Smart Mirror Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

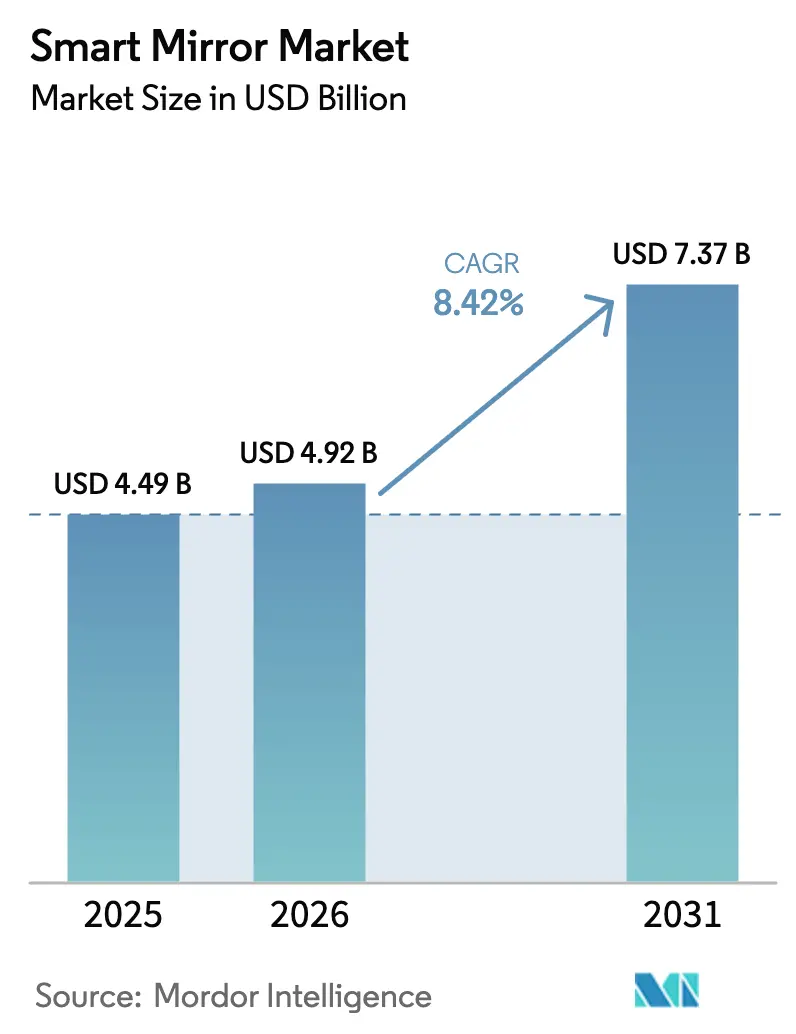

| Market Size (2026) | USD 4.92 Billion |

| Market Size (2031) | USD 7.37 Billion |

| Growth Rate (2026 - 2031) | 8.42% CAGR |

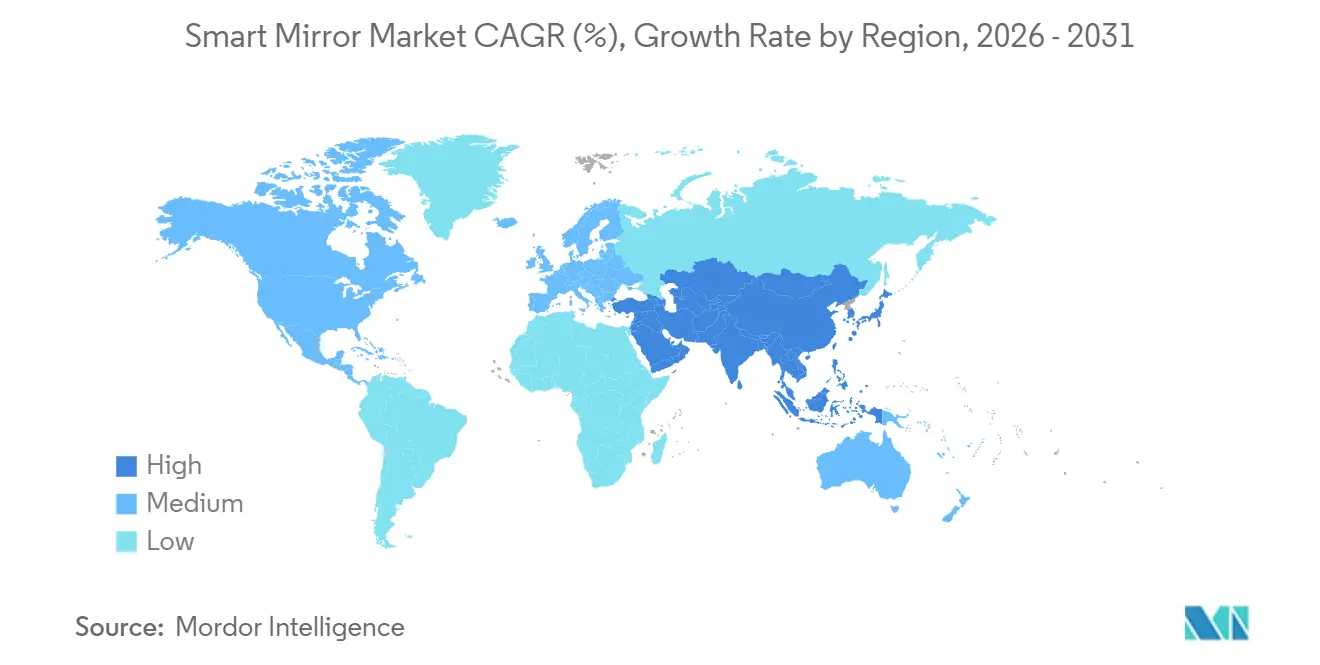

| Fastest Growing Market | Asia Pacific |

| Largest Market | Europe |

| Market Concentration | Medium |

Major Players*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Smart Mirror Market Analysis by Mordor Intelligence

The smart mirror market size is projected to expand from USD 4.49 billion in 2025 and USD 4.92 billion in 2026 to USD 7.37 billion by 2031, registering a CAGR of 8.42% between 2026 to 2031. This trajectory rests on five pillars: binding European camera-monitor regulations, AI-driven personalization that pushes mirrors beyond passive reflection, transparent OLED roadmaps that shrink thickness and power draw, hospitals’ embrace of reimbursable remote-monitoring hardware, and connected-retail pilots that lift conversion rates. Automotive OEMs equip heavy-duty trucks with digital rear-view systems that trim aerodynamic drag, while residential buyers warm to voice-activated bathroom mirrors that sync with smart-home platforms. Retailers justify capital outlays by measuring higher basket values in fitting rooms, and national R&D programs in South Korea and Japan de-risk the display supply chain. Cyber-security mandates and glass-substrate bottlenecks temper momentum, yet disciplined vertical integration by tier-one suppliers buffers near-term volatility.

Key Report Takeaways

- By application, automotive led with 41.89% revenue in 2025; healthcare is set to post the fastest 10.02% CAGR through 2031.

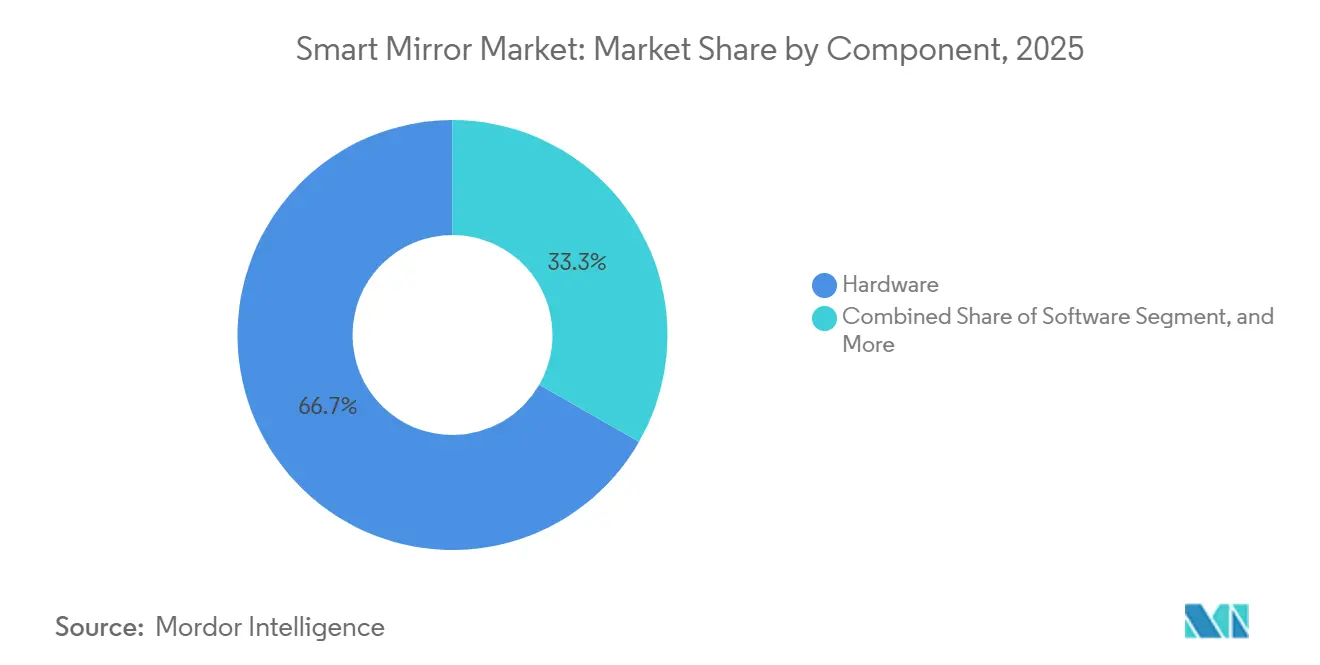

- By component, hardware captured 66.73% of 2025 sales, while services are forecast to rise at 9.61% CAGR to 2031.

- By display technology, liquid-crystal panels held 73.07% smart mirror market share in 2025, but OLED revenue will climb at 11.13% CAGR.

- By channel, business-to-business accounted for 81.21% of the 2025 smart mirror market size, yet business-to-consumer will expand at 12.27% CAGR through 2031.

- By region, Europe commanded 31.47% revenue in 2025, whereas Asia Pacific is on track for a 10.86% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Smart Mirror Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growing Adoption of Smart Mirrors in Automotive Sector | +2.1% | Europe and Asia Pacific core; spillover to Middle East commercial fleets | Medium term (2–4 years) |

| Rapid Integration of AI-Based Personalization Features | +1.8% | Global, with early gains in North America residential and Asia Pacific retail | Short term (≤ 2 years) |

| Expansion of Connected Retail Fitting-Room Solutions | +1.3% | North America and Europe luxury retail; ASEAN emerging | Medium term (2–4 years) |

| Rising Demand for Tele-health and Remote Patient Monitoring | +1.5% | North America and Europe aging demographics; Japan leading | Long term (≥ 4 years) |

| Government Mandates for Automotive Digital Rear-View Systems | +1.9% | Europe and Asia Pacific; North America pending NHTSA rulemaking | Short term (≤ 2 years) |

| Aging-in-Place Tech Driving Smart Bathroom Mirrors | +1.2% | North America and Europe; Japan and South Korea early adopters | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Growing Adoption of Smart Mirrors in Automotive Sector

Europe and Asia Pacific truck makers embraced camera-monitor systems after UN ECE R158 removed the legal need for physical mirrors, enabling Mercedes-Benz, Volvo, Scania, and MAN to equip more than 200,000 heavy-duty vehicles by 2025.[1]United Nations Economic Commission for Europe, “Regulation No. 158,” unece.org Hyundai and Kia embedded driver-state cameras in interior mirrors of new EV platforms to secure Euro NCAP five-star ratings.[2]Hyundai Motor Group, “Driver State Monitoring Systems,” hyundaimotorgroup.com Gentex’s 2025 Full Display Mirror fuses an OLED panel, rear-camera feed, and driver-monitoring into a single 12-inch unit, signaling a shift from discrete sensors to multifunction modules.[3]Gentex Corporation, “CES 2025 Full Display Mirror,” gentex.com Regulations accelerate adoption because aerodynamic drag falls 5% when external mirrors disappear, extending EV range without battery cost penalties. Suppliers consequently ramp dedicated production lines in Mexico and Poland, locking in three-year contracts with OEMs eager to differentiate cockpit UX.

Rapid Integration of AI-Based Personalization Features

Residential and retail units now package convolutional neural networks that grade skin hydration, detect fine lines, and recommend cosmetics, turning the mirror into a daily health advisor. CareOS’s BMind mirror won a 2024 CES Innovation Award for pairing mood tracking with guided breathing in hotel bathrooms. L’Oréal and ModiFace pilots in French department stores raised conversion by 30% as mirrors suggested shades proven to lift dwell time.[4]L’Oréal, “Annual Report 2024 – Digital Innovation,” loreal.com HiMirror’s new firmware references dermatology databases and offers teledermatology hand-offs when it detects suspicious moles. AI personalization widens addressable use cases, motivating vendors to ship monthly model updates via secure over-the-air channels. User opt-in rates exceed 70% when data never leaves the device, validating an edge-first architecture that satisfies stringent European privacy rules.

Expansion of Connected Retail Fitting-Room Solutions

Luxury chains struggle with online return rates hovering near 40%, and mirrors that identify garments with RFID tags now mitigate size uncertainty. Samsung demoed a retail setup at NRF 2024 where shoppers tapped a virtual button to request new sizes, cutting assistant wait time by 60%. Kohler-owned Oak Labs rolled out interactive mirrors at Neiman Marcus and Bloomingdale’s, letting customers dial lighting scenes, compare outfits side-by-side, and share looks with friends for real-time feedback. The EU Digital Services Act forces retailers to declare how video data is processed, so suppliers integrate on-device anonymization that strips faces before analytics. As pilot metrics show basket lifts of 15% and reduced returns, retailers earmark 2026 capex for chain-wide deployments, amplifying smart mirror market demand.

Rising Demand for Tele-health and Remote Patient Monitoring

CMS reimbursement codes since 2024 pay for devices that capture physiologic data at least 16 days per month, allowing mirrors with weight scales and blood-pressure cuffs to qualify as durable medical equipment. Japan’s health ministry fitted 500 senior-living facilities with fall-detection mirrors and cut ER visits 18% within a year. Vendors now pursue ISO 13485 certification to secure hospital tenders and open high-margin service contracts built around data analytics. Edge algorithms generate alerts for pulse irregularities and transmit coded summaries directly to electronic health records via FHIR APIs, slicing clinician review time by 30%. Hospital CIOs cite mirrors’ unobtrusive form factor, patients interact during daily grooming, as a key driver for chronic-care compliance.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Initial Cost and Limited Consumer Awareness | -1.4% | Global, acute in South America and Africa | Short term (≤ 2 years) |

| Cyber-Security and Data-Privacy Concerns | -1.1% | Europe and North America regulatory scrutiny; Asia Pacific emerging | Medium term (2–4 years) |

| Fragile Supply Chain for Specialized Display Glass | -0.8% | Global, concentrated in East Asia manufacturing hubs | Short term (≤ 2 years) |

| Regulatory Uncertainty on Camera-Enabled Mirrors | -0.7% | North America primary; Middle East and Africa secondary | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High Initial Cost and Limited Consumer Awareness

Residential smart mirrors retail between USD 800 and USD 3,000, far above a USD 150 conventional lit mirror, limiting penetration outside affluent households. A 2024 Deloitte poll found that only 22% of U.S. homeowners recognized “smart mirror,” and fewer than 5% cited a health benefit. Hotels such as Marriott and Hilton therefore deploy mirrors in premium suites to showcase benefits, collecting feedback that feeds cost-benefit analyses for broader rollouts. Bundled financing and buy-now-pay-later options on e-commerce platforms mitigate sticker shock, yet middle-income consumers remain hesitant until killer apps appear. Price compression hinges on OLED yield gains and commoditized edge AI chips due in 2027.

Cyber-Security and Data-Privacy Concerns

GDPR identifies biometric data as sensitive, forcing vendors to process facial geometry on-device and store only anonymized metrics. Pen-testing in 2024 showed 40% of consumer mirrors shipped with default admin passwords, triggering calls for security-by-design regulations. Gentex moved to a closed-loop design where driver-monitoring footage never leaves the mirror, outputting only alertness scores to the EC. ISO 27001 certification is emerging as a prerequisite for enterprise deals, inflating compliance costs for startups ISO.ORG. Retailers add privacy statements in fitting rooms, and vendors provide physical camera shutters to reassure shoppers, curbing data-breach fears that could derail the smart mirror market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Component: Services Monetization Accelerates

Hardware still delivered 66.73% of 2025 revenue, but services are on pace for a 9.61% CAGR to 2031 as platforms shift to SaaS licenses, cloud storage tiers, and premium analytics bundles. Gentex’s 2024 tie-up with Solace Systems introduced wireless power transfer and firmware updates that unlock high-definition recording and fatigue-prediction dashboards post-sale.[5]Gentex Corporation, “Solace Systems Partnership,” gentex.com Retailers rent AR try-on engines from ModiFace and Perfect Corp on a per-session basis, turning capital budgets into operating outlays. Tele-health mirrors integrate with EHR vendors through annual maintenance contracts that represent 35% of hospital project value. Services revenue also scales through privacy-centric data lakes that scrub identifiers yet reveal macro trends such as peak dressing-room occupancy, giving retailers actionable insights.

Hardware roadmaps prioritize slimmer bezels and glare suppression via edge-lit LEDs that cut energy draw 40%, advantages prized in hotel corridors where mirrors run 18 hours daily. Software teams focus on voice UI and conversational AI to enable hands-free selection of news feeds, lighting, and wellness content in humid bathrooms and vibrating cabs. Services differentiation flows from federated learning models that train on-device, update centrally, then redeploy, keeping sensitive frames local while enhancing algorithm accuracy. This pivot underpins recurring income crucial for investor valuations in the smart mirror market.

By End-User Application: Healthcare Outpaces Automotive Growth

Automotive dominated the 2025 smart mirror market size with 41.89% revenue as EU and Asia Pacific mandates triggered mass truck deployments. Yet healthcare mirrors will clock a 10.02% CAGR, propelled by CMS reimbursements and Japan’s aging-in-place policies. Retail follows as conversion-boost evidence grows, while residential adoption remains confined to luxury renovations exceeding USD 50,000 per bathroom. Hilton’s 2025 pilots in 12 properties showed 25% higher guest-satisfaction scores for smart-mirror rooms, prompting chain-wide assessments.

Hospitals demand ISO 13485 compliance, galvanic-skin sensors, and FHIR interoperability, extending sales cycles to 18 months but yielding multiyear support contracts. Automotive end users stress FMVSS 201 head-impact endurance and -40 °C thermal resilience. Retailers push for 99.5% uptime and remote diagnostics, whereas residential customers buy frames that match décor and pair with Apple HomeKit for unified control. Hospitality buyers negotiate five-year warranties and bundle smart mirrors with IPTV upgrades to capture economies of scale, thereby broadening the total contract value.

By Display Technology: OLED Gains on Thinness and Contrast

Liquid-crystal displays retained 73.07% of 2025 revenue due to cost and durability, yet OLED panels will surge at 11.13% CAGR as transparent models attain 60% transmittance by 2027, allowing mirrors to toggle seamlessly between reflection and video. Samsung Display invested in quantum-dot OLED lines compliant with AEC-Q100 automotive reliability, ensuring pixel stability under ultraviolet stress. MicroLED and electrophoretic displays fill niches where ultra-low power trumps cost, such as battery-powered camper mirrors.

OLED eliminates backlights, enabling curved, frameless designs that automotive stylists crave. Suppliers project BOM savings once yields climb past 85%, narrowing the cost delta with LCD to below USD 20 per square foot. Hybrid OLED-LCD architectures from Japan Display promise high brightness and deep blacks, targeting dashboards exposed to 100,000 lux sunlight. As flexible substrates mature, mirrors may wrap A-pillars to widen drivers’ fields of view, a concept in prototype at European test tracks.

By Sales Channel: B2C Emerges as Residential Adoption Climbs

Business-to-business accounted for 81.21% of 2025 sales because OEM, hotel, and retail contracts involve hundreds of units, but direct-to-consumer growth at 12.27% CAGR will reshape distribution by 2031. Amazon listings and Home Depot aisles now showcase voice-ready bathroom mirrors, and buy-now-pay-later plans trim upfront pain. OEM deals lock margin yet guarantee volume for six model-years, whereas B2C purchases are impulse-driven and see higher return rates if installation proves complex.

Customization defines B2B deals; hotels embed brand logos in idle screens, and retailers sync mirrors to POS systems for real-time stock checks. B2C brands counter with AR visualization apps that let homeowners preview mirrors in situ before purchase. Logistics partners now offer white-glove installation bundles that cut return rates by 20%. As AI features become table stakes, consumer channels gain negotiating power, nudging ASPs down and accelerating mainstream adoption of the smart mirror market.

Geography Analysis

Europe controlled 31.47% of 2025 revenue, anchored by Regulation 2019/2144 which mandated driver-drowsiness detection systems and propelled demand for interior cameras. Germany’s supply cluster houses Ficosa, Murakami, and Valeo, each feeding Volkswagen and BMW programs, while France’s Valeo spent EUR 200 million (USD 213 million) expanding camera module capacity.[6]Valeo, “Annual Report 2024,” valeo.com The UK mirrors UN ECE rules but with a 12-month lag, complicating pan-European homologation.

North America trails in automotive adoption because NHTSA still mandates physical exterior mirrors, yet residential and hospitality sales rise as smart-home spending climbs. Gentex runs a 500,000-square-foot Tijuana plant that ships duty-free under USMCA, curbing tariff risk. Mexico City hotels and boutique gyms pilot mirrors to differentiate guest wellness offerings, proving regional appetite beyond U.S. borders. South America and Africa remain early-stage due to price sensitivity, but pilot installs in São Paulo’s luxury condos and Cape Town’s spa resorts hint at future upside.

Asia Pacific’s 10.86% CAGR stems from China’s EV boom, South Korea’s display R&D grants, and Japan’s geriatrics-driven tele-health push. MOTIE labeled transparent displays a strategic industry in 2024 and funds joint projects between LG Display and Hyundai Mobis. India’s urban middle class buys voice assistants and seeks mirrors that sync with them, though tickets above USD 1,000 curb penetration.[7]India Brand Equity Foundation, “Smart Home Overview,” ibef.org Australia and New Zealand import mirrors from Asia and Europe, prioritizing 230-volt safety ratings and solar-friendly standby power.

Middle East buyers in the Gulf Cooperation Council outfit premium apartments with smart mirrors as part of smart-city visions, combining Arabic voice packs and sand-resistant coatings. Government housing initiatives in the UAE require mirrors to integrate at the protocol layer with building energy-management systems, ensuring compliance with net-zero goals.

Regulatory Landscape

Smart mirrors operate across automotive safety rules, consumer-electronics conformity, and privacy requirements. In automotive, UN/ECE rules for indirect vision devices (notably UN/ECE Regulation No. 46) support camera-monitor system adoption, while Europe is also expanding in-cabin sensing through Regulation (EU) 2019/2144 (linked to driver drowsiness and attention features that are frequently implemented via mirror-integrated cameras). In the United States, FMVSS No. 111 (49 CFR 571.111) continues to define rear-visibility requirements and remains a key constraint for camera-only exterior mirror replacements, keeping OEM programs and homologation pathways region-specific.

For residential, retail, hospitality, and healthcare deployments, market access depends on electrical safety and EMC compliance, alongside data-protection obligations. In the EEA, CE-marking typically requires meeting the Low Voltage Directive 2014/35/EU and EMC requirements aligned with standards such as EN 55032/EN 55035 and the IEC 61000 series; in the US, mirrors with wireless connectivity must meet FCC Part 15 requirements for RF emissions. When mirrors handle camera or biometric-derived data, GDPR obligations such as Data Protection by Design (Article 25) and UK IoT consent expectations (reinforced in the UK through PECR guidance) influence system architecture, including on-device processing, anonymization, and physical camera shutters in customer-facing deployments.

Value Chain Analysis

Upstream value creation concentrates in specialty glass (two-way mirror substrates and coatings), display modules (LCD and OLED, including transparent OLED roadmaps), and optical and sensing components such as cameras, microphones, proximity/motion sensors, and wireless modules. Display suppliers such as Samsung Display and LG Display shape availability and cost, and the market remains sensitive to bottlenecks in specialized display glass and to the qualification burden for automotive-grade components.

Midstream integration is driven by tier-one automotive suppliers and smart-mirror OEMs that combine glass, display, optics, compute, and enclosure design into certified assemblies, then differentiate through software, device management, and services. Players such as Gentex, Magna International, and Ficosa (Panasonic) anchor automotive programs where mirrors function as multi-purpose hubs (rear camera view plus driver and occupant monitoring behind the glass), and consolidation steps such as Gentex integrating VOXX capabilities reflect the shift toward vertically integrated cabin-experience stacks. Downstream, go-to-market strategies split between large B2B deployments (OEM, retail chains, hospitals, hotels) and expanding B2C channels that rely on installers, marketplaces, and smart-home platform compatibility; compliance testing, cybersecurity hardening, and OTA update operations increasingly sit alongside physical manufacturing as key nodes in the chain.

Competitive Landscape

The smart mirror market is moderately fragmented; automotive stalwarts Gentex and Magna International deliver integrated camera-mirror modules, whereas Electric Mirror, Séura, and CareOS innovate on design and wellness software. Gentex’s USD 196 million buyout of VOXX International bundled EyeLock iris-biometrics and high-fidelity audio into a holistic cabin-experience stack, widening its moat. Display giants LG Display and Samsung Display hold upstream bargaining power via transparent OLED panels, but reliance on tier-one integrators limits direct end-customer reach. Séura’s 2024 Smart TV Mirror hit 1,200 nits brightness, satisfying sunlit bathroom demands.[8]Séura, “Product Launches 2024,” seura.com

Startups differentiate with edge AI and privacy guarantees; CareOS’s BMind embeds guided breathing and sleep tracking, landing hotel partnerships that target wellness-conscious guests. Standards bodies SAE and ISO draft interoperability specs for camera-monitor systems, promising to harmonize interfaces and lower integration risk.[9]SAE International, “Camera Monitor Systems Roadmap,” sae.org Consolidation looms as services revenue overtakes hardware, incentivizing vertical mergers where software firms secure reliable hardware pipelines and vice versa.

Smart Mirror Industry Leaders

Gentex Corp.

Ficosa (Panasonic)

Magna International Inc.

Samsung Electronics Co., Ltd.

Japan Display Inc.

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

Healthcare-grade smart mirrors represent a clear whitespace where reimbursement, compliance, and interoperability weigh more than display form factor alone. Since 2024, CMS remote patient monitoring reimbursement codes that require physiologic data capture at least 16 days per month support mirror-based devices that bundle weight and blood-pressure peripherals, encouraging vendors to pursue ISO 13485 and FHIR-based integration with EHR workflows. This creates room for suppliers that package certified hardware with recurring service contracts (monitoring dashboards, alert routing, and maintenance), rather than relying on one-time mirror sales.

Retail and hospitality opportunities focus on operational metrics and privacy-by-design deployment models. Connected fitting-room pilots cited in-market, including Samsung demonstrations at NRF 2024 and Oak Labs rollouts at Neiman Marcus and Bloomingdale's, link smart mirrors to measurable outcomes such as reduced associate wait time and improved conversion. In Europe, data-handling disclosure requirements, including the EU Digital Services Act context, are pushing architectures toward anonymizing on-device before analytics. On the automotive side, supplier roadmaps that integrate rear-view, driver monitoring, and occupant monitoring behind the glass align with regulatory and safety-rating incentives, and recent OEM program awards for mirror-integrated camera architectures reinforce demand for scalable, software-updatable modules; the main opportunity sits with vendors that can industrialize secure OTA, meet automotive reliability standards, and manage multi-source constraints around specialized glass and advanced display panels.

Recent Industry Developments

- May 2026: Magna International announced it was awarded a driver and occupant monitoring system program with a European OEM, built around a mirror-integrated behind-the-glass camera architecture. The award underscores the shift of rearview mirrors into central safety and sensing modules, tightening integration between cabin monitoring software and optical hardware. It also strengthens Magna's position in platform-level supply relationships where multi-year vehicle programs drive volume and services attach.

- April 2026: Panasonic Holdings finalized its exit from the automotive device business by divesting its complete stake in Ficosa International S.A. to the founding family. The separation changes strategic control of a tier-one mirror and mechatronics supplier, with implications for investment priorities and partnership structures across camera-mirror and cockpit-electronics programs. It also signals continued portfolio reshaping among large electronics groups around capital intensity and margin profiles in automotive components.

- December 2024: Gentex completed its acquisition of VOXX International at USD 7.50 per share. The deal broadened Gentex's cabin-experience stack with added biometrics and audio-related capabilities that can be integrated into mirror-based modules. It also supports a more vertically integrated approach as smart mirrors evolve from discrete hardware into multi-sensor, software-managed platforms.

Research Methodology Framework and Report Scope

Market Definition and Coverage

This market covers smart mirrors that combine a reflective surface with an embedded display and connected electronics. In practice, these units are sold for both consumer settings and business installations, where digital content can be shown and interaction can be driven through sensors and software.

Scope exclusions: We exclude ordinary mirrors that do not provide connected display capability, and we also exclude adjacent smart home devices that are not integrated into a mirror form factor.

Segmentation Overview

- By Component

- Hardware

- Software

- Services

- By End-User Application

- Automotive

- Retail and Marketing

- Healthcare

- Residential

- Hospitality

- By Display Technology

- LCD

- OLED

- Other Display Technologies

- By Sales Channel

- Business-to-Business (B2B)

- Business-to-Consumer (B2C)

- By Geography

- North America

- United States

- Canada

- Mexico

- South America

- Brazil

- Argentina

- Rest of South America

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Russia

- Benelux

- Nordics

- Rest of Europe

- Asia-Pacific

- China

- India

- Japan

- South Korea

- ASEAN

- Australia and New Zealand

- Rest of Asia-Pacific

- Middle East

- GCC

- Turkey

- Israel

- Rest of Middle East

- Africa

- Egypt

- South Africa

- Rest of Africa

- North America

Data Sources, Market Sizing, and Validation

Desk Research

Desk research starts by building a clean picture of where smart mirrors are being adopted and what pushes shipments and pricing. For geography and trade context, we refer to public sources such as US Census and International Trade Administration releases, Eurostat trade and industry statistics, and UN Comtrade flows for mirrors and display related categories. We also pull standards and policy notes from bodies such as UNECE where automotive camera systems influence mirror substitution decisions.

Alongside these, we review company annual reports, earnings decks, product brochures, and reputable press to understand product positioning, channel focus, and typical price bands for different use cases. A paid subscription for company financials and intelligence is used selectively to normalize revenue splits and to reduce double counting across parent and subsidiary reporting. The sources listed here are illustrative only, since the final dataset is a mix of public and paid references used for data collection, validation, and follow up as questions came up.

Primary Interviews and Surveys

Primary work is used to pressure test assumptions that are not visible in public data, especially adoption rates by end use, realistic ASP movement, and the pace of feature upgrades (display type, connectivity, and sensing). We speak with stakeholders across manufacturing, distribution, installers, and large buyers in retail, automotive supply chains, hospitality, healthcare, and residential channels, then reconcile differences across regions so the final view stays consistent.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 28% | CXOs: 12% | APAC: 42% |

| Mid tier: 58% | Functional/Unit leaders: 43% | EMEA: 35% |

| Smaller Players: 14% | Managers: 45% | Americas: 23% |

Market-Sizing & Forecasting

Sizing starts with a top-down build where the demand pool is reconstructed by end-use adoption and replace cycles, and then converted into value using observed price bands and feature mix by region. Once the market total is formed, it is corroborated with selective bottom-up approximations like sampled vendor revenue ranges, channel checks with installers and distributors, and an ASP times volume sense check for key applications.

The model is most sensitive to penetration of smart mirrors in retail fitting rooms and in-store marketing, the share of connected bathroom mirrors within premium residential renovations, and automotive mirror substitution signals linked to camera-monitor adoption. We also track display technology mix shifts (LCD versus OLED), along with typical upgrade cycles that change unit value over time. Where bottom-up views have gaps, the missing portion is handled through conservative allocation tied to channel coverage and import intensity, then adjusted after expert feedback.

For forecasting, scenario analysis is used so that adoption and pricing can be flexed in a controlled way. Scenario weights are guided by what interviewees consider most realistic for procurement timing and consumer willingness to pay. The output is kept traceable so each major driver can be followed back to a clear assumption and updated without rebuilding the full model.

Data Validation & Update Cycle

Validation is done through a series of cross checks, where model results are compared against independent signals like trade direction, announced rollout programs, and price movement patterns observed in public catalogs. If a variance looks unusually high, we revisit the driver assumptions and recheck the arithmetic, then re-contact primary sources when needed to confirm whether the movement reflects real change or timing effects.

Before sign-off, the model and key assumptions go through multi-step analyst review so anomalies are questioned and resolved in writing. Reports are refreshed annually, with interim updates when material events happen, such as regulatory shifts that affect automotive use or step changes in display supply. Right before delivery, a fresh final pass is completed so clients receive the latest updated view.

Mordor Intelligence's Smart Mirror Market Estimate Compared With Other Published Estimates

Published smart mirror market values often do not match because firms draw the scope line differently, and they also apply different assumptions for adoption speed and pricing changes. The starting year, the treatment of automotive mirror substitution, and currency timing can all create large spreads in the final number.

The main gap comes from whether automotive display mirrors and camera-monitor linked replacements are counted as part of smart mirrors. Mordor Intelligence counts them only when the product is sold as a smart, connected mirror with embedded display functionality rather than a conventional mirror upgrade. Differences are also driven by how retail and residential volumes are projected. Some estimates apply aggressive penetration rates without checking installer throughput and procurement cycles, while others hold ASPs flat even when feature mix shifts.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 4.92 B (2026) | |

| Global Consultancy A | USD 3.38 B (2026) | Uses a narrower counted scope in the base year by leaning more on historical product revenues and a tighter definition of smart mirrors, which can undercount commercial deployments and newer automotive-display use cases. |

| Industry Publisher B | USD 0.64 B (2025) | Reports a much smaller number because the scope appears closer to consumer and residential smart mirrors, and the sizing year is earlier, which reduces the captured value from retail, hospitality, and automotive-related demand. |

Taken together, the spread in the table is mainly explained by what gets included as a smart mirror and how quickly adoption is assumed to scale outside the home. By tying the model to adoption signals, replace cycles, and practical price bands that can be rechecked, we keep the estimate transparent and easier to reproduce when assumptions are updated.

Key Questions Answered in the Report

What is the forecast revenue for the smart mirror market in 2031?

The smart mirror market is projected to reach USD 7.37 billion by 2031, supported by an 8.42% CAGR.

Which application is expected to grow the fastest?

Healthcare mirrors are forecast to advance at a 10.02% CAGR through 2031 due to tele-health reimbursement and aging-in-place demand.

Why are OLED panels gaining traction in smart mirrors?

OLED's thin form factor and superior contrast, alongside transparent variants reaching 60% transmittance, are driving accelerating OEM adoption.

How will services revenue evolve?

Subscription software, cloud storage, and analytics bundles are set to grow at a 9.61% CAGR, outpacing hardware sales.

What regions offer the highest growth potential?

Asia Pacific is poised for a 10.86% CAGR, benefiting from EV production, display R&D incentives, and smart-home adoption in China, South Korea, and Japan.

What is the primary regulatory hurdle in North America?

NHTSA FMVSS 111 still requires physical exterior mirrors, delaying widespread adoption of camera-only systems in U.S. vehicles.

Page last updated on: