Isopropyl Alcohol (IPA) Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 3.46 Billion |

| Market Size (2031) | USD 4.27 Billion |

| Growth Rate (2026 - 2031) | 4.28% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Isopropyl Alcohol (IPA) Market Analysis by Mordor Intelligence

The Isopropyl Alcohol Market size was valued at USD 3.32 billion in 2025 and estimated to grow from USD 3.46 billion in 2026 to reach USD 4.27 billion by 2031, at a CAGR of 4.28% during the forecast period (2026-2031). Moderate feedstock volatility, ongoing pharmaceutical capacity additions, and the transition toward ultra-high-purity grades together shape the growth trajectory of the Isopropyl Alcohol market. Strong propylene integration shields large producers from margin erosion, while specialty suppliers secure pricing premiums in electronic- and pharma-grade niches. Rapid expansion of semiconductor fabs in the United States, South Korea, and Taiwan creates a widening demand gap for 99.999% purity grades, reinforcing the strategic importance of domestic production hubs. Simultaneously, European green hydrogen initiatives deliver long-run cost and emissions advantages and establish a differentiated tier within the Isopropyl Alcohol market. Across all regions, sustained consumption in healthcare disinfection formulations and personal-care products underpins baseline volume, ensuring that the Isopropyl Alcohol market remains resilient despite cyclical swings in broader petrochemical demand.

Key Report Takeaways

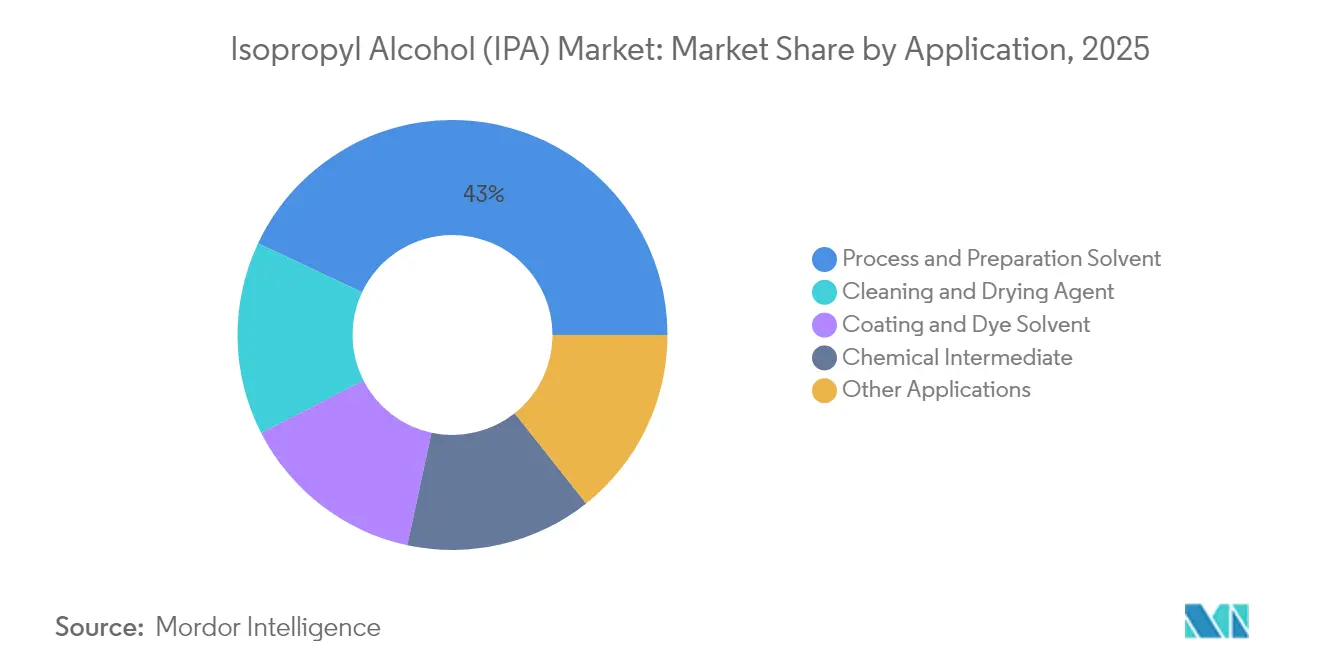

- By application, Process and Preparation Solvents commanded 42.98% of the Isopropyl Alcohol market share in 2025.

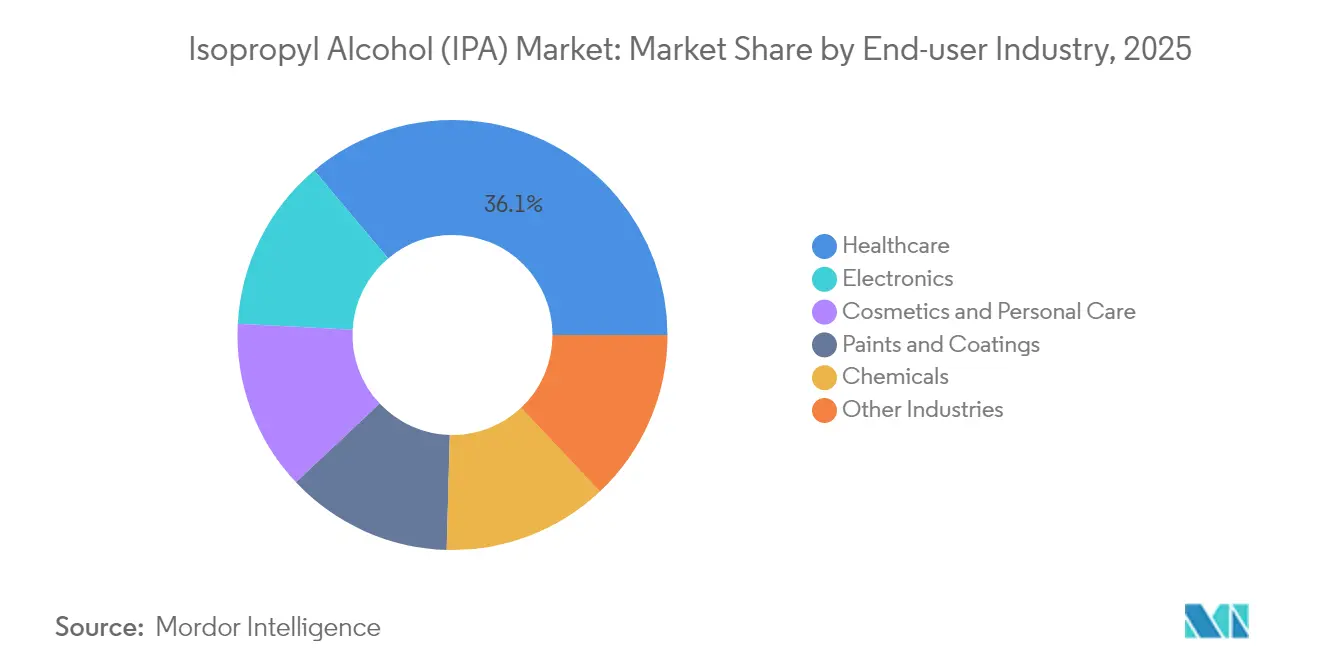

- By end-user industry, Healthcare captured 36.12% of the Isopropyl Alcohol market size in 2025 and is expanding at a 4.97% CAGR through 2031.

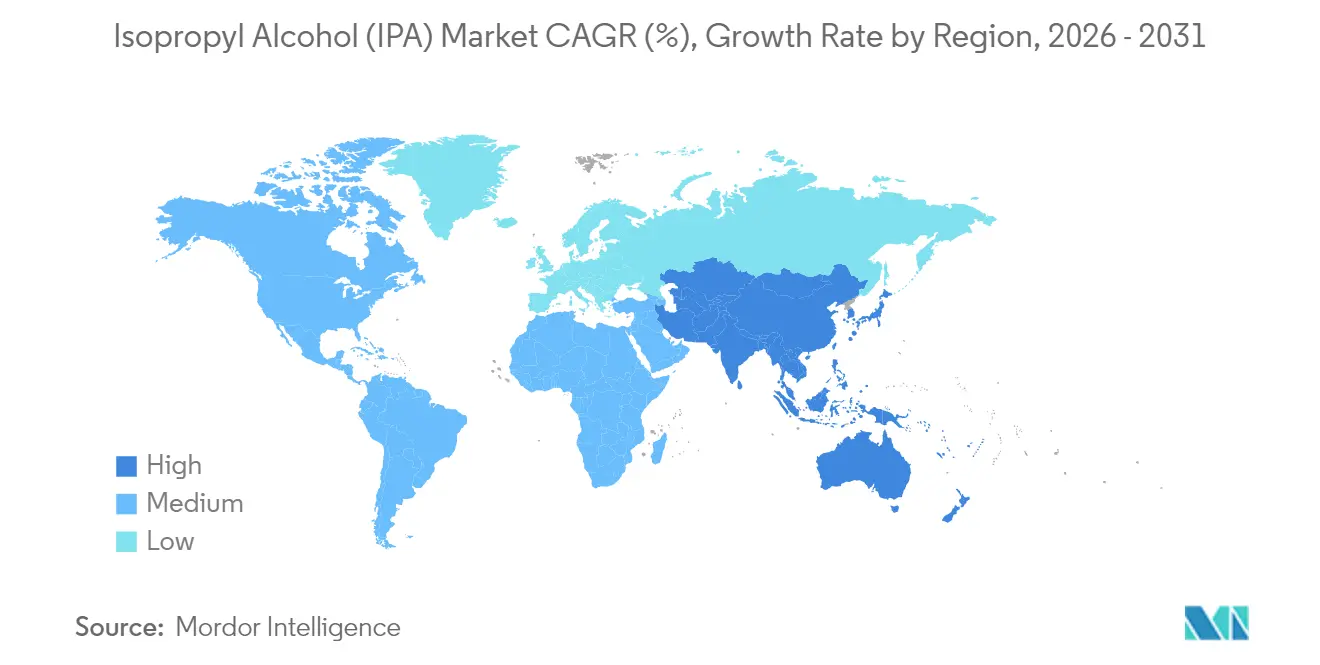

- By geography, Asia-Pacific held 42.10% of the Isopropyl Alcohol market share in 2025, while the region is forecast to post the fastest 5.22% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Isopropyl Alcohol (IPA) Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Surging Demand from Pharmaceutical API Production | +1.2% | North America, Europe, Asia-Pacific | Medium term (2-4 years) |

| Rising Usage in Healthcare Disinfection Products | +0.9% | Global | Short term (≤ 2 years) |

| Growing Consumption in Personal-care Formulations | +0.7% | Asia-Pacific with spill-over to North America | Medium term (2-4 years) |

| Demand for Electronic-grade IPA in Advanced Lithography | +1.1% | Asia-Pacific core, North America semiconductor corridors | Long term (≥ 4 years) |

| Cost Advantages from Green-hydrogen Direct Hydration Routes | +0.4% | Europe with expansion potential to North America | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Surging Demand from Pharmaceutical API Production

Pharmaceutical manufacturers rely on IPA for synthesis, purification, and crystallization steps because the solvent mixes readily with water and evaporates rapidly, minimizing contamination risks. Food and Drug Administration (FDA) cGMP (Good Manufacturing Practices) frameworks specify minimum purity and microbial standards that raise switching barriers and lock in long-term offtake contracts[1]U.S. Food & Drug Administration, “Current Good Manufacturing Practice,” fda.gov. Post-pandemic on-shoring of generic drug manufacturing in India and the United States elevates baseline consumption, while continuous manufacturing lines intensify solvent throughput requirements. Low price elasticity within the pharmaceutical segment shields volumes from short-term price hikes, reinforcing a stable core for the Isopropyl Alcohol market. Forward-looking operators certifying low-carbon or renewable IPA grades position themselves with ESG-focused pharma buyers for preferred-supplier status.

Rising Usage in Healthcare Disinfection Products

IPA-based disinfectants deliver broad-spectrum microbial efficacy at 70% aqueous concentration, achieving rapid kill times against enveloped viruses and bacteria without residue. Hospitals increasingly integrate automated dilution and dispensing systems that require bulk IPA deliveries with tight batch-to-batch consistency. Infection-control guidelines from the Centers for Disease Control and Prevention (CDC) and the World Health Organization continue to reference IPA, anchoring demand in routine cleaning workflows. Demand spikes observed in 2020–2022 have normalized but remain well above pre-pandemic baselines, creating a structurally larger slice of the Isopropyl Alcohol market. Suppliers who document pharmaceutical-grade manufacturing practices enjoy preferred status in tenders covering hand rubs, surface wipes, and instrument reprocessing fluids.

Growing Consumption in Personal-care Formulations

Asia-Pacific’s expanding middle class favors premium cosmetics where IPA is a fast-evaporating carrier for actives and fragrance oils. Consumption accelerates in toners, astringents, and nail lacquers that require clean, streak-free drying. Formulators also use IPA’s antimicrobial side benefit to bolster preservative systems, allowing reduced parabens and phenoxyethanol levels. Rising disposable incomes in China and India lift per-capita expenditure on personal-care products, broadening the consumer base and sustaining growth in the Isopropyl Alcohol market. Regulatory shifts nudging toward lower volatile organic compound (VOC) thresholds encourage innovation around low-odor IPA blends rather than outright solvent replacement, protecting the solvent’s share in beauty products.

Demand for Electronic-grade IPA in Advanced Lithography

Sub-5 nm semiconductor processes can lose entire wafer lots if trace metals exceed parts-per-billion thresholds. Ultra-high-purity IPA at 99.999% concentration removes particles and photoresist residues without watermark formation, making it irreplaceable during critical drying stages. ExxonMobil’s USD 100 million Baton Rouge expansion underscores the commercial pull of this niche, which commands up to 300% price premiums over commodity grades[2]ExxonMobil, “Baton Rouge IPA Expansion Press Release,” exxonmobil.com. Domestic supply chain security drives fab operators in the United States and Europe to diversify away from Asian solvent imports. The proliferation of AI and cloud data centers pushes chip output higher, ensuring sustained demand for electronic-grade IPA and anchoring a high-value tier within the broader Isopropyl Alcohol market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Volatile Propylene Feedstock Prices | -0.8% | North America & Europe | Short term (≤ 2 years) |

| Substitution by Less-flammable Solvents in Consumer Products | -0.5% | North America & EU | Medium term (2-4 years) |

| Capital Risk from Electro-chemical IPA Synthesis Technologies | -0.3% | Europe & North America | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Substitution by Less-flammable Solvents in Consumer Products

New safety protocols in consumer electronics and aerospace maintenance call for non-flammable alternatives to IPA, such as Honeywell’s Solstice and 3M’s Novec fluids. EU regulations on storage volumes for Class IB flammables restrict inventory at manufacturing sites, nudging formulators toward substitutes. Nonetheless, many low-GWP solvents carry higher costs and lower evaporation rates, preserving IPA’s foothold in cost-sensitive segments. Where substitution occurs, it concentrates in enclosed-equipment cleaning systems that recover and recycle solvent vapors, limiting net volume displacement. Still, the perceived hazard profile caps IPA penetration in certain consumer product categories, modestly curbing growth potential in the Isopropyl Alcohol market.

Volatile Propylene Feedstock Prices

Propylene accounts for up to 70% of variable production costs in conventional IPA plants. U.S. polymer-grade propylene is projected to breach 40 cents per pound by Q2 2025 after LyondellBasell’s Houston refinery shutdown removes 136,000 t of supply. This squeeze narrows margins for standalone IPA producers lacking cracker integration. In Europe, tight refinery margins limit propylene availability, forcing traders to import high-cost material from the Middle East. Asian producers suffer from periodic Propane Dehydrogenation (PDH) unit outages driven by negative cash margins. These swings compel buyers to diversify suppliers, but long-term contracts remain critical to assure supply, favoring vertically integrated petrochemical majors within the Isopropyl Alcohol market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Application: Process Dominance Drives Premium Positioning

Process and Preparation Solvents represented 42.98% of the Isopropyl Alcohol market share in 2025, generating the largest absolute revenue and registering a 4.88% CAGR through 2031. The segment benefits from the solvent’s dual polarity, which supports broad solubility profiles during pharmaceutical synthesis and specialty chemical reactions. Chemical engineers value rapid vaporization that eases downstream drying and limits thermal degradation. Cleaning and Drying Agents form the second-largest slice of the Isopropyl Alcohol market. Demand here converges with semiconductor roadmap milestones, where each node shrink tightens contamination thresholds and locks in higher solvent purity tiers. As fabs commercialize gate-all-around architectures, 99.999% IPA volumes scale rapidly, commanding margins triple those of commodity-grade solvent.

Coating and Dye Solvent applications hold smaller but stable demand, anchored in automotive refinish, industrial primers, and architectural emulsions. IPA’s compatibility with acrylic and nitrocellulose resins ensures adhesion and consistent film formation. Meanwhile, Chemical Intermediate usage tracks acetone production dynamics, providing a balancing outlet for by-product streams. Novel 3D printing post-processing and extraction technologies expand Other Applications, adding high-growth micro-niches that together lift demand elasticity. Across every use case, suppliers advertising renewable energy inputs differentiate themselves, capturing Environmental, Social, and Governance (ESG)-linked premiums that enhance revenue diversity in the Isopropyl Alcohol market.

By End-user Industry: Healthcare Leadership Sustains Growth Momentum

Healthcare held 36.12% of the Isopropyl Alcohol market size in 2025 and is projected to expand at a 4.97% CAGR thanks to elevated infection-control vigilance in hospitals, clinics, and long-term care facilities. IPA’s compatibility with medical plastics, stainless steel, and latex seals reinforces its use across disinfectant wipes, instrument rinses, and hard-surface cleaners. Electronics ranks as the second-largest consumer, moving in lockstep with wafer-fab build-outs in Texas, Arizona, and Dresden. Ultra-high-purity IPA ensures defect-free lithography, making it non-negotiable within fab chemical lists. Cosmetics and Personal Care continue to post high-single-digit growth in Asia, buoyed by rising disposable incomes and the popularity of fast-dry makeup products that depend on IPA for skin-feel optimization.

Paints and Coatings maintain mid-single-digit growth, supported by the recovery in construction activity and automotive output. Meanwhile, Chemicals absorb IPA for acetone and specialty solvent production, cycling with general industrial output. Diverse other industries, from automotive electronics cleaning to renewable-energy equipment assembly, diversify the consumption base and buffer cyclicality. The tiered quality structure across end-users—from commodity to electronic grade—allows suppliers to tailor portfolios and mitigate margin volatility, reinforcing strategic depth in the Isopropyl Alcohol market.

Geography Analysis

Asia-Pacific dominated the Isopropyl Alcohol market with a 42.10% share in 2025 and is forecast to grow at a 5.22% CAGR through 2031. China’s 22.87 million t propylene capacity pipeline underpins feedstock security, while India’s USD 142 billion petrochemical program accelerates backward integration into solvents. Regional electronics clusters in South Korea, Taiwan, and mainland China anchor demand for electronic-grade IPA, and local pharmaceutical producers tap domestic supply for API synthesis. Southeast Asian countries, notably Vietnam and Thailand, liberalize healthcare spending and expand personal-care manufacturing, further widening regional demand.

North America ranks as the second-largest region in the Isopropyl Alcohol market, benefiting from robust pharmaceutical output and a resurgent semiconductor build cycle driven by the United States CHIPS Act. ExxonMobil’s Baton Rouge debottlenecking project adds badly needed electronic-grade capacity, reducing dependency on Japanese imports. However, propylene price swings, influenced by refinery closures and PDH unit maintenance, inject cost volatility that can ripple into contract renegotiations. Canada’s clean-energy incentives stimulate interest in renewable hydrogen projects, potentially leading to the first North American green-route IPA plant before the decade ends.

Europe trails in volume but leads sustainability initiatives. CEPSA’s Andalusian plant, powered by solar-sourced green hydrogen, exemplifies the region’s push toward carbon-neutral solvents. Stringent REACH regulations and proposed PFAS restrictions encourage ongoing solvent reformulations, but IPA retains favored status in critical healthcare and pharma uses. Emerging adoption of low-carbon procurement clauses in public tenders aligns with renewable IPA offerings, protecting market share despite higher production costs.

South America and the Middle East & Africa collectively account for under 10% of global consumption today but register above-average growth. Brazil’s universal healthcare expansion lifts disinfectant demand, while Saudi Arabia’s integrated refinery-to-chemicals projects could create the first regional surplus of competitively priced IPA. Sub-Saharan Africa’s pharmaceutical localization policies, particularly in Nigeria and Kenya, gradually unlock solvent demand and stimulate smaller scale local production. The global trade matrix therefore becomes more complex as new production hubs emerge, but Asia maintains its primacy in both supply and demand within the Isopropyl Alcohol market.

Competitive Landscape

The Isopropyl Alcohol market is moderately fragmented. Integrated oil-to-chemicals giants such as ExxonMobil, Dow, Shell, and INEOS leverage captive propylene streams for cost leadership and enjoy logistics synergies across global footprints. Strategic investments skew toward purity and sustainability. ExxonMobil’s Baton Rouge upgrade introduces advanced ion-exchange polishing and gas-phase dehydration, pushing purity to the 99.999% threshold. Some North American independents explore bio-propane dehydrogenation to hedge carbon exposure, though commercialization remains distant. For now, integrated petrochemical complexes capture the bulk of value, but specialty niches tilt bargaining power toward purified-grade suppliers, shaping a two-tier hierarchy within the Isopropyl Alcohol market.

Isopropyl Alcohol (IPA) Industry Leaders

Dow

ExxonMobil Corporation

Shell plc

INEOS

LCY

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2025: ExxonMobil Corporation revealed plans to invest USD 100 million in its Baton Rouge, Louisiana, chemical plant. The upgrade aims to produce a pure form of isopropyl alcohol, a key ingredient for cleaning and processing microchips in the tech industry.

- June 2024: Cepsa (Moeve) commenced construction on Spain's inaugural isopropyl alcohol (IPA) plant. IPA finds its applications not just in hydroalcoholic gels, but also in both household and industrial cleaning products. Situated in Palos de la Frontera (Huelva), this new IPA plant comes with a backing of a EUR 75 million (USD 80.25 million) investment.

Global Isopropyl Alcohol (IPA) Market Report Scope

Isopropyl alcohol (IPA), or isopropanol, 2-propanol, propane-2-ol, etc., is a colorless liquid with a sharp, musty odor. It is commonly found in rubbing alcohol, hand sanitizers, cosmetics, perfumes, pharmaceutical products, and cleaning products. It is also widely used as a process and preparation solvent, cleaning and drying agent, coating and dye solvent, and intermediate for various chemical formulations.

The isopropyl alcohol market is segmented by application, end-user industry, and geography. The market is segmented by application into process and preparation solvent, cleaning and drying agent, coating and dye solvent, intermediate, and other applications. In the end-user industry, the market is segmented into cosmetics and personal care, healthcare, electronics, paints and coatings, chemicals, and other end-user industries. The report also covers the market size and forecast for the isopropyl alcohol (IPA) market in 27 countries across major regions. The market size and forecasts were made for each segment based on volume (tons) and revenue (USD million).

| Process and Preparation Solvent |

| Cleaning and Drying Agent |

| Coating and Dye Solvent |

| Chemical Intermediate |

| Other Applications |

| Healthcare |

| Cosmetics and Personal Care |

| Electronics |

| Paints and Coatings |

| Chemicals |

| Other Industries |

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| Malaysia | |

| Thailand | |

| Indonesia | |

| Vietnam | |

| Rest of Asia-Pacific | |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Nordic Countries | |

| Turkey | |

| Russia | |

| Rest of Europe | |

| South America | Brazil |

| Argentina | |

| Colombia | |

| Rest of South America | |

| Middle East and Africa | Saudi Arabia |

| United Arab Emirates | |

| Qatar | |

| South Africa | |

| Nigeria | |

| Egypt | |

| Rest of Middle East and Africa |

| By Application | Process and Preparation Solvent | |

| Cleaning and Drying Agent | ||

| Coating and Dye Solvent | ||

| Chemical Intermediate | ||

| Other Applications | ||

| By End-user Industry | Healthcare | |

| Cosmetics and Personal Care | ||

| Electronics | ||

| Paints and Coatings | ||

| Chemicals | ||

| Other Industries | ||

| By Geography | Asia-Pacific | China |

| India | ||

| Japan | ||

| South Korea | ||

| Malaysia | ||

| Thailand | ||

| Indonesia | ||

| Vietnam | ||

| Rest of Asia-Pacific | ||

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Nordic Countries | ||

| Turkey | ||

| Russia | ||

| Rest of Europe | ||

| South America | Brazil | |

| Argentina | ||

| Colombia | ||

| Rest of South America | ||

| Middle East and Africa | Saudi Arabia | |

| United Arab Emirates | ||

| Qatar | ||

| South Africa | ||

| Nigeria | ||

| Egypt | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

What purity grades are most in demand for the Isopropyl Alcohol market?

Commodity 99.9% grades satisfy bulk solvent needs, but 99.999% ultra-high-purity grades are growing fastest due to sub-5 nm semiconductor manufacturing and command up to 300% price premiums.

How will green hydrogen impact future IPA production costs?

Plants integrating renewable hydrogen and solar power can cut scope 1 and 2 emissions and may achieve cost parity where carbon pricing exceeds USD 50 per t, positioning them for ESG-linked procurement advantages.

Which region is projected to add the largest new IPA capacity by 2031?

Asia-Pacific, led by China’s 22.87 million t propylene build-out and India’s USD 142 billion petrochemical pipeline, is expected to contribute the bulk of new capacity.

What is driving healthcare demand for IPA post-pandemic?

Ongoing infection-control protocols, automated dispensing systems, and regulatory backing from bodies like the CDC keep hospital and clinic consumption above pre-2020 levels.

Are alternative solvents expected to displace IPA in electronics cleaning?

Some non-flammable fluorinated solvents gain share in enclosed systems, but high cost and slower evaporation limit broad replacement, leaving IPA essential for most wafer-cleaning steps.

What is the current market size of Isopropyl Alcohol Market?

The Isopropyl Alcohol Market size is estimated at USD 3.46 billion in 2026, and is expected to reach USD 4.27 billion by 2031.

Page last updated on: