Smart Pills Boxes And Bottles Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 217.25 Million |

| Market Size (2031) | USD 350.15 Million |

| Growth Rate (2026 - 2031) | 10.02% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Smart Pills Boxes And Bottles Market Analysis by Mordor Intelligence

The Smart Pills Boxes And Bottles Market size is expected to grow from USD 201.12 million in 2025 to USD 217.25 million in 2026 and is forecast to reach USD 350.15 million by 2031 at 10.02% CAGR over 2026-2031.

Sustained growth rests on three structural shifts: payers now link reimbursement to real-time adherence data, chronic disease prevalence keeps climbing, and connected packaging lowers the cost of measuring dose-by-dose compliance. Device shipments rose after U.S. Medicare Advantage plans began subsidizing Bluetooth pill boxes, while Germany’s 2025 digital health law added smart dispensers to reimbursable “digital health applications.” Clinical-trial sponsors also accelerated demand, embracing cellular-enabled bottles that verify investigational-drug intake without patient smartphones. Vendors are responding with lower-cost NFC blister packs, predictive analytics that flag likely non-adherence, and battery-saving chips that meet European e-waste rules. Supply-chain fragility has eased since 2025 as new semiconductor fabs have come online; yet, long-term growth still hinges on interoperable data platforms that satisfy GDPR and HIPAA requirements.

Key Report Takeaways

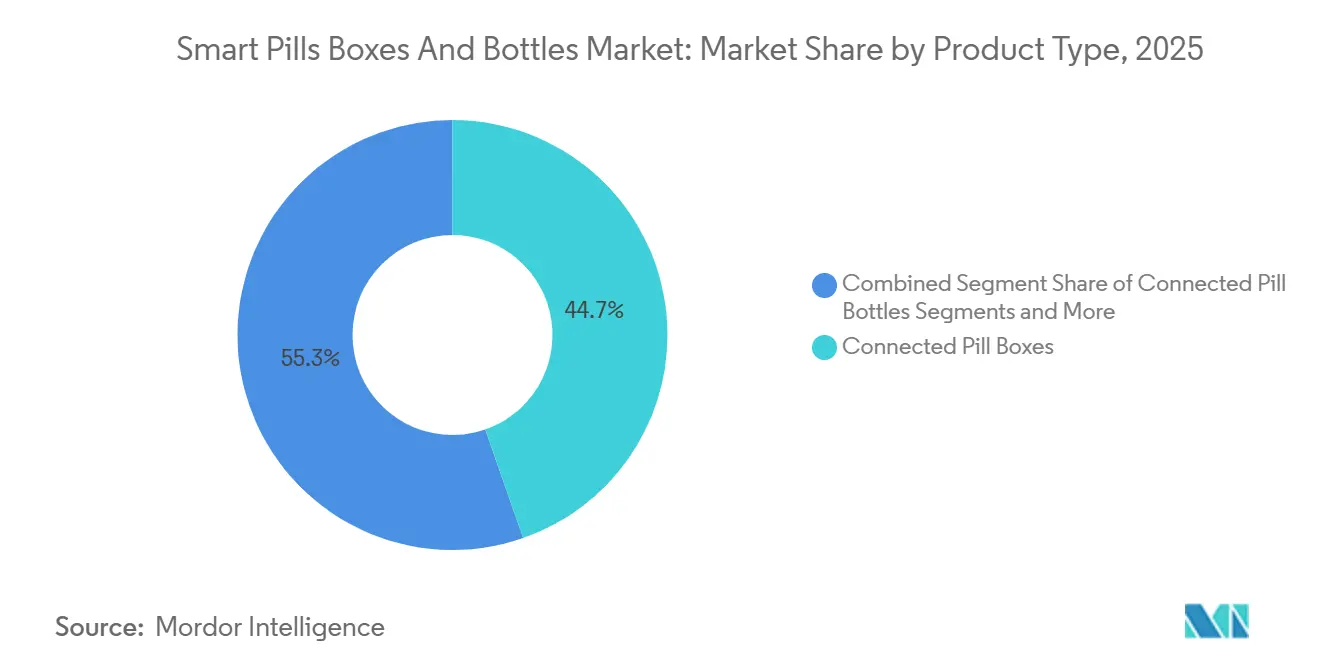

- By product type, connected pill boxes held 44.67% revenue share in 2025; smart blister packs are projected to expand at an 8.26% CAGR through 2031.

- By connectivity, Bluetooth Low-Energy commanded 53.26% of the smart pill boxes and bottles market share in 2025, while cellular and NB-IoT recorded the highest projected CAGR at 7.23% through 2031.

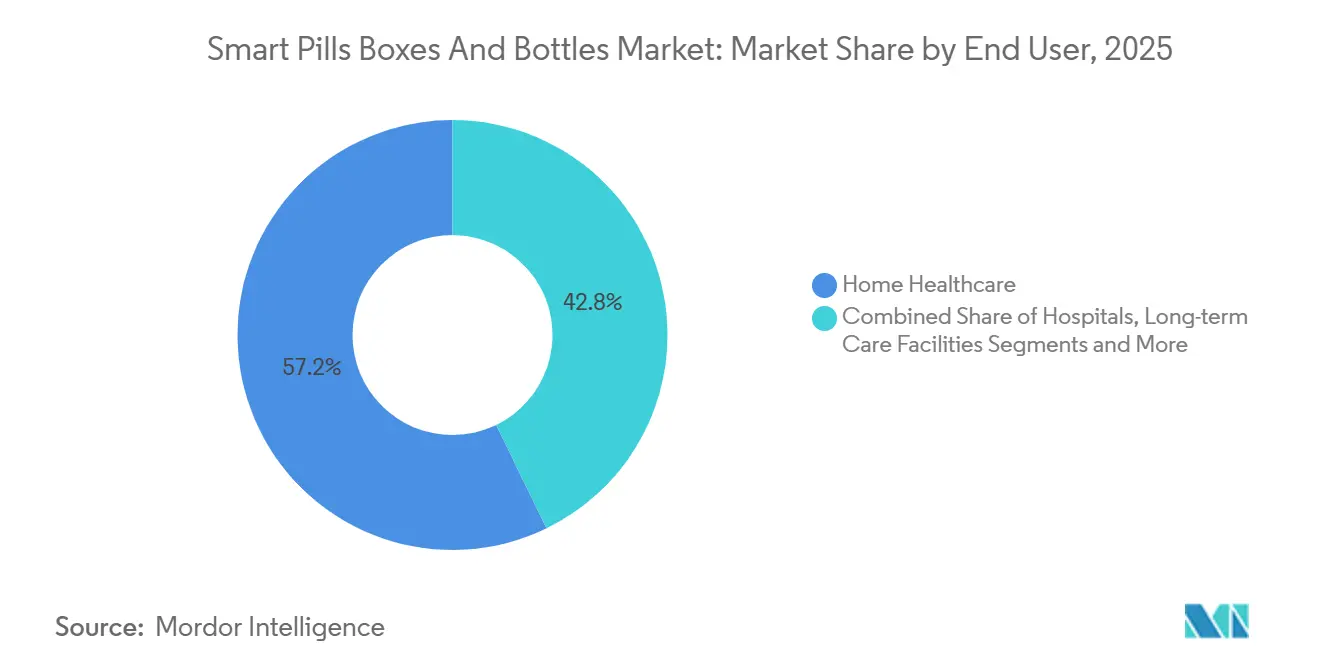

- By end user, home healthcare captured 57.21% of the smart pill boxes and bottles market size in 2025, and clinical-trial sponsors are advancing at an 8.66% CAGR through 2031.

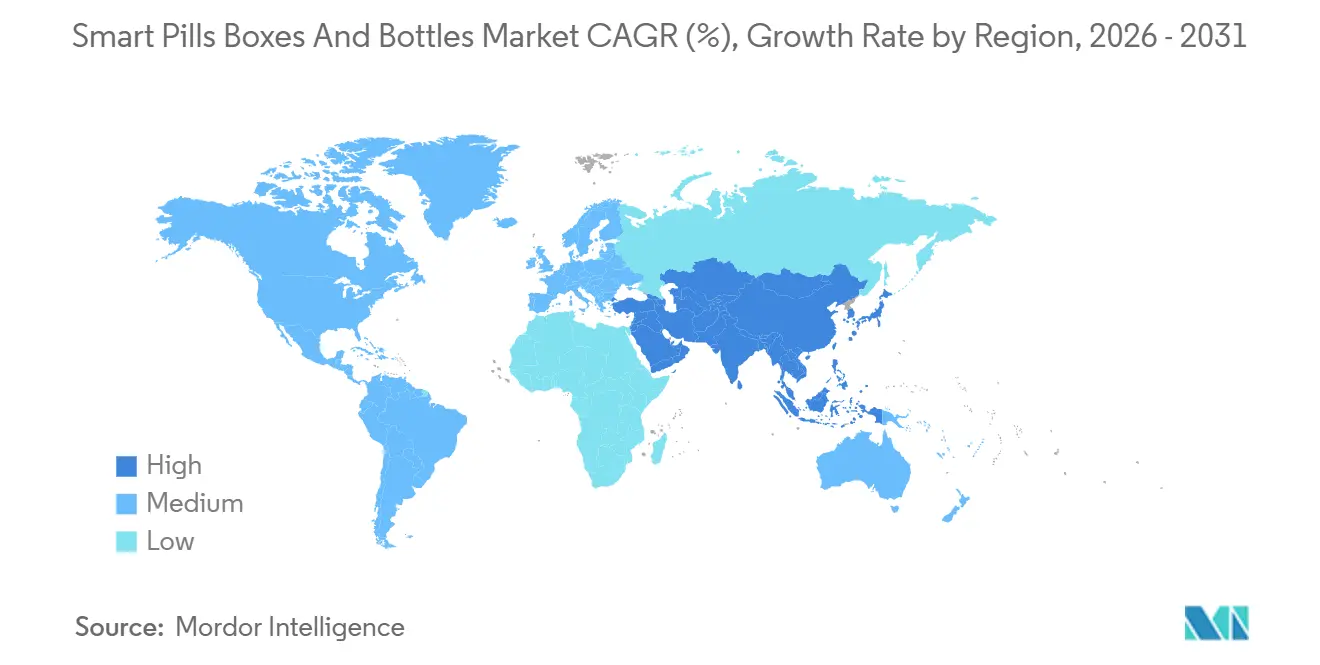

- By geography, North America led with 36.52% revenue share in 2025; Asia-Pacific is set to grow at a 6.34% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Smart Pills Boxes And Bottles Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rapid rise in chronic disease prevalence & poly-pharmacy | +2.1% | Global, with highest intensity in North America, Europe, and high-income Asia-Pacific | Long term (≥ 4 years) |

| Push by payers for medication-adherence linked reimbursements | +1.8% | North America and Western Europe, early pilots in Australia | Medium term (2-4 years) |

| Integration of smart packaging into digital therapeutics ecosystems (DTx) | +1.5% | North America and EU, with regulatory pathways opening in Japan and South Korea | Medium term (2-4 years) |

| Ageing population in high-income Asia driving home-care tech uptake | +1.3% | Japan, South Korea, Singapore, urban China | Long term (≥ 4 years) |

| Smart blister refill programs from e-pharmacies | +1.2% | North America, UK, Germany, emerging in India and Brazil | Short term (≤ 2 years) |

| Emergence of "track-and-trace as a service" for clinical trials | +1.1% | Global, led by United States, EU, and contract research hubs in Eastern Europe and Asia | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rapid Rise in Chronic Disease Prevalence and Poly-Pharmacy

Non-communicable diseases now account for 74% of global deaths, and 40% of adults over 65 in high-income countries take five or more medications daily.[1]World Health Organization, “Noncommunicable Diseases Fact Sheet,” WHO, who.int Each added drug increases missed-dose risk by 12%, a gap that connected pill boxes close through time-stamped reminders reviewed during telehealth visits.[2]European Medicines Agency, “EMA Regulatory Science to 2025 — Strategic Reflection,” EMA, ema.europa.eu U.S. payers spend USD 300 billion annually on avoidable hospitalizations tied to non-adherence, so Medicare Advantage plans subsidize devices for high-risk enrollees. Oncology regimens with narrow therapeutic windows intensify the need for real-time dosing logs. These forces keep the smart pills boxes and bottles market on a durable upward path.

Push by Payers for Medication-Adherence-Linked Reimbursements

The U.S. CMS 2024 rule lets Part D plans count digital adherence endpoints, and some European insurers now offer 5%–10% premium discounts for members who share certified device data. Specialty drugs exceeding USD 50,000 per patient gain higher net revenue when adherence tops 80%, so manufacturers bundle smart bottles to strengthen formulary bids. A Philips pilot showed 87% adherence with connected bottles versus 62% for standard packaging, supporting payer ROI arguments. EMA draft guidance in 2025 allows smart-device data as secondary endpoints in post-marketing studies.[3]Lisa Rosenbaum and William H. Shrank, “Taking Our Medicine — Improving Adherence in the Accountability Era,” New England Journal of Medicine, nejm.org

Integration of Smart Packaging into Digital Therapeutics Ecosystems

FDA cleared 37 software-based therapeutics in 2024, many requiring hardware proof of medication use. Germany’s BfArM reimbursed 12 digital health apps in 2025, four bundled with pill dispensers. Novartis and Roche each partnered with connected-device vendors for oral oncology portfolios, indicating that smart packaging is becoming mandatory within broader digital-health offerings.

Ageing Population in High-Income Asia Driving Home-Care Tech Uptake

Japan subsidizes smart dispensers for residents over 75, affecting 8 million potential users. South Korea earmarked KRW 140 billion to deploy connected health devices in 500,000 households by 2027. China’s provincial insurers reimburse pill boxes for chronic-care patients, while Singapore pilots cut medication-related emergency visits by 34%. These programs aim to avert costly hospitalizations and will intensify demand as the 75-plus cohort expands 40% between 2025 and 2035.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Data-privacy compliance costs (GDPR/HIPAA) | -0.9% | EU and North America, with spillover to countries adopting similar frameworks | Medium term (2-4 years) |

| Low margins in retail pharmacy channel | -0.7% | Global, most acute in North America and Western Europe | Short term (≤ 2 years) |

| Battery-life and electronic waste concerns | -0.6% | Global, with regulatory scrutiny highest in EU under WEEE Directive | Long term (≥ 4 years) |

| IC shortages delaying IoT component supply | -0.5% | Global, with most severe impact in 2024-2025, easing by 2027 | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Data-Privacy Compliance Costs Under GDPR and HIPAA

Digital-health companies spend about USD 520,000 a year on audits, data-protection officers, and breach insurance, a fixed cost that weighs on startups. EU regulators issued EUR 1.2 billion in fines across health tech during 2025. Vendors must maintain parallel systems for FDA’s MyStudies and Europe’s Health Data Space, slowing multi-region roll-outs.

Low Margins in the Retail Pharmacy Channel

Independent U.S. pharmacies earn 2%–4% net profit, so they would need to charge USD 40–60 per device to break even, exceeding typical willingness to pay. Chain pilots remain confined to high-value chronic patients, under 5% of prescription volume. Germany allows EUR 15 monthly billing for digital adherence counseling, but payer uptake is slow, limiting channel growth.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Blister Packs Accelerate on E-Pharmacy Momentum

Connected pill boxes generated 44.67% of 2025 revenue, yet smart blister packs are projected to grow at an 8.26% CAGR as e-pharmacy subscriptions scale. Pre-filled packs with embedded NFC tags reduce patient effort and enable pharmacies to trigger auto-refills five days before depletion. Smart blister pricing of EUR 3–5 per unit undercuts the USD 40–80 reusable pill box, enabling payer-subsidized roll-outs. Automatic dispensers serve long-term care facilities with carousel rotation that prevents double-dosing. In 2024, FDA draft guidance proposed a new “medication adherence system” classification, which is likely to shorten 510(k) timelines and favor integrated blister solutions. Europe’s MDR now requires outcome evidence, so vendors with real-world adherence data gain a head start. The smart pills boxes and bottles market will therefore shift toward disposable, pre-filled formats as e-pharmacies expand.

By Connectivity Technology: Cellular Gains Ground in Decentralized Trials

Bluetooth Low-Energy held a 53.26% share in 2025 thanks to low power draw and native smartphone pairing, but its reliance on patient devices leaves data gaps. Cellular and NB-IoT modules, forecast to grow at 7.23% annually, transmit dose logs directly to the cloud and satisfy trial sponsors that need uninterrupted data. GSMA reported NB-IoT modules fell below USD 5 in 2025, tipping cost-benefit calculus toward embedded SIM designs. Wi-Fi dispensers cover home-care agencies that install broadband hubs, while NFC blister packs deliver the lowest tag cost but require active patient scanning. FDA decentralized-trial guidance endorses cellular devices as a preferred real-time capture method, so connectivity mix will bifurcate: BLE remains dominant in consumer retail, while cellular wins institutional deployments.

By End User: Clinical Trial Sponsors Drive Fastest Adoption

Home healthcare accounts for 57.21% of demand, as agencies seek higher Medicare scores and reduced caregiver burden. Hospitals deploy devices in discharge kits to curb readmissions during the vulnerable transition period. Long-term care facilities rely on automatic dispensers for regulatory compliance. Clinical-trial sponsors, though smaller in volume, are projected to grow at an 8.66% CAGR, fueled by remote studies that need objective adherence logs. NIH data shows 34% of 2025 trials include remote monitoring, and connected devices lift evaluable-patient rates to 91%. Sponsors expense per-patient fees as trial costs, so adoption is less price-sensitive than in consumer channels.

By Distribution Channel: Online Pharmacies Reshape Fulfillment Models

Retail pharmacies held 39.63% share in 2025 but face margin pressure and unclear reimbursement. Online pharmacies are projected to grow at 7.89% annually by bundling smart blister subscriptions at USD 15 per month, boosting retention and lifetime value. Hospital pharmacies focus on discharge and specialty-drug programs, while direct-to-consumer subscriptions attract tech-savvy patients willing to pay for convenience. DEA policy now permits Schedule II drugs in tamper-evident connected packs, expanding prescription scope by roughly 15%. Europe considers a unified e-pharmacy framework, which could unlock cross-border scale.

Geography Analysis

North America captured 36.52% of 2025 revenue, propelled by Medicare subsidies and FDA’s clear 510(k) pathway. Roughly 4.2 million Medicare Advantage members used connected devices by mid-2025. Canada’s Ontario pilot hints at broader provincial adoption, while Mexican private insurers begin offering smart boxes as differentiators. High smartphone penetration and mature e-pharmacy infrastructure further accelerate growth.

Asia-Pacific is forecast to grow at a 6.34% CAGR, the strongest regional rate. Japan subsidizes devices for patients managing five or more medications, South Korea’s Silver Tech program deploys 500,000 units by 2027, and China’s provincial schemes reimburse pill boxes for chronic conditions. Australia’s Pharmaceutical Benefits Scheme covers up to AUD 100 per patient annually for digital adherence support, stimulating general-practitioner uptake. India and Southeast Asia remain nascent but show traction in urban private hospitals.

Germany’s statutory insurers reimburse devices for chronic patients who meet adherence thresholds, France approved three connected devices for oncology and anticoagulation, and the UK cut medication-related admissions by 19% during NHS pilots. Southern and Eastern Europe lag, but Catalonia’s diabetic pilot signals momentum. Middle East, Africa, and South America together account for under 10% of revenue, with Brazil and South Africa leading regional pilots.

Competitive Landscape

The smart pills boxes and bottles market is moderately fragmented. BD and Philips leverage global hospital relationships and regulatory expertise, while Hero Health, AdhereTech, and Pillsy compete on user experience and subscription models. Baxter integrates connected bottles into its DoseEdge workflow, extending adherence tracking from inpatient to outpatient settings. Philips patented a multi-device aggregation platform in 2024, aiming to satisfy payer demand for unified dashboards. CRO partnerships allow smaller firms to bundle hardware and analytics for decentralized trials. Predictive analytics that forecast non-adherence before it happens now differentiate top vendors, since large datasets and AI talent raise entry barriers.

Smart Pills Boxes And Bottles Industry Leaders

Koninklijke Philips N.V.

MedMinder Systems

AdhereTech Inc.

Spencer Health Solutions

Hero Health Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- September 2025: PillSafe opened a SAFE investment round ahead of its 2026 commercial launch, promising secure prescription delivery from pharmacy to medicine cabinet.

- July 2025: Pillbox Health added a Remote Therapeutic Monitoring feature to its PillPal app, enabling pharmacies and caregivers to raise adherence and generate new revenue.

- April 2025: Centor, a Gerresheimer company, introduced a connected weekly pill organizer that records real-time intake and supports pharmacies and clinical partners with simple therapy support.

Global Smart Pills Boxes And Bottles Market Report Scope

As per the scope of the report, the smart pill boxes and bottles are focused on patients who frequently take medications or on attendants who deal with the more seasoned patients. These smart pill boxes and bottles are programmable and enable medical caretakers or clients to determine the pill amount and timing to take pills, as well as the service times for every day.

The Smart Pills Boxes and Bottles Market is Segmented by Product Type, connectivity technology, end user, distribution channel, and geography. By Product Type, market is segmented into Connected Pill Boxes, Connected Pill Bottles, Automatic Pill Dispensers, Smart Blister Packs. By Connectivity Technology, the market is segmented into Bluetooth Low-Energy, Wi-Fi, Cellular/NB-IoT, and NFC. By Distribution Channel, the market is segmented into Retail Pharmacies, Online Pharmacies, Hospital & Clinic Pharmacies, and Direct-to-Consumer Subscriptions. By End User, the market is segmented into Home Healthcare, Hospitals, Long-term Care Facilities, Clinical Trial Sponsors, and By Geography, the market is segmented into North America, Europe, Asia-Pacific, the Middle East & Africa, and South America. The market report also covers the estimated market sizes and trends for 17 different countries across major regions globally. The report offers the value (in USD) for the above segments.

| Connected Pill Boxes |

| Connected Pill Bottles |

| Automatic Pill Dispensers |

| Smart Blister Packs |

| Bluetooth Low-Energy (BLE) |

| Wi-Fi |

| Cellular / NB-IoT |

| Near-Field Communication (NFC) |

| Retail Pharmacies |

| Online Pharmacies |

| Hospital & Clinic Pharmacies |

| Direct-to-Consumer Subscriptions |

| Home Healthcare |

| Hospitals |

| Long-term Care Facilities |

| Clinical Trial Sponsors |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| France | |

| United Kingdom | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| South Korea | |

| Australia | |

| Rest of Asia-Pacific | |

| Middle East & Africa | GCC |

| South Africa | |

| Rest of Middle East & Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Product Type | Connected Pill Boxes | |

| Connected Pill Bottles | ||

| Automatic Pill Dispensers | ||

| Smart Blister Packs | ||

| By Connectivity Technology | Bluetooth Low-Energy (BLE) | |

| Wi-Fi | ||

| Cellular / NB-IoT | ||

| Near-Field Communication (NFC) | ||

| By Distribution Channel | Retail Pharmacies | |

| Online Pharmacies | ||

| Hospital & Clinic Pharmacies | ||

| Direct-to-Consumer Subscriptions | ||

| By End User | Home Healthcare | |

| Hospitals | ||

| Long-term Care Facilities | ||

| Clinical Trial Sponsors | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| France | ||

| United Kingdom | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| Middle East & Africa | GCC | |

| South Africa | ||

| Rest of Middle East & Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

What is the current value of the smart pills boxes and bottles market?

The market is valued at USD 217.25 million in 2026 and is projected to reach USD 350.15 million by 2031.

Which product type is growing fastest?

Smart blister packs are the fastest-growing product, expanding at an 8.26% CAGR through 2031.

Why are clinical-trial sponsors adopting connected pill bottles?

Cellular-enabled bottles provide real-time adherence data that reduces protocol deviations and strengthens regulatory submissions.

How does Bluetooth compare with cellular connectivity in these devices?

Bluetooth dominates consumer use due to low cost and smartphone pairing, while cellular connectivity wins institutional deployments that need independent cloud uploads.

Which region shows the highest growth potential?

Asia-Pacific leads in growth with a forecast CAGR of 6.34% through 2031, driven by aging populations and government subsidies for home-care technology.

What is the main regulatory hurdle for vendors?

Complying with GDPR and HIPAA data-privacy rules, which together add roughly USD 520,000 in annual compliance costs for dual-region operations.

Page last updated on: