Composable Infrastructure Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 9.89 Billion |

| Market Size (2031) | USD 21.87 Billion |

| Growth Rate (2026 - 2031) | 17.21% CAGR |

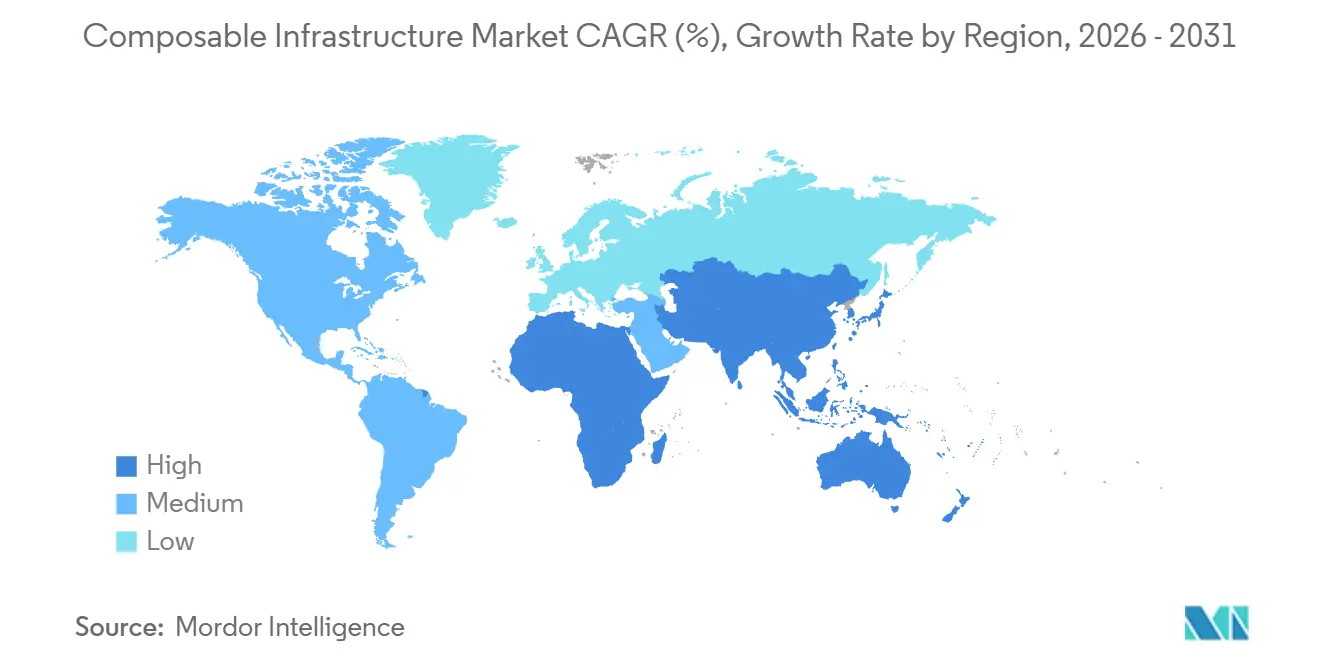

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

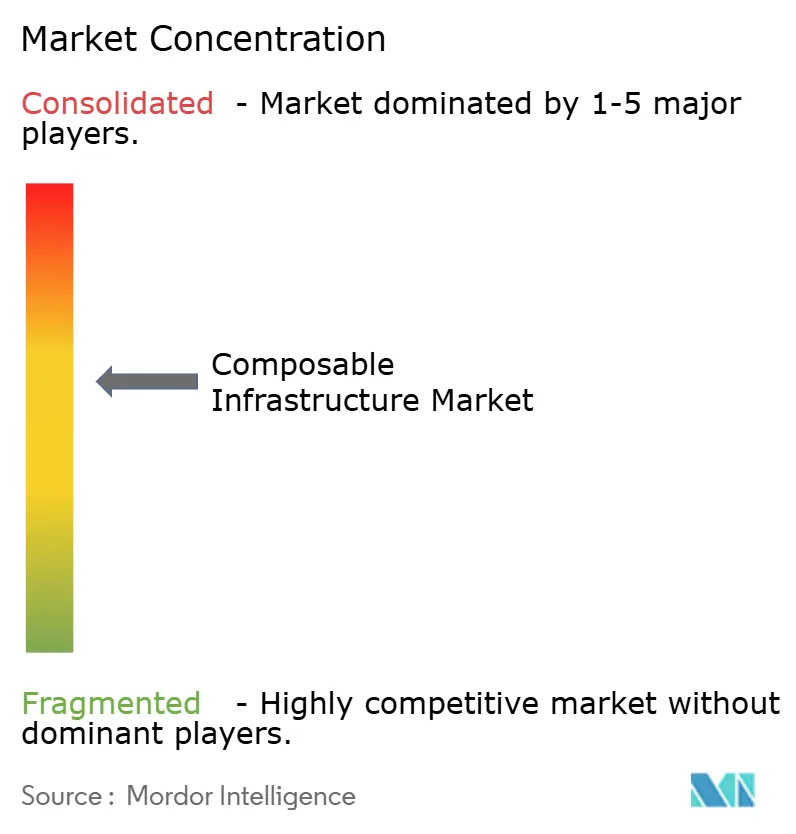

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Composable Infrastructure Market Analysis by Mordor Intelligence

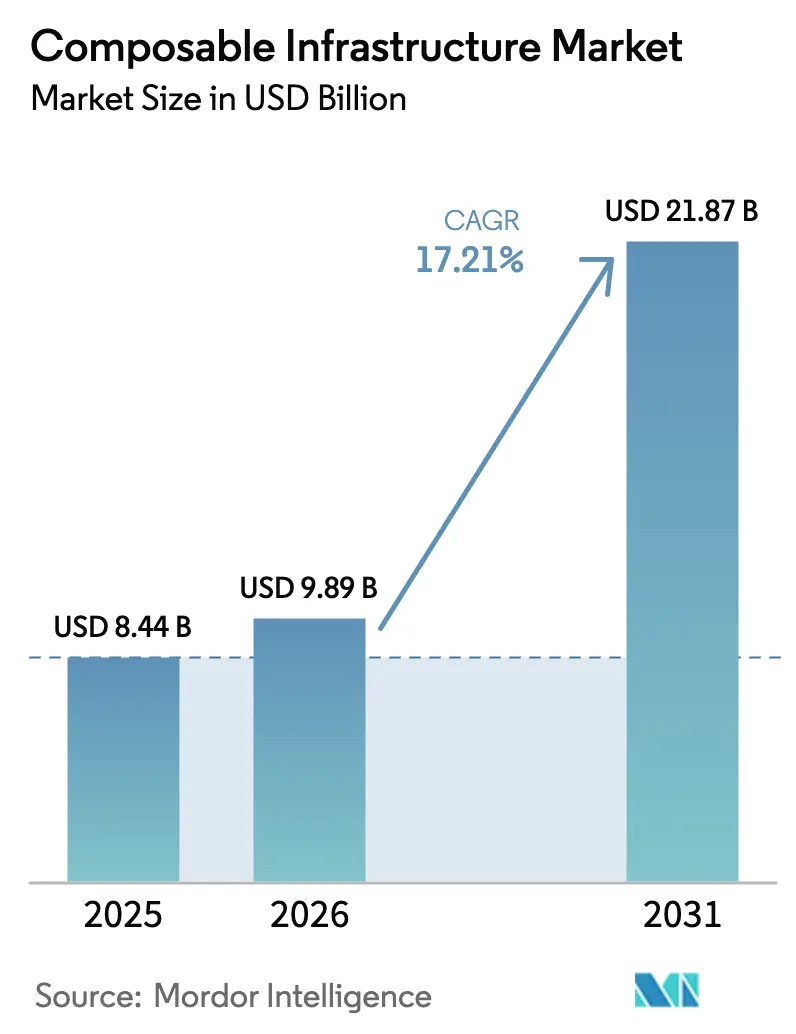

The composable infrastructure market size reached USD 9.89 billion in 2026 and is projected to climb to USD 21.87 billion by 2031, expanding at a 17.21% CAGR over the period, as enterprises pivot from monolithic data-center stacks toward software-defined resource pools that can be allocated on demand. Workload diversification, sovereign-cloud mandates, and the surge in generative-AI training are the dominant tailwinds. Leading hyperscalers now embed Compute Express Link (CXL) enabled memory fabrics into public-cloud instances, while on-premises deployments remain critical for industries bound by data-residency or low-latency needs. Hardware continues to account for most spending, but orchestration software is accelerating as fabric intelligence migrates into code, lowering integration barriers for heterogeneous servers. Start-ups specializing in PCIe Gen5 and CXL switch fabrics intensify competitive dynamics by shortening lead times for GPU and memory pooling at rack scale. Supply-chain disruptions for advanced switching ASICs and the operational effort required to retrofit legacy virtual-machine estates temper the overall growth trajectory, yet heavy investment from financial services, telecom, and healthcare offsets these headwinds.

Key Report Takeaways

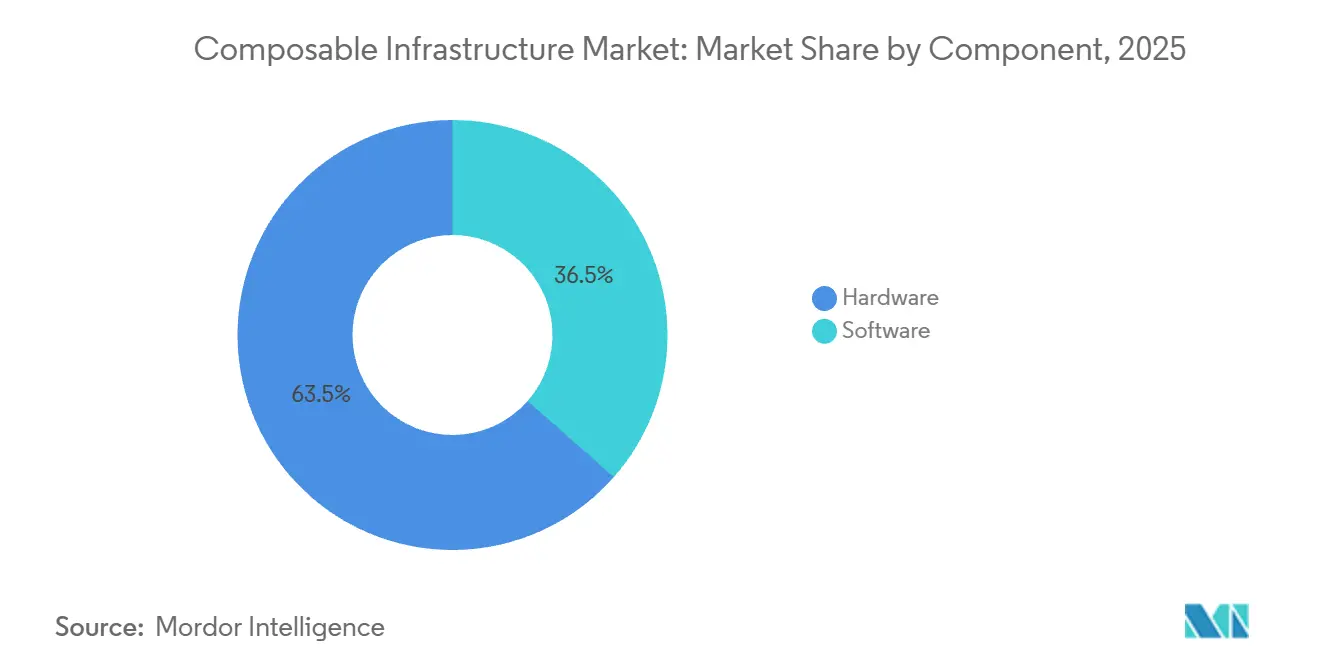

- By component, hardware held 63.51% of 2025 revenue, whereas software is forecast to expand at a 19.87% CAGR through 2031.

- By deployment model, on-premises commanded 71.63% of 2025 revenue, while cloud-based offerings post the fastest growth at a 19.97% CAGR.

- By organization size, large enterprises captured 68.74% of 2025 revenue, whereas small and medium enterprises are advancing at a 20.19% CAGR.

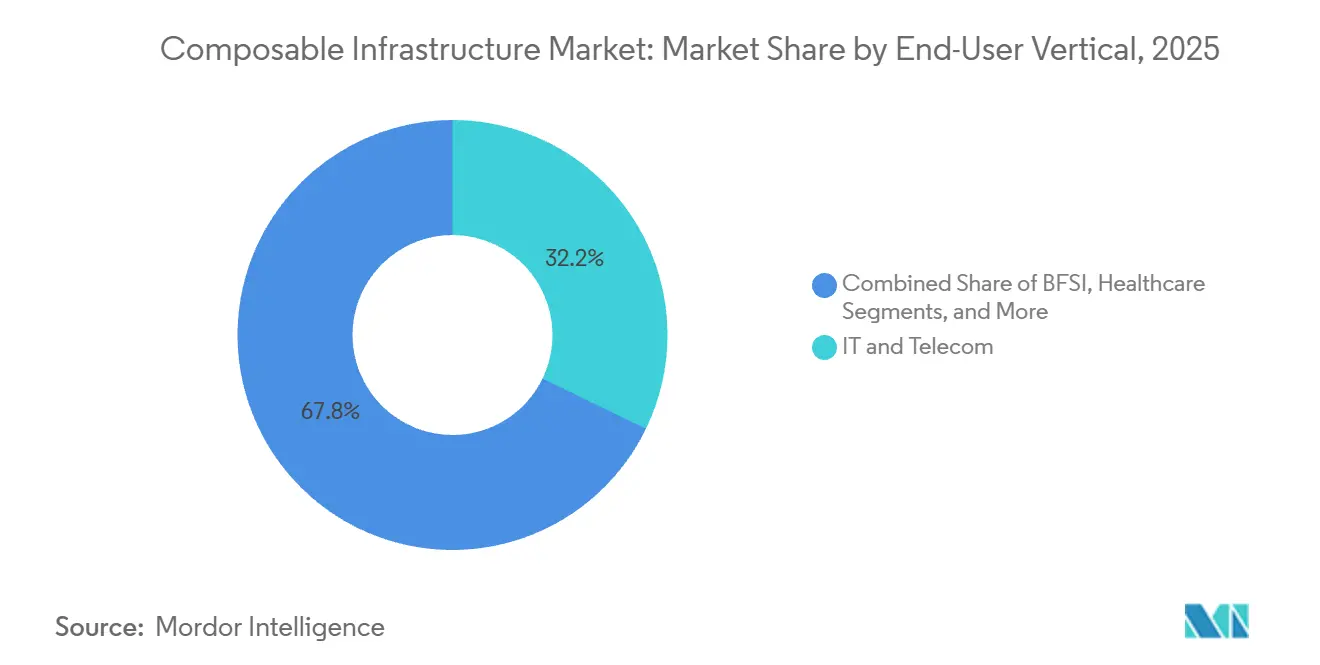

- By end-user vertical, IT and telecom led with 32.18% revenue share in 2025; healthcare records the highest projected CAGR at 18.14% to 2031.

- By application, AI and ML and HPC workloads accounted for 46.92% of 2025 revenue and are growing at an 18.19% CAGR.

- By geography, North America dominated with 38.54% share in 2025; Asia Pacific is the fastest-growing region at 18.96% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Composable Infrastructure Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| AI and ML GPU-Pooling Demand | +4.2% | Global, with concentration in North America and APAC | Medium term (2-4 years) |

| Cloud-Native and Micro-services Scalability Needs | +3.1% | Global, led by North America and Europe | Short term (≤2 years) |

| Data-Center Consolidation and CapEx Optimisation | +2.8% | North America, Europe, APAC core | Medium term (2-4 years) |

| Edge-Computing Deployment Acceleration | +2.5% | APAC, North America, Middle East | Long term (≥4 years) |

| CXL-Enabled Memory Composability | +2.3% | North America, Europe, APAC early adopters | Long term (≥4 years) |

| Sovereign-Cloud Compliance Boosting On-Prem Builds | +2.2% | Europe, APAC, Middle East | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

AI And ML GPU-Pooling Demand

Generative-AI training saturates GPU clusters for hours, then idles them for longer spells, leaving 40-60% of accelerator capacity unused in fixed servers. Composable infrastructure decouples GPUs from hosts through PCIe Gen5 or CXL fabrics that sustain sub-500-nanosecond latency. Nvidia’s DGX SuperPOD already pools up to 32 nodes, allowing a single H100 GPU to serve inference micro-services while joining a distributed training job in parallel. Liqid customers report 85% GPU utilization after reallocating accelerators every four hours, versus 45% in static racks. Financial-services firms benefit when fraud-detection models burst to 16 GPUs for milliseconds, then relinquish resources to other jobs. ISO/IEC 23009 interoperability guidance nudges vendors toward open APIs, further mitigating lock-in risk.[1]ISO, “ISO/IEC 23009 Interoperability Standard,” iso.org

Cloud-Native And Micro-Services Scalability Needs

Kubernetes clusters trigger erratic compute, memory, and NVMe demand that traditional appliances over-provision. Composable infrastructure satisfies pod scheduling spikes by attaching extra CPUs, DRAM, or storage from a pooled fabric in seconds via Container Storage Interface hooks. Red Hat OpenShift 4.15 introduced native composable storage back-ends in 2025, eliminating static drive binding. Cisco Intersight automates fabric provisioning when VMware Tanzu or Amazon EKS launches additional pods, cutting time-to-provision from hours to seconds. Financial-trading desks cite 60% tail-latency reductions relative to hyperconverged appliances, and CNCF security best practices favor hardware isolation baked into modern composable switch ASICs.

Data-Center Consolidation And CapEx Optimization

Enterprises transitioning from regionally dispersed server farms to high-density composable clusters shrink floor space and energy budgets. Fortune 500 adopters report 40% physical footprint reductions once storage and GPU expansion chassis move to shared pools. Consumption-based pricing by HPE GreenLake and Dell APEX turns what was capital expense into pay-per-use operating expense, a major lure for CFOs. Regulatory focus on energy efficiency, exemplified by the United States Department of Energy’s latest data-center guidelines, adds momentum to consolidation strategies.

CXL-Enabled Memory Composability

Compute Express Link revision 3.1 introduced multi-level switching so as many as 4,096 devices share a single memory namespace. Samsung and SK Hynix shipped 512 GB CXL 2.0 modules in 2024 and demoed 1 TB prototypes in 2025. SAP HANA users now tap an 8 TB pool rather than dedicating DRAM per node, avoiding costly over-provisioning. HPE’s Cray EX integrates CXL switches to expose remote memory with under 200-nanosecond latency, achieving 400 GB per-second bandwidth per node. JEDEC DDR5-CXL interoperability governance aids multi-vendor deployments.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Legacy Integration Complexity | -2.1% | Global, acute in North America and Europe | Short term (≤2 years) |

| High Up-Front CapEx and Vendor Lock-In | -1.8% | Global, particularly SMEs in APAC and South America | Medium term (2-4 years) |

| PCIe Gen5 Switch Supply-Chain Bottlenecks | -1.5% | Global, most severe in North America and Europe | Short term (≤2 years) |

| Limited Persistent-Memory Orchestration Skills | -1.3% | Global, with skills gaps in emerging markets | Long term (≥4 years) |

| Source: Mordor Intelligence | |||

Legacy Integration Complexity

Organizations entrenched in VMware vSphere, Microsoft Hyper-V, or OpenStack environments face six-to-twelve-month retrofits when fabric managers must translate hypervisor calls into PCIe or CXL operations. vSphere 8.0 U2 added experimental CXL pooling yet remains uncertified for production. European survey data show 62% of firms flag legacy compatibility as the chief barrier to adoption. Regression testing for mission-critical workloads can devour 40% of project budgets, delaying payback periods. ISO 20000 prompts vendors to publish reference blueprints, but these often trail rapid ASIC road maps.

PCIe Gen5 Switch Supply-Chain Bottlenecks

Lead times for Broadcom and Marvell Gen5 switch ASICs exceed nine months as 5-nanometer fab capacity favors AI accelerators and phone chipsets. Crehan Research logged a 47% year-over-year jump in Gen5 Ethernet switch shipments in 2025, yet backlogs hit record highs. Vendors now ration scarce ASICs to top-revenue accounts, postponing mid-market deals by up to six months. Microchip retimer shortages force shorter cable runs, curbing rack-scale composability. New fab lines are not expected to reach volume until late 2026, leaving growth somewhat constrained.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Component: Software Orchestration Gains As Fabric Intelligence Deepens

Hardware contributed 63.51% of 2025 revenue, anchored by PCIe and CXL switch fabrics, disaggregated compute sleds, and NVMe-over-Fabrics arrays. Within the composable infrastructure market size for components, Hewlett Packard Enterprise and Dell Technologies claimed the lion’s share through pre-integrated racks that embed fabric managers. Orchestration software, though smaller, is racing ahead at a 19.87% CAGR as enterprises standardize on REST-based APIs to build automated workflows.

Liqid Command Center and GigaIO FabreX allow administrators to drag-and-drop GPUs, NVMe drives, and DRAM into logical servers, provisioning the builds through Kubernetes or VMware pipelines. Nutanix AHV 6.7 natively exposes composable storage, letting Kubernetes persistent volumes carve capacity from shared NVMe pools. Cisco Intersight, Lenovo XClarity, and IBM Cloud Pak unify telemetry across hybrid pools, and TidalScale pools multiple x86 nodes into a single logical system with terabytes of memory. Heightened ISO 27001 scrutiny accelerates this shift because software layers now embed role-based access and audit logs.

By Deployment Model: Cloud Composability Accelerates As Hyperscalers Embed CXL

On-premises builds commanded 71.63% of 2025 revenue, a reflection of data-sovereignty imperatives and the latency intolerance of high-frequency trading or defense workloads. This portion of the composable infrastructure market share remains solid among banks and governments seeking physical control over hardware.

Cloud-based composability is, however, the fastest-growing track at 19.97% CAGR. Microsoft Azure previewed composable VMs with up to 8 TB of CXL-shared memory per instance, while AWS EC2 P5 allows dynamic H100 GPU attachment by the minute. Google Cloud A3 Mega adds hot-resize NVMe volumes for genomics researchers. Hybrid consumption models such as HPE GreenLake and Dell APEX blur CapEx and OpEx distinctions, letting enterprises burst to cloud pools during spikes and shrink on-prem uses off-peak.

By Organization Size: SMEs Embrace Consumption Models To Sidestep CapEx

Large enterprises generated 68.74% of 2025 revenue, financing rack-scale fabrics that feed AI training clusters and massive simulations. Automotive OEMs use shared pools to run CFD workloads needing 2 TB of memory a job, flexing resources without idle hardware.

Small and medium enterprises form the fastest-expanding cohort at 20.19% CAGR. Lenovo TruScale and Dell APEX Flex on Demand convert infrastructure into monthly bills pegged to measured consumption, avoiding million-dollar outlays. Mid-market SaaS providers now isolate tenant workloads at the fabric layer, mitigating noisy-neighbor risks. Integration remains challenging for SMEs lacking in-house modernization talent, and proprietary control planes still raise vendor-lock-in concerns.

By End-User Vertical: Healthcare Imaging Drives Storage Composability

IT and telecom dominated 2025 with 32.18% revenue as service providers ran 5G cores, edge nodes, and vRAN workloads on dynamically rebalanced pools. Telcos like Verizon consolidate regional data centers, trimming site counts by 40% without sacrificing latency.[2]Cisco, “Intersight Cloud Operations,” cisco.com

Healthcare climbs at an 18.14% CAGR thanks to radiology departments moving petabyte-scale Picture Archiving and Communication Systems into composable NVMe arrays. Dell APEX for Healthcare supplies AI-assisted image analysis while two-second retrieval SLAs persist. BFSI firms deploy GPU pools for millisecond fraud screening, and industrial manufacturers run predictive-maintenance models at the edge. Government deployments gain momentum through sovereign-cloud programs that specify composable architectures for classified workloads.

By Application And Workload: AI Training Clusters Dominate Resource Pools

AI, ML, and HPC workloads captured 46.92% of 2025 revenue and are expanding at an 18.19% CAGR, underpinning the composable infrastructure market for workloads through 2031. Nvidia DGX SuperPOD pools accelerators across 32 nodes, splitting a single H100 between concurrent inference and training.

Research labs such as Lawrence Livermore dynamically allocate 16,384 CPU cores and 512 TB of memory from shared pools to run climate models. GitLab CI/CD pipelines running on composable nodes slash build times 70%, and SAP HANA users cut total cost of ownership by 50% when drawing memory from CXL pools at night. VDI and cloud gaming leverage burst GPU allocation, with Nvidia GeForce NOW curbing idle GPU capacity by 60% compared to static racks.

Geography Analysis

North America generated 38.54% of 2025 revenue, propelled by hyperscaler adoption and Fortune 500 data-center consolidation. United States banking giants trimmed physical footprints 40% after moving to pooled resources, and Canada’s Shared Services tender mandates that sovereign workloads run on HPE GreenLake composable services. Mexico’s carriers pool compute for 5G vRAN, while National Institute of Standards and Technology guidelines push federal agencies toward hardware-isolated composable nodes to counter supply-chain risks.

Asia Pacific is the fastest-growing region at 18.96% CAGR. India’s 2025 data-sovereignty rules push ministries toward domestic providers such as Yotta Infrastructure, and China’s USD 12 billion subsidy fosters AI training farms on Inspur and Huawei gear. Japan’s factories pool edge compute for Industry 4.0, South Korea’s SK Telecom invests USD 800 million in CXL memory fabrics for generative-AI, and Singapore’s Digital Realty now offers composable colocation to local cloud-service vendors. Southeast Asia’s service providers, burdened by fluctuating demand, embrace pay-per-use resource pools.

Europe maintains a sizeable slice, anchored by Digital Operational Resilience Act requirements. Germany’s BaFin forces banks to keep transaction data on locally controlled hardware, prompting Deutsche Bank and Commerzbank to roll out Dell and HPE composable racks. The United Kingdom’s National Health Service signs a GBP 150 million (USD 190 million) NetApp contract for electronic health records backed by composable storage. France’s sovereign-cloud project favors domestic hosts like Atos and OVHcloud. Middle Eastern data-center operators equip smart-city rollouts with disaggregated fabrics, and UAE sovereign funds commit USD 5 billion to AI training clusters built on pooled GPUs.[3]UAE Government, "Smart City and AI Initiatives," u.ae South Africa pilots Cisco-based composable platforms for real-time payments, whereas Brazil’s import tariffs slow broader Latin American uptake despite Anatel’s incentive program.

Competitive Landscape

The top five vendors Hewlett Packard Enterprise, Dell Technologies, Cisco Systems, Lenovo Group, and Nutanix controlled about 55% of 2025 revenue, pointing to a moderately concentrated structure. Each leverages entrenched server or hyperconverged install bases to upsell composable extensions, yet faces agile challengers such as Liqid, GigaIO Networks, and One Stop Systems that specialize in PCIe Gen5 and CXL fabrics with shorter release cycles.

Incumbents debate closed versus open stances. HPE’s silicon root of trust and Dell’s PowerEdge kinetic nodes represent proprietary differentiators, whereas others rally behind CXL standards and the Open Compute Project for multivendor rack designs. Edge computing remains under-served, yielding white-space for ruggedized form factors that tolerate industrial temperatures and vibration.

Software differentiation intensifies. Cisco Intersight integrates with Red Hat OpenShift and Amazon EKS to automate GPU and NVMe allocation after container scheduling events. Nvidia Base Command predicts job completion and reallocates accelerators in advance, while AWS Outposts and Microsoft Azure Stack HCI blur cloud and on-prem form factors with pay-as-you-go nodes. With VMware now under Broadcom, deeper integration of composable orchestration into vSphere is expected, although regulatory hurdles slow cross-portfolio harmonization.

Composable Infrastructure Industry Leaders

-

Hewlett Packard Enterprise Co.

-

Dell Technologies Inc.

-

Cisco Systems Inc.

-

Lenovo Group Ltd.

-

NetApp Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- December 2025: Hewlett Packard Enterprise released GreenLake for Composable Cloud, a consumption-based service delivering CXL memory pools and GPU disaggregation on-premises.

- November 2025: Dell Technologies launched the liquid-cooled PowerEdge XE9680L supporting eight Nvidia H200 GPUs with 60-second hot-swap over PCIe Gen5 fabrics.

- October 2025: Cisco Systems rolled out Intersight 2.0, automating composable orchestration across on-prem and public clouds.

- October 2025: SK Telecom committed USD 800 million to deploy CXL-enabled composable nodes for generative-AI clusters.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study defines the composable infrastructure market as revenue from purpose-built chassis, fabric interconnects, pooled accelerator enclosures, and orchestration software that disaggregate compute, storage, memory, and GPU resources inside enterprise or colocation data centers, then recombine them on demand through a fabric manager.

Scope exclusion: Public cloud IaaS, refurbished hardware, OEM support contracts, and generic PCIe switches sold outside resource-pooling projects are not sized.

Segmentation Overview

-

By Component

- Hardware

- Software

-

By Deployment Model

- On-Premises

- Cloud

-

By Organisation Size

- Large Enterprises

- Small and Medium Enterprises (SMEs)

-

By End-User Vertical

- IT and Telecom

- BFSI

- Healthcare

- Industrial Manufacturing

- Government and Public Sector

- Other End-User Verticals

-

By Application / Workload Type

- AI and ML and HPC

- DevOps and CI/CD

- Databases and Analytics

- VDI and Cloud Gaming

- Other Workloads

-

By Geography

-

North America

- United States

- Canada

- Mexico

-

South America

- Brazil

- Argentina

- Rest of South America

-

Europe

- United Kingdom

- Germany

- France

- Italy

- Spain

- Russia

- Rest of Europe

-

Asia Pacific

- China

- India

- Japan

- South Korea

- Australia

- Southeast Asia

- Rest of Asia Pacific

-

Middle East

- United Arab Emirates

- Saudi Arabia

- Turkey

- Rest of Middle East

-

Africa

- South Africa

- Nigeria

- Egypt

- Rest of Africa

-

North America

Detailed Research Methodology and Data Validation

Primary Research

Mordor analysts interviewed data-center architects, fabric-silicon suppliers, and hyperscale procurement heads across North America, Europe, and Asia. Their insight refined penetration ratios, cost-per-rack assumptions, and the likely timing of memory-pooling deployments.

Desk Research

We began by reviewing open datasets such as US International Trade Commission HS-code exports, European Data Centre Association capacity surveys, and OCP Foundation design notes, which anchored hardware volumes and emerging form factors. Company 10-Ks, investor decks, and respected press helped us map average selling prices and launch timelines, while Questel patents, D&B Hoovers, and Dow Jones Factiva let our team cross-check vendor revenues and design cycles.

Next, we tracked CXL Consortium membership growth, rack-level GPU density benchmarks, and edge colocation build-outs to sense regional adoption momentum and to spot early inflection points. The sources named are illustrative; many additional publications informed the desk phase.

Market-Sizing & Forecasting

A top-down reconstruction starts with global x86 server shipments, adjusts for the share shipped as disaggregated chassis, and multiplies by blended ASPs to establish the 2025 baseline. Select bottom-up roll-ups of pooled GPU enclosures and composer licenses cross-check the total. Core levers such as CXL port attach rate, pooled memory sled ASP, installed rack count, and AI workload share feed a multivariate regression that projects results through 2030. Data gaps are bridged through primary feedback before final reconciliation, and we mention that Mordor's dual-lens approach is purposely straightforward for repeat use by clients.

Data Validation & Update Cycle

Outputs pass three-layer peer review, and any anomaly drives a fresh source check. The model refreshes each year with interim updates after major silicon launches or policy shifts, and a senior analyst signs off every release so buyers receive the latest view.

Why Mordor's Composable Infrastructure Market Baseline Commands Trust

Published estimates often diverge because some studies mix public-cloud revenue, apply steep ASP erosion, or treat every new server as composable. Our disciplined scope, yearly refresh, and variable-driven modeling avoid those pitfalls and keep the baseline dependable.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 8.40 B | Mordor Intelligence | |

| USD 13.24 B | Global Consultancy A | Includes cloud services and aggressive price rollback |

| USD 12.98 B | Industry Journal B | Counts all new server shipments as composable |

These contrasts show how our bounded scope and transparent model let decision-makers rely on Mordor Intelligence for a balanced, traceable starting point. Our team will continue to refine inputs as technology, pricing, and adoption patterns evolve.

Key Questions Answered in the Report

What is the projected CAGR for composable infrastructure through 2031?

The composable infrastructure space is expected to expand at 17.21% CAGR between 2026 and 2031.

Which component segment is growing fastest?

Orchestration software is forecast to advance at a 19.87% CAGR as fabric intelligence migrates from hardware into code.

How big is the North American share?

North America captured 38.54% of 2025 revenue, driven by hyperscaler adoption and Fortune 500 data-center consolidation.

Why are SMEs adopting composable platforms?

Consumption models like Lenovo TruScale and Dell APEX convert CapEx into operating expense, lowering entry barriers for SMEs.

What role does CXL play in composable infrastructure?

CXL 3.1 enables multi-level memory switching so thousands of devices share a single namespace with sub-200-nanosecond latency, unlocking elastic DRAM pools for large databases.

Which workload types dominate current deployments?

AI and ML and HPC workloads held 46.92% of 2025 revenue and continue to lead growth with an 18.19% CAGR.

Page last updated on: