Smart Personal Protective Equipment Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

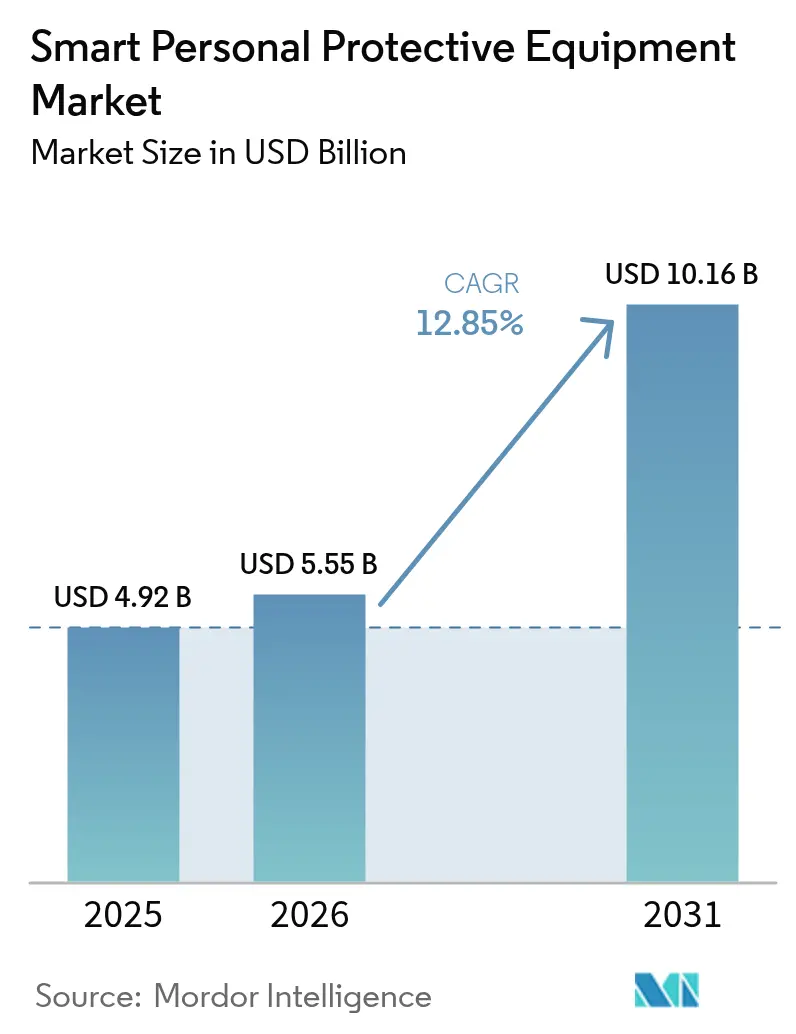

| Market Size (2026) | USD 5.55 Billion |

| Market Size (2031) | USD 10.16 Billion |

| Growth Rate (2026 - 2031) | 12.85% CAGR |

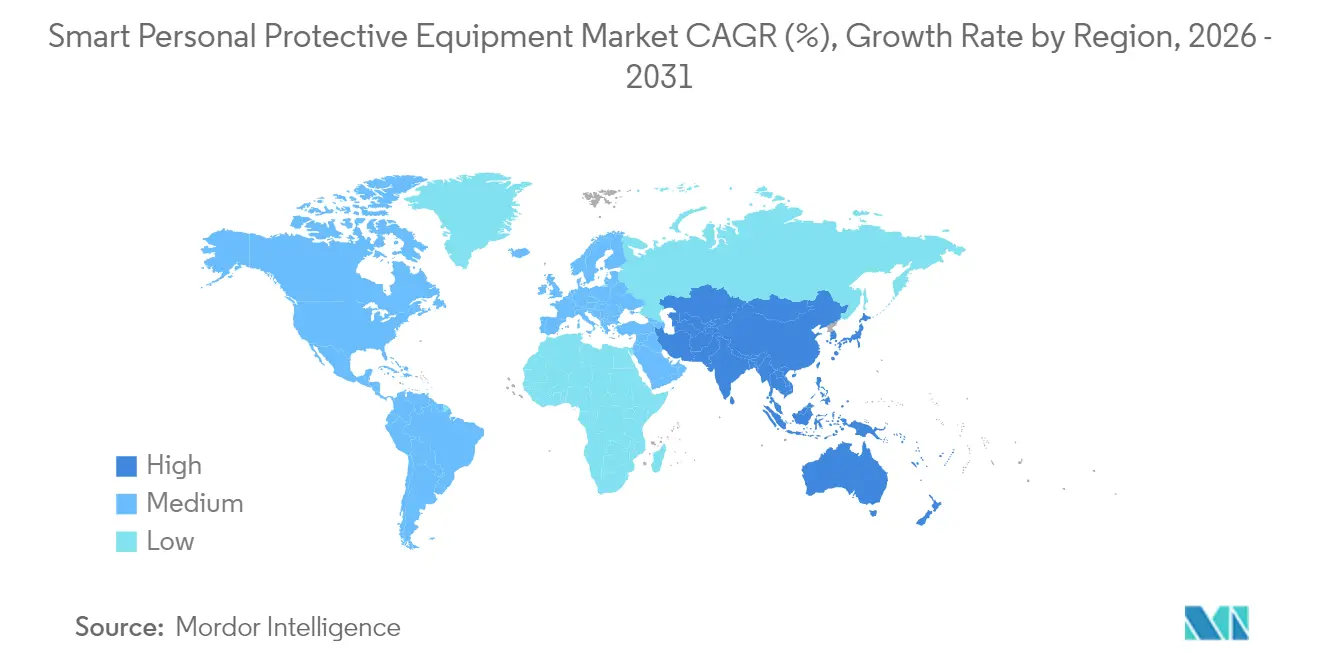

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Smart Personal Protective Equipment Market Analysis by Mordor Intelligence

The smart personal protective equipment market size was valued at USD 4.92 billion in 2025 and estimated to grow from USD 5.55 billion in 2026 to reach USD 10.16 billion by 2031, at a CAGR of 12.85% during the forecast period (2026-2031). Accelerated growth stems from OSHA’s 2025 heat-safety standards, European Union privacy mandates, and expanding Construction 4.0 programs that embed connected monitoring into day-to-day operations. Real-time biometrics, sensor miniaturization, and falling connectivity costs shift procurement decisions from reactive compliance toward proactive productivity gains. Industrial insurers increasingly discount premiums when connected-worker programs are in place, further strengthening the business case for smart PPE adoption. Battery innovations such as textile-integrated fiber cells extend runtime in remote settings, while edge analytics resolve privacy tensions by processing sensitive data on the device rather than in the cloud.

Key Report Takeaways

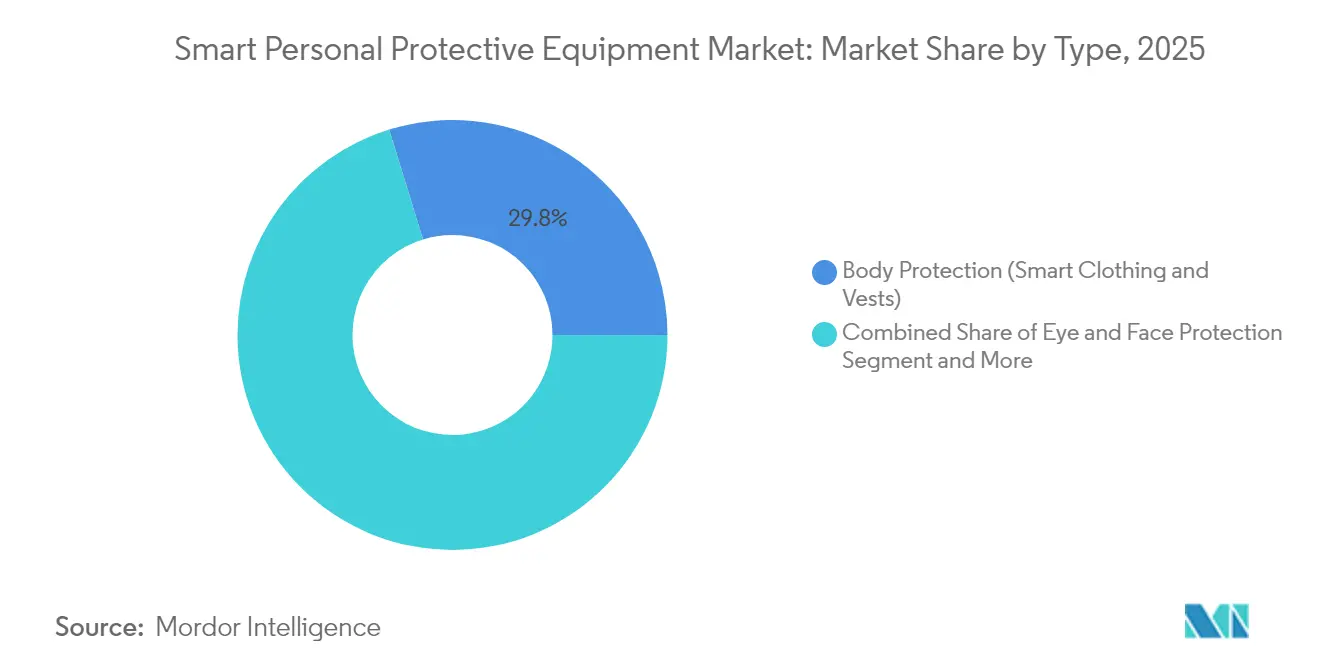

- By type, body protection led with 29.76% of smart personal protective equipment market share in 2025, whereas smart gloves are set to expand at a 14.11% CAGR through 2031.

- By technology, IoT-enabled PPE dominated with 60.85% market share in 2025, while AR/VR smart glasses are forecast to advance at a 13.04% CAGR to 2031.

- By connectivity, Bluetooth Low Energy held 49.12% share of smart personal protective equipment market size in 2025 and cellular solutions are rising at a 13.83% CAGR through 2031.

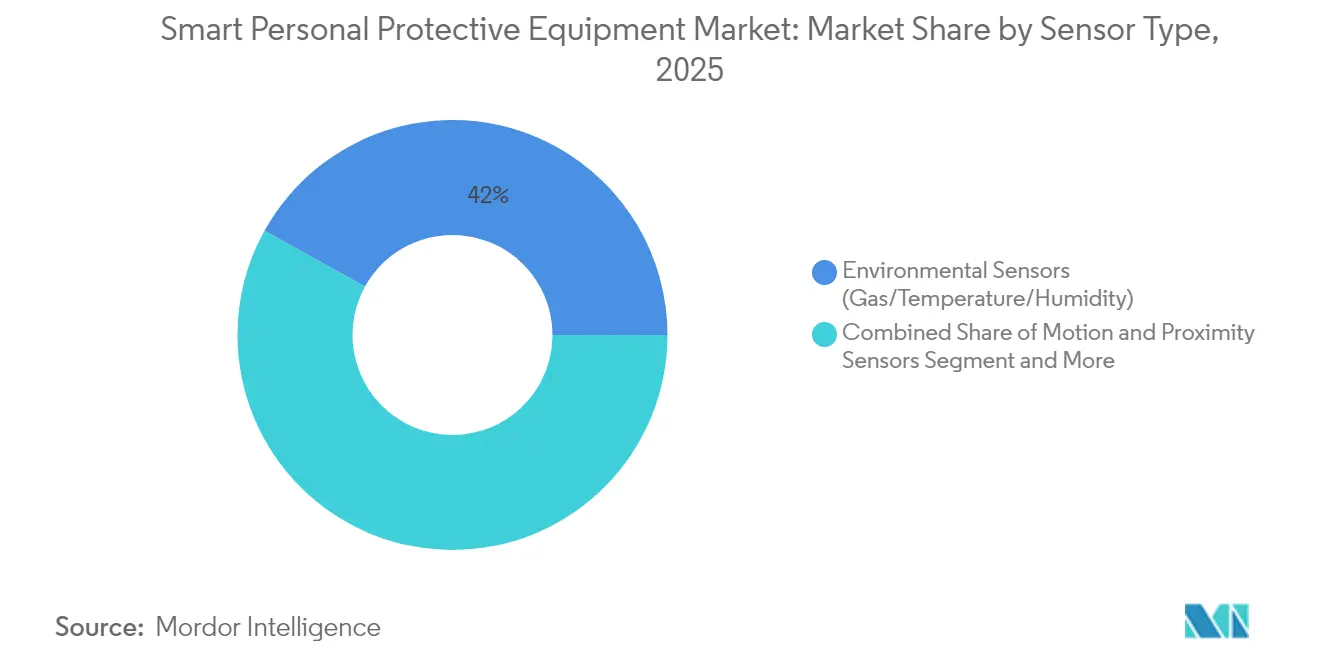

- By sensor type, environmental sensors accounted for 41.95% of smart personal protective equipment market size in 2025 and motion plus proximity sensors are tracking a 14.04% CAGR to 2031.

- By end-user industry, oil and gas captured 24.05% of smart personal protective equipment market share in 2025, while construction is growing fastest at a 12.95% CAGR up to 2031.

- By geography, North America accounted for 39.98% revenue share in 2025 and Asia Pacific is advancing at a 12.96% CAGR over the forecast horizon.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Smart Personal Protective Equipment Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Stringent Safety Regulations in Europe and North America | +2.8% | Europe and North America | Medium term (2-4 years) |

| Real-time Biometric and Location Monitoring in Underground Mining | +2.1% | Global, concentrated in Asia-Pacific and Americas | Long term (≥ 4 years) |

| Connected-Worker Programs Lowering Insurance Costs in Oil and Gas | +1.9% | Global, led by North America and Middle East | Medium term (2-4 years) |

| Construction-4.0 Megaprojects in Asia-Pacific | +2.3% | Asia-Pacific core, spill-over to MEA | Long term (≥ 4 years) |

| Post-COVID Demand for Contact-less Safety Monitoring in Manufacturing | +1.7% | Global | Short term (≤ 2 years) |

| Declining IoT Sensor Costs Driving SME Retro-fit Adoption (LatAm) | +1.4% | Latin America, expanding to emerging markets | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Stringent Safety Regulations in Europe and North America

OSHA’s 2025 heat-safety rule compels real-time physiological monitoring, and updated fitting guidelines close protection gaps for female and smaller-statured workers.[1]Occupational Safety and Health Administration, “Personal Protective Equipment in Construction,” osha.gov European GDPR constraints create a paradox because continuous biometrics raise privacy concerns. Manufacturers respond with edge-computing smart glasses that anonymize data yet still trigger instant alerts. Enterprise buyers see these hybrid solutions as the optimal route to meet dual compliance and privacy requirements.

Real-time Biometric and Location Monitoring in Underground Mining

Smart helmets with integrated gas sensors deliver 97% toxic-gas detection accuracy and cut response times by half in deep mines.[2]Eyab Alshehab, “Enhancing Occupational Safety in Mining: Evaluating the Effectiveness of an Integrated Toxic Gas Detection Wearable,” figshare.com BLE beacons combined with 6G backhaul extend coverage to previously unreachable shafts. Operators aggregate gas, temperature, and location data to fine-tune ventilation systems and schedule predictive maintenance, framing smart PPE as an operational intelligence layer rather than a simple safety accessory.

Connected-Worker Programs Lowering Insurance Costs in Oil and Gas

Major producers deploy hydration patches, fatigue sensors, and environmental monitors to validate risk-mitigation programs for insurers. Chevron’s three-year agreement with Epicore Biosystems is the reference case; early results show fewer heat-related incidents and demonstrable premium reductions.[3]Chevron Policy Government and Public Affairs, “Wearable tech helps remind workers to stay hydrated,” chevron.com Exoskeletons supply quantifiable strain-reduction metrics that strengthen negotiations with workers ’-comp carriers.

Construction-4.0 Megaprojects in Asia Pacific

Regional contractors embed IoT-enabled safety systems into Building Information Modeling workflows. AI body cameras and vital sign wearables reduce collision incidents and optimize task sequencing on dense sites. The Osaka-Kansai Expo validates large-scale deployment economics, creating credible case studies that help smaller contractors justify investments.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Up-front Investment and Uncertain ROI for SMEs | -1.8% | Global, particularly pronounced in emerging markets | Short term (≤ 2 years) |

| GDPR and CCPA Restricting Continuous Biometric Capture | -1.2% | Europe and North America, expanding globally | Medium term (2-4 years) |

| Battery-Life Constraints Causing Device Downtime in Remote Sites | -1.5% | Global, critical in mining and offshore operations | Medium term (2-4 years) |

| Lack of Interoperability Across PPE and IoT Platforms | -1.1% | Global | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High Up-front Investment and Uncertain ROI for SMEs

Smart PPE often costs 300 % to 500 % more than conventional gear, so many small enterprises delay adoption. Modular retrofit kits and PPE-as-a-Service leasing reduce capital intensity, while falling sensor prices make phased rollouts viable for Latin American manufacturers.

GDPR and CCPA Restricting Continuous Biometric Capture

Privacy law limits heart rate, location, and fatigue monitoring unless data are anonymized or processed on-device. Vendors now integrate differential-privacy algorithms and consent portals, complying with regulations yet retaining real-time alerting capabilities. Added complexity raises development costs but creates niches for privacy-first platform providers.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Type: Body Protection Dominates Smart Integration

Body protection held a 29.76% revenue share in 2025, cementing its status as the anchor layer for multi-sensor arrays. Smart vests fuse temperature, gas, and posture tracking without compromising comfort. This category benefits from established textile supply chains that enable conductive fiber integration at scale. The large surface area also supports embedded fiber batteries, solving run-time challenges during extended shifts.

Smart gloves are tracking a 14.11% CAGR, the fastest within the segment. Voice-free gesture recognition and haptic feedback allow technicians to interact with automation systems while wearing chemical-resistant protection. Manufacturers add micro-electromechanical sensors that tally grip-force data, which supervisors mine to identify musculoskeletal strain patterns. These analytics minimize downtime and elevate productivity.

By Technology: IoT Platforms Enable Connected Ecosystems

IoT-enabled PPE retained 60.85% of the smart personal protective equipment market in 2025, forming the backbone for cloud analytics and fleet management. Standardized APIs let enterprises plug multiple PPE types into a single dashboard and feed incidents directly into enterprise resource planning modules. This uniformity shortens proof-of-concept cycles and underpins multiyear replacement contracts.

AR/VR smart glasses, growing at 13.04% CAGR, provide hands-free instructions and remote expert support. Battery advances now allow a full shift of operation, removing a historical adoption barrier. The hardware integrates thermal imaging, which overlays heat maps onto the user’s view to flag hot surfaces before contact. AI-driven predictive safety software mines sensor trends to forecast near-miss scenarios, pushing preemptive warnings.

By Connectivity: Bluetooth Leads with 5G Acceleration

Bluetooth Low Energy owns 49.12% share because of low power draw and near-universal smartphone compatibility. Wearables offload processing to the user’s handset or a ruggedized industrial gateway, extending battery life in harsh conditions. BLE mesh capabilities allow peer-to-peer data relay when cellular service is weak, sustaining alert coverage in remote mines.

Cellular connectivity, expanding at a 13.83% CAGR, removes the need for local gateways in widespread oilfields or linear construction corridors. The advent of private 5G networks brings low-latency data paths that support AR overlays and real-time video troubleshooting. Wi-Fi persists inside fixed plants where bandwidth-intensive streaming is required. Zigbee and LPWAN support agriculture and long-tunnel operations due to kilometer-scale range at minimal power draw.

By Sensor Type: Environmental Monitoring Drives Adoption

Environmental sensors captured 41.95% revenue in 2025. Gas, temperature, and humidity modules serve as immediate life-saving devices by issuing audible alerts once thresholds are crossed. Vendors now integrate AI pattern-recognition to cut false positives while remaining sensitive to sudden hazards.

Motion and proximity sensors, the fastest-growing sub-segment at 14.04% CAGR, enable collision avoidance between heavy equipment and pedestrian workers. Combining ultrawide-band ranging with inertial measurement units gives centimeter-level precision, critical on congested construction sites. Vital-sign sensors detect dehydration, fatigue, and cardiac stress without invasive contacts, further broadening monitoring scope.

By End-user Industry: Oil and Gas Leads with Construction Accelerating

Oil and gas held 24.05% revenue in 2025, reflecting decades of high-risk operations and deeper pockets for innovation adoption. Offshore teams use satellite-linked smart vests to share vitals with onshore medical centers, achieving faster triage decisions when evacuations are triggered. Connected exoskeletons feed strain readings to asset-integrity models, linking human performance data with equipment-health metrics.

Construction, projected to grow 12.95% CAGR, rides momentum from megaprojects that bundle IoT safety, autonomous machinery, and BIM. Contractors rationalize investments by lowering incident downtime and meeting new government mandates that penalize safety breaches. Mining, utilities, and manufacturing round out demand as each sector connects previously isolated workflows to corporate dashboards.

Geography Analysis

North America generated 39.98% of global revenue in 2025. OSHA’s heat-safety mandate plus insurance premium incentives have cemented connected-worker programs as standard practice. Chevron’s hydration-patch deployment provides benchmark evidence, demonstrating measurable reductions in heat events and workers-comp costs. Mature 4G/5G coverage and robust data-protection frameworks underpin large-scale rollouts.

Asia Pacific is advancing at a 12.96% CAGR through 2031. China converted advisory PPE guidelines into binding requirements, immediately enlarging the addressable base. Japan’s Osaka-Kansai Expo acted as a live laboratory for heat-stress wearables on 300 cleaning staff, showcasing real-time dashboards for supervisors. India’s SAMARTH Udyog Bharat 4.0 policy weaves smart PPE into national manufacturing modernization, aligning safety with productivity.

Europe records steady uptake. GDPR drives edge-processing adoption, while sustainability goals shift buyers toward durable, sensor-rich garments that reduce waste. The Middle East and Africa leverage smart PPE in high-temperature oil fields and deep mines where remote medical infrastructure is sparse. Latin America benefits from falling sensor costs and emerging PPE-as-a-Service models that lower entry barriers for SMEs.

Competitive Landscape

The market shows moderate concentration. Legacy manufacturers recalibrate portfolios toward connected solutions. Honeywell divested its conventional PPE unit for USD 1.325 billion, reallocating capital to automation and aerospace focus areas. Protective Industrial Products acquired those assets to deepen its industrial channel presence. Ansell added the Kimtech and KleenGuard brands for USD 640 million, expanding clean-room and scientific lines.

Technical differentiation hinges on power management, analytics, and interoperability. Johns Hopkins University’s textile-embedded fiber battery patent tackles run-time limitations without adding bulk. AI body cameras from pair video with GPS and LTE, enabling remote supervisors to audit compliance in real time. Partnerships between PPE makers and cloud-analytics firms surface integrated stacks that streamline deployment, addressing the key barrier of multi-vendor fragmentation.

Emerging firms focus on vertical niches. Mining-specific gas helmets claim accuracy advantages in methane detection, while construction-centric fall-arrest harnesses link to BIM platforms. Privacy-preserving analytics, a European imperative, becomes a global differentiator as regulators elsewhere study GDPR’s template.

Smart Personal Protective Equipment Industry Leaders

Honeywell International Inc.

3M Company

MSA Safety Inc.

Ansell Ltd.

Uvex Group

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2025: Mitsufuji Corporation’s “hamon band 2” heat-stress wearable deployed for 300 cleaning staff at Osaka-Kansai Expo to meet new Japanese safety regulations.

- May 2025: Senseway Inc. presented “Worker Connect” wrist-sensor suite for heart-rate, temperature, and fall detection at Osaka-Kansai Expo, targeting 2025 heat-stroke mandates.

- April 2025: Honeywell reported 8% sales growth while classifying its PPE business as held for sale to focus on automation and energy-transition growth vectors.

- December 2024: Honeywell completed the USD 1.325 billion PPE divestiture to Protective Industrial Products, unlocking capital for strategic verticals.

Global Smart Personal Protective Equipment Market Report Scope

Smart PPE allows site managers to know the location of their workers and ensure their protection and safety. It saves time and increases compliance, resulting in improved worker protection, comfort, health, and safety and, consequently, a happier workforce. The enriched tracking information, data, and communication provided by smart PPE will result in a more profitable business.

The smart personal protective equipment market is segmented by type (eye and face protection, hearing protection, head protection, fall protection, smart clothing, and other types), end-user industry (construction, mining, oil and gas, manufacturing, automotive, and other end-user industries), and geography (North America, Europe, Asia-Pacific, Latin America, and Middle East, and Africa). The market sizes and forecasts are provided in terms of value (USD) for all the above segments.

| Eye and Face Protection |

| Hearing Protection |

| Head Protection |

| Respiratory Protection |

| Hand Protection (Smart Gloves) |

| Body Protection (Smart Clothing and Vests) |

| Fall Protection Devices |

| Foot Protection (Smart Footwear) |

| Integrated Multi-Sensor PPE |

| IoT-Enabled PPE |

| AR/VR-Enabled Smart Glasses |

| AI-Based Predictive Safety Analytics |

| Cloud-Connected PPE Platforms |

| Bluetooth Low Energy |

| Wi-Fi |

| Cellular (4G/LTE/5G) |

| Zigbee / LPWAN |

| Wired |

| Environmental Sensors (Gas/Temperature/Humidity) |

| Motion and Proximity Sensors |

| Biometric and Vital-Sign Sensors |

| Construction |

| Oil and Gas |

| Mining |

| Manufacturing |

| Automotive |

| Chemicals and Pharmaceuticals |

| Utilities (Energy and Power) |

| Healthcare and Life Sciences |

| Firefighting and Law Enforcement |

| Transportation and Logistics |

| North America | United States | |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Chile | ||

| Rest of South America | ||

| Europe | Germany | |

| France | ||

| United Kingdom | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| ASEAN | ||

| Australia | ||

| New Zealand | ||

| Rest of Asia Pacific | ||

| Middle East and Africa | Middle East | GCC |

| Turkey | ||

| Israel | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Nigeria | ||

| Egypt | ||

| Rest of Africa | ||

| By Type | Eye and Face Protection | ||

| Hearing Protection | |||

| Head Protection | |||

| Respiratory Protection | |||

| Hand Protection (Smart Gloves) | |||

| Body Protection (Smart Clothing and Vests) | |||

| Fall Protection Devices | |||

| Foot Protection (Smart Footwear) | |||

| Integrated Multi-Sensor PPE | |||

| By Technology | IoT-Enabled PPE | ||

| AR/VR-Enabled Smart Glasses | |||

| AI-Based Predictive Safety Analytics | |||

| Cloud-Connected PPE Platforms | |||

| By Connectivity | Bluetooth Low Energy | ||

| Wi-Fi | |||

| Cellular (4G/LTE/5G) | |||

| Zigbee / LPWAN | |||

| Wired | |||

| By Sensor Type | Environmental Sensors (Gas/Temperature/Humidity) | ||

| Motion and Proximity Sensors | |||

| Biometric and Vital-Sign Sensors | |||

| By End-user Industry | Construction | ||

| Oil and Gas | |||

| Mining | |||

| Manufacturing | |||

| Automotive | |||

| Chemicals and Pharmaceuticals | |||

| Utilities (Energy and Power) | |||

| Healthcare and Life Sciences | |||

| Firefighting and Law Enforcement | |||

| Transportation and Logistics | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| South America | Brazil | ||

| Argentina | |||

| Chile | |||

| Rest of South America | |||

| Europe | Germany | ||

| France | |||

| United Kingdom | |||

| Italy | |||

| Spain | |||

| Rest of Europe | |||

| Asia Pacific | China | ||

| Japan | |||

| India | |||

| South Korea | |||

| ASEAN | |||

| Australia | |||

| New Zealand | |||

| Rest of Asia Pacific | |||

| Middle East and Africa | Middle East | GCC | |

| Turkey | |||

| Israel | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Nigeria | |||

| Egypt | |||

| Rest of Africa | |||

Key Questions Answered in the Report

What is the current value of the smart personal protective equipment market?

The market is valued at USD 5.55 billion in 2026 and is forecast to grow to USD 10.16 billion by 2031.

Which region leads the smart personal protective equipment market?

North America leads with 39.98% revenue share in 2025, driven by stringent OSHA regulations and early connected-worker adoption.

Which technology segment is growing fastest?

AR/VR-enabled smart glasses are expanding at a 13.04% CAGR due to hands-free remote guidance and training advantages.

How are insurers influencing smart PPE adoption?

Insurance carriers offer premium discounts when connected-worker programs are in place, providing a direct financial return on investment.

What are the main barriers for small and medium enterprises?

High initial costs and uncertain payback periods deter SMEs, although PPE-as-a-Service models and falling sensor prices are reducing this hurdle.

Page last updated on: