Cough Remedies Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 11.82 Billion |

| Market Size (2031) | USD 22.65 Billion |

| Growth Rate (2026 - 2031) | 6.04% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Cough Remedies Market Analysis by Mordor Intelligence

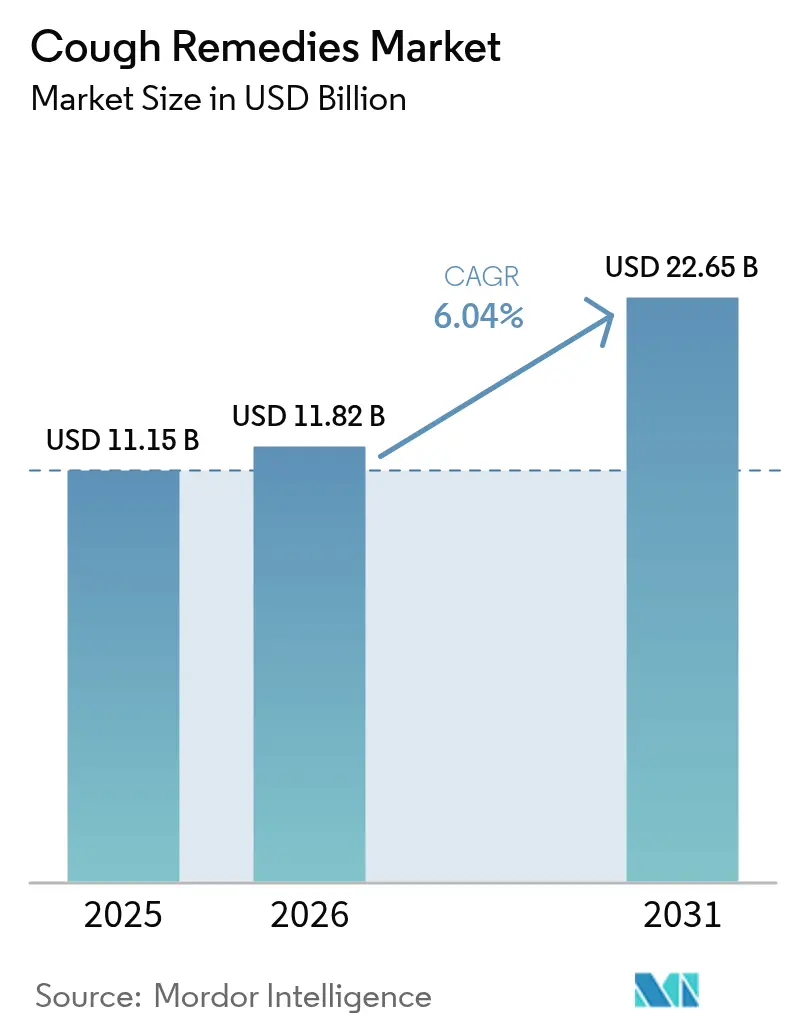

The Cough Remedies Market size is expected to grow from USD 11.15 billion in 2025 to USD 11.82 billion in 2026 and is forecast to reach USD 22.65 billion by 2031 at 6.04% CAGR over 2026-2031.

The growing global burden of respiratory diseases, coupled with rapid over-the-counter (OTC) reclassifications and advanced digital retail tools, is driving strong demand in the market. Expectorants dominated revenue in 2025; however, bronchodilators are witnessing accelerated growth as regulatory support for self-managed chronic obstructive pulmonary disease (COPD) protocols increases. E-pharmacies are steadily capturing market share from traditional pharmacies by leveraging mobile ordering, AI-driven solutions, and same-day delivery, aligning with consumer preferences for convenience. Simultaneously, stricter codeine regulations and climate-induced shortages of licorice root and ivy leaf extract are prompting a shift in product portfolios toward non-opioid antitussives and botanically sourced expectorants.

Key Report Takeaways

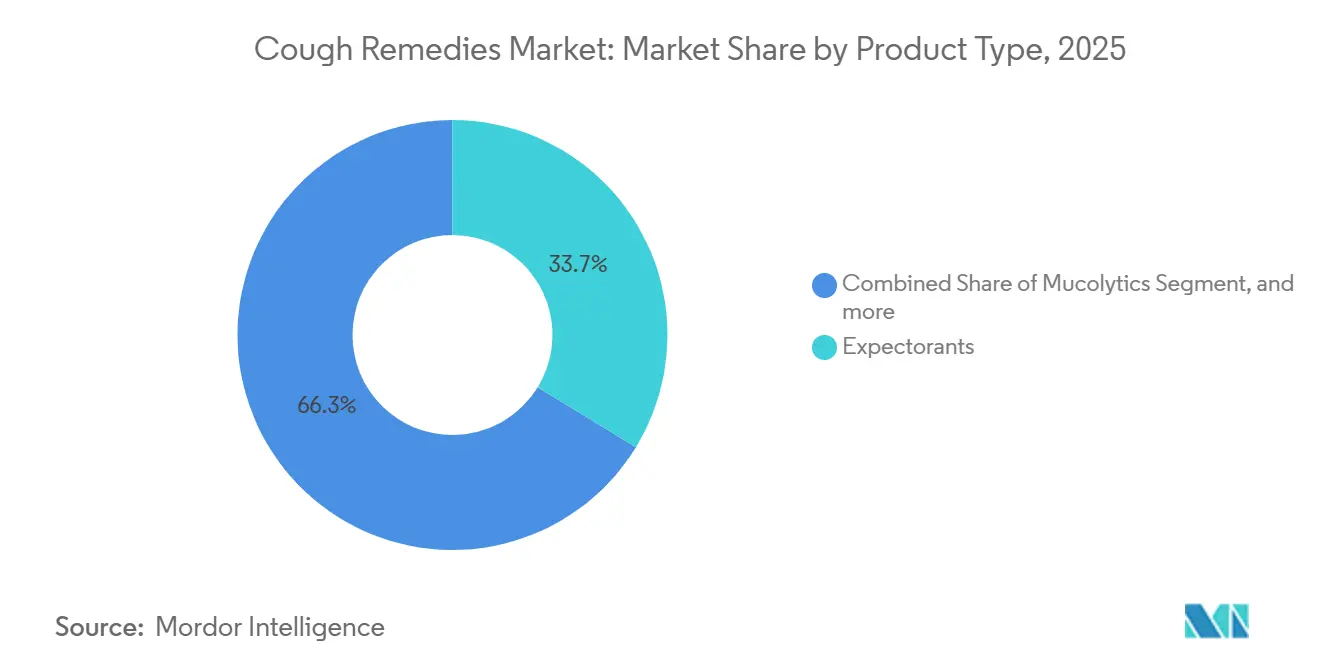

- By product type, expectorants captured 32.65% of the cough remedies market share in 2025, while bronchodilators are projected to expand at an 8.54% CAGR to 2031.

- By dosage form, syrup and linctus formats accounted for 39.54% of the cough remedies market size in 2025, whereas gummies and confectionery variants are forecast to grow at 8.76% through 2031.

- By distribution channel, hospital and clinic pharmacies held 41.76% of revenue in 2025; online channels are advancing at a 9.54% CAGR over the forecast period.

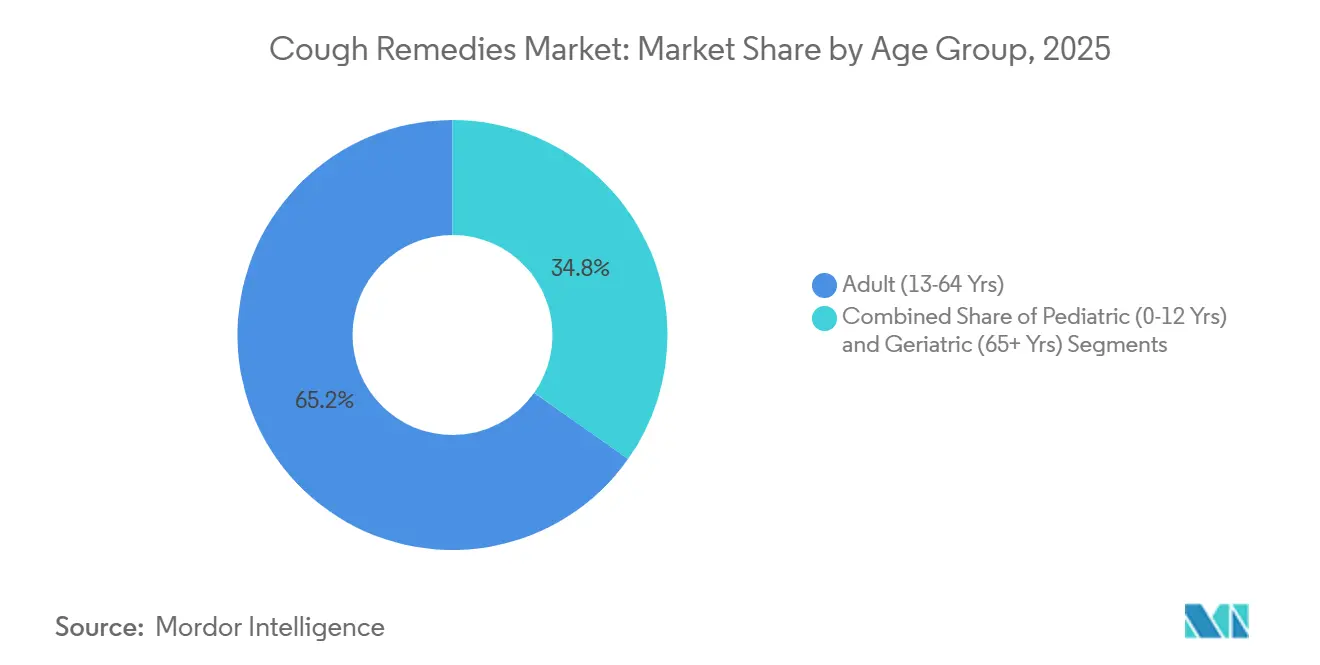

- By age group, adults aged 18-60 years accounted for 65.21% of usage in 2025, but the pediatric and adolescent segment is rising at a 9.12% CAGR through 2031.

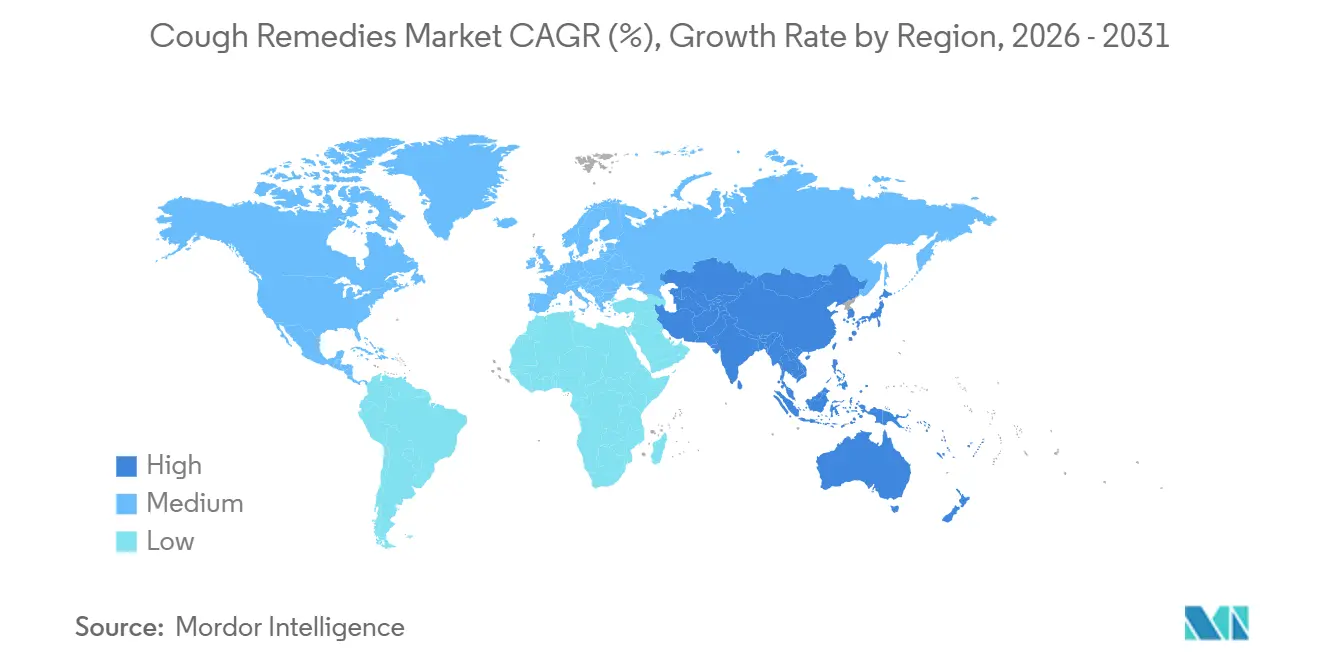

- By geography, North America led with a 42.76% revenue share in 2025, while Asia-Pacific is anticipated to record the fastest regional CAGR of 7.54% through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Cough Remedies Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growing global burden of respiratory diseases | +1.8% | Global (higher in APAC & MEA) | Long term (≥ 4 years) |

| Expanding over-the-counter drug accessibility | +1.2% | North America & EU, expanding in APAC | Medium term (2-4 years) |

| Rising consumer preference for self-care healthcare | +1.5% | Global, led by developed markets | Medium term (2-4 years) |

| Increasing adoption of digital retail channels | +0.9% | Global, strongest in urban areas | Short term (≤ 2 years) |

| Development of novel non-opioid antitussive therapies | +0.4% | North America & EU initially | Long term (≥ 4 years) |

| Government initiatives promoting public health awareness | +0.3% | Global, varies by system maturity | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Growing Global Burden of Respiratory Diseases

More than 569 million people lived with chronic respiratory ailments in 2023, and respiratory infections remained the fourth-leading global cause of mortality. Urban air pollution in megacities such as Delhi and Beijing is driving up COPD and asthma incidence, while aging populations in Europe and Japan are expanding the pool of people requiring long-term cough control. Drug makers are answering by reformulating legacy products to limit side effects and by launching multi-symptom combinations that address allergic rhinitis or post-viral irritation, thereby increasing per-episode spending.

Expanding Over-The-Counter Drug Accessibility

Regulators increasingly view pharmacist-guided OTC access as a path to relieve overstretched clinics. The U.S. Food and Drug Administration authorized several bronchodilator inhalers for non-prescription sale in 2024, and Japan’s health ministry broadened OTC expectorant categories in 2025[1]U.S. Food and Drug Administration, “FDA Approves Over-the-Counter Use of Certain Bronchodilators,” fda.gov. Lower barriers cut time-to-market for generics and let manufacturers divert marketing budgets from physician detailing to consumer-centric digital campaigns.

Growth of E-Pharmacies and Digital Retail Platforms

E-pharmacy volumes surged after the pandemic as home delivery and subscription refill models proved sticky with chronic users. Chinese and Indian platforms embed recommendation engines that draw on past purchases and symptom inputs to raise order values, while the European Medicines Agency’s 2025 guidance created a single market for cross-border non-prescription shipments[2]European Medicines Agency, “Guideline on Cross-Border Sales of Non-Prescription Medicines,” ema.europa.eu. Smaller brands exploit these channels to bypass brick-and-mortar gatekeepers and target niche consumer groups directly.

Adoption of AI-Based Symptom-Triage Apps Driving Targeted Self-Medication

Clinical studies published in 2024 found that cough-audio classifiers exceeded 90% diagnostic accuracy, distinguishing between productive and dry coughs and providing tailored OTC suggestions. Integrated telemedicine escalation enables seamless physician referral when red-flag criteria are met. Pharmaceutical firms partner with app developers, embedding product vouchers within triage workflows to create data-rich, closed-loop ecosystems.

Restraints Impact Analysis*

| Restraints Impact Analysis | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Stringent regulatory framework for cough medication ingredients | -1.1% | Global, stricter in developed markets | Medium term (2-4 years) |

| Safety concerns related to opioid and codeine-based formulations | -0.8% | North America & EU | Short term (≤ 2 years) |

| Limited clinical evidence supporting product efficacy | -0.6% | Global, pronounced in emerging markets | Medium term (2-4 years) |

| Availability of alternative non-pharmacological therapies | -0.5% | Global, higher in wellness-focused regions | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Safety Concerns Around Opioid- and Codeine-Based Formulations

The FDA and European regulators tightened warnings on codeine cough syrups after sustained reports of misuse and respiratory depression, culminating in shelf withdrawals by several U.K. and German retailers in 2025. Dextromethorphan, though non-opioid, now faces age-restriction laws in multiple U.S. states due to adolescent abuse cases. Manufacturers are accelerating pivots to honey-based suppressants and botanical alternatives, although evidence standards remain under debate.

Supply-Chain Vulnerability to Climate-Related Botanical Shortages

Drought in Central Asia cut licorice root yields by about 15% between 2022 and 2024, while late frosts hit ivy crops in Eastern Europe[3]Food and Agriculture Organization, “Climate Impacts on Medicinal Plant Yields 2024 Report,” fao.org. Cost spikes and quality variance threaten small herbal specialists that lack diversified sources. Multinationals respond with contract farming in Morocco and Turkey and explore plant-cell-culture biotechnologies to stabilize active-compound supply.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Bronchodilators Gain as COPD Self-Care Expands

Bronchodilators are projected to rise at a 8.54% CAGR, well above the overall cough remedies market. OTC approval of low-dose beta-agonist inhalers in Japan and South Korea lets COPD patients manage mild flare-ups without clinic visits, moving a traditionally prescription category into retail space. Expectorants accounted for 32.65% of 2025 revenue, led by guaifenesin syrups and herbal variants such as licorice and ivy. Antitussives face codeine-related headwinds, prompting reformulation with honey, marshmallow, and other naturals. Combination cold-and-cough packs are proliferating as retailers favor SKUs that deliver multi-symptom coverage within limited shelf space.

Second-order impacts include rising R&D around abuse-deterrent polymers for dextromethorphan and extended-release bead technology that keeps blood levels stable overnight. Differential positioning is clear: evidence-backed bronchodilators and mucolytics appeal to physicians, whereas botanically formulated expectorants and antitussives attract wellness-oriented consumers. Flexible brand architecture that addresses both cohorts is becoming a strategic necessity.

By Dosage Form: Gummies Reshape Pediatric Compliance

Syrups still accounted for 39.54% of the cough remedies market in 2025, yet gummy and chewable formats are forecast to expand by 8.76% annually as child-friendly flavors curb dosing resistance. Tablets and capsules dominate adult usage because portability offsets slower onset, and lozenges fill the niche for throat-soothing menthol or benzocaine. Rapid-dissolve herbal film strips have received pediatric approvals in India and parts of Southeast Asia, offering sublingual uptake and eliminating the need to swallow.

Investment momentum is strong: Reckitt Benckiser commissioned new gummy lines in 2025, and Haleon piloted orally disintegrating tablets for its Robitussin franchise. Contract manufacturers with expertise in pectin-based or vegan gelatin command premium valuations as brands outsource specialized production.

By Age Group: Pediatrics Drive Innovation Cycles

Adults aged 18-60 accounted for 65.21% of use in 2025, reflecting work absenteeism costs and a self-care culture that favors OTC first. However, the pediatrics and adolescents segment, with a 9.12% CAGR, is driving R&D toward taste-masked ingredients and dosing formats that prevent choking or spillage. Abuse-deterrent dextromethorphan matrices won FDA clearance in 2025, addressing teen misuse without limiting legitimate relief. Geriatric formulations avoid anticholinergic load and sedative antihistamines, leaning instead on low-dose natural actives that minimize drug-interaction risk with polypharmacy regimens.

Regulators compel pediatric investigation plans for every new submission in Europe, raising development costs but ultimately boosting caregiver confidence in labeled dosing. Age-tailored branding and pack design—dropper bottles for infants, single-serve sachets for schoolchildren—have become key levers for differentiation.

By Distribution Channel: E-Pharmacies Disrupt Traditional Retail

Hospital and clinic pharmacies remained the leading channel in 2025 with 41.76% share, owing to physician recommendations and captive patient traffic. Yet online outlets are advancing at 9.54% and reshaping the cough remedies market. Mobile apps integrate algorithmic product advice, loyalty points, and subscription refills that bind chronic cough sufferers into predictable revenue streams.

Brick-and-mortar chains respond with click-and-collect lockers and in-store digital kiosks, but margin squeeze is evident as price transparency grows. Amazon Pharmacy’s 2024 U.S. launch compressed average selling prices, forcing regional chains to renegotiate supplier terms. The next battleground is omnichannel inventory integration, where real-time stock visibility and unified consumer data underpin seamless switching between online and offline touchpoints.

Geography Analysis

North America generated 42.76% of global revenue in 2025, underpinned by high health-spending elasticity, brand loyalty to heritage labels, and extensive pharmacy networks. Growth is steady rather than explosive as the region approaches saturation, yet innovation in naturals and digital-ecosystem tie-ins helps sustain premium price points. The FDA’s move to allow OTC bronchodilators opened a previously out-of-reach secondary prevention segment, while Canada’s inclusion of certain cough syrups in public drug plans widened access for low-income groups.

Asia-Pacific is the fastest-expanding region, projected to grow at a 7.54% CAGR to 2031, and now contributes a rising share of total cough remedies market revenue. Urban air pollution and smartphone ubiquity spur both incidence and digital-first purchasing behaviors. China’s dual structure separates traditional Chinese medicine (TCM) dominance in rural areas from Western synthetic medicine preferred by urban millennials. In India, Ayurvedic leaders leverage rural distribution muscle, while multinationals cluster around e-commerce growth in metros. Mature Japan and South Korea see demand lift from aging COPD patients and national insurance systems that reimburse select OTC respiratory therapies. Regulatory heterogeneity across ASEAN continues to complicate product registration, but ongoing harmonization efforts promise smoother pan-regional launches within three years.

Europe’s scene blends strict pharmacovigilance with a strong herbal tradition, especially in Germany, where ivy leaf and thyme syrups share shelf space with synthetic brands. The European Medicines Agency’s 2025 clampdown on codeine shortened the lifecycles of legacy products, shifting volume to naturals and combination packs. South America and the Middle East & Africa remain smaller contributors today, yet Gulf Cooperation Council retail expansion and Mercosur regulatory alignment are setting a foundation for mid-term acceleration. Currency volatility in Brazil and Argentina gives domestic producers a price advantage over imports, while Africa’s nascent e-pharmacy models aim to bypass infrastructure gaps and counterfeit risks alike.

Competitive Landscape

By 2025, the five largest vendors—Haleon, Reckitt Benckiser, Johnson & Johnson Consumer Health, Procter & Gamble (Vicks), and Perrigo—are projected to hold a combined market share of approximately 40%. These key players leverage extensive global distribution networks, consistent media investments, and patented delivery technologies to maintain their competitive advantage. Their combination formulations, designed to address multiple nasal and chest symptoms, secure prominent shelf space and discourage retailers from rationalizing SKUs.

In January 2026, Haleon partnered with Hyfe AI to integrate cough-monitoring analytics into the Robitussin app, offering personalized dosing reminders and coupon incentives. This initiative aligns consumer health with digital therapeutics. Reckitt expanded its gummy production capacity in the United Kingdom to capture growth in the pediatric segment, while Johnson & Johnson collaborated with JD Health to capitalize on China’s rapidly growing e-pharmacy market.

Niche Ayurvedic and Traditional Chinese Medicine (TCM) companies, such as Dabur, Himalaya Wellness, and Nin Jiom, are targeting wellness-conscious consumers who prefer natural products over synthetics. These firms enhance their authenticity claims through climate-resilient herb sourcing, vertical farming, and blockchain-enabled traceability. Generic manufacturers, while aggressively competing on price as patents expire—particularly for guaifenesin and dextromethorphan combinations—struggle to match the flavor-masking expertise and child-proof packaging investments of multinational corporations. Strategic growth opportunities lie in non-opioid antitussives, plant-cell-culture actives, and AI-driven omnichannel engagement, with both established players and start-ups striving to secure first-mover advantages in these areas.

Cough Remedies Industry Leaders

Johnson & Johnson

Reckitt Benckiser Group plc

GlaxoSmithKline plc

Bayer AG

Pfizer Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2025: Schmittgall HEALTH launched a campaign to introduce the Silomat cough suppressant for the client STADA Consumer Health.

- February 2025: Hyfe, Inc., one of the global leaders in AI-powered respiratory care, partnered with KYORIN Pharmaceutical Co., Ltd for the development and commercialization of the world’s first prescription digital therapeutic (DTx) to treat chronic cough in the Japanese market.

- August 2025: Kenvue, one of the leading consumer health companies and maker of Benadryl, partnered with the Association of Physicians of India to launch India's first Cough Clinics, aiming to advance respiratory primary care and symptom science. This industry-first initiative focuses on improving the diagnosis and treatment of cough-related conditions.

Global Cough Remedies Market Report Scope

As per the scope of the report, cough remedies are medications or treatments used to alleviate or suppress coughing, often targeting the underlying cause or providing symptomatic relief. They include over-the-counter products like cough syrups, lozenges, and natural remedies.

The Cough Remedies Market is Segmented by Product Type (Antitussives, Expectorants, Mucolytics, Bronchodilators, Antihistamines, Decongestants, Combination Medications, and Other Product Types), Dosage Form (Syrup/Linctus, Tablets & Capsules, Lozenges/Pastilles, Nasal Drops/Sprays, Gummies & Confectionery, and Balms/Inhalers), Age Group (Pediatrics & Adolescents, Adults, and Geriatrics), Distribution Channel (Retail Pharmacies, Hospital/Clinic Pharmacies, and Online/E-Pharmacies), and Geography (North America, Europe, Asia-Pacific, Middle East & Africa, and South America). The Market Forecasts are Provided in Terms of Value (USD). The market report also covers the estimated market sizes and trends for 17 countries across major regions globally. The report offers the value (in USD million) for the above segments.

| Antitussives (Opioid & Non-Opioid) |

| Expectorants |

| Mucolytics |

| Bronchodilators |

| Antihistamines |

| Decongestants |

| Combination Medications |

| Other Product Types |

| Syrup / Linctus |

| Tablets & Capsules |

| Lozenges / Pastilles |

| Nasal Drops / Sprays |

| Gummies & Confectionery |

| Balms / Inhalers |

| Pediatrics & Adolescents (Below 18 Years) |

| Adults (18-60 Years) |

| Geriatrics (Above 60 Years) |

| Retail Pharmacies |

| Hospital / Clinic Pharmacies |

| Online / E-Pharmacies |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| Australia | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East & Africa | GCC |

| South Africa | |

| Rest of Middle East & Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Product Type | Antitussives (Opioid & Non-Opioid) | |

| Expectorants | ||

| Mucolytics | ||

| Bronchodilators | ||

| Antihistamines | ||

| Decongestants | ||

| Combination Medications | ||

| Other Product Types | ||

| By Dosage Form | Syrup / Linctus | |

| Tablets & Capsules | ||

| Lozenges / Pastilles | ||

| Nasal Drops / Sprays | ||

| Gummies & Confectionery | ||

| Balms / Inhalers | ||

| By Age Group | Pediatrics & Adolescents (Below 18 Years) | |

| Adults (18-60 Years) | ||

| Geriatrics (Above 60 Years) | ||

| By Distribution Channel | Retail Pharmacies | |

| Hospital / Clinic Pharmacies | ||

| Online / E-Pharmacies | ||

| Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| Australia | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East & Africa | GCC | |

| South Africa | ||

| Rest of Middle East & Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

What is the projected value of the cough remedies market by 2031?

The sector is forecast to reach USD 22.65 billion by 2031 on a 6.04% CAGR trajectory.

Which product category is growing the fastest?

Bronchodilators, expanding at a 8.54% CAGR, outpace all other categories through 2031.

Why are gummies gaining popularity in pediatric cough care?

Child-friendly flavors and chewable formats improve dosing compliance, driving a 8.76% CAGR for gummy and confectionery variants.

How significant is e-pharmacy to future sales?

Online channels are projected to grow 9.54% annually, steadily capturing share from traditional hospital and clinic pharmacies.

What regulatory trend most affects formulation strategy?

Heightened restrictions on codeine and dextromethorphan misuse are pushing manufacturers toward non-opioid and botanical alternatives.

Page last updated on: