Smart Shelf Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 6.28 Billion |

| Market Size (2031) | USD 17.76 Billion |

| Growth Rate (2026 - 2031) | 23.12% CAGR |

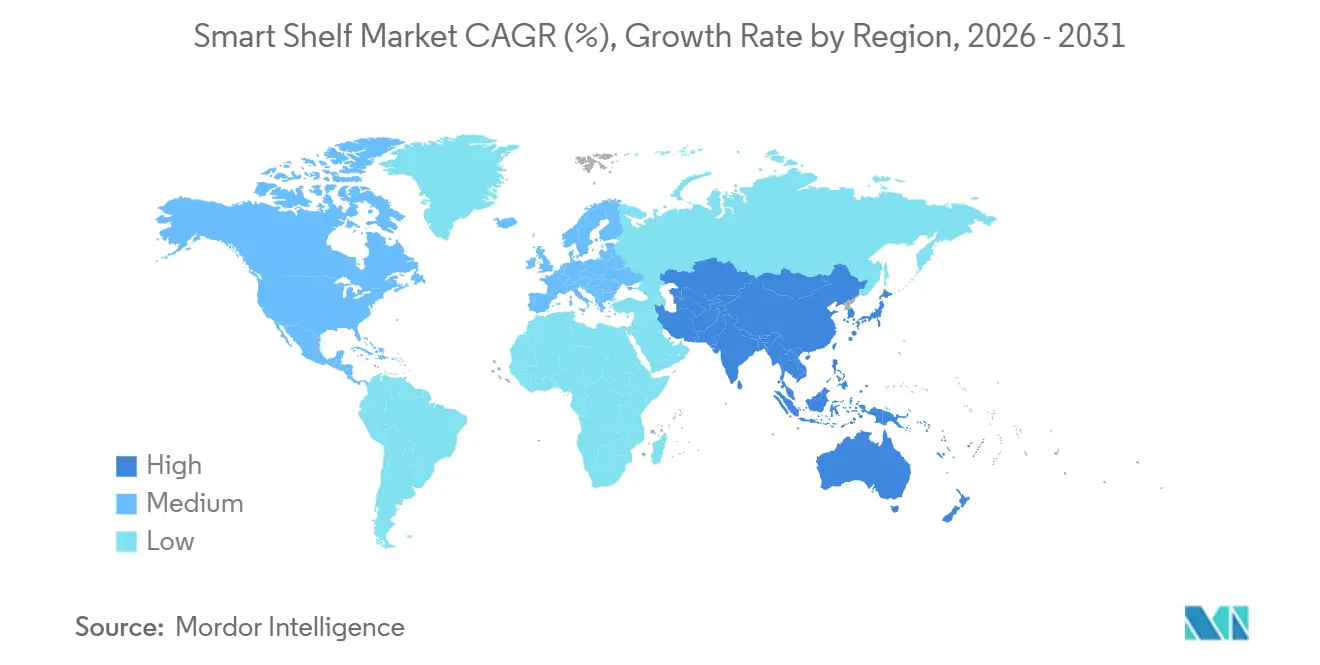

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

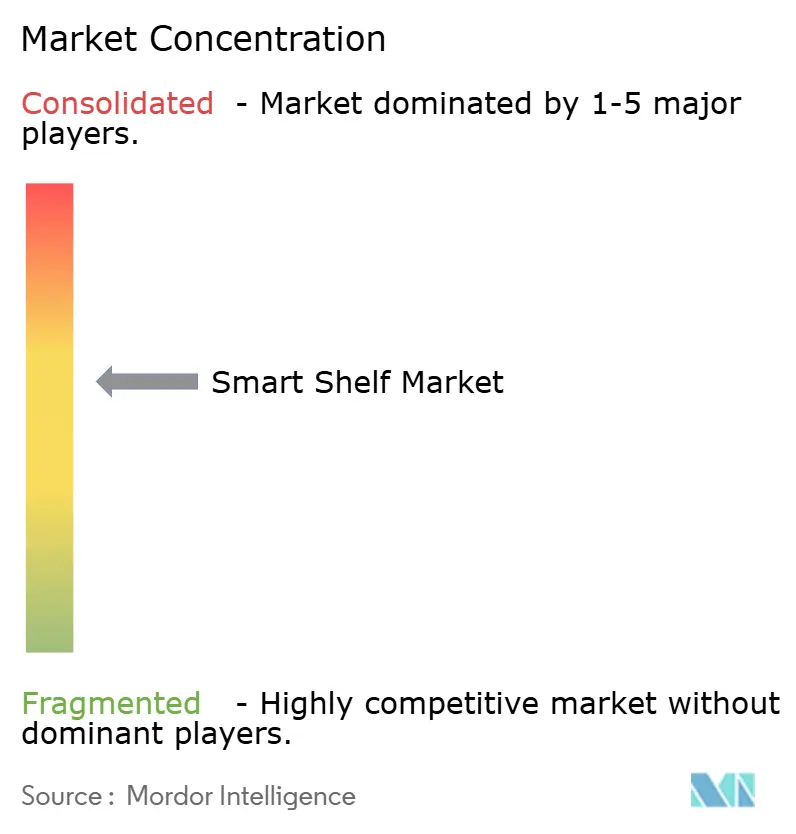

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Smart Shelf Market Analysis by Mordor Intelligence

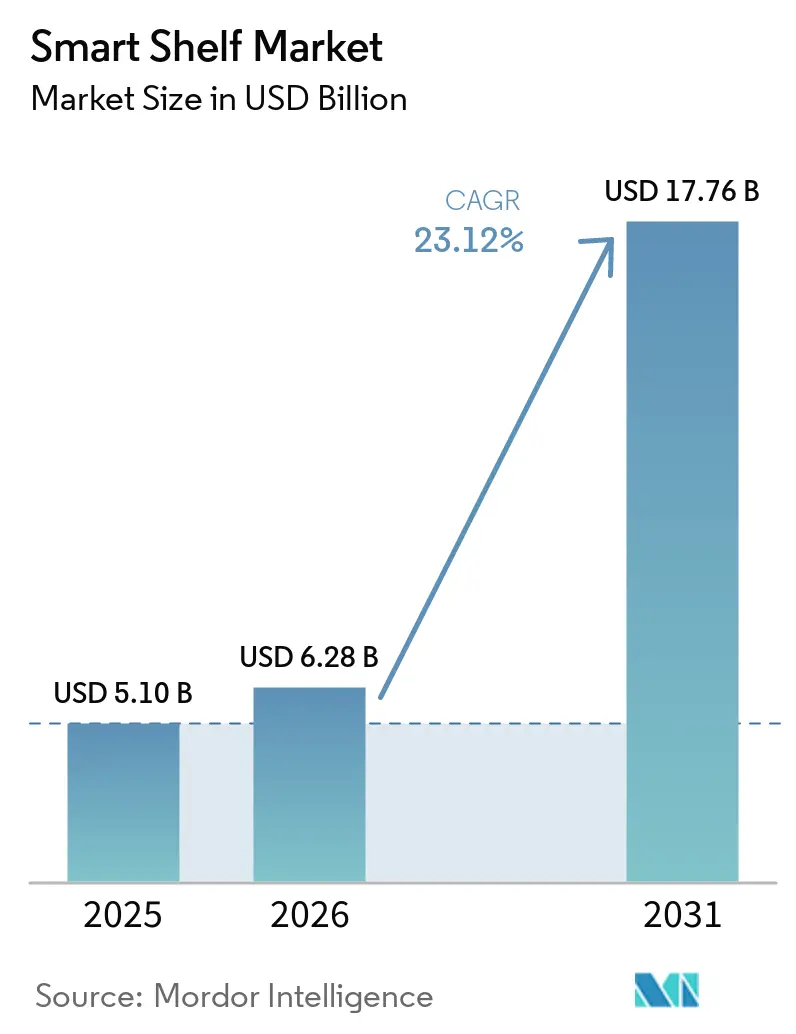

The smart shelf market size is expected to increase from USD 5.10 billion in 2025 to USD 6.28 billion in 2026 and reach USD 17.76 billion by 2031, growing at a CAGR of 23.12% over 2026-2031. Retailers are fast-tracking rollouts of electronic shelf labels (ESLs), radio-frequency identification (RFID), and computer vision to shrink labor, paper, and shrinkage costs while capturing incremental advertising revenue. Labor shortages across North America and Europe have shortened return-on-investment timelines, sustainability mandates are phasing out paper labels, and ultra-low-power RFID innovation is pushing total cost of ownership below historical thresholds.[1]U.S. Bureau of Labor Statistics, “Real Earnings Summary,” bls.gov At the same time, edge AI models now perform planogram compliance in seconds, turning shelf edges into real-time data nodes that feed merchandising, supply chain, and retail media platforms. These structural tailwinds are encouraging both global chains and mid-tier grocers to move past pilots into chain-wide deployments of smart shelf market technology.

Key Report Takeaways

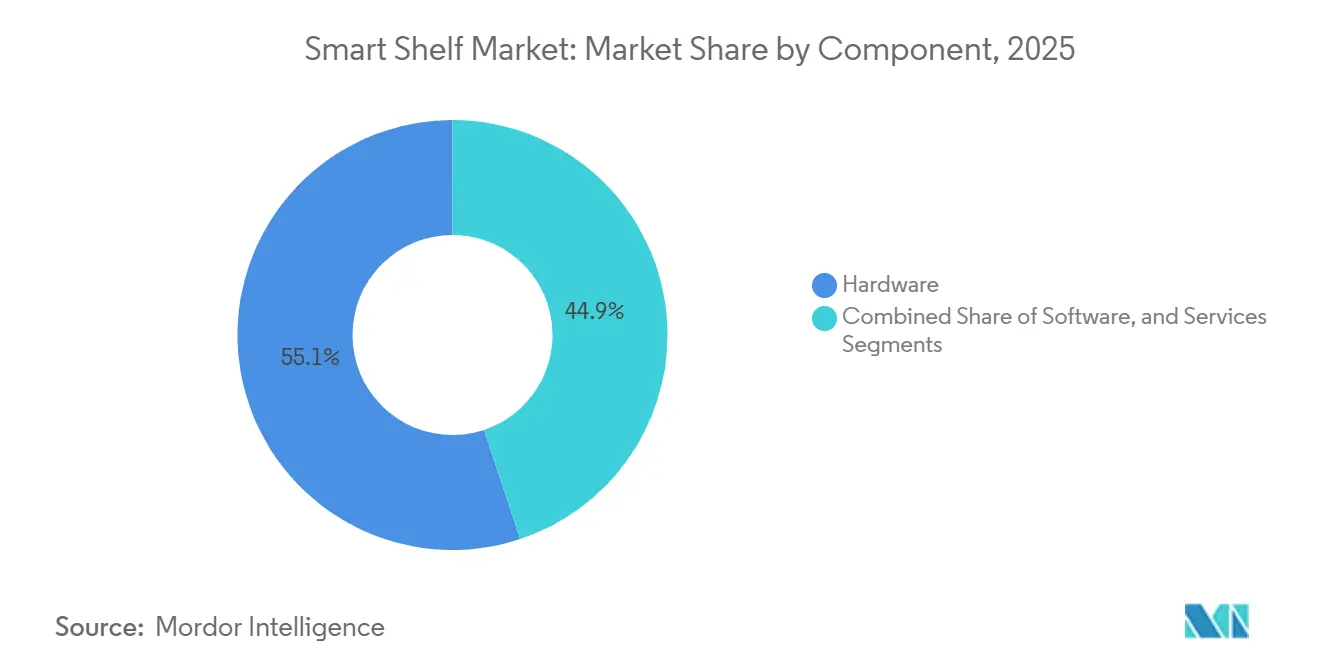

- By component, hardware commanded 55.11% of smart shelf market share in 2025, while services is projected to expand at a 23.51% CAGR through 2031.

- By technology, RFID-based smart shelves held 40.18% of smart shelf market share in 2025, whereas vision and camera systems are forecast to grow at 24.28% over 2026-2031.

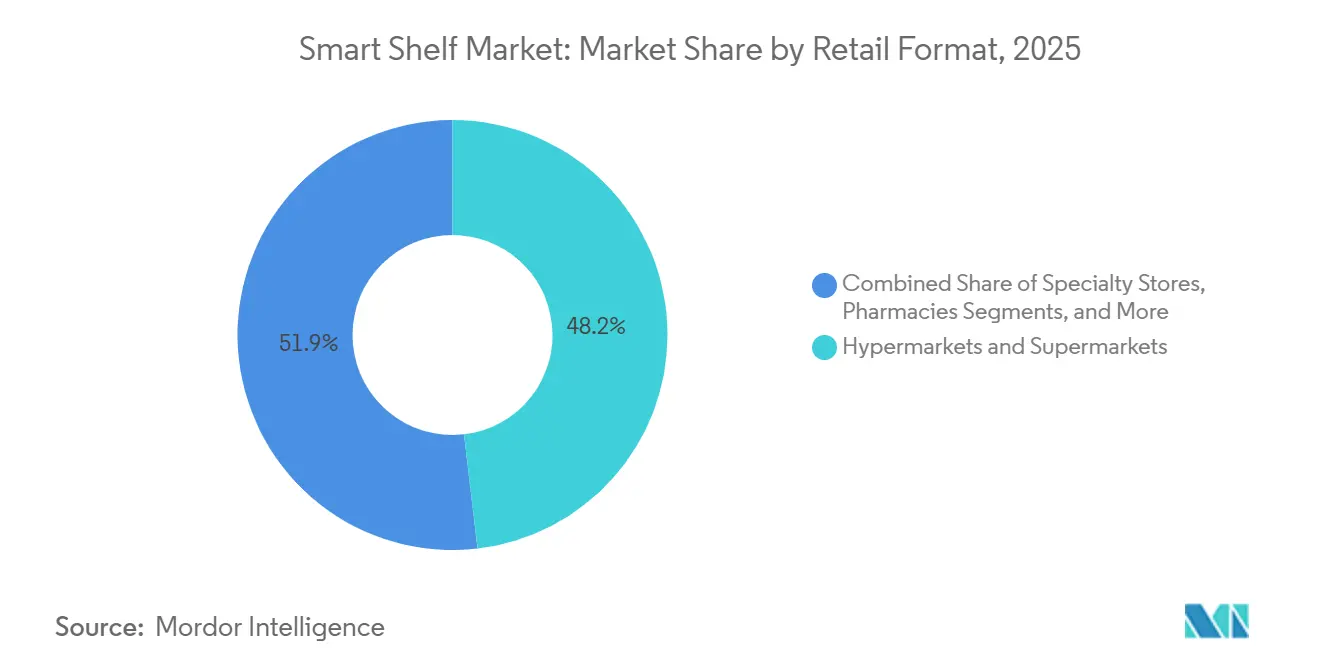

- By retail format, hypermarkets and supermarkets led with 48.15% of smart shelf market share in 2025; convenience stores are the fastest-growing format at a 24.19% CAGR through 2031.

- By application, inventory management accounted for 45.11% of smart shelf market share in 2025, and planogram management is advancing at a 23.47% CAGR through 2031.

- By geography, North America captured 34.16% of smart shelf market share in 2025, whereas Asia-Pacific is projected to record the highest regional CAGR of 24.55% to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Smart Shelf Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Retail-Wide Push for Real-Time Pricing Accuracy | +4.2% | Global, early adoption in North America and Europe | Short term (≤ 2 years) |

| Rising Labor Costs Accelerating Retail Automation | +5.8% | North America and Europe, spillover to APAC cities | Medium term (2-4 years) |

| Shrinkage Reduction Mandates by Large Grocers | +3.6% | Global, concentrated in North America and Europe | Medium term (2-4 years) |

| ESG Pressure to Eliminate Paper Shelf Labels | +2.4% | Europe and North America, expanding to APAC | Long term (≥ 4 years) |

| Computer-Vision Shelf Analytics Enabling Dynamic In-Store Media | +4.1% | North America, Europe, APAC tier-1 cities | Medium term (2-4 years) |

| Battery-Free RFID Tag Research and Development Unlocking Ultra-Low-Cost Deployments | +3.1% | Global, pilots in North America and APAC | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Retail-Wide Push For Real-Time Pricing Accuracy

Chains are discarding batch overnight price changes because competitive show-rooming demands intraday updates that sync in-store and online prices. United Kingdom grocer Morrisons synchronized 10.8 million ESLs across its estate in 2025, eliminating checkout disputes and aligning with e-commerce prices. Walmart connected 2,300 U.S. stores by early 2026, cutting a full workday of label changes down to minutes while improving gross margin. India’s Legal Metrology Act obliges supermarkets to display tamper-proof prices, accelerating ESL adoption among national chains. Dynamic markdowns tied to expiration windows now help reduce food waste, linking operational savings to corporate sustainability targets.

Rising Labor Costs Accelerating Retail Automation

Average hourly retail wages in the United States rose 4.8% year over year in 2025, putting pressure on grocers that still rely on manual label swaps and stock audits. ESLs redeploy associates toward assisted checkout and e-commerce picking, with Waitrose forecasting annual labor savings exceeding GBP 8 million (USD 10.1 million) once its United Kingdom rollout finishes in 2026. Co-op freed staff for online fulfillment after fitting 2,400 stores with ESLs, and sensor-based shelves now flag out-of-stocks automatically, replacing time-consuming aisle walks. Minimum-wage legislation across Europe and North America is shortening investment payback periods, making the smart shelf market attractive to regional retailers.

Shrinkage Reduction Mandates By Large Grocers

Retail shrinkage wiped out USD 112 billion globally in 2024, prompting chief operating officers to invest in technology that closes visibility gaps. Fresh Market reached 99% on-shelf availability after implementing computer-vision shelves that push real-time refill alerts, while Kroger’s RFID bakery pilot cut shrink by 18% by flagging impending expirations. Checkpoint Systems now unifies RFID tags with electronic article surveillance to pinpoint theft hotspots, and weight-sensor shelves instantly detect variances between expected and actual item counts. As inflation erodes margins, shrinkage control has shifted from a loss-prevention task to a strategic mandate driving smart shelf market deployments.[2]Source: National Retail Federation, “National Retail Security Survey 2024,” nrf.com

Computer-Vision Shelf Analytics Enabling Dynamic In-Store Media

Programmable ESLs and camera modules are morphing shelf edges into retail-media assets projected to top USD 6 billion in annual revenue by 2030. Pricer’s 2025 platform lets consumer goods brands bid for slot-based promotions, and early users report 3% lift on featured items. Vision systems measure dwell time and interaction, letting retailers sell premium ad slots on high-traffic shelves. The 2026 Trax-FORM merger fused shelf analytics with content orchestration, enabling labels to change creative based on inventory, shopper profile, or time of day. By combining operational and advertising benefits in a single network, the smart shelf market is moving from a cost center to a profit generator.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Up-Front Capital for Store-Wide Retrofits | -2.8% | Global, acute in emerging markets and small-format retailers | Short term (≤ 2 years) |

| Integration Complexity with Legacy POS and ERP | -1.9% | North America and Europe where legacy platforms dominate | Medium term (2-4 years) |

| Data-Privacy Compliance Burden (GDPR, CCPA) | -1.4% | Europe and North America, expanding to APAC | Medium term (2-4 years) |

| Growing Counterfeit Component Supply Risk | -0.7% | Global, concentrated in Asia-Pacific component supply chains | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High Up-Front Capital For Store-Wide Retrofits

A single hypermarket installation can cost between USD 500,000 and USD 1.5 million, placing a strain on grocers operating on single-digit EBITDA. Convenience stores average 2,500 SKUs yet pay USD 15-20 per label after installation and networking, limiting deployments unless labor and shrinkage savings exceed 15%. Low-margin operators in emerging markets confront even steeper hurdles because transaction values are smaller, while financing products that amortize hardware into service fees remain scarce outside tier-one chains.[3]Source: Retail Dive, “Capital Outlay Hinders Smart Shelf Rollouts,” retaildive.com

Integration Complexity With Legacy POS And ERP

Smart shelf platforms must handshake with decades-old point-of-sale and enterprise software, stretching timelines and inflating consulting budgets. Albertsons experienced price mismatches after early SAP integrations, triggering an emergency rollback to paper tags. Even Honeywell’s 2026 Smart Shopping Platform, which ships with pre-built connectors for leading ERPs, still requires weeks of custom mapping and testing. Retailers running multi-vendor stacks face additional dashboard fragmentation that raises the total cost of ownership and deters mid-market chains from committing capital.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Component: Subscription Services Gain Momentum

Services with 23.51% CAGR growth outpace hardware as retailers convert one-time purchases into recurring contracts that bundle analytics, maintenance, and software upgrades. The smart shelf market for services is scaling rapidly because managed programs offload battery changes, firmware updates, and network monitoring to vendors, freeing internal IT capacity. Hardware, while still the largest revenue contributor at 55.11% in 2025, is undergoing price deflation as Chinese ESL production expands and e-paper yields climb. Within hardware, IoT weight sensors and edge AI cameras are capturing share because they detect shelf gaps and misplacements within seconds, complementing passive RFID readers.

Software platforms powering those services now charge USD 5,000-15,000 annually per store for dashboards that visualize shrinkage heat maps, planogram compliance, and retail-media bidding. E Ink’s collaboration with Himax on on-device AI has shifted image recognition from cloud to shelf, reducing bandwidth costs and latency.[4]Source: E Ink Holdings, “E Ink and Himax Partner on WiseEye AI Integration,” eink.com Meanwhile, ultra-high-frequency RFID Gen2v2 readers interrogate up to 1,000 tags per second, opening warehouse and distribution center cases for the smart shelf market.

By Technology: Vision Systems Accelerate, RFID Retains Core Share

RFID-based shelves hold 40.18% smart shelf market share because they work without line-of-sight and plug into global supply-chain standards. Kroger extended RFID from apparel into the fresh bakery to automate expiry, validating use cases beyond hardlines. Yet vision and camera systems are scaling at a 24.28% CAGR, driven by falling edge AI compute costs and improved planogram accuracy. Trax alone photographs more than 400,000 stores worldwide, proving image-based audits can match or exceed RFID for some merchandising tasks.

Electronic shelf labels overlap both technologies and now carry near-field communication chips that let shoppers tap for ingredient data, uniting physical shelves with digital content. Weight-sensor shelves fill safety-critical niches such as pharmacy narcotics tracking, where instant removal alerts deter diversion. New battery-free RFID prototypes from Energous and Georgia Tech promise to eliminate maintenance costs and unlock ultra-dense tagging that was previously uneconomic, reinforcing RFID relevance in the smart shelf market.

By Retail Format: Convenience Stores Close The Gap

Hypermarkets and supermarkets held a 48.15% share, led 2025 deployments, and remain volume anchors because their high SKU counts and floor areas magnify ROI. Walmart’s 2,300-store ESL program underscores scale leverage in the smart shelf market. Nevertheless, convenience stores clock the fastest growth at a 24.19% CAGR through 2031. Limited staff and high traffic make automated price changes and real-time stock alerts disproportionately valuable in small boxes, evidenced by Asda’s 250 Express-store rollout.

Pharmacies are adopting ESLs to comply with serialization requirements and to synchronize promotional pricing across the chain, while specialty stores such as electronics retailers use RFID to protect high-value goods and enable self-checkout. Warehouses and distribution centers represent a nascent format but are layering smart shelves onto autonomous mobile robot workflows for frictionless inventory updates. Modular kits enable pop-up and club formats to reposition shelves without rewiring, broadening the addressable market for the smart shelf market.

By Application: Planogram Precision Rises In Priority

Inventory management captured 45.11% of 2025 revenue because grocers still rank on-shelf availability as the top operational metric. Focal Systems improved Fresh Market's availability to 99% by moving from daily human checks to continuous computer vision monitoring. Planogram management, however, is advancing at a 23.47% CAGR as headquarters demand automatic proof that every SKU sits in its authorized lane. The 2026 Trax-FORM platform lets store managers receive mobile prompts and close the compliance loop in hours rather than days.

Pricing management has shifted from differentiator to table stakes as competitive price-comparison apps proliferate. Content management, meanwhile, is gaining momentum owing to EU Farm-to-Fork origin-labeling rules that ESLs can implement instantly without paper changes. Engagement-focused applications, from QR codes that link to recipes to labels that display loyalty points, are broadening the smart shelf market beyond efficiency into experience and storytelling.

Geography Analysis

North America generated 34.16% of 2025 revenue as Walmart and Kroger scaled ESL and RFID programs. U.S. labor inflation and an established vendor ecosystem underpin mainstream adoption, while Canadian pilots accelerate following Walmart Canada's requirement that suppliers tag apparel and home goods. Mexico’s leading grocers are testing ESLs to align omnichannel prices and curb checkout disputes, yet high capital costs are slowing broad mid-market adoption.

Europe follows as the second-largest region, led by the United Kingdom, where Morrisons, Co-op, and Waitrose each committed to nationwide ESL coverage. Germany’s Kaufland, France’s Carrefour, and Spain’s pharmacy chains illustrate the breadth of the continent, and the EU AI Act is shaping transparent shopper analyticsshopper analytics deployments. Northern and Eastern Europe are rolling out at a steadier pace, with Norway experimenting with demand-based dynamic pricing.

Asia-Pacific is the fastest-growing region, projected at 24.55% CAGR. China’s new retail pioneers, India’s Legal Metrology compliance, and Japan’s labor-scarce convenience chains all drive momentum, while South Korea’s domestic ESL makers scale exports. Australia’s pharmacies and Singapore’s convenience pilots showcase incremental wins in mature sub-markets, whereas wider Southeast Asia adopts cautiously amid financing limitations.[5]Economic Times, “Indian Supermarkets Adopt Electronic Shelf Labels,” retail.economictimes.indiatimes.com Middle East operators leverage government modernization funds, with Israel’s Carrefour deploying smart carts and Saudi hypermarkets embracing ESLs under Vision 2030. South Africa leads African pilots, and South America mirrors inflation-driven North American logic, with Brazil and Argentina retail chains using daily commodity swings to justify ESL speed.

Competitive Landscape

Top Companies in Smart Shelf Market

The smart shelf market exhibits moderate concentration. VusionGroup, Pricer, Hanshow, and SoluM collectively hold significant market share, but dozens of regional and specialist firms diversify the field. VusionGroup’s 2024 Retail Insight purchase expanded its analytics stack, and Hanshow’s 2025 Tesco deal signaled aggressive European share capture. Pricer is countering by bundling retail-media services, while SoluM benefits from in-house manufacturing scale.

Disruptors Trax and Focal Systems package computer vision with shelf displays to deliver dual operational- and media-ROI, winning pilots at chains that previously used single-purpose hardware. Zebra Technologies’ 2026 AI-powered mobile computers converge RFID and computer vision into a single device, reducing hardware redundancy. Patent activity around battery-free RFID from Energous, Tageos, and Georgia Tech hints at another competitive axis focused on maintenance-free sensors.[6]Zebra Technologies, “Zebra Unveils AI-Powered Retail Solutions,” zebra.com

Standards bodies GS1 and ISO are finalizing interoperability guidelines that could slice switching costs and intensify price competition. Vendors therefore compete on display refresh speed, battery life, and low-touch integration.

Smart Shelf Industry Leaders

VusionGroup S.A.

Pricer AB

Hanshow Technology Co., Ltd.

Displaydata Limited

SoluM Co., Ltd.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2026: Trax and FORM closed a USD 1 billion merger to unite shelf analytics and task management.

- February 2026: Zebra Technologies debuted TC501 and TC701 handhelds with integrated RFID for faster inventory audits.

- January 2026: Honeywell rolled out Smart Shopping Platform with Google Cloud, bundling ERP connectors to streamline integrations.

- December 2025: Waitrose and SOLUM forged a partnership to roll out electronic shelf labels (ESLs) in all Waitrose stores across the UK. The initiative, set to wrap up by 2026, aims to cut down the time spent on manual ticket updates.

- October 2025: Morrisons finished installing 10.8 million ESLs across its UK estate, enabling intraday price updates.

Global Smart Shelf Market Report Scope

The Smart Shelf Market Report is Segmented by Component (Hardware, Software, and Services), Technology (RFID-Based, Weight Sensor-Based, Vision/Camera-Based, ESL Systems, and Other Technologies), Retail Format (Hypermarkets and Supermarkets, Convenience Stores, Specialty Stores, Pharmacies, Warehouses and Distribution Centers, and Other Retail Formats), Application (Inventory, Pricing, Content, Planogram, and Other Applications), and Geography (North America, Europe, Asia-Pacific, Middle East, Africa, and South America). Market Forecasts are Provided in Terms of Value (USD).

| Hardware | IoT Sensors |

| RFID Tags and Readers | |

| Electronic Shelf Lables (ESL) | |

| Cameras | |

| Software | |

| Services |

| RFID-Based Smart Shelves |

| Weight Sensor-Based Smart Shelves |

| Vision/Camera-Based Smart Shelves |

| Electronic Shelf Label (ESL) Systems |

| Other Technologies |

| Hypermarkets and Supermarkets |

| Convenience Stores |

| Specialty Stores |

| Pharmacies |

| Warehouses and Distribution Centers |

| Other Retail Formats |

| Inventory Management |

| Pricing Management |

| Content Management |

| Planogram Management |

| Other Applications |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | United Kingdom |

| Germany | |

| France | |

| Italy | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East | Israel |

| Saudi Arabia | |

| United Arab Emirates | |

| Turkey | |

| Rest of Middle East | |

| Africa | South Africa |

| Egypt | |

| Rest of Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Component | Hardware | IoT Sensors |

| RFID Tags and Readers | ||

| Electronic Shelf Lables (ESL) | ||

| Cameras | ||

| Software | ||

| Services | ||

| By Technology | RFID-Based Smart Shelves | |

| Weight Sensor-Based Smart Shelves | ||

| Vision/Camera-Based Smart Shelves | ||

| Electronic Shelf Label (ESL) Systems | ||

| Other Technologies | ||

| By Retail Format | Hypermarkets and Supermarkets | |

| Convenience Stores | ||

| Specialty Stores | ||

| Pharmacies | ||

| Warehouses and Distribution Centers | ||

| Other Retail Formats | ||

| By Application | Inventory Management | |

| Pricing Management | ||

| Content Management | ||

| Planogram Management | ||

| Other Applications | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | United Kingdom | |

| Germany | ||

| France | ||

| Italy | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East | Israel | |

| Saudi Arabia | ||

| United Arab Emirates | ||

| Turkey | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Egypt | ||

| Rest of Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

What is the current size of the global smart shelf market?

The smart shelf market size stands at USD 6.28 billion in 2026 and is projected to reach USD 17.76 billion by 2031.

Which component category is expanding the fastest?

Services are the fastest-growing component, advancing at a 23.51% CAGR because retailers increasingly purchase subscription bundles for analytics and maintenance.

Why are convenience stores investing heavily in smart shelves?

Convenience stores face acute labor shortages and margin pressure, and smart shelves automate price updates and shrinkage control, delivering a forecast 24.19% CAGR for the format.

How are smart shelves generating new revenue streams?

ESLs now double as programmable mini-screens that display paid brand promotions, enabling retailers to monetize shelf edges as part of in-store retail-media networks.

What is the most significant technical hurdle during deployment?

Integration with legacy point-of-sale and ERP software often adds weeks of custom development, inflates consulting costs and delays go-live schedules.

Which region is expected to record the highest growth rate?

Asia-Pacific is forecast to grow at a 24.55% CAGR through 2031, propelled by China's new-retail chains, India's pricing compliance rules and Japan's labor challenges.

Page last updated on: