Millimeter Wave Technology Market Size and Share

Market Overview

| Study Period | 2020 - 2032 |

|---|---|

| Market Size (2026) | USD 5.61 Billion |

| Market Size (2032) | USD 20.5 Billion |

| Growth Rate (2026 - 2032) | 24.11% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

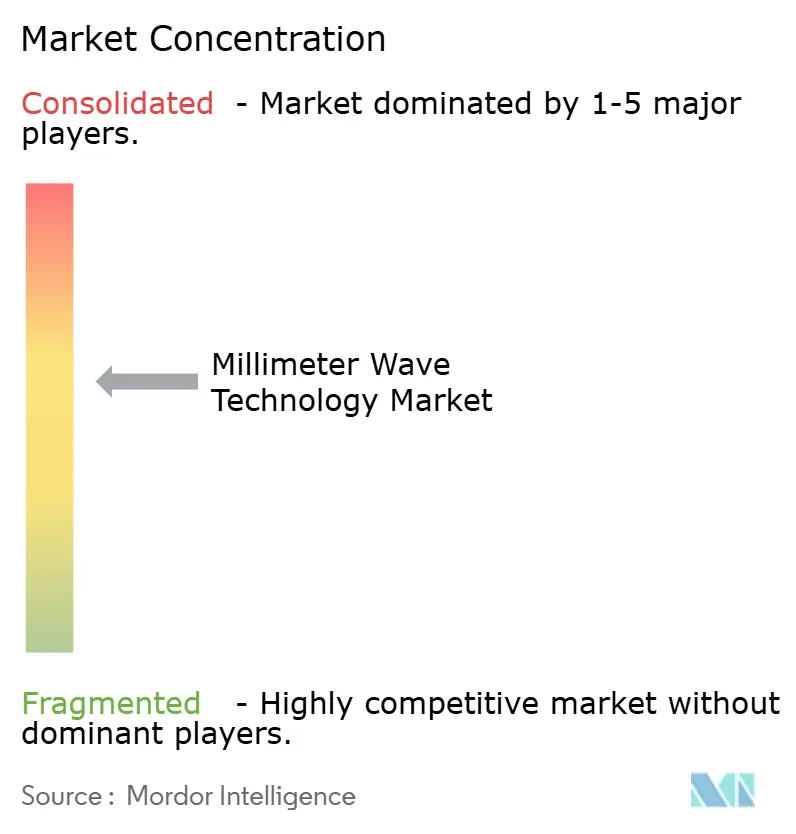

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Millimeter Wave Technology Market Analysis by Mordor Intelligence

The Millimeter Wave Technology Market size is expected to grow from USD 4.52 billion in 2025 to USD 5.61 billion in 2026 and is forecast to reach USD 20.5 billion by 2032 at 24.11% CAGR over 2026-2032.

Network operators are turning to frequencies above 24 GHz for capacity relief, and defense agencies are upgrading radar systems to 94 GHz for higher-resolution targeting. Dual demand arising from dense 5G rollouts and early 6G trials sustains capital spending, while falling device costs encourage adoption in medical imaging, industrial automation, and automotive ADAS. Asia Pacific commands the largest regional position thanks to multi-million-site 5G deployments, whereas North America drives innovation through spectrum liberalization and CHIPS-Act-backed semiconductor funding. Component suppliers benefit from patent-protected RF front-ends, yet supply-chain exposure to gallium-nitride wafers introduces strategic risk.

Key Report Takeaways

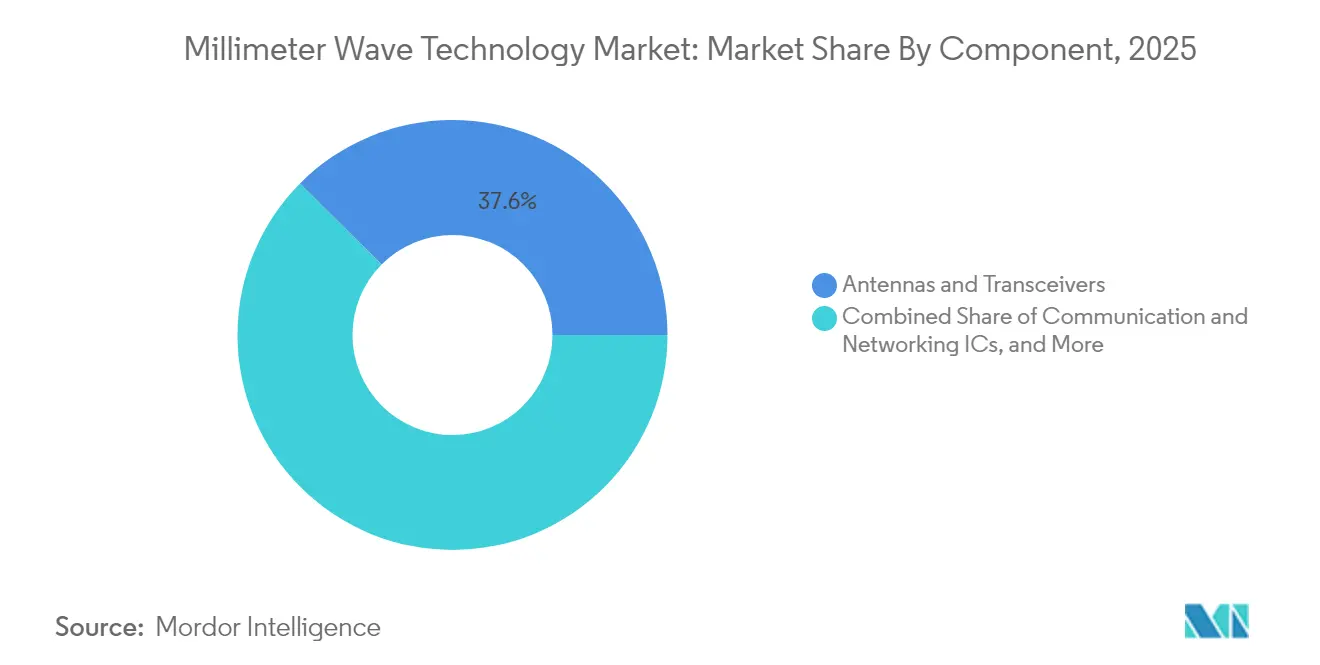

- By component, Antennas and Transceivers led with 37.55% revenue share in 2025; Imaging Sensors are forecast to expand at a 24.86% CAGR through 2031.

- By licensing model, the Fully/Partly Licensed segment held 77.20% of the millimeter wave technology market share in 2025, while Unlicensed bands recorded the highest projected CAGR at 25.60% to 2031.

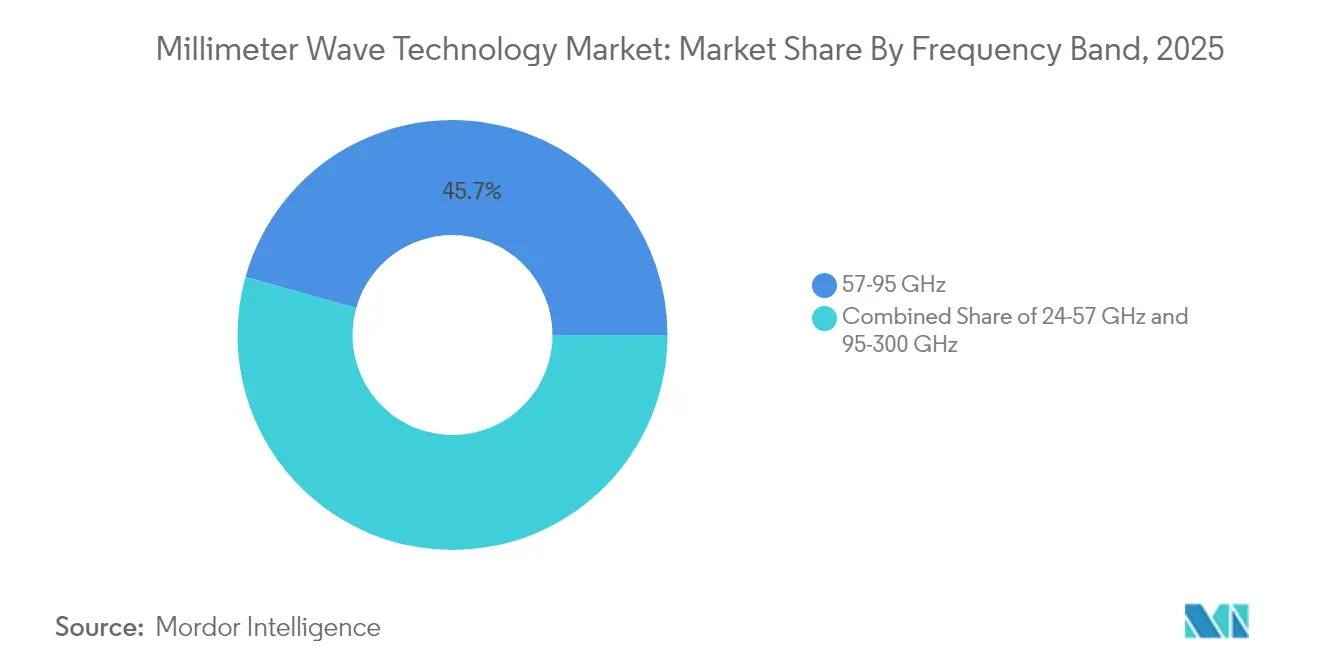

- By frequency band, the 57-95 GHz range accounted for 45.65% of the millimeter wave technology market size in 2025, and the 95-300 GHz band is advancing at a 25.90% CAGR through 2031.

- By application, Telecom Infrastructure captured 53.20% of the millimeter wave technology market size in 2025; Automotive ADAS and V2X are growing fastest at 26.20% CAGR to 2031.

- By geography, Asia Pacific occupied 41.60% of the millimeter wave technology market share in 2025 and is rising at a 27.20% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Market Trends and Insights

Drivers Impact Analysis of Millimeter Wave Technology Market*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| 5G network densification and small-cell backhaul demand | +6.20% | Global with a concentration in Asia Pacific and North America | Medium term (2-4 years) |

| Rising mobile and fixed-wireless data traffic in 24–100 GHz bands | +5.80% | Global, strongest in Asia Pacific and Europe | Short term (≤ 2 years) |

| Spectrum liberalisation and new auctions above 40 GHz | +4.10% | North America and Europe, emerging in the Asia Pacific | Long term (≥ 4 years) |

| Defense radar upgrades to 94 GHz for low-latency targeting | +3.70% | North America and Europe, selective in the Middle East | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

5G network densification and small-cell backhaul demand

Operators quickly discover that fiber becomes uneconomical when small-cell density exceeds urban zoning caps, so 60 GHz and E-band radio links are adopted to connect sites within weeks instead of months. Field trials in China, the United States, and India deliver multi-gigabit throughput, confirming that millimeter-wave backhaul can substitute for high-cost trenching activities. Equipment vendors now integrate software-defined beam steering to reduce alignment time, while urban authorities streamline rooftop permitting to accelerate site activation. Capital efficiency and time-to-market gains make wireless backhaul a cornerstone of the millimeter wave technology market.

Rising mobile and fixed-wireless data traffic in 24–100 GHz bands

Fixed-wireless customers consume up to five times the data of mobile subscribers, forcing operators to allocate contiguous 28 GHz blocks to residential gateways. Regulatory agencies respond by harmonizing 70/80/90 GHz rules to enable wider channels, and chipset makers have announced second-generation CPE platforms with integrated AI for link optimization. These advances support rural broadband programs and stimulate demand across the millimeter wave technology market.

Spectrum liberalization and new auctions above 40 GHz

The FCC is finalizing sharing frameworks for the 37 GHz band, and Europe is evaluating unpaired 42 GHz allocations for 5G-Advanced use cases. License holders view contiguous blocks above 95 GHz as future assets for terabit-per-second links. Early capital commitments by satellite-to-cell and industrial-sensor vendors intensify bidding interest, underpinning long-term growth for the millimeter wave technology market.

Defense radar upgrades to 94 GHz

Procurement budgets earmark USD 647 million for SPY-6 radar deliveries and USD 213 million for upgraded Sentinel systems that exploit 94 GHz for low-latency detection[2]Theresa Hitchens, “Navy Adds USD 647 Million to Raytheon SPY-6 Contract,” govconwire.com. Shared R&D between defense primes and commercial fabs shortens design cycles, enabling dual-use chips suitable for both military and civilian mmWave applications. The convergence lowers unit costs and sustains volume growth.

Restraints Impact Analysis of Millimeter Wave Technology Market*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| RF front-end thermal management limits above 100 GHz | -3.40% | Global, acute in high-temperature environments | Medium term (2-4 years) |

| High-cost phased-array calibration in volume production | -2.80% | Global, higher impact in cost-sensitive markets | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

RF front-end thermal management limits above 100 GHz

Heat concentration rises disproportionately as frequency increases, pushing gallium-nitride devices toward junction temperatures that degrade reliability. Advanced packaging using diamond substrates and micro-fluidic cooling is under evaluation, yet these approaches add material cost and prolong qualification cycles. Until scalable thermal solutions emerge, near-term deployments will cluster below 100 GHz, tempering the millimeter wave technology market’s upper-band growth.

High-cost phased-array calibration in volume production

Current automated test equipment cannot efficiently characterize thousands of antenna elements per module, doubling end-of-line costs in consumer devices. Start-ups are developing self-calibrating beamformers and over-the-air test techniques, but commercial roll-out remains two years away[4]Sivers Semiconductors, “FR3 Beamformer Wins CHIPS Grant,” sivers-semiconductors.com. This cost hurdle limits the deep penetration of millimeter-wave hardware into mid-priced handsets and IoT sensors.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Millimeter Wave Technology Market Segment Analysis

By Component:

Imaging Sensors Open New Clinical FrontiersImaging Sensors deliver the fastest 24.86% CAGR through 2031, as terahertz imaging enables label-free tissue diagnosis in oncology and burn assessment. In contrast, Antennas and Transceivers preserve the largest 37.55% share in 2025 by supplying radio front-ends for mobile base stations. The millimeter wave technology market size for Imaging Sensors is expected to cross USD 3.25 billion by 2031 as hospitals adopt non-ionizing diagnostic tools. Complementary growth in Communication and Networking ICs arises from densified macro-cell deployments, while Interface and Control ICs ride the trend toward radar-on-chip integration.

R&D breakthroughs such as NTT’s 280 Gbps signal generation at 300 GHz improve link budgets and stimulate demand for frequency-agile synthesizers. Meanwhile, Other Components, chiefly advanced substrates and thermal interface materials, gain visibility as integrators seek higher power density. The result is a broadening component stack that anchors the millimeter wave technology market.

By Licensing Model:

Unlicensed Bands Lower Entry BarriersFully or Partly Licensed spectrum delivered 77.20% of 2025 revenue, reflecting the premium attached to interference-free operations in telecom macro cells and defense networks. However, unlicensed allocations above 95 GHz advance at 25.60% CAGR as regulators create industrial presence-sensing rules that require minimal paperwork. SMEs leverage the simplified regime to deploy factory-floor radar for robotics and quality inspection, adding fresh revenue streams to the millimeter wave technology market.

Vendors now introduce dual-mode chipsets that auto-detect regulatory environments and adjust EIRP settings in real time, removing a key adoption barrier. Licensed spectrum will remain critical for mission-critical links, yet the unlicensed surge broadens the overall addressable base.

By Frequency Band:

Sub-Terahertz Momentum BuildsThe 57-95 GHz band held 45.65% millimeter wave technology market size in 2025, buoyed by 60 GHz indoor WiGig and 77 GHz automotive radar. Attention is shifting to the 95-300 GHz range, forecast to expand at 25.90% CAGR as 6G trials and imaging radar demand ever-wider bandwidths. Demonstrations at 300 GHz reach 280 Gbps over laboratory distances, validating the physics for future terabit links.

Component makers focus on waveguide-free packaging to cut insertion loss and ease assembly, while test-equipment suppliers invest in sub-THz vector-network analyzers. These innovations strengthen the foundation of the millimeter wave technology market and accelerate ecosystem readiness for commercial sub-terahertz rollouts.

By Application:

Automotive ADAS Shifts Toward Imaging RadarTelecom Infrastructure maintained a 53.20% share in 2025 as carriers raced to meet 5G capacity targets, yet Automotive ADAS advances at 26.20% CAGR on the promise of 4D imaging radar that outperforms legacy 24 GHz sensors in resolution and range. Vehicle platforms now specify 76-81 GHz corner radars for blind-spot detection and 90 GHz forward-looking units for adaptive cruise control.

Fixed-Wireless Access gains traction in suburban areas where fiber remains cost-prohibitive, and factory automation adds demand for precision presence sensing at 122 GHz. Medical and life-science imaging capitalizes on label-free diagnostics, while aerospace and defense communications sustain steady investment cycles. Collectively, these diversified use cases reinforce the millimeter wave technology market’s long-term growth narrative.

Geography Analysis

APAC Millimeter Wave Technology Market

Asia Pacific commands 41.60% of 2025 revenue and is forecast to grow at 27.20% CAGR through 2031, propelled by China’s 4.4 million 5G base stations and India’s rapid FWA penetration. Regional governments allocate public funds to 5G-Advanced research, and contract manufacturers invest in gallium-nitride wafer lines to localize supply. Japan’s private 5G model shows slower mmWave uptake due to site-acquisition complexity, but corporate campuses are piloting 60 GHz indoor networks for AR training.

North America Millimeter Wave Technology Market

North America aligns spectrum policy with industrial innovation, releasing 37 GHz and 70/80/90 GHz bands while channeling CHIPS-Act incentives toward domestic fabs. Defense radar upgrades and fixed-wireless deployments underpin a resilient customer base, and partnerships such as Nokia-T-Mobile secure multi-year equipment pipelines. Canada adopts mmWave for rural broadband pilots, further expanding the millimeter wave technology market.

EMEA and South America Millimeter Wave Technology Market

Europe positions itself as a technology laboratory. Germany supports 6G testbeds and micro-electronics clusters, and regulators craft 42 GHz auction terms that prioritize manufacturing innovation. Automotive radar demand from German OEMs drives collaboration with specialist chipmakers, while the UK explores 60 GHz transport-infrastructure links. The Middle East invests in smart-city proof-of-concepts, South Africa pilots 28 GHz FWA, and Brazil introduces targeted tax breaks for mmWave CPE assembly. Although revenue contributions from these emerging markets remain single-digit, growth rates surpass mature regions, adding dynamism to the millimeter wave technology market.

Regulatory Landscape

Regulation is increasingly shaped by coexistence rules and harmonized equipment standards across the 24-300 GHz range. In the United States, the Federal Communications Commission (FCC) moved in December 2025 to facilitate more intensive use of upper microwave spectrum by recalibrating the Upper Microwave Flexible Use Service (UMFUS) framework across bands including 24 GHz, 28 GHz, upper 37 GHz, 39 GHz, 47 GHz, and 50 GHz, reflecting growing pressure to balance terrestrial 5G needs with Fixed Satellite Service access.

In Europe, Ofcom progressed auction design for 26 GHz and 40 GHz mobile spectrum in 2025, while also making Shared Access licensing available from January 2025, which lowers entry barriers for localized, enterprise-grade mmWave deployments. Standards development also widened beyond telecom: ETSI issued harmonized standards in 2025 for short-range and radiodetermination equipment at 57-64 GHz (EN 305 550-5) and at higher sub-THz ranges (EN 305 550-6 covering 116-148.5 GHz, 167-182 GHz, and 231.5-250 GHz), and published EN 303 940-1 in February 2026 for indoor mmWave security scanners operating at 69.8-80.5 GHz, supporting compliance-ready productization in screening and sensing use cases.

Value Chain Analysis

The value chain runs from specialty RF and mixed-signal design through wafer fabrication, advanced packaging, module assembly, compliance testing, and OEM integration into telecom, automotive radar, defense, industrial sensing, and imaging systems. Upstream technology and materials are anchored in compound semiconductors (notably GaN for power and InP for very-high-frequency performance) and high-frequency substrates, while downstream value is concentrated in phased-array antennas, RF front-ends, frequency generation, and application-tuned algorithms embedded in radar or backhaul equipment.

Manufacturing and validation are key pinch points. Filtronic highlighted in February 2026 that repeatable mechanical alignment and thermal engineering at scale are gating factors in moving mmWave hardware from prototype to production, while the broader ecosystem remains constrained by specialized foundry capacity, high-frequency laminate availability, and limited firmware and signal-processing talent. Certification and qualification cycles can also stretch time-to-revenue for hardware vendors; compliance pathways such as FCC Part 15 and automotive radar requirements can extend development schedules, elevating the strategic importance of test automation, packaging know-how, and established manufacturing relationships.

Competitive Landscape

Market concentration remains moderate as no single firm exceeds one-third of global shipments. Horizontal platform providers Qualcomm, Nokia, and Ericsson leverage broad patent portfolios to supply chipsets and RAN software across multiple verticals. Vertical specialists such as Arbe Robotics and Aeva differentiate through application-specific algorithms embedded in radar SoCs, securing design wins in Chinese and European automotive programs.

Acquisition activity intensifies: Qorvo bought Anokiwave for USD 31 million to secure beamforming IP, while Keysight committed USD 1.46 billion for Spirent to bolster test automation in sub-THz domains. Foundries expand gallium-nitride capacity after Polymatech’s USD 130 million investment in India, but wafer availability remains a bottleneck. Software-defined radios and AI-based channel estimation are emerging battlegrounds where hardware incumbents face competition from cloud-native entrants. The competitive narrative centers on time-to-market, thermal efficiency, and software differentiation all pivotal to success in the millimeter wave technology market.

Millimeter Wave Technology Industry Leaders

BridgeWave Communications (REMEC)

Ducommun Incorporated

Millimeter Wave Products Inc.

Intel Corporation

Siklu Communication (Ceragon)

- *Disclaimer: Major Players sorted in no particular order

Millimeter Wave Technology Market Companies Covered in this Report

- Anokiwave Inc.

- Aviat Networks

- Broadcom Inc.

- BridgeWave Communications (REMEC)

- Ducommun Incorporated

- Eravant (SAGE Millimeter)

- Farran Technology

- Huawei Technologies

- Intel Corporation

- Keysight Technologies

- L3Harris Technologies

- Millimeter Wave Products Inc.

- NEC Corporation

- Nokia Corporation

- NXP Semiconductors

- Qualcomm Technologies

- Samsung Electronics

- Sivers Semiconductors

- Siklu Communication (Ceragon)

- Smiths Interconnect

- Vubiq Networks

Market Opportunities and Future Outlook

Operator investment is shifting from basic mmWave coverage claims toward deployment efficiency and targeted capacity. This creates whitespace for hardware that reduces site count, improves coverage uniformity, and simplifies integration. A concrete example is the May 2026 KDDI and NTT DOCOMO announcement of a shared millimeter-wave repeater concept to improve coverage efficiency in high-traffic areas, pointing to demand for repeaters, beam-steering antennas, and compact RF front-ends that address propagation limits without relying solely on dense new macro sites. In parallel, Canada has taken formal steps to broaden accessible mmWave spectrum for flexible use through its decision to repurpose the 26 GHz band (24.25-27.5 GHz), creating clearer pathways for equipment investment tied to future licensing and deployment programs.

Standards and pre-commercial roadmaps are also expanding addressable opportunities for component suppliers above traditional 5G bands. In June 2026, 3GPP approved its first 6G RAN study (TR 38.914) aligned with IMT-2030 objectives, reinforcing demand for sub-THz-ready RF chains, test equipment, and packaging innovations that can operate into the 95-300 GHz range highlighted in the market scope. Non-telecom opportunities are becoming more compliance-driven as well, with ETSI harmonized standards covering radiodetermination bands up to 250 GHz and a February 2026 harmonized standard for indoor mmWave security scanners, which supports product launches in industrial sensing and screening where procurement teams typically require standards-backed conformity and predictable certification timelines.

Recent Industry Developments in Millimeter Wave Technology Market

- May 2026: Ducommun Incorporated reported that its defense business momentum continued, supported by multi-year framework agreements with prime contractors (including RTX and Lockheed Martin) and ongoing participation in major missile and radar-related programs. The update reinforces the durability of defense-led demand for high-reliability electronic assemblies and RF-related content that feeds into millimeter-wave radar supply chains.

- June 2025: NTT demonstrated 280 Gbps signal generation in the 300 GHz band, advancing the technical foundation for sub-terahertz communications hardware. This milestone raises requirements for frequency-agile sources, packaging, and validation tooling that can sustain performance at the upper end of the report's 24-300 GHz scope.

- April 2024: Ducommun Incorporated announced two major awards totaling over USD 50 million in revenue tied to the Raytheon SPY-6 family of radar systems. The awards underscore how large radar modernization programs can translate into material order flow for component and assembly suppliers supporting mmWave-enabled defense systems.

Millimeter Wave Technology Market Report Scope and Research Methodology

Market Definition and Coverage

For this report, the millimeter wave technology market is defined as revenue generated from mmWave hardware that operates in the 24 GHz to 300 GHz band and is sold into communications, imaging, sensing, and radar type use cases.

Scope exclusions: We exclude mmWave-related services and software stacks, and we also exclude sub-6 GHz radio equipment.

Segments Covered in This Report

- By Component

- Antennas and Transceivers

- Communication and Networking ICs

- Interface and Control ICs

- Frequency Generation and Filters

- Imaging Sensors

- Other Components

- By Licensing Model

- Fully/Partly Licensed

- Unlicensed

- By Frequency Band

- 24-57 GHz

- 57-95 GHz

- 95-300 GHz

- By Application

- Telecom Infrastructure (RAN and backhaul)

- Mobile and Consumer Devices

- Fixed Wireless Access (FWA)

- Radar and Security Imaging

- Automotive ADAS and V2X

- Industrial Automation and IIoT

- Medical and Life-Sciences Imaging

- Aerospace and Defense Communications

- Other Applications

- By Geography

- North America

- United States

- Canada

- Mexico

- South America

- Brazil

- Argentina

- Rest of South America

- Europe

- United Kingdom

- Germany

- France

- Italy

- Russia

- Rest of Europe

- Asia-Pacific

- China

- Japan

- India

- South Korea

- Rest of Asia-Pacific

- Middle East and Africa

- Middle East

- United Arab Emirates

- Saudi Arabia

- Turkey

- Rest of Middle East

- Africa

- Nigeria

- South Africa

- Rest of Africa

- Middle East

- North America

Data Sources, Market Sizing, and Validation

Desk Research

Desk research was used to set the market boundaries, map where mmWave hardware is shipped, and build a clean historical context before any modeling was started. We referenced public spectrum and licensing material, plus telecom and device standards, because band definitions and rollout timelines determine where demand can show up.

To anchor model inputs, we used sources such as regulator and spectrum bodies (for example, FCC-style releases and auction outcomes), standards organizations (such as 3GPP and IEEE publications), and trade data where applicable (for cross-border RF module movement). We also reviewed patent databases for activity direction, peer reviewed papers for component performance trends, and company filings and investor presentations for shipment, design win, and capacity signals. For a few consistency checks, we used paid subscriptions for company financials and news, plus patent intelligence and shipment-level import-export records. These sources are not exhaustive, and we also reviewed additional public references for data collection, validation, and research clarification.

Primary Interviews and Surveys

Primary interviews and surveys were used to validate adoption timing and pricing behavior across the mmWave value chain. Coverage included component suppliers, module and equipment integrators, operators, and large end users in mobility, security, and industrial sensing. We used respondent input to confirm where deployments are scaling, where they are still pilots, and how average selling prices shift as volumes move from early orders to broader rollouts.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 38% | CXOs: 16% | APAC: 44% |

| Mid tier: 44% | Functional/Unit leaders: 31% | EMEA: 33% |

| Smaller Players: 18% | Managers: 53% | Americas: 23% |

Market-Sizing & Forecasting

Sizing starts with a top-down build that reconstructs the addressable demand pool from mmWave deployment signals and hardware intensity, then converts it into value using practical price and mix assumptions. The demand pool was shaped using indicators such as 5G mmWave site additions and densification plans, backhaul and fixed wireless link deployments, radar and imaging sensor shipment direction, licensed band availability, and replacement cycles for high frequency modules.

After that structure is established, selective bottom-up approximations were used to keep totals realistic. This included sampled revenue rollups from public company disclosures, channel checks on typical module ASP ranges, and unit-based multipliers (for example, radios per site, antennas per node, and sensor content per system). Where a supplier or application had limited disclosure, we handled gaps by applying range-based ASPs and conservative volume proxies, then rechecking them through expert feedback.

For forecasting, scenario analysis was used because demand is sensitive to rollout timing, spectrum readiness, and the pace of network densification. The scenarios were anchored on a base case aligned to the most common view from interviews, then stress-tested with faster and slower adoption paths. These paths adjust site counts, component content per deployment, and price erosion rates.

Data Validation & Update Cycle

Model outputs were checked against independent signals, including public rollout milestones, spectrum announcements, shipment direction, and the implied hardware content per deployment. Any inconsistencies were reviewed before sign-off. When a variance appeared structural rather than noise, we rechecked the assumption chain, and follow-up outreach was used to confirm whether the change came from pricing, mix, or timing.

The report is refreshed annually, with interim updates when material events occur, such as large spectrum releases, major policy shifts, or clear acceleration in deployments. Before delivery, a final pass is completed so clients get the latest updated view with consistent assumptions and clean currency conversions.

Mordor Intelligence's Millimeter Wave Technology Market Size Measured Against Other Published Estimates

Published market sizes for millimeter wave technology can differ even when the topic label looks the same, because the counted revenue pool is not always consistent and the timing of deployment led demand can shift quickly. We also see gaps when pricing is treated as static, or when the cut between hardware, software, and services is not kept stable across years.

In practice, the spread usually comes from three areas: what is included (for example, component only versus broader system value), how ASP decline is modeled as volumes ramp, and the currency timing used when vendors report in different periods. By refreshing the price and rollout assumptions on an annual cadence and rechecking outliers through repeat validation calls, Mordor Intelligence keeps the 2026 value tied to mmWave hardware revenue only, which reduces accidental double counting from adjacent connectivity spend.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 5.61 B (2026) | |

| Industry Publisher A | USD 4.50 B (2024) | Uses an earlier base year and a slower adoption curve, and the scope appears broader across license types and end users, which can mix different maturity levels and keep near term value lower. |

| Industry Publisher B | USD 5.18 B (2024) | Anchors the estimate to a 2024 value with aggressive growth expectations to 2030, and the scope definition is less explicit on hardware-only boundaries, which can pull in system level value and inflate the total. |

The comparison shows that year selection and scope control matter as much as the math. When the counted boundary stays focused on mmWave hardware, and pricing plus rollout timing are updated with repeat checks, the market size becomes easier to trace back to the underlying drivers and to explain on a decision timeline.

Key Questions Answered in the Report

What is the current size of the millimeter wave technology market and how fast is it growing?

The market stands at USD 5.61 billion in 2026 and is projected to reach USD 20.5 billion by 2032, reflecting a 24.11% CAGR.

Which region leads the millimeter wave technology market?

Asia Pacific holds 41.60% revenue share in 2025 and is expanding at a 27.20% CAGR through 2031, outpacing every other region.

What application segment is projected to grow fastest?

Automotive ADAS and V2X posts the highest 26.20% CAGR to 2031 due to demand for high-resolution imaging radar.

Which frequency band offers the greatest near-term revenue, and which is slated for the fastest growth?

The 57-95 GHz band captures 45.65% of 2025 revenue, while the 95-300 GHz range is forecast to expand at a 25.90% CAGR.

Why are unlicensed bands gaining traction in this market?

New 95 GHz-plus allocations and simplified rules for industrial sensing lower entry barriers, driving a 25.60% CAGR for unlicensed deployments.

What primary challenge could limit adoption above 100 GHz?

RF front-end thermal management remains the chief technical restraint, exerting a negative 3.4% impact on the forecast CAGR.

Page last updated on: