Smart Cities And Critical Infrastructure Security Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

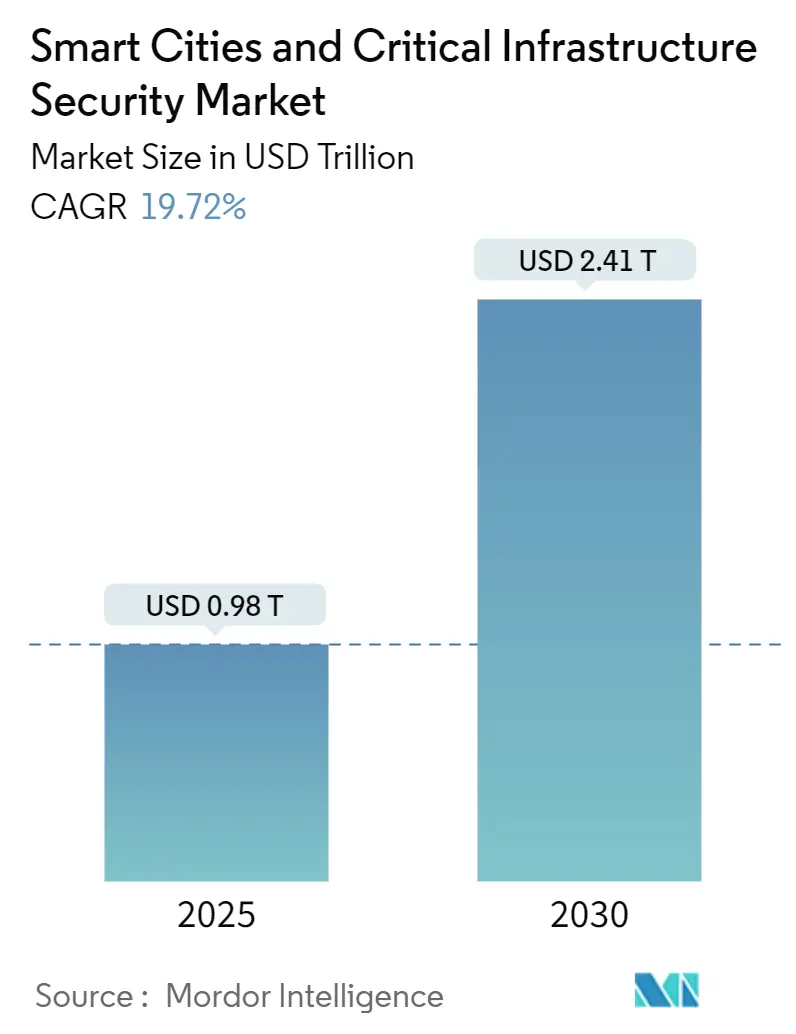

| Market Size (2025) | USD 0.98 Trillion |

| Market Size (2030) | USD 2.41 Trillion |

| Growth Rate (2025 - 2030) | 19.72% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Smart Cities And Critical Infrastructure Security Market Analysis by Mordor Intelligence

The Smart Cities and Critical Infrastructure Security market size is valued at USD 0.98 trillion in 2025 and is forecast to reach USD 2.41 trillion by 2030, translating into a 19.72% CAGR during the period. Geopolitical rivalry, federally funded modernization programs, and rapid roll-outs of AI-enabled sensor networks are prompting cities to treat cyber-physical resilience as a national security priority.[1]Cybersecurity and Infrastructure Security Agency, “State and Local Cybersecurity Grant Program,” cisa.gov North America’s Cybersecurity Grant Program and the European Union’s Digital Europe investments together signal a coordinated public-sector push that has accelerated procurements of converged OT-IT platforms.[2]European Commission, “Digital Europe Programme Cybersecurity Work Programme,” europa.eu Services are advancing faster than hardware as municipal buyers shift toward outcome-based, long-term contracts, while cloud and edge architectures lower entry barriers for real-time analytics. Escalating nation-state attacks—such as the April 2025 Iberian grid disruption—continue to justify urgent budget reallocations toward critical infrastructure defense.

Key Report Takeaways

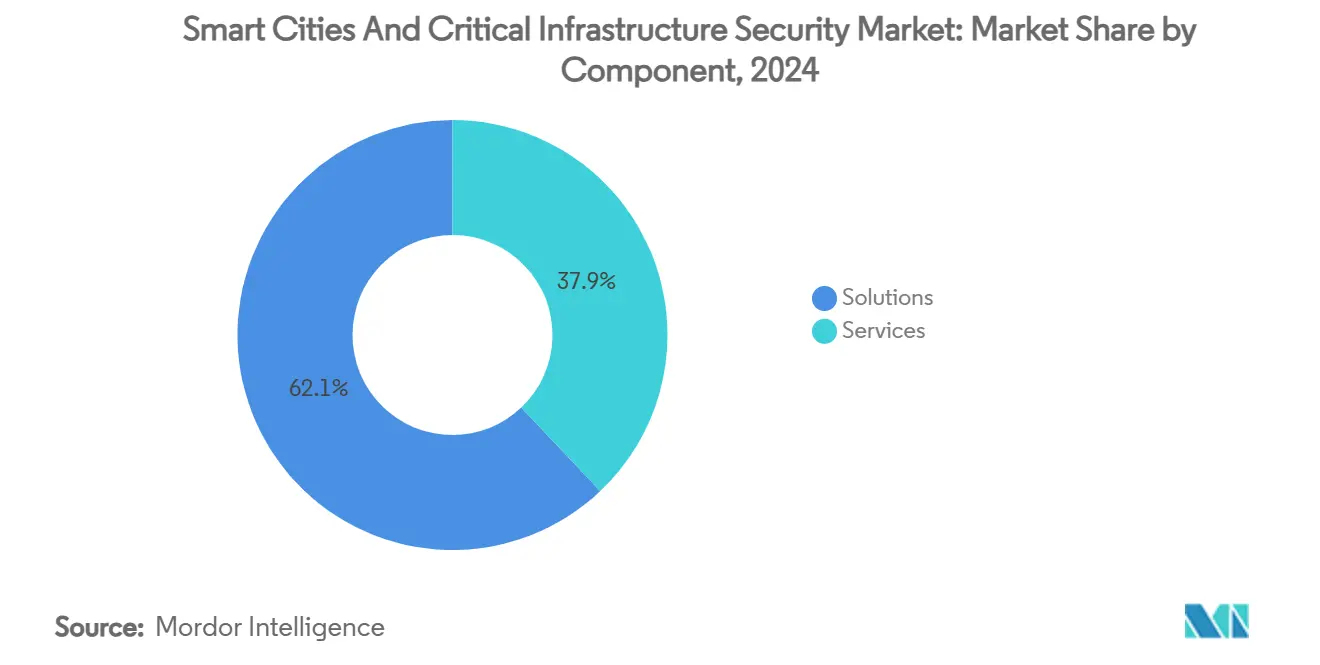

- By component, Solutions captured 62.07% of the Smart Cities and Critical Infrastructure Security market share in 2024; Services are forecast to expand at a 21.07% CAGR through 2030.

- By security type, Physical Security retained 43.21% revenue in 2024, while Cybersecurity is projected to rise at 22.75% CAGR between 2025-2030.

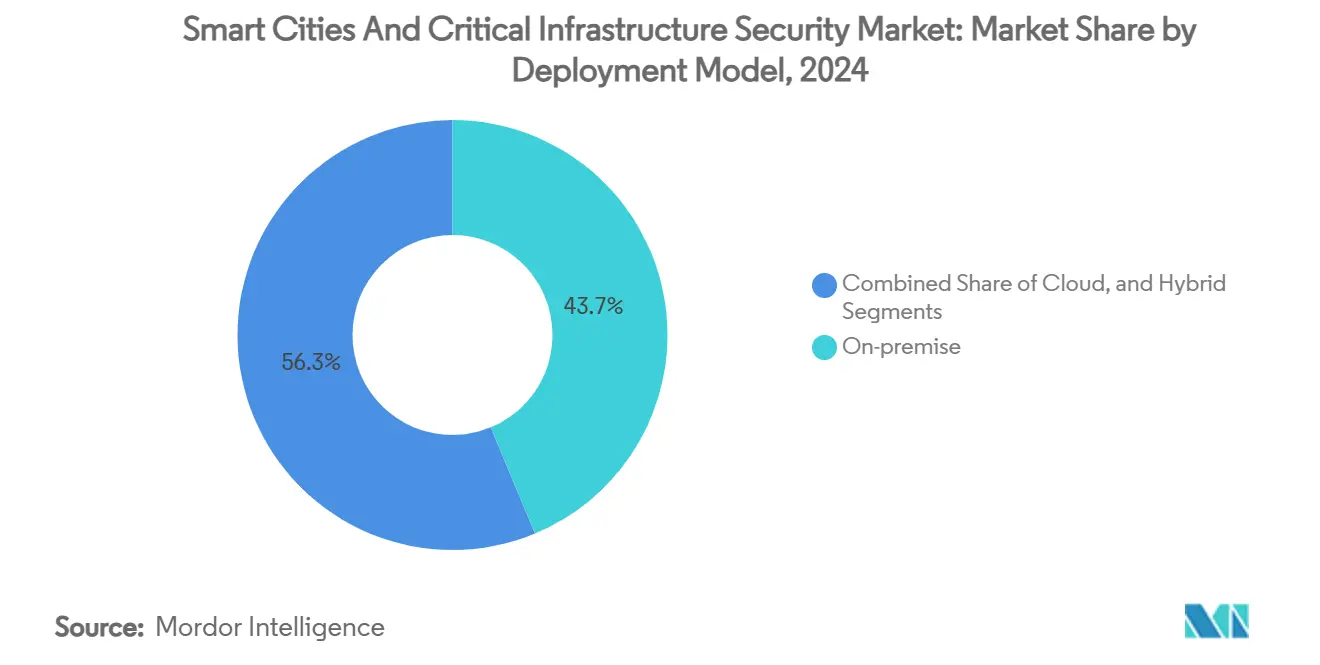

- By deployment model, on-premise installations held 43.74% of 2024 spending, whereas cloud deployments are poised for a 20.07% CAGR to 2030.

- By end-user vertical, Energy and Utilities commanded 28.57% of the Smart Cities and Critical Infrastructure Security market size in 2024, and Transportation & Smart Mobility is set to grow at a 22.09% CAGR during the forecast window.

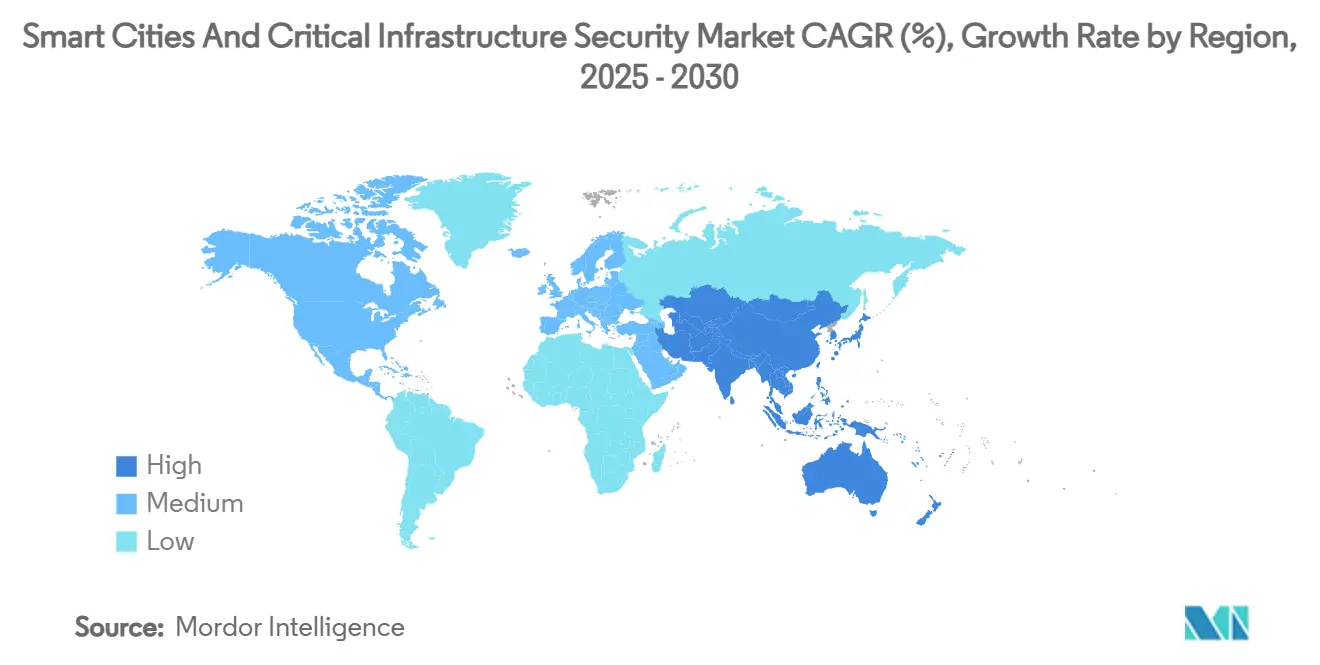

- By geography, North America generated 35.72% of 2024 revenue; Asia-Pacific is expected to post a 23.84% CAGR to 2030.

Global Smart Cities And Critical Infrastructure Security Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| AI-enabled predictive policing and situational awareness platforms | +4.2% | Global, with early adoption in North America & APAC | Medium term (2-4 years) |

| Convergence of OT-IT cyber frameworks for critical utilities | +3.8% | Global, strongest in North America & Europe | Long term (≥ 4 years) |

| National safe-city programs with earmarked budgets | +5.1% | North America & Europe primary, expanding to APAC | Short term (≤ 2 years) |

| 5G network slicing for low-latency public-safety applications | +2.9% | APAC core, spill-over to North America | Medium term (2-4 years) |

| Rise in nation-state attacks on smart grids and transport SCADA | +2.7% | Global, heightened in North America & Europe | Short term (≤ 2 years) |

| ESG-linked municipal bonds tied to resilient infrastructure | +1.5% | North America & Europe, emerging in APAC | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

AI-enabled Predictive Policing and Situational Awareness Platforms

A growing number of transit and law-enforcement agencies now deploy computer-vision analytics that flag anomalous behavior before incidents escalate, turning cameras into proactive sensors rather than passive recorders. The New York City Metropolitan Transportation Authority’s subway pilot exemplifies this paradigm shift, using pattern recognition to trigger alerts that shrink response times.[3]Dominic Preston, “New York City Wants Subway Cameras to Predict ‘Trouble’,” The Verge, theverge.com Korean researchers demonstrated 82.8% crime-forecast accuracy by fusing real-time CCTV feeds with historical data, proving that predictive models can scale to dense urban settings. While early successes are evident, municipalities emphasise governance after Argentina’s controversial social-media-driven crime-prediction plan raised civil-liberty concerns. Cities adopting transparent oversight frameworks-such as San Jose’s public engagement model-are likely to sustain long-term adoption, thereby reinforcing Smart Cities and Critical Infrastructure Security market momentum.

Convergence of OT-IT Cyber Frameworks for Critical Utilities

Utilities are integrating IT visibility tools directly into plant-floor devices to blunt threats that traverse enterprise and process networks. Microsoft’s 2024 findings that 78% of industrial control systems contain exploitable vulnerabilities pushed operators to adopt zero-trust postures that treat every sensor as an attack surface. China-linked Volt Typhoon’s stealth infiltration of Western grids underscored that air-gapped strategies are obsolete. In response, Siemens and ServiceNow launched Sinec Security Guard to combine vulnerability management and workflow orchestration, illustrating how industrial OEMs now package cybersecurity as part of lifecycle support. Converged SOCs give operators real-time anomaly detection across plant assets, strengthening demand across the Smart Cities and Critical Infrastructure Security market.

National Safe-city Programs with Earmarked Budgets

Targeted federal and supranational grants are compressing sales cycles by supplying municipalities with predefined funding lines. The US SMART Grants program alone has financed 127 planning projects and USD 85 million in implementation awards for connected vehicles and smart traffic signals. Parallel infrastructure law allocations earmark USD 65 billion for smart energy grids and USD 55 billion for digital water systems, creating cross-domain security requirements that multiply addressable spending. Europe’s Connecting Europe Facility injects EUR 1.69 billion (USD 1.83 billion) into dual-use transport corridors, ensuring that cybersecurity considerations are baked into civil-military logistics upgrades. These synchronized programs accelerate purchase decisions, supporting a robust pipeline for the Smart Cities and Critical Infrastructure Security market.

5G Network Slicing for Low-latency Public-safety Applications

Stand-alone 5G cores now offer logical slices that dedicate bandwidth to first responders during emergencies. T-Mobile’s T-Priority promises up to 5× network resources for approved agencies and has already been adopted by New York City public safety departments. Verizon’s Frontline slice operates across 29 US markets without additional fees, intensifying carrier competition. Beyond terrestrial deployments, Singapore’s Maritime & Port Authority uses 5G slices to run its next-generation vessel traffic system, validating maritime use cases. When combined with edge AI, slicing orchestrates bandwidth dynamically, further growing the Smart Cities and Critical Infrastructure Security market footprint.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Fragmented procurement across city departments | -2.8% | Global, most pronounced in North America & Europe | Medium term (2-4 years) |

| Legacy analog assets delaying sensor roll-outs | -3.2% | Global, particularly challenging in mature markets | Long term (≥ 4 years) |

| Cyber-talent shortages in municipal IT and OT teams | -1.9% | Global, acute in APAC & emerging markets | Long term (≥ 4 years) |

| Privacy-first legislation restricting video analytics | -1.4% | Europe primary, expanding globally | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Fragmented Procurement Across City Departments

Separate departmental budgets impede end-to-end visibility and duplicate cyber purchases. The US Government Accountability Office found that incompatible standards across transport, law enforcement, and utilities inflate costs and slow project approvals. DHS’s interoperability reference architecture offers a blueprint, yet adoption remains voluntary, creating a patchwork of partial implementations. Until governance mechanisms mature, fragmentation will dampen the near-term growth trajectory of the Smart Cities and Critical Infrastructure Security market.

Legacy Analog Assets Delaying Sensor Roll-outs

Many municipalities still operate analog SCADA or copper-based comms that cannot process AI or IoT telemetry. Utilities such as DC Water demonstrate that large-scale retrofits require phased upgrades and staff re-skilling, extending deployment timelines. Chattanooga’s USD 22 million quantum initiative highlights that only well-capitalised entities can leapfrog generations of technology, leaving smaller cities resource-constrained. Prolonged coexistence of analog and digital systems dilutes immediate addressable revenue for vendors in the Smart Cities and Critical Infrastructure Security market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Component: Services Accelerate Lifecycle Adoption

Solutions commanded 62.07% revenue in 2024, illustrating the capital intensity of initial urban sensor grids and integrated command-and-control systems. Municipalities then turn to long-term managed offerings to keep those platforms patched, monitored, and compliant, propelling Services at a 21.07% CAGR toward 2030. Motorola Solutions’ 15-year TETRA maintenance deal with Singapore’s SBS Transit underscores the shift to outcome-based contracting. Siemens’ Xcelerator ecosystem adds field-service AI, representing how OEMs recast themselves as lifecycle partners. Services will therefore anchor recurring revenue across the Smart Cities and Critical Infrastructure Security market.

The convergence of cyber and physical domains means municipal buyers increasingly demand packaged threat-hunting, vulnerability assessments, and compliance reporting. Specialist firms providing 24/7 SOC functions keep critical infrastructure operators within regulatory thresholds, encouraging multi-year contracts that stabilize budgets and strengthen vendor lock-in.

By Security Type: Cybersecurity Outpaces Traditional Physical Controls

Physical infrastructure retained 43.21% revenue in 2024, driven by CCTV, access control, and perimeter hardware. However, cyber platforms grow faster because the attack surface is now dominated by connected devices. The April crash of Iberia’s grid dramatized physical consequences of cyber sabotage, galvanizing utilities to invest in SIEM and zero-trust tools. LogRhythm’s SIEM integration into Singapore’s smart lamp-post network exemplifies how lighting assets become cybersecurity end-points. Cybersecurity will therefore capture an increasing share of Smart Cities and Critical Infrastructure Security market revenue.

Hardware vendors respond by embedding encryption and intrusion detection directly into cameras and controllers, evidenced by Motorola Solutions’ AI-driven Pelco portfolio. As cities adopt unified threat dashboards, demand will coalesce around solutions that correlate cyber and physical events, accelerating cross-segment spend.

By Deployment Model: Cloud and Edge Architectures Scale Analytics

On-premise deployments accounted for 43.74% of 2024 spending because many agencies still perceive local control as synonymous with resilience. Yet device proliferation and the compute demands of AI models make cloud attractive, pushing it toward a 20.07% CAGR. American Water’s cloud metering program shows utilities offloading analytics to hyperscale platforms while retaining operational continuity locally. Edge nodes perform latency-sensitive tasks but sync with cloud dashboards for city-wide situational awareness.

Hybrid models therefore bridge sovereignty and scalability, offering tiered data-residency options. CISA’s AI-enabled vulnerability detection experiment employs a public-cloud backbone but allows local agencies to ingest only sanitized metadata, illustrating a federated approach to threat intelligence. Together, cloud and edge will underpin future growth across the Smart Cities and Critical Infrastructure Security market.

By End-user Vertical: Energy & Utilities Dominate, Mobility Surges

Energy and Utilities led with 28.57% of the Smart Cities and Critical Infrastructure Security market share in 2024, reflecting the sector’s exposure to nation-state adversaries and strict regulatory oversight. The US Department of Energy’s USD 30 million R&D program for next-gen cyber tools further increases sectoral demand. Transportation & Smart Mobility is projected to climb at 22.09% CAGR as connected vehicles and autonomous shuttles proliferate. 5G slices ensure reliable vehicle-to-infrastructure communication, raising the security baseline and expanding addressable spending for vendors.

Smart Buildings form a secondary growth pocket as landlords integrate IoT sensors for energy optimisation and occupant safety. Government and Public Safety Agencies sustain demand through grant-funded roll-outs like DHS’s SCITI Labs that test interoperable IoT devices. Water & Waste-management utilities accelerate upgrades after a spate of cyber intrusions, adding remote monitoring and digital twins that require robust endpoint hardening.

Geography Analysis

North America generated 35.72% of 2024 revenue on the back of the Infrastructure Investment and Jobs Act and high-profile projects such as Texas’s USD 135.5 million Cyber Command, which positions San Antonio as a national threat-intelligence hub. Strong federal-state collaboration, deep vendor ecosystems, and mature insurance markets collectively provide a stable runway for continued investment.

Europe benefits from EUR 390 million (USD 422 million) in Digital Europe Programme financing for 2025-2027, incentivising cross-border projects that embed privacy-by-design principles. Strict data-protection laws push municipalities toward local-cloud or on-premise deployments, strengthening regional solution providers that specialise in compliance-oriented offerings.

Asia-Pacific is the fastest-growing region, posting a 23.84% CAGR, fuelled by Singapore’s Smart Nation initiatives and rising cybercrime that now accounts for 31% of global incidents. Rapid urbanisation in Southeast Asian and South Asian cities multiplies infrastructure projects where security is embedded from the design phase. Domestic firms with local-language support and regulatory insight gain early traction, reshaping competitive dynamics in the Smart Cities and Critical Infrastructure Security market.

Competitive Landscape

The market exhibits moderate concentration, with diversified industrial conglomerates anchoring multi-year city deals while cybersecurity specialists capture niche workloads. Siemens reported EUR 6.0 billion (USD 6.5 billion) in Smart Infrastructure orders for Q3 2024, underlining the pull-through from its installed base of building-automation and grid-control systems. Partnerships now decide addressable scope: Siemens–ServiceNow integrates generative-AI workflows to automate patch management; Motorola Solutions pivots into managed services via its Pelco acquisition, bundling edge AI cameras with SOC capabilities.

Emergent players tackle identity, quantum-safe encryption, and AI-driven anomaly detection. Semperis’ Singapore expansion signals regional focus on Active Directory hardening for critical services. Managed SOC vendors leverage subscription pricing to undercut capital-heavy offerings, appealing to mid-tier municipalities that lack deep technical staff.

Vendor differentiation increasingly hinges on integration agility across OT protocols, cloud APIs, and regulatory reporting templates. Those able to collapse multiple functions—video analytics, network monitoring, asset management—into a single pane of glass are best placed to grow wallet share within the Smart Cities and Critical Infrastructure Security market.

Smart Cities And Critical Infrastructure Security Industry Leaders

Cisco Systems Inc.

International Business Machines Corporation (IBM)

Honeywell International Inc.

Johnson Controls International plc

Siemens AG

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2025: Texas Governor Greg Abbott signed legislation establishing the Texas Cyber Command at the University of Texas at San Antonio, with USD 135.5 million in funding through 2027 to create 130 jobs and develop a Cyber Threat Intelligence Center for protecting state government systems and critical infrastructure.

- April 2025: Chattanooga’s EPB utility announced the purchase of a USD 22 million quantum computer in partnership with IonQ, expected to be operational by early 2026, aimed at enhancing cybersecurity for critical infrastructure and improving operational efficiencies through quantum computing applications.

- March 2025: The European Cybersecurity Competence Centre adopted its first Cybersecurity Work Programme under the Digital Europe Programme for 2025-2027, allocating EUR 390 million (USD 422 million) for projects focused on AI technologies, post-quantum cryptography, and critical infrastructure protection.

- February 2025: T-Mobile formally launched T-Priority, a 5G network-slicing service for first responders, with New York City selecting T-Mobile as its primary carrier for public safety agencies, providing up to 5 times the network resources compared to average users.

Global Smart Cities And Critical Infrastructure Security Market Report Scope

| Network Security |

| Application Security |

| Cloud and Virtualization Security |

| Data and Encryption Security |

| Identity and Access Management |

| Security Analytics/SIEM |

| Managed Security Services |

| Lawful Interception Solutions |

| On-Premise |

| Cloud |

| Hybrid |

| Physical Layer Security |

| Transport Layer |

| Signalling Security |

| Application Layer Security |

| Control-Plane Security |

| Tier-1 CSPs / Large Telecom Groups |

| Regional and MVNO / SME Operators |

| Professional Services (Consulting and Integration) |

| Managed Security Services |

| Security-as-a-Service (SECaaS) |

| Incident Response and Forensics |

| Training and Certification |

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | United Kingdom | |

| Germany | ||

| France | ||

| Italy | ||

| Spain | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| South Korea | ||

| India | ||

| Australia | ||

| Indonesia | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Argentina | ||

| Chile | ||

| Rest of South America | ||

| Middle East and Africa | Middle East | United Arab Emirates |

| Turkey | ||

| Saudi Arabia | ||

| Israel | ||

| Qatar | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Nigeria | ||

| Kenya | ||

| Egypt | ||

| Rest of Africa | ||

| By Solution Type | Network Security | ||

| Application Security | |||

| Cloud and Virtualization Security | |||

| Data and Encryption Security | |||

| Identity and Access Management | |||

| Security Analytics/SIEM | |||

| Managed Security Services | |||

| Lawful Interception Solutions | |||

| By Deployment Mode | On-Premise | ||

| Cloud | |||

| Hybrid | |||

| By Security Layer | Physical Layer Security | ||

| Transport Layer | |||

| Signalling Security | |||

| Application Layer Security | |||

| Control-Plane Security | |||

| By Organization Size | Tier-1 CSPs / Large Telecom Groups | ||

| Regional and MVNO / SME Operators | |||

| By Service Model | Professional Services (Consulting and Integration) | ||

| Managed Security Services | |||

| Security-as-a-Service (SECaaS) | |||

| Incident Response and Forensics | |||

| Training and Certification | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| Europe | United Kingdom | ||

| Germany | |||

| France | |||

| Italy | |||

| Spain | |||

| Russia | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| Japan | |||

| South Korea | |||

| India | |||

| Australia | |||

| Indonesia | |||

| Rest of Asia-Pacific | |||

| South America | Brazil | ||

| Argentina | |||

| Chile | |||

| Rest of South America | |||

| Middle East and Africa | Middle East | United Arab Emirates | |

| Turkey | |||

| Saudi Arabia | |||

| Israel | |||

| Qatar | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Nigeria | |||

| Kenya | |||

| Egypt | |||

| Rest of Africa | |||

Key Questions Answered in the Report

What is the forecast value of the Smart Cities and Critical Infrastructure Security market by 2030?

The market is projected to reach USD 2.41 trillion by 2030, growing at a 19.72% CAGR.

Which component is expanding fastest within smart-city security programs?

Services, supported by long-term managed contracts, are forecast to rise at 21.07% CAGR through 2030.

Why is Asia-Pacific the fastest-growing region for smart-city security spending?

Comprehensive national initiatives, rapid urbanisation, and a rising share of global cyber incidents drive a 23.84% CAGR in APAC.

How are 5G network slices improving public-safety communications?

They allocate dedicated bandwidth to first responders, ensuring reliable low-latency connectivity during emergencies without compromising commercial traffic.

Which end-user vertical currently spends the most on converged security solutions?

Energy and Utilities leads, holding 28.57% of 2024 market share due to regulatory mandates and national-security concerns.

What factor most constrains municipal roll-outs of advanced analytics?

Legacy analog systems that cannot interface with AI-driven sensors extend upgrade timelines and increase project complexity.

Page last updated on: