India Consumer Speaker Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

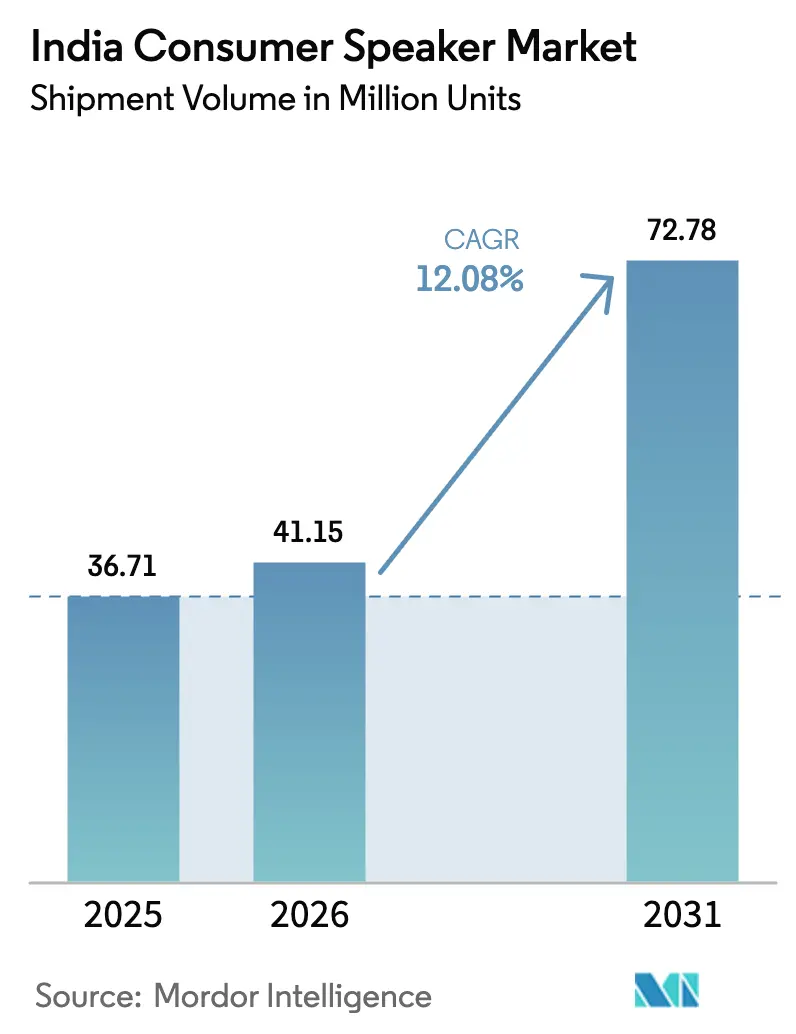

| Base Year Market Size (2025) | 36.71 Million units |

| Market Volume (2026) | 41.15 Million units |

| Market Volume (2031) | 72.78 Million units |

| Growth Rate (2026 - 2031) | 12.08% CAGR |

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

India Consumer Speaker Market Analysis by Mordor Intelligence

India Consumer Speaker market size in 2026 is estimated at 41.15 Million units, growing from 2025 value of 36.71 Million units with 2031 projections showing 72.78 Million units, growing at 12.08% CAGR over 2026-2031. Volume growth reflects steady gains in discretionary incomes, aggressive 5G and fiber roll-outs, and the government-led drive to anchor more audio production locally. Wider adoption of connected televisions is translating into attach rates for companion soundbars, while smartphone ubiquity keeps Bluetooth-only models relevant for price-sensitive buyers. Local firms such as boAt and Zebronics are capitalizing on production-linked incentives to shorten design-to-launch cycles and defend share against international brands. Supply-chain headwinds around rare-earth magnets remain a cost threat, yet the market continues to absorb premium models as urban consumers pay for multi-room audio and voice-assistant convenience. Competitive intensity is rising, but the sheer scale of demand from tier-2 and tier-3 cities sustains a broad playing field across price tiers.

Key Report Takeaways

- By device type, wireless speakers led with 51.64% of the India consumer speaker market share in 2025 and soundbars are advancing at a 13.05% CAGR through 2031.

- By connectivity, Bluetooth-only models commanded 67.58% share of the India consumer speaker market size in 2025 while dual BT + Wi-Fi configurations are expanding at 12.12% CAGR.

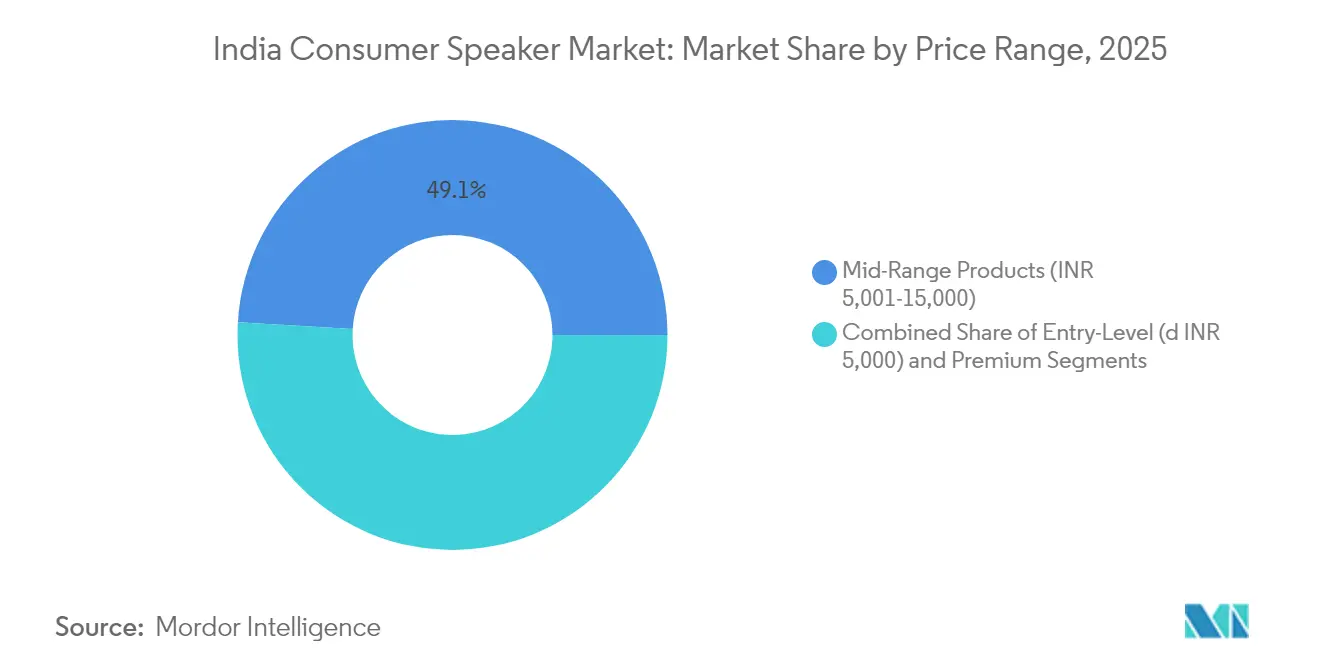

- By price range, mid-range products (INR 5,001-15,000) captured 49.05% of the India consumer speaker market size in 2025; premium units (≥ INR 15,001) are growing fastest at 12.74% CAGR.

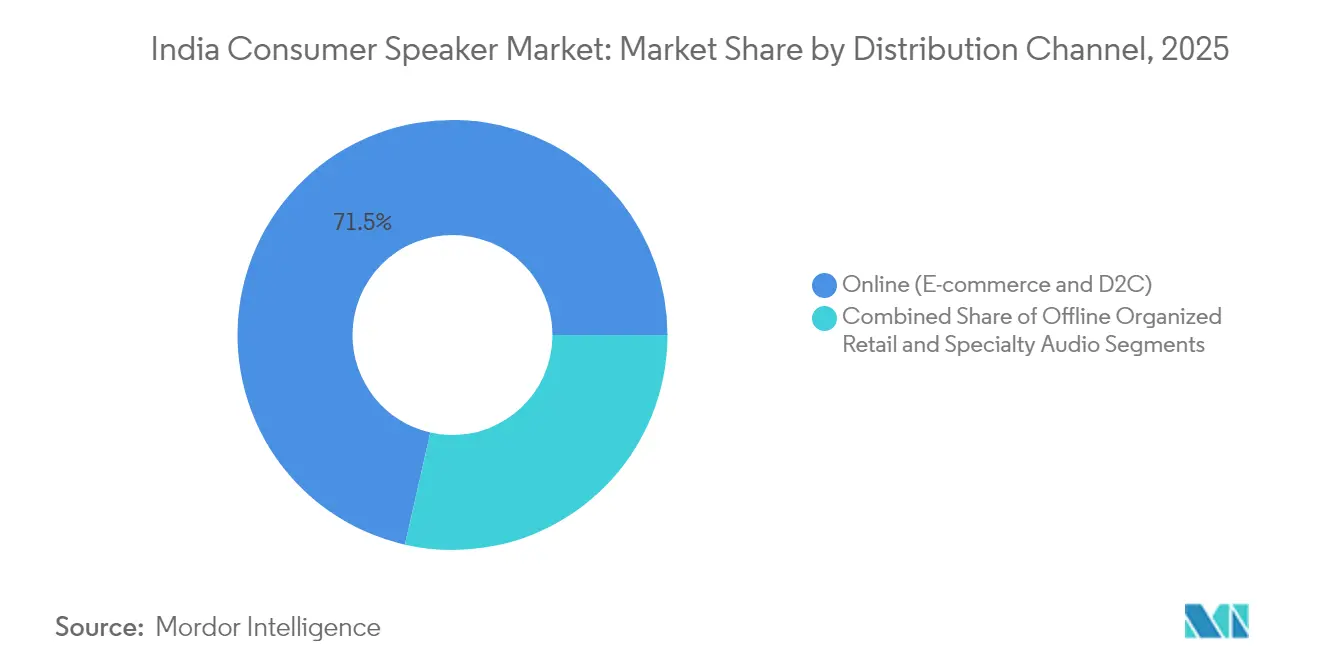

- By distribution channel, online platforms secured 71.45% share of the India consumer speaker market in 2025, whereas specialty audio stores are climbing at 12.94% CAGR.

- By region, West India accounted for 28.10% of the India consumer speaker market share in 2025 and North-East India is projected to expand at an 12.22% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

India Consumer Speaker Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rapid 5G and Fiber Roll-out | +2.8% | National, with early gains in Mumbai, Delhi, Bangalore | Medium term (2-4 years) |

| Affordable Made-in-India SKUs | +2.1% | National, strongest in Tier-2/3 cities | Long term (≥ 4 years) |

| Surge in Voice-assistant Adoption | +1.9% | Urban centers, expanding to semi-urban markets | Medium term (2-4 years) |

| OTT and Gaming-led Premium Audio Demand | +1.7% | Metro cities, spill-over to Tier-1 urban areas | Short term (≤ 2 years) |

| Government PLI and Manufacturing Incentives | +1.4% | Manufacturing hubs in Tamil Nadu, Karnataka, Andhra Pradesh | Long term (≥ 4 years) |

| Expansion of Tier-2/3 Online Retail | +1.3% | Semi-urban and rural markets across all states | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rapid 5G and fiber roll-out

Telecom operators continue to light up 5G in urban clusters, enabling low-latency audio streaming and multi-room synchronization. Fiber penetration into tier-2 cities stabilizes home-network bandwidth, which boosts demand for Wi-Fi-capable speakers that run voice assistants reliably. Consistent connectivity is helping first-time buyers bypass legacy wired systems and jump straight to wireless units, accelerating upgrade cycles for households that already own Bluetooth-only models.

Affordable “Made-in-India” SKUs

Production-linked incentives and a sharper focus on component localization have lowered bill-of-materials costs while trimming import duties. Domestic assembly now covers dust-resistant casings, higher-capacity batteries, and regional-language voice prompts tailored to Indian usage patterns. The availability of feature-rich devices at sub-INR 10,000 price points draws first-time users in tier-3 districts into the India consumer speaker market and shields local brands from currency-related import shocks.

Surge in voice-assistant adoption

Speaker makers embed Alexa, Google Assistant, and proprietary AI engines that parse Hindi and other vernaculars with higher accuracy than previous generations. Improved natural-language processing makes smart speakers the control hub for smart-lighting, fan, and air-conditioning ecosystems in urban homes. Privacy-first firmware options that process select commands locally rather than in the cloud are emerging as selling points for digitally aware households.

OTT and gaming-led premium audio demand

Nearly every new smart television now ships with Dolby Atmos support, setting user expectations for immersive sound. Gamers, now a 450 million-strong cohort, demand low-latency, high-fidelity speakers that handle positional audio cues. Higher-income families pair large-screen TVs with 3.1- or 5.1-channel soundbars, while single-cabinet party speakers with > 80 W output remain popular for social gatherings, helping lift average selling prices.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Data-privacy and Security Concerns | -1.8% | Urban markets with higher digital awareness | Short term (≤ 2 years) |

| Counterfeit and Grey-market Products | -1.5% | Tier-2/3 cities and online marketplaces | Medium term (2-4 years) |

| Semiconductor Supply-chain Volatility | -1.2% | National, affecting all price segments | Short term (≤ 2 years) |

| Low Indian-language NLP Accuracy | -0.9% | Rural and semi-urban non-English speaking markets | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Data-privacy and security concerns

Households increasingly question always-on microphones and cloud storage of voice recordings. Brands now highlight physical mute switches, on-device processing, and transparent data-retention policies.[1]Government of India, Central Consumer Protection Authority press release archive, goi.gov.in Delay in consumer adoption of smart speakers is most visible among professionals wary of corporate or family conversations being captured inadvertently.

Counterfeit and grey-market products

Look-alike speakers undercut legitimate models by 20–40%, eroding brand equity and confusing buyers about expected sound quality. While enforcement has intensified, the volume of fake goods circulating through informal offline outlets and certain e-commerce listings still drains revenue from compliant manufacturers.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Device Type: Wireless leadership and soundbar momentum

Wireless speakers hold a 51.64% share of the India consumer speaker market in 2025, with smart sub-variants posting a significant CAGR through 2031. The cut-the-cord mindset matches a mobile-first culture where a smartphone acts as the primary audio source. Portable Bluetooth cylinders remain weekend companions, yet smart speakers are taking center stage as living-room gateways for home automation. Soundbars, although with a smaller base, benefit from smart TV proliferation; their forecast 13.05% CAGR places them as the fastest-expanding device class. Party speakers larger than 80 W maintain relevance for social events, sustaining a 27% volume slice. Hi-Fi towers, promoted as hybrid music-and-movie solutions, address listeners who seek better bass response without investing in multi-unit setups.

Mid-tier brands merge categories by adding detachable satellites to party speakers or voice assistants to traditional boomboxes. Samsung’s 20.1% global soundbar share highlights technological trickle-down that now influences domestic buying decisions. Local challengers reply with value-engineered wireless bundles that ship with karaoke microphones and RGB lighting to match cultural preferences for group entertainment. The device spectrum therefore ranges from pocket-sized 5 W sticks to 400 W tower rigs, ensuring every income band finds a fitting proposition in the India consumer speaker market.

By Connectivity: Bluetooth prevalence and dual-mode ascent

Bluetooth-only products accounted for 67.58% of the India consumer speaker market size in 2025, cementing their place as entry-level workhorses. Simplicity of pairing and ever-lower chip costs keep BOM structures lean. Yet dual BT + Wi-Fi units are arching upward at a 12.12% CAGR as households appreciate lossless streaming, multi-room grouping, and voice-command responsiveness. Pure Wi-Fi speakers serve a niche of audiophiles who prize uncompressed codecs, but they anchor brand portfolios as halo offerings.

Automatic source switching is becoming standard, allowing a speaker to prioritize Wi-Fi when available and revert to Bluetooth outdoors. Amazon Echo and Google Nest families exemplify this versatility, using tri-band antennas to sustain connectivity in congested urban homes. OEMs now bundle companion apps that map Wi-Fi coverage and suggest optimal placement, driving incremental upgrades for mesh routers. Connectivity diversification, therefore, accelerates ASP growth while future-proofing devices against protocol obsolescence.

By Price Range: Mid-range heft and premium surge

Mid-range devices between INR 5,001 and INR 15,000 secured 49.05% of the India consumer speaker market size in 2025. Economies of scale on drivers, batteries, and plastic enclosures allow brands to layer extra features, IPX ratings, LED lighting, and voice control without breaching affordability thresholds. Entry-level models below INR 5,000 still court first-time buyers, though razor-thin margins leave little headroom to absorb commodity cost spikes.

Premium units priced at or above INR 15,001 are registering the strongest 12.74% CAGR. Higher disposable incomes, EMI schemes, and influencer reviews that stress soundstage depth nudge up purchase values. Global labels such as Sennheiser place calibrated tweeters and proprietary DSPs to justify four-figure price tags in USD terms. Import duties remain a hurdle, yet selective SKD assembly in India cushions outlays for top-end variants, making the premium cluster an outsized contributor to revenue, if not volume, inside the India consumer speaker market.

By Distribution Channel: E-commerce scale and experiential retail revival

Online platforms captured 71.45% share of the India consumer speaker market in 2025, helped by flash sales, influencer-led unboxings, and same-day delivery in 50-plus cities. Direct-to-consumer storefronts push limited-edition collaborations and gather first-party data for rapid firmware iteration. While cashless payments and easy return policies fuel click-through rates, specialty audio stores are rebounding at a 12.94% CAGR. Shoppers chasing premium acoustics want in-person demos before parting with five-digit rupees, and retailers respond with treated listening rooms and bundled installation.

Organized multi-brand chains such as Croma added 149 outlets in FY 2024, signaling sustained faith in brick-and-mortar relevance. Omnichannel approaches now dominate strategy decks; a launch exclusive begins online, then migrates to offline displays for broader reach. Channel segmentation, therefore, pivots on basket value: mass-market models move fastest through virtual carts, while high-ticket SKUs lean on human consultants to articulate sonic nuances.

Geography Analysis

West India’s 28.10% share reflects concentrated urban wealth and entrenched organized retail. Mumbai and Pune host media conglomerates and film studios that propagate audio trends quickly, prompting early uptake of multi-channel systems. Gujarat’s export-oriented industrial clusters facilitate distribution not just within the state but across northern trade routes, maintaining high inventory turns for mid-range SKUs.

North-East India’s 12.22% CAGR signals the payoff from sustained infrastructure spending and digital-inclusion drives. Rail and road upgrades shorten transit times for consumer electronics, while state-financed fiber projects elevate broadband penetration. Speaker brands partner with local influencers who broadcast in regional dialects, aligning product marketing to cultural preferences and boosting brand recall in smaller townships.

Southern metros bring steady demand anchored in IT and startup employment, where work-from-home routines justify premium audio for video calls and entertainment. Chennai’s port enhances the availability of imported components for high-end speakers assembled locally. North India continues to reward aggressive pricing and wide distribution; bundled festival promotions in Delhi-NCR and Lucknow deliver volume spikes. Central and Eastern belts, from Bhopal to Kolkata, mature in tandem with retail mall growth, pushing multi-brand kiosks deeper into semi-urban catchments and enlarging the footprint of the India consumer speaker market.

Competitive Landscape

The India consumer speaker market hosts major players, pointing to moderate concentration. boAt and Zebronics leverage domestic assembly to refresh catalogs every quarter and sustain attractive price-performance ratios.[4]boAt, “boAt’s Local Production Crosses 5 Crore Units,” economictimes.com Global majors Samsung, Sony, JBL, and Xiaomi, match with technology differentiation such as object-based surround processing, larger passive radiators, and proprietary AI tuning.

Price transparency in e-commerce squeezes margins, so brands bundle value-added services: extended warranties, in-app EQ presets, and subscription trials for music platforms. Supply-chain agility is a clear moat; firms with domestic plastic-injection and PCB capacities recover faster from component shortages. Collaborations between Indian upstarts and global audio specialists, exemplified by Noise partnering with Bose on earbuds, hint at future co-development models crossing over to speaker form factors.

Channel partnerships grow strategic weight. International companies court large retailers for exclusive shelf space, while homegrown labels double down on direct-to-consumer apps that capture granular usage analytics. Marketing spend is shifting from celebrity endorsements to community-led referrals on Discord and Telegram, indicating evolving playbooks even for established incumbents in the India consumer speaker market.

India Consumer Speaker Industry Leaders

Amazon.com, Inc.

Boat Ltd.(Imagine Marketing Limited)

Sony Group Corporation

Samsung Electronics Co., Ltd.

LG Electronics Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2025: Noise partnered with Bose to debut Master Buds using Bose tuning, underscoring the appeal of co-branding for acoustic credibility.

- February 2025: Samsung unveiled its flagship HW-Q990F soundbar with dual active subwoofers and refined Q-Symphony integration, targeting India’s premium home-entertainment buyers.

- February 2025: Xiaomi introduced the Smart Speaker Pro featuring upgraded AI processing and balanced-armature drivers, broadening its smart-home stack.

- January 2025: JBL rolled out the Flip 7, Charge 6, and PartyBox 520, each equipped with AI Sound Boost and Auracast support for low-latency group playback, reinforcing multi-segment coverage.

India Consumer Speaker Market Report Scope

Consumer speakers are very popular consumer electronic devices, and their penetration is rapidly increasing in the Indian market owing to the steady growth of the entertainment industry in the country. The report presents a comprehensive analysis of the Indian Consumer Speaker Market segmented by different types of devices and includes the regional trends having an impact on the growth of the market.

India Consumer Speaker Market is segmented by Type of Device (Wireless Speakers (Smart Speakers, Traditional Speakers), Soundbars, Hi-Fi Systems).

| Wireless Speakers | Smart Speakers |

| Traditional Bluetooth Speakers | |

| Soundbars | |

| Hi-Fi and Party Speakers |

| Bluetooth |

| Wi-Fi |

| Dual (BT + Wi-Fi) / Multi-room |

| Entry-level (≤ INR 5,000) |

| Mid-range (INR 5,001-15,000) |

| Premium (≥ INR 15,001) |

| Online (E-commerce and D2C) |

| Offline Organised Retail |

| Specialty Audio Stores |

| North India |

| South India |

| West India |

| East India |

| Central India |

| North-East India |

| By Device Type | Wireless Speakers | Smart Speakers |

| Traditional Bluetooth Speakers | ||

| Soundbars | ||

| Hi-Fi and Party Speakers | ||

| By Connectivity | Bluetooth | |

| Wi-Fi | ||

| Dual (BT + Wi-Fi) / Multi-room | ||

| By Price Range | Entry-level (≤ INR 5,000) | |

| Mid-range (INR 5,001-15,000) | ||

| Premium (≥ INR 15,001) | ||

| By Distribution Channel | Online (E-commerce and D2C) | |

| Offline Organised Retail | ||

| Specialty Audio Stores | ||

| By Region | North India | |

| South India | ||

| West India | ||

| East India | ||

| Central India | ||

| North-East India |

Key Questions Answered in the Report

How big is the India Consumer Speaker Market?

The India Consumer Speaker Market size is expected to reach 41.15 million units in 2026 and grow at a CAGR of 12.08% to reach 72.78 million units by 2031.

What is the current India Consumer Speaker Market size?

In 2026, the India Consumer Speaker Market size is expected to reach 41.15 million units.

Who are the key players in India Consumer Speaker Market?

Amazon Retail India Private Limited, Google India Private Limited, HARMAN International India Pvt Ltd (JBL), Sony India Private Limited and Imagine Marketing Pvt Ltd (Boat) are the major companies operating in the India Consumer Speaker Market.

What years does this India Consumer Speaker Market cover, and what was the market size in 2025?

In 2025, the India Consumer Speaker Market size was estimated at 41.15 million units. The report covers the India Consumer Speaker Market historical market size for years: 2019, 2020, 2021, 2022, 2023 and 2024. The report also forecasts the India Consumer Speaker Market size for years: 2026, 2027, 2028, 2029, 2030 and 2031.

What is the forecast volume for consumer speakers in India by 2031?

The India consumer speaker market is projected to reach 72.78 million units by 2031, reflecting a 12.08% CAGR from 2026.

Which device category is growing fastest?

Soundbars are forecast to expand at a 13.05% CAGR through 2031, outpacing other device types.

How important is online retail for speaker sales?

Online platforms accounted for 71.45% of unit shipments in 2025 and remain the dominant purchase route, although specialty stores are regaining traction.

Which price tier shows the highest growth momentum?

Premium speakers priced at or above INR 15,001 are advancing at a 12.74% CAGR as urban consumers trade up for better fidelity.

Which Indian region offers the fastest growth opportunity?

North-East India is forecast to grow at an 12.22% CAGR, benefiting from new connectivity infrastructure and rising vernacular content demand.

What key factor differentiates leading brands?

Local manufacturing depth and rapid product refresh cycles help top brands balance pricing flexibility with feature innovation.

Page last updated on: