Market Overview

| Study Period | 2020 - 2031 |

|---|---|

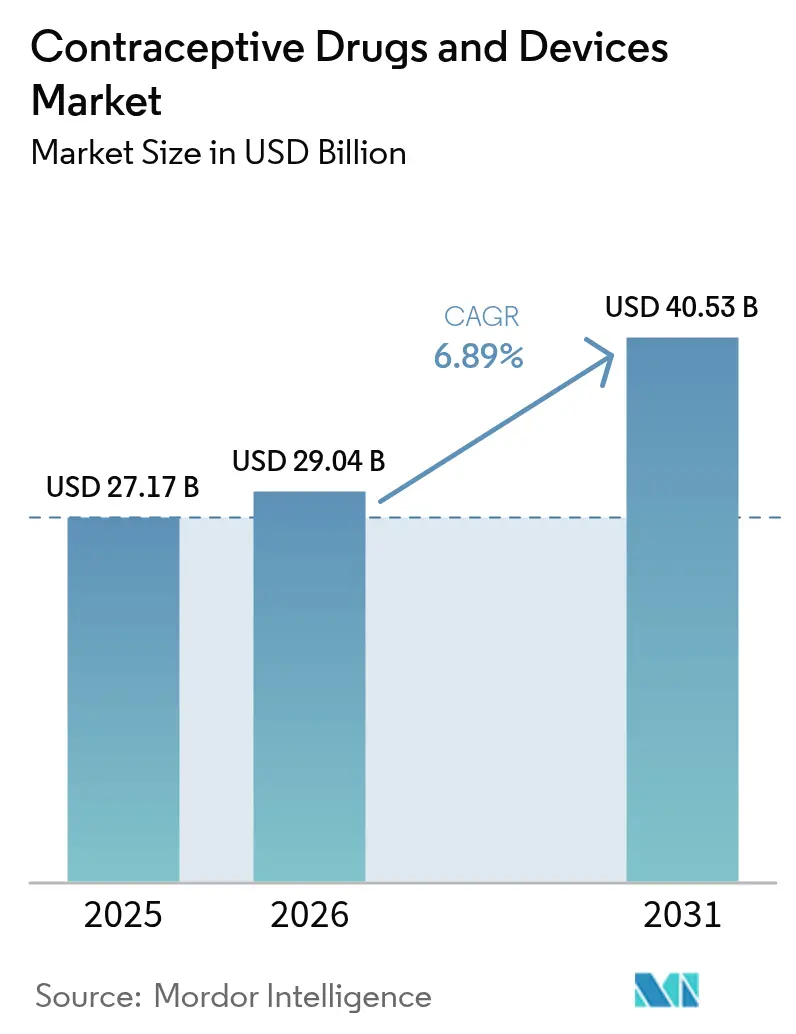

| Market Size (2026) | USD 29.04 Billion |

| Market Size (2031) | USD 40.53 Billion |

| Growth Rate (2026 - 2031) | 6.89% CAGR |

| Fastest Growing Market | Middle East and Africa |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Contraceptive Drugs And Devices Market Analysis by Mordor Intelligence

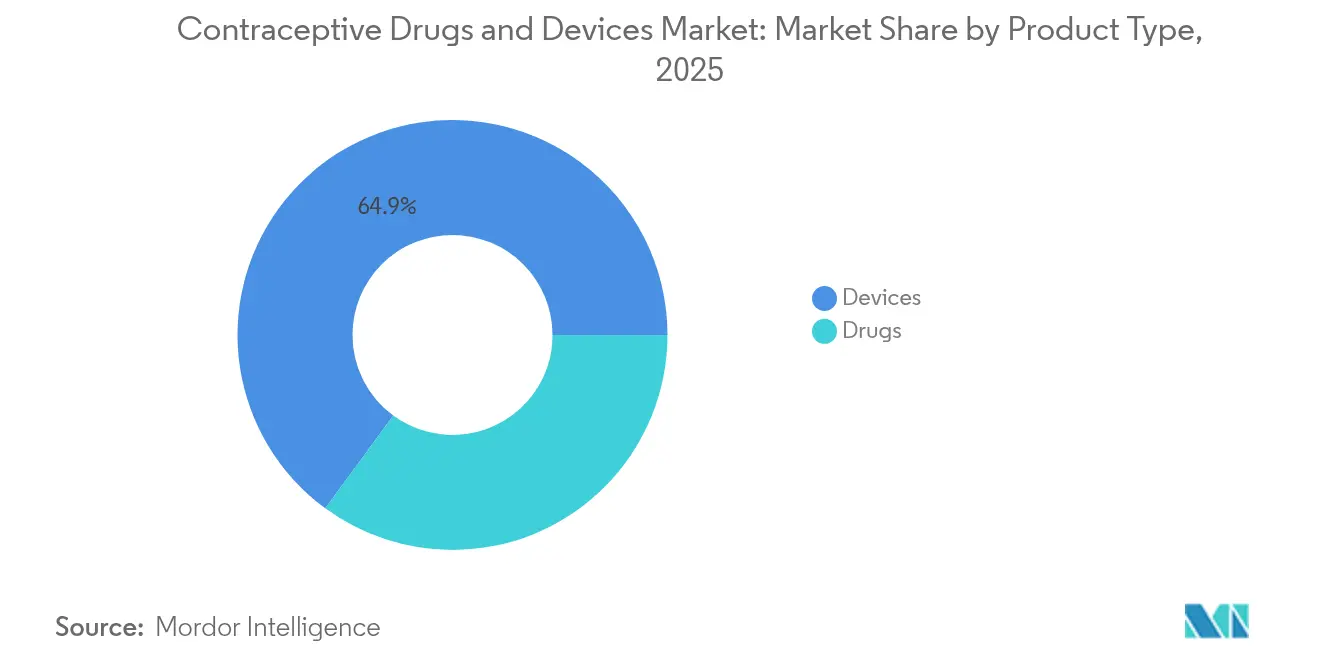

The contraceptive drugs and devices market size is expected to grow from USD 27.17 billion in 2025 to USD 29.04 billion in 2026 and is forecast to reach USD 40.53 billion by 2031 at 6.89% CAGR over 2026-2031. Growth is underpinned by sustained investment in long-acting reversible contraceptives (LARCs), rising demand for non-hormonal methods, and a steady shift toward digital purchasing channels that reduce access barriers. Asia-Pacific accounted for 33.33% of 2024 revenue, buoyed by government family-planning programs, while the Middle East & Africa is on track for the fastest expansion at 8.67% CAGR on the back of new reimbursement schemes that temper cultural resistance.[1]United Nations Population Fund, “UNFPA Supplies Performance Measurement Report 2023,” UNFPA, unfpa.org Devices captured 65.34% of 2024 sales and are tracking an 8.2% yearly gain as implants and hormonal intrauterine devices deliver >99% effectiveness with limited user input. Online distribution, expanding 9.78% per year, is reshaping procurement by pairing telehealth consultations with direct-to-consumer logistics.

Key Report Takeaways

- By product type, devices led with 64.92% revenue share in 2025, while the drugs is advancing at an 7.03% CAGR through 2031.

- By hormonal class, hormonal methods held 60.75% of the contraceptive drugs and devices market share in 2025; non-hormonal options are projected to expand at an 8.61% CAGR to 2031.

- By gender, female-focused products dominated with 79.86% share in 2025, whereas male solutions posted the highest projected CAGR at 7.98% through 2031.

- By age group, 25-34 year-olds accounted for 35.92% of the market in 2025; the 15-24 cohort is on course for a 7.67% CAGR to 2031.

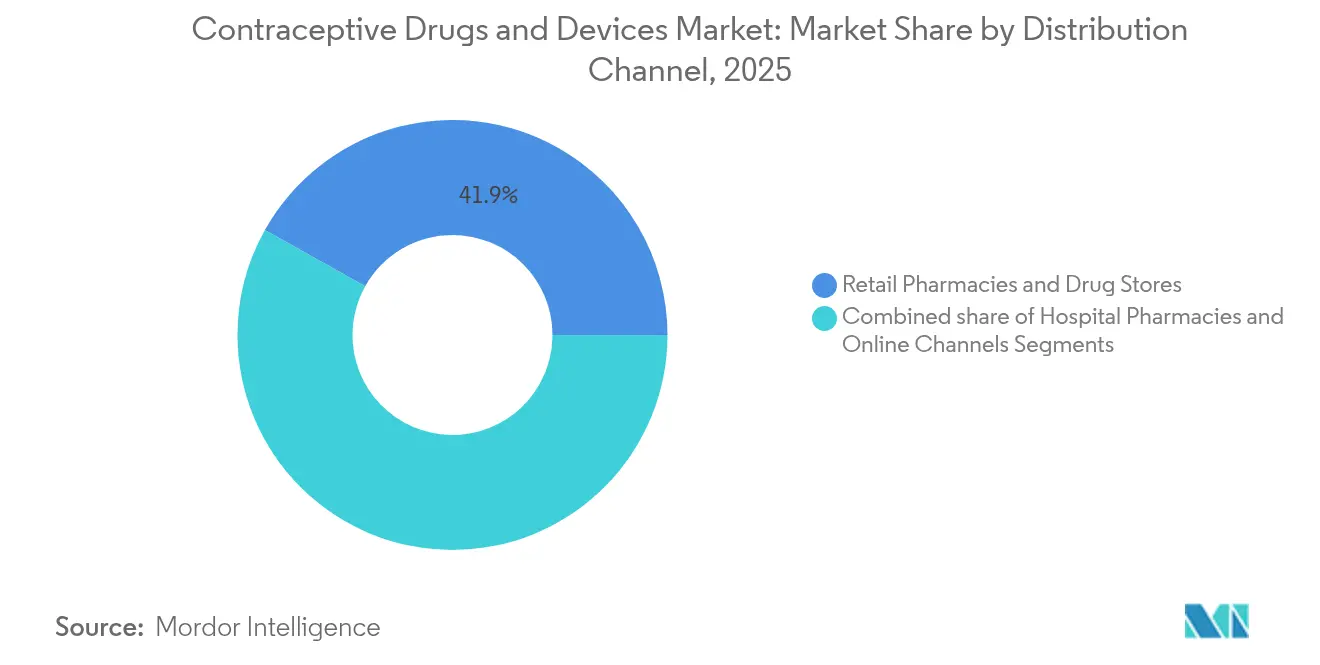

- By distribution channel, retail pharmacies controlled 41.88% of 2025 revenue, but online platforms are climbing at a 9.56% CAGR to 2031.

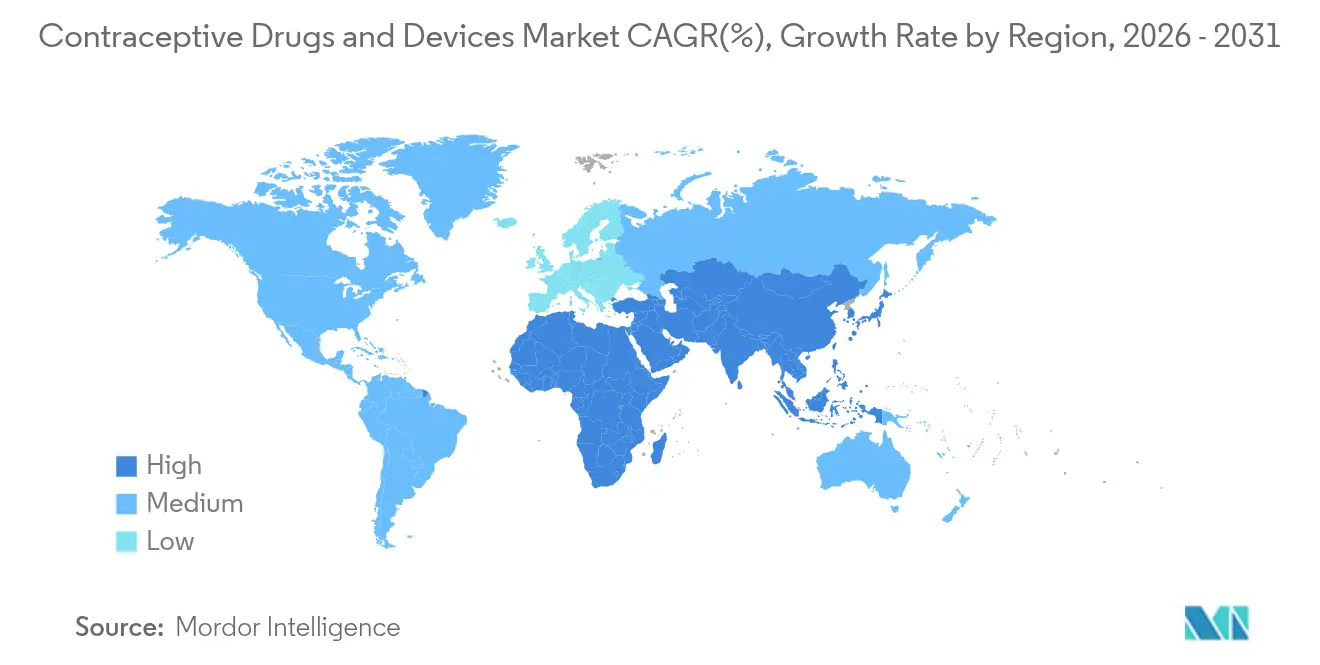

- By geography, Asia-Pacific held the largest 33.05% share in 2025, while the Middle East and Africa is projected to grow fastest at 8.54% CAGR between 2026-2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Contraceptive Drugs And Devices Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising uptake of LARCs | +2.1% | North America, Europe, Global | Medium term (2-4 years) |

| Expansion of reimbursement & awareness | +1.7% | Asia-Pacific, Middle East & Africa, Global | Medium term (2-4 years) |

| Technological advancement & innovation pipeline | +1.5% | North America, Europe, Global | Long term (≥ 4 years) |

| Shift to e-commerce for OTC barrier products | +0.9% | Developed regions, Global | Short term (≤ 2 years) |

| Rising awareness of family planning | +0.6% | Developing regions, Global | Medium term (2-4 years) |

| Rising global population & unintended pregnancy | +0.8% | Asia-Pacific, Africa, Global | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising Uptake of Long Acting Reversible Contraceptives

LARCs offer over 99% effectiveness and significantly reduce user error, making them the first-line recommendation among clinicians. Policy shifts such as separate Medicaid reimbursement for immediate postpartum placement lifted utilization by 0.74 percentage points.[2]Journal of Adolescent Health, “Study on Contraceptive Satisfaction Among Youth,” Journal of Adolescent Health, jahonline.org Innovation surrounding biodegradable implants in Phase 1 trials aims to eliminate the need for removal procedures. Cost savings accrue to payers as even modest migration from short-acting pills to LARCs lowers unintended pregnancy rates, strengthening payer support. Together, these dynamics keep the contraceptive drugs and devices market on a structurally higher growth path.

Expansion of Reimbursement Initiatives Coupled with Access and Awareness Programs

A USD 390 million U.S. Title X budget for 2025—up 36%—broadens subsidized access for low-income users. Fourteen other governments maintained or grew allocations, totaling USD 35.3 million.[1]United Nations Population Fund, “UNFPA Supplies Performance Measurement Report 2023,” UNFPA, unfpa.org British Columbia’s province-wide free-contraception policy demonstrates the volume lift that occurs when cost barriers are removed, although legacy providers must recalibrate their revenue models. Digital partnerships—such as Bayer’s collaborations with Your Life and UNFPA India—blend education and fulfillment, deepening penetration in low- and middle-income countries. These initiatives collectively raise modern‐method prevalence and sustain the contraceptive drugs and devices market expansion.

Technological Advancement and Innovation Pipeline

The NIH committed USD 420 million to contraceptive R&D for 2024-2025, earmarking nearly one-third of the funds for male solutions. WHO estimates that broadening the method mix could raise global contraceptive prevalence by eight percentage points by 2030.[3]World Health Organization, “Sexual and Reproductive Health for All,” who.int Next-generation formats range from microneedle patches and six-month injectables to dual-prevention pills that combine pregnancy and HIV protection. Casea S, a biodegradable implant, and Ovaprene, a hormone-free intravaginal ring in Phase 3 trials, illustrate how non-hormonal design addresses the side-effect gap. These pipelines diversify choice and reinforce long-term momentum in the contraceptive drugs and devices market.

Shift to E-commerce for OTC Barrier Products

Barrier products are increasingly purchased online, driving segment growth at a 10.20% CAGR. Telecontraception merges web-based consultations with doorstep delivery, expanding access, particularly in rural areas. Yet counterfeit risk is material; FDA seizures of fake contraceptives rose 43% in 2024. Platforms are responding with authentication technology and pharmacist chat features to safeguard users. Overall, digital channels complement brick-and-mortar outlets, widening the footprint of the contraceptive drugs and devices market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Cultural-religious barrier in contraceptive adoption | –0.8% | Middle East & Africa, parts of Asia-Pacific & Latin America | Long term (≥ 4 years) |

| Side effects and perceived risk factors | –0.5% | Global | Medium term (2-4 years) |

| Regulatory issues & counterfeit proliferation | –0.3% | Developing regions, Global | Medium term (2-4 years) |

| High upfront device cost & limited rural access | –0.4% | Developing regions, rural areas | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Cultural-Religious Barrier in Adoption of Contraceptives

Religious objections account for 37% of non-use in Saudi Arabia, 42% in Nigeria, and 28% in Pakistan. Countries with strong faith influence post contraceptive prevalence rates 18 points lower than peers of similar income. Policy examples, such as Indiana’s Medicaid restrictions on IUDs, illustrate the institutionalization of such barriers. Province-level disparities in Mozambique underline localized nuance contraceptionmedicine.biomedcentral.com. Manufacturers increasingly engage religious leaders and deploy community outreach to soften resistance and protect the contraceptive drugs and devices market trajectory.

Regulatory Issues and Proliferation of Counterfeit Products

Thirty-nine percent of seized counterfeit medicines in 2024 were contraceptives, underscoring quality risks in informal channels. Regulatory divergence creates complexity: while 29 U.S. jurisdictions now allow pharmacist prescribing, other regions still mandate physician visits, slowing adoption. Harmonizing standards and boosting post-market surveillance remain industry priorities.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Devices Dominate Through Efficacy Advantage

Devices held 64.92% of 2025 revenue, giving them the largest contraceptive drugs and devices market share, thanks to the more than 99% effectiveness of IUDs and implants. The category is growing at a rate of 6.15% annually, as biodegradable implants and extended-duration hormonal IUDs boost uptake. Hormonal IUDs also treat heavy bleeding, adding clinical appeal. Emerging non-hormonal devices like Ovaprene aim to address the side-effect-conscious segment.

Drug-based products represented the remaining 35.08% in 2025, but are expected to experience faster growth. The contraceptive drugs and devices market size for emergency pills is nevertheless expanding in markets where awareness of the 72-hour window rises. FDA clearance of Opill for OTC sale in March 2024 removes prescription friction and could revive pill volumes.

By Hormonal Class: Non-Hormonal Methods Gain Momentum

Hormonal methods controlled 60.75% revenue, yet non-hormonal alternatives are expanding 8.61% yearly, far above the total contraceptive drugs and devices market CAGR. Copper IUD demand is also rising as users seek hormone-free choices. Ovaprene’s 86-91% efficacy in early studies suggests a strong commercial outlook.

Lower-dose hormonal innovations seek to mitigate systemic effects while maintaining efficacy. Meanwhile, the Gates Foundation’s USD 280 million annual pledge to non-hormonal R&D underscores investor conviction. This funding influx is expected to expand the contraceptive drugs and devices market size for hormone-free solutions.

By Gender: Male Contraception Emerges as Growth Frontier

Female-focused products accounted for 79.86% of 2025 sales, underpinned by an extensive product mix that included pills, rings, implants, and IUDs. The CE-marked FemBloc system introduces the first non-surgical, permanent option, reinforcing the breadth of innovation.

Male methods, currently at 20.14%, are expanding at an annual rate of 7.98% as societal attitudes shift. Plan A, a reversible hydrogel in Australian trials, and the Galactic Cap are illustrative of the R&D pipeline. A 2025 JAMA survey found 78% of men aged 18-45 were willing to adopt novel contraception, signaling meaningful latent demand.

By Age Group: Youth Segment Drives Future Growth

Consumers aged 25-34 accounted for 35.92% of 2025 spending, aligning with their higher fertility management needs. They are 31% more likely than 15-24 year-olds to adopt modern methods.

The 15-24 cohort, however, is the fastest-growing, with a 7.67% CAGR to 2031. Dissatisfaction with hormonal side effects, cited by 42% in a U.S. study, propels interest in user-friendly non-hormonal options. Telehealth channels resonate strongly with this digital-native segment, expanding awareness and access.

By Distribution Channel: Online Platforms Revolutionize Access

Retail pharmacies maintained a 41.88% share in 2025, spotlighted by pharmacist-prescribed programs in 29 states and D.C. OTC Opill at USD 19.99 per month further strengthens this channel.

Online portals are scaling at 9.56% CAGR, integrating virtual consultations and discreet home delivery. Telehealth contraceptive prescriptions almost doubled between 2023 and 2025, with rural usage surging. Authenticity challenges persist; FDA seizures of counterfeit goods increased by 43% year-over-year, prompting platforms to tighten supply-chain verification.

Geography Analysis

North America benefits from substantial reimbursement, with USD 390 million Title X funding in 2025 and OTC Opill availability that removes prescription hurdles. Nonetheless, initiatives such as Project 2025 threaten to curtail free emergency contraception for 48 million women, creating policy uncertainty.

The Asia-Pacific region holds the most prominent regional position, with a 33.05% share, yet intra-regional disparities persist, only 20.2% of Bangladeshi women wishing to avoid pregnancy use LARCs, highlighting a sizeable runway. Digital distribution and expanded reimbursement are expected to narrow this gap.

The Middle East & Africa’s 8.54% CAGR through 2031 stems from enhanced funding and outreach, such as Zambia’s plan to lift prevalence to 40% by 2026. Youth surveys in Uganda reveal 72.4% intend to use contraception once barriers ease.

Europe’s mature market posts steady growth amid varied method mixes; hormonal usage ranges from 28% in southern to 54% in northern states. EMA approvals of three formulations in 2024 sustain product refresh cycles.

South America registers solid demand where no-cost LARCs drive adherence; Brazil reports 82.1% continuation for LNG IUDs at 24 months, validating public-sector procurement strategies.

Competitive Landscape

Bayer AG leverages the Mirena franchise and pledges contraception access for 100 million women by 2030. Organon & Co. derives 27% of 2022 revenue from Nexplanon and NuvaRing, underscoring its stake in the contraceptive drugs and devices market.

Innovation-centric players gain visibility: Daré Bioscience advances Ovaprene and Casea S, partnering with Theramex to commercialize biodegradable implants. NEXT Life Sciences raised USD 20 million for Plan A, highlighting investor appetite for male solutions. Competitive intensity is rising as incumbents and start-ups jostle to fill unmet needs with differentiated delivery systems, dosage profiles, and gender-balanced portfolios.

Contraceptive Drugs And Devices Industry Leaders

Bayer AG

Teva Pharmaceutical Industries Ltd

Johnson and Johnson

Organon

CooperSurgical Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2025: NEXT Life Sciences began Australian trials of Plan A, a reversible male contraceptive lasting up to 10 years.

- March 2025: Femasys secured CE mark for FemBloc, the first non-surgical permanent birth-control device.

- February 2025: Daré Bioscience and Theramex agreed to co-develop Casea S, an 18-24-month biodegradable implant.

- January 2025: Daré Bioscience highlighted Ovaprene progress at the J.P. Morgan Women’s Health Series.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study defines the contraceptive drugs and devices market as all prescription and over-the-counter pharmaceutical products, oral pills, patches, injectables, emergency pills, and mechanical, implantable, or permanent devices such as condoms, diaphragms, vaginal rings, IUDs, sub-dermal implants, and tubal or vas deferens blockers that are specifically promoted to prevent pregnancy and sold through hospital, retail, and online channels.

Scope Exclusions: Fertility-tracking apps, non-contraceptive hormonal therapies, and surgical abortion equipment lie outside this scope.

Segmentation Overview

- By Product Type

- Drugs

- Oral Pills

- Transdermal Patch

- Injectable Contraceptives

- Emergency Pills

- Devices

- Barrier Devices

- Male Condom

- Female Condom

- Diaphragm

- Cervical Cap

- Contraceptive Sponge

- Long-Acting Reversible

- Hormonal IUD

- Copper IUD

- Sub-dermal Implant

- Vaginal Ring

- Permanent

- Tubal Occlusion Device

- Barrier Devices

- Drugs

- By Hormonal Class

- Hormonal Methods

- Non-Hormonal Methods

- By Gender

- Male

- Female

- By Age Group

- 15-24 Years

- 25-34 Years

- 35-44 Years

- 45+ Years

- By Distribution Channel

- Hospital Pharmacies

- Retail Pharmacies & Drug Stores

- Online Channels

- Geography

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Rest of Europe

- Asia-Pacific

- China

- Japan

- India

- Australia

- South Korea

- Rest of Asia-Pacific

- Middle East and Africa

- GCC

- South Africa

- Rest of Middle East and Africa

- South America

- Brazil

- Argentina

- Rest of South America

- North America

Detailed Research Methodology and Data Validation

Primary Research

Mordor analysts interviewed gynecologists, public-sector family-planning buyers, online-pharmacy category managers, and contract manufacturers across North America, Asia-Pacific, Latin America, and Africa. These discussions clarified uptake barriers, channel volumes, and price dispersion, refining assumptions derived from secondary work.

Desk Research

We drew baseline prevalence and user-cohort data from publicly available sources such as the WHO Family-Planning Dashboard, UN DESA fertility projections, World Bank population indicators, the CDC's National Survey of Family Growth, and Guttmacher Institute briefs. Pricing corridors were checked against UNFPA procurement lists and customs shipment statistics. Corporate filings, investor presentations, and news archives accessed through D&B Hoovers and Dow Jones Factiva supplied revenue bands and unit flows. The sources cited are illustrative; many additional records informed data collection and cross-checks.

Market-Sizing & Forecasting

A single top-down reconstruction multiplies each country's women of reproductive age by modern contraceptive prevalence and method mix, then applies validated average selling prices to arrive at baseline revenue. Supplier roll-ups and sampled ASP × volume checks provide a selective bottom-up overlay for error correction. Key model inputs include GDP per capita, female secondary-school completion, public reimbursement budgets, e-commerce penetration, and long-acting reversible contraceptive share. A multivariate regression projects demand through 2030; missing national statistics are bridged with regionally weighted benchmarks vetted by primary experts.

Data Validation & Update Cycle

Models pass two-tier analyst review, variance thresholds trigger re-contact with original respondents, and outputs are reconciled against external shipment trends before sign-off. Reports refresh yearly, with interim updates for major regulatory or reimbursement shifts.

Why our Contraceptive Drugs and Devices Baseline commands reliability

Published estimates vary because firms adopt different scopes, pricing anchors, and refresh cadences.

According to public sources, 2024 market values range from USD 19.8 billion to USD 31.18 billion.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 27.17 bn (2025) | Mordor Intelligence | - |

| USD 31.18 bn (2024) | Global Consultancy A | Bundles retail condom sales at face value and uses 2023 FX rates |

| USD 19.80 bn (2024) | Trade Journal B | Covers drugs only, omitting IUDs and implants |

The comparison shows how Mordor's clear scope capture, mixed-method validation, and annual recalibration deliver a balanced, transparent baseline that decision-makers can reuse with confidence.

Key Questions Answered in the Report

What is the current size of the contraceptive drugs and devices market?

The market is valued at USD 29.04 billion in 2026 and is projected to reach USD 40.53 billion by 2031.

Which product category leads the market?

Devices dominate with 64.92% revenue share in 2025, driven by the effectiveness and convenience of IUDs and implants.

Why are non-hormonal methods growing faster than hormonal options?

Rising consumer concern over hormonal side effects and expanding R&D investment in hormone-free technologies are propelling a 8.61% CAGR for non-hormonal products.

How is e-commerce changing contraceptive access?

Online channels, growing at 9.56% per year, integrate telehealth consultations with doorstep delivery, expanding reach to rural and privacy-conscious users.

Which region is expanding fastest?

The Middle East & Africa is forecast to grow at 8.54% CAGR between 2026-2031, driven by new reimbursement programs and awareness campaigns.

What innovations are emerging in male contraception?

Pipeline products such as Plan A hydrogel and the Galactic Cap aim to offer reversible, hormone-free male options, with early clinical trials underway.

Page last updated on: