Physical Security Information Management Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 2.24 Billion |

| Market Size (2031) | USD 4.66 Billion |

| Growth Rate (2026 - 2031) | 15.85% CAGR |

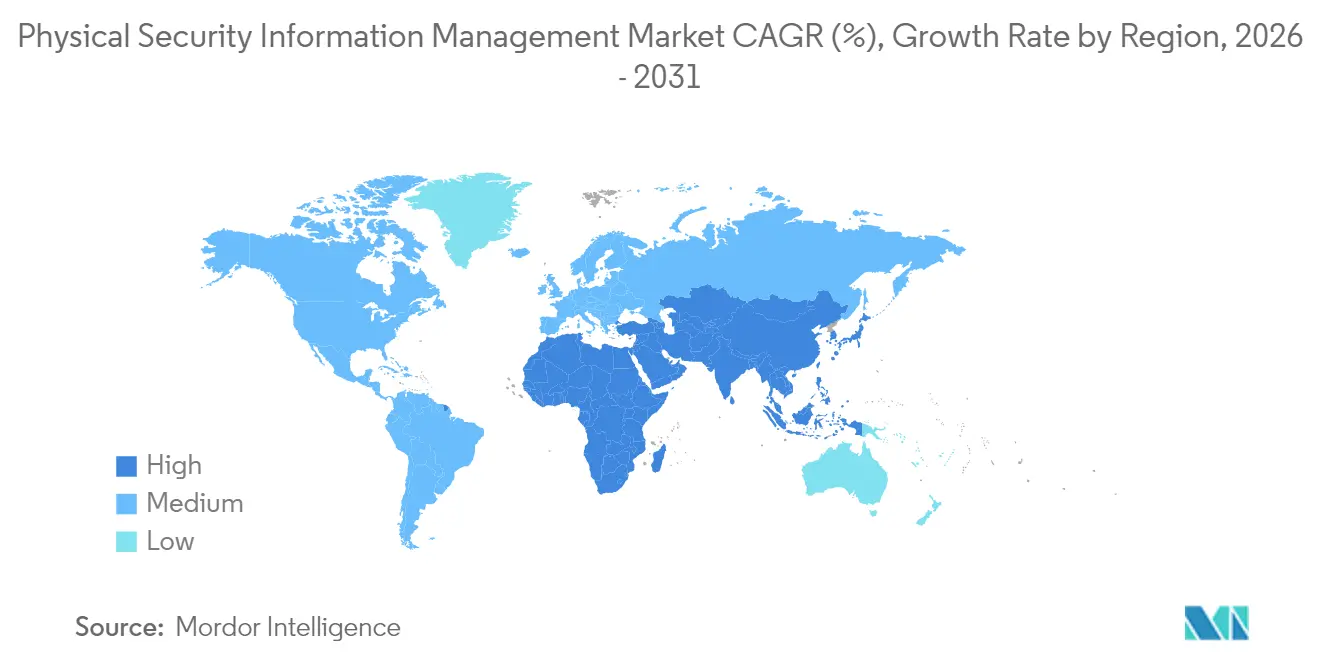

| Fastest Growing Market | Asia Pacific |

| Largest Market | Europe |

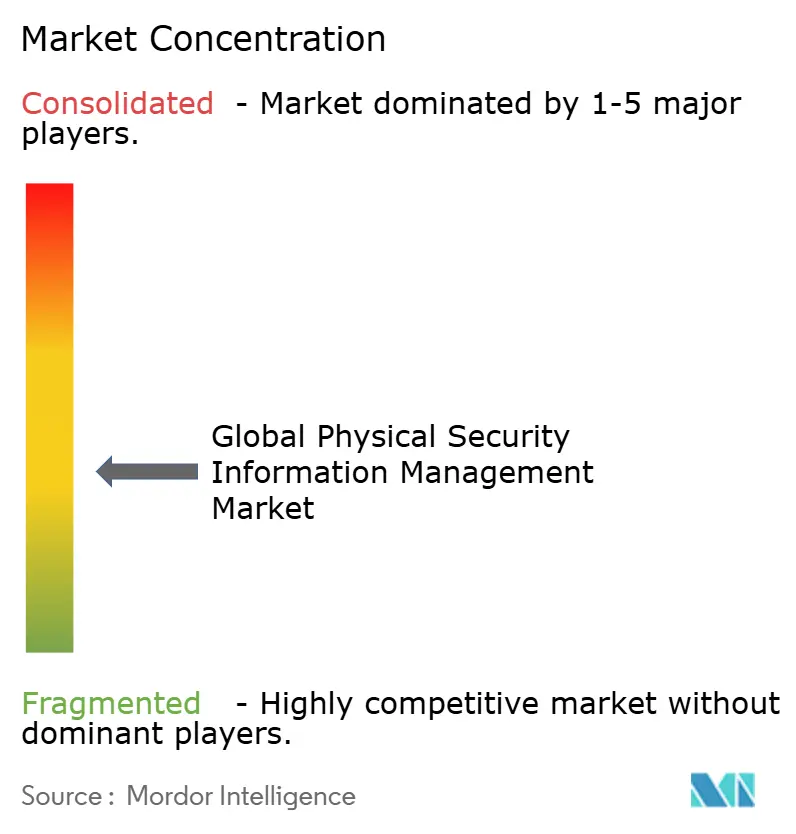

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Physical Security Information Management Market Analysis by Mordor Intelligence

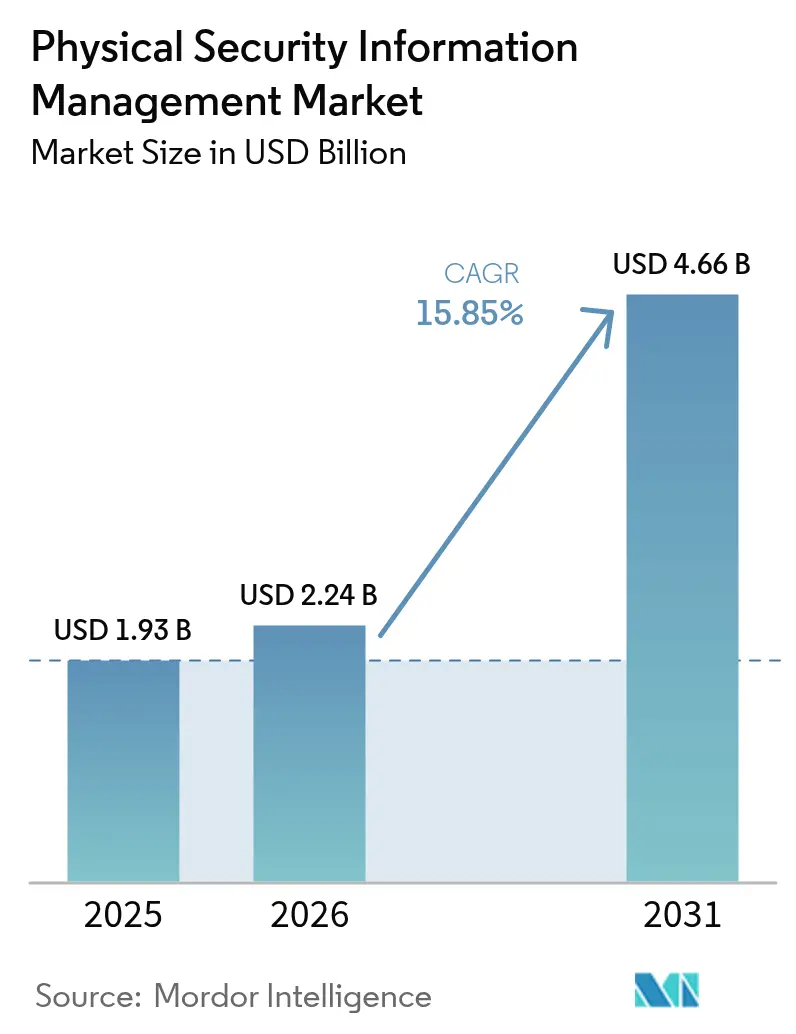

physical security information management market size in 2026 is estimated at USD 2.24 billion, growing from 2025 value of USD 1.93 billion with 2031 projections showing USD 4.66 billion, growing at 15.85% CAGR over 2026-2031. Rapid sensor proliferation, tighter regulations, and a pivot toward converged physical-cyber protection are reshaping capital allocation decisions, pushing chief security officers to prioritize unified command platforms. Demand is intensifying in transportation hubs, data-center campuses, and healthcare networks where diverse sensor estates, hybrid-work patterns, and liability exposures intersect. Vendors are responding with open orchestration layers, cloud-ready deployments, and subscription-based managed services that lower entry barriers while shortening deployment cycles. Competitive intensity is rising as established building-automation leaders, specialist PSIM providers, and public-cloud hyperscalers race to embed AI analytics, geospatial visualization, and workflow automation into a single operational picture.

Key Report Takeaways

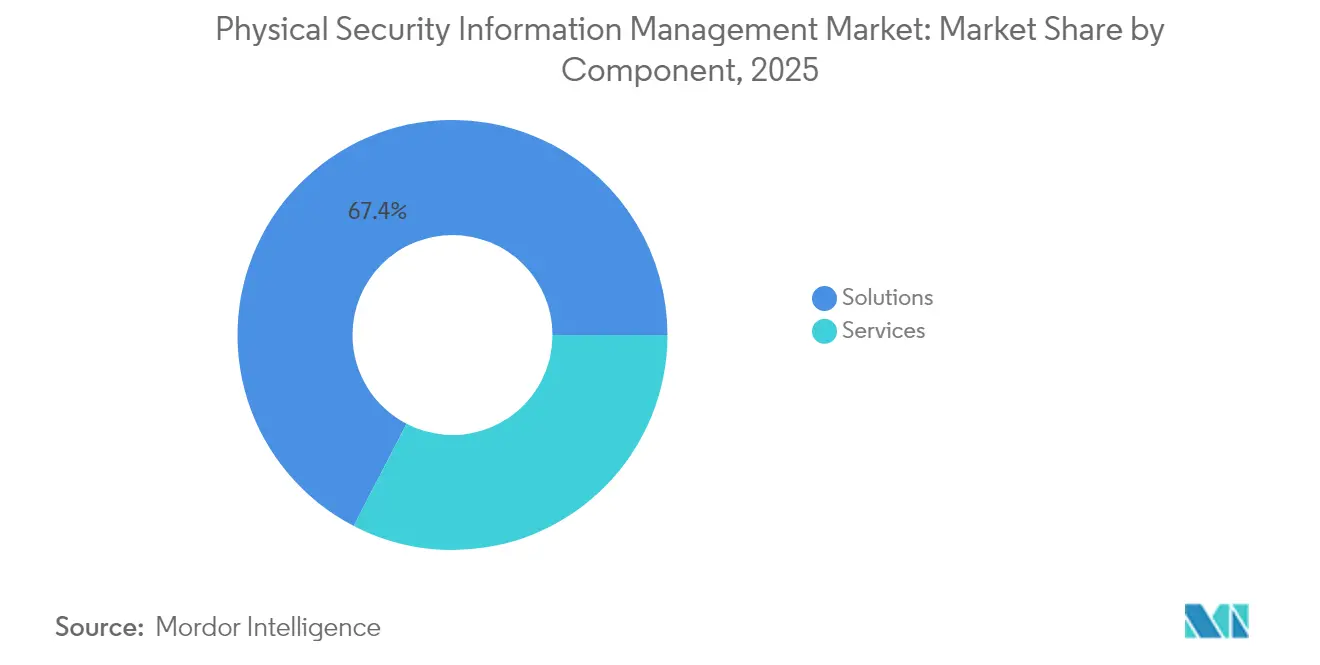

- By component, solutions accounted for 67.40% of the physical security information management market share in 2025; managed services are forecast to expand at a 16.25% CAGR to 2031.

- By deployment model, on-premise installations held 73.20% of the physical security information management market size in 2025, while cloud deployments are set to grow at an 17.55% CAGR through 2031.

- By end-user industry, transportation and logistics led with a 21.60% revenue share of the physical security information management market in 2025; healthcare is projected to accelerate at a 16.95% CAGR to 2031.

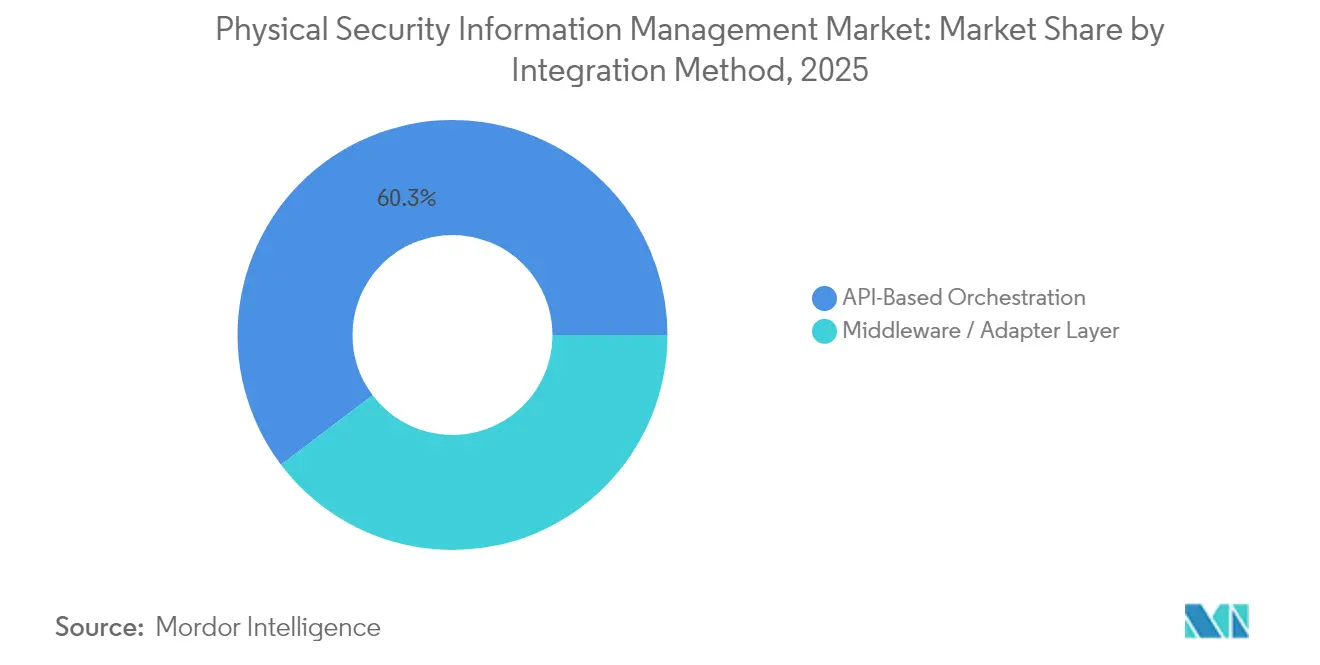

- By integration method, API-based Orchestration led with a 60.30% share of the physical security information management market in 2025; middleware/adapter layer is projected to accelerate at a 16.8% CAGR to 2031.

- By geography, North America captured 34.70% of the physical security information management market size in 2025, whereas Asia is poised to register the fastest 17.25% CAGR between 2026 and 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Physical Security Information Management Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Proliferation of IoT-enabled Edge Sensors Driving Unified Command Platforms | +2.8 % | Global, with concentration in North America & Europe | Medium term (~ 3-4 yrs) |

| EU NIS2 & U.S. CISA Critical-Infrastructure Mandates Accelerating Adoption | +3.5 % | Europe & North America | Short term (≤ 2 yrs) |

| Asian Mega-Transit Projects Requiring Centralised Situational Awareness | +2.1 % | Asia, with focus on China, India, Japan | Medium term (~ 3-4 yrs) |

| Rapid Uptake of AI Video-Analytics Creating Demand for Open PSIM Orchestration | +3.2 % | Global, led by North America | Medium term (~ 3-4 yrs) |

| Hybrid-Work Security Gaps Fueling Physical-Cyber Converged Solutions | +1.8 % | North America & Europe | Short term (≤ 2 yrs) |

| Insurance Premium Discounts Linked to PSIM Compliance for Data Centres | +1.5 % | North America, with emerging impact in Europe | Long term (≥ 5 yrs) |

| Source: Mordor Intelligence | |||

Proliferation of IoT-enabled Edge Sensors

A surge to 41.6 billion connected devices by 2025 is driving record volumes of telemetry that siloed tools cannot correlate. Critical facilities now juggle more than 500 heterogeneous sensors, a 43% jump since 2022, compelling operators to adopt vendor-agnostic orchestration engines that normalize metadata and prioritize alerts.[1]Security Informed, "How Is The Internet Of Things (IoT) Impacting Physical Security?", securityinformed.comOpen APIs have become a must-have procurement criterion as security managers seek future-proof integration paths for smart cameras, environmental probes, and biometric endpoints. Heightened data granularity is also improving root-cause analysis, allowing response teams to trace event chains and shorten mean time to resolution. The resulting operational gains are reinforcing the business case for next-generation platforms across energy, utilities, and smart-city programs.

EU NIS2 and U.S. CISA Critical-Infrastructure Mandates

Regulatory pressure now carries meaningful financial teeth: the revised NIS2 framework sets penalties up to EUR 10 million (USD 11.3 million) for non-compliance, while CISA’s CIRCIA rule enforces 24- to 72-hour reporting windows. Operators in power, transport, and healthcare sectors are therefore accelerating platform upgrades that automate incident documentation, evidence retention, and audit trails. Procurement teams favor solutions delivering out-of-the-box policy templates, role-based access, and encryption controls that align with European GDPR requirements. Early adopters in finance and pharmaceuticals report smoother board approvals once compliance automation is quantified against potential fines. Vendors with native policy-mapping engines and pre-built regulator dashboards are consequently widening their addressable base.

Rapid Uptake of AI Video-Analytics

Enterprises deploy an average of 3.7 discrete analytics engines ranging from facial recognition to behavior analysis, complicating event correlation across proprietary stacks. Open PSIM layers reduce custom middleware effort by 30-40%, enabling security directors to swap algorithms without forklift upgrades. Transportation authorities leverage object-detection feeds to automate platform evacuation alerts, while data-center operators combine anomaly detection with badge-access logs to flag insider threats. Scalable GPU resources in cloud environments further entice end users to offload computationally intensive models. This confluence of AI specialization and orchestration flexibility elevates integration depth to a board-level KPI for digital risk mitigation.

Asian Mega-Transit Projects

Regional governments have earmarked USD 1.7 trillion for new rail and metro systems, multiplying surveillance endpoints and interagency coordination needs. China’s 45 planned metro deployments and India’s USD 23 billion urban-transit outlay require platforms that support multi-modal workflows across rail, bus, and aviation networks. Geospatial dashboards that render sensor status atop dynamic transport maps help control-room supervisors triage incidents, minimizing service interruptions. Domestic system-integrator shortages, however, inflate project timelines, prompting operators to engage global consultancies with turnkey delivery models. Standard-based interoperability is thus rising on request-for-proposal scorecards to future-proof long-lifecycle projects.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Integration complexity with legacy systems | −2.1% | Europe, North America | Short term (≤ 2 years) |

| High up-front licensing and customization costs | −1.8% | Emerging markets | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Integration Complexity with Legacy Analog and Proprietary Systems

Industrial plants and transport hubs often rely on proprietary protocols first deployed 15-20 years ago, elevating data normalization challenges that extend implementation timelines by up to 60%. Adapter layers frequently struggle to translate low-bandwidth serial feeds into modern data schemas, forcing integrators to script custom converters that raise the total cost of ownership. Energy utilities face the sharpest hurdles where SCADA interfaces resist open API exposure. The resulting project overruns dent stakeholder confidence and slow rollouts in sectors where downtime tolerance is close to zero. Vendors offering pre-certified driver libraries and migration toolkits are therefore gaining a comparative advantage.[2]Advancis Software & Services GmbH, "Increase security and save costs with an open PSIM Platform.", securityworldmarket.com

High Up-front Licensing & Customisation Costs

Tier-1 implementations command USD 100,000–500,000 in core licensing, with complex sites seeing duplicate outlays for professional services. Mid-market hospitals and secondary airports struggle to align these sums with capital budgets, especially when qualitative benefits like situational awareness resist straight-line ROI calculations. Annual maintenance, often pegged at 15-20% of licence value, further pressures operating expenditure. Managed-services bundles that shift spending from capex to opex are mitigating the sticker shock, yet CFOs continue to demand transparent payback models tied to insurance-premium reductions or labor efficiencies. Vendors showcasing consumption-based pricing and outcome-linked contracts are widening funnel conversion rates in cost-sensitive geographies.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Component: Services Momentum Builds on Solutions Base

Solutions retained a 67.40% slice of the physical security information management market share in 2025, anchored by perpetual licences and subscription renewals for command-and-control software. The physical security information management market size generated by solutions is buoyed by critical infrastructure refresh cycles and feature expansions such as AI plug-ins and geospatial dashboards.

However, managed services are set to chart a 16.25% CAGR, a pace outstripping the core software line. Demand is strongest among organizations lacking in-house operators for 24/7 monitoring, incident triage, and threat-hunting routines. Service providers leverage multitenant architectures to amortize analyst teams across contracts, offering clients predictable monthly outlays and service-level guarantees. Professional services—consulting, design, and integration continue to underpin complex rollouts, particularly where legacy PLCs, fire-alarm panels, and building-management systems must be bridged. Vendor success increasingly hinges on bundling advisory and run operations into cohesive outcome-based packages that ease buyer concerns over skill shortages and long-term platform upkeep.

By Deployment Model: Cloud Growth Outpaces On-Premise Dominance

On-premise systems controlled 73.20% of the physical security information management market size in 2025 as operators in utilities, defense, and financial services favored data-sovereign, air-gapped installations. These environments often integrate directly with emergency intercoms, access gates, and industrial controls that demand millisecond latencies and deterministic network behavior.

Yet, cloud deployments will expand at an 17.55% CAGR, fueled by demand for elastic compute to run AI inference, centralized reporting across distributed estates, and simplified patch management. Early adopters leverage cloud video surveillance to offload storage costs, routing only event flags to local edge devices for rapid interdiction. Hybrid architectures are gaining traction where sensitive streams stay on-site while analytics dashboards and machine-learning pipelines reside in regional data centers.

By Integration Method: API-Centric Orchestration Gains Strategic Primacy

API-based Orchestration holds a 60.30% share in 2025. It is eclipsing custom middleware as the preferred integration path, cutting deployment effort by 30-40% and enabling modular swap-outs of subsystems without cascading failures. Modern platforms expose RESTful endpoints, WebSocket streams, and event-driven architectures that align with enterprise application-integration strategies. This design ethos simplifies the onboarding of emerging analytics engines, robotics patrol units, and environmental sensors, preserving investment longevity.

However, Middleware is the fastest-growing segment by 16.8% CAGR. Middleware adapters remain indispensable for analogue CCTV and proprietary badge panels that lack direct software hooks; however, their share in new contracts is contracting as capital planners accelerate IP refresh cycles. Consistency in data schemas is enhancing downstream analytics, allowing security operations centers to overlay incident heat maps, KPI dashboards, and SLA metrics atop homogenized event logs.

By End-User Industry: Transportation Anchors Volume, Healthcare Accelerates

Transportation and logistics held a 21.60% revenue share of the physical security information management market in 2025, reflecting heavy investment by airports, seaports, and rail networks seeking synchronized incident management across sprawling assets. Use cases increasingly extend to operational metrics such as dwell-time analysis and resource scheduling, deepening platform stickiness. Public-private funding models, coupled with national critical-infrastructure mandates, ensure a steady pipeline of terminal expansions that sustain vendor order books.

Healthcare will record a 16.95% CAGR to 2031 as hospitals contend with workplace violence, pharmaceutical theft, and patient-safety incidents. Multi-building campuses require coordination between infant-tracking tags, fire-alarm systems, and emergency-department access controls, elevating demand for unified situational awareness.

Geography Analysis

North America commanded 34.70% of global revenue for the physical security information management market in 2025, underpinned by federal critical-infrastructure mandates and mature systems-integration ecosystems. Insurance carriers offering 15–30% premium incentives for verifiable monitoring platforms further encourage adoption, especially among colocation data-center operators and regional utilities. Convergence of physical and cyber telemetry remains a strategic agenda, with 68% of chief security officers noting incident overlaps since 2023.

Asia is projected to expand at an 17.25% CAGR through 2031, propelled by USD 1.7 trillion in transit megaprojects and escalating smart-city deployments. Local authorities prioritize centralized situational awareness to coordinate multi-agency responses across metro lines, bus terminals, and airports. Vendor strategies increasingly incorporate joint ventures with domestic integrators to offset skill shortages and comply with procurement localization rules. Asia will eclipse North America in physical security information management market size within the next decade.

Europe’s growth trajectory is tightly linked to the enforcement timetable for the NIS2 Directive, which broadens compliance scope to thousands of essential and important entities. Security leaders are deploying platforms that automate incident reporting, evidence archiving, and role-based escalation to satisfy regulators. Preference for open standards is pronounced, reflecting diverse installed bases across member states. Sustainability is emerging as a procurement criterion, with PSIM rollouts expected to integrate energy-management insights and contribute to corporate ESG disclosures.

Regulatory Landscape

Regulation is increasingly influencing PSIM procurement as platforms become part of audited cyber-physical control environments. In the European Union, the Cyber Resilience Act (Regulation (EU) 2024/2847) extends security-by-design, vulnerability handling, and lifecycle support expectations to products with digital elements, shaping PSIM hardening, update practices, and the documentation demanded in critical sites and large enterprises. In the United States, federal control baselines such as NIST SP 800-53 Rev. 5 and guidance around PIV-enabled physical access control systems (E-PACS) continue to anchor requirements for access-control integration, identity assurance, and evidence-grade logging in government-aligned deployments.

Site-assurance and sector standards are also acting as gatekeepers for critical infrastructure deployments. The UK National Protective Security Authority (NPSA) Cyber Assurance of Physical Security Systems (CAPSS) evaluations provide an assurance pathway for physical security systems used in sensitive settings, reinforcing expectations around cybersecurity posture, resilience, and supply-chain assurance. In parallel, NFPA 3000 (2024 Edition) is increasingly referenced in U.S. facility security planning and incident preparedness, supporting demand for PSIM capabilities that handle coordinated workflows, incident documentation, and post-event reporting across multi-vendor estates.

Value Chain Analysis

The PSIM value chain begins with upstream security device and subsystem vendors (video surveillance, access control, intrusion detection, fire and building systems, and IoT sensors) that generate heterogeneous events and telemetry. Core PSIM software providers operate at the orchestration layer, where standardized event models, open APIs, and connector libraries shape integration speed and the ability to normalize data for command-and-control dashboards, case management, and audit trails. Implementation is typically delivered through system integrators and specialist consultants who carry out site assessment, design, connector configuration, workflow playbook mapping, and cybersecurity hardening, followed by validation in operational environments where degraded-mode handling and high availability are required.

Downstream, managed and support services increasingly drive ongoing value by providing 24/7 monitoring, incident triage, maintenance, and patching across distributed estates, particularly for transportation, government, and critical infrastructure operators. Partnerships between adjacent platform vendors also act as a channel enabler. For example, TKH Security and Nanodems (February 2025) announced a strategic partnership to integrate their VMS and PSIM software, illustrating how vendor-to-vendor interoperability agreements can reduce integration friction for buyers and speed up multi-product deployments.

Competitive Landscape

The physical security information management market exhibits moderate fragmentation, with diversified building-automation leaders, specialized PSIM vendors, and IT service providers vying for wallet share. Genetec, Johnson Controls, and Hexagon leverage entrenched customer relationships and global channel footprints to protect incumbency, bundling video-management and access-control suites into enterprise subscriptions. Boutique specialists such as Qognify and CNL Software differentiate through deep domain templates and rapid-integration toolkits that shorten time to value in transportation and healthcare verticals.

Strategic partnerships are accelerating product roadmaps and market access. CNL Software’s alliance with Cepton brings LiDAR-enabled 3D perimeter detection into its orchestration layer, strengthening value propositions for data-center and airport perimeters.[3]CNL Software, "CNL Software's IPSecurityCenter PSIM Software Provides Security Management for South African Hospital.", securityinformed.comCloud adoption is catalyzing collaboration between PSIM publishers and video-surveillance-as-a-service providers.

Investment priorities coalesce around AI augmentation and cloud-native architectures. Vendors are embedding real-time inference engines, automated playbooks, and predictive maintenance into baseline licences, creating upsell pathways into advanced analytics tiers. Simultaneously, migration to containerized microservices accelerates DevOps cycles, enabling fortnightly feature drops that keep pace with rapidly evolving threat landscapes.

Physical Security Information Management Industry Leaders

-

Johnson Controls International PLC

-

Genetec Inc.

-

Qognify Inc.

-

Verint Systems Inc.

-

Vidsys Inc.

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

Government-led standardization and large, formal procurements are creating whitespace for PSIM vendors that can document interoperability, cybersecurity controls, and resilience in mission-critical environments. In June 2026, the U.S. General Services Administration published ADM 3490.1, setting baseline minimum security standards for Video Surveillance Systems (VSS) and Intrusion Detection Systems (IDS) in federally owned facilities. This elevates the importance of centralized monitoring, evidence retention, and policy-aligned workflows across multi-site estates. Similarly, in April 2026 the U.S. Department of State issued a solicitation (19AQMM26N0033) seeking capability information for a globally deployed PSIM platform integrating enterprise VMS, access control, IDS, and 3D mapping with high-availability requirements (greater than 99.9% uptime). The solicitation points to demand for resilient architectures that support global operations and complex integration.

Technology and delivery opportunities are concentrating on modularity and data consistency rather than simple device connectivity. Buyers are prioritizing multi-vendor interoperability, standardized event models, and clear operational logic to reduce vendor lock-in and to incorporate edge analytics where latency and bandwidth constraints limit centralized processing. Vendors that can show local site autonomy (degraded-mode operations), governance-ready audit trails, and compliance alignment, including European cyber requirements and national certification regimes such as ANSSI in France, are better placed to convert regulated-sector demand into repeatable templates across transportation hubs, healthcare networks, and critical infrastructure campuses.

Recent Industry Developments

- March 2026: Johnson Controls unveiled next-generation access control and video solutions at ISC West 2026, expanding its portfolio for enterprise and commercial deployments. The releases strengthen end-to-end integration across intrusion, access, and video subsystems, improving the addressable integration surface for PSIM and unified command workflows in multi-site environments.

- February 2026: Genetec announced Cloudlink 2210, a cloud-managed appliance for enterprise-scale physical security deployments, with global shipping slated to begin in May 2026. The product direction supports hybrid architectures by bridging existing on-premise devices with cloud-managed operations, aligning with buyer demand for centralized management without full infrastructure replacement.

- March 2025: Google Cloud expanded its Risk Protection Program to 30 EMEA markets in partnership with Beazley and Chubb, tying insurance offerings to security deployments and risk controls. The move reinforced the role of verifiable monitoring, reporting, and control automation as procurement inputs, supporting PSIM adoption in regulated and risk-sensitive organizations.

Research Methodology Framework and Report Scope

Market Definition and Coverage

This market covers PSIM software platforms that connect physical security and related building systems, then bring events into one command interface for monitoring, correlation, response workflows, and reporting.

Scope exclusions: we exclude standalone hardware, pure video management systems, and standalone identity management software that is not sold as part of a PSIM platform.

Segmentation Overview

-

By Component

-

Solutions

- Video / Incident Management

- Access-Control Integration

- Command-and-Control Dashboards

- Case and Evidence Management

-

Services

- Professional (Consulting, Design and Integration)

- Managed and Support

-

Solutions

-

By Deployment Model

- On-premise

- Cloud

- Hybrid

-

By Integration Method

- API-Based Orchestration

- Middleware / Adapter Layer

-

By End-user Industry

- BFSI

- Government and Defense

-

Transportation and Logistics

- Airports

- Maritime Ports

- Rail and Metro

- Energy and Utilities

- Retail

- Healthcare

- Manufacturing and Industrial

- Education

- IT and Telecom

-

By Geography

-

North America

- United States

- Canada

- Mexico

-

South America

- Brazil

- Argentina

- Rest of South America

-

APAC

- China

- India

- Japan

- South Korea

- Australia

- New Zealand

- Rest of APAC

-

Europe

- Germany

- United Kingdom

- France

- Italy

- Nordics

- Rest of Europe

-

Middle East and Africa

- Saudi Arabia

- UAE

- Turkey

- South Africa

- Rest of Middle East and Africa

-

North America

Data Sources, Market Sizing, and Validation

Desk Research

Desk research was used to set market boundaries and anchor assumptions that were later tested in interviews. We reviewed public sources such as U.S. DHS and NIST guidance, FBI and BJS public safety statistics, transport and aviation security rules where relevant, and standards bodies that influence physical security system interoperability.

We also leaned on company filings, investor presentations, tender portals, and trusted press to understand buying cycles, typical deployment patterns, and how PSIM is packaged with services. In a few cases, we used paid subscriptions for company financials and news intelligence, patent databases to track product direction, and contracts and tenders databases to spot larger command center projects and refresh timing. These examples are not exhaustive, and many other sources were checked to collect data, validate assumptions, and clarify open questions.

Primary Interviews and Surveys

Primary work focused on interviews and short surveys with PSIM buyers, system integrators, and product and delivery leaders who handle platform deployments and renewals. Respondent input was used to confirm what gets counted as PSIM revenue (license, subscription, embedded analytics, and tightly bundled configuration services), and to pressure-test regional momentum across APAC, EMEA, and the Americas before finalizing the model.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 32% | CXOs: 13% | APAC: 51% |

| Mid tier: 48% | Functional/Unit leaders: 35% | EMEA: 29% |

| Smaller Players: 20% | Managers: 52% | Americas: 20% |

Market-Sizing & Forecasting

Sizing starts with a top-down build that reconstructs the addressable PSIM demand pool from physical security software spend signals and the share of sites that need multi-system event correlation, followed by regional adoption checks. Once the high-level number is formed, we corroborate it with selective bottom-up approximations, such as sampled deal sizes from integrator channel checks, typical license or subscription levels for command centers, and a sanity roll-up of supplier revenue where disclosures allow it.

Key inputs that move the model include the installed base of video surveillance and access control systems being unified, the pace of upgrades toward centralized command centers, cloud versus on-premises preference, average platform pricing progression (license to subscription mix), and the share of projects tied to critical infrastructure and transportation hubs. Where data is patchy, gaps are handled through ranges that are narrowed using interview feedback, then rechecked against procurement patterns and implementation timelines.

For the forecast, we use scenario analysis with a central case guided by how fast large sites standardize workflows, how procurement cycles shorten or extend, and how subscription mix increases over time. Scenarios are then adjusted by region based on local digitization pace and program funding visibility shared by primary respondents.

Data Validation & Update Cycle

Results are validated through triangulation across independent signals, including vendor commentary, tender activity, and implied volumes of large command center deployments. Outliers are flagged when growth rates or pricing assumptions drift away from what interviewees described, and those points are reviewed again before sign-off.

A multi-step review is followed, where another analyst checks scope rules, math, and whether inputs align with known adoption patterns. If a key assumption changes or a gap remains material, we re-contact sources to close it. Reports are refreshed annually, with interim updates when major events affect budgets, regulations, or deployment timing, and a final freshness pass is completed right before delivery.

Mordor Intelligence's Physical Security Information Management Market Size Compared Against Other Published Estimates

Published PSIM market values often differ because teams draw the line around different revenue items and then apply different adoption speeds to large-site deployments. Differences also show up when the base year is not the same, or when currency conversion timing and inflation handling are not stated clearly.

The main gap comes from whether adjacent platforms like standalone VMS and identity tools are blended into the total. Mordor Intelligence counts PSIM only when the platform is the event-correlation and command layer and the related services are inseparable from the platform contract. Another driver is how fast subscriptions are assumed to replace licenses, which can lift the forecast quickly if renewal uplift is applied without checks against procurement cycles and implementation lead times.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 2.24 B (2026) | |

| Global Consultancy A | USD 3.72 B (2024) | Uses a different base year and appears to count a wider smart city program scope, which can pull in adjacent software and project services beyond the PSIM command layer. |

| Industry Dataset B | USD 4.86 B (2024) | Reported under a broader physical security systems context, which can inflate totals when PSIM is grouped with neighboring system software categories and not separated by platform function. |

The spread in the table is mainly explained by scope breadth and year alignment rather than simple math differences. By keeping revenue tied to PSIM platform functionality, and by checking adoption and pricing assumptions against buyer and integrator feedback, the sizing steps stay traceable and repeatable for future updates.

Key Questions Answered in the Report

What is driving the strong growth of the physical security information management market?

Unified sensor orchestration, stricter regulatory mandates, and AI-enabled analytics are persuading operators to replace siloed tools with integrated command platforms that improve compliance and risk mitigation.

Which region will grow fastest between 2026 and 2031?

Asia is forecast to register an 17.25% CAGR, buoyed by USD 1.7 trillion in transport infrastructure projects and expansive smart-city programs.

Why are managed services gaining traction within the physical security information management industry?

Organizations lacking 24/7 security operations centers outsource monitoring and incident response to service providers, exchanging high capital outlays for predictable operating expenses.

How are new regulations influencing platform adoption?

Frameworks such as the EU NIS2 Directive and U.S. CISA mandates impose steep penalties for non-compliance, prompting critical-infrastructure operators to deploy automated incident-documentation and reporting capabilities.

What challenges slow down PSIM deployments?

High up-front licensing fees and the need to integrate legacy analogue systems can extend project timelines by up to 60% and inflate costs by about 35%, particularly in mature facilities.

Page last updated on: