Cell Sorting Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

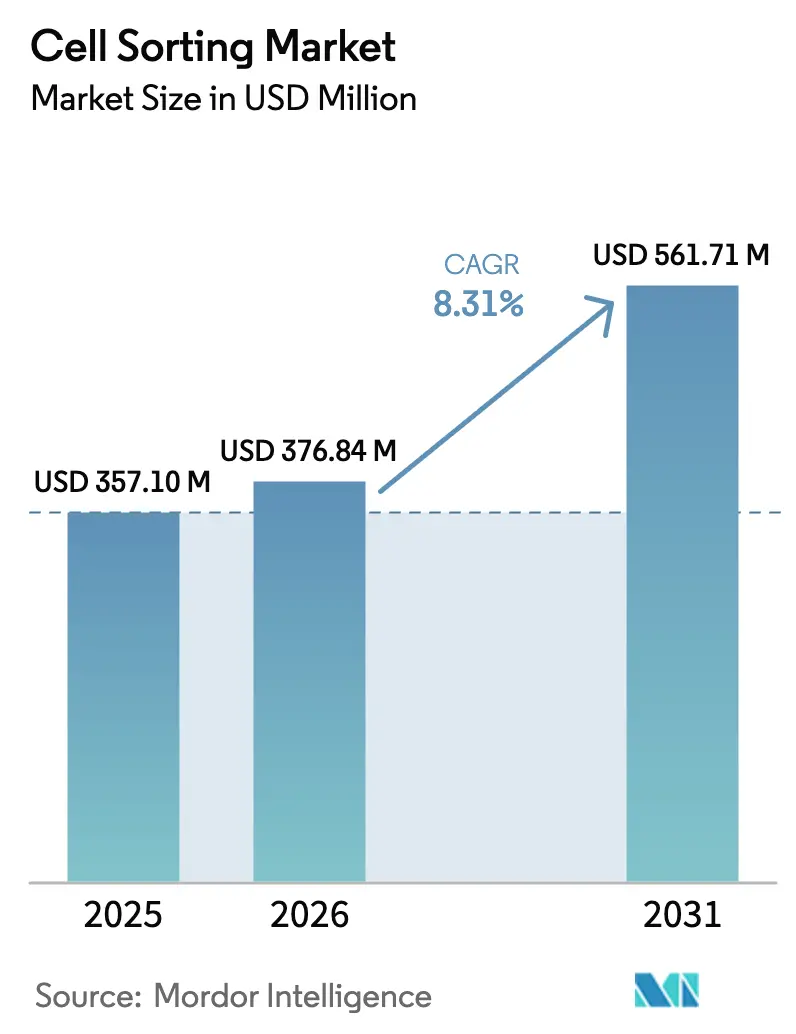

| Market Size (2026) | USD 376.84 Million |

| Market Size (2031) | USD 561.71 Million |

| Growth Rate (2026 - 2031) | 8.31% CAGR |

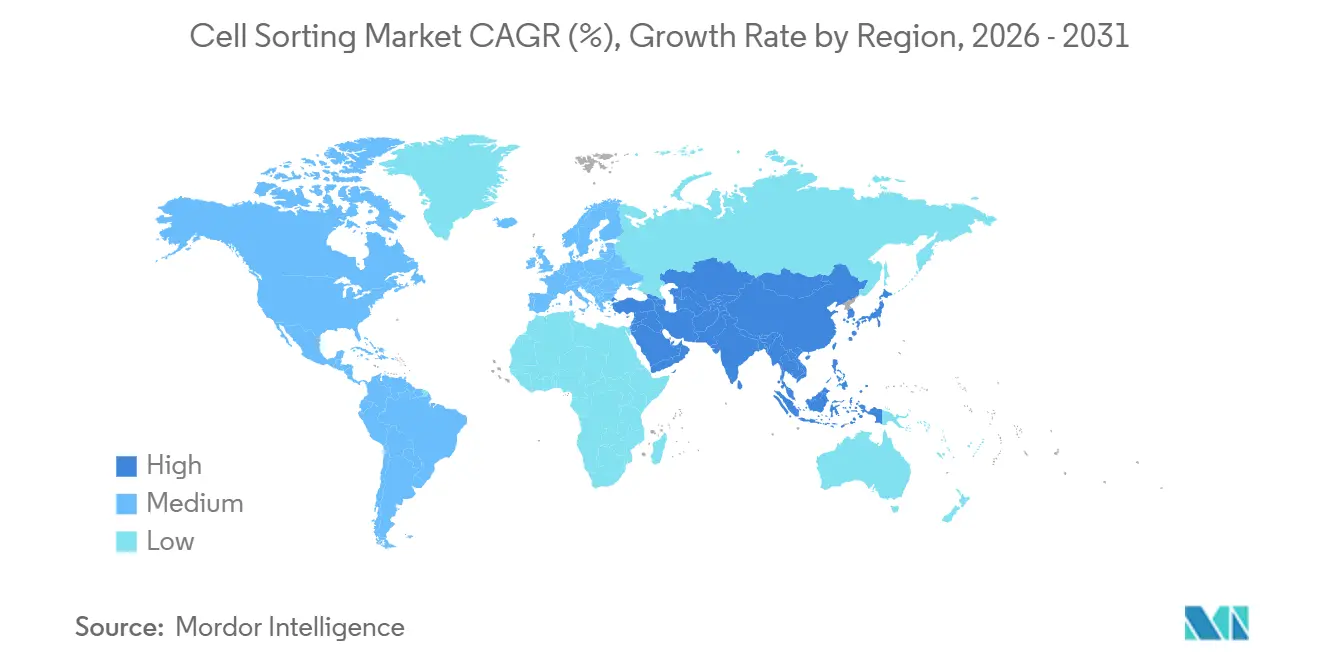

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

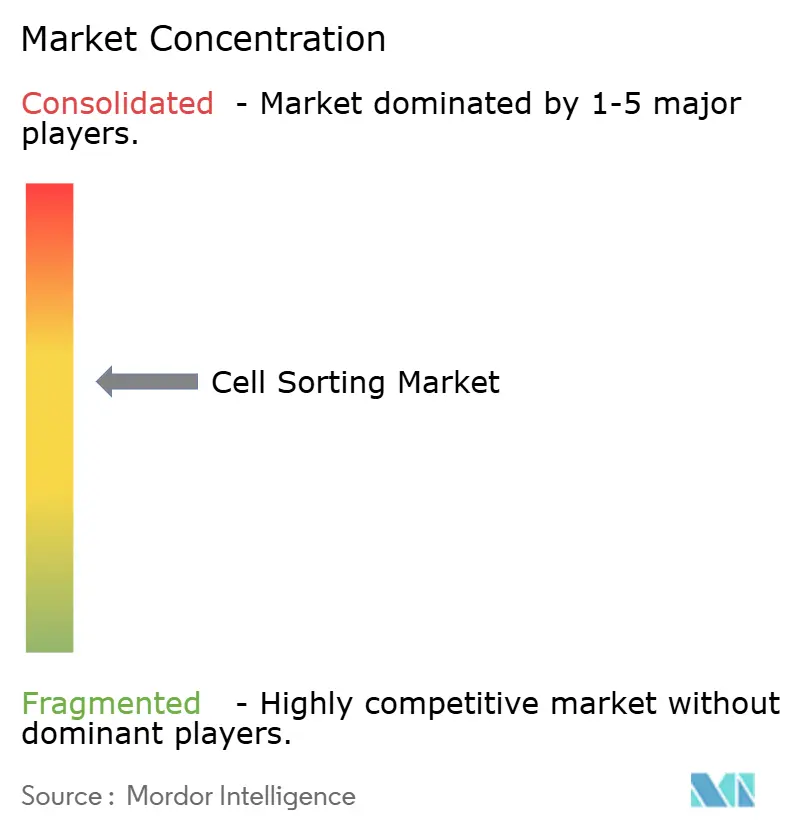

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Cell Sorting Market Analysis by Mordor Intelligence

The Cell Sorting Market size is projected to expand from USD 357.10 million in 2025 and USD 376.84 million in 2026 to USD 561.71 million by 2031, registering a CAGR of 8.31% between 2026 to 2031.

The cell sorting market is shifting from a research convenience toward a critical bottleneck in cell and gene therapy (CGT) manufacturing, changing procurement priorities for instruments, reagents, and services. Demand is amplifying as image-enabled and spectral technologies displace filter-based droplet systems, while contract sorting services scale to meet good manufacturing practice (GMP) requirements. Supply-chain vulnerabilities—particularly for lasers and microfluidic chips—put pricing power in the hands of qualified vendors, and regulatory emphasis on post-sort viability compels users to adopt gentler, high-parameter platforms. Together, these forces are redefining capital-allocation strategies, driving recurring consumable revenue, and consolidating sorting capacity in organizations capable of sustaining 24/7 operations.

Key Report Takeaways

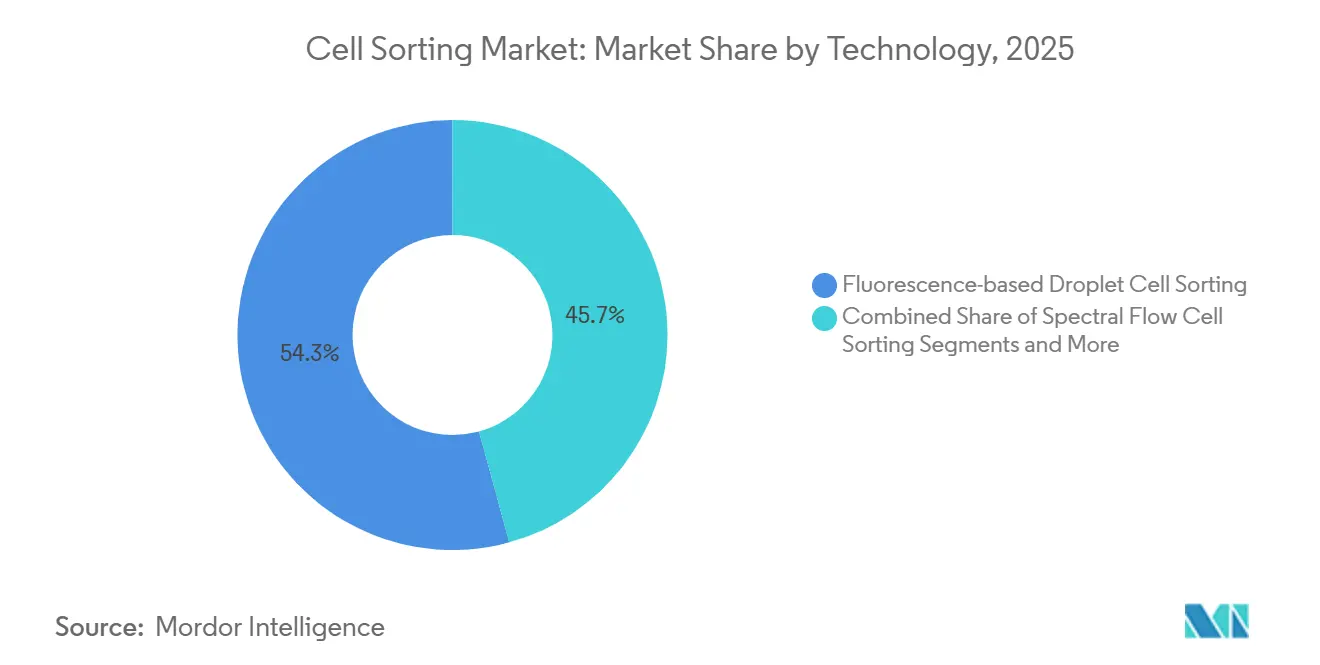

- By technology, fluorescence-based droplet systems commanded 54.26% of the cell sorting market share in 2025, while image-enabled platforms are projected to advance at a 12.35% CAGR through 2031.

- By product and service, reagents and consumables accounted for 42.63% of the cell sorting market size in 2025, whereas services are expected to grow at an 11.45% CAGR over the forecast period.

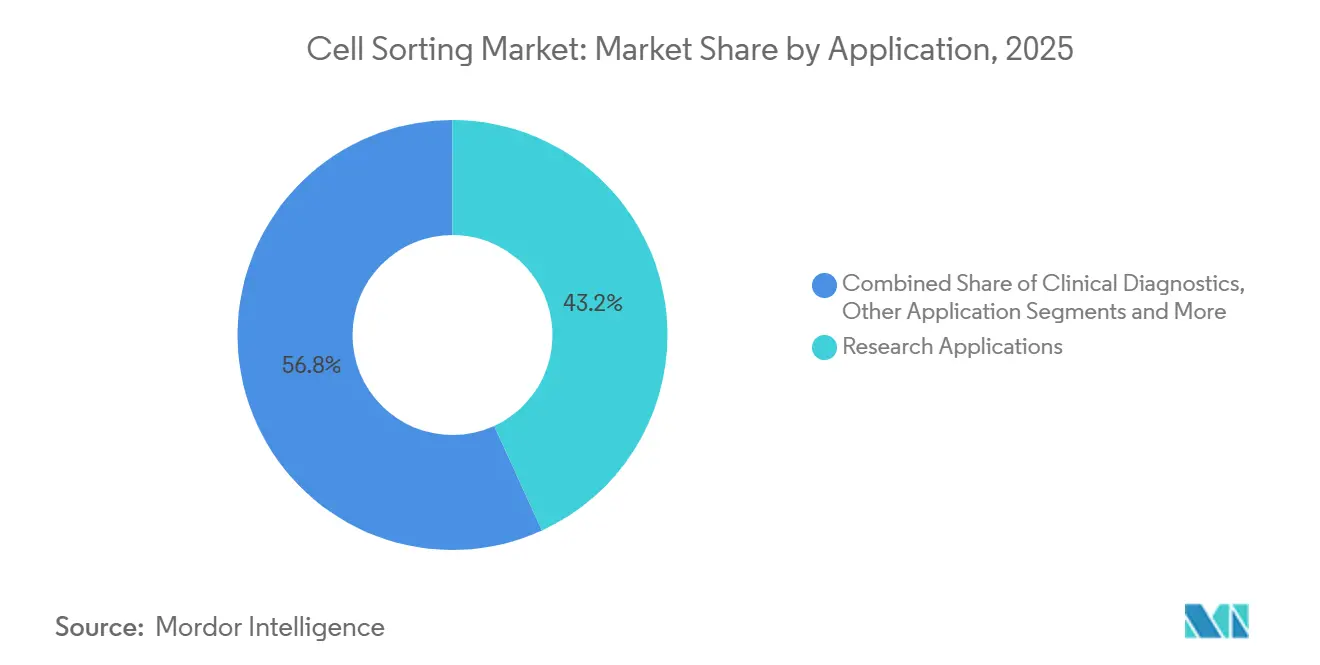

- By application, research retained 43.16% revenue share in 2025, yet cell and gene therapy manufacturing is poised to record an 11.73% CAGR to 2031.

- By cell type, mammalian cells dominated with 71.63% share of the cell sorting market size in 2025, while exosomes and extracellular vesicles are set to increase at a 10.32% CAGR through 2031.

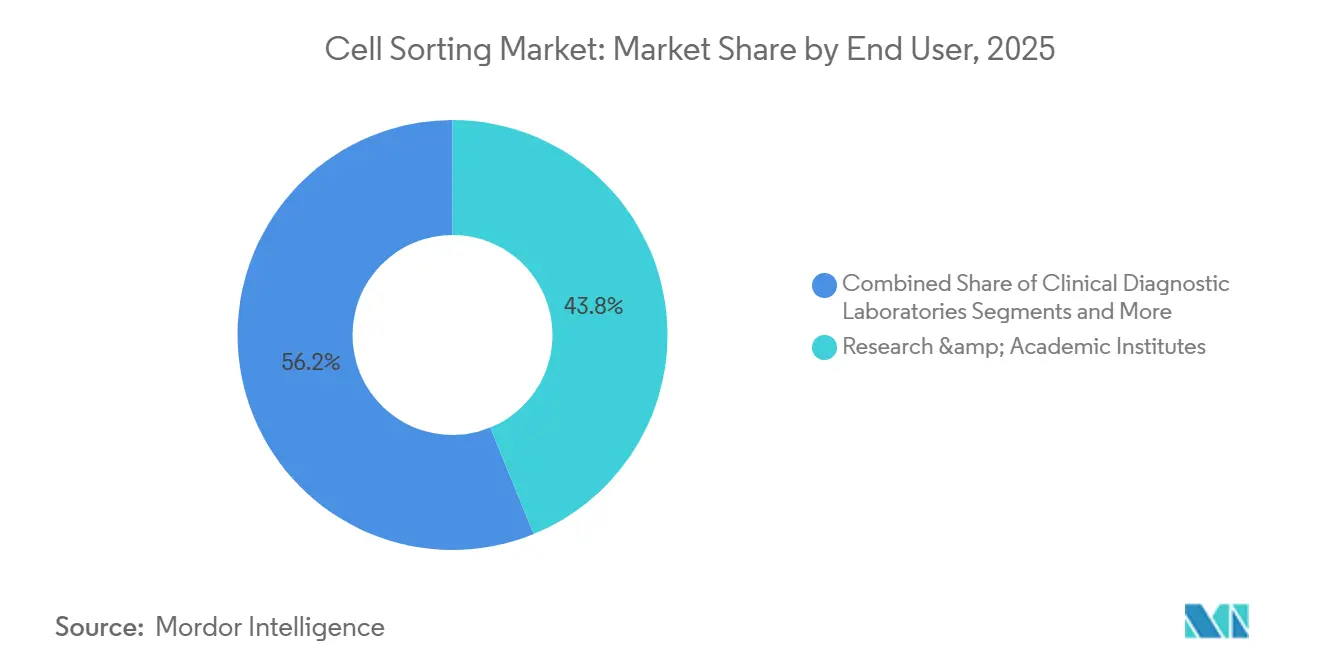

- By end user, research and academic institutes led with 43.83% of the cell sorting market share in 2025, but clinical diagnostic laboratories are projected to expand at a 10.52% CAGR during the same horizon.

- By geography, North America held 39.62% of revenue in 2025, whereas Asia-Pacific is forecast to achieve the fastest regional growth at a 9.89% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Cell Sorting Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growing prevalence of cancer, HIV, immune disorders | +1.4% | North America, Europe, emerging Asia | Medium term (2–4 years) |

| Expansion of pharmaceutical and biotech R&D pipelines | +1.6% | North America, Europe, China, Japan, South Korea | Long term (≥ 4 years) |

| Rapid instrument innovation (spectral, image-enabled) | +1.8% | Global, early adoption in North America and Europe | Short term (≤ 2 years) |

| Surge in single-cell multi-omics workflows | +1.2% | North America, Europe, spillover to Asia-Pacific | Medium term (2–4 years) |

| Image-enabled morphological gating unlocking new assays | +1.0% | North America, Europe, Japan | Medium term (2–4 years) |

| China-centric CGT trial boom | +1.3% | China with spillover to Southeast Asia | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Growing Prevalence of Cancer, HIV & Immune Disorders

More than 2 million new cancer cases projected for the United States in 2024 sustain multi-parameter isolation of tumor-infiltrating lymphocytes and circulating tumor cells.[1]American Cancer Society Staff, “Cancer Statistics,” American Cancer Society, cancer.org HIV monitoring still relies on flow-based CD4 enumeration across parts of sub-Saharan Africa and Southeast Asia, while autoimmune-disease studies require high-purity B-cell and regulatory T-cell fractions. Functional sorting for downstream omics increases throughput requirements, favoring spectral platforms that resolve overlapping fluorescence spectra without complex compensation. This disease burden underpins instrument refresh cycles and keeps core facilities operating near full capacity.

Expansion of Pharmaceutical & Biotech R&D Pipelines

Novartis reports that Kymriah production involves multiple enrichment steps to secure consistent CD4:CD8 ratios for every lot. Similar protocols underpin approved CAR-T products from Bristol Myers Squibb and Gilead. China authorized 13 CAR-T investigational new drug (IND) applications in 2024, compelling contract manufacturers to install redundant sorters. The enlarged pipeline positions the cell sorting market at the heart of commercial manufacturing schedules and quality-control documentation.

Rapid Instrument Innovation (Spectral, Image-Enabled Sorters)

Cytek’s Aurora CS enables full-spectrum unmixing with post-sort viabilities above 95%.[2]Cytek Biosciences Team, “Aurora CS Spectral Cell Sorter,” Cytek Biosciences, cytekbio.com BD’s FACSDiscover S8 integrates real-time imaging that distinguishes subcellular morphology for fragile induced pluripotent stem cells. Sony’s MA900 chips reduce sample waste by 60%.[3]Sony Biotechnology Team, “MA900 Multi-Application Cell Sorter,” Sony Biotechnology, sonybiotechnology.com These launches shorten assay-development timelines and render decade-old droplet instruments functionally obsolete, encouraging labs to accelerate replacement cycles.

Surge in Single-Cell Multi-Omics Workflows

10x Genomics notes that customers frequently use upstream sorting to enrich rare cell populations before sequencing, cutting per-cell costs. The Human Cell Atlas and pharma biomarker programs rely on high-purity inputs, creating a flywheel that sustains reagent demand and pushes instrument throughput limits. Every growth step in sequencing volume boosts the cell sorting market, widening its downstream influence.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High capital and maintenance costs | -0.9% | Global, especially emerging markets | Short term (≤ 2 years) |

| Shortage of highly skilled flow-cytometry operators | -0.7% | Acute in APAC and Middle East & Africa | Medium term (2–4 years) |

| Regulatory concern over shear-induced perturbations | -0.5% | North America, Europe | Long term (≥ 4 years) |

| Single-source component supply risks | -0.4% | Global, concentrated in Asian manufacturing hubs | Medium term (2–4 years) |

| Source: Mordor Intelligence | |||

High Capital & Maintenance Costs of Advanced Sorters

Entry-level benchtop units approach USD 200,000, while high-parameter spectral systems exceed USD 600,000. Annual service contracts add 12–15% to purchase price, and single-use cartridges can cost USD 50–150 per run. These expenses concentrate ownership within well-funded institutions and push small biotech firms toward contract services, postponing broad adoption of next-generation platforms.

Shortage of Highly Skilled Flow-Cytometry Operators

Only 30% of new PhD graduates receive formal cytometry training, leaving a gap as instruments gain complexity. Contract manufacturers require multiple certified operators per GMP suite, yet competition for talent drives wage inflation. Automation mitigates but does not eliminate regulatory requirements for human oversight, prolonging assay-transfer timelines and heightening quality-control risks.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Technology: Image-Enabled and Spectral Platforms Reconfigure Workflows

Fluorescence-based droplet systems retained 54.26% of cell sorting market share in 2025. The segment’s dominance stems from installed fleets of BD FACSAria and Sony SH800 units across academic cores. Yet the fastest growth now lies in image-enabled sorters, projected at 12.35% CAGR through 2031. Users adopt these platforms to separate circulating tumor cells from leukocytes using nuclear-to-cytoplasmic ratios that fluorescence alone cannot capture. Spectral detection, nested within the fluorescence category, enables 40-parameter panels that resolve autofluorescence in tumor biopsies. As a result, legacy filter-based systems face accelerated depreciation schedules. Magnetic-activated cell sorting remains the default for large-scale CD3 or CD34 enrichment in autologous therapies because of closed-system compliance, but its growth moderates as spectral platforms prove GMP-ready. Microfluidic and acoustic technologies hold niche but strategic value. NanoCellect’s WOLF G2 sorts fragile stem cells with 98% post-sort viability, appealing to regenerative medicine players. Bulldog Bio’s acoustic sorters offer label-free separation for organoid workflows. Collectively, these alternatives expand the cell sorting market by adding use cases once limited by shear stress or antibody costs.

Adoption trajectories vary by lab mission. Core facilities with high instrument utilization gravitate toward spectral upgrades because they can redeploy existing antibody inventories. Pharma manufacturing suites prioritize validated droplet systems for continuity but earmark capital budgets for image-enabled add-ons that document cell morphology. Emerging biotech startups, under cost pressure, favor microfluidic instruments that combine lower entry price with reduced consumable spend. Vendors now bundle AI-powered gating software, enabling novice operators to run 30-color panels with guided workflows, shrinking the skills gap. Over the forecast period, technology fragmentation will persist, but spectral and image-enabled platforms are poised to command premium pricing, nudging average selling prices upward and sustaining revenue growth in the cell sorting market.

By Product & Service: Services Outpace Hardware as GMP Outsourcing Surges

Reagents and consumables delivered 42.63% of 2025 revenue, underscoring the annuity-like nature of antibody and cartridge sales. Services will expand at 11.45% CAGR as CGT developers outsource GMP-compliant sorting. Instrument sales still matter because each GMP suite demands redundant units, yet budget cycles stretch when list prices break past USD 600,000. Thermo Fisher’s Attune CytPix integrates acoustic focusing and imaging, giving mid-tier labs a stepping stone into spectral territory.

Consumables break down into antibodies, magnetic beads, and single-use fluidic paths. BD Biosciences, BioLegend, and Miltenyi Biotec compete intensely on antibody panel breadth, while Miltenyi dominates magnetic bead workflows through its CliniMACS Prodigy system. Disposable microfluidic cartridges, though costlier per run, reduce cross-contamination risk, a critical selling point for contract manufacturers juggling multiple client campaigns. Service providers such as Lonza and Charles River offer turnkey cell sorting market solutions, including assay design, regulatory filing support, and chain-of-custody documentation. Their rise reallocates industry profit pools from hardware to expertise and positions high-touch services as the fastest revenue accelerator within the cell sorting industry.

By Application: CGT Manufacturing Drives Structural Demand Shift

Research occupied 43.16% demand in 2025 as cancer and stem-cell biology generated sample throughput. However, CGT manufacturing is tracking an 11.73% CAGR, poised to eclipse pure research spending by the decade’s end. Clinical diagnostics, especially leukemia minimal residual disease testing, follows closely with a 10.52% growth rate. Hospitals replace four-color analyzers with eight-color or spectral sorters to conform to European Hematology Association guidelines. Research adoption is stabilizing; grant budgets are flat and reviewers favor translational proposals that bridge benchtop insights to patient outcomes. The cell sorting market size for diagnostics benefits from standardized reimbursement codes that de-risk capital purchases for community labs, extending technology penetration beyond academic strongholds.

In CGT workflows, cell sorting is mission-critical. Each autologous CAR-T infusion requires multiple purification rounds under sterile, closed conditions, making sorter uptime a gatekeeper for patient scheduling. Process deviations trigger expensive batch failures, incentivizing redundant instrument arrays and premium service contracts. Regulatory filings increasingly include image-based documentation of sorted populations, strengthening the case for image-enabled platforms. In clinical diagnostics, throughput trumps parameter count, so mid-speed droplet instruments remain adequate, yet adoption of spectral panels accelerates as labs confront multiplex antibody shortages. Collectively, these trends reshape the application mix and elevate CGT to the anchor segment dictating technology road maps.

By Cell Type: Exosome Isolation Becomes a Strategic Frontier

Mammalian cells commanded 71.63% share in 2025, spanning T cells, B cells, natural killer cells, and induced pluripotent stem cells. Exosomes and extracellular vesicles will expand at 10.32% CAGR as liquid-biopsy assays and EV-mediated drug delivery platforms enter late-stage trials. Fluorescence-based immunocapture of CD63-positive vesicles now rivals ultracentrifugation in purity, improving quantitation of tumor-derived RNA cargo. T cells dominate volume because every CAR-T lot requires multiple enrichments. NK-cell programs from Fate Therapeutics and Nkarta rely on sorting to eliminate feeder cells and normalize activation markers. Stem-cell pipelines for spinal-cord injury and macular degeneration cannot tolerate droplet shear, pushing demand toward acoustic or microfluidic systems.

Exosome workflows introduce a new consumable category—affinity antibodies conjugated to magnetic nanobeads—opening cross-sell angles for vendors already supplying stem-cell and immune panels. Microbial sorting remains a niche, yet synthetic biology companies use high-speed dispensing to clone thousands of yeast variants each day, expanding market breadth. Over the forecast horizon, the interplay of mammalian dominance and exosome momentum will stabilize average selling prices and expand addressable applications, underpinning steady growth of the cell sorting market.

By End User: Clinical Labs Accelerate Adoption for MRD Testing

Research and academic institutes represented 43.83% of 2025 revenue, reflecting entrenched fleets and high utilization rates. However, clinical diagnostic laboratories will post a 10.52% CAGR as hematology departments deploy spectral sorters for acute myeloid leukemia minimal residual disease panels. Pharmaceutical and biotech companies maintain significant spend, yet split strategies. Large pharma builds internal GMP suites to secure timelines, while early-stage biotech relies on contract development and manufacturing organizations (CDMOs) for everything from protocol design to regulatory audits. CDMOs, in turn, are the fastest-growing buyer cohort, installing multiple redundant sorters to guarantee 100% uptime.

Core facilities at R1 universities face booking queues exceeding 90% utilization, forcing researchers to plan experiments months in advance. This congestion nudges institutions to invest in additional units or negotiate volume discounts with vendors. Clinical labs in Europe and North America benefit from updated reimbursement frameworks that justify capital investment in spectral analyzers. Collectively, shifting end user dynamics reinforce services and consumables as the cell sorting market’s growth flywheels.

Geography Analysis

North America, with 39.62% share in 2025, remains the cell sorting market’s revenue anchor. The FDA cleared six new cell and gene therapies in 2024, each requiring validated sorting documentation. Canada’s regenerative-medicine hubs in Toronto and Vancouver advance stem-cell applications, while Mexico’s vaccine developers integrate benchtop sorters into infectious-disease workflows. Asia-Pacific will record a 9.89% CAGR through 2031, propelled by China’s 13 CAR-T IND approvals in 2024 and the country’s push for localized sorter components. Japan leverages its conditional approval pathway to run iPSC trials for macular degeneration, requiring gentle acoustic sorters inside hospital clean rooms. India’s contract research organizations attract off-shore pharma screening campaigns, boosting reagent volumes.

Europe ranks second in regional revenue. Germany’s university hospitals host dense fleets of spectral sorters for tumor microenvironment studies. The United Kingdom pilots national minimal residual disease monitoring, potentially standardizing spectral flow across public hospitals. France emphasizes microbial cell sorting in infectious-disease research. EMA guidance on advanced therapy medicinal products places higher weight on process consistency, spurring automated sorter adoption. Southern European labs, constrained by public-sector budgets, enter shared-facility agreements to access high-parameter platforms, keeping unit sales steady.

Middle East & Africa and South America offer smaller bases but strategic upside. Gulf Cooperation Council states import high-end sorters to populate new biotech parks in Dubai and Riyadh, aiming to localize precision medicine. South Africa’s HIV programs keep legacy droplet units busy, but grant cycles limit upgrades. Brazil’s vaccine institutes demand benchtop sorters for yellow fever and dengue projects, while Argentina’s currency volatility delays capital expenditures, pushing users toward fee-for-service sorting. These regions collectively contribute modest volume but broaden the distribution footprint, offering vendors risk diversification and long-term growth optionality for the cell sorting market.

Competitive Landscape

The cell sorting industry has a moderate concentration profile. BD’s FACSDiscover S8 commands premium pricing through 40-parameter detection and automated quality control. Danaher’s CytoFLEX SRT addresses mid-throughput needs, and the corporation’s 2024 acquisition of Cytek signals a bet on spectral technology. Thermo Fisher captures mid-market users with the Attune CytPix, bundling acoustic focusing and imaging to differentiate from droplet incumbents. Smaller challengers include NanoCellect with microfluidic units, Bulldog Bio with acoustic sorting platforms, and Akadeum Life Sciences with microbubble depletion kits.

Strategic patterns diverge. Integrated suppliers bundle instruments, reagents, and service plans, creating lock-in for large pharma. Open-architecture vendors court core facilities seeking flexibility on antibody sourcing and software. Patent activity centers on AI-assisted gating; BD’s February 2024 patent covers real-time morphology-based classification. Disruptors target neglected niches such as organoid screening and exosome sorting, suggesting future competition will hinge on automation depth, AI workflows, and expansion into non-traditional sample types. This evolving mix maintains competitive tension and spurs continuous innovation in the cell sorting market.

Cell Sorting Industry Leaders

Becton, Dickinson and Company

Bio-Rad Laboratories, Inc.

Sony Biotechnology Inc.

Miltenyi Biotec GmbH

Danaher

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- September 2025: BD placed its 1,000th Rhapsody single-cell system at Addenbrooke’s Hospital, Cambridge, expanding multi-omics capacity.

- May 2025: BD launched the first cell analyzer combining spectral detection and real-time imaging for higher-throughput experiments.

- January 2025: SGS opened Germany’s first commercial FACS service for advanced therapy medicinal products using BD FACSAria Fusion instrumentation.

Global Cell Sorting Market Report Scope

As per the scope of the cell sorting market report, cell sorting is a technique employed for the separation of cells based on their intracellular and extracellular properties. The intracellular properties include properties such as DNA, RNA, and protein molecule interaction and extracellular properties consist of surface protein expression and morphology of the cell. The techniques of isolating and sorting different types of a cell have unlocked many applications in research and medicinal industry.

The cell sorting market is segmented by technology, product and service, application, cell type, end user and geography. By technology, market is segmented into Fluorescence-based Droplet, Spectral Flow, Image-Enabled, MACS, Microfluidic MEMS, Acoustic & Dielectrophoresis. By product and service, market is segmented into Instruments, Reagents & Consumables, Services. By Application, market is segmented into Research, Clinical Diagnostics, CGT Manufacturing. By Cell Type, market is sgemented into Mammalian, Microbial, Exosomes & EVs. By End User, market is segmented intoResearch & Academic, Pharma & Biotech, CDMOs, Clinical Labs. By Geography, market is segmented into North America, Europe, Asia-Pacific, MEA, South America. The market report also covers the estimated market sizes and trends for 17 different countries across major regions globally. The report offers the value (in USD) for the above segments.

| Fluorescence-based Droplet Cell Sorting |

| Spectral Flow Cell Sorting |

| Image-Enabled Cell Sorting |

| Magnetic-Activated Cell Sorting (MACS) |

| Microfluidic (MEMS) Cell Sorting |

| Acoustic & Dielectrophoresis-based Sorting |

| Instruments | Benchtop Sorters |

| High-Parameter / Spectral Sorters | |

| Microfluidic Single-Cell Dispensers | |

| Reagents & Consumables | Fluorochrome-Conjugated Antibodies |

| Magnetic Beads & Columns | |

| Disposable Microfluidic Cartridges | |

| Sorting Buffers & Kits | |

| Services | Cell Sorting Services |

| CGT Manufacturing Sorting Services |

| Research Applications | Cancer Research |

| Immunology & Inflammation | |

| Stem-Cell & Developmental Biology | |

| Microbiology & Environmental | |

| Clinical Diagnostics | HIV/CD4 Monitoring |

| Leukemia & Lymphoma Phenotyping | |

| Cell & Gene Therapy Manufacturing | |

| Other Applications |

| Mammalian Cells | T Cells |

| B Cells | |

| NK Cells | |

| Stem Cells (iPSC, MSC) | |

| Tumour / CTCs | |

| Microbial Cells (Bacteria, Yeast) | |

| Exosomes & Extracellular Vesicles |

| Research & Academic Institutes |

| Pharmaceutical & Biotechnology Companies |

| Contract Manufacturers / CDMOs |

| Clinical Diagnostic Laboratories |

| Other End Users (CROs, Core Facilities) |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| France | |

| United Kingdom | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| South Korea | |

| Australia | |

| Rest of Asia-Pacific | |

| Middle East & Africa | GCC |

| South Africa | |

| Rest of Middle East & Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Technology | Fluorescence-based Droplet Cell Sorting | |

| Spectral Flow Cell Sorting | ||

| Image-Enabled Cell Sorting | ||

| Magnetic-Activated Cell Sorting (MACS) | ||

| Microfluidic (MEMS) Cell Sorting | ||

| Acoustic & Dielectrophoresis-based Sorting | ||

| By Product & Service | Instruments | Benchtop Sorters |

| High-Parameter / Spectral Sorters | ||

| Microfluidic Single-Cell Dispensers | ||

| Reagents & Consumables | Fluorochrome-Conjugated Antibodies | |

| Magnetic Beads & Columns | ||

| Disposable Microfluidic Cartridges | ||

| Sorting Buffers & Kits | ||

| Services | Cell Sorting Services | |

| CGT Manufacturing Sorting Services | ||

| By Application | Research Applications | Cancer Research |

| Immunology & Inflammation | ||

| Stem-Cell & Developmental Biology | ||

| Microbiology & Environmental | ||

| Clinical Diagnostics | HIV/CD4 Monitoring | |

| Leukemia & Lymphoma Phenotyping | ||

| Cell & Gene Therapy Manufacturing | ||

| Other Applications | ||

| By Cell Type | Mammalian Cells | T Cells |

| B Cells | ||

| NK Cells | ||

| Stem Cells (iPSC, MSC) | ||

| Tumour / CTCs | ||

| Microbial Cells (Bacteria, Yeast) | ||

| Exosomes & Extracellular Vesicles | ||

| By End User | Research & Academic Institutes | |

| Pharmaceutical & Biotechnology Companies | ||

| Contract Manufacturers / CDMOs | ||

| Clinical Diagnostic Laboratories | ||

| Other End Users (CROs, Core Facilities) | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| France | ||

| United Kingdom | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| Middle East & Africa | GCC | |

| South Africa | ||

| Rest of Middle East & Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

What is the projected value of the cell sorting market in 2031?

The market is expected to reach USD 561.71 million by 2031.

Which segment will grow the fastest through 2031?

CGT manufacturing applications, with an 11.73% CAGR, lead growth.

How large is fluorescence-based droplet sorting within the market?

It represented 54.26% of cell sorting market share in 2025.

Why are services outpacing instrument sales?

Pharma and biotech firms outsource GMP-compliant sorting, driving an 11.45% CAGR for services.

Which regions present the highest growth rates?

Asia-Pacific leads with a projected 9.89% CAGR, driven by China’s CGT pipeline.

What is a primary barrier to wider adoption in smaller labs?

High instrument prices and maintenance contracts limit purchases among budget-constrained institutions.

Page last updated on: