Personal Protective Equipment Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

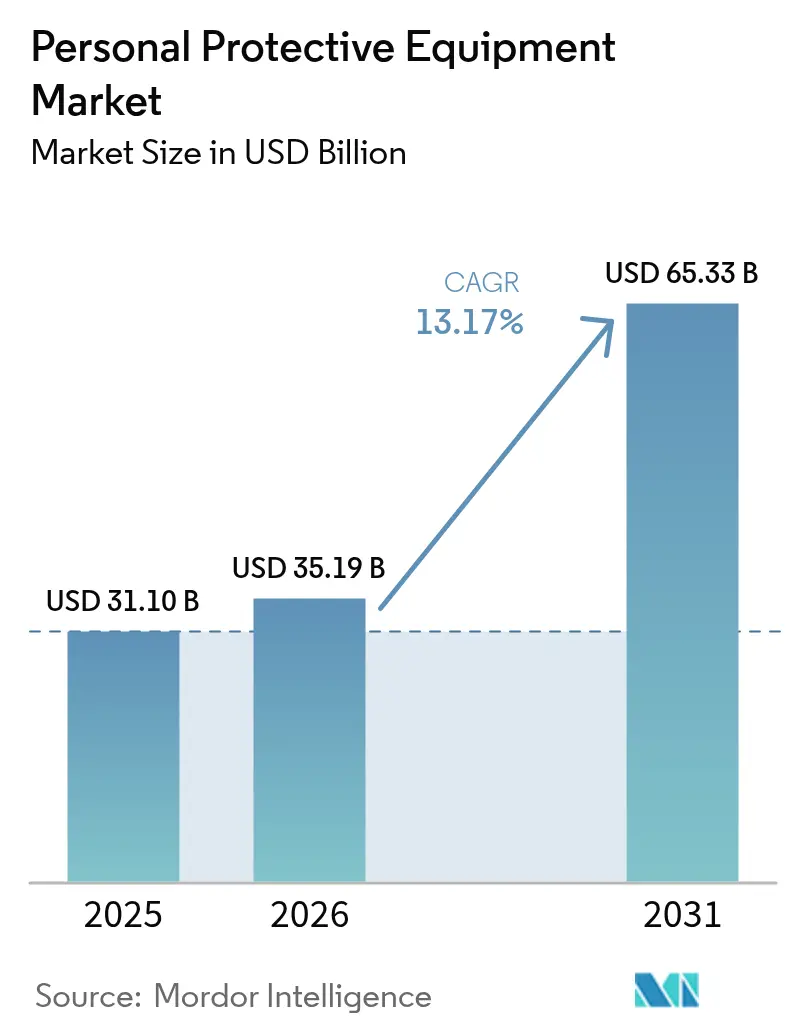

| Market Size (2026) | USD 35.19 Billion |

| Market Size (2031) | USD 65.33 Billion |

| Growth Rate (2026 - 2031) | 13.17% CAGR |

| Fastest Growing Market | Middle East |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Personal Protective Equipment Market Analysis by Mordor Intelligence

The personal protective equipment market size is expected to grow from USD 31.10 billion in 2025 to USD 35.19 billion in 2026 and is forecast to reach USD 65.33 billion by 2031 at 13.17% CAGR over 2026-2031. Continuous regulatory tightening, higher employer liability exposure, and a widespread corporate commitment to zero-harm cultures are propelling demand across both mature and emerging economies. Rapid miniaturisation of sensors, falling connectivity costs, and increased cloud analytics adoption are turning formerly passive gear into data-rich safety nodes, sharpening the value proposition beyond basic protection. Mounting sustainability expectations are reshaping material choices and lifecycle models, while consolidation among tier-one suppliers is realigning bargaining power across the value chain. Collectively, these forces position the personal protective equipment market for sustained double-digit expansion during the second half of the decade.

Key Report Takeaways

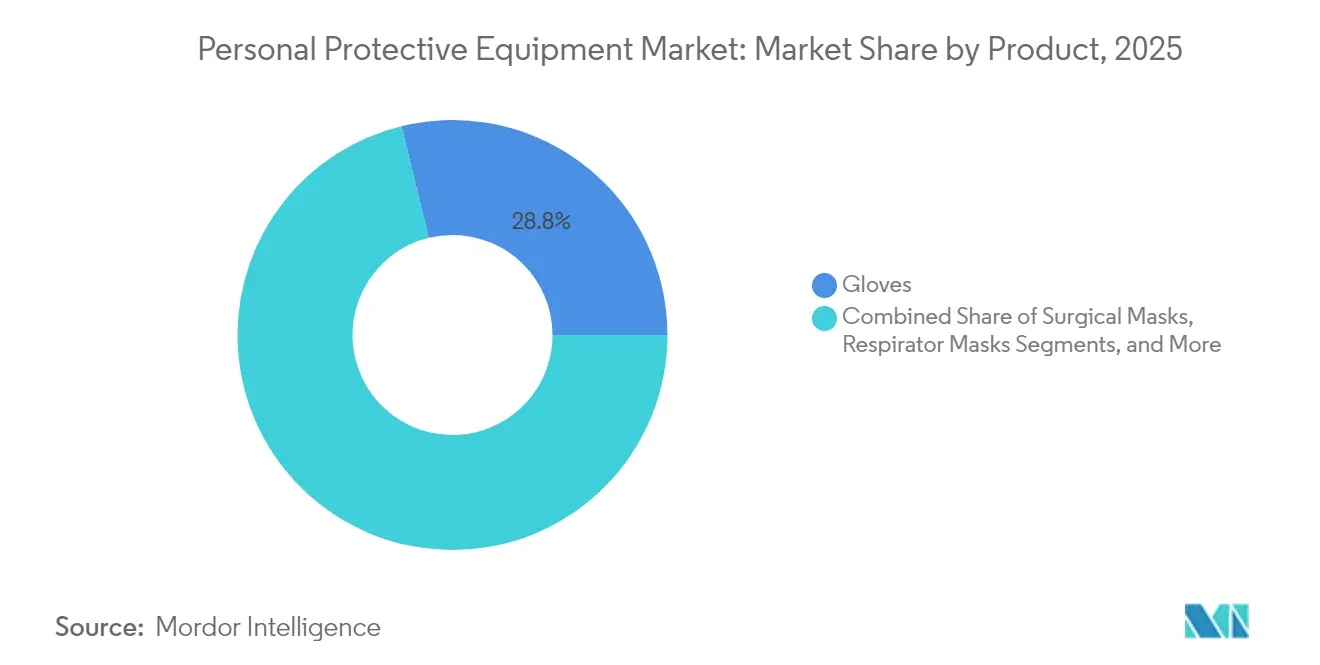

- By product category, Gloves led with 28.82% of personal protective equipment market share in 2025, while Respiratory Protection is set to expand at a 12.48% CAGR to 2031.

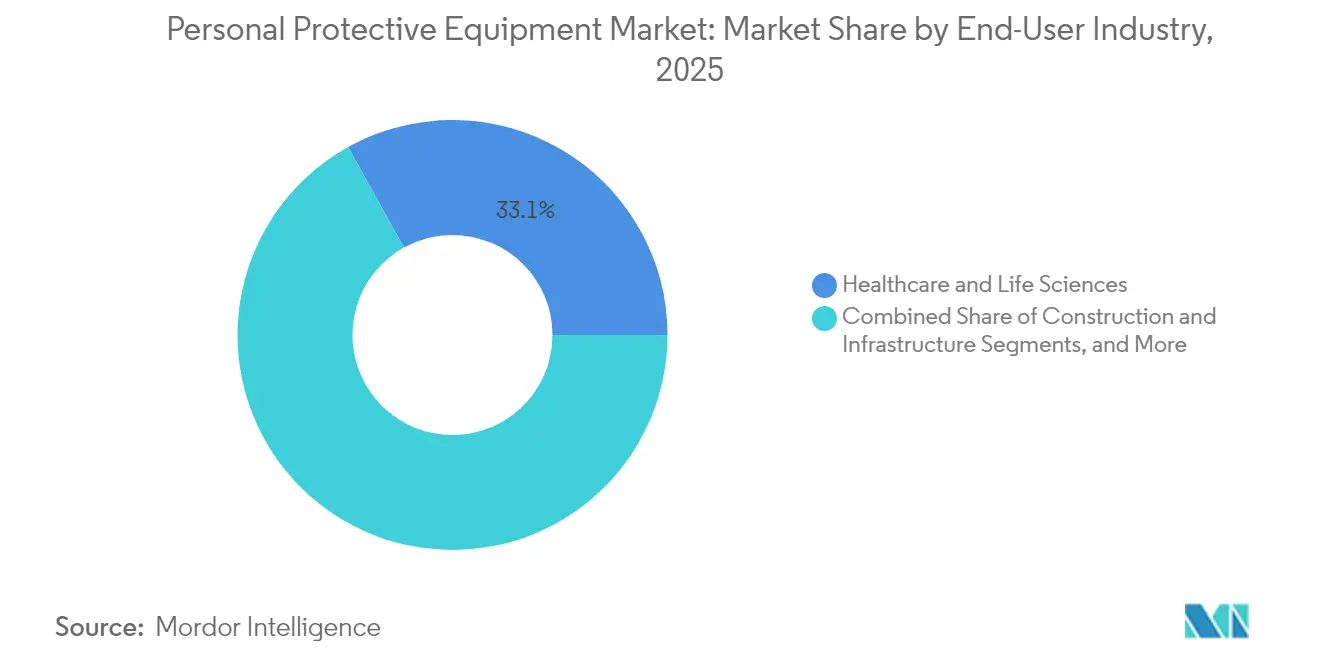

- By end-user industry, Healthcare and Life Sciences held 33.07% revenue share in 2025; Semiconductor Manufacturing registers the highest projected CAGR at 12.18% through 2031.

- By distribution channel, Direct Institutional Contracts controlled 46.45% of the personal protective equipment market size in 2025, whereas E-commerce and Digital Marketplaces are advancing at a 14.90% CAGR.

- By geography, Asia-Pacific commanded 39.05% of the personal protective equipment market size in 2025; the Middle East is forecast to grow the fastest at a 13.86% CAGR between 2026 and 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Personal Protective Equipment Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Accelerated Workplace-Safety Mandates in Asian Manufacturing Hubs | +3.10% | Asia, with spillover effects in North America and Europe | Medium term (2-4 years) |

| Stricter EU Ecodesign and Circularity Rules for Disposable PPE | +2.40% | Europe, with global supply chain implications | Long term (≥ 4 years) |

| Rapid Digitalisation of Industrial PPE Procurement via B2B Marketplaces in North America | +2.00% | North America, with gradual adoption in Europe and Asia | Short term (≤ 2 years) |

| Integration of IoT-Enabled Smart PPE for Real-Time Worker Monitoring in Oil and Gas | +1.60% | Global, with early adoption in North America and Middle East | Medium term (2-4 years) |

| Boom in Clean-Room Expansion for Semiconductor Fabs (Respiratory and Garment Demand) | +1.30% | Asia and North America, with emerging presence in Europe | Medium term (2-4 years) |

| Defence Modernisation Programs Driving Military-Grade Ballistic PPE in Middle East | +1.10% | Middle East, with spillover to North America and Europe | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Accelerated workplace-safety mandates in Asian manufacturing hubs

China’s updated Work Safety Law obliges high-risk sectors to deploy connected PPE that streams exposure data in real time, boosting premium-grade demand across the region [1]National Institute of Standards and Technology, “Health and Safety in the Semiconductor Industry,” nist.gov. India’s Occupational Safety, Health and Working Conditions Code is generating similar momentum, prompting Mallcom to invest INR 100 crore (USD 12 million) to expand domestic capacity. Local suppliers are therefore pivoting from low-cost competition toward performance differentiation, raising average selling prices and tightening compliance across supply chains.

Stricter EU ecodesign and circularity rules for disposable PPE

The EU’s new Extended Producer Responsibility schemes force manufacturers to finance end-of-life collection and recycling of masks and gloves, accelerating R&D in biodegradable polymers. Early pilot programs have recovered up to 60% of materials in single-use categories, turning compliance into a branding advantage for companies such as UVEX and 3M Deutschland.

Rapid digitalisation of industrial PPE procurement via B2B marketplaces in North America

Specialised online exchanges now shorten the quotation-to-order cycle from days to minutes, with industry revenues from GPO-mediated e-sourcing reaching USD 6.3 billion in 2024. Visual-commerce tools, including 3-D configurators, cut product-return rates by enabling virtual fit checks before purchase.

Integration of IoT-enabled smart PPE for real-time worker monitoring in oil and gas

Connected gas detectors and exoskeletons have reduced heat-stress incidents by 25% and musculoskeletal injuries by 20% in pilot programs [2]Source: Ezekiel Smart et al., “Smart PPE and Wearable Technology for Enhancing Worker Safety in the Oil and Gas Industry,” irejournals.com. Devices such as the Blackline Safety G7 feed telemetry into predictive-analytics platforms that alert supervisors before hazardous thresholds are breached.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Environmental Push-back on Single-Use Synthetic Polymers in Europe | -1.90% | Europe, with growing influence in North America | Long term (≥ 4 years) |

| Volatile Nitrile and Latex Prices Disrupting Glove Supply Economics | -1.50% | Global, with highest impact in Asia | Short term (≤ 2 years) |

| Compliance Fatigue Among SMEs in Emerging Markets | -1.20% | Asia, Africa, South America | Medium term (2-4 years) |

| Fragmented Certification Standards Hindering Cross-border Trade | -0.90% | Global, with particular impact on emerging markets | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Environmental Push-Back on Single-Use Synthetic Polymers in Europe

Healthcare alone has doubled disposable PPE use since 2005, amplifying landfill pressures and carbon footprints. Advocacy groups now spotlight the climate impact of petro-chemical gloves and masks, prompting hospitals to insert sustainability clauses into tender documents. Alternatives such as bio-based polyhydroxyalkanoate gloves are promising but still cost a premium and struggle to meet stringent filtration or tensile requirements. Manufacturers therefore face a profitability squeeze as they pursue parallel R&D paths while maintaining current production lines to satisfy mandatory performance standards. The net effect is a medium-to-long-term drag on margin expansion, particularly for firms heavily weighted toward high-volume disposables.

Volatile Nitrile and Latex Prices Disrupting Glove Supply Economics

Spot nitrile prices swung more than 150% over the past 18 months, ripping through contract negotiations and exposing smaller converters to working-capital stress. Healthcare providers reported procurement spikes of 200–300% during the worst tightness, forcing some to ration usage. Asian producers, which supply the bulk of global volume, faced energy-cost surges and shipping bottlenecks, reinforcing price gyrations. Larger brands are responding with multi-region feed-stock strategies and forward-buy hedges, yet the unpredictability still erodes forecasting accuracy and clouds investment timing for additional lines.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product: Smart technology transforms respiratory protection

Respiratory Protection is projected to grow at a 12.48% CAGR through 2031, powered by smart filters with embedded biometric sensors that warn users of abnormal breathing patterns. Gloves retained 28.82% personal protective equipment market share in 2025, supported by cut-resistant fibres and touchscreen-compatible coatings that suit digital shop-floor workflows.

Design improvements now emphasise breathability and weight reduction; Johns Hopkins experts recommend investment in reusable elastomeric respirators to replace legacy single-use models. As buyers evaluate gear on lifecycle cost rather than ticket price, premium variants-often IoT-enabled-are gaining shelf space across institutional and e-commerce channels.

By End-User Industry: Semiconductor expansion drives specialised demand

Semiconductor fabs are forecast to expand PPE outlays at a 12.18% CAGR to 2031, reflecting the build-out of globally subsidised chip capacity and stringent cleanroom standards. Healthcare and Life Sciences held 33.07% revenue in 2025 and remains the baseline volume anchor for masks, gowns, and examination gloves.

Oil and gas operators deploying real-time monitoring harnesses have cut overall accident rates by 40%, demonstrating quantifiable ROI that accelerates C-suite approval for premium gear. Food processors seek PPE that balances cut resistance with low linting to avoid foreign-material recalls, while defence agencies demand multi-threat ensembles that withstand flame, chemicals, and ballistics in a single configuration .

By Distribution Channel: Digital Platforms Revolutionise Procurement

E-commerce and digital marketplaces are scaling at a 14.90% CAGR, the highest among channels, as safety officers embrace self-service portals that integrate into enterprise resource-planning stacks. The personal protective equipment market size transacted through online specialist platforms is expected to exceed USD 13.24 billion by 2031, doubling its 2025 baseline. Direct Institutional Contracts nevertheless retain 46.45% share due to locked-in service agreements and bundled training offerings.

Industrial distributors are counter-punching against online erosion by embedding safety consultancy, on-site vending machines, and vendor-managed inventory into their value propositions. Visual-commerce toolkits, including 3-D fit checks, are shortening sampling cycles, a critical advantage when lead times for some custom gloves stretch beyond 12 weeks. Retail DIY channels service small contractors and a swelling consumer cohort more attuned to personal safety in home workshops, yet remain peripheral to enterprise-scale PPE flows.

Geography Analysis

Asia-Pacific held 39.05% of the personal protective equipment market in 2025, underwritten by its outsized manufacturing footprint and expanding construction pipeline. China’s chemical, electronics, and ship-building clusters drive bulk orders, while India’s medical-device sector is on track to reach USD 20.51 billion by 2029, boosting domestic demand for cleanroom-grade consumables. Governments are scaling fiscal incentives for local PPE production, reducing import dependence and enhancing supply-chain resilience.

North America maintains a robust position characterised by stringent OSHA oversight and early adoption of smart PPE in oil and gas and healthcare. Federal funding for semiconductor expansion is set to lift demand for contamination-control garments, reinforcing the region’s premium-product bias. Europe’s market is pivoting toward eco-compliance, with circularity deadlines pressuring suppliers to offer take-back schemes and recycled-content portfolios. These sustainability prerequisites act as soft trade barriers that encourage regional sourcing.

The Middle East is the fastest-growing pocket, forecast at a 13.86% CAGR to 2031 on the back of USD 2 trillion worth of mega-projects across Saudi Arabia and the UAE. National regulations now require internationally certified PPE for site workers, opening avenues for premium brands. South America exhibits uneven adoption; Brazil is raising enforcement after high-profile industrial incidents, while fiscal constraints temper acceleration elsewhere. Africa presents a long-horizon opportunity: industrialisation and mining expansion are stepping up enforcement of safety codes, yet supply chains remain nascent, favouring first movers able to localise last-mile distribution.

Competitive Landscape

The competitive arena is moderately consolidated, with the top five suppliers controlling roughly 40% of global revenue. Protective Industrial Products’ USD 1.325 billion acquisition of Honeywell’s PPE division augmented its head-to-toe portfolio and deepened its exposure to high-margin respiratory lines. Kimberly-Clark’s USD 640 million divestiture of its professional-grade unit to Ansell signals a sharpening strategy around core consumer franchises, while granting Ansell greater cleanroom leverage. Portfolio optimisation is the dominant theme as conglomerates shed non-core assets and specialist players scale through targeted bolt-ons.

Differentiation is shifting from unit cost to data-enabled services and circular credentials. Smart-helmet producers now bundle subscription-based analytics dashboards that visualise compliance metrics, anchoring sticky recurring revenue. Material innovators are exploring graphene-infused fabrics with superior cut resistance at lower weight, positioning against commoditised aramids. Industry-association conformity protocols such as ANSI/ISEA 125-2014 raise the documentation bar, advantaging firms with end-to-end quality management and in-house testing labs.

White-space opportunities reside in closed-loop collection for high-volume consumables and in industry-specific niches such as battery-cell production, which requires dual chemical and antistatic protection. Barriers to entry are rising as regulatory filings, fit-testing data, and cyber-security certifications inflate compliance budgets. Consequently, small-cap innovators frequently pursue licensing or joint development with tier-ones rather than stand-alone scale-ups.

Personal Protective Equipment Industry Leaders

3M Company

Honeywell International Inc.

Ansell Ltd

DuPont de Nemours Inc.

Kimberly-Clark Corporation

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2025: Honeywell confirmed the mid-year closing timeline for the USD 1.325 billion sale of its PPE segment to Protective Industrial Products, reallocating capital toward aviation, automation, and energy-transition focus areas.

- March 2025: Techtronic Industries launched the MILWAUKEE BOLT Safety Helmet featuring integrated chip-ready accessory mounts, reinforcing its strategy to bundle ergonomic design with cross-platform modularity.

- February 2025: The American Society of Safety Professionals issued gender-specific fit guidelines, addressing latent safety gaps and enabling manufacturers to target the 30% of the industrial workforce now represented by women.

- January 2025: Kimberly-Clark finalised the USD 640 million transfer of its Kimtech cleanroom line to Ansell, sharpening category focus for both firms and broadening Ansell’s semiconductor exposure.

Global Personal Protective Equipment Market Report Scope

Personal protective equipment or PPE is referred to as equipment that is worn to minimize exposure to hazards causing workplace injuries and illnesses. These injuries or illnesses could arise from contact with varied chemical, electrical, mechanical, and radiological hazards, to name a few. The study characterized the market into products, such as Surgical Masks and N95 Respirators, Gloves, Suits or Coveralls, and Aprons.

The personal protective equipment market is segmented by product (surgical masks, respirator masks, gloves, suits or coveralls, aprons, and other products) and geography (North America, Europe, Asia Pacific, and Rest of World). The market sizes and forecasts regarding value (USD) for all the above segments are provided.

| Surgical Masks | |

| Respirator Masks | N-Series (N95, N99, N100) |

| P-Series (P95, P99, P100) | |

| R-Series (R95, R99, R100) | |

| FFP1 | |

| FFP2 | |

| FFP3 | |

| Gloves | Disposable (Latex) |

| Disposable (Nitrile) | |

| Industrial Re-usable | |

| Suits and Coveralls | |

| Aprons and Gowns | |

| Protective Eyewear and Face Shields | |

| Hearing Protection | Earplugs |

| Earmuffs | |

| Protective Footwear | Safety Shoes |

| Rubber Boots | |

| Helmets and Hard Hats | |

| Fall Protection | Harnesses and Lanyards |

| Fire-Resistant and Arc-Flash Clothing |

| Healthcare and Life Sciences |

| Manufacturing (Heavy and Light) |

| Construction and Infrastructure |

| Oil and Gas, Mining and Metals |

| Chemicals and Pharmaceuticals |

| Food and Beverage Processing |

| Transportation and Logistics |

| Military, Law Enforcement and Homeland Security |

| Direct Institutional Contracts |

| Industrial Distributors and Wholesalers |

| E-commerce and Digital Marketplaces |

| Retail (DIY and Hardware Stores) |

| North America | United States |

| Canada | |

| Mexico | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Europe | Germany |

| France | |

| United Kingdom | |

| Italy | |

| Spain | |

| Nordics (Sweden, Norway, Denmark, Finland, Iceland) | |

| Benelux (Netherlands, Belgium, Luxembourg) | |

| Central and Eastern Europe (Poland, Czech Republic, Russia, Others) | |

| Middle East and Africa | Saudi Arabia |

| United Arab Emirates | |

| Turkey | |

| South Africa | |

| Nigeria | |

| Kenya | |

| Rest of Middle East and Africa | |

| APAC | China |

| Japan | |

| India | |

| South Korea | |

| ASEAN-5 (Indonesia, Thailand, Malaysia, Vietnam, Philippines) | |

| Australia | |

| New Zealand | |

| Rest of APAC |

| By Product | Surgical Masks | |

| Respirator Masks | N-Series (N95, N99, N100) | |

| P-Series (P95, P99, P100) | ||

| R-Series (R95, R99, R100) | ||

| FFP1 | ||

| FFP2 | ||

| FFP3 | ||

| Gloves | Disposable (Latex) | |

| Disposable (Nitrile) | ||

| Industrial Re-usable | ||

| Suits and Coveralls | ||

| Aprons and Gowns | ||

| Protective Eyewear and Face Shields | ||

| Hearing Protection | Earplugs | |

| Earmuffs | ||

| Protective Footwear | Safety Shoes | |

| Rubber Boots | ||

| Helmets and Hard Hats | ||

| Fall Protection | Harnesses and Lanyards | |

| Fire-Resistant and Arc-Flash Clothing | ||

| By End-User Industry | Healthcare and Life Sciences | |

| Manufacturing (Heavy and Light) | ||

| Construction and Infrastructure | ||

| Oil and Gas, Mining and Metals | ||

| Chemicals and Pharmaceuticals | ||

| Food and Beverage Processing | ||

| Transportation and Logistics | ||

| Military, Law Enforcement and Homeland Security | ||

| By Distribution Channel | Direct Institutional Contracts | |

| Industrial Distributors and Wholesalers | ||

| E-commerce and Digital Marketplaces | ||

| Retail (DIY and Hardware Stores) | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | Germany | |

| France | ||

| United Kingdom | ||

| Italy | ||

| Spain | ||

| Nordics (Sweden, Norway, Denmark, Finland, Iceland) | ||

| Benelux (Netherlands, Belgium, Luxembourg) | ||

| Central and Eastern Europe (Poland, Czech Republic, Russia, Others) | ||

| Middle East and Africa | Saudi Arabia | |

| United Arab Emirates | ||

| Turkey | ||

| South Africa | ||

| Nigeria | ||

| Kenya | ||

| Rest of Middle East and Africa | ||

| APAC | China | |

| Japan | ||

| India | ||

| South Korea | ||

| ASEAN-5 (Indonesia, Thailand, Malaysia, Vietnam, Philippines) | ||

| Australia | ||

| New Zealand | ||

| Rest of APAC | ||

Key Questions Answered in the Report

What is the current value of the personal protective equipment market?

The personal protective equipment market stands at USD 35.19 billion in 2026 and is projected to reach USD 65.33 billion by 2031.

Which product segment is growing the fastest?

Respiratory Protection is the fastest-growing segment, expected to expand at a 12.48% CAGR through 2031 on the back of smart-filter innovations.

How significant is Asia in the global landscape?

Asia accounted for 39.05% of personal protective equipment market share in 2025, driven by large-scale manufacturing and stricter safety mandates.

Why are smart PPE solutions gaining traction?

Embedded sensors provide real-time monitoring that has proven to cut incidents by up to 25%, enabling predictive safety management and lowering insurance exposure.

Page last updated on: