Technology, Media and Telecom

5th MayPricing Strategy for Semiconductor Components

3 Min Read

Industrial Metaverse Market is Segmented by Component (Software, Hardware, Services), Technology (Augmented Reality, Virtual Reality, Mixed Reality, Digital Twin and Simulation, Industrial IoT and Edge-AI), End-User (Manufacturing, Automotive, Energy and Utilities, Logistics and Transportation, Healthcare, Other End-Users), and by Geography. The Market Forecasts are Provided in Terms of Value (USD).

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

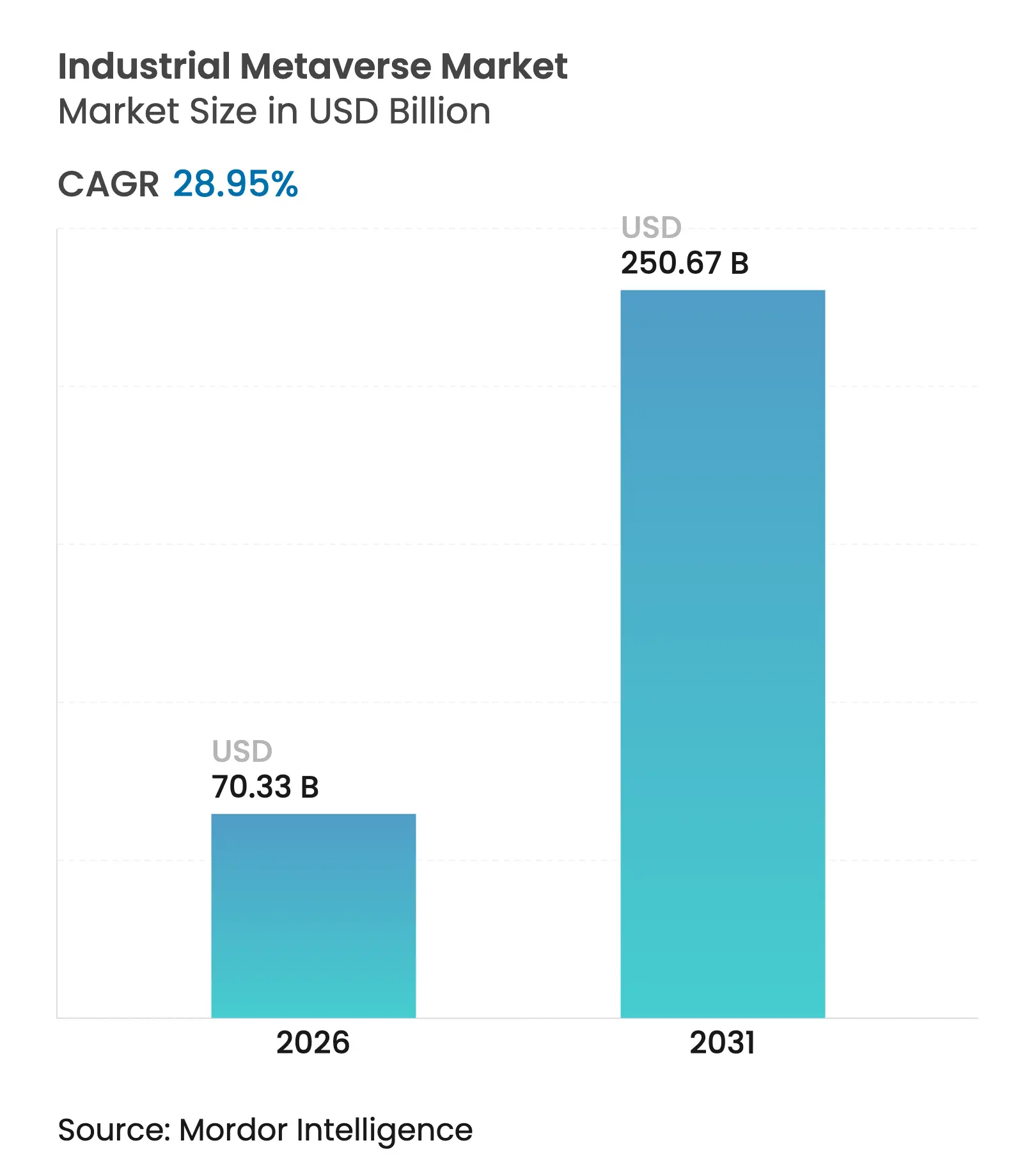

| Market Size (2026) | USD 70.33 Billion |

| Market Size (2031) | USD 250.67 Billion |

| Growth Rate (2026 - 2031) | 28.95 % CAGR |

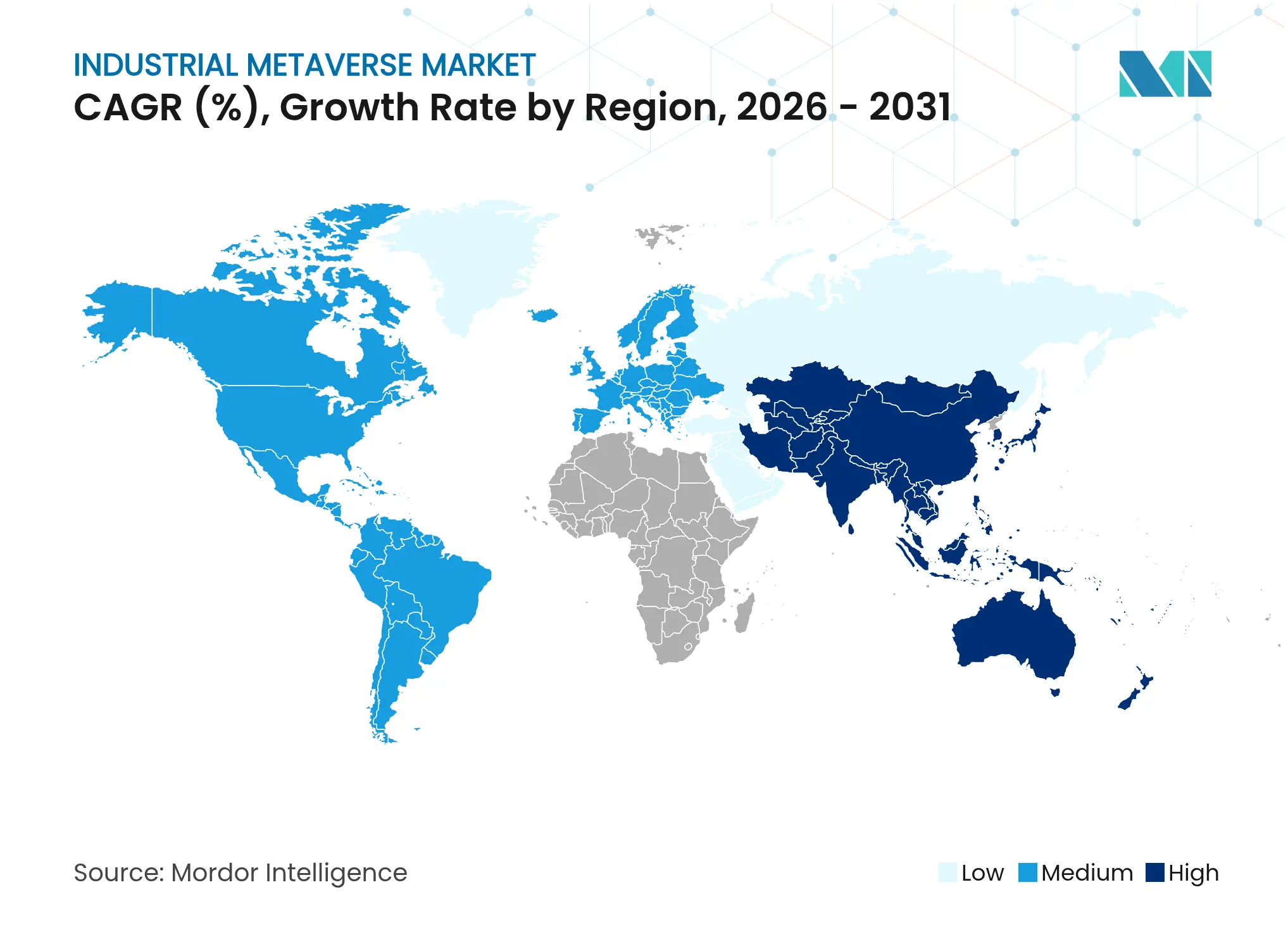

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order. Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

The Industrial Metaverse market size was valued at USD 54.53 billion in 2025 and estimated to grow from USD 70.33 billion in 2026 to reach USD 250.67 billion by 2031, at a CAGR of 28.95% during the forecast period (2026-2031). This rapid climb is propelled by a synchronized build-out of digital-twin platforms, extended-reality (XR) hardware, and industrial IoT networks that allow factories, energy grids, and logistics hubs to operate inside persistent, data-rich virtual environments. Early adopters highlight carbon-cutting virtual commissioning results—Schneider Electric recorded a 25% reduction in CO₂ while shortening product launch cycles—which reinforce the return-on-investment logic for immersive engineering workflows.

Demand is further lifted by mixed-reality training that narrows workforce skill gaps, private-5G rollouts enabling millisecond latency, and a growing ecosystem of edge-AI chipsets optimized for real-time simulation workloads. Software keeps the largest component foothold because digital twins and physics engines remain the metaverse’s functional core, yet service providers capture the fastest expansion track as enterprises rely on outside expertise for integration, cybersecurity hardening, and change management. Geographically, the Industrial Metaverse market witnesses North American revenue leadership, but APAC policy incentives, notably South Korea’s metaverse road map, give Asia the steepest growth slope.

Key Report Takeaways

Note: Market size and forecast figures in this report are generated using Mordor Intelligence's proprietary estimation framework, updated with the latest available data and insights as of 2026.

Drivers Impact Analysis

| Driver | (≈) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline | |||

|---|---|---|---|---|---|---|

Digital-twin-led predictive

maintenance

Digital-twin-led predictive

maintenance

| +8.2% | Global; strong in North America and EU | Medium term (2-4 years) |

(≈) % Impact on CAGR

Forecast

:

+8.2%

|

Geographic Relevance

:

Global; strong in North America

and EU

|

Impact Timeline

:

Medium term (2-4 years)

|

Remote monitoring and

collaboration across distributed plants

Remote monitoring and

collaboration across distributed plants

| +6.8% | Global; Asia-Pacific hubs scaling fastest | Short term (≤ 2 years) | |||

IIoT + 5G + edge-AI integration

IIoT + 5G + edge-AI integration

| +7.5% | North America and EU first movers | Medium term (2-4 years) | |||

Sustainability-focused virtual

commissioning

Sustainability-focused virtual

commissioning

| +4.9% | EU regulations drive; NA following | Long term (≥ 4 years) | |||

Immersive AI upskilling for

industrial workforce

Immersive AI upskilling for

industrial workforce

| +5.3% | Global; developed markets | Medium term (2-4 years) | |||

OEM monetization of virtual

product twins

OEM monetization of virtual

product twins

| +3.8% | North America and EU OEM clusters | Long term (≥ 4 years) | |||

| Source: Mordor Intelligence | ||||||

Rising Adoption of Digital-Twin-Led Predictive Maintenance

Renault saved USD 595 million by pairing IoT sensors with digital twins that predict asset failure early, a blueprint now replicating across automotive, semiconductor, and chemical plants.[1]Siemens, “Renault Saves USD 595 Million Using Digital Twins,” siemens.com LG Innotek cut substrate warping analysis from 11 days to 3.6 hours, underscoring how virtual replicas compress RandD cycles. As machine-learning models continuously ingest live shop-floor data, manufacturers report 18% fewer workplace incidents after switching from textbook maintenance to immersive, VR-based safety drills. OEMs are also bundling post-sale “virtual twin subscriptions,” turning one-off equipment deals into recurring digital revenue streams.

Need for Remote Monitoring and Collaboration Across Distributed Plants

Industrial metaverse workspaces let engineers “walk through” remote facilities in real time. Siemens and Microsoft link Omniverse with Teams so multidisciplinary teams annotate the same digital factory regardless of continent. Verizon’s campus-wide 5G rollouts supply the sub-10 ms latency engineers need to share high-fidelity holograms, improving issue-resolution speed by 30% over standard video calls.[2]Verizon, “Low-Latency 5G Powers Remote Industrial Collaboration,” verizon.com This real-time co-presence reduces travel-related emissions and accelerates root-cause analysis for complex machinery.

Integration of IIoT, 5G and Edge-AI Enabling Real-Time Metaverse Workloads

Private 5G spending is forecast to reach USD 6 billion by 2027, with 60% tagged to factory and energy projects where deterministic connectivity is mandatory. Qualcomm and Honeywell embed low-power AI cores at machinery edge nodes so vibration, thermal, and acoustic signals are processed locally, trimming cloud-backhaul latency and sharpening metaverse response loops.[3]Honeywell, “Edge-AI and 5G Combine for Energy Sector Twins,” honeywell.com Tesla’s Gigafactory networks illustrate how autonomous forklifts reference live digital-twin maps that update routes every second to avoid congestion.

Sustainability-Focused Virtual Commissioning to Cut CO₂ and Time-to-Market

Testing production lines in a virtual sandbox cut Schneider Electric’s commissioning emissions 25% and raised first-time-right rates. BASF drafts entire chemical plants in AR, running thousands of parameter permutations to select the lowest energy pathway before any steel is ordered. McKinsey finds product digital twins slice launch timelines by 50% and uplift quality 25%, benefits now factored into corporate ESG scorecards.

Restraints Impact Analysis

| Restraint | (≈) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline | |||

|---|---|---|---|---|---|---|

Lack of standards and

interoperability

Lack of standards and

interoperability

| -4.2% | Global; fragmentation acute in emerging markets | Medium term (2-4 years) |

(≈) % Impact on CAGR

Forecast

:

-4.2%

|

Geographic Relevance

:

Global; fragmentation acute in

emerging markets

|

Impact Timeline

:

Medium term (2-4 years)

|

High CAPEX for XR hardware and

private-5G

High CAPEX for XR hardware and

private-5G

| -6.1% | Cost-sensitive regions, SME segment | Short term (≤ 2 years) | |||

Cyber-physical security risks

Cyber-physical security risks

| -3.7% | Critical infrastructure everywhere | Long term (≥ 4 years) | |||

Cross-border data-sovereignty

uncertainty

Cross-border data-sovereignty

uncertainty

| -2.8% | EU GDPR zones, China localization | Long term (≥ 4 years) | |||

| Source: Mordor Intelligence | ||||||

Lack of Standards and Interoperability Across Metaverse Platforms

The Industrial Metaverse market still lacks a lingua franca. IEEE’s Metaverse Standards Forum and NIST’s February 2025 call-to-action both urge common schemas for asset semantics, yet competing vendors often pursue proprietary data models. Siemens and Microsoft are aligning Digital Twin Definition Language with W3C Thing Description, but without consistent adoption, multi-vendor rollouts stay cumbersome. ISO/IEC 5927:2024 and ISO 23247 give safety and framework guidance, yet a full stack standard is years away.

High CAPEX for XR Hardware and Private-5G Infrastructure

First-generation industrial HMDs, such as Siemens-Sony’s USD 4,750 headset, stretch ROI calculations for smaller plants. Private-5G deployments can top USD 9 million for a single multi-site enterprise, causing many SMEs to delay investment. Neutral-host architectures and falling component prices are easing the burden, but budget constraints remain the biggest near-term headwind for the Industrial Metaverse market.

By Component: Services Accelerate Digital Transformation

The Services segment is on track to clock a 36.42% CAGR through 2031, reflecting boardroom recognition that immersive environments demand multidisciplinary expertise in cybersecurity, change management, and OT-IT integration. Capgemini’s Digital Continuity playbook bundles strategy, architecture, and field rollout into one service stack, shortening client payback windows. Accenture’s collaboration with Vitesco Technologies shows how implementation partners increasingly get paid on performance milestones tied to operational metrics rather than on billable hours alone.

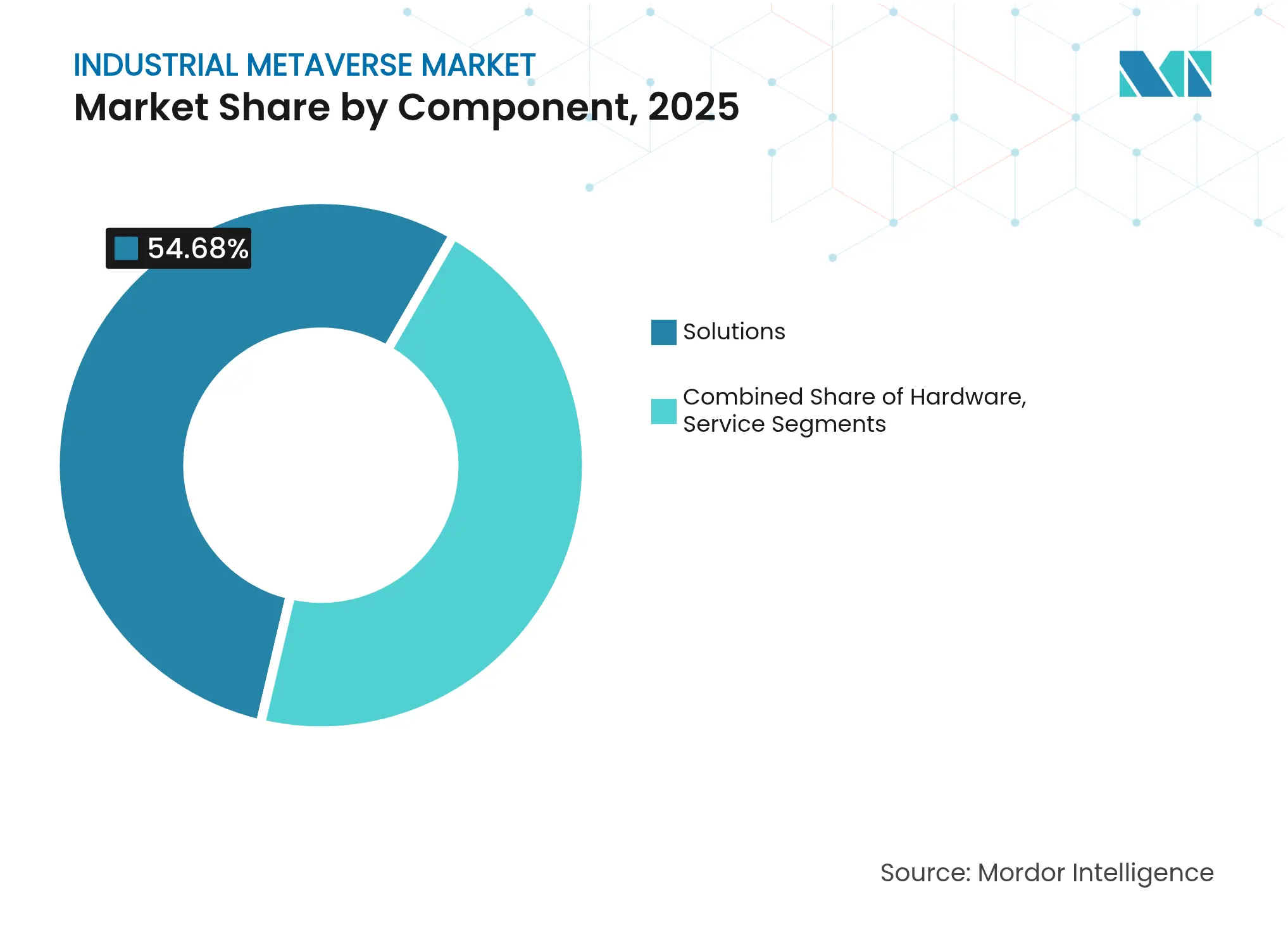

Software nonetheless holds 54.68% Industrial Metaverse market share in 2025 because digital twin kernels, physics solvers, and simulation orchestration engines form the backbone of every deployment. Hardware demand scales at a steady clip as enterprises order advanced XR displays, photogrammetry rigs, and edge-AI gateways that secure and synchronize real-time model updates. Together, these spending patterns confirm that the Industrial Metaverse market size gains hinge on a balanced value chain where services grow fastest but software retains margin leadership.

Note: Segment shares of all individual segments available upon report purchase

By Technology: Mixed Reality Emerges as Growth Leader

Digital twin and simulation tools captured 28.05% of Industrial Metaverse market size in 2025, indicating enterprises have largely accepted virtual replicas as a must-have for modern operations. Mixed reality, however, races ahead at a 38.1% CAGR as HoloLens 2 and purpose-built headsets overlay live telemetry onto physical assets so technicians can fix faults hands-free. Siemens-Sony’s engineered optics reduce eye fatigue during eight-hour shifts, a prerequisite for scale on the factory floor.

Augmented reality fills in-line guidance gaps while virtual reality excels in safety drills for confined-space or high-heat scenarios. Complementing both, edge-AI inference chips from Qualcomm compress vision and Lidar feeds on device, guaranteeing frame-accurate overlays even inside noisy RF environments. This multi-technology stack validates that the Industrial Metaverse market will not be winner-take-all but a portfolio play where MR gains velocity yet digital twins stay the value anchor.

By End-User: Energy and Utilities Drive Fastest Adoption

Energy and utilities adopt at a 34.2% CAGR because grid operators confront growing volatility from renewables, aging transformers, and cyber-physical threats. IBM’s AI-fueled twin for a North American utility trimmed fault-location time by 25%, freeing maintenance crews for high-value work . Hydrogen-electrolyzer projects model thermal loads virtually to avoid costly overspecification, driving 5-15% capex savings and underlining why boardrooms now earmark digital twin spend in every green-energy budget.

Manufacturing retains a 33.25% revenue share through entrenched Industry 4.0 programs, notably in automotive, where Tesla streams live machine states into cell-assembly twins to safeguard takt-time. Healthcare, logistics, aerospace, and chemicals follow, experimenting with virtual prototyping and regulatory compliance simulations. These patterns underline that the Industrial Metaverse industry remains cross-vertical, but investment intensity correlates with asset criticality and sustainability imperatives.

Recognized by Experts. Trusted by Leaders.

A trusted intelligence partner to global decision-makers across 90+ countries.

North America anchors 41.10% of 2025 revenue on the back of deep cloud penetration, abundant edge AI startups, and hyperscale-backed ecosystems. Federal tax incentives for smart-manufacturing gear, such as the CHIPS Act, further strengthen capital outlays. The region also fields the most pilot-to-production conversions, making it the benchmark sub-market for proof-of-value studies.

APAC, with a forecast 33.9% CAGR, grows fastest as South Korea invests USD 4.7 million to crack the global top-five metaverse league and China rolls out its Three-Year Action Plan that grants tax rebates to factory digital-twins built on domestic clouds. LG’s smart-factory unit lines up multi-industry orders that could tally USD 170 million by 2030, signaling broad private-sector appetite. India’s electronics clusters co-develop Omniverse-based twins with NVIDIA to leapfrog legacy automation stages.

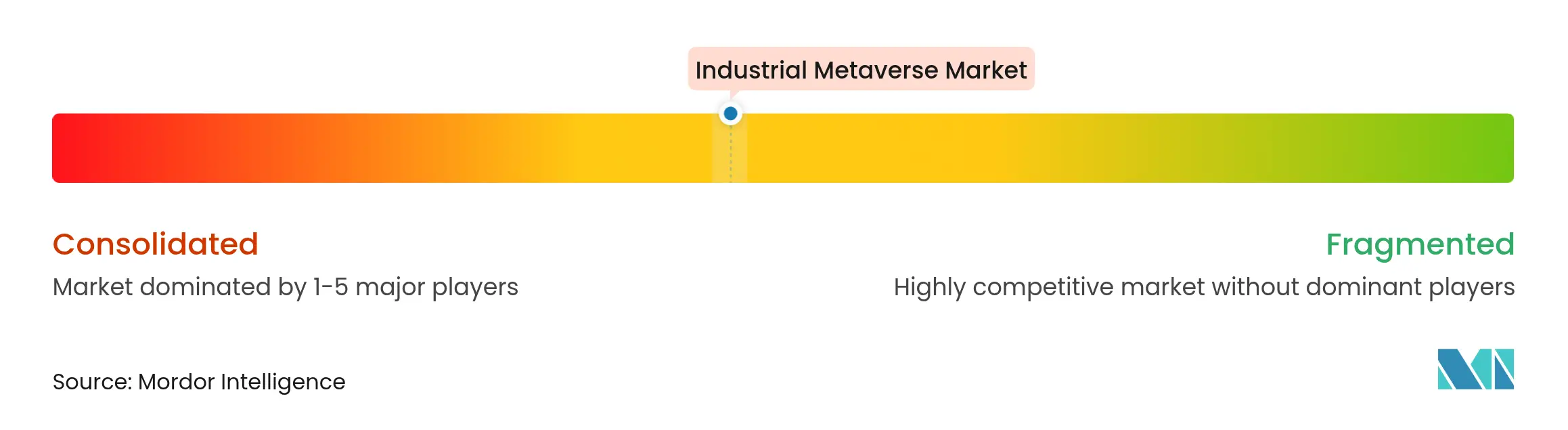

Market Concentration

Global revenue is distributed across a mix of integrated giants and niche innovators. NVIDIA’s USD 39.3 billion Q4 2025 turnover, driven by data-center GPUs that render colossal scene graphs, underscores the hardware gravity well around which the wider ecosystem orbits. Siemens and Microsoft leverage cross-licensing to weave automation stacks with cloud twins, while Unity and Dassault Systèmes concentrate on gaming-grade rendering engines and PLM integrations, respectively.

Consultancies such as Accenture and Capgemini parlay domain knowledge into turnkey deployments, often assuming outcome-based contracts tied to uptime or energy-saving metrics. Start-ups add competitive spice: MetAI, backed by NVIDIA, layers generative AI onto CAD pipelines to fabricate high-resolution digital twins in minutes rather than weeks. Standards bodies become indirect competitive arenas; vendors shaping IEEE or ISO schemas will capture mindshare when buyers insist on future-proofed architectures. Overall competitive intensity is moderate, with platform lock-in strategies counter-balanced by open-source consortia that lobby for vendor-neutral APIs.

*Disclaimer: Major Players sorted in no particular order

1. INTRODUCTION

2. RESEARCH METHODOLOGY

3. EXECUTIVE SUMMARY

4. MARKET LANDSCAPE

5. MARKET SIZE AND GROWTH FORECASTS

6. COMPETITIVE LANDSCAPE

7. MARKET OPPORTUNITIES AND FUTURE OUTLOOK

Industrial metaverse is a blending of the digital and physical world that accelerates efficiency through engineering, manufacturing, and field service. The vision is for it to enable real-time collaboration, connectivity, and spatially-aware context within industrial environments.

The industrial metaverse market is segmented by component (software, hardware, services), by technology (AR, VR, MR), by end-user (automotive, healthcare, logistics & transportation, manufacturing, energy and utilities, other end-users), by geography (North America, Europe, Asia-Pacific, Latin America, Middle East and Africa). The market sizes and forecasts are provided in terms of value (USD) for all the above segments.

Pricing Strategy for Semiconductor Components

3 Min Read

Accelerating Additive Manufacturing Adoption in India

3 Min Read

Unlocking Growth in India’s Luxury Beauty & Skincare Market

3 Min Read

When decisions matter, industry leaders turn to our analysts. Let’s talk.