Smart Window Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

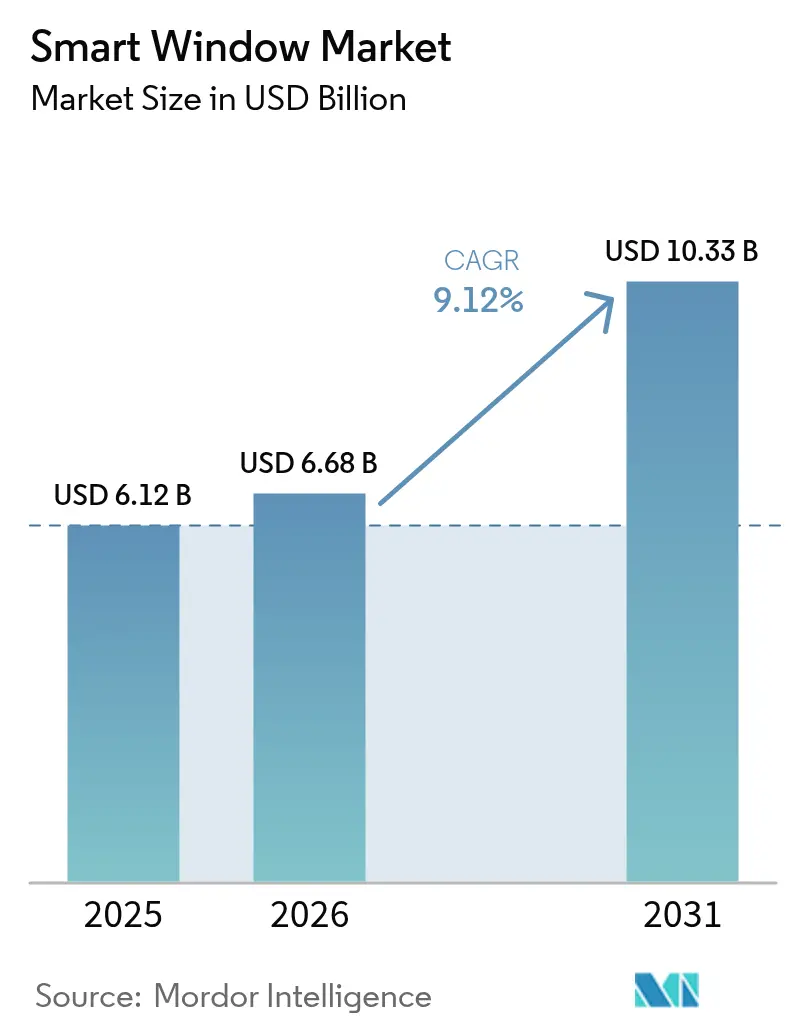

| Market Size (2026) | USD 6.68 Billion |

| Market Size (2031) | USD 10.33 Billion |

| Growth Rate (2026 - 2031) | 9.12% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Smart Window Market Analysis by Mordor Intelligence

The Smart Window market size is expected to grow from USD 6.12 billion in 2025 to USD 6.68 billion in 2026 and is forecast to reach USD 10.33 billion by 2031 at 9.12% CAGR over 2026-2031. This trajectory aligns with global moves to curb building energy use, the expansion of connected-home ecosystems, and regulatory mandates that now treat automated shading as core infrastructure [1]U.S. Department of Energy, “Building Energy Codes,” energy.gov. Rising adoption across offices, healthcare campuses, and premium residences supports volume growth, while integration with voice assistants and Matter-enabled IoT platforms unlocks higher average selling prices. Regulatory sticks such as California’s Title 24 and the 2024 IECC edition intersect with corporate net-zero targets, anchoring non-discretionary demand in commercial real estate. Suppliers respond by fusing edge computing into motor controllers to cut latency, by layering cybersecurity controls that satisfy GDPR and US state privacy statutes, and by exploring ESCO financing models to compress payback cycles in retrofit projects. Competitive intensity remains moderate: incumbent shade leaders defend share through channel reach and reliability, whereas electrochromic glass specialists pursue premium envelopes that promise 20-30% HVAC savings.

Key Report Takeaways

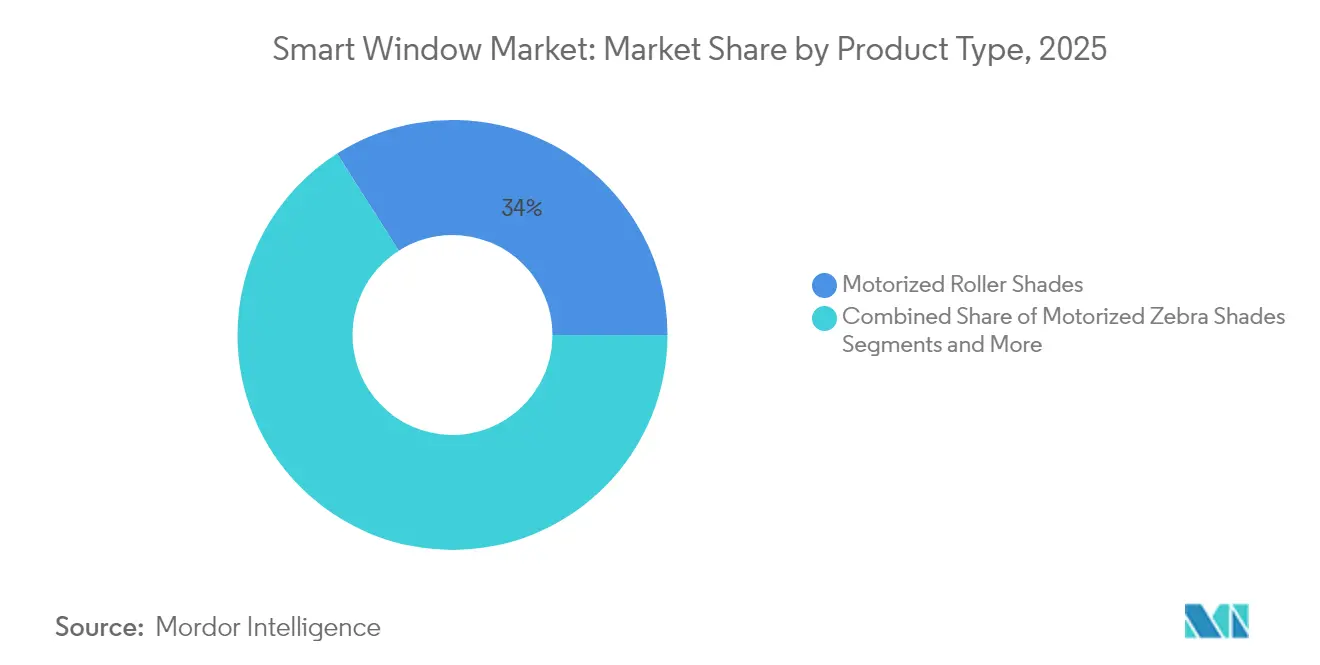

- By product type, motorized roller shades led with 34.02% of the smart window market share in 2025, while smart glass panels and controllers are advancing at an 10.88% CAGR through 2031.

- By power source, hard-wired systems accounted for 40.65% of the smart window market size in 2025, while solar-powered solutions are expanding at a 12.05% CAGR to 2031.

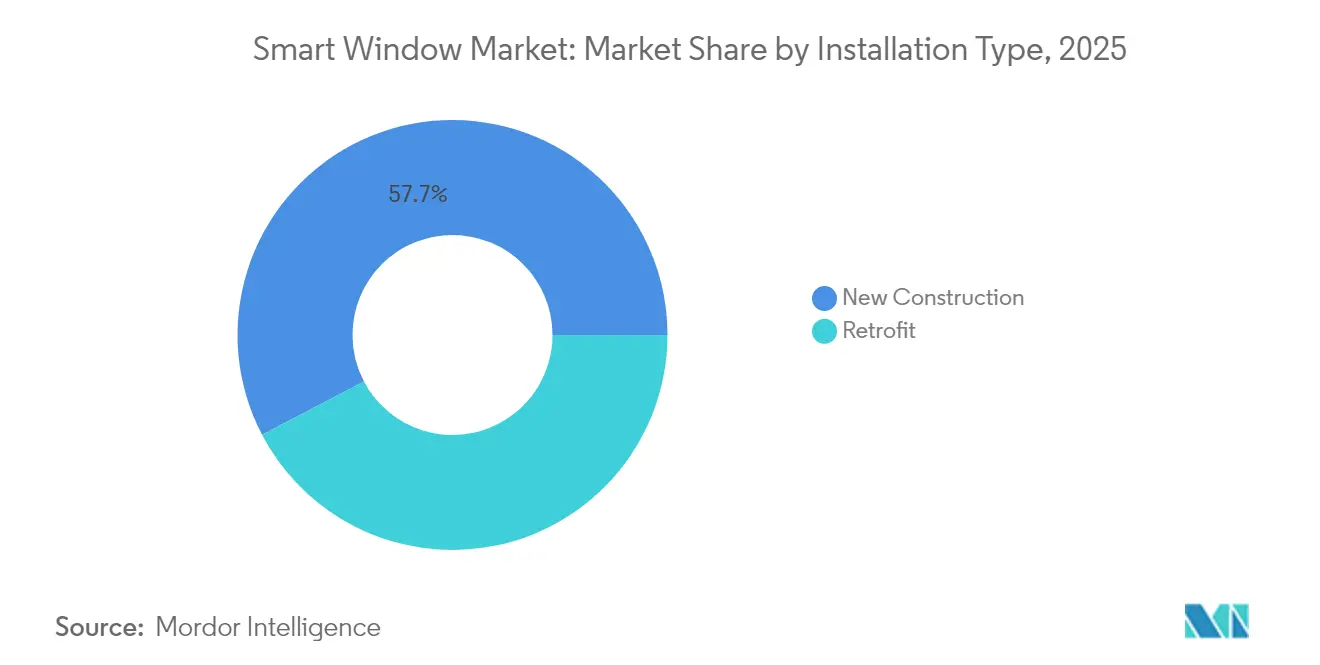

- By installation type, new-construction projects captured a 57.68% share of the smart window market size in 2025, whereas retrofit applications are registering a 10.22% CAGR to 2031.

- By application, commercial deployments held 37.10% of the smart window market share in 2025, while residential use cases are recording the fastest growth at a 11.74% CAGR through 2031.

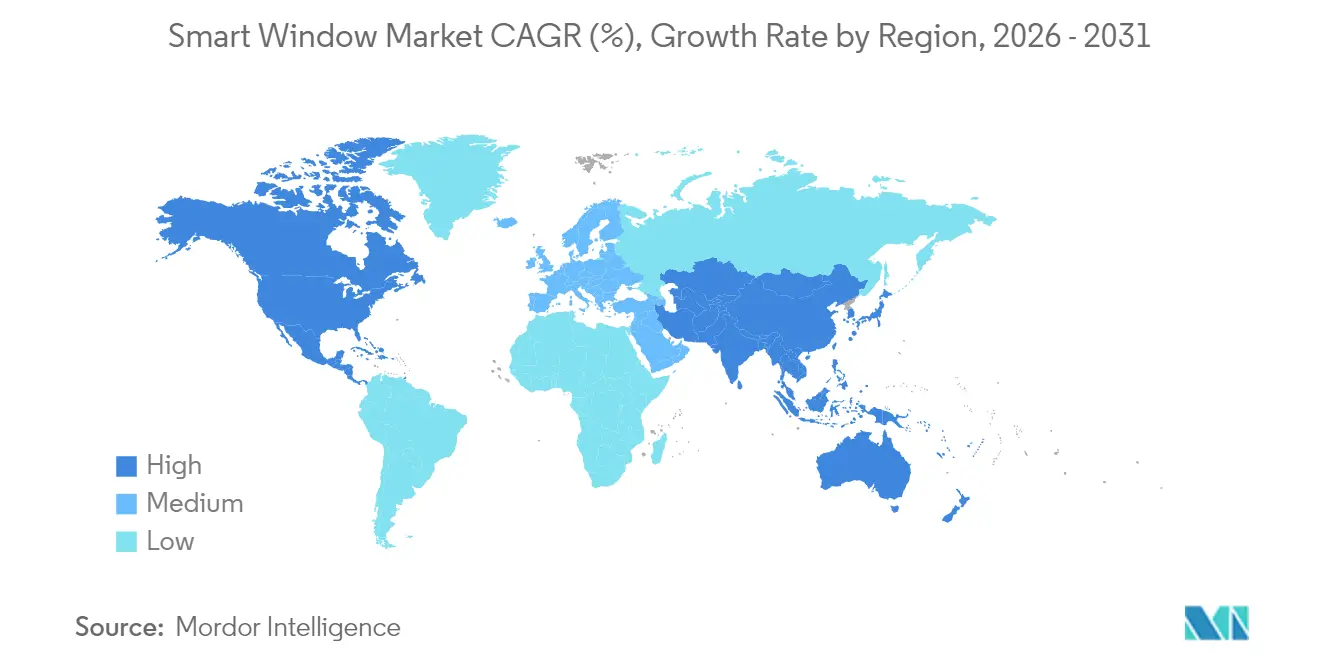

- By geography, North America retained 32.12% of global revenue in 2025, while the Asia Pacific is projected to post a 12.31% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Smart Window Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growing prominence of smart homes | +2.1% | Global, early uptake in North America and Europe | Medium term (2-4 years) |

| Energy-efficiency regulations and green-building codes | +2.8% | North America and EU core, expanding to Asia Pacific | Long term (≥ 4 years) |

| Integration with voice assistants and wider IoT ecosystems | +1.9% | Global, led by North America and developed APAC | Short term (≤ 2 years) |

| Demand for daylighting and circadian-lighting solutions | +1.4% | Global, premium segment in developed economies | Medium term (2-4 years) |

| Aging-in-place and accessibility retrofits | +0.8% | North America and Europe, emerging in developed APAC | Long term (≥ 4 years) |

| Smart-building certifications pushing automation | +1.2% | Global, concentrated in commercial real-estate hubs | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Growing prominence of smart homes

Smart-home penetration reached 15.2% of households in 2024, transforming consumer expectations for shading from simple motorization to predictive automation. Matter and Thread protocols now enable multi-vendor interoperability, while voice assistant links allow windows to respond automatically to occupancy schedules and tariff changes. Edge processors inside shade motors cut cloud latency and support localized decision logic. Channel partners in North America report attachment rates above 45% when smart windows are bundled with security and HVAC packages. Suppliers that expose open APIs are gaining integrator loyalty, reducing reliance on proprietary hubs.

Energy-efficiency regulations and green-building codes

California’s Title 24 mandates dynamic glazing or motorized shading for commercial spaces above 10,000 square feet. The 2024 IECC introduced automated daylight controls for sidelighting zones, while the EU’s EPBD recast compels member states to elevate building automation standards. Because compliance spend is non-discretionary, vendors see higher margins in code-driven projects than in purely aesthetic residential upgrades. Certifications such as LEED v4.1 and BREEAM award points for automated glare and solar-heat-gain mitigation, positioning smart windows as a cost-effective route to rating thresholds.

Integration with voice assistants and wider IoT ecosystems

Amazon disclosed that more than 100 million Alexa-compatible devices were active in homes in 2024, with shade control among the fastest-rising categories. Matter adoption has slashed commissioning time by at least 30% for installers, broadening retail distribution. Office landlords embed smart-window endpoints in the same BACnet or MQTT fabric that governs HVAC, facilitating holistic demand-response programs. Local analytics embedded in controllers reduce dependence on cloud uptime and better protect user data under GDPR constraints.

Demand for daylighting and circadian-lighting solutions

Clinical studies show that automated daylight management can raise sleep-quality scores by 23% and cut eye strain by 31% in offices [2]PubMed (J. Clinical Medicine), “Impact of Automated Daylighting on Sleep Quality,” pubmed.ncbi.nlm.nih.gov . Hospitals outfit patient rooms with electrochromic glass to support recovery protocols while minimizing pathogen reservoirs that accumulate on fabric shades. Commercial developers market circadian-optimized lighting as a tenant-retention lever. Spectral sensors coupled with machine-learning algorithms now adjust tint or shade position every 15 seconds to maintain target lux levels without introducing glare, boosting worker satisfaction scores in post-occupancy surveys.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Lack of interoperability standards | -1.8% | Global, heightened in fragmented regional markets | Short term (≤ 2 years) |

| High upfront costs for retrofit installations | -2.3% | Global, stronger in price-sensitive emerging economies | Medium term (2-4 years) |

| Cyber-security and data-privacy concerns | -1.1% | Global, with regulatory focus in EU and California | Short term (≤ 2 years) |

| Supply-chain volatility for electronics and semiconductors | -1.4% | Global, concentrated impact on Asian manufacturing bases | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Lack of interoperability standards

Despite Matter’s 2024 launch, legacy devices run on Zigbee, Z-Wave, or proprietary RF, forcing integrators to juggle bridges that raise cost and complexity [3]Connectivity Standards Alliance, “Matter Standard,” csa-iot.org. Surveys show compatibility headaches trigger 35% of commercial installation delays. Enterprise buyers hesitate to lock into closed ecosystems that risk obsolescence. Manufacturers that still guard APIs face channel pushback, prompting an industry shift toward software-defined gateways capable of translating multiple protocols in real time.

High upfront costs for retrofit installations

Retrofit projects run 40-60% more than new-build equivalents once electricians, drywall repair, and integration labor are tallied. Cash-flow pressures are acute in small hospitality and retail properties where downtime erodes revenue. Although ESCO contracts can roll costs into energy savings, only a fraction of banks in emerging markets recognize smart-window assets as collateral. Battery-powered kits reduce wiring expenses yet introduce maintenance cycles that facilities teams often overlook in net-present-value analysis.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Motorization Drives Traditional Categories

Motorized roller shades accounted for 34.02% of the smart window market share in 2025 on the strength of proven reliability and installer familiarity. Their fabric versatility suits both residential décor changes and commercial glare-control requirements. Smart window market growth within this segment is reinforced by cost-optimized tubular motors that can lift wider spans while drawing less than 0.5 amps. In contrast, electrochromic smart glass panels capture media attention and post an 10.88% CAGR yet remain capital-intensive. Controllers now ship with quad-core processors, supporting on-device scene orchestration and over-the-air security patches.

The convergence of mechanical shading and dynamic glazing suggests hybrid façades in future projects. Manufacturers bundle integration hubs that stitch roller shades, blinds, and glass together under a single BACnet object, letting facility managers tune solar-heat gain precisely. Vendors like SageGlass showcase 20-30% HVAC savings in post-occupancy audits, bolstering the smart window market narrative around operational payback. Niche categories such as motorized venetian blinds serve laboratories where doctors calibrate light angles to avoid reflective glare on monitors. Motorized drapery systems continue in hospitality suites, though growth lags due to fabric cost and longer installation times.

By Power Source: Hard-wired Dominance Faces Solar Challenge

Hard-wired solutions contributed 40.65% to the smart window market size in 2025, owing to uninterrupted power and direct integration to building management systems. They draw from low-voltage DC buses, simplifying compliance with electrical codes that restrict line-voltage wiring by non-electricians. However, solar-powered units are expanding at a 12.05% CAGR as panel efficiency breaches 22% and lithium-iron-phosphate packs retain 80% capacity beyond 3,000 cycles.

Transparent photovoltaic strips embedded in glazing promise a dual benefit: daylight modulation and renewable energy harvesting. Battery-powered kits occupy retrofit niches where drill paths or conduit runs are impractical. Manufacturers embed super-capacitors to buffer intermittent sunlight in cloudy regions. Energy-harvesting motors that recycle kinetic energy from shade motion remain experimental but illustrate how the smart window market pursues autonomy from grid power.

By Installation Type: New Construction Leads Despite Retrofit Acceleration

New builds commanded 57.68% of 2025 revenue because electrical routes, framing pockets, and network drops are cheaper to provision before drywall goes up. Smart window market adoption in Class-A offices often starts at the architectural spec stage, where shading counts toward LEED daylighting credits. In contrast, retrofits post a 10.22% CAGR because owners face mounting energy mandates and tenant expectations for wellness-focused interiors.

Wireless meshes and stick-on solar panels compress installation timelines to weekend turnovers, curbing occupant disruption. The US building stock erected before 2000 represents more than 60% of floor area, offering a vast retrofit runway. ESCOs package shading alongside LED and HVAC projects, monetizing energy savings to offset capital outlay. Software updates delivered over cellular fallback channels keep legacy buildings current without ripping out drywall for new cabling.

By Application: Commercial Leadership Faces Residential Disruption

Commercial deployments held 37.10% of the smart window market size in 2025, bolstered by Title 24 compliance in the United States and performance-based building codes in Europe. Offices seek glare-free environments that raise employee productivity metrics, and hospitals value electrochromic glass for infection-control protocols. Hospitality chains adopt motorized draperies to differentiate guest experiences and to cut cooling loads during peak tariffs.

Residential uptake, climbing at a 11.74% CAGR, taps smart-home ecosystems that now treat shading as integral as thermostats. Voice assistants allow mobility-challenged users to operate blinds without manual force, aligning with aging-in-place trends. Educational facilities install daylight-optimized façades that raise student cognitive scores, while industrial cleanrooms specify venetian blinds tuned for particulate minimization. Retail stores automate display windows to mitigate UV damage on merchandise during unstaffed hours.

Geography Analysis

North America maintained a 32.12% revenue share in 2025 due to stringent codes and a 46% smart-home penetration rate. The US federal leasing policies stipulate energy-efficient envelopes, ensuring baseline demand even when discretionary budgets tighten. Canada’s cold climate sharpens heating-savings payback, and Mexico’s factory boom under the USMCA trade pact pushes commercial adoption despite tighter budgets.

Asia Pacific is the fastest-growing region at 12.31% CAGR. China’s smart-city pilots in Shenzhen and Shanghai embed intelligent shading in high-rise clusters, while Japan equips senior housing blocks with automated blinds to aid occupants with limited mobility. South Korea integrates Matter-compatible façades in Seoul’s premium apartments. India’s Smart Cities Mission names automated daylight control as an eligible EMS investment, though uptake concentrates in Grade-A offices. Europe sustains mid-single-digit growth on the back of its Renovation Wave program, with Germany funding low-interest loans for building automation. UAE and Saudi Arabia install electrochromic glass in megaprojects to battle peak-time cooling costs.

Regulatory Landscape

Smart-window adoption is increasingly shaped by building-energy codes and test standards that quantify glazing and shading performance. In the United States, California Energy Commission enforcement of the 2025 Building Energy Efficiency Standards (Title 24, Part 6) took effect on January 1, 2026, tightening envelope performance requirements and reinforcing automated shading and high-performance glazing in code-driven commercial projects. At the international level, ISO updates provide common reference points for performance claims, including ISO 52016-3:2023/Amd 1:2025 for calculation procedures covering adaptive building envelope elements (including chromogenic glazing), and ISO 11983:2025 for standardized testing of electro-switchable glazing in road vehicles.

Policy actions also target affordability and compliance pathways for dynamic glazing. In the United States, S. 4730 (Dynamic Glass 2.0 Act) was introduced on June 21, 2024 to extend eligibility for the federal energy investment tax credit to electrochromic glass construction projects beginning before January 1, 2033, highlighting legislative attention to upfront-cost barriers. On the standards side, ISO 9050 (solar and luminous transmittance characteristics for glazing) reached an under-publication stage in July 2026, supporting more consistent comparisons of smart glass and coated glazing products used in buildings.

Value Chain Analysis

The smart window value chain covers material suppliers (glass substrates, interlayers, coatings, electronics), component and module manufacturing (motors, controllers, sensors, electrochromic/PDLC/SPD stacks), system integration, and multi-channel distribution through glazing fabricators, window and facade OEMs, shade dealers, electrical contractors, and smart-home or BA systems integrators. For smart glass, manufacturing includes substrate preparation, transparent conductive oxide deposition, active layer integration, edge sealing, and lamination or autoclave steps before final IGU assembly, while motorized shading centers on tubular motors, batteries or solar harvesters, RF modules, and control firmware that connects into home platforms and BMS environments.

Scale-up and quality control depend on yield and materials economics: conductive coatings and specialty glass can be major bill-of-materials items, and lamination yield losses can limit throughput and cost-down efforts. Partnerships between advanced-material suppliers and electrochromic developers show upstream-to-downstream coordination, including Mativ's October 2024 joint development agreement with Miru on lamination interlayers, followed by a first commercial purchase order in May 2025 for Argotec specialty TPU interlayer films used in Miru eWindow stacks, and an equity investment announced by Mativ in January 2026 to support commercial production. Standardization and safety certification run alongside production and installation, with governance and compliance touchpoints that include ASTM committees (for glazing and fenestration-related standards) and certification against ANSI Z97.1 and 16 CFR 1201 via bodies such as the Safety Glazing Certification Council (SGCC).

Competitive Landscape

The smart window market hosts moderate concentration. Lutron Electronics, Somfy Systems, and Hunter Douglas leverage broad dealer networks and proven reliability. Start-ups such as View Inc. and SageGlass lead electrochromic innovations but face heavy capex. View filed for Chapter 11 in 2024, opening consolidation opportunities. Ecosystem fit is now a prime differentiator. Players rush to certify Matter compatibility and to expose RESTful APIs that integrators script into building dashboards.

Software prowess increasingly dictates competitive edge. Vendors fold AI into shade controllers to predict sun paths based on local weather-feed ingestion. Lutron’s Triathlon Select launched in November 2024 with on-device scene learning that trims commissioning time by up to 40%. Hunter Douglas updated Pirouette shadings in June 2025, embedding ambient sensors and edge analytics to pre-empt glare. Suppliers pursue ESCO alliances to shoulder upfront costs in exchange for multi-year service annuities, a model gaining traction in municipal retrofits. Cybersecurity certifications such as ISO 27001 and US FedRAMP create bidding advantages in healthcare and government tenders that handle sensitive data.

Smart Window Industry Leaders

Lutron Electronics Co. Inc.

Somfy Systems Inc.

Hunter Douglas N.V.

Griesser AG

Springs Window Fashions LLC

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

White space is emerging where code-driven envelope upgrades intersect with retrofit-friendly implementations and higher-value software control. Regulatory anchors such as the EU Energy Performance of Buildings Directive (EPBD) and California's 2025 California Energy Code effective January 1, 2026 increase the emphasis on verified glazing and envelope performance, which raises demand for solutions that can document daylight, glare, and HVAC impact within whole-building compliance workflows. This favors vendors that pair smart windows with measurable control strategies, including BMS integration, analytics, and commissioning tools that reduce installer time and support ongoing verification.

Technology and deployment evidence also points to additional headroom in multifunctional smart windows and scalable manufacturing. In June 2026, TNO reported the first real-world application of thermochromic SunSmart windows, with over 300 square meters installed in buildings including the Brightlands Circular Space building in Geleen, indicating a shift from lab results into building projects. R&D activity broadens the feature set as well, including multicolor electrochromic switching demonstrations and concepts combining switchable transparency with solar-window architectures, creating room for suppliers across materials, coatings, lamination equipment, and controls software serving premium commercial facades and retrofit pathways that avoid full window replacement.

Recent Industry Developments

- January 2026: Mativ Holdings announced an equity investment into Miru Smart Technologies to accelerate commercial production of Miru's dynamic electrochromic eWindow technology. The move tightens upstream materials support and manufacturing readiness for electrochromic glazing stacks, reinforcing a pathway from development to higher-volume supply.

- July 2025: Hunter Douglas announced firmware upgrades for its PowerView Gen 3 platform to add support for the Matter connectivity standard. Matter support improves multi-ecosystem interoperability and expands addressable demand from households and integrators standardizing on Apple Home, Google Home, and other compatible platforms.

- June 2024: The Dynamic Glass 2.0 Act (S. 4730) was introduced in the US Senate to extend investment tax credit eligibility to electrochromic glass construction projects beginning before January 1, 2033. The proposal spotlights policy attention on lowering upfront cost hurdles for dynamic glazing in building projects, which can influence specification and financing discussions for smart-window deployments.

Research Methodology Framework and Report Scope

Market Definition and Coverage

We size the smart window market as revenue from smart, motorized window covering systems and their enabling controllers that allow automated movement and remote or scheduled operation across buildings.

Scope exclusions: We exclude conventional manual blinds and curtains, basic building glass, and broader smart glass glazing products that tint or switch transparency without a motorized window covering system.

Segmentation Overview

- By Product Type

- Motorized Roller Shades

- Motorized Zebra Shades

- Motorized Drapery Systems

- Motorized Venetian Blinds

- Other Product Types (Smart Glass Panels, Controllers and Integration Hubs, etc.)

- By Power Source

- Hard-wired

- Battery-powered

- Solar-powered

- By Installation Type

- New Construction

- Retrofit

- By Application

- Residential

- Commercial

- Offices

- Hospitality

- Healthcare

- Education

- Retail

- Industrial

- By Geography

- North America

- United States

- Canada

- Mexico

- South America

- Brazil

- Argentina

- Rest of South America

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Russia

- Rest of Europe

- Asia Pacific

- China

- Japan

- South Korea

- India

- Australia and New Zealand

- Rest of Asia Pacific

- Middle East

- Saudi Arabia

- United Arab Emirates

- Turkey

- Rest of Middle East

- Africa

- South Africa

- Nigeria

- Rest of Africa

- North America

Data Sources, Market Sizing, and Validation

Desk Research

Desk research started with understanding where demand is formed, which is typically tied to building activity, renovation cycles, and energy efficiency upgrades. We used public reference points such as U.S. Energy Information Administration (building energy end use context), U.S. Census Bureau (construction indicators), Eurostat (construction and housing statistics), and International Energy Agency publications that discuss efficiency measures and adoption signals.

To avoid building the model on one data stream, we also reviewed broader sources like company annual reports and investor presentations, import and export trade releases where relevant for components, and reputed press coverage of retrofit programs and building code changes. When needed, we cross-checked company financials and patent activity using paid subscriptions for company intelligence and patent databases. These examples are not exhaustive, and many other public documents and datasets were used to collect, validate, and clarify inputs.

Primary Interviews and Surveys

Primary work focused on confirming what gets counted as a smart window in real buying decisions and how pricing changes by power source, installation type, and control feature set. We spoke with manufacturers, channel partners, installers, and commercial and residential decision makers across major regions, then used follow-up calls to close gaps found during desk research. Respondent input was also used to sanity check adoption rates, typical replacement and retrofit behavior, and the split between controller-only retrofits and full system installations.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 35% | CXOs: 15% | APAC: 45% |

| Mid tier: 50% | Functional/Unit leaders: 41% | EMEA: 32% |

| Smaller Players: 15% | Managers: 44% | Americas: 23% |

Market-Sizing & Forecasting

Sizing relied on a top-down build where construction activity and renovation intensity were translated into an addressable window covering demand pool, which was then filtered by smart adoption and average system value. The totals were corroborated with selective bottom-up approximations using sampled ASP x volume checks from channel feedback, installer throughput patterns, and supplier revenue disclosures, and then adjusted where the two views did not align.

Key inputs included indicators like residential and non-residential building completions, retrofit versus new-install mix, battery versus hard-wired versus solar share, typical controller attach rates, and the observed premium for connectivity and automation features. Forecasting used scenario analysis, since adoption can shift quickly when energy codes tighten, retrofit incentives change, or component costs fall, and we applied the expert consensus ranges from interviews to keep the forward curve realistic. Where company disclosures were incomplete, gaps were handled through regional penetration proxies and installer-led volume estimates, then rechecked against the final global roll-up.

Data Validation & Update Cycle

Validation was done through stepwise triangulation, where model outputs were compared with independent signals like construction cycles, announced project activity, and implied shipment direction from channel feedback. Outliers were flagged, assumptions were revisited, and when a single input moved the market too sharply, experts were re-contacted to confirm whether the change was real or a data artifact.

Before sign-off, the work is reviewed in multiple analyst passes so calculation logic, currency handling, and year-to-year transitions remain consistent. Reports refresh annually, and interim updates are made when material events occur that can shift adoption or pricing. Before delivery, a final update pass is completed so clients receive the most current view available at that time.

Mordor Intelligence's Smart Window Market Size Compared Against Other Published Estimates

Published market values for smart windows can look far apart because the term is used differently across sources, and the year anchors and included product types are not always aligned. Differences also come from how pricing is treated, especially when controller-only retrofits and full system installations are blended without a clear rule.

In this study, the spread is mainly explained by whether smart glass (switchable glazing) is folded into the number, and whether automotive and aviation glazing is counted as part of the same revenue pool. Another driver is refresh timing, since fast-changing construction demand and retrofit programs can move a 12-month view, and currency conversion timing can widen gaps further.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 6.12 B (2025) | |

| Trade Journal A | USD 4.26 B (2025) | Often treats smart windows as switchable smart glass only, which can undercount motorized shades, drapery systems, and controller-driven retrofit kits that make up a material part of installed value. |

| Industry Release B | USD 6.70 B (2024) | Uses a combined smart glass and smart window definition and anchors to a 2024 base, which typically pulls in broader glazing end uses (including transportation) and can inflate totals versus a window covering focused scope. |

The table shows that the biggest swings are created by scope choices, especially around switchable glazing versus motorized coverings, and by the base year used for currency and pricing. By separating controller-only retrofits from full installed systems and keeping the count tied to building-installed window covering revenue, the market number stays traceable to repeatable inputs, a modeling choice applied by Mordor Intelligence.

Key Questions Answered in the Report

How large is the smart window market in 2026?

The smart window market size is USD 6.68 billion in 2026 and is projected to reach USD 10.33 billion by 2031.

Which product category leads global revenue?

Motorized roller shades hold 34.02% of 2025 revenue, reflecting their versatility and installer familiarity.

What is the fastest-growing region through 2031?

Asia Pacific posts a 12.31% CAGR due to smart-city investments and rapid urbanization.

How do solar-powered smart windows differ from battery-driven units?

Solar-powered systems harvest sunlight through integrated PV strips, reducing maintenance cycles that typical battery-only models require.

Why are retrofit projects more expensive than new-build installations?

Retrofits involve structural access, electrical rewiring, and occupant disruption, driving costs 40-60% higher than new construction.

Which regulations most influence commercial adoption in the United States?

California’s Title 24 and the 2024 International Energy Conservation Code mandate dynamic glazing or automated shading in large commercial buildings.

Page last updated on: