Europe Data Center Physical Security Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

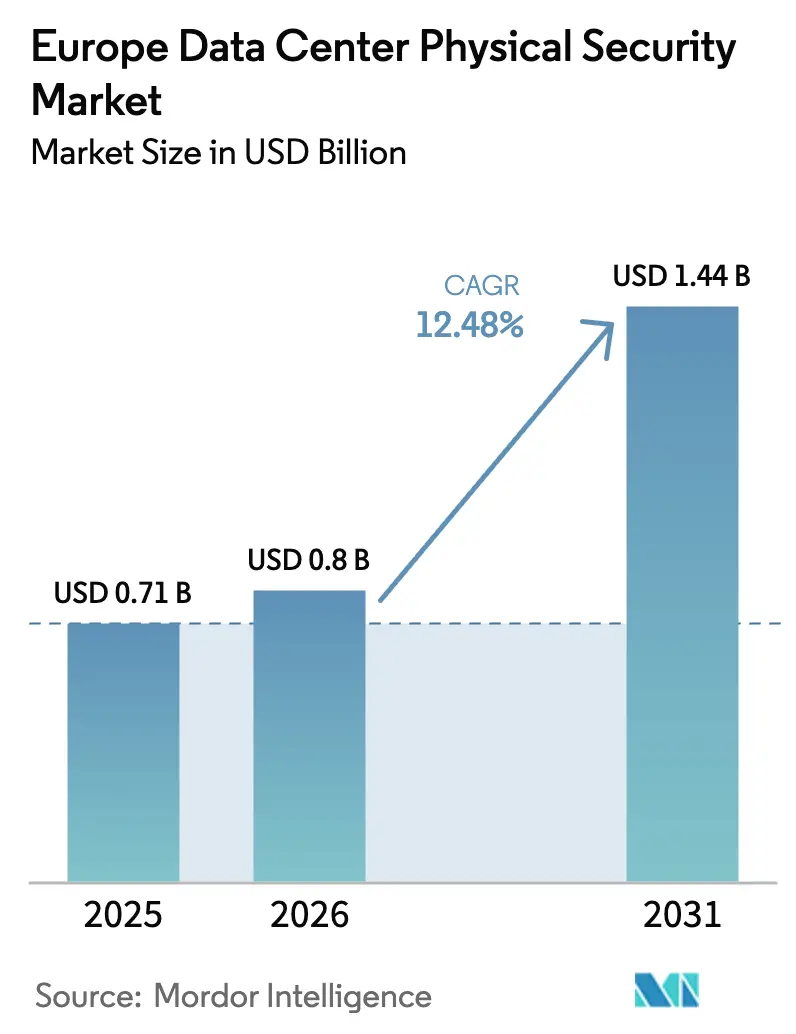

| Base Year Market Size (2025) | USD 0.71 Billion |

| Market Size (2026) | USD 0.8 Billion |

| Market Size (2031) | USD 1.44 Billion |

| Growth Rate (2026 - 2031) | 12.48% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Europe Data Center Physical Security Market Analysis by Mordor Intelligence

Europe data center physical security market size in 2026 is estimated at USD 0.80 billion, growing from 2025 value of USD 0.71 billion with 2031 projections showing USD 1.44 billion, growing at 12.48% CAGR over 2026-2031. Momentum stems from three forces: hyperscale buildouts across the FLAPD corridor, EU-level regulations that tighten compliance obligations, and rapid uptake of AI-driven surveillance and access control platforms. Capital is flowing toward giga-scale projects such as BSO’s 400 MW “DataOne” campus in France, while operators redirect budgets from stand-alone hardware to integrated, zero-trust systems able to align physical and logical controls. Supply-chain disruptions for hardened chips remain a drag on deployment schedules, yet sustained demand from cloud, edge, and AI workloads keeps growth trajectories intact. Competitive intensity is escalating as global conglomerates deepen portfolios through acquisitions that add compliance management and managed-service capabilities.

Key Report Takeaways

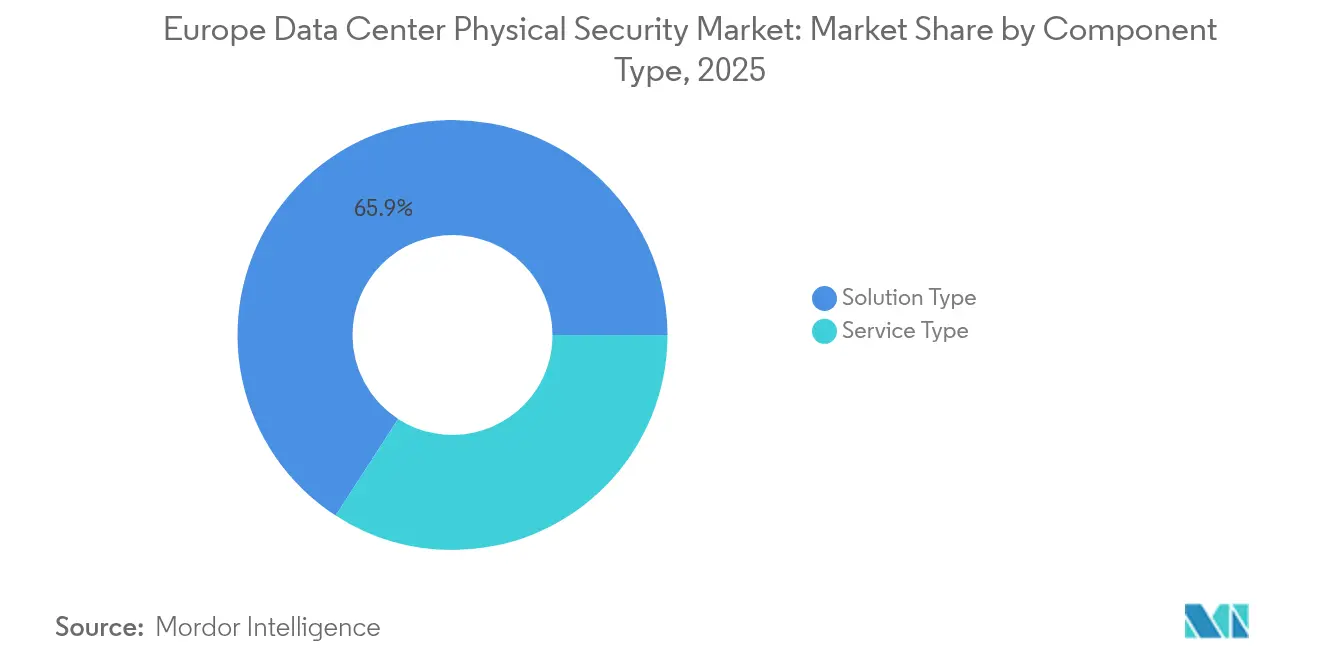

- By component, solution-type offerings led with 65.85% of the Europe data center physical security market share in 2025, while service lines are accelerating at a 16.44% CAGR through 2031.

- By data-center tier, Tier III sites captured 58.35% of the Europe data center physical security market share in 2025; Tier IV facilities are on track for the fastest 17.08% CAGR to 2031.

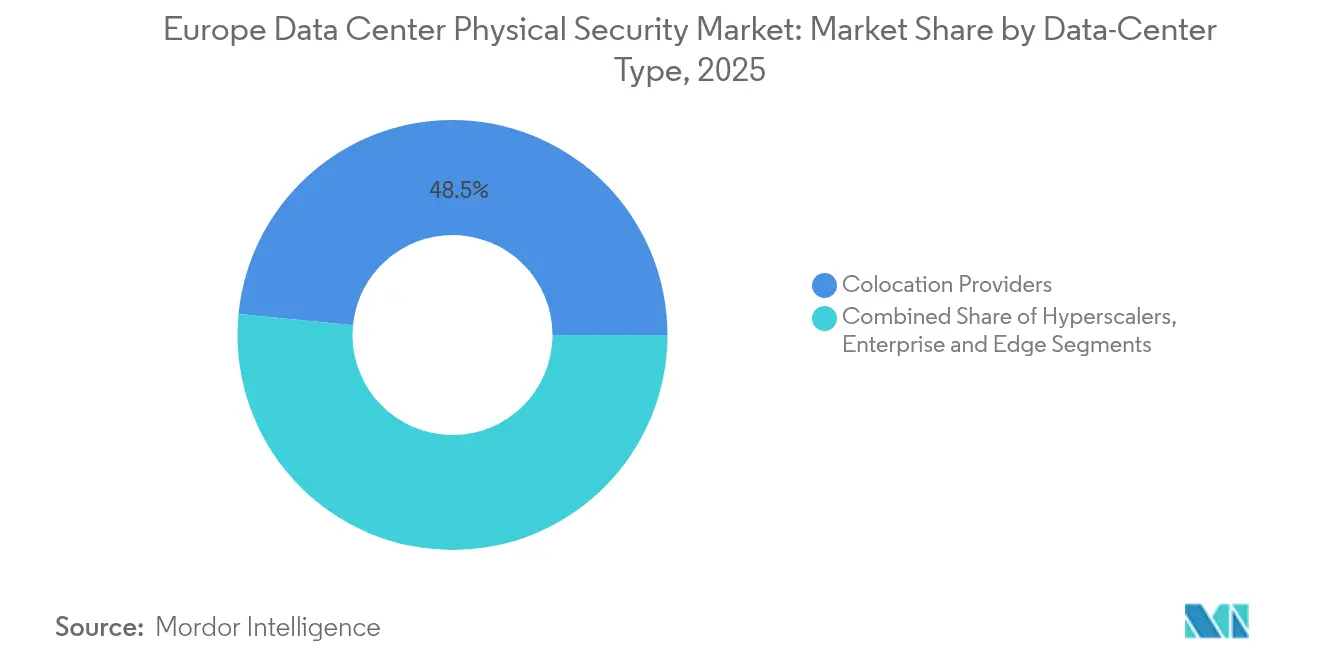

- By data-center type, colocation providers accounted for 48.45% revenue in 2025, whereas hyperscalers are expanding at a 16.12% CAGR to 2031.

- By country, the United Kingdom held 16.45% revenue in 2025; Ireland is projected to grow at 14.12% CAGR through 2031.

- Johnson Controls, Schneider Electric, Honeywell, and ASSA ABLOY collectively commanded an estimated 31.60% share of 2025 EMEA revenues tied to data-center physical security j

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Competitive positioning in Europe reflects both domestic market structures and the presence of firms operating internationally. The market landscape study of the global data center physical security industry shows how these players are arranged across regions.

Europe Data Center Physical Security Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Hyperscale and colocation build-outs across FLAPD corridor | +3.2% | FLAPD, widening to Tier 2 cities | Medium term (2-4 years) |

| EU Cyber Resilience Act mandating Class II secure-by-design hardware | +2.8% | EU-wide, early in Germany and Netherlands | Short term (≤ 2 years) |

| AI-enabled VSaaS for 24/7 remote guarding | +2.1% | UK and Nordics | Medium term (2-4 years) |

| Shift to zero-trust physical-logical convergence architectures | +1.9% | Enterprise and hyperscaler estates | Long term (≥ 4 years) |

| Carbon-neutral designs driving sensor-based intrusion systems | +1.4% | Nordics and Germany | Long term (≥ 4 years) |

| Edge-site proliferation requiring rack-level biometric locks | +1.3% | Urban 5G corridors | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Hyperscale and Colocation Build-outs Across FLAPD Corridor

Hyperscale expansions are redrawing the competitive map for the Europe data center physical security market. Vantage Data Centers earmarked EUR 1.4 billion for its EMEA platform in 2025, signalling multi-site rollouts that lift demand for perimeter analytics, integrated access management, and explosion-rated fencing.[1] Vantage Data Centers, “Vantage Closes First Euro-Denominated ABS,” vantage-dc.com Capacity pressure in core metros is pushing operators into Tier 2 locations such as Madrid, where national capacity is on track to exceed 600 MW by 2026. New builds position security at blueprint stage, inserting smart bollards, license-plate analytics, and unified incident response rooms that link to corporate SOCs. Sustainability targets also influence physical layouts: EcoDataCenter’s SEK 18 billion Swedish campus combines low-carbon construction with microgrid-powered surveillance for round-the-clock operation. High rack densities and AI workloads mean every square meter now concentrates more asset value, reinforcing the business case for advanced analytics and biometric multi-factor controls. Providers that can scale with hyperscalers while tailoring designs to regional codes gain clear advantage.

EU Cyber Resilience Act Mandating Class II Secure-by-Design Hardware

The EU Cyber Resilience Act pulls physical security into a broader compliance regime that demands software bills of material, continuous patching, and secure update pipelines for any device connected to a network.[2]European Commission, “EU Energy Efficiency Directive – Data Center KPIs,” ec.europa.eu Class II labeling covers cameras, readers, and controllers, shifting procurement preferences toward vendors with long-term firmware support and in-house cryptography labs. German and Dutch operators are early adopters, synchronizing CRA audits with energy-efficiency reporting to streamline documentation cycles. Established manufacturers such as Honeywell integrate verifiable cryptographic chips across access-control boards to shorten validation. Smaller integrators without lifecycle engineering capacity face higher certification overhead, accelerating vendor consolidation. The act’s emphasis on “security by design” is also pushing demand for converged dashboards that evidence compliance in real time, an emerging differentiator as customers embed regulatory KPIs in service-level agreements.

AI-Enabled VSaaS Adoption for 24/7 Remote Guarding

Labor shortages and wage inflation have propelled a shift toward AI Video Surveillance-as-a-Service, especially in the United Kingdom and Nordic markets where guard staffing costs exceed EUR 35 per hour. Cloud-native analytics now filter false alarms, execute breadcrumb searches, and issue automated playbooks when policy thresholds trip. Securitas Technology’s 2025 Technology Outlook flagged AI video analytics and cloud connectivity as priority investment areas for European data-center operators.[3]Securitas Technology, “2025 Technology Outlook,” securitastechnology.com Operators gain centralized oversight of dispersed edge cabinets while containing power draw and rack footprint. The subscription model translates capital expenditure into opex, aligning with hyperscaler preferences for variable cost structures. For smaller colos, platform pricing levels the playing field by delivering enterprise-grade analytics without onsite data scientists.

Shift to Zero-Trust Physical-Logical Convergence Architectures

Attackers increasingly exploit weak links between physical assets and IT systems, prompting operators to converge both domains under zero-trust principles. Continuous verification now covers who a user is, where the user is located, and what the user is attempting to access. Johnson Controls links retina scanners to its C-CURE logical framework, blocking a network login if the user’s last door entry is outside the authentication geofence. GDPR and the Digital Operational Resilience Act reinforce this discipline by holding operators accountable for any breach that starts with badge cloning or tailgating. Hyperscalers extend the concept to micro-segments within the data hall, authorizing technicians only at racks relevant to a work order and only for the duration of that order. Over time, this paradigm is expected to replace traditional “harden the perimeter” thinking, embedding context-aware checks at every doorway, port, and API.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Persistent ROI concerns on retro-fits for legacy sites | -2.4% | UK, Germany, France | Short term (≤ 2 years) |

| Supply-chain delays for hardened chips and camera modules | -1.8% | EU-wide, heavier on Tier III–IV builds | Medium term (2-4 years) |

| Compliance burden from GDPR/CRA documentation | -1.2% | All member states | Short term (≤ 2 years) |

| Skilled-labour shortage for multi-vendor integration | -1.1% | Nordics and Germany | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Persistent ROI Concerns on Retro-fits for Legacy Sites

Legacy halls across mature hubs still rely on mid-2000s CCTV and PIN pads that fall short of current threat profiles. Upgrading to biometric trip-bars, encrypted readers, and AI analytics can consume more than 30% of original build cost once downtime and re-cabling are included. Colocation operators with narrow profit margins hesitate to pass retrofit charges to tenants locked into fixed-price contracts. Payback periods lengthen further when equipment life cycles shrink under fast CRA revision schedules. As a workaround, many adopt managed security contracts that spread upgrades across operating budgets while offloading technology obsolescence risk onto service providers. The model favours scale players who negotiate bulk hardware buys and redeploy inventory across multiple campuses, leaving smaller independents exposed to stranded asset risk.

Supply-Chain Delays for Hardened Chips and Camera Modules

Lead times for FIPS-compliant processors and industrial-temperature camera boards have stretched from 12 weeks to beyond 24 weeks since late 2024. Operators respond by over-ordering, yet tying up inventory raises working-capital needs and increases unsold spares when designs iterate. Larger vendors cushion the impact through multisourcing and buffer stocks, whereas mid-tier integrators often cede delivery milestones to rivals with deeper supplier contracts. Extended timelines disrupt coordinated go-live plans, forcing phased handovers that elevate installation costs and complicate compliance testing. The squeeze is loosening gradually as new European fab capacity comes online, but a full return to 2019 lead-time norms is unlikely before 2027.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Component: Services Accelerate Amid Integration Complexity

Services are gaining momentum within the Europe data center physical security market. Although solutions held 65.85% revenue in 2025, the services sub-market is expanding at 16.44% CAGR through 2031 as multivendor integration, CRA audits, and zero-trust adoption exceed in-house skill sets. Consulting engagements often open with threat-and-gap assessments that map physical layouts to regulatory clauses, then progress into turnkey projects combining AI cameras, hardened edge switches, and identity-governance software. Operators channel follow-on budgets toward managed-service contracts that guarantee 24/7 compliance monitoring and firmware patching. These agreements eliminate capital peaks, curb staffing shortages, and deliver predictable cost visibility, reinforcing a long-term shift from asset ownership to service consumption.

Second-generation service bundles now include environmental sensors, predictive-maintenance analytics, and energy-usage dashboards, enabling clients to satisfy simultaneous efficiency and security mandates. Johnson Controls noted high single-digit growth in EMEA fire and security service revenues for FY25, attributing the rise to data-center outsourcing deals where SLA penalties tie directly to uptime and audit scores johnsoncontrols.com. As AI workloads intensify heat loads, operators also require continuous calibration of thermal cameras, leak detectors, and particulate sensors to pre-empt incidents that could trigger both safety and regulatory liabilities.

By Data-Center Tier: Tier IV Drives Premium Security Investments

Tier III sites remain the backbone of the Europe data center physical security market, claiming 58.35% revenue in 2025. These facilities apply multi-layered defences that balance resiliency and cost, such as dual-factor lobby controls, mantraps, and zoned surveillance analytics. However, hyperscalers favour Tier IV builds for mission-critical AI clusters, pushing this segment toward a 17.08% CAGR. The Europe data center physical security market size for Tier IV deployments is forecast to expand as redundant power, diverse fibre paths, and biometric rack-level locks become mandatory specifications.

BSO’s DataOne campus illustrates premium demand: its 400 MW design integrates iris-match vestibules, machine-learning perimeter radars, and autonomous patrol units that reduce guard headcount while compressing response times. Capital tolerance at Tier IV sites allows early adoption of quantum-safe encryption chips in access controllers, piloting technologies that later migrate to lower tiers when costs fall.

By Data-Center Type: Hyperscalers Reshape Security Requirements

Colocation operators held 48.45% of 2025 revenues, reflecting enterprises’ reliance on shared facilities that provide baseline compliance under cost-effective tenancy models. Hyperscalers, though, present the sharpest growth at 16.12% CAGR as they race to provision AI training clusters across Europe. Each megawatt under hyperscale control packs higher compute density, raising stakes for any physical intrusion. Google’s layered “defence-in-depth” design specifies ballistic-rated walls, multi-modal biometrics, and dedicated incident-response teams with overlapping jurisdictions, setting benchmarks that ripple throughout the supply chain. The Europe data center physical security market size attached to hyperscale campuses is projected to exceed USD 0.58 billion by 2031, emphasising solutions that integrate physical telemetry with SIEM dashboards.

Edge facilities add another dimension. Compact shelters adjacent to 5G towers now host micro-data-centres that support low-latency services. These unmanned boxes require ruggedised locks, vibration sensors, and cloud-managed cameras delivered as turnkey kits. Service providers that master rapid deployment templates for hundreds of edge nodes unlock new annuity streams, strengthening long-term revenue diversity within the Europe data center physical security industry.

Geography Analysis

Western Europe retains the highest installed base, yet growth dynamics vary. The United Kingdom continues to attract international finance clients that demand layered security aligned to Financial Conduct Authority directives, driving sizeable renewal cycles for access hardware, intrusion analytics, and hardened enclosures. Germany’s industrial clusters favour on-premises AI workloads that require strict segregation between customer zones, prompting widespread adoption of air-gap monitoring and geo-fencing tags. France benefits from government incentives designed to match London and Frankfurt in colocation scale, unlocking brownfield conversions that embed modern biometric corridors within legacy warehouses.

The Netherlands and Ireland carry strategic weight by virtue of submarine cable landings that shorten latency to North America. Their respective energy policies rely on wind and hydro assets that power data centers at scale, encouraging the use of low-energy camera models and PoE-driven badge readers within the Europe data center physical security market. Nordic nations combine year-round free cooling with green-power grids, positioning campuses like EcoDataCenter’s Överby estate to pioneer high-resolution thermal tracking powered entirely by renewables. Southern Europe is catching up quickly; Spain alone is on a sixfold capacity trajectory to 2026, creating a greenfield zone where operators can embed zero-trust architectures without the constraints of retrofit economics.

Regulatory diversity shapes procurement choices. While the CRA sets a common baseline, member states impose local nuances around video retention, biometric consent, and overtime rules for guards. Vendors that maintain multilingual compliance templates, country-specific data-sovereignty hosting, and localised field-service fleets are best placed to gain share. Against this mosaic, the Europe data center physical security market continually rewards suppliers that pivot fast between regional tender specifications, yet underpin all projects with consistent platform codebases that streamline lifecycle support.

Mordor Intelligence evaluates the global data center physical security market across all key regional markets, including South America, Middle East, and Asia, with deeper country-level insights covering Belgium, Austria, Italy, Norway, Poland, and Denmark.

Competitive Landscape

Competition blends scale, integration breadth, and regulatory expertise. Honeywell’s USD 4.95 billion acquisition of LenelS2 and on-premises brands expanded its access-control footprint to more than 20 million installed readers worldwide. ASSA ABLOY followed a similar trajectory, absorbing 3millID and Third Millennium Systems to unite credential management with advanced biometrics. Johnson Controls leverages its C-CURE software suite plus alliances with Evolv and Everbridge to deliver active-shooter detection and mass-notification overlays that resonate with hyperscale risk-models. Schneider Electric bundles power, cooling, and security into integrated reference designs that allow operators to monitor environmental and threat telemetry from a single pane of glass, a persuasive proposition in energy-constrained hubs.

Barriers to entry rise as the CRA increases documentation demands that favour incumbents with dedicated compliance teams. Smaller integrators survive by specialising in edge deployments or in retrofit advisory that separates design from capital expense. Managed-service models also reshape rivalry: cloud-native platforms handle updates, certificate rotations, and event correlation for hundreds of sites, effectively embedding vendors within client operations for multi-year horizons. Over time, differentiation hinges less on discrete devices and more on the ability to orchestrate converged incident response across nested physical and digital domains within the Europe data center physical security market.

Technological leapfrogging remains brisk. AI analytics lower false-positive rates to below 0.5% in well-tuned models, while quantum-safe readers enter pilot phase to future-proof credential exchanges. Robotics start-ups trial autonomous patrol units that integrate LiDAR, thermal imaging, and badge-verification kiosks, reducing routine guard sweeps. Companies with R&D pipelines tied to hyperscaler roadmaps gain faster feedback loops, enabling them to harden products ahead of mainstream adoption. Despite these forces, end-user preference for multi-vendor sourcing ensures no single supplier dominates, sustaining a moderately fragmented environment.

Europe Data Center Physical Security Industry Leaders

Johnson Controls International plc

Honeywell International Inc.

Bosch Sicherheitssysteme GmbH

Axis Communications AB

Schneider Electric SE

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2025: Vantage Data Centers raised EUR 720 million via Europe’s first data-center asset-backed securitisation, refinancing four German sites and signalling investor appetite for digital infrastructure.

- June 2025: AWS launched its European Sovereign Cloud subsidiary to address jurisdictional control, influencing procurement of region-locked physical security systems

- June 2025: Brookfield disclosed a USD 10 billion plan for a Swedish AI campus, underlining Nordic appeal for green power and resilient physical security.

- May 2025: BSO commenced phase one of the 400 MW DataOne project in France with ISO-certified, carrier-neutral infrastructure and hardened perimeter controls

Europe Data Center Physical Security Market Report Scope

The data center physical security market refers to the industry focused on providing products and services to safeguard the physical infrastructure and assets of data centers. This includes measures to protect data centers from unauthorized access to premises, hardware theft, vandalism, sabotage, terrorist acts, and other physical threats. The key components of data center physical security include video surveillance and monitoring, access control systems, physical barriers, biometric authentication, and environmental controls designed to ensure the safety and integrity of the data center environment.

The European data center physical security market is segmented by solution type (video surveillance and access control solutions), service type (consulting services and professional services), end user (IT and telecommunication, BFSI, government, healthcare, and other end users), and country. The market sizes and forecasts are provided in terms of value (USD) for all the above segments.

| By Solution Type | Video Surveillance |

| Access Control | |

| Perimeter Security (Mantraps, Fences, Bollards) | |

| Intrusion Detection and Monitoring | |

| Environmental and Fire Safety Systems | |

| By Service Type | Consulting |

| Integration and Deployment | |

| Maintenance and Managed Services |

| Tier I and II |

| Tier III |

| Tier IV |

| Hyperscaler/Cloud Service Providers |

| Colocation Providers |

| Enterprise and Edge Data Center |

| United Kingdom |

| Germany |

| France |

| Netherlands |

| Ireland |

| Spain |

| Italy |

| Sweden |

| Norway |

| Denmark |

| Poland |

| Austria |

| Belgium |

| Switzerland |

| By Component | By Solution Type | Video Surveillance |

| Access Control | ||

| Perimeter Security (Mantraps, Fences, Bollards) | ||

| Intrusion Detection and Monitoring | ||

| Environmental and Fire Safety Systems | ||

| By Service Type | Consulting | |

| Integration and Deployment | ||

| Maintenance and Managed Services | ||

| By Data-center Tier | Tier I and II | |

| Tier III | ||

| Tier IV | ||

| By Data Center Type | Hyperscaler/Cloud Service Providers | |

| Colocation Providers | ||

| Enterprise and Edge Data Center | ||

| By Country | United Kingdom | |

| Germany | ||

| France | ||

| Netherlands | ||

| Ireland | ||

| Spain | ||

| Italy | ||

| Sweden | ||

| Norway | ||

| Denmark | ||

| Poland | ||

| Austria | ||

| Belgium | ||

| Switzerland | ||

Key Questions Answered in the Report

What is the current value of the Europe data center physical security market?

The market stands at USD 0.80 billion in 2026 and is forecast to reach USD 1.44 billion by 2031.

Which segment is growing fastest within the market?

Tier IV facilities are expanding at 17.08% CAGR owing to hyperscale demand for maximum uptime.

Why is Ireland’s market growth outpacing other countries?

Ireland offers transatlantic connectivity, supportive tax policy, and heavy hyperscaler investment, driving a 14.12% CAGR through 2031.

How does the EU Cyber Resilience Act affect procurement?

The act mandates secure-by-design hardware and continuous patch management, favouring vendors with compliance engineering capacity.

Are services replacing hardware purchases?

Yes. Managed and integration services are growing at 16.44% CAGR as operators outsource skill-intensive tasks like multi-vendor orchestration and CRA audit readiness.

What drives adoption of AI-enabled surveillance?

Labour shortages and the need for proactive threat detection are pushing operators toward Video Surveillance-as-a-Service models that deliver analytics and remote monitoring at scale.

Page last updated on: