Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 89.07 Billion |

| Market Size (2031) | USD 168.66 Billion |

| Growth Rate (2026 - 2031) | 13.62% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

E-commerce Packaging Market Analysis by Mordor Intelligence

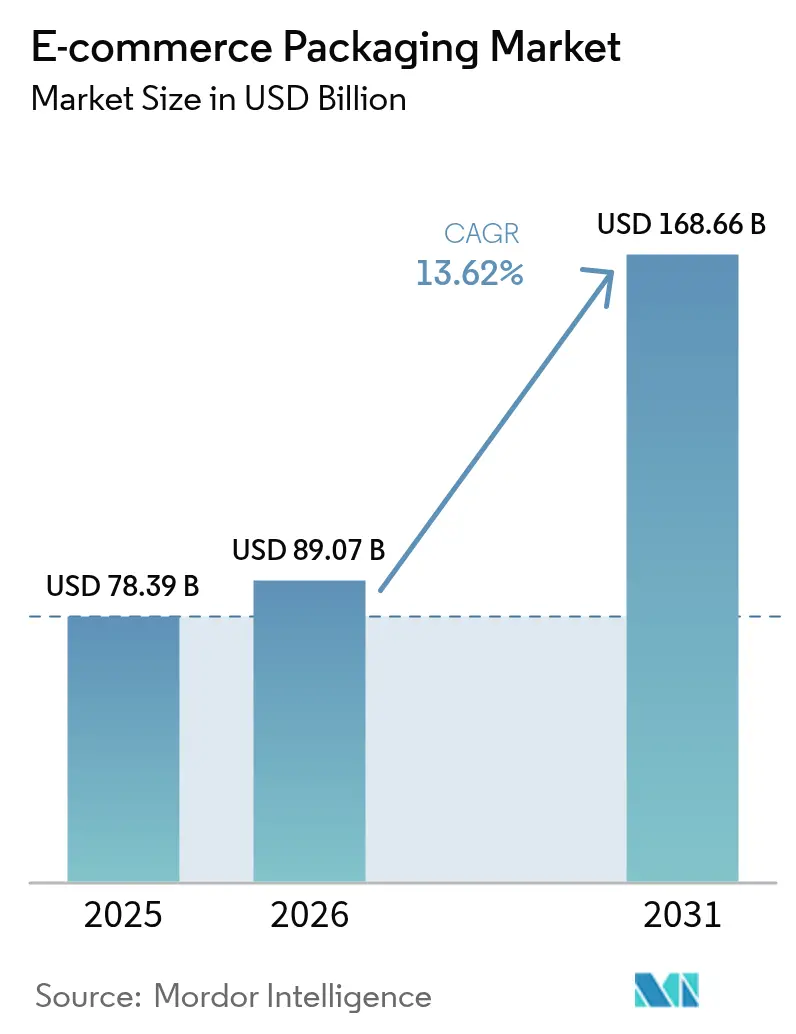

The E-commerce Packaging Market size is expected to grow from USD 78.39 billion in 2025 to USD 89.07 billion in 2026 and is forecast to reach USD 168.66 billion by 2031 at 13.62% CAGR over 2026-2031.

Volume growth stems from the surge in online retail transactions, where every single-parcel shipment replaces what was once a consolidated store delivery. Regulatory mandates that penalize difficult-to-recycle materials, coupled with rapid advances in automation and fit-to-product design software, continue to propel demand for smarter, lighter, and more sustainable packs. Material substitution toward paper, bioplastic, and mono-material flexible films is accelerating as brands align with new recycled-content quotas while still protecting goods in omnichannel logistics networks. Meanwhile, consumer expectations for premium unboxing experiences force sellers to balance aesthetics with end-of-life circularity, elevating packaging from a cost center to a revenue-generating brand asset[1]Sustainable Packaging Coalition, “Protective Packaging Design Guide,” sustainablepackaging.org.

Key Report Takeaways

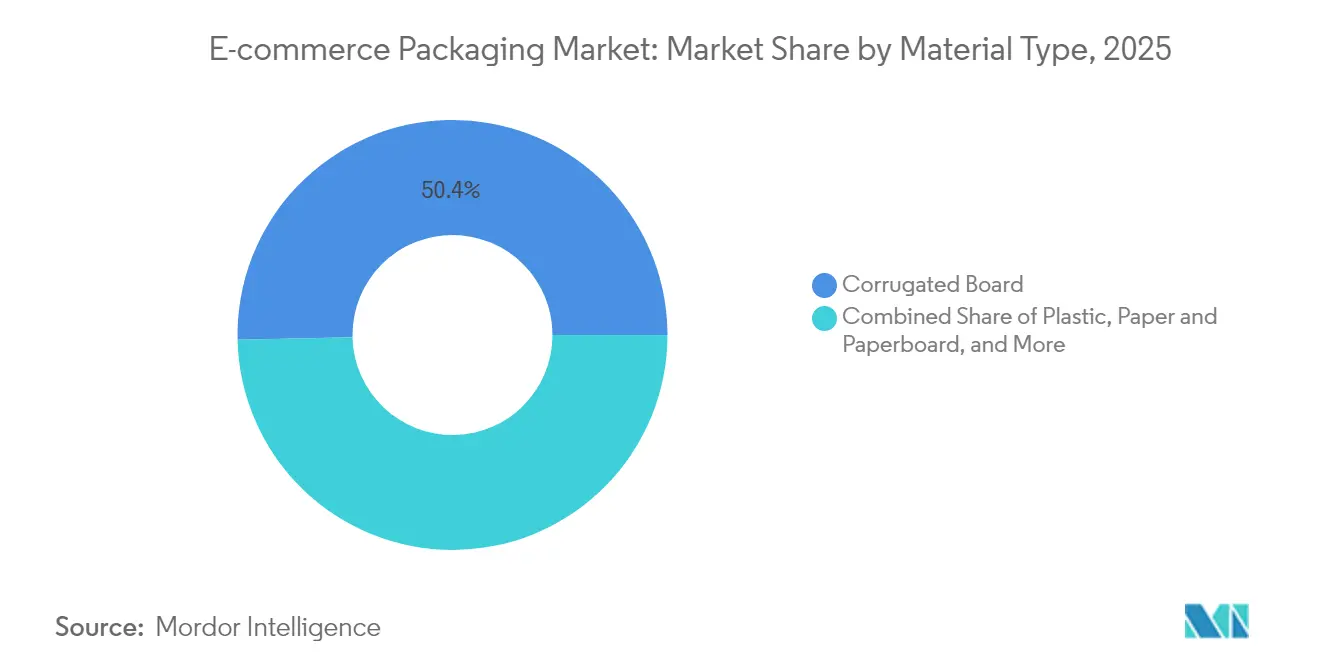

- By material type, corrugated board held 50.35% of the e-commerce packaging market share in 2025, while bioplastics are forecast to expand at a 14.72% CAGR through 2031.

- By packaging format, boxes and cartons delivered 61.20% of the e-commerce packaging market size in 2025; protective void-fill and cushioning systems are advancing at a 15.95% CAGR to 2031.

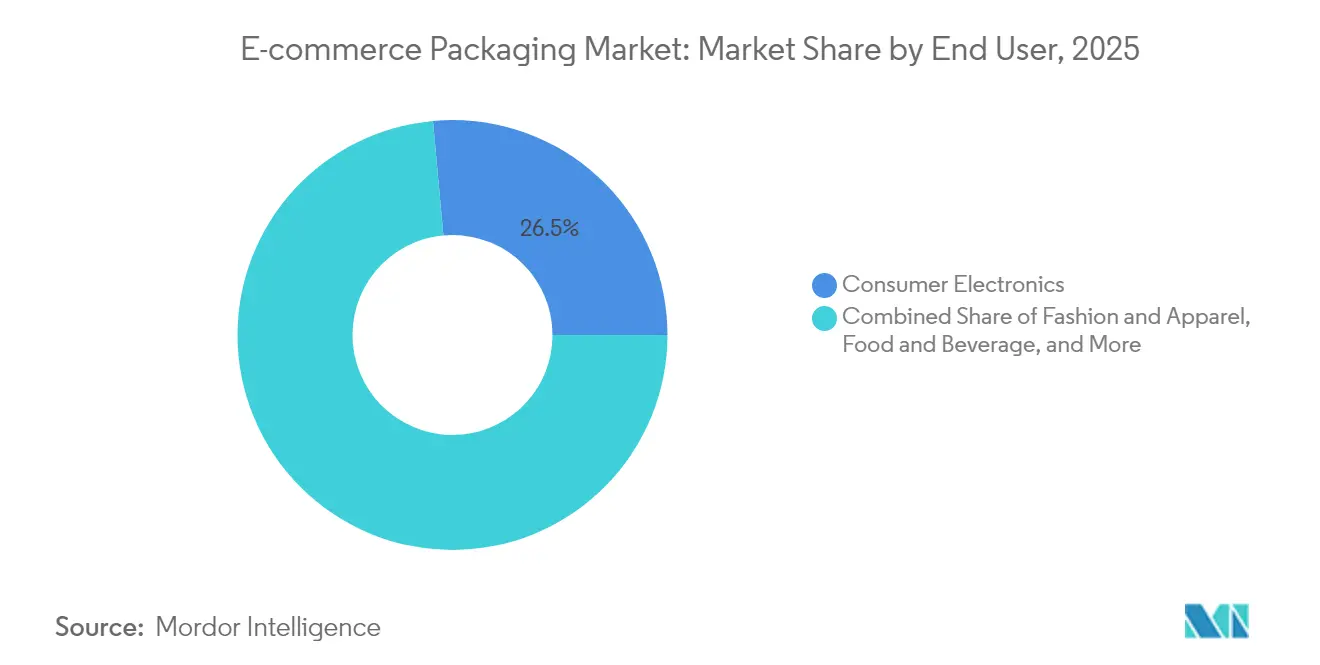

- By end user, consumer electronics accounted for 26.45% of the e-commerce packaging market size in 2025; grocery and quick-commerce are set to grow the fastest at a 14.55% CAGR between 2026 and 2031.

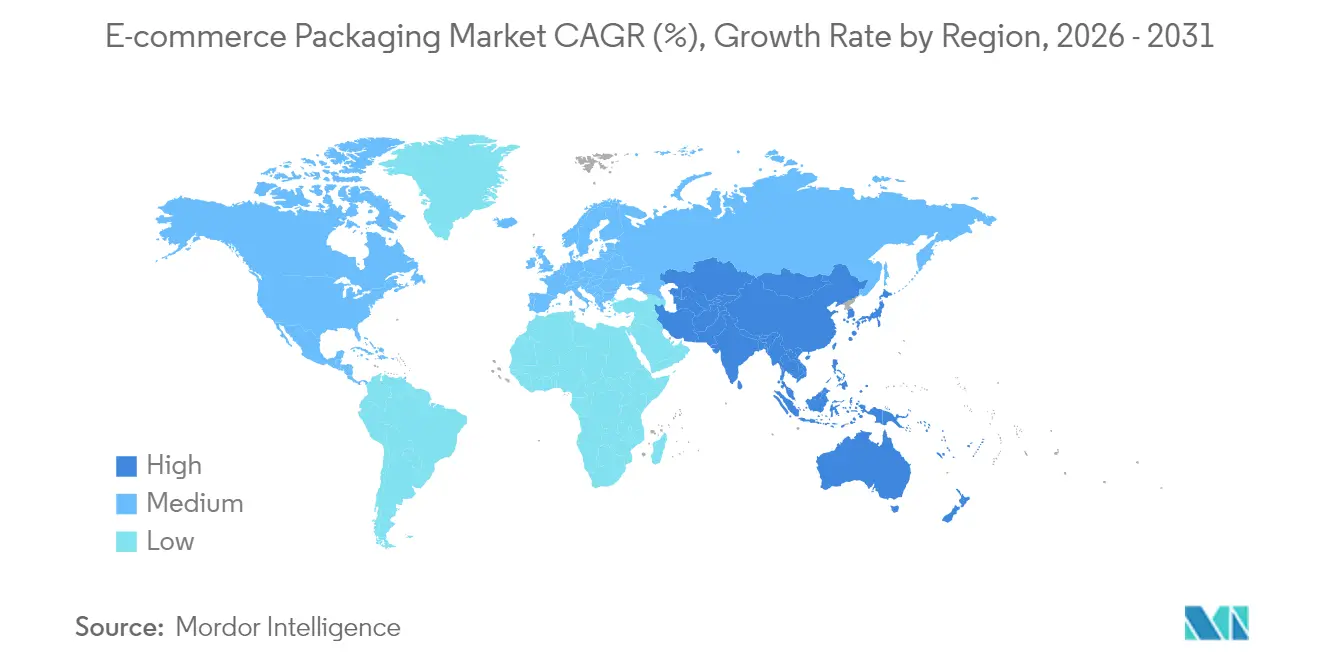

- By geography, Asia Pacific commanded 51.30% revenue share of the e-commerce packaging market in 2025 and is expanding at a 15.39% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global E-commerce Packaging Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Explosive growth of online retail GMV | +3.20% | Global, APAC leading | Short term (≤ 2 years) |

| Shift toward lightweight and flexible formats to cut DIM-weight charges | +2.10% | North America and the EU first movers, spreading to APAC | Medium term (2–4 years) |

| Sustainability regulations are accelerating paper and bio-based adoption | +2.80% | EU core, North America following, APAC selective | Medium term (2–4 years) |

| “Unboxing experience” as a brand-engagement channel | +1.40% | Global, premium segments concentrated in developed markets | Long term (≥ 4 years) |

| AI-enabled fit-to-product automation that reduces material waste | +1.90% | North America and EU early adoption, APAC scaling | Medium term (2–4 years) |

| Rapid rise of quick-commerce and subscription retail | +2.40% | Urban centers worldwide, India and China strongest | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Explosive Online Retail GMV Growth

E-commerce gross merchandise value continues to climb in double digits worldwide, and every incremental order ships in its protective pack, multiplying packaging demand faster than headline retail sales. China’s 165 cross-border pilot zones alone processed nearly 20 million packages daily in 2024, underscoring how country-level GMV expansion directly fuels corrugated and mailer consumption. Urban India’s quick-commerce operators now target 10-to-15-minute grocery delivery windows, raising packaging-to-product ratios because fragile fresh items ship individually rather than in bulk crates. Subscription commerce further amplifies volumes as recurring shipments deliver monthly replenishments in branded cartons. Longer trade lanes in cross-border commerce, from Shenzhen fulfilment hubs to Western consumers, elevate the need for thicker flute grades and engineered cushioning that can withstand multi-modal handling. These volume and performance shifts anchor the growth trajectory of the global e-commerce packaging market.

Shift Toward Lightweight and Flexible Formats

Courier dimensional-weight pricing penalizes half-empty cartons, pushing sellers to adopt right-sized mailers, collapsible pouches, and gusseted bags that shave airspace and freight spend. Amazon’s on-demand packaging initiative trimmed shipping damage 24% and cut outbound freight costs 5% by pairing machine-learning software with auto-baggers that seal film around each order. Lower-margin categories such as fast-fashion rely on flexible poly-mailers to keep packaging costs below 5% of product value, while mono-material films answer recyclability rules without sacrificing density gains. Early adoption is strongest in the United States and Europe, but the trend accelerates in Asia Pacific, where last-mile costs can exceed 30% of total logistics spend. As couriers tighten volumetric pricing, lightweight formats are likely to capture an increasing share of the e-commerce packaging market.

Sustainability Regulations Accelerating Paper and Bio-Based Adoption

The European Union’s Packaging and Packaging Waste Regulation, enacted in January 2025, mandates 30% recycled content in all plastic packs by 2030, with eco-modulated EPR fees penalizing non-recyclable formats. Complying firms turn toward paper-based wraps and bio-based polymers to sidestep fee multipliers, catalysing the “paperization” of e-retail packaging. Patagonia replaced virgin fiber shipping boxes with agricultural-waste molded fiber, slashing forest resource use while satisfying curbside-recycling requirements. Similar frameworks in California, Oregon, and Colorado extend fee structures to North America. Early movers gain supply-chain credibility and avert future market-access hurdles, giving sustainability regulations one of the highest positive impacts on e-commerce packaging market growth.

Unboxing Experience as a Brand Channel

Packaging now doubles as both shipper and storyteller. H&M’s redesigned paper mailers eliminated 2,000 tons of annual plastic while adding printed interior graphics that elevate customer experience. Luxury D2C labels embed NFC chips inside rigid boxes to authenticate goods and spark post-purchase digital engagement. Social platforms amplify these efforts, with “unboxing” videos repeatedly ranking among top e-commerce content views. As user-generated content becomes a low-cost marketing multiplier, even value retailers introduce branded tissue and variable-print box liners. The dual need for aesthetic appeal and recyclability, however, forces brands to invest in water-based inks, debossing, and mono-material adhesives to maintain end-of-life compatibility. This push–pull dynamic around beauty and responsibility underpins premium-segment growth within the broader e-commerce packaging market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Plastic bans and EPR fees are increasing compliance costs | -1.80% | EU primary, ripple to global supply chains | Short term (≤ 2 years) |

| Kraft paper and resin price volatility | -2.30% | Global, North America, and Europe are the most exposed | Short term (≤ 2 years) |

| Cross-border damage and return rates | -1.10% | Global trade routes | Medium term (2–4 years) |

| Carbon-footprint audits amid data gaps | -0.90% | Developed markets | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Stringent Plastics Bans and EPR Fees Inflate Costs

Extended Producer Responsibility schemes levy fees that vary with each material’s real-world recyclability, doubling the cost of difficult-to-recycle multilayer pouches in some EU markets. California’s Plastic Pollution Prevention Act tags flat fees on every kilogram of packaging sold, compelling brands to overhaul portfolios or absorb penalties. Smaller online sellers lacking regulatory staff struggle to complete fee filings, tilting competitive advantage toward integrated players that can spread compliance fixed costs across higher volumes. These financial headwinds pare back the potential CAGR of the e-commerce packaging market over the next two years.

Kraft Paper and Resin Price Volatility Squeezes Margins

Energy spikes and mill downtimes lifted North American linerboard prices by USD 70 per ton in early 2025, forcing box plant margins below historical 10% thresholds. Flexible-film converters faced 12% resin price swings during the same quarter as Gulf Coast cracker outages tightened supply. With packaging often capped at 3–8% of a product’s landed cost, brand owners face trade-offs between absorbing price hikes or passing them to consumers, which could soften demand. Such volatility constrains investment in capacity expansions and slows material conversion in the e-commerce packaging industry.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Material Type: Bioplastics Drive Innovation Despite Corrugated Dominance

Corrugated board captured 50.35% of the e-commerce packaging market in 2025 thanks to cost efficiency, high stacking strength, and near-universal curbside recyclability. The segment continues to benefit from China’s national express-packaging quality standard, which formalizes corrugate flute grades for domestic and export shipments. Meanwhile, bioplastics form the fastest-growing material group at a 14.72% CAGR through 2031, reflecting both regulatory tailwinds and shifting consumer sentiment. Converters blend PLA with post-consumer recyclate to create mailers that meet EU 30% recycled-content thresholds without compromising tensile performance. Investments in scalable fermentation facilities across Southeast Asia will gradually lower bio-resin premiums, enabling wider uptake beyond premium cosmetics and organic food sellers.

Brand owners balance corrugated’s reliable protection with renewable alternatives to reduce Scope 3 emissions. Although corrugate commands volume, bioplastics bring differentiation; D2C electronics sellers tout compostable film shrink sleeves as a visible sustainability upgrade. Traditional PE and PP operators respond by designing mono-material variants compatible with mechanical recycling, seeking to defend their share. The coexistence of renewable and fossil-based polymers signals a transition, not an overnight swap, ensuring both material clusters remain essential to the e-commerce packaging market.

By Packaging Format: Protective Solutions Outpace Traditional Boxes

Boxes and cartons generated 61.20% of the e-commerce packaging market size in 2025, reflecting their versatility across SKUs from apparel to small appliances. Yet protective systems, void-fill cushions, molded pulp, and air pillows are expanding at a 15.95% CAGR as retailers tackle returns tied to in-transit damage. U.S. consumer goods firms spent nearly USD 1 billion on damage-related write-offs in 2024, incentivizing thicker padding and engineered inserts that drop breakage rates below 1%. Parallel growth in flexible mailers for fashion items displaces rigid cartons, reducing cube waste and last-mile CO₂ emissions.

Cold-chain e-grocery further intensifies demand for specialized insulation. Temperature-controlled parcels for frozen meals and biologic drugs require phase-change liners that keep contents between 2 °C and 8 °C for 48 hours, pushing protective packaging revenues upward. Automated kitting lines now combine right-sized corrugated shells with on-demand air cushions, balancing performance and throughput. Integrated format portfolios give converters an edge, enabling them to service multiple needs under a single contract and strengthen their position within the e-commerce packaging industry.

By End User: Quick-Commerce Transforms Grocery Packaging

Consumer electronics remained the largest buyer group with 26.45% e-commerce packaging market share in 2025, driven by high average order values and the need for multi-layer protection. Phones, laptops, and gaming consoles travel through lengthy parcel networks, making anti-static bags and custom EPS corner blocks indispensable. Apparel follows closely, but it is the grocery and quick-commerce channel that accelerates fastest at a 14.55% CAGR to 2031. Rapid ultrafast deliveries in dense metros favor leak-proof paper bags coated with bio-waxes that resist condensation from refrigerated goods. Urban dark-store operators ship hundreds of micro-orders per hour, necessitating ergonomic tote-to-bag transfer stations and slim nested crates. Meal-kit companies, another growth node, integrate QR codes on ice-packs for end-user disposal instructions, marrying food safety with sustainability education. Cosmetics and personal-care brands invest in premium unboxing; rigid board boxes wrapped in printed kraft provide tactile cues that reinforce luxury positioning. Each vertical thus imposes distinct functional and branding requirements, sustaining product-development pipelines throughout the e-commerce packaging market.

Geography Analysis

Asia Pacific led the e-commerce packaging market with a 51.30% revenue share in 2025 and is scaling at a 15.39% CAGR through 2031. China’s national standard GB 43352-2023 defines mandatory performance metrics for express packs, driving uniform quality expectations across 6 million active online sellers. Concurrently, India’s quick-commerce sales triple between 2025 and 2030, elevating demand for lightweight yet durable bags that perform in monsoon humidity. Southeast Asian marketplaces adopt similar rules, leveraging paper cushioning to cut plastic waste, reinforcing regional momentum.

North America ranks second. California’s plastic-source-reduction targets and Canada’s ban on difficult-to-recycle foam prompt accelerated substrate shifts. Fulfilment centers invest in AI-driven box-selection tools that trim corrugated usage by 12%, supporting both cost and sustainability goals. The United States also incubates cold-chain innovations as online grocery penetration touches 16% in 2025, spurring demand for temperature-stable liners across food and pharma.

Europe remains the global test bed for circularity, with the PPWR’s recycled-content and reuse mandates shaping formats that eventually scale worldwide. Retailers in Germany pilot returnable e-grocery crates that cut single-use packs by 80% in dense urban districts. Elsewhere, the Middle East and Africa trail in adoption but record double-digit gains as cross-border platforms extend logistics footprints. Infrastructure gaps and customs complexities temper volume, yet rising smartphone penetration unlocks long-run upside, embedding emerging regions in future expansion of the e-commerce packaging market.

Competitive Landscape

The e-commerce packaging market features moderate fragmentation, yet consolidation is quickening as compliance costs rise. Amcor closed a USD 8.4 billion all-stock deal for Berry Global in April 2025, creating a USD 24 billion revenue champion with deep flexible-film and specialty carton portfolios. Three months earlier, International Paper acquired DS Smith, targeting USD 514 million in synergies and expanding its European corrugated reach. Smurfit Kappa merged with WestRock in 2024, forming Smurfit WestRock and instantly commanding more than 500 converting plants across 40 nations.

Scale matters because upcoming EPR fees demand life-cycle data and closed-loop infrastructure investments often out of reach for smaller independents. Leading groups deploy digital twins and SaaS configurators that model cube, weight, and emissions trade-offs in real time, helping clients hit both budget and ESG targets. Meanwhile, midsize specialists carve footholds in cold-chain and reusable packaging niches; Spanish startup Cool Chain’s nine-day gel-pack solution extends delivery radii for meal-kit firms, underscoring how performance-driven sub-segments can defend pricing power even as commodity corrugate margins compress.

Sustainability credentials shape buyer shortlists. Recycled-content display boxes, water-based inks, and certified-compostable mailers differentiate offerings. However, input-cost volatility threatens profitability. Vertically integrated majors hedge Kraft-Liner risk via captive paper mills, whereas converters reliant on external supply juggle spot purchases and pass-through clauses. As regulators and marketplaces raise the bar on recyclability disclosures, technology partnerships, not just raw capacity, will likely dictate future share shifts inside the e-commerce packaging industry.

E-commerce Packaging Industry Leaders

Amcor PLC

Mondi PLC

International Paper Company

Smurfit Kappa Group PLC

DS Smith PLC

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2025: Amcor completed its USD 8.4 billion combination with Berry Global, projecting USD 650 million in annual synergies and 12% EPS accretion by FY 2026.

- February 2025: International Paper finalized its acquisition of DS Smith, issuing 179,847,780 new shares and targeting USD 514 million in synergies.

- January 2025: The European Union enforced the Packaging and Packaging Waste Regulation, mandating 30% recycled content in plastic packaging by 2030.

Global E-commerce Packaging Market Report Scope

In E-commerce packaging, businesses wrap their products so they are shipped to the customer after being stored in a warehouse. It's a kind of protective package that must be able to accommodate travel and protect the product from damage.

The e-commerce packaging market is segmented by material (plastics, corrugated board, paper, and other materials), end-user vertical (fashion and apparel, consumer electronics, food & beverages, personal care products, and other end users), and geography (North America (United States, Canada), Europe (United Kingdom, Germany, France, Rest of Europe), Asia-Pacific (China, India, Japan, Rest of Asia-Pacific), (Latin America (Brazil, Argentina, Rest of Latin America), Middle East & Africa (United Arab Emirates, Saudi Arabia, South Africa, Rest of Middle & Africa)). The market sizes and values are provided in terms of value (USD) for all the above segments.

By Material Type

| Plastic |

| Paper and Paperboard |

| Corrugated Board |

| Flexible Films and Mailers |

| Bioplastics |

| Others |

By Packaging Format

| Boxes and Cartons |

| Mailers and Envelopes |

| Protective Packaging (void-fill, cushioning, liners) |

| Labels, Tapes and Closures |

| Specialty/Returnable Systems |

By End User

| Fashion and Apparel |

| Consumer Electronics |

| Food and Beverage |

| Personal Care and Cosmetics |

| Grocery and Quick-Commerce |

| Home and Living/Furniture |

| Other Online Retailers |

By Geography

| North America | United States |

| Canada | |

| Mexico | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Europe | United Kingdom |

| Germany | |

| France | |

| Italy | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East and Africa | United Arab Emirates |

| Saudi Arabia | |

| South Africa | |

| Rest of Middle East and Africa |

| By Material Type | Plastic | |

| Paper and Paperboard | ||

| Corrugated Board | ||

| Flexible Films and Mailers | ||

| Bioplastics | ||

| Others | ||

| By Packaging Format | Boxes and Cartons | |

| Mailers and Envelopes | ||

| Protective Packaging (void-fill, cushioning, liners) | ||

| Labels, Tapes and Closures | ||

| Specialty/Returnable Systems | ||

| By End User | Fashion and Apparel | |

| Consumer Electronics | ||

| Food and Beverage | ||

| Personal Care and Cosmetics | ||

| Grocery and Quick-Commerce | ||

| Home and Living/Furniture | ||

| Other Online Retailers | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | United Kingdom | |

| Germany | ||

| France | ||

| Italy | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | United Arab Emirates | |

| Saudi Arabia | ||

| South Africa | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

What is the current value of the e-commerce packaging market?

The e-commerce packaging market is valued at USD 89.07 billion in 2026.

How fast is the e-commerce packaging market expected to grow?

It is forecast to grow at a 13.62% CAGR, reaching USD 168.66 billion by 2031.

Which region leads the e-commerce packaging market?

Asia Pacific holds the leading position with 51.30% revenue share in 2025 and the highest growth outlook through 2031.

Which material accounts for the largest volume in e-commerce packaging?

Corrugated board remains the dominant material, capturing 50.35% of global volume in 2025.

Why are protective packaging formats gaining momentum?

Retailers focus on damage reduction, with void-fill and cushioning solutions growing at a 15.95% CAGR as they cut returns and enhance customer experience.

How are regulations influencing material choices?

EU and North American recycled-content mandates push brands toward paper and bio-based alternatives that avoid escalating EPR fees while supporting circular-economy goals.

Page last updated on: