Smart Warehousing Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

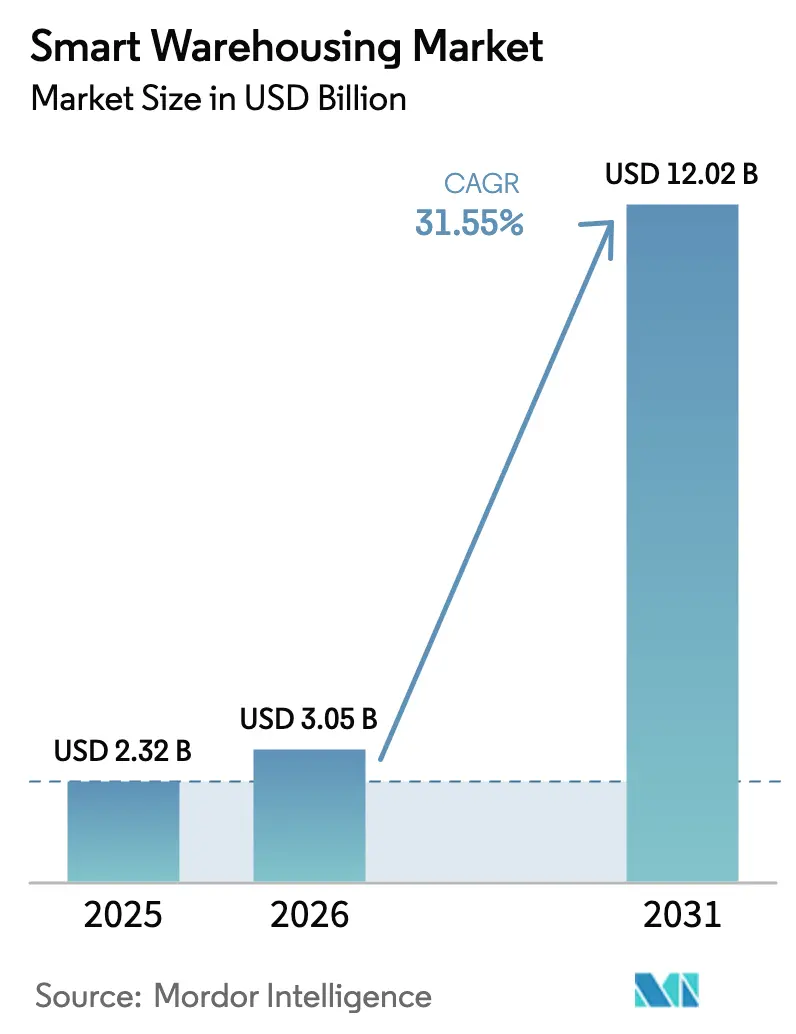

| Market Size (2026) | USD 3.05 Billion |

| Market Size (2031) | USD 12.02 Billion |

| Growth Rate (2026 - 2031) | 31.55% CAGR |

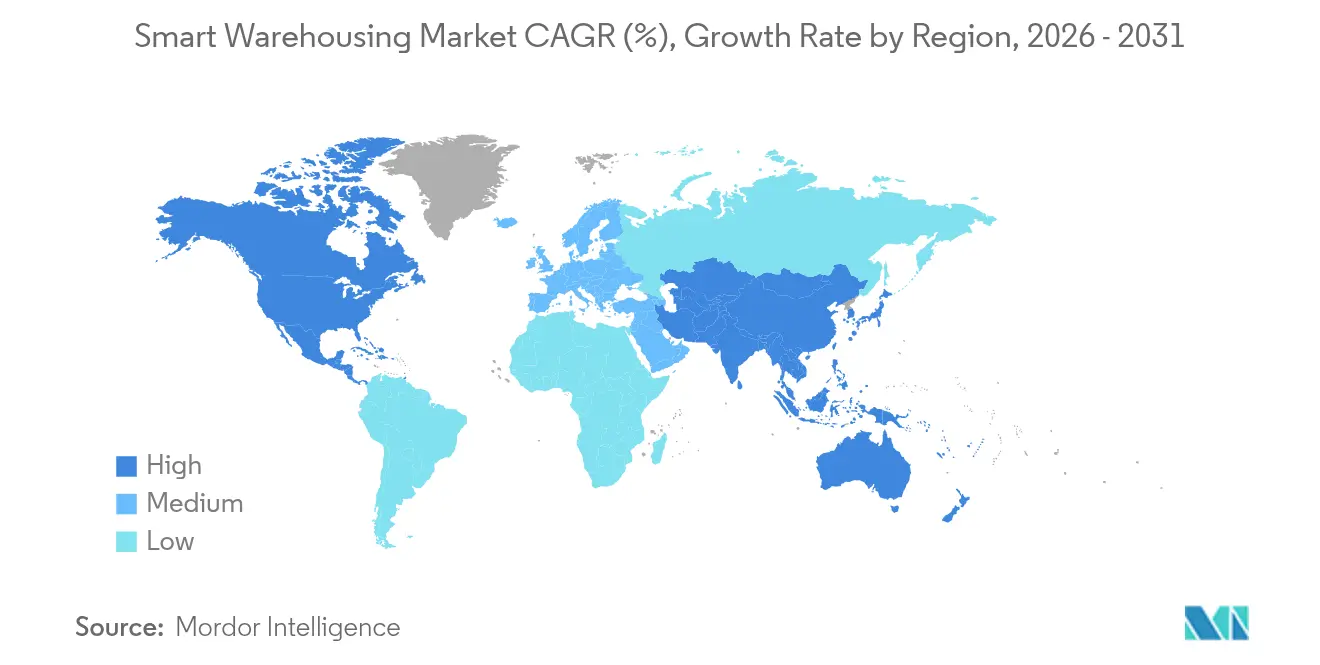

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Smart Warehousing Market Analysis by Mordor Intelligence

The smart warehousing market size is expected to grow from USD 2.32 billion in 2025 to USD 3.05 billion in 2026 and is forecast to reach USD 12.02 billion by 2031 at 31.55% CAGR over 2026-2031. Accelerated e-commerce expansion, labor shortages, and the quest for real-time visibility are reshaping fulfillment operations in every major logistics hub. Continuous price pressure on warehouse space and rising energy costs further push operators toward automation that maximizes cubic utilization and lowers total cost to serve. Cloud-native warehouse management systems (WMS), autonomous mobile robots (AMR), and sensor-rich Internet of Things (IoT) networks now converge into cohesive platforms that deliver near-perfect inventory accuracy while cutting travel time inside facilities by double-digit percentages. Venture investment and strategic acquisitions indicate that integrated automation stacks rather than single-point tools will capture the largest pools of value in the smart warehousing market.

Key Report Takeaways

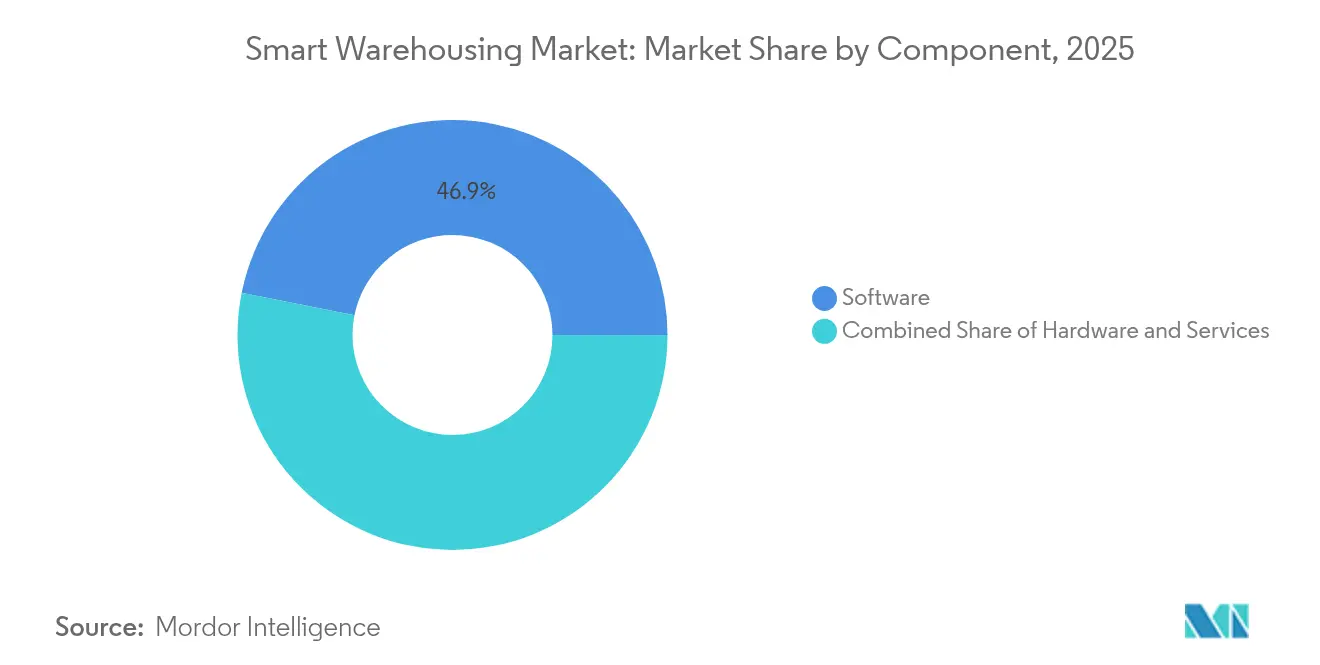

- By component, software led with 46.85% revenue share in 2025, while services are projected to grow at an 17.9% CAGR through 2031.

- By deployment, cloud platforms accounted for 60.35% of the smart warehousing market share in 2025 and are expected to post a 18.75% CAGR to 2031.

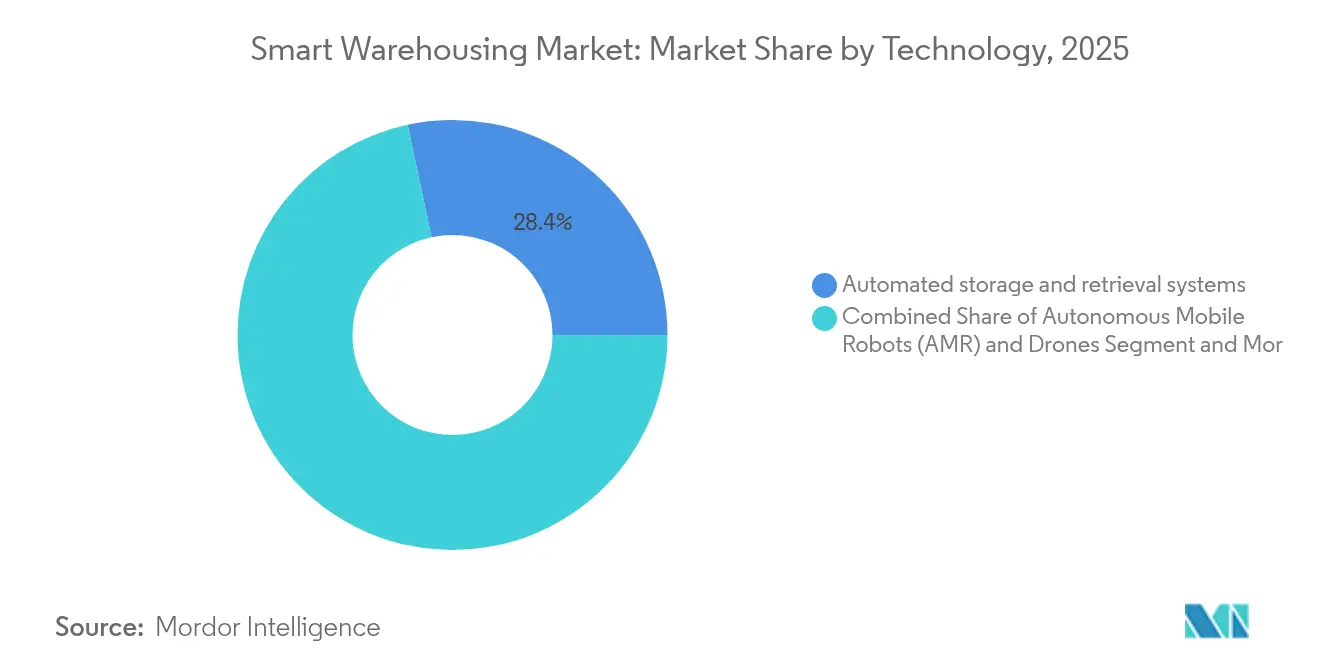

- By technology, automated storage and retrieval systems captured 28.35% of the smart warehousing market size in 2025; autonomous mobile robots and drones are forecast to expand at a 23.4% CAGR between 2026-2031.

- By end-user, retail and e-commerce held 38.10% of smart warehousing market share in 2025, while healthcare and pharmaceuticals are set to advance at a 20.7% CAGR through 2031.

- By geography, North America led with 33.40% revenue share in 2025; Asia-Pacific is projected to register the fastest regional CAGR of 16.6% over the same period.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Market Trends and Insights

Drivers Impact Analysis of Smart Warehousing Market*

| Driver | ( ~ ) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Expansion of e-commerce ecosystems | +8.2% | Global; strong in North America & Asia-Pacific | Medium term (2-4 years) |

| Rising demand for warehouse automation and robotics | +7.5% | Global; led by North America & Europe | Long term (≥ 4 years) |

| Rapid adoption of cloud-native WMS platforms | +6.1% | Global; early in North America | Short term (≤ 2 years) |

| IoT-enabled real-time inventory visibility | +4.8% | Global; strong uptake in Asia-Pacific | Medium term (2-4 years) |

| Government incentives for logistics tech upgrades | +3.2% | North America, Europe, select Asia-Pacific markets | Medium term (2-4 years) |

| 5G private networks powering large-scale warehouse IoT | +2.9% | North America, Europe, Japan, South Korea | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Expansion of E-commerce Ecosystems

E-commerce order profiles shift SKU velocity from pallets to single-unit picks, forcing operators to adopt flexible automation that processes thousands of discrete lines per hour. Material Bank scaled its robotic fleet from 10 to 45 units within seven months to handle over 300,000 units monthly, tripling revenue without expanding floor space[1]Material Bank, “Automated Fulfillment Case Study,” locusrobotics.com. Same-day delivery promises amplify the need for dense urban fulfillment nodes, where smart warehousing systems cut cycle times by routing AMR fleets through algorithm-optimized paths. Retailers also cite energy savings and reduced lighting needs as secondary gains when goods-to-person systems shrink travel distances. Together, these factors make automated micro-fulfillment a default roadmap item for omnichannel leaders in the smart warehousing market.

Rising Demand for Warehouse Automation and Robotics

Projected shortages of 85 million logistics workers by 2030 elevate automation from optional improvement to operational safeguard. Dorman Products recorded a 16% cut in picker travel distance after AMR rollout, freeing employees for exception handling and value-added kitting[2]Dorman Products, “AMR Deployment Results,” zebra.com. Robotics adoption lowers incident rates; facilities report up to 60% fewer safety events owing to reduced forklift traffic. Higher hourly wages since 2024 compress payback periods to 18-24 months, strengthening investment cases for end-to-end robotics inside the smart warehousing market.

Rapid Adoption of Cloud-native WMS Platforms

Micro-services-based WMS eliminate version lock-in and push continuous feature drops that keep pace with shifting order profiles. Manhattan Associates’ platform allows rule changes without downtime, enabling a national distributor to standardize picking logic across 110 sites. Subscription pricing turns once-capital-heavy software into an operating expense, widening access for mid-tier warehouses. Scalability in peak seasons—automatic server headroom that supports Black Friday order spikes—is a decisive advantage driving cloud preference across the smart warehousing market.

IoT-enabled Real-time Inventory Visibility

Sensor tags deliver perpetual stock counts that lift inventory accuracy from 95% to 98%, reducing stockouts and cutting working capital needs. Temperature and humidity sensors secure pharmaceutical chains, with alerts triggering robotics-based relocations to safe zones in minutes. Predictive analytics harness this data to recommend reorder points and pre-empt slotting bottlenecks, deepening value extraction from IoT in the smart warehousing market.

Restraints Impact Analysis of Smart Warehousing Market*

| Restraint | ( ~ ) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High upfront capital expenditure | -4.1% | Global; burdens SMEs | Short term (≤ 2 years) |

| Legacy system integration complexity | -3.8% | Global; acute in mature markets | Medium term (2-4 years) |

| Cyber-security talent gap in operational technology | -2.3% | Global; acute in North America & Europe | Long term (≥ 4 years) |

| Fragmented global robotics safety standards | -1.9% | Global; regional variation | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High Upfront Capital Expenditure

Autonomous forklifts in Japan carry price tags near 15 million yen (USD 100,000), versus 2 million yen (USD 13,300) for manual units, with network upgrades adding to the bill. Robotics-as-a-service models smooth budgets but asset-heavy mechanical systems still demand credit lines beyond many SMEs’ reach. Rising steel and energy prices inflate new-build warehouses, pushing operators to weigh brownfield retrofits against pure greenfield automation. Although ROI windows compress, sticker shock continues to temper adoption pace within the smart warehousing market.

Legacy System Integration Complexity

WMS and ERP platforms built on monolithic codebases resist low-code interfaces that modern automation vendors supply. Integration services can represent up to 40% of project spend, particularly where multiple robotics brands converge. Lapses during cut-overs risk shipping delays, so operators schedule phased rollouts that extend timelines and inflate costs. API standardization efforts gain momentum, yet fragmented data models still slow seamless orchestration across the smart warehousing market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Smart Warehousing Market Segment Analysis

By Component:

Software Dominance Drives Platform IntegrationSoftware controlled 46.85% of revenue in 2025, reflecting its position as the orchestration layer of every smart warehousing market deployment. Cloud-native WMS and execution platforms allow dynamic slotting, algorithmic task allocation, and predictive maintenance scheduling that elevate overall equipment effectiveness. Services, projected to grow at an 17.9% CAGR, address integration complexity and ongoing optimization demands as operators layer robotics, IoT, and analytics into legacy buildings. Hardware growth remains steady as falling sensor and servo costs widen automation’s addressable base.

The traction of software-defined warehousing shows how value migrates from physical machinery to data-rich control towers. Manhattan Associates uses machine learning to recalibrate pick paths hourly, producing double-digit throughput lifts without new conveyors. Service providers monetize continuous improvement mandates through managed automation contracts, reinforcing annuity revenue streams in the smart warehousing market.

By Deployment:

Cloud Platforms Accelerate Market TransformationCloud installations covered 60.35% of sites in 2025 and will outpace on-premises solutions at a 18.75% CAGR. Elastic compute resources help warehouses ramp during holiday peaks, while vendor-managed updates cut IT workload. Security-sensitive industries, such as defense logistics, still retain on-prem systems to keep traffic behind firewalls, yet even those facilities test hybrid models that bridge local control with cloud analyts.

Sysco’s migration to a multi-tenant WMS across 110 distribution centers shows cloud’s ability to unify standard operating procedures without capital spikes. Subscription pricing shifts spend from capex to opex, letting small operators enter the smart warehousing market sooner than legacy models allowed.

By Technology:

AMR Innovation Disrupts Traditional AutomationAutomated storage and retrieval systems accounted for 28.35% of the smart warehousing market size in 2025. These high-density towers remain dominant in unit-load environments where throughput is predictable. AMR and drones, however, are slated for 23.4% CAGR as their plug-and-play nature sidesteps heavy steel and track infrastructure. IoT sensor grids supply live status feeds, while execution software synchronizes task cues across robots, conveyors, and humans.

CJ Logistics achieved 20% productivity gains after deploying AMR fleets on private 5G, proof that reliable connectivity multiplies robotics output. The convergence of AI navigation, machine vision, and 5G backbones forms the next innovation curve within the smart warehousing market.

By End-user:

Healthcare Transformation Leads GrowthRetail and e-commerce produced 38.10% of revenue in 2025, leveraging automation to fulfill single-item orders with millimeter-level accuracy. Healthcare and pharmaceuticals will expand at a 20.7% CAGR, propelled by temperature-controlled storage and serialization laws that require item-level tracking. Manufacturers continue embedding warehouses into Industry 4.0 production loops, while third-party logistics providers position automation as a premium differentiator.

Cardinal Health doubled overall effectiveness after rolling out AMR fleets, slashing cycle times while lifting worker satisfaction. Such results fortify automation commitments across regulated sectors of the smart warehousing market.

Geography Analysis

North America Smart Warehousing Market

North America maintained 33.40% revenue share in 2025 thanks to early technology adoption, robust venture funding, and programs such as the USD 160 million SMART Grants that subsidize logistics technology upgrades. Retail giants have steered more than USD 520 million into warehouse robotics partnerships, accelerating ecosystem maturity. Canada’s Green Freight Program adds a USD 200 million incentive pool that offsets capital and fuels energy-efficient retrofits.

APAC Smart Warehousing Market

Asia-Pacific is projected to post a 16.6% CAGR through 2031, narrowing the leadership gap. Chinese vendors such as Hai Robotics raised USD 100 million Series D+ funding to scale autonomous case-handling exports. In Japan, acute labor shortages justify 15 million yen autonomous forklifts despite high entry costs. Private 5G rollouts underpin warehouse IoT backbones, with early deployments demonstrating 15% capex savings versus wired alternatives.

EMEA and South America Smart Warehousing Market

Europe sustains steady growth, buoyed by European Investment Bank loans such as the EUR 8 million line to Nomagic for AI-enabled picking R&D. Vendors like Exotec surpassed USD 1 billion in systems sold and now target Central and Eastern European markets. Emerging regions in the Middle East, Africa, and South America remain nascent, yet rising e-commerce penetration and infrastructure investment signal mid-term lift for the smart warehousing market.

Competitive Landscape

The smart warehousing market shows moderate fragmentation. Enterprise software incumbents—including Manhattan Associates, Oracle, and SAP—extend orchestration layers that integrate robotics from specialist vendors. Robotics leaders such as Locus Robotics, Hai Robotics, and Symbotic push hardware and AI boundaries, while automation integrators bundle multi-vendor portfolios into turnkey deployments.

Recent consolidation underscores the race for integrated platforms. Symbotic acquired Walmart’s advanced systems unit for USD 200 million, adding proven solutions and a 400-site commitment to its backlog. Zebra Technologies purchased Photoneo to marry 3D vision with its scanning line, broadening appeal inside pick-and-place cells. Strategic partnerships, such as Manhattan Associates’ agreement with Shopify, fuse front-end commerce data with back-end inventory orchestration, highlighting omnichannel imperatives.

Competitive differentiation now turns on ecosystem breadth, time-to-value, and outcome-based pricing. As-a-service models let mid-size operators defer capital outflow, eroding barriers historically favoring giants. Patent activity around predictive maintenance, human-robot collaboration, and AI navigation indicates future battle lines across the smart warehousing market.

Smart Warehousing Industry Leaders

Manhattan Associates, Inc.

Korber AG

Oracle Corporation

SAP SE

Tecsys Inc.

- *Disclaimer: Major Players sorted in no particular order

Smart Warehousing Market Companies Covered in this Report

- Manhattan Associates, Inc.

- Korber AG

- Oracle Corporation

- SAP SE

- Tecsys Inc.

- PSI Logistics GmbH

- International Business Machines Corporation (IBM)

- Generix Group SA

- Microsoft Corporation

- Mantis Informatics, Inc.

- Dematic Corp. (a KION Group Company)

- Honeywell International Inc.

- Swisslog Holding AG (part of KUKA AG)

- Blue Yonder Group, Inc.

- Infor Inc.

- Zebra Technologies Corporation

- GreyOrange Pte. Ltd.

- Locus Robotics Corporation

- KNAPP AG

- Amazon.com, Inc.

Recent Industry Developments in Smart Warehousing Market

- January 2025: Symbotic completed a USD 200 million acquisition of Walmart’s Advanced Systems and Robotics business, securing commitments for 400 automation sites Symbotic.

- January 2025: Shopify and Manhattan Associates launched an omnichannel alliance; Nautica became the inaugural customer Manhattan.

- December 2024: Zebra Technologies acquired Photoneo to strengthen machine-vision robotics portfolios Robotics 24/7.

- December 2024: Exotec surpassed USD 1 billion in systems sold, marking a milestone in robotics adoption Exotec.

Smart Warehousing Market Report Scope and Research Methodology

Market Definition and Coverage

Our study defines the smart warehousing market as every software module, connected sensor, autonomous robot, and intelligent material-handling system that together digitize, automate, and orchestrate activities from receiving through dispatch inside warehouses and fulfillment centers. Revenues counted include new hardware sales, cloud or on-premise software licenses, and systems-integration services that enable real-time, data-driven operations, which lets us mirror what buyers actually spend.

Scope exclusion: Land or building rental income and conventional forklifts with no connectivity layer are left out.

Segments Covered in This Report

- By Component

- Hardware

- Software

- Services

- By Deployment

- Cloud

- On-Premises

- By Technology

- Automated Storage and Retrieval Systems (AS/RS)

- Autonomous Mobile Robots (AMR) and Drones

- IoT Sensors and Connectivity

- Warehouse Management and Execution Software

- By End-user

- Retail and E-commerce

- Manufacturing

- Healthcare and Pharmaceuticals

- Automotive

- Energy and Utilities

- Third-Party Logistics (3PL) Providers

- By Geography

- North America

- United States

- Canada

- Mexico

- South America

- Brazil

- Argentina

- Rest of South America

- Europe

- United Kingdom

- Germany

- France

- Italy

- Spain

- Nordics

- Rest of Europe

- Middle East and Africa

- GCC

- Israel

- South Africa

- Rest of Middle East and Africa

- Asia-Pacific

- China

- India

- Japan

- South Korea

- ASEAN

- Australia

- New Zealand

- Rest of Asia-Pacific

- North America

Data Sources, Market Sizing, and Validation

Primary Research

Mordor analysts interviewed warehouse-automation integrators, WMS product leads, 3PL operations heads, and e-commerce fulfillment managers across North America, Europe, and Asia-Pacific. Those conversations clarified average selling prices, payback expectations, and cloud-WMS penetration assumptions that generic desk sources rarely reveal.

Desk Research

We began with open datasets from the US Census Annual Survey of Warehousing, Eurostat structural business statistics, and UN COMTRADE shipment codes that track automated handling equipment. We then matched those baselines with technology-adoption surveys released by the International Federation of Robotics. Trade briefs from MHI, Logistics UK, and JPN-LOG served to benchmark regional automation uptake, while reputable news archives in Dow Jones Factiva captured fresh investment signals. Company 10-Ks, IPO filings, and D&B Hoovers revenue splits helped our team link headline spending to individual vendors, and customs duty digests showed cross-border robot flows that many public sources miss. This list is illustrative; numerous additional public documents informed data checks and narrative framing.

Market-Sizing & Forecasting

We start with a top-down reconstruction that scales national warehousing floor space and parcel volumes, applies technology-penetration ratios, and then multiplies them by sampled average prices to approximate spend pools. Select bottom-up roll-ups of integrator revenues and hardware shipments validate and fine-tune totals, ensuring one approach does not dominate. Key variables include new warehouse completions, share of picks executed by robots, median cloud-WMS subscription fees, labor-cost inflection points, and regional capital-spending appetites. A multivariate regression projects those drivers to 2030, while scenario analysis captures swings caused by interest-rate shocks or supply-chain realignments.

Data Validation & Update Cycle

Outputs move through anomaly checks that compare model signals with import logs, robotics installation trackers, and quarterly earnings calls. Any variance beyond preset bands triggers a second analyst review before sign-off. Reports refresh each year, and an interim update is released if major policy or demand shocks emerge, so clients always receive the latest calibrated view.

How Mordor Intelligence's Smart Warehousing Market Size Compares to Other Published Estimates

Estimates from different publishers often diverge because each one selects unique service scopes, price ladders, and refresh cadences.

By restricting the scope to assets that truly digitize intralogistics and by refreshing annually, we give decision-makers a stable starting point.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 2.32 B (2025) | Mordor Intelligence | - |

| USD 25.30 B (2024) | Global Consultancy A | Counts traditional WMS plus building retrofits, inflating base value |

| USD 31.21 B (2025) | Global Consultancy B | Aggregates entire logistics IT stack and applies low 8 % CAGR without primary validation |

Taken together, the comparison shows that once scope creep and limited field checks are stripped away, Mordor Intelligence delivers a balanced, transparent baseline that executives can rely on when sizing investments and benchmarking growth plans.

Key Questions Answered in the Report

What is the current size of the smart warehousing market?

The smart warehousing market is valued at USD 3.05 billion in 2026.

How fast is the smart warehousing market growing?

It is forecast to expand at a 31.55% CAGR, reaching USD 12.02 billion by 2031.

Which region leads the smart warehousing market?

North America holds the largest revenue share at 33.40% due to early automation adoption and supportive funding programs.

Which technology segment is growing the fastest?

Autonomous mobile robots and drones are projected to grow at a 23.4% CAGR between 2026-2031.

Why is healthcare the fastest-growing end-user?

Stringent regulatory mandates, temperature-controlled storage needs, and traceability requirements drive a 20.7% CAGR in healthcare and pharmaceutical warehouses.

What is the main barrier for smaller companies adopting smart warehousing?

High upfront capital expenditure remains the top obstacle, especially for small and medium-sized enterprises, though robotics-as-a-service models are easing that burden.

Page last updated on: