross-brand streaming compatibility as a purchase trigger. Bose announced general availability of its Lifestyle Collection in May 2026 with built-in support for Google Cast, Apple AirPlay, and Spotify Connect alongside Bluetooth, aligning with demand for flexible source switching across phones, TVs, and streaming services. At the same time, smart-home convergence is expanding the channel for wireless speakers, and Google started shipping a new Google Home Speaker in June 2026 that functions as a Matter controller and Thread Border Router. This reinforces speakers as smart-home infrastructure rather than standalone playback devices, and it encourages product strategies that address audio, control, and connectivity expectations together.

Recent Industry Developments

- July 2026: Marshall Group launched the Acton IV and Stanmore IV wireless home speakers, adding Bluetooth Auracast alongside acoustic updates such as upgraded tweeters and redesigned bass ports. The lineup also introduced repairability elements via replaceable parts, positioning durability and serviceability as competitive attributes in the home speaker segment.

- June 2026: Bose Corporation acquired StreamUnlimited Engineering GmbH, a provider of integrated streaming software platforms and hardware modules used in connected audio systems. The deal strengthens Bose's control over the streaming and connectivity software layer, supporting faster feature rollout and deeper integration across Wi-Fi and multi-room products.

- March 2025: General Motors implemented Dolby Atmos with Amazon Music on Cadillac EVs, equipping vehicles with 19- and 23-speaker arrays as standard depending on the model. This expands OEM-fitted, premium multi-speaker deployments and reinforces automotive cabins as a high-value endpoint for wireless speaker technologies and tuning ecosystems.

Research Methodology Framework and Report Scope

Market Definition and Coverage

This market covers revenue generated from wireless speakers that receive audio over wireless connectivity, including portable and fixed form factors that are bought for home and commercial listening and entertainment.

Scope exclusions: Excludes wired-only speakers, passive speaker cabinets sold without wireless audio electronics, and replacement parts and accessories sold as standalone items.

Segmentation Overview

- By Connectivity Type

- Bluetooth

- Wi-Fi (incl. Combo, excl. Smart)

- Smart Speakers

- Cellular/LTE Speakers

- By Form Factor

- Portable Mini/Pocket-Sized

- Soundbars

- Smart-Display Speakers

- Floor-Standing/Tower

- Clip-on/Sports and Outdoor

- By Distribution Channel

- Online E-commerce

- Specialty Audio Retail

- Mass-Merchandisers/Hypermarkets

- OEM-Fitted and Installer Networks

- By End-User

- Resdential

- Commercial

- Hospitality Corporate/Enterprise

- Automotive OEM

- Others (Education, Public Venues)

- By Geography

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Nordics

- Rest of Europe

- South America

- Brazil

- Rest of South America

- Asia-Pacific

- China

- Japan

- India

- South-East Asia

- Rest of Asia-Pacific

- Middle East and Africa

- Middle East

- Gulf Cooperation Council Countries

- Turkey

- Rest of Middle East

- Africa

- South Africa

- Rest of Africa

- Middle East

- North America

Data Sources, Market Sizing, and Validation

Desk Research

Desk research is used to set the starting structure for the model and to ensure our assumptions align with what is visible in public data. We mainly look for signals that explain demand, such as consumer electronics shipment trends, household connectivity, and retail seasonality, which we then map to wireless speaker adoption.

Common public sources include US Census retail trade releases, OECD and World Bank macro indicators, ITU connectivity statistics, UN Comtrade trade codes for audio equipment flows, and standards and regulatory references from bodies such as the FCC and the European Commission. We also use company filings and investor presentations, reputable press coverage on product cycles, and selective paid subscriptions for company financials and intelligence, news and financials, patent databases, and shipment-level trade records where available. These examples are not exhaustive, and we used additional public sources for data collection, validation, and clarification.

Primary Interviews and Surveys

Primary work is used to pressure-test the market math and to close gaps that desk research does not answer well, especially around mix shifts between Bluetooth and Wi-Fi products and channel pricing. We speak with a mix of manufacturers, component and channel participants, and commercial buyers across APAC, EMEA, and the Americas, then we circle back when inputs do not align with observed demand signals.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 35% | CXOs: 12% | APAC: 51% |

| Mid tier: 51% | Functional/Unit leaders: 28% | EMEA: 29% |

| Smaller Players: 14% | Managers: 60% | Americas: 20% |

Market-Sizing & Forecasting

The sizing starts with a top-down build where consumer electronics spend and device penetration indicators are translated into a wireless speaker demand pool, then converted into revenue using observed price bands and mix. To keep the total realistic, we check it using selective bottom-up approximations, such as sampled average selling price (ASP) by channel multiplied by implied unit volumes from shipment and retail signals, then adjust where the two views do not match.

Key inputs used in the model include wireless speaker shipment and trade movement proxies, the direction of online versus offline channel share, portable versus fixed mix, Bluetooth versus Wi-Fi connectivity mix, and ASP progression during major launch and promotion windows. For forecasting, we run scenario analysis around replacement cycles, smart home attachment rates, and inflation-driven pricing. We then align the final trajectory to what interviewees indicate in their order books and product roadmaps. Where direct unit visibility is weak in a country, we use ratios from comparable markets and scale back using income and connectivity indicators so the gap-fill does not overstate demand.

Data Validation & Update Cycle

Outputs are cross-checked against independent signals, including import and export direction, channel inventory commentary, and consumer electronics retail growth. This helps catch values that look too high or too low for the demand context. When a variance is spotted, we re-test assumptions such as ASP, mix, or adoption, and we re-contact relevant respondents if the gap is material.

A multi-step review is followed before sign-off, including peer checks on formulas, unit consistency, and currency conversion timing. Reports are refreshed annually, and interim updates are made when major events materially change pricing, supply, or demand. Before delivery, a final review pass is completed so clients receive the latest updated view.

Mordor Intelligence's Wireless Speaker Market Size Versus Other Published Estimates

Published market values for wireless speakers can differ widely, even when the market name looks identical, because each publisher counts different device categories, price points, and revenue points along the chain. Timing also contributes, since a model built on a newer pricing cycle or a different currency conversion month can shift the market total by a noticeable amount.

Passive speaker cabinets sold without wireless audio electronics sit outside Mordor Intelligence's scope, and that single exclusion explains a meaningful part of the spread versus estimates that blend wired and wireless speaker revenue. Other gaps typically come from whether factory-gate revenue is used versus retail value, how bundles and smart-home speaker ecosystems are treated, and whether ASP change is assumed from promotions or from list prices, which tends to push totals in opposite directions.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 38.84 B (2026) | |

| Global Consultancy A | USD 39.28 B (2025) | Uses a 2025 base year and a broader technology list that may blend voice-enabled speakers and adjacent wireless audio categories, which can shift totals depending on how smart features and bundles are counted. |

| Trade Journal B | USD 45.07 B (2025) | States a factory-gate revenue lens and reports a higher 2025 value, which can diverge from retail-value based builds and may reflect wider inclusion of creator-sold related services and a different cut of product scope. |

Across the three values, the biggest pattern is that scope boundaries and the revenue point being measured drive more variation than the arithmetic itself. By keeping variables like connectivity mix, channel pricing, and replacement behavior explicit, our model stays traceable to inputs that can be rechecked and updated without rewriting the full logic.

Key Questions Answered in the Report

What is the current value of the wireless speaker market?

The wireless speaker market stood at USD 38.84 billion in 2026 and is on track to reach USD 53.66 billion by 2031.

Which region leads the wireless speaker market and why?

Asia-Pacific leads with a 34.42% revenue share due to high smartphone penetration, competitive local brands and large-scale manufacturing capacity.

How fast are smart-speaker connectivity segments growing?

Smart-speaker connectivity is projected to rise at an 8.12% CAGR between 2026 and 2031 as voice-AI capabilities improve and ecosystem integration deepens.

Which distribution channel is most important for wireless speakers?

E-commerce dominates with 64.72% of 2025 revenue and continues to grow fastest at a 7.08% CAGR, reflecting direct-to-consumer purchasing preferences.

Why are automotive OEMs important to the wireless speaker market?

Premium electric vehicles embed detachable, multi-speaker systems to differentiate cabin experiences, pushing the automotive segment to a 9.62% CAGR through 2031.

What are the major factors restraining wireless speaker adoption?

Key restraints include Bluetooth codec fragmentation in audiophile markets, privacy concerns in countries like France and Canada, and ongoing Class-D amplifier chip shortages.

Page last updated on: