Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

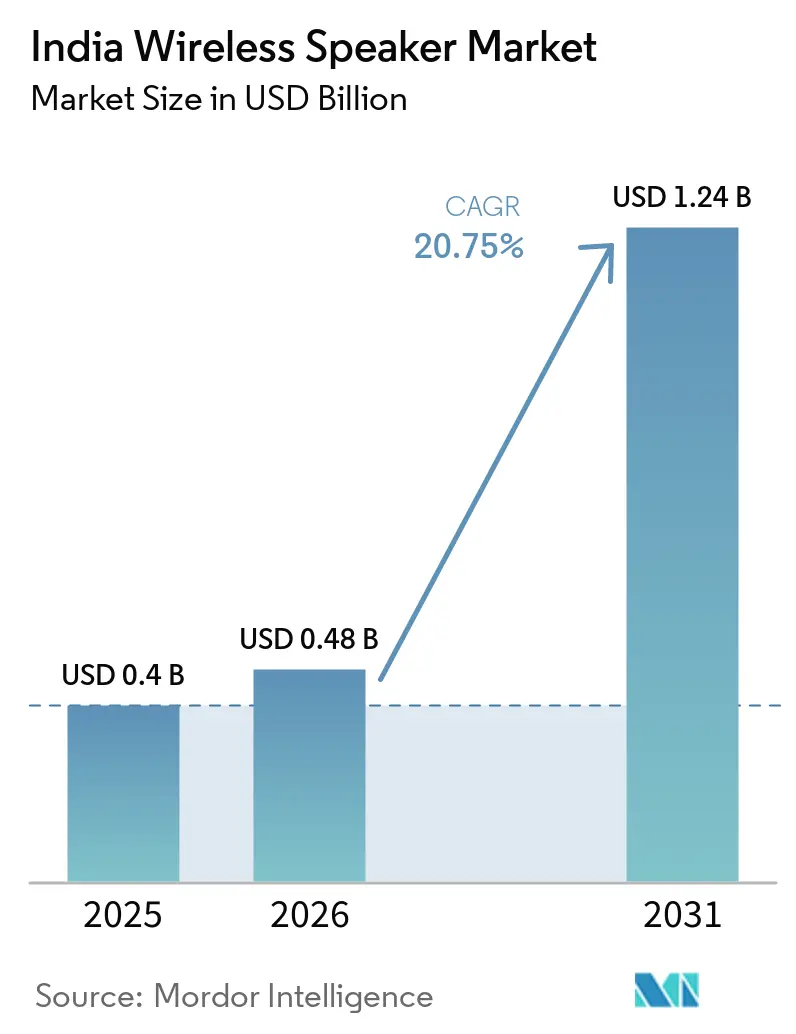

| Base Year Market Size (2025) | USD 0.4 Billion |

| Market Size (2026) | USD 0.48 Billion |

| Market Size (2031) | USD 1.24 Billion |

| Growth Rate (2026 - 2031) | 20.75% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

India Wireless Speaker Market Analysis by Mordor Intelligence

India Wireless Speaker Market size in 2026 is estimated at USD 0.48 billion, growing from 2025 value of USD 0.4 billion with 2031 projections showing USD 1.24 billion, growing at 20.75% CAGR over 2026-2031.

The surge reflects wider 4G/5G coverage in small towns, a 547 million-strong OTT user base that listens almost exclusively on smartphones, and an INR 22,919 crore PLI stimulus that has accelerated domestic audio-electronics output. Demand also tracks the rapid expansion of India’s smart-home sector toward INR 36,000 crore by 2028 and the premiumization wave that lifted the country’s high-end smartphone sales 36% year over year in 2024. Online channels, supported by near-nationwide logistics networks, currently generate two-thirds of unit sales, yet specialist audio stores are expanding fastest as consumers seek hands-on product trials. Bluetooth-only devices still lead shipments, but smart speakers are advancing at an even steeper clip on the back of Hindi, Tamil, and Punjabi voice-assistant roll-outs. The competitive field is tightening as brands localize production, compress design-to-launch cycles, and court tier-2 and tier-3 buyers through financing schemes, installment plans, and telco bundles.

Key Report Takeaways

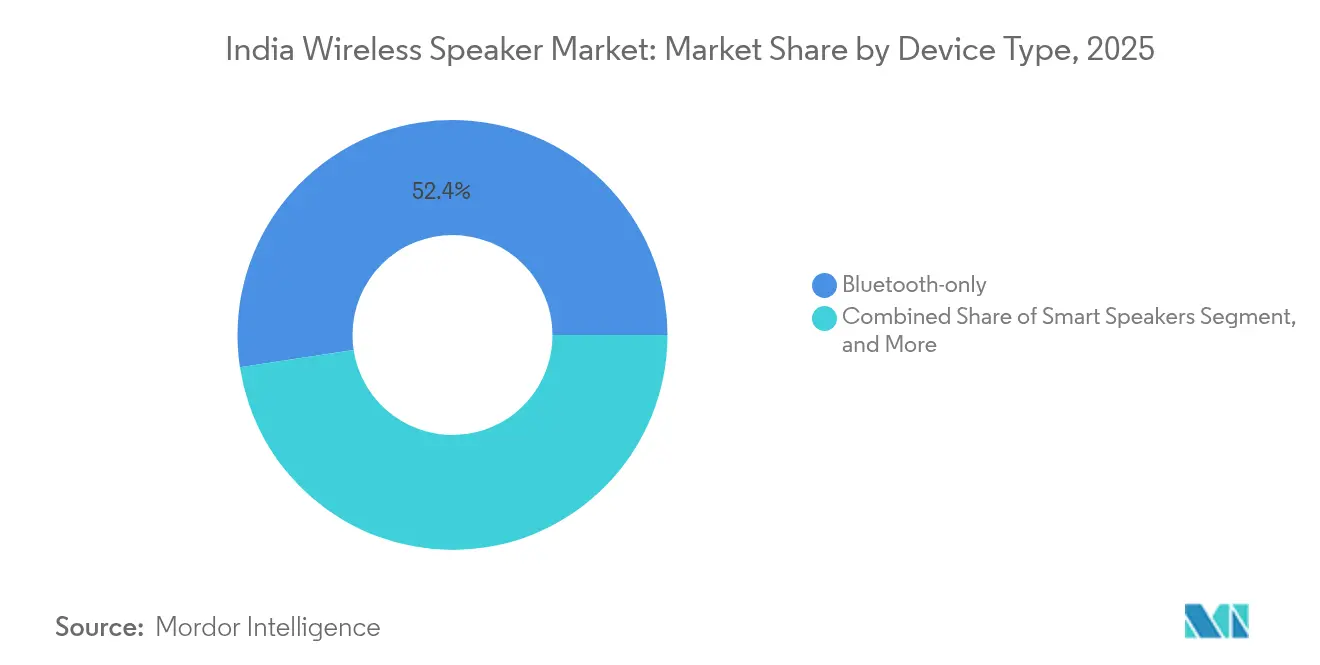

- By device type, Bluetooth-only speakers led with 52.40% revenue share of the India wireless speaker market in 2025, while smart speakers are projected to post a 22.60% CAGR through 2031.

- By distribution channel, online platforms accounted for 65.90% of the 2025 sales of the India wireless speaker market; offline specialist audio stores are expected to grow the fastest at 22.30% CAGR to 2031.

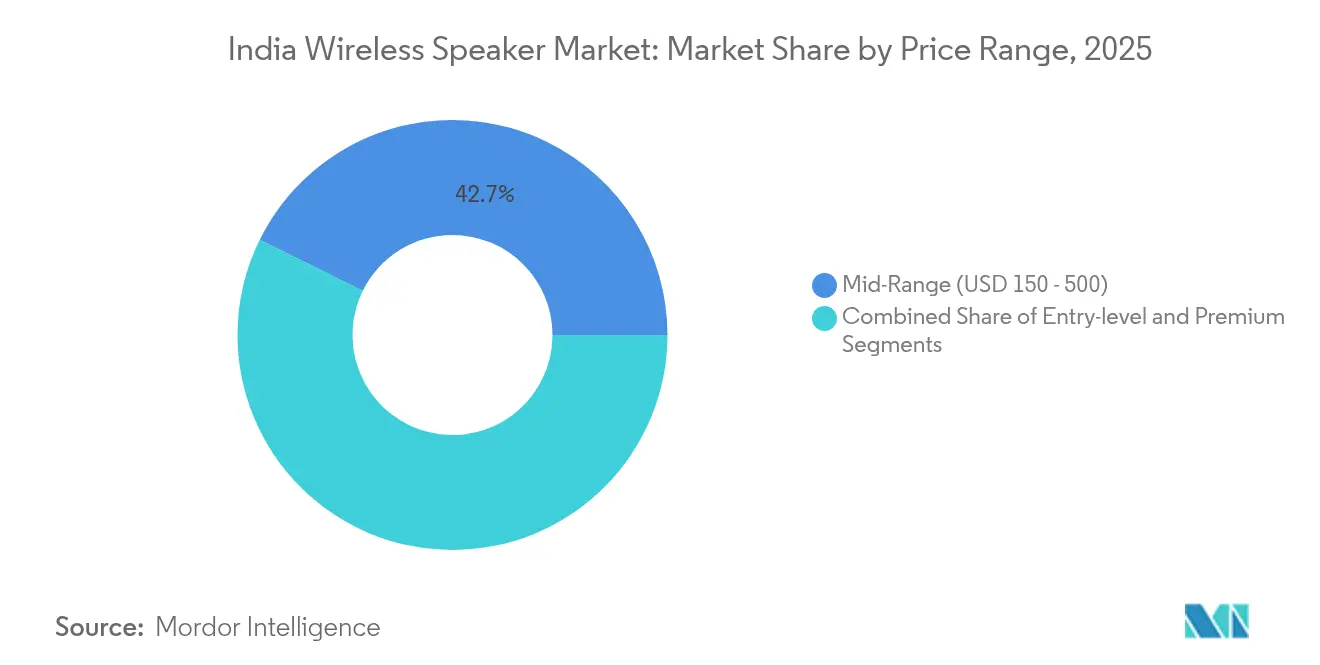

- By price range, mid-range models captured 42.70% share of the India wireless speaker market in 2025, and premium units above USD 500 are on track for a 21.80% CAGR through 2031.

- By end-user, residential buyers controlled 82.10% of the 2025 demand of the India wireless speaker market, and the segment is moving at a 21.90% CAGR toward 2031.

- By geography, West India held 26.10% of the India wireless speaker market share in 2025, whereas North-East India is forecast to expand at 21.40% CAGR over the outlook period.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

India Wireless Speaker Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising smartphone and affordable data penetration | +4.2% | National, tier-2/3 lead | Short term (≤ 2 years) |

| Proliferation of OTT music/video streaming services | +3.8% | National, urban and semi-urban | Medium term (2-4 years) |

| Rising disposable income and aspiration for smart-home gadgets | +3.1% | West and South India | Medium term (2-4 years) |

| PLI incentives for domestic audio-electronics manufacturing | +2.7% | Tamil Nadu, Karnataka, Maharashtra | Long term (≥ 4 years) |

| Regional-language voice-assistant roll-outs | +2.3% | National, Hindi/Tamil/Punjabi belts | Medium term (2-4 years) |

| Telco-bundled speaker + content offers | +1.9% | Metro and tier-1 | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Rising Smartphone and Affordable Data Penetration

Expanded 4G/5G coverage and aggressive handset financing have drawn millions of first-time buyers into the digital ecosystem. Tier-2 and tier-3 cities now post double-digit smartphone growth versus single-digit gains in metros, and their users stream 35-40 GB of data each month, 15-20% higher than urban counterparts.[1]Gulveen Aulakh, “Telecom operators to boost network coverage, capacity in small towns, villages,” Livemint, livemint.com The leap in handset ownership directly fuels hardware attach rates for entry-level Bluetooth speakers and opens a gateway for premium audio upgrades once disposable incomes rise.

OTT Streaming Services Proliferation Reshapes Audio Consumption Patterns

Streaming accounts for 88% of recorded-music revenue, with Indian users listening 26.7 hours weekly, well above global averages. Paid subscriptions rose 58.5%; 69.4% tuned into music livestreams in the previous month. YouTube’s 95.2% penetration confirms a mobile-first habit that aligns with portable speaker ownership, while the demand for higher fidelity is steering urban buyers toward Wi-Fi-enabled smart speakers.

Smart-Home Aspirations Fuel Premium Segment Growth

India’s smart-home spending is set to quadruple by 2028, turning speakers into control hubs for lighting, security, and climate devices. Premium smartphone sales jumped 36% in 2024, signaling willingness to pay for connected experiences that carry over to audio accessories.[2]David Delima, “India's Premium Mobile Market Rose 36 Percent YoY in 2024: CMR,” Gadgets360, gadgets360.com Brands such as boAt leverage this appetite with premium-look models that fit tighter budgets, helped by buy-now-pay-later plans and zero-down EMIs at organized retail.

PLI Scheme Manufacturing Incentives Strengthen Domestic Supply Chains

An INR 22,919 crore PLI tranche sanctioned in March 2025 has encouraged global contract manufacturers, Foxconn, Pegatron, and Dixon, to scale local assembly lines, cut import dependence, and pass on cost savings to consumers. BoAt now makes 70-75% of its volume domestically and has crossed 50 million ‘Made in India’ products, reducing lead times while protecting margins.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High price sensitivity in premium tier | -2.8% | National, sharper in tier-2/3 | Medium term (2-4 years) |

| RF-radiation and child-health concerns | -1.4% | Urban clusters | Short term (≤ 2 years) |

| Patchy after-sales network beyond metros | -1.9% | Tier-2/3 and rural | Long term (≥ 4 years) |

| BIS RF-compliance certification delays | -1.2% | National | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Premium Segment Price Sensitivity Constrains Market Expansion

Although the premium tier is registering the quickest growth, the >USD 500 bracket faces a ceiling in smaller towns where disposable incomes are still normalizing. Surveys show 60% of Gen Z shoppers rely on installment options for experiential buys, making flexible financing essential for premium speaker uptake. Brands counter by offering luxurious designs at mid-range prices, as seen in boAt’s Stone Opus that mirrors the Marshall Acton aesthetic at one-third the cost.[3]T.E. Raja Simhan, “Export of electronics and electrical products from Chennai airport jumps four-fold,” The Hindu BusinessLine, thehindubusinessline.com

RF-Radiation Health Concerns Create Consumer Hesitancy

Government advisories recommending ≤2 hours of daily headphone use at 50 dB have spilled over into speaker purchases, heightening scrutiny on RF emissions. BIS certification under IS 616:2017 provides reassurance, yet the 15-60 day approval cycle can stall launches and add compliance costs that smaller firms struggle to absorb.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Device Type: Smart Speakers Gain Ground Against Bluetooth Leaders

Bluetooth-only units held 52.40% revenue in 2025, underscoring the India wireless speaker market preference for simple pairing with smartphones. Smart speakers, propelled by multilingual voice assistants, are advancing at a 22.60% CAGR and are likely to close the gap by 2031. The India wireless speaker market size for smart speakers is projected to climb from USD 0.06 billion in 2025 to USD 0.2 billion in 2031. Display-equipped models such as Amazon Echo Spot broaden use cases from audio playback to recipe help and security feeds. Wi-Fi-only and combo devices address high-fidelity and multi-room needs in premium homes, while BIS-mandated RF caps keep all form factors within safety norms.

Early adoption began in metros, but Hindi, Tamil, and Punjabi language support is unlocking demand among first-time voice-assistant users in tier-2 cities. JBL’s Auracast-enabled PartyBox range demonstrates how legacy audio brands are embedding future-proof wireless protocols to maintain relevance. Longer replacement cycles for fixed smart speakers versus portable Bluetooth units imply higher average selling prices and greater revenue-per-user upside, which the India wireless speaker industry leaders view as a strategic growth lever.

By Distribution Channel: Specialist Stores Register Quickest Upside

Online vendors controlled 65.90% of the India wireless speaker market in 2025, benefiting from deep discounting, fast delivery pledges, and reach across 90% of PIN codes. Organized audio boutiques, however, are growing 22.30% annually as shoppers in the USD 150-plus bracket look to audition devices before paying. The India wireless speaker market size attributed to specialist stores is forecast at USD 0.12 billion by 2031. In metros, brand-owned showrooms double as experience centers, while in tier-2 cities, chains are franchising smaller footprints that combine product demos with immediate service options.

E-commerce remains crucial for entry-level and refresh sales because price comparisons are easiest online. Yet premium buyers often seek advice on codec support, room acoustics, and warranty add-ons that store staff are trained to supply. Successful brands now execute synchronized releases: product goes live on websites and shelves the same day, and invoice data feeds directly into central CRMs to streamline after-sales. Over time, hybrid strategies that let customers buy online and pick up in store are poised to dominate.

By Price Range: Premium Accelerates as Mid-Range Anchors Volume

Mid-range speakers priced USD 150-500 captured 42.70% of 2025 revenue, proving the sweet spot for value-seeking professionals. The entry tier under USD 150 continues to onboard first-time buyers, especially in rural belts where smartphones are the sole entertainment screen. The premium bracket above USD 500 is set to outpace all others at a 21.80% CAGR, driven by aspirational households in metros and tech corridors. The India wireless speaker market share of premium models is predicted to rise from 13.10% in 2025 to 19.20% by 2031.

Premium growth echoes the 36% YoY leap seen in high-end smartphones. Products such as Sony’s SRS-XZ7, Bose’s Smart Ultra, and Marshall’s Acton III offer spatial audio, HDMI-ARC, and app-based EQ, nudging average selling prices upward. Financing tools, BNPL, and zero-interest cards, are critical in accelerating uptake beyond the metro bubble. Meanwhile, brands fine-tune BOM costs through localized sourcing of drivers, PCBs, and plastics made feasible by the PLI boost.

By End-User: Residential Dominance Sustains but Commercial Niche Matures

Residential buyers accounted for 82.10% of shipments in 2025 and are advancing at a 21.90% CAGR. Within the India consumer speaker market, this dominance is supported by sustained work-from-home practices, growing streaming consumption, and the increasing use of speakers as smart-home control hubs. The India wireless speaker market size linked to homes should touch USD 1.02 billion by 2031. Compact form factors, voice control, and décor-friendly finishes resonate with urban apartments as well as independent homes in smaller cities.

Commercial adoption, while smaller, is diversifying. Restaurants and cafés opt for Wi-Fi mesh speakers for zone control, while event organizers favor rugged Bluetooth models that support daisy-chain pairing. Sporting venues and campus festivals, which grew to 2,000-plus shows in 2024, are testing battery-powered towers with 100 W-plus output. Over the forecast horizon, co-working chains and boutique hotels are expected to represent fertile ground for premium multi-room systems that double as marketing assets.

Geography Analysis

West India captured 26.10% of 2025 revenue thanks to Mumbai’s financial clout, Pune’s IT workforce, and Gujarat’s manufacturing heft. Superior retail density and higher disposable incomes continue to position the region as the prime launchpad for premium introductions. Chennai and Pune are also central to component sourcing, giving brands quick access to parts and service centers.

North-East India is the runaway growth champion at 21.40% CAGR to 2031. Government-funded highways, fiber roll-outs, and 4G/5G sites have narrowed the digital divide, while cultural affinity for music creates an eager user base for portable speakers. Local language voice assistants further untap latent demand, offering brands a first-mover advantage if they align content marketing to regional preferences.

South India, home to tech hubs Bangalore, Hyderabad, and Chennai, sustains strong premium uptake among IT professionals and early adopters. North India, spanning NCR and Tier-2 towns such as Jaipur and Lucknow, provides a balanced mix of mid-range and entry-level demand. Central and East India remain emerging opportunities, with e-commerce logistics improvements serving as a critical catalyst.

Competitive Landscape

Domestic hero boAt leads volume terms with a significant share in hearables and local output through Dixon’s factories. Its design-to-market cycle of under 120 days lets it shadow global trends quickly while pricing sharply for the India wireless speaker market. Global majors, Sony, JBL, Bose, bank on signature audio profiles and long-haul warranties to capture higher ASP segments.

Manufacturing localization is now table stakes. Foxconn’s 550,000-sq-ft Chennai warehouse and Pegatron’s INR 50 crore unit boost the parts pipeline for both domestic and international brands. Samsung’s INR 1,000 crore expansion at Sriperumbudur underscores the area’s importance to speaker, TV, and smartphone lines. Cost savings from duty exemption and freight elimination are reinvested in R&D and brand marketing.

Product roadmaps tilt toward ecosystem lock-in. Amazon bundles Prime Music, Alexa skills, and IoT control; Google’s Nest lineup banks on Matter protocols; Xiaomi leverages its phone UI for seamless casting. JBL’s Auracast roll-outs and Marshall’s retro-modern aesthetics keep heritage labels fresh. Market risk remains around BIS bottlenecks: a 60-day wait can derail synchronized global launches, favoring players with in-house compliance teams.

India Wireless Speaker Industry Leaders

Amazon Retail India Private Limited

HARMAN International India Pvt. Ltd. (JBL)

Sony India Private Limited

Samsung India Electronics Private Limited

Bose Corporation India Private Limited

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2025: Samsung India committed INR 1,000 crore to expand its Sriperumbudur plant, lifting annual device capacity by 20%.

- April 2025: Foxconn leased 550,000 sq ft of warehousing in Chennai’s Oragadam Industrial Park to handle rising exports of audio components.

- April 2025: boAt confidentially filed for an IPO, signaling possible USD 1.2 billion valuation.

- March 2025: The government cleared INR 22,919 crore in PLI incentives for electronic components, including wireless-audio drivers and chipsets.

India Wireless Speaker Market Report Scope

Wireless Speakers run through infrared or radio transmission and, therefore, need not be connected to any central unit. These can be connected to various other devices through Bluetooth or Wi-Fi, providing benefits, such as built-in assistant, multiroom audio, and better sound quality and voice assistance.

The report provides a detailed analysis of various types of wireless speakers, distribution channels, and vendor analysis in the Indian marketplace. The impact of COVID-19 on the market and impacted segments are also covered under the scope of the study. Furthermore, the disruption of the factors affecting the market's expansion in the near future has been covered in the study regarding drivers and restraints. The market sizes and forecasts are provided in terms of value (USD million) for all the above segments.

By Device Type

| Bluetooth-only |

| Wi-Fi-only |

| Smart Speakers |

| Combo (Bluetooth + Wi-Fi) |

By Distribution Channel

| Online (E-tailers, Brand.com) |

| Offline - Organised Retail |

| Offline - Specialist Audio Stores |

| Offline - Hyper/Super-markets |

By Price Range

| Entry-Level (Less than USD 150) |

| Mid-Range (USD 150 - 500) |

| Premium (Greater than USD 500) |

By End-User

| Residential |

| Commercial |

By Region (India)

| North India |

| West India |

| South India |

| East India |

| Central India |

| North-East India |

| By Device Type | Bluetooth-only |

| Wi-Fi-only | |

| Smart Speakers | |

| Combo (Bluetooth + Wi-Fi) | |

| By Distribution Channel | Online (E-tailers, Brand.com) |

| Offline - Organised Retail | |

| Offline - Specialist Audio Stores | |

| Offline - Hyper/Super-markets | |

| By Price Range | Entry-Level (Less than USD 150) |

| Mid-Range (USD 150 - 500) | |

| Premium (Greater than USD 500) | |

| By End-User | Residential |

| Commercial | |

| By Region (India) | North India |

| West India | |

| South India | |

| East India | |

| Central India | |

| North-East India |

Key Questions Answered in the Report

How large is the India wireless speaker market in 2026?

The market is valued at USD 483.17 million in 2026 and is on course for USD 1.24 billion by 2031 at a 20.75% CAGR.

Which device category is growing the fastest?

Smart speakers lead growth with a projected 22.60% CAGR to 2031 on the back of multi-lingual voice-assistant adoption.

Why are specialist audio stores expanding faster than online channels?

Shoppers increasingly want in-person demos and expert advice for premium models, driving a 22.30% CAGR for specialist outlets.

What role does the PLI scheme play in this market?

The INR 22,919 crore incentive is boosting domestic component sourcing, lowering costs, and accelerating product release cycles.

Which region in India shows the highest growth potential?

North-East India is forecast to scale at 21.40% CAGR because of new 4G/5G coverage and growing smartphone penetration.

Page last updated on: