Technology, Media and Telecom

5th MayPricing Strategy for Semiconductor Components

3 Min Read

The Metaverse Market Report Segmented by Component (Hardware (HMDs, Sensors), Software Platform and More), Platform Type (Centralized Closed Platforms, Open Decentralized Platforms (Web3) and More), Revenue Model (Direct Consumer Spend, Advertising and More), End-User Industry (Gaming and Esports, Media and Live Entertainment, and More) and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

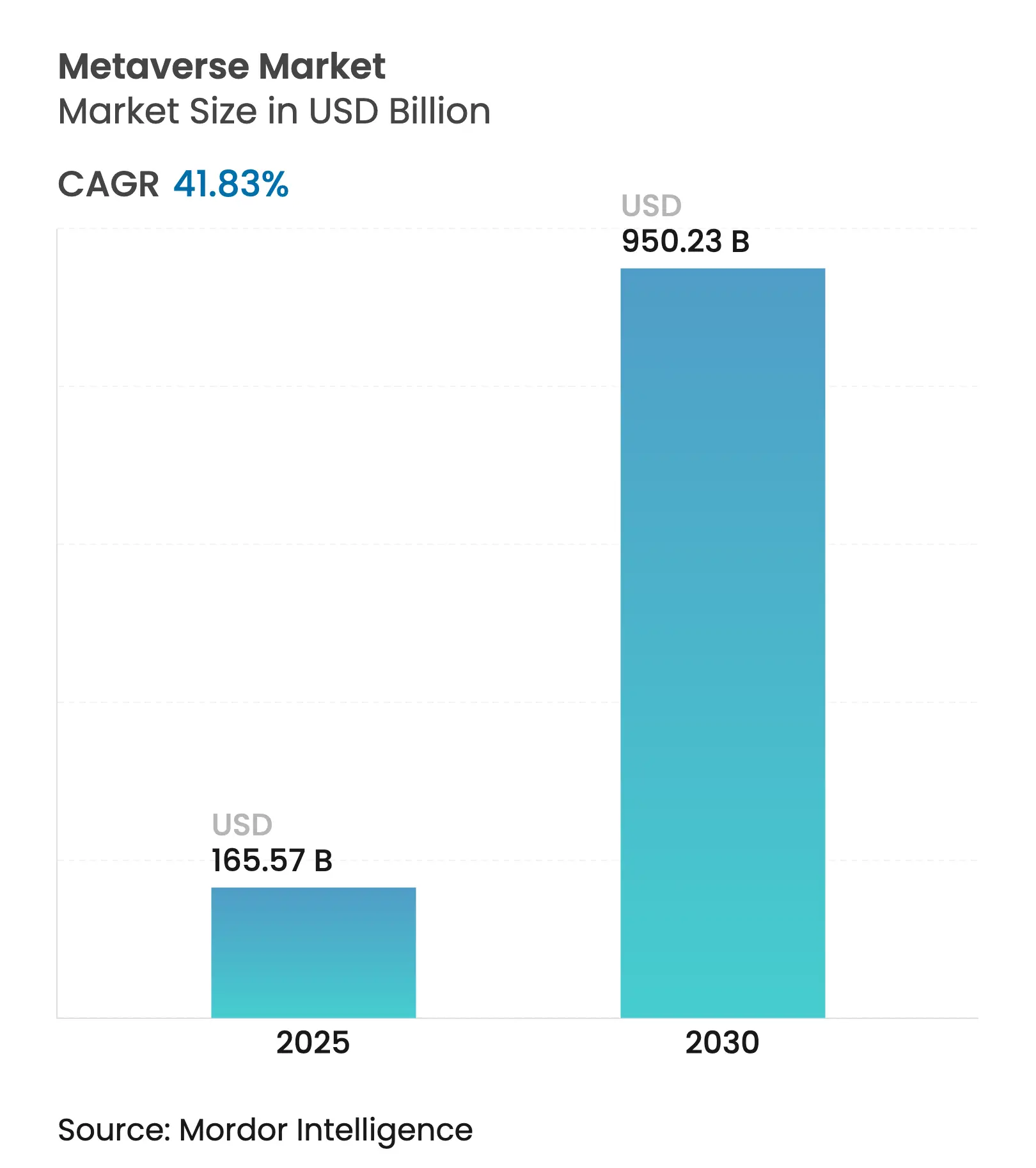

| Market Size (2025) | USD 165.57 Billion |

| Market Size (2030) | USD 950.23 Billion |

| Growth Rate (2025 - 2030) | 41.83 % CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order. Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

The metaverse market stood at USD 165.57 billion in 2025 and is forecast to reach USD 950.23 billion by 2030, expanding at a 41.83% CAGR, which places it among the fastest-growing technology segments worldwide. Intensifying enterprise demand for industrial digital twins, immersive commerce and real-time collaboration platforms is accelerating mainstream adoption. Rapid advances in AR/VR optics, cloud-edge infrastructure and 5G network slicing are compressing latency and broadening addressable use cases. Big Tech capital-expenditure cycles topping USD 80 billion annually provide the compute backbone and developer tooling that smaller firms quickly leverage for vertical-focused solutions. Monetization is diversifying from advertising toward virtual goods, subscriptions and industrial services, underpinning longer-term revenue stability. Meanwhile, privacy regulation, sustainability scrutiny and hardware ergonomics remain the principal brake on full-scale consumer uptake.

Key Report Takeaways

Note: Market size and forecast figures in this report are generated using Mordor Intelligence's proprietary estimation framework, updated with the latest available data and insights as of 2026.

Drivers Impact Analysis

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline | |||

|---|---|---|---|---|---|---|

Convergence of gaming & social media platforms Convergence of gaming & social media platforms | 8.50% | Global, with APAC leadership in social commerce integration | Medium term (2-4 years) | (~) % Impact on CAGR Forecast:8.50% | Geographic Relevance:Global, with APAC leadership in social commerce integration | Impact Timeline:Medium term (2-4 years) |

Advances in AR/VR hardware & networking Advances in AR/VR hardware & networking | 7.20% | North America & EU leading R&D, APAC manufacturing scale | Long term (≥ 4 years) | |||

Heavy capex by Big Tech ecosystems Heavy capex by Big Tech ecosystems | 6.80% | Global, concentrated in US tech giants and Chinese platforms | Short term (≤ 2 years) | |||

Generative-AI driven content cost collapse Generative-AI driven content cost collapse | 5.10% | Global, with early gains in content creation hubs | Short term (≤ 2 years) | |||

5G/6G network-slicing enabling B2B metaverse 5G/6G network-slicing enabling B2B metaverse | 4.30% | APAC core, spill-over to North America and EU | Medium term (2-4 years) | |||

Enterprise digital transformation acceleration Enterprise digital transformation acceleration | 3.70% | Global, with North America and EU leading enterprise adoption | Medium term (2-4 years) | |||

| Source: Mordor Intelligence | ||||||

Convergence of Gaming & Social Media Platforms

Roblox’s integration of social commerce let developers earn USD 922.8 million in 2024, a 25% rise that accompanied 97.8 million daily active users in Q1 2025. Seamless in-experience purchasing removes friction between engagement and transaction, pushing longer session times and higher average revenue per user. WPP’s global pact with Roblox to define 3-D brand-engagement metrics shows advertisers shifting budget toward immersive placements. Retailers are following: Walmart’s link-up with Unity allows physical goods to be bought inside virtual worlds, turning gameplay into a direct sales channel. The momentum demonstrates how a gaming foundation speeds user acquisition for social-commerce extensions. As these ecosystems mature, incremental ad spend migrates from flat-screen social feeds to interactive worlds, lifting the overall metaverse market. [1]Roblox Corporation, “Roblox Reports First Quarter 2025 Financial Results,” ir.roblox.com

Advances in AR/VR Hardware & Networking

Apple’s Vision Pro carries a USD 3,500 list price yet its bill of materials is USD 1,542, largely driven by micro-OLED screens and custom silicon that compress size and weight. Meta responded with the USD 299 Quest 3S, lowering the consumer entry cost by 40% compared with its predecessor. In industrial settings Siemens and Sony unveiled a USD 4,750 headset optimized for prolonged design reviews, underscoring enterprises’ willingness to pay premium for productivity gains. On the network side, Ericsson forecasts 6G commercial rollout by 2030, requiring about 3 GHz of contiguous spectrum for wide-area coverage, a leap that will render cloud-rendered immersive scenes nearly lag-free. These combined hardware and network advances shrink barriers to adoption, reinforcing the positive CAGR impulse. [2]CNBC, “Here's why the $3,500 Apple Vision Pro headset is so expensive,” cnbc.com

Heavy Capex by Big Tech Ecosystems

Microsoft plans roughly USD 80 billion in 2025 capital outlays to scale Azure, whose AI services grew 33% year-over-year. Meta spent USD 14.3 billion for 49% of Scale AI to secure core large-language-model talent for immersive content automation. Disney placed USD 1.5 billion into Epic Games to weave Marvel and Star Wars IP across Fortnite’s persistent universe. OpenAI’s Stargate data-center campus will house 400,000 NVIDIA GPUs drawing 1.2 GW of power, epitomizing the scale of compute required for photoreal worlds. Such outsized spending accelerates platform capabilities and fuels third-party developer ecosystems, raising the ceiling for the metaverse market.

5G/6G Network-Slicing Enabling B2B Metaverse

Enterprise 5G revenues are set to lift the telecom sector from USD 3 trillion in 2024 to USD 4 trillion by 2028 as firms adopt AR/VR for shop-floor collaboration. The 5G IoT sub-segment scales from USD 13 billion in 2023 to USD 60 billion by 2028, wiring factories for real-time digital twins. IOWN Global Forum, backed by Microsoft, Google and Intel, is piloting all-photonic networks that promise low-energy, terabit-speed backbones aligned with 6G roadmaps. Renault already connects 15,000 devices and saves EUR 700 million through its plant-wide metaverse, proving tangible ROI. Dedicated network slices thus transform immersive collaboration from proof-of-concept to mission-critical workflow, fuelling premium connectivity revenue.

Restraints Impact Analysis

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline | |||

|---|---|---|---|---|---|---|

Privacy, accessibility & regulatory constraints Privacy, accessibility & regulatory constraints | -4.20% | EU leading regulation, global compliance spillover | Long term (≥ 4 years) | (~) % Impact on CAGR Forecast:-4.20% | Geographic Relevance:EU leading regulation, global compliance spillover | Impact Timeline:Long term (≥ 4 years) |

High headset cost & motion sickness High headset cost & motion sickness | -3.80% | Global, particularly impacting mass market adoption | Medium term (2-4 years) | |||

Interoperability challenges between platforms Interoperability challenges between platforms | -2.90% | Global, with fragmentation most acute in Web3 platforms | Long term (≥ 4 years) | |||

GPU datacenter carbon-footprint scrutiny GPU datacenter carbon-footprint scrutiny | -2.10% | Global, with stricter enforcement in EU and California | Long term (≥ 4 years) | |||

| Source: Mordor Intelligence | ||||||

Privacy, Accessibility & Regulatory Constraints

The EU’s Digital Services Act augments GDPR by obliging platforms to curb harmful content and protect biometric data harvested by eye-tracking and gesture sensors. Roblox combines AI and 2,400 human moderators to police 380 million users, illustrating the steep compliance overhead. OECD guidance urges cross-border alignment on AI ethics, further raising governance complexity. Motion sickness and bulky form factors hinder prolonged use, especially where workforce safety standards are stringent. Together these factors temper consumer and enterprise rollouts, trimming the metaverse market’s upward slope.

High Headset Cost & Motion Sickness

Even after Meta’s USD 299 Quest 3S price move, an entry headset remains a discretionary outlay. Bulk purchase decisions in education and healthcare still hinge on ergonomic ratings and duty-cycle limitations. Apple’s premium Vision Pro targets professionals yet excludes cost-sensitive segments. Ergonomic advances are progressing, but until average session comfort surpasses two hours, mass adoption will lag the content and network readiness curve.

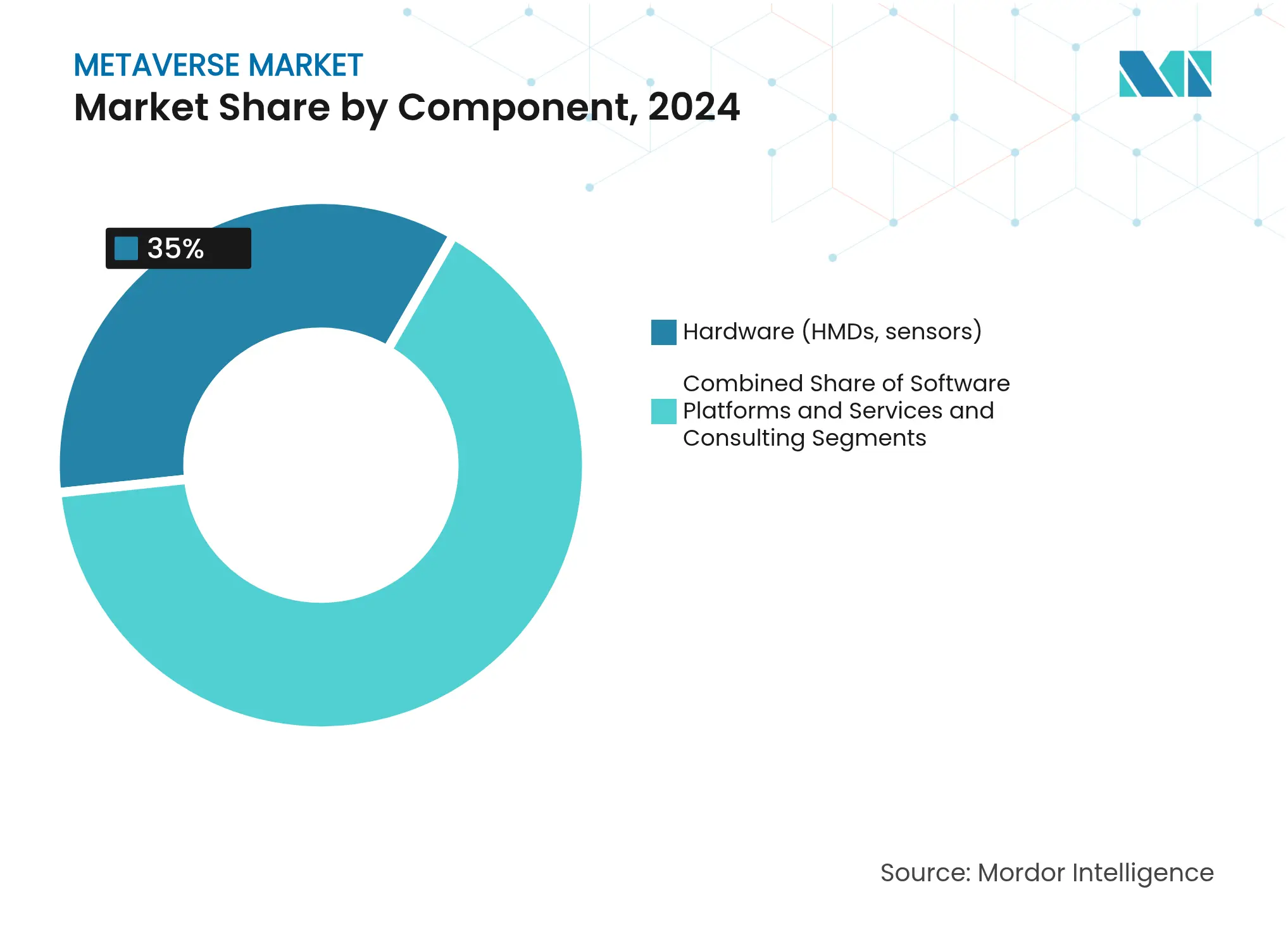

By Component: Hardware Drives Initial Adoption

Hardware captured 35% of the metaverse market share in 2024 as head-mounted displays, sensors and controllers form the user entry point. Segment revenue will soften to single-digit share by 2030 as services outpace unit growth but remains a vital on-ramp for new users. Services & consulting, growing at a 48% CAGR, reflects enterprise need for integration, change management and cybersecurity support. The metaverse market size allocated to this advisory layer is projected to overtake hardware spending by 2028.

Price compression is accelerating. Meta’s USD 299 Quest 3S and China-based ODM volume production cut average headset pricing by 22% in 2024 alone. Conversely, industrial buyers embrace premium devices such as Siemens-Sony’s USD 4,750 HMD, paying for durable optics and all-day comfort. This barbell pricing fuels divergent margin profiles across consumer and enterprise channels. Software platforms, meanwhile, deliver recurring license revenue that cushions hardware volatility, underscoring a strategic pivot from capital goods toward subscription economics. [3]CNBC, “Meta unveils $299 Quest 3S VR headset, Orion AR glasses prototype,” cnbc.com

Note: Segment shares of all individual segments available upon report purchase

By Platform Type: Centralized Dominance Faces Decentralized Challenge

Centralized ecosystems held 46% of the metaverse market in 2024, benefitting from seamless hardware-software optimization and curated content safeguards. Reality Labs and Apple Vision stacks exemplify closed-loop control that reduces latency and simplifies payment flows. Industrial digital-twin platforms, however, will expand at a 45% CAGR as manufacturers digitize plants to trim downtime and inventory.

Open decentralized networks lag in user adoption due to wallet UX friction and high gas fees, yet they gain traction in creator economies where true asset ownership is prized. NVIDIA’s Omniverse positions itself as a quasi-open hub, interfacing with USD and Pixar’s open-source standards while selling premium compute and AI services. The coming decade will likely see hybrid architectures where permissioned blockchains interoperate with managed cloud back-ends, balancing interoperability with performance.

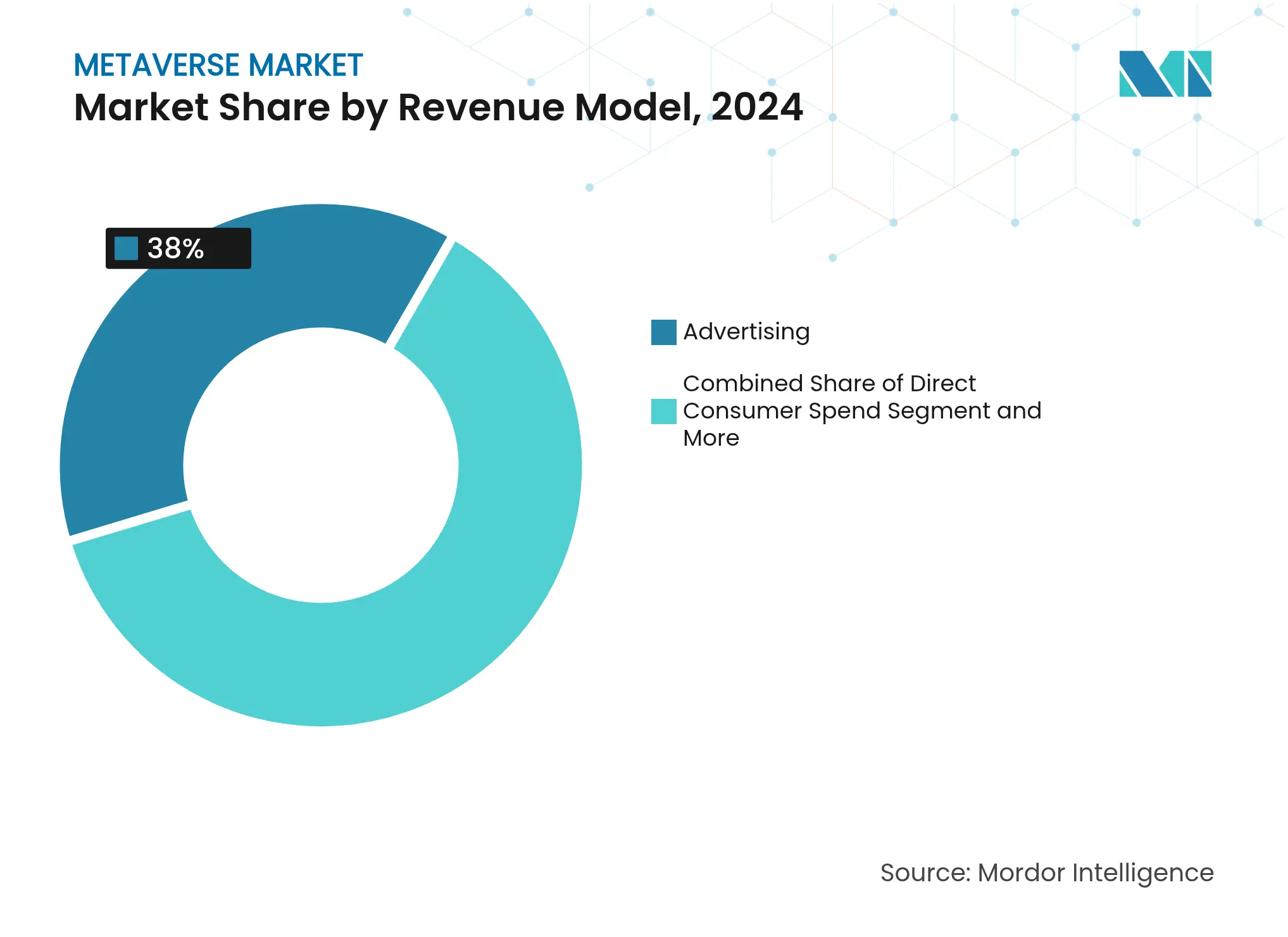

By Revenue Model: Advertising Leads Monetization Evolution

Advertising supplied 38% of the metaverse market size in 2024 as brands shift budget from social feeds to immersive placements. In-world billboards, branded mini-games and event sponsorships deliver higher dwell times than static banners. Yet virtual goods & NFTs, forecast to grow 47% CAGR, illustrate the rise of direct micro-transactions.

Roblox paid out USD 922.8 million to creators in 2024, with over 750 developers earning six-figure incomes, proving virtual asset income sustainability. Enterprise SaaS subscriptions also rise as digital-twin vendors bundle analytics and remote-assist features. This income diversity de-risks platform P&Ls compared with ad-only models. [4]SEC, “Roblox Corp Form 10-K,” sec.gov

Note: Segment shares of all individual segments available upon report purchase

By End-User Industry: Gaming Foundation Enables Enterprise Expansion

Gaming & esports supplied the user funnel and delivered 42% of 2024 revenue, yet corporate/industrial deployments will grow fastest at 44% CAGR. Digital twins cut factory defect rates and training simulations shorten onboarding cycles, delivering clear ROI that accelerates budget approvals.

Media & live entertainment exploits the metaverse for fan engagement, highlighted by Disney’s stake in Epic Games to generate persistent Marvel and Star Wars experiences. Retail & e-commerce hybridize storefronts with virtual try-ons, while education pilots VR labs that remove hazardous real-world variables. These adjacent verticals compound demand, reinforcing the metaverse market’s expansion path.

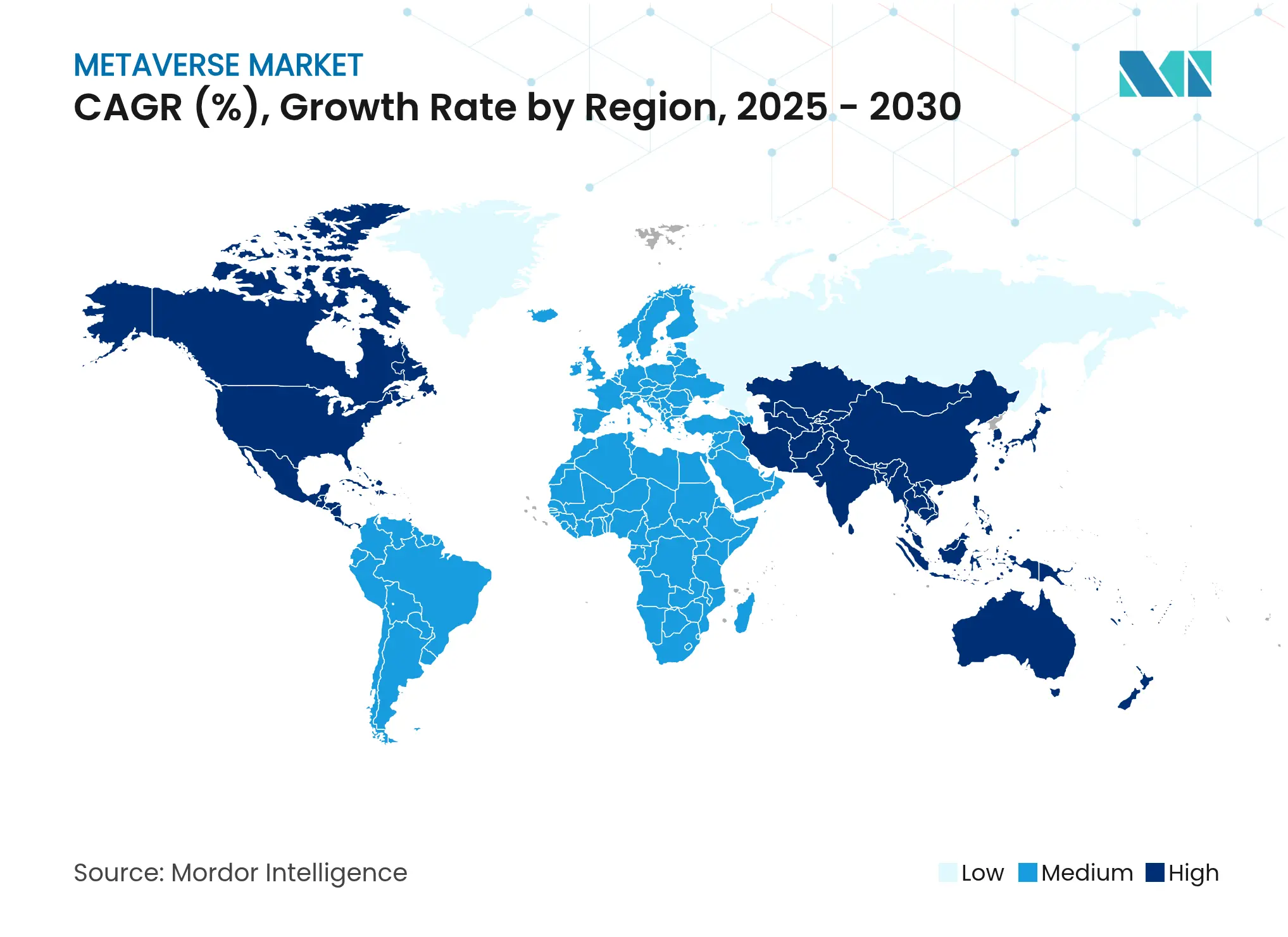

North America controlled 41% of 2024 revenue, thanks to hyperscale cloud density and venture capital depth. Microsoft’s Azure build-out and Meta’s Reality Labs anchor a supplier ecosystem ranging from optics to AI middleware. Regulatory concern over energy use, though, could temper future datacenter approvals, nudging firms toward energy-efficient designs.

Asia-Pacific is on track for a 43% CAGR through 2030, underpinned by a USD 880 billion mobile economy and 1.8 billion mobile internet users. The region leapfrogged desktop to mobile payments and social video, providing a template for rapid metaverse uptake. China’s hardware manufacturing scale cuts BOM costs, while Japan and South Korea’s esports cultures supply early adopter communities. Advanced 5G rollouts with network slicing enable factory-floor AR maintenance, crucial for industrial adoption.

Europe balances innovation with stringent privacy laws. The European Parliament’s 2024 guidance applies existing offline illegality within virtual worlds, obliging platforms to install real-time content filters. Compliance adds time-to-market friction yet builds consumer trust, potentially turning into a differentiation asset. Emerging regions in South America and Middle East & Africa may skip legacy PC phases altogether by implementing cloud-rendered XR streamed to low-cost devices once local 5G coverage matures.

Market Concentration

The metaverse market is fragmented, with no single vendor holding double-digit holistic share across hardware, software and services. Meta’s Reality Labs posted a cumulative USD 58 billion loss since 2020 on USD 270 million Q3 2024 revenue, underscoring heavy upfront capex. Roblox represents a profitable creator-focused model, pulling USD 1.04 billion in Q1 2025 revenue on 29% year-over-year growth.

Apple invests an estimated USD 33 billion to secure a premium stack, filing more than 20,000 patents that lock users into its closed ecosystem. NVIDIA advances an infrastructure-first play, embedding Omniverse into enterprise CAD pipelines through alliances with Accenture and Siemens. Acquisition activity remains brisk: CoStar took over Matterport for USD 1.6 billion to blend digital twins with real-estate listings, showing vertical specialists can command strategic premiums.

Start-ups focus on niche pain points—medical-device training, avatar middleware, spatial-audio meshes—capitalizing on gaps left by platform giants fixated on scale. These dynamics indicate a maturing yet unconsolidated field where partnership networks and open standards will shape competitive moats more than raw device shipments.

*Disclaimer: Major Players sorted in no particular order

1. INTRODUCTION

2. RESEARCH METHODOLOGY

3. EXECUTIVE SUMMARY

4. MARKET LANDSCAPE

5. MARKET SIZE AND GROWTH FORECASTS (VALUE)

6. COMPETITIVE LANDSCAPE

7. MARKET OPPORTUNITIES AND FUTURE OUTLOOK

The term "metaverse" refers to a highly immersive 3D virtual world experience obtained using a combination of AR, VR, and MR technologies. By creating a virtual world where users can play immersive games, conduct business, interact socially, buy and sell virtual properties, and enjoy immersive entertainment, the metaverse platform enhances the overall internet experience.

The metaverse market is segmented by type (AR & VR hardware, social media engagement (Ads), virtual live entertainment - epic, games and roblox, gaming services), by end-user industry (gaming, media & entertainment, commercial, retail), and geography (North America, Europe, Asia Pacific, Rest of the World).

The market sizes and forecasts are provided in terms of value (USD) for all the above segments.

Pricing Strategy for Semiconductor Components

3 Min Read

Accelerating Additive Manufacturing Adoption in India

3 Min Read

Wealth Management Intelligence for the Middle East

4 Min Read

When decisions matter, industry leaders turn to our analysts. Let’s talk.