Government And Public Sector Cybersecurity Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 84.61 Billion |

| Market Size (2031) | USD 153.36 Billion |

| Growth Rate (2026 - 2031) | 12.63% CAGR |

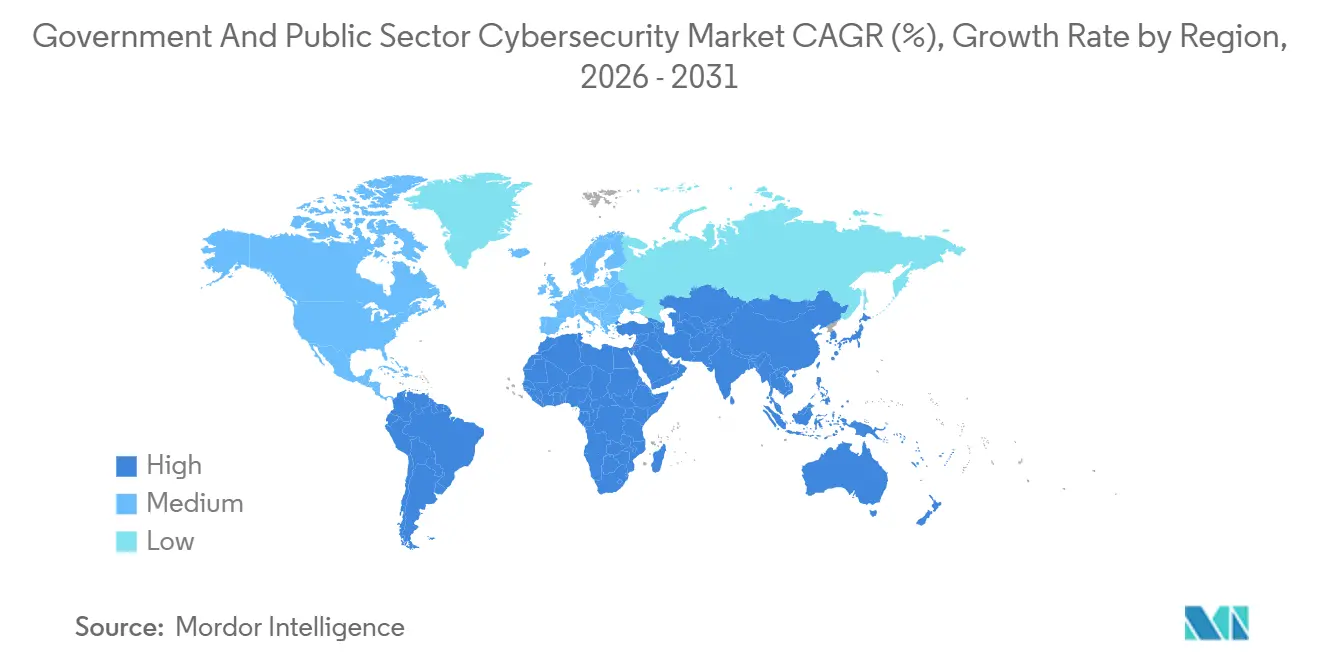

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

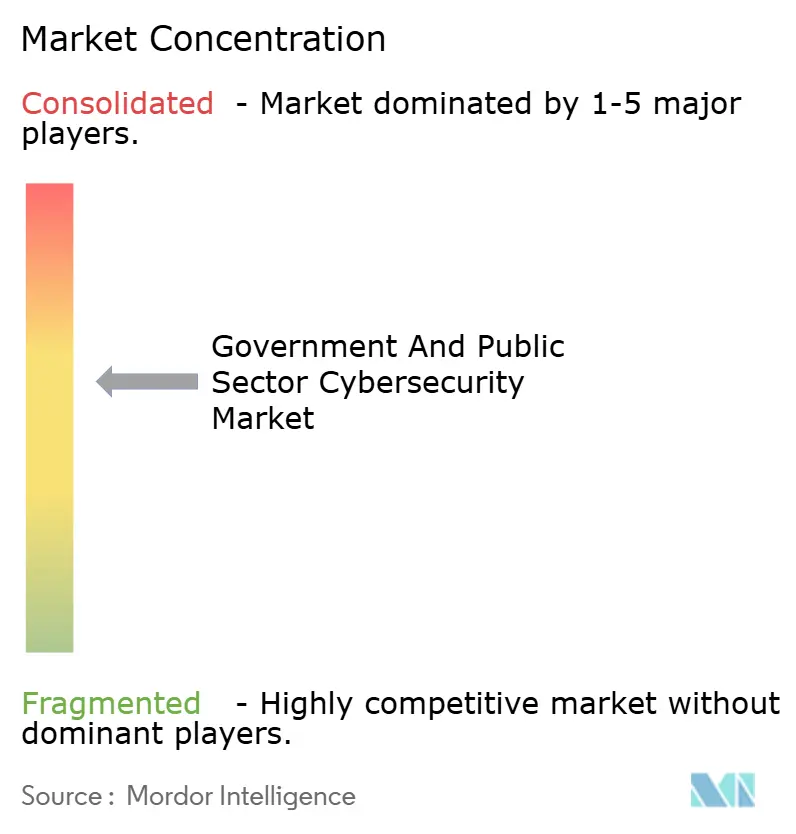

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Government And Public Sector Cybersecurity Market Analysis by Mordor Intelligence

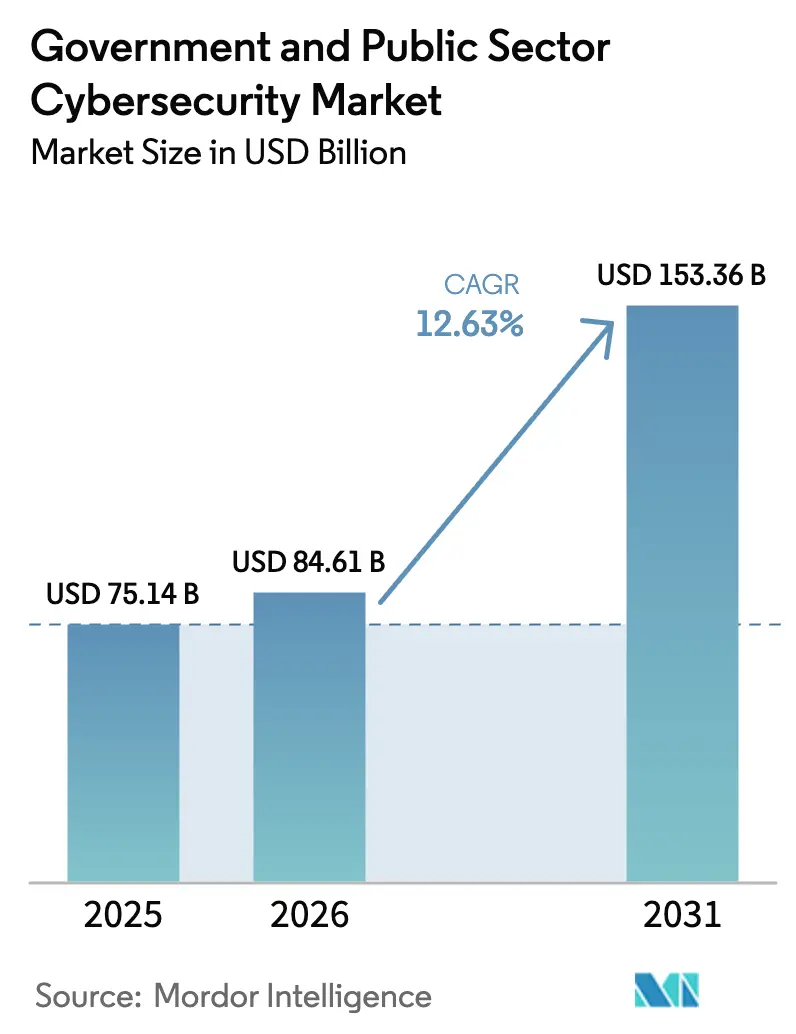

The government and public sector cybersecurity market size is expected to increase from USD 75.14 billion in 2025 to USD 84.61 billion in 2026 and reach USD 153.36 billion by 2031, growing at a CAGR of 12.63% over 2026-2031. Stronger alignment between national defense planning and cyber resilience, rising attack volumes that blur the line between espionage and sabotage, and compliance mandates such as the European Union’s NIS2 Directive are sustaining double-digit expansion. Federal grant programs in the United States and Australia, together with sovereign-cloud requirements in Japan and Germany, are fueling procurement of integrated platforms that consolidate network, cloud, and identity security. At the same time, the chronic shortfall of cleared professionals and the persistence of legacy mainframes are prolonging services engagements, pushing spending toward managed detection, response, and advisory offerings. Vendors that can deliver turnkey, clearance-ready teams are capturing budget realignments once reserved for pure-play software licenses.

Key Report Takeaways

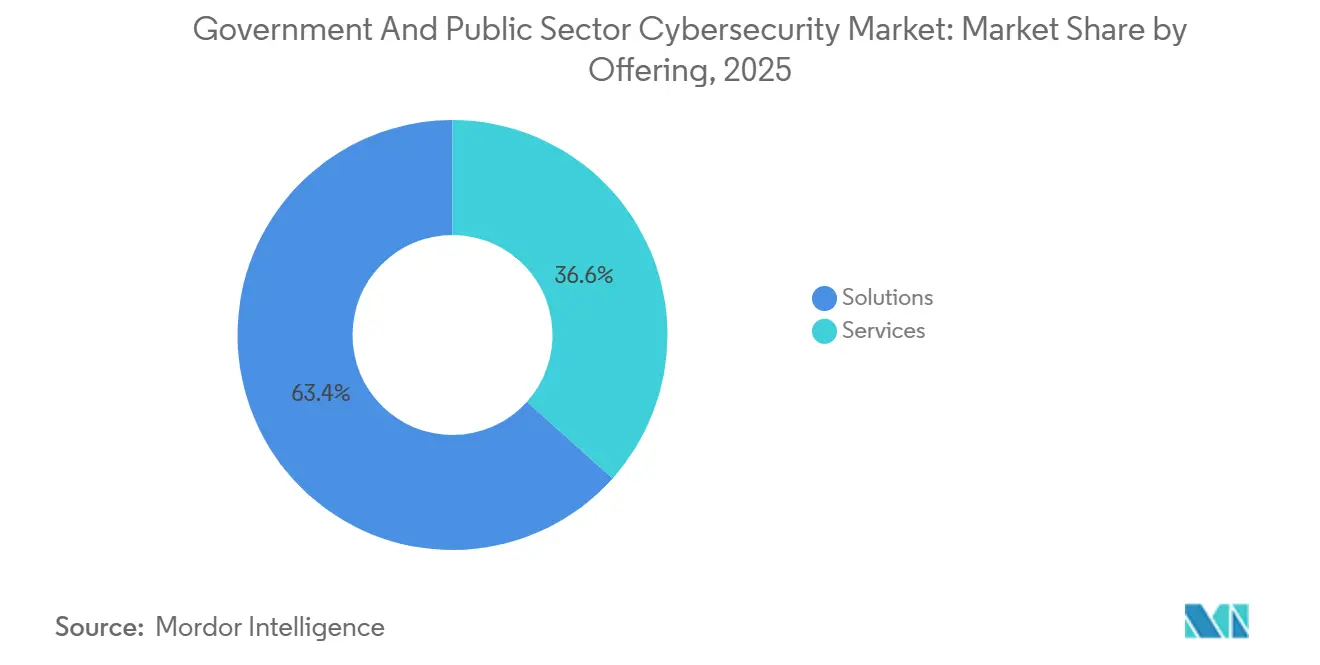

- By offering, solutions led with 63.38% of government and public sector cybersecurity market share in 2025, while services are forecast to expand at a 13.23% CAGR through 2031.

- By deployment mode, on-premises held 58.36% share of the government and public sector cybersecurity market size in 2025, yet cloud deployments are projected to grow at a 13.24% CAGR to 2031.

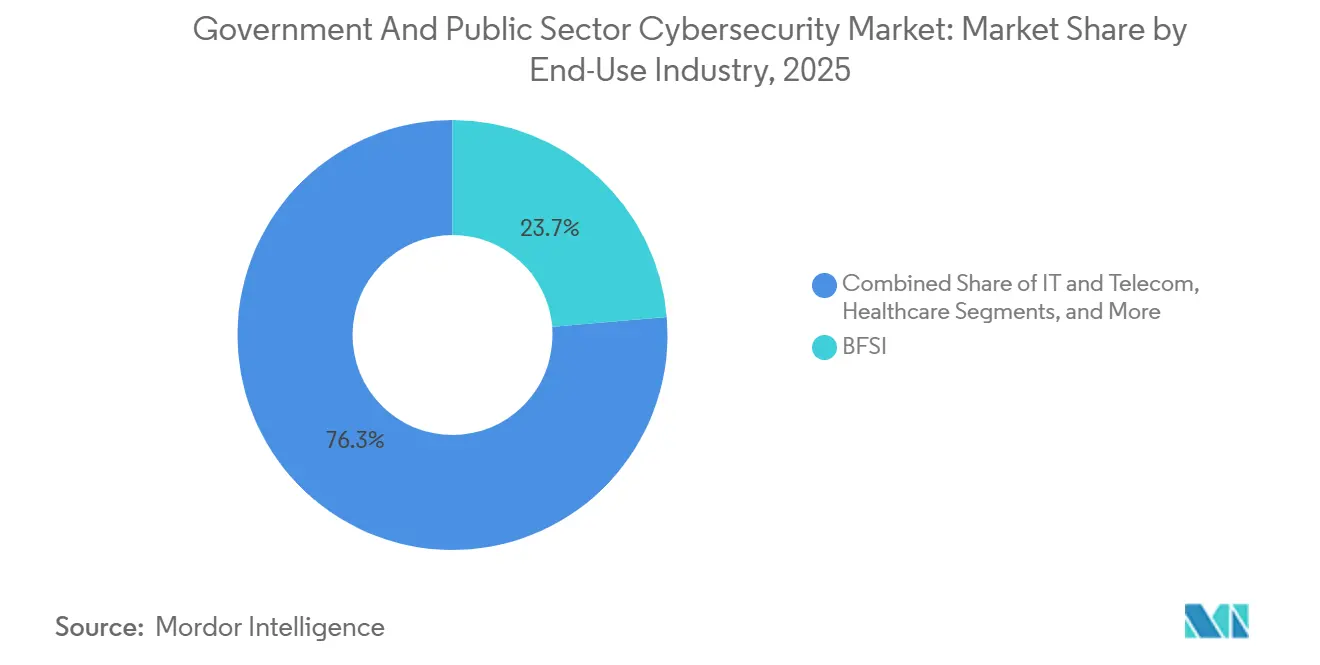

- By end-use industry, banking, financial services, and insurance captured 23.67% spending in 2025, whereas healthcare is advancing at a 14.12% CAGR through 2031.

- By enterprise size, large entities commanded 70.53% of the government and public sector cybersecurity market size in 2025, but small and medium enterprises are growing at a 12.86% CAGR to 2031.

- By geography, North America retained 34.81% share in 2025, and Asia Pacific is the fastest-growing region at a 13.48% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Government And Public Sector Cybersecurity Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Escalation of Nation-State Cyber Threats Targeting Government Infrastructure | +2.8% | Global, with acute intensity in North America, Europe, and Asia Pacific | Short term (≤ 2 years) |

| Proliferation of Zero Trust and Identity-Centric Security Mandates | +2.3% | North America and Europe, expanding to Asia Pacific | Medium term (2-4 years) |

| Surge in Government Cloud Migration and Adoption of Hybrid Environments | +2.1% | Global, led by North America and Europe | Medium term (2-4 years) |

| Introduction of Cybersecurity Performance Goals and Funding Programs | +1.6% | North America, with nascent adoption in Europe and Asia Pacific | Short term (≤ 2 years) |

| Rapid Deployment of AI-Powered Cyber Defense Platforms in Public Sector SOCs | +1.4% | North America and Europe, pilot programs in Asia Pacific | Medium term (2-4 years) |

| Shift Toward Sovereign and Community Clouds to Meet Data Residency Requirements | +1.2% | Asia Pacific, Europe, and Middle East and Africa | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Escalation Of Nation-State Cyber Threats Targeting Government Infrastructure

Advanced persistent threat groups intensified operations during 2025, with 47% of critical-infrastructure intrusions traced to state actors. Incidents such as the Salt Typhoon campaign, which compromised telecommunications across 14 nations, underscore the pivot from espionage toward pre-positioning for disruption. Governments are therefore embedding continuous monitoring and assume-breach principles into procurement, elevating demand for extended detection and response platforms that blend IT, operational technology, and cloud telemetry. Ransomware aimed at municipalities jumped 34% year over year in Europe, reinforcing the urgency of unified security operations even for small public bodies.[1]European Union Agency for Cybersecurity, “Threat Landscape Report 2025,” ENISA.EUROPA.EU

Proliferation Of Zero Trust And Identity-Centric Security Mandates

By mid-2026 every U.S. civilian agency must deploy phishing-resistant multifactor authentication, while the United Kingdom requires central departments to adhere to zero trust blueprints by March 2025. The outcome is a reallocation of budgets from perimeter firewalls to identity governance, privilege controls, and software-defined perimeters. Okta reported a 41% jump in public-sector client additions in fiscal 2025, mirroring a procurement shift that favors vendors with passwordless and policy-driven access capabilities. Legacy mainframes, however, complicate the journey, as 58% of U.S. agencies cite integration roadblocks.

Surge In Government Cloud Migration And Adoption Of Hybrid Environments

FedRAMP lists 312 authorized cloud service offerings as of January 2026, up 17% since 2024, reflecting acceptance that elastic infrastructure can patch and scale faster than traditional data centers.[2]U.S. General Services Administration, “FedRAMP Marketplace,” FEDRAMP.GOVHybrid remains dominant because agencies balance classified, sovereign-cloud, and commercial workloads, creating identity federation and API-gateway challenges. United Kingdom policy now mandates cloud-native designs for all new services, with full migration targeted for 2027, while Germany and Japan enforce in-region data residency that pushes workloads to domestically controlled providers.

Introduction Of Cybersecurity Performance Goals And Funding Programs

CISA’s Cybersecurity Performance Goals and the State and Local Cybersecurity Grant Program dispense USD 3 billion in 2025 alone, unlocking projects for municipalities without in-house expertise. Europe’s Digital Europe Programme has already released EUR 580 million (USD 638 million) for competence centers, and Australia earmarks AUD 1.3 billion (USD 885 million) for sub-national government uplift. Although competitive-match requirements impede some jurisdictions, the funding tide is lifting penetration of managed detection and response and shared SOC models.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Chronic Shortage of Cleared Cybersecurity Professionals | -1.7% | Global, most acute in North America and Europe | Long term (≥ 4 years) |

| Fragmented Legacy Systems Hindering Zero Trust Implementation | -1.3% | Global, particularly in North America and Europe | Medium term (2-4 years) |

| Rising Compliance Costs from Overlapping Security Frameworks | -0.9% | North America and Europe | Medium term (2-4 years) |

| Delayed Procurement Cycles Limiting Rapid Technology Refresh | -0.7% | Global, with extended timelines in Asia Pacific and Middle East and Africa | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Chronic Shortage Of Cleared Cybersecurity Professionals

An estimated 700,000 cleared positions remained vacant worldwide in 2025, inflating labor costs 18-22% for roles that require Top-Secret vetting.[3](ISC)², “Cybersecurity Workforce Study 2025,” ISC2.ORG Clearance processing in the United States averages 287 days, delaying program deployment, while the United Kingdom cites a 14,200-person deficit. Contractors offer cleared staff on flexible contracts, but that concentration adds supply-chain risk if a single vendor becomes overstretched.

Fragmented Legacy Systems Hindering Zero Trust Implementation

Mainframe dependence persists at 63% of U.S. federal agencies, obstructing micro-segmentation and continuous authentication targets. Municipal ERP platforms average more than 15 years in age, and 38% of UK central-government IT spending maintains legacy estates, consuming budgets that could fund modernization. Overlay strategies exist, yet they introduce complexity that further strains scarce cleared talent.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Offering: Services Narrow The Gap With Solutions

Solutions accounted for 63.38% of government and public sector cybersecurity market share in 2025, but professional and managed services are projected to outpace the overall expansion at a 13.23% CAGR. Identity and access management remains the fastest-growing solution family as mandates for phishing-resistant authentication become universal. Services demand escalates because agencies confront integration of zero trust, DevSecOps, and extended detection architectures across mixed legacy and cloud estates. Booz Allen Hamilton, Accenture, and SAIC report double-digit public-sector revenue gains as federal and regional governments outsource roadmap creation, FedRAMP support, and 24/7 SOC operations. Application, cloud, data, network, and endpoint security continue to form the platform core, yet risk-quantification modules and software-supply-chain controls are now embedded by default.

Expanding services spend also reflects talent scarcity. Municipalities adopt managed detection and response when internal staffing fails to satisfy around-the-clock monitoring goals. CrowdStrike Falcon Complete, Palo Alto Networks Cortex XSIAM, and Leidos Global SOC facilities illustrate vendor pivots toward outcome-based contracts. As zero trust overlays mature, projects shift from one-off hardening to continuous-improvement retainers, further boosting the service trajectory within the government and public sector cybersecurity market.

By Deployment Mode: Cloud Momentum Builds Within Hybrid Estates

On-premises infrastructure retained 58.36% of 2025 spending, yet cloud subscriptions are projected to grow 13.24% CAGR, steadily raising their share of the government and public sector cybersecurity market size. FedRAMP High has expanded to 47 cloud service offerings, removing significant procurement friction for highly sensitive U.S. workloads. Similar accreditation tracks in the United Kingdom, Canada, and Australia replicate the template, while Germany, France, and Japan insert sovereignty clauses that require EU- or domestic-entity ownership. As a result, regional providers and defense primes increasingly bid against U.S. hyperscalers for strategic workloads.

Hybrid remains the prevailing architecture because certain classified or latency-sensitive applications will reside on government premises for the foreseeable future. Multi-cloud governance frameworks now receive budget priority to prevent lock-in, and 38% of U.S. agencies already orchestrate workloads across two or more commercial clouds. The result is an enlarged attack surface spanning API gateways, identity brokers, and inter-cloud networking, raising demand for holistic posture-management solutions within the government and public sector cybersecurity market.

By End-Use Industry: Healthcare Accelerates Amid Ransomware Pressure

Banking, financial services, and insurance absorbed 23.67% of 2025 demand, reflecting compliance drivers such as the European Union Digital Operational Resilience Act. However, healthcare is forecast to grow fastest at a 14.12% CAGR because ransomware incidents against public hospitals doubled from 2024 to 2025. Life-critical care disruption forces rapid investment in network segmentation, endpoint protection, and immutable backups. Energy and utilities allocate rising budgets to industrial-control security, while aerospace, military, and defense pay premium pricing for air-gapped, clearance-only solutions.

Retail, e-commerce, and state-run logistics entities also step up spending as they process payment data. Industrial manufacturing is pulled in via supply-chain implications of the U.S. Department of Defense Cybersecurity Maturity Model Certification, requiring 110 practices by 2026. Collectively these verticals reinforce a use-case-diverse government and public sector cybersecurity market.

By End-User Enterprise Size: Shared Services Empower Small Agencies

Large entities still generated 70.53% of 2025 outlays, yet small and medium enterprises are closing the gap with a 12.86% CAGR, supported by shared SOCs, threat-intelligence exchanges, and managed detection contracts. Twenty-eight U.S. states now sponsor statewide SOCs that aggregate municipal telemetry, while India’s National Cyber Coordination Centre shares curated feeds with local authorities. Subscription pricing from Zscaler, CrowdStrike, and Okta eliminates heavy capital commitments and accelerates SME adoption inside the government and public sector cybersecurity market.

Large departments continue to lead in absolute dollars because they must protect classified networks, broad IT estates, and operational technology. Programs such as the U.S. Continuous Diagnostics and Mitigation initiative now cover 4.2 million federal endpoints, underlining scale requirements that only enterprise-grade platforms satisfy. Nevertheless, the services wave brings advanced capabilities to even the smallest county or school district once priced out of enterprise toolsets.

Geography Analysis

North America commanded 34.81% of global revenue in 2025, led by the U.S. Federal Civilian Executive Branch’s USD 13.2 billion cybersecurity budget for fiscal 2026, up 12% from fiscal 2025.[4]The White House, “Budget of the U.S. Government FY 2026,” WHITEHOUSE.GOV CISA’s USD 3 billion 2025 grant pool shapes purchasing behavior across states and counties, while Canada’s CAD 1.9 billion (USD 1.4 billion) National Cyber Security Strategy directs comparable investments into provincial infrastructure. Workforce shortages remain acute, concentrating bidding power among vendors able to supply cleared talent at scale.

Asia Pacific is the fastest-expanding theater, advancing at a 13.48% CAGR through 2031. India allocates INR 23,000 crore (USD 2.76 billion) for digital public infrastructure hardening, and Japan’s sovereign-cloud mandate demands wholesale migration of central workloads by 2027. Australia invests AUD 9.9 billion (USD 6.73 billion using 2025 average 0.68 USD/AUD) over 2023-2030, blending national and sub-national priorities. Singapore’s SGD 1 billion (USD 740 million) operational-technology program reinforces critical-infrastructure defenses. Fragmented procurement rules and a 1.2 million-professional skills gap temper the pace but do not derail momentum inside the government and public sector cybersecurity market.

Europe’s trajectory accelerates under the NIS2 Directive and a EUR 1.9 billion (USD 2.10 billion at 2025 average 1.11 USD/EUR) Digital Europe envelope. Germany’s sovereign-cloud framework and France’s SecNumCloud certifications re-shape provider rosters as EU data-residency rules tighten. The United Kingdom mandates zero-trust rollouts across government, ensuring sustained growth despite fiscal headwinds. The Middle East and Africa invest through national strategies such as the United Arab Emirates’ AED 2.5 billion (USD 680 million at 2025 average 0.27 USD/AED) plan, while South America lags, with Brazil dedicating BRL 1.8 billion (USD 360 million at 2025 average 0.20 USD/BRL) essentially to federal agencies.

Competitive Landscape

Roughly 42% of 2025 global revenue accrued to the top ten suppliers, placing the government and public sector cybersecurity market in a moderately concentrated tier. Palo Alto Networks, Cisco, Fortinet, and Check Point dominate integrated platforms that unify firewalling, SASE, and endpoint protection. Defense primes BAE Systems, Leidos, Raytheon, Northrop Grumman, and General Dynamics hold high-barrier classified contracts.

Cloud-native challengers CrowdStrike, Zscaler, and Okta ride subscription demand tied to workload migration, while services majors Accenture and Booz Allen Hamilton expand managed offerings following zero-trust advisory engagements.

White-space growth resides in operational-technology security and sovereign-cloud stacks. Vendors embed large-language models into security-information and event-management consoles to automate triage, as illustrated by Fortinet’s FortiGuard AI. Consolidation accelerated when Cisco closed the USD 28 billion Splunk acquisition in December 2025, signalling an arms race for telemetry dominance. Competitive viability increasingly hinges on FedRAMP, CMMC, ISO/IEC 27001:2022, and regional sovereign-cloud qualifications.

Government And Public Sector Cybersecurity Industry Leaders

Palo Alto Networks, Inc.

Cisco Systems, Inc.

IBM Corporation

Accenture plc

BAE Systems plc

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2026: Palo Alto Networks won a USD 425 million Pentagon deal to deploy Prisma SASE across 1,200 military installations globally, replacing legacy VPNs with zero-trust network access.

- December 2025: CrowdStrike and Amazon Web Services integrated Falcon Horizon posture management directly into AWS GovCloud, trimming FedRAMP High compliance overhead by 30%.

- November 2025: Cisco closed its USD 28 billion Splunk buyout, merging networking visibility with SIEM analytics for federal customers.

- October 2025: Leidos secured a USD 1.3 billion extension to operate CISA’s Continuous Diagnostics and Mitigation program through 2030.

Global Government And Public Sector Cybersecurity Market Report Scope

The Government and Public Sector Cybersecurity Market is witnessing significant growth due to the increasing frequency of cyberattacks targeting critical infrastructure and sensitive government data. The rising adoption of digital transformation initiatives across public sector organizations and the implementation of stringent regulatory frameworks are further driving the demand for advanced cybersecurity solutions and services globally.

The Government and Public Sector Cybersecurity Market Report is Segmented by Segmented by Offering (Solutions [Application Security, Cloud Security, Data Security, Identity and Access Management, Infrastructure Protection, Integrated Risk Management, Network Security, End Point Security], Services [Professional Services, Managed Services]), Deployment Mode (On-Premises, Cloud), End-Use Industry (IT and Telecom, BFSI, Healthcare, Industrial Manufacturing, Retail and E-commerce, Energy and Utilities, Aerospace, Military and Defense, Other End-Use Industries), and End-User Enterprise Size (Large Enterprises, Small and Medium Enterprises), and Geography (North America, Europe, Asia Pacific, Middle East and Africa, and South America). The Market Forecasts are Provided in Terms of Value (USD).

| Solutions | Application Security |

| Cloud Security | |

| Data Security | |

| Identity and Access Management | |

| Infrastructure Protection | |

| Integrated Risk Management | |

| Network Security | |

| End Point Security | |

| Services | Professional Services |

| Managed Services |

| On-Premises |

| Cloud |

| IT and Telecom |

| BFSI |

| Healthcare |

| Industrial Manufacturing |

| Retail and E-commerce |

| Energy and Utilities |

| Aerospace, Military and Defense |

| Other End-use Industries |

| Large Enterprises |

| Small and Medium Enterprises (SMEs) |

| North America | United States |

| Canada | |

| Mexico | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Nordic Region | |

| Russia | |

| Rest of Europe | |

| Asia Pacific | China |

| India | |

| Japan | |

| South Korea | |

| Southeast Asia | |

| Rest of Asia Pacific | |

| Middle East | UAE |

| Saudi Arabia | |

| Turkey | |

| Rest of Middle East | |

| Africa | South Africa |

| Nigeria | |

| Rest of Africa |

| By Offering | Solutions | Application Security |

| Cloud Security | ||

| Data Security | ||

| Identity and Access Management | ||

| Infrastructure Protection | ||

| Integrated Risk Management | ||

| Network Security | ||

| End Point Security | ||

| Services | Professional Services | |

| Managed Services | ||

| By Deployment Mode | On-Premises | |

| Cloud | ||

| By End-use Industry | IT and Telecom | |

| BFSI | ||

| Healthcare | ||

| Industrial Manufacturing | ||

| Retail and E-commerce | ||

| Energy and Utilities | ||

| Aerospace, Military and Defense | ||

| Other End-use Industries | ||

| By End-User Enterprise Size | Large Enterprises | |

| Small and Medium Enterprises (SMEs) | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Nordic Region | ||

| Russia | ||

| Rest of Europe | ||

| Asia Pacific | China | |

| India | ||

| Japan | ||

| South Korea | ||

| Southeast Asia | ||

| Rest of Asia Pacific | ||

| Middle East | UAE | |

| Saudi Arabia | ||

| Turkey | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Nigeria | ||

| Rest of Africa | ||

Key Questions Answered in the Report

How large will government and public sector cybersecurity spending be by 2031?

Spending is expected to reach USD 153.36 billion by 2031 on a 12.63% CAGR.

Which region is projected to grow fastest in public-sector cybersecurity?

Asia Pacific is forecast to expand at a 13.48% CAGR through 2031, led by India, Japan, and Australia.

What segment is expanding more quickly, services or solutions?

Services outpace solutions with a 13.23% CAGR because agencies need integration and managed SOC support.

Why is healthcare a priority vertical for government cybersecurity budgets?

Ransomware attacks on public hospitals doubled between 2024 and 2025, driving a 14.12% CAGR in healthcare security outlays.

How are sovereign-cloud policies influencing provider selection?

Mandates in Germany and Japan require data residency with domestically controlled infrastructure, favoring regional or defense-affiliated cloud operators.

Page last updated on: