Security Camera Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

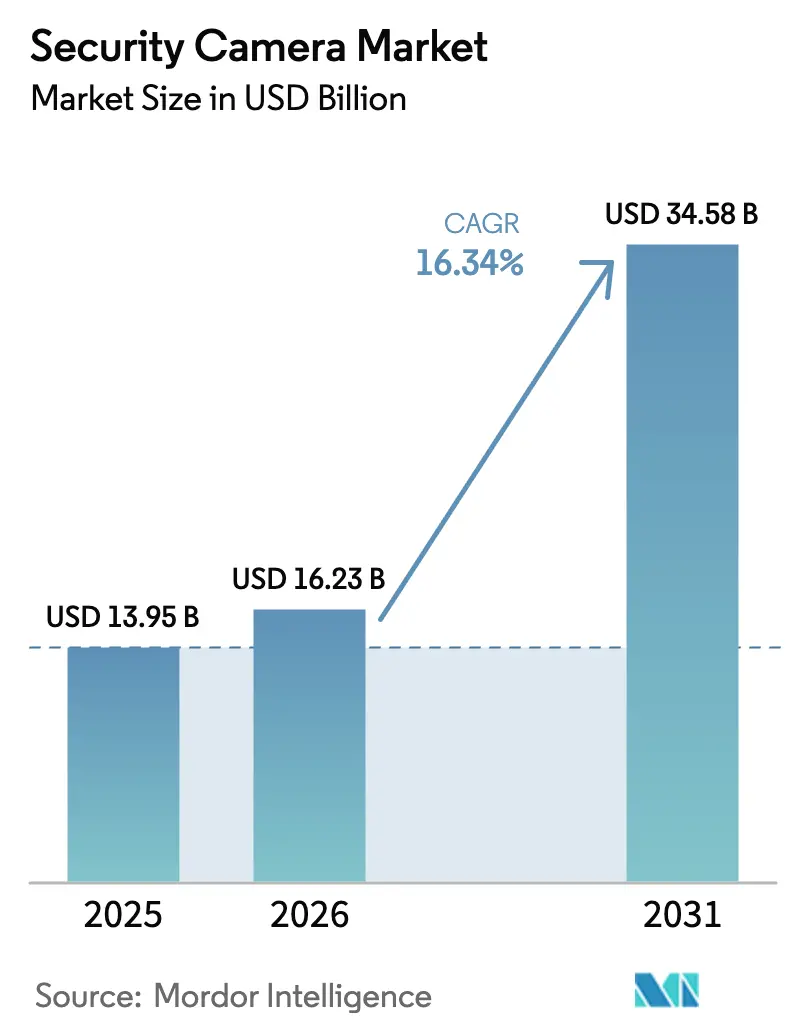

| Market Size (2026) | USD 16.23 Billion |

| Market Size (2031) | USD 34.58 Billion |

| Growth Rate (2026 - 2031) | 16.34% CAGR |

| Fastest Growing Market | Middle East and Africa |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Security Camera Market Analysis by Mordor Intelligence

The security camera market size was valued at USD 13.95 billion in 2025 and estimated to grow from USD 16.23 billion in 2026 to reach USD 34.58 billion by 2031, at a CAGR of 16.34% during the forecast period (2026-2031). This strong growth reflects government-mandated migrations from analog to IP infrastructure, heightened cyber-resilience rules, and accelerated integration of artificial intelligence across surveillance ecosystems. A shift toward Video Surveillance as a Service (VSaaS) is broadening access to enterprise-grade analytics for small and mid-sized businesses, while the Middle East and Asia Pacific channel massive smart-city budgets into multi-sensor installations. Supply-chain constraints in 4K image sensors and NDAA-driven reshoring are lifting compliant vendors’ pricing power, creating both margin expansion potential and deployment delays. Form-factor innovation - from vandal-resistant domes to integrated doorbell units - continues to broaden use-case fit, reinforcing volume gains for the overall security camera market.

Key Report Takeaways

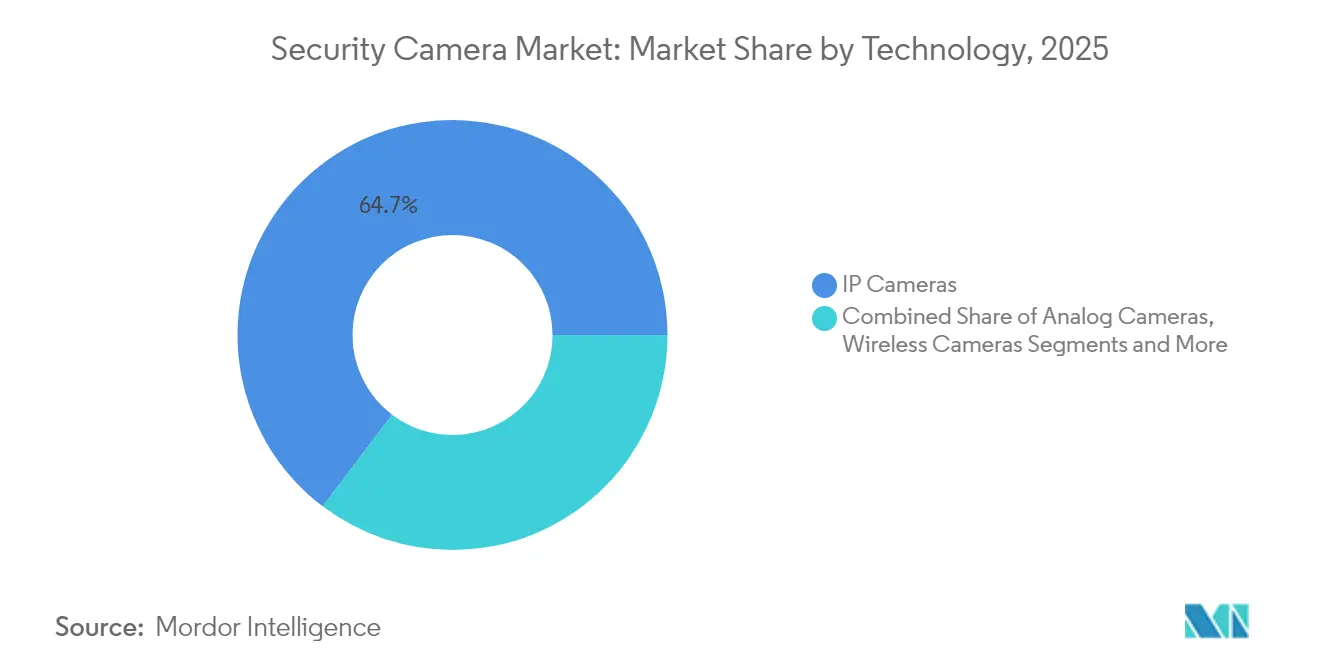

- By technology, IP cameras led with 64.68% of security camera market share in 2025; wireless cameras are projected to expand at 16.78% CAGR through 2031.

- By camera form factor, dome units captured 30.78% revenue share in 2025; doorbell cameras are forecast to grow at 16.71% CAGR to 2031.

- By end-user industry, commercial and infrastructure applications held 36.54% share of the security camera market size in 2025, while residential adoption is advancing at 17.55% CAGR through 2031.

- By resolution, HD systems commanded 53.62% share in 2025 and 4K cameras are set to post 16.58% CAGR through 2031.

- By connectivity, wired solutions maintained 67.74% share of the security camera market size in 2025; wireless units exhibit an 17.72% CAGR outlook through 2031.

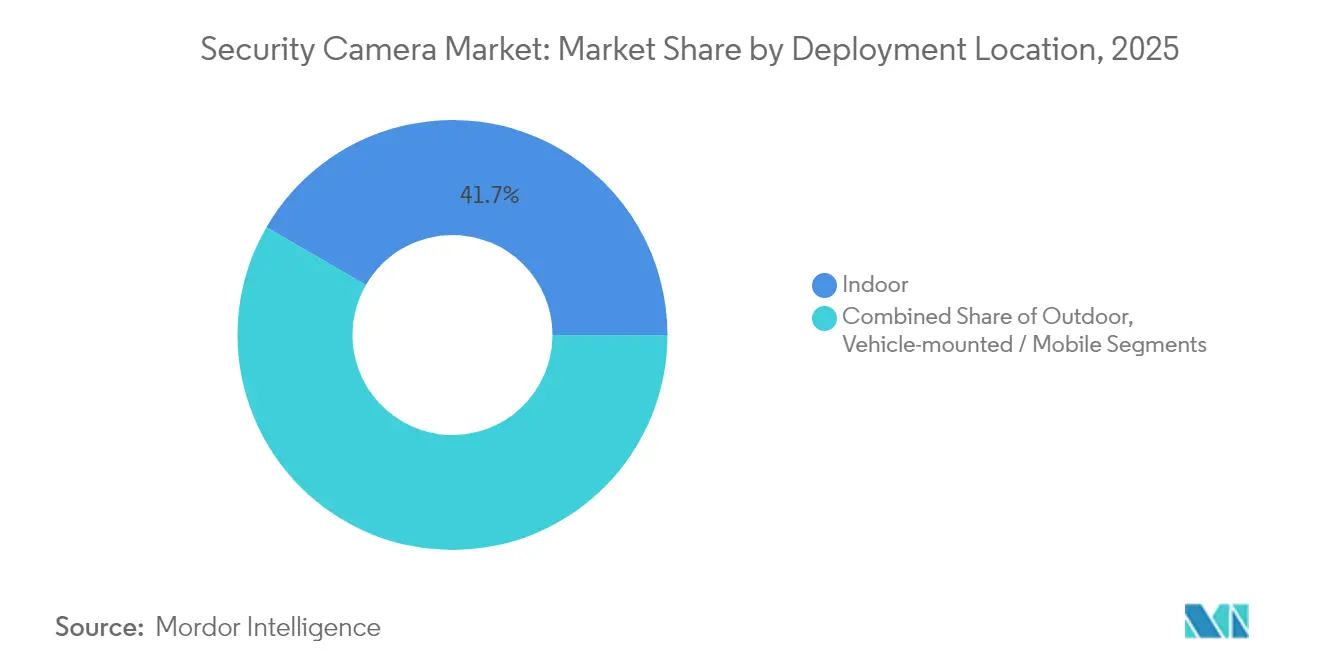

- By Deployment Location, indoor cameras accounted for 41.65% of 2025 revenue yet outdoor and doorbell units are projected to rise 17.21% CAGR through 2031.

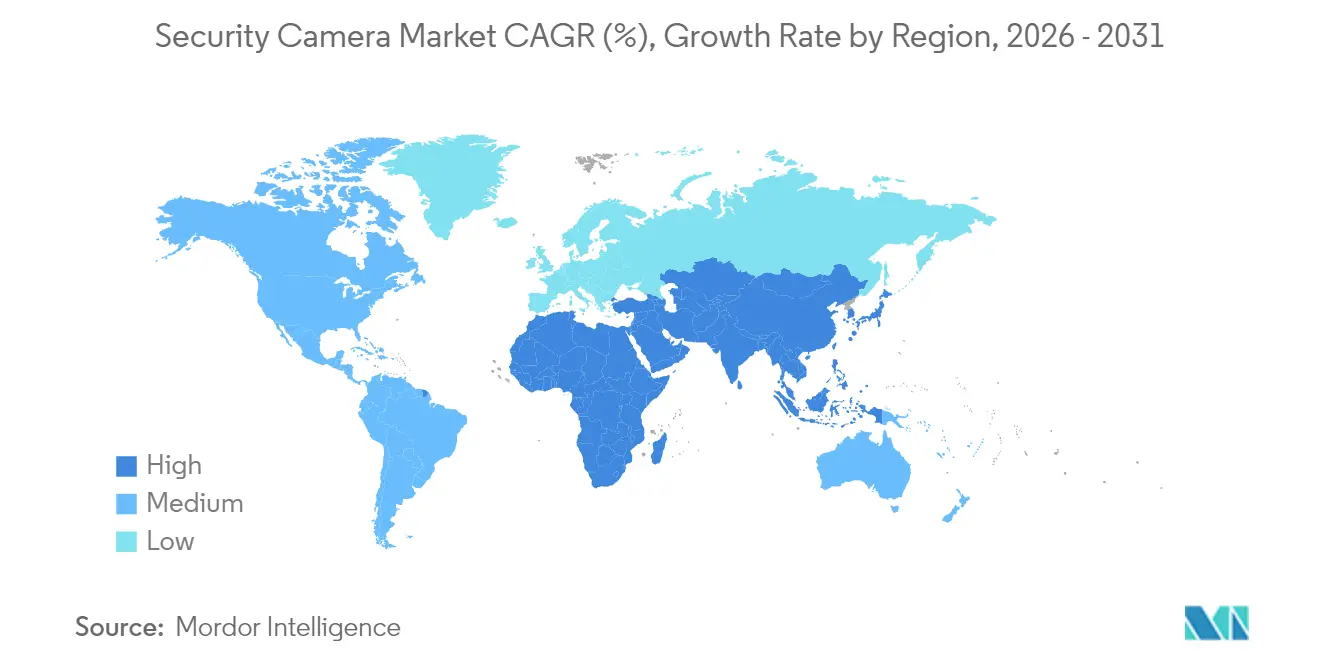

- By geography, Asia Pacific accounted for 41.92% of the security camera market share in 2025; the Middle East is registering the highest 15.24% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Security Camera Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| AI-enabled analytics demand in Asian smart cities | +3.2% | Asia Pacific core, spill-over to MEA | Medium term (2-4 years) |

| Mandated migration from analog to IP under EU NIS2 and CER | +2.8% | Europe and North America | Short term (≤ 2 years) |

| VSaaS adoption among U.S. SMEs | +2.1% | North America, expanding global | Medium term (2-4 years) |

| Retail shrinkage crisis in South-American supermarkets | +1.9% | South America, selective North America | Short term (≤ 2 years) |

| Multi-sensor deployment in Middle-East mega projects | +1.7% | Middle East, selective Asia Pacific | Long term (≥ 4 years) |

| Insurance-led residential smart-camera uptake | +1.4% | North America and EU | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

AI-enabled Analytics Demand for Proactive Threat Detection in Asian Smart Cities

Asian municipalities deploy predictive video algorithms that process tens of millions of facial images daily, reducing manned-monitoring requirements and enabling automated incident triage. Real-time high-dynamic-range imaging, powered by stacked CMOS sensors, enhances accuracy across variable lighting and crowd densities. Regional programs integrate surveillance data into digital-twin city platforms, strengthening emergency response coordination and public-service planning. Privacy-preserving, on-premise analytics frameworks answer rising data-sovereignty demands and maintain regulatory alignment.[1]Rochester Institute of Technology, "Artificial Intelligence for Smarter Surveillance Using CCTV Cameras in the UAE," repository.rit.edu

Government-Mandated Migration from Analog to IP Cameras under EU NIS2 and CER Directives

New European cyber-resilience rules oblige encrypted video transport, firmware audit trails, and network segmentation - standards legacy analog hardware cannot satisfy. Operators are consequently replacing up to 40% of installed bases by 2027, favoring vendors offering NDAA-compliant, security-hardened IP devices. Budget re-allocations include lifecycle cybersecurity services and staff up-skilling, reshaping total ownership cost models and boosting demand for European manufacturers that ship pre-certified solutions.

Subscription Uptake of VSaaS among U.S. SMEs Shifting to OPEX Security Budgets

Cloud-native platforms now deliver sub-second live streaming and AI incident summaries via predictable monthly fees, eliminating capex hurdles. Embedded generative-AI tools automate threat narratives, enabling lean teams to oversee multi-site estates. Edge-enhanced architectures further lower bandwidth costs by performing in-camera analytics, broadening VSaaS applicability to bandwidth-limited or rural operations.[2]IPVM, "Shanghai District Tripling Mass Surveillance, Expanding Behavioral Analytics," ipvm.com

Retail Shrinkage Crisis Accelerating Video Analytics in South-American Supermarkets

Organized retail crime pushes shrinkage above 2.5% of sales, spurring chains to integrate behavioral-analysis engines that flag coordinated theft patterns, employee misconduct, and unconventional dwell times. Early adopters record double-digit loss reductions within six months, validating return-on-investment cases and triggering broader regional deployments.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| NDAA and EU Sanction Barriers on Chinese OEMs Slowing Deployment Cycles | -2.4% | Global, concentrated in North America and EU | Short term (≤ 2 years) |

| 4K Image-Sensor Shortages Constraining Premium Camera Supply Chains | -1.8% | Global, acute in Asia Pacific manufacturing | Medium term (2-4 years) |

| GDPR-Driven Compliance Costs for Edge Recording in Europe | -1.3% | Europe, extending to Global data flows | Medium term (2-4 years) |

| Escalating IoT Cyber-attacks Deterring Cloud Deployments in Healthcare Vertical | -1.1% | Global, concentrated in North America and EU | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

NDAA and EU Sanction Barriers on Chinese OEMs Slowing Deployment Cycles

Heightened origin-traceability requirements lengthen procurement lead times by 3-6 months as buyers validate component supply chains. Restricted vendors exit federal and critical-infrastructure tenders, while compliant manufacturers command premium prices, pressuring project budgets but unlocking higher gross margins for approved suppliers.

4K Image-Sensor Shortages Constraining Premium Camera Supply Chains

Limited 4K CMOS fabrication capacity and cross-sector competition from automotive and mobile device makers trigger 6-12 month delivery delays for high-resolution models. Allocation systems and interim lower-resolution substitutions heighten channel complexity and encourage makers to redesign portfolios around emerging stacked-sensor architectures that promise higher yields but require additional capital investment.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Technology: IP Infrastructure Dominance Accelerates Wireless Adoption

The security camera market size for IP deployments represented 64.68% of 2025 revenue, underlining a decisive shift toward network-centric video frameworks. Wireless units register the fastest 16.78% CAGR as installers appreciate cable-free retrofits and smart-building compatibility. Declining analog estates linger in cost-sensitive sites, while hybrid bridges support phased migration strategies. Edge-embedded AI on Wi-Fi cameras now rivals wired counterparts in low-light clarity and response latency, enlarging addressable use cases.

Enhanced 5G backhaul empowers real-time 4K streams, and on-device inference offloads cloud compute demands. Vendors differentiate through zero-trust firmware, automatic certificate rotation, and open API integration that curbs vendor lock-in risk. As a result, wireless devices shift from auxiliary to primary coverage roles in pop-up retail, temporary events, and distributed branch networks, strengthening volume prospects for the security camera market.

By End-User Industry: Commercial Leadership Challenged by Residential Surge

Commercial and infrastructure environments held 36.54% of 2025 revenue within the security camera market share, reflecting stringent compliance needs in banking, transit, and government applications. Residential smart-home uptake is expanding at 17.55% CAGR as insurers underwrite premium discounts for verified video devices, and homeowners leverage unified home-automation control hubs. Healthcare uptake remains cautious pending robust cyber-hygiene proof points, whereas retail chains couple shelf-analytics with loss-prevention video streams to sharpen merchandising.

Doorbell units symbolise residential momentum, combining two-way audio and parcel-tracking features that extend perceived value beyond security. Educational campuses balance safety with student privacy through zoned monitoring and opt-in analytics suites. Industrial plants merge security and production-line inspection into consolidated camera grids, maximizing capital productivity. Collectively, these trends reinforce sustained diversification within the security camera market.

By Camera Form Factor: Dome Reliability Meets Doorbell Innovation

Dome cameras retained 30.78% revenue share in 2025 given their vandal-resistant enclosures and discreet aesthetics suited to retail aisles and transportation hubs. Doorbell devices, advancing at 16.71% CAGR, integrate seamlessly into smart-home ecosystems, emphasizing convenience and contactless logistics. Bullet models persist outdoors where directional focus and rugged housings are critical, while PTZ units fulfil active-tracking needs in large perimeters.

Aesthetic-driven designs now conceal sensors inside architectural fittings, broadening residential appeal. Panoramic multi-sensor domes reduce infrastructure counts in stadiums and airports, enhancing total-cost efficiencies. AI-powered dome models perform in-camera anomaly detection, shortening investigative cycles and containing bandwidth use. Such form-factor variety sustains device replacement cycles across the security camera market.

By Resolution: HD Prevalence Confronts 4K Transition

HD systems (720p-1080p) delivered 53.62% of 2025 volumes, balancing clarity and storage economics for mainstream surveillance. The 4K tier is posting 16.58% CAGR, propelled by falling storage costs and AI models that benefit from pixel-rich inputs. Ongoing sensor shortages temper near-term conversions, but stacked-CMOS breakthroughs promise greater sensitivity and energy efficiency, preparing the security camera market for an eventual high-resolution tipping point.

Edge compression algorithms and dynamic-frame-rate tuning mitigate network and cloud-bucket inflation, enabling cost-conscious enterprises to plan gradual upgrades. In sectors like banking and public transit, jurisdictional mandates for face-level clarity accelerate 4K refresh cycles despite supply-chain friction.

By Deployment Location: Indoor Security Expands Outdoor Integration

Indoor cameras accounted for 41.65% of 2025 revenue yet outdoor and doorbell units are projected to rise 17.21% CAGR, mirroring heightened perimeter-defense emphasis. Harsh-environment designs with IP66-rated casings and integrated heaters ensure uptime across extreme climates. Indoor units increasingly double as occupancy-analytics sensors, supplying facilities teams with space-utilization metrics.

Thermal and multi-spectral modalities augment outdoor perimeter coverage, detecting intruders in zero-light or smoke conditions. Mobile vehicle-mounted cameras support policing and event security, while battery-powered models furnish temporary construction sites. The interplay of fixed and mobile nodes enriches situational awareness across the security camera market.

By Connectivity: Wired Stability Supports Wireless Flexibility

PoE and coaxial links preserved 67.74% share of 2025 deployments, favored for uninterrupted power and low latency in mission-critical areas. Wireless Wi-Fi devices, growing at 17.72% CAGR, simplify retrofits and remote site coverage. Cellular 4G/5G backhaul unlocks surveillance in infrastructure-poor territories, with multi-path failover boosting reliability.

Mesh networking extends node reach and adds redundancy, while edge analytics limit uplink loads. Hybrid architectures combine wired trunks with Wi-Fi edge devices, enabling scale without excessive cabling. These advancements sustain robust penetration gains within the security camera market.

Geography Analysis

Asia Pacific commanded 41.92% of 2025 revenue within the security camera market, supported by large-scale smart-city rollouts, strong manufacturing ecosystems, and sustained public-safety funding. Shanghai’s latest deployment now processes over 25 million facial records daily, illustrating both scale and data-analytics sophistication. Japan and South Korea pioneer sensor miniaturization and edge inference, while India’s urban-modernization schemes amplify demand for cost-efficient yet AI-ready devices.

The Middle East is forecast to post the fastest 15.24% CAGR through 2031. Projects such as Saudi Arabia’s NEOM and Dubai’s Expo City embed multi-sensor grids that integrate license-plate recognition, crowd analytics, and environmental monitoring. Generous government funding and mandates for resilience elevate system specifications, fostering early adoption of 5G-enabled, AI-embedded cameras.

North America exhibits steady replacement demand centered on NDAA-compliant inventories and cloud migration. Enterprises recalibrate vendor rosters, and small-business segments pivot toward VSaaS for budgetary alignment. Europe stands out for regulatory-driven refresh cycles under NIS2 and CER directives, intensifying preference for encrypted, firmware-signed IP hardware. South America’s urban centers implement video analytics to counter soaring organized crime, while cyber-attack prevalence spurs interest in edge-processed deployments to minimize cloud exposure.

Competitive Landscape

Market concentration remains moderate. Hikvision recorded USD 9.31 billion revenue in 2024, with Dahua at USD 4.32 billion. NDAA restrictions, however, bar both from many U.S. and European bids, shifting share toward Axis Communications, Bosch Security Systems, and Hanwha Vision, each leveraging regulatory compliance as a competitive wedge. Consolidation persists as firms acquire analytics start-ups to expand AI portfolios and diversify away from pure hardware margins.

Edge-AI differentiation is pivotal. Manufacturers embed neural-network accelerators to perform real-time object and behavior detection on the device, cutting bandwidth loads and latency. Cloud-first challengers such as Verkada and Eagle Eye Networks convert hardware into annuity revenue by bundling continuous software updates, cyber-patching, and AI features into subscription tiers. Supply-chain volatility, in turn, drives inventory hedging and dual-sourcing strategies that favor financially resilient players within the security camera market.

Strategic alliances emerged in 2025 between component suppliers and camera OEMs to secure 4K sensor allocations, while software firms co-develop SDKs for faster third-party analytics integration. These moves underscore a convergence trend: hardware makers morph into platform providers, and cloud vendors invest in edge devices, tightening competitive boundaries yet enhancing end-user value.

Security Camera Industry Leaders

-

Hangzhou Hikvision Digital Technology Co., Ltd.

-

Dahua Technology Co., Ltd

-

Bosch Security Systems GmbH

-

Hanwha Group

-

Axis Communication AB

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2025: Shanghai’s Xuhui District completed a CNY 31 million facial-recognition network adding 3,700 cameras to handle 25.9 million daily images, reinforcing China’s smart-city leadership

- January 2025: Uniview Technologies issued a full NDAA compliance statement and updated certification registry, positioning for U.S. federal and critical-infrastructure tenders.

- May 2024: Valiant Power became the preferred OEM for surveillance trailer systems priced above USD 15,000 per unit, broadening mobile-security options for construction and events.

- April 2024: ISC West showcased generative-AI video analytics from IronYun, NVIDIA, and Verkada, illustrating a shift toward natural-language incident summarization that reduces operator workload.

Global Security Camera Market Report Scope

Security cameras, whether monitoring indoors or outdoors, capture images or record videos to detect intruders or thieves. These devices are prevalent in businesses, retail stores, schools, homes, parking lots, roads, and other locations frequented by people. Security cameras not only assist in apprehending criminals but also act as a deterrent, discouraging potential wrongdoers. The study tracks revenues from the sales of major product categories like analog and IP cameras offered by worldwide vendors. It also tracks the geopolitical and macroeconomic factors impacting the market.

The security camera market is segmented by type (analog cameras, IP cameras), end-user industry (banking and financial institutions, transportation and infrastructure, government and defense, healthcare, industrial, retail, enterprises, residential, others), and geography (North America, Europe, Asia-Pacific, Latin America, Middle East and Africa). The market sizes and forecasts are provided in terms of value (USD) for all the above segments.

| Analog Cameras |

| IP Cameras |

| Wireless Cameras |

| Hybrid Cameras |

| Bullet Cameras |

| Dome Cameras |

| PTZ Cameras |

| Box Cameras |

| Panoramic / Multi-sensor Cameras |

| Doorbell Cameras |

| Others |

| Standard Definition (<720p) |

| HD (720p-1080p) |

| Full-HD (2 MP) |

| 4K & Above |

| Indoor |

| Outdoor |

| Vehicle-mounted / Mobile |

| Wired (Coax / PoE) |

| Wi-Fi |

| Cellular (4G / 5G) |

| Banking and Financial Institutions |

| Transportation and Infrastructure |

| Government and Defense |

| Healthcare Facilities |

| Industrial and Manufacturing |

| Retail and Malls |

| Enterprises and Commercial Buildings |

| Residential / Smart Homes |

| Education Campuses |

| Hospitality and Leisure |

| Others |

| North America | United States | |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | United Kingdom | |

| Germany | ||

| France | ||

| Italy | ||

| Spain | ||

| Nordics (Denmark, Sweden, Norway) | ||

| Rest of Europe | ||

| Asia Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| ASEAN | ||

| Australia | ||

| New Zealand | ||

| Rest of Asia Pacific | ||

| Middle East and Africa | Middle East | GCC |

| Turkey | ||

| Israel | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Nigeria | ||

| Egypt | ||

| Rest of Africa | ||

| By Technology | Analog Cameras | ||

| IP Cameras | |||

| Wireless Cameras | |||

| Hybrid Cameras | |||

| By Camera Form Factor | Bullet Cameras | ||

| Dome Cameras | |||

| PTZ Cameras | |||

| Box Cameras | |||

| Panoramic / Multi-sensor Cameras | |||

| Doorbell Cameras | |||

| Others | |||

| By Resolution | Standard Definition (<720p) | ||

| HD (720p-1080p) | |||

| Full-HD (2 MP) | |||

| 4K & Above | |||

| By Deployment Location | Indoor | ||

| Outdoor | |||

| Vehicle-mounted / Mobile | |||

| By Connectivity / Power | Wired (Coax / PoE) | ||

| Wi-Fi | |||

| Cellular (4G / 5G) | |||

| By End-User Industry | Banking and Financial Institutions | ||

| Transportation and Infrastructure | |||

| Government and Defense | |||

| Healthcare Facilities | |||

| Industrial and Manufacturing | |||

| Retail and Malls | |||

| Enterprises and Commercial Buildings | |||

| Residential / Smart Homes | |||

| Education Campuses | |||

| Hospitality and Leisure | |||

| Others | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| South America | Brazil | ||

| Argentina | |||

| Rest of South America | |||

| Europe | United Kingdom | ||

| Germany | |||

| France | |||

| Italy | |||

| Spain | |||

| Nordics (Denmark, Sweden, Norway) | |||

| Rest of Europe | |||

| Asia Pacific | China | ||

| Japan | |||

| India | |||

| South Korea | |||

| ASEAN | |||

| Australia | |||

| New Zealand | |||

| Rest of Asia Pacific | |||

| Middle East and Africa | Middle East | GCC | |

| Turkey | |||

| Israel | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Nigeria | |||

| Egypt | |||

| Rest of Africa | |||

Key Questions Answered in the Report

What is the current value of the security camera market?

The security camera market is valued at USD 16.23 billion in 2026 and is forecast to reach USD 34.58 billion by 2031.

Which technology segment leads the security camera market?

IP cameras account for 64.68% of 2025 revenue, highlighting the dominance of network-based surveillance.

Why are doorbell cameras growing so quickly?

Doorbell cameras pair security with convenience, integrate into smart-home platforms, and therefore show a 16.71% CAGR through 2031.

How do NDAA regulations influence vendor selection?

NDAA compliance restricts procurement of certain Chinese equipment, channeling demand toward vendors that meet stringent component-origin and cybersecurity criteria.

Which region is expanding the fastest?

The Middle East leads in growth with a projected 15.24% CAGR, catalyzed by mega-project investments that specify advanced, AI-enabled surveillance grids.

Page last updated on: