Amniocentesis Needle Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

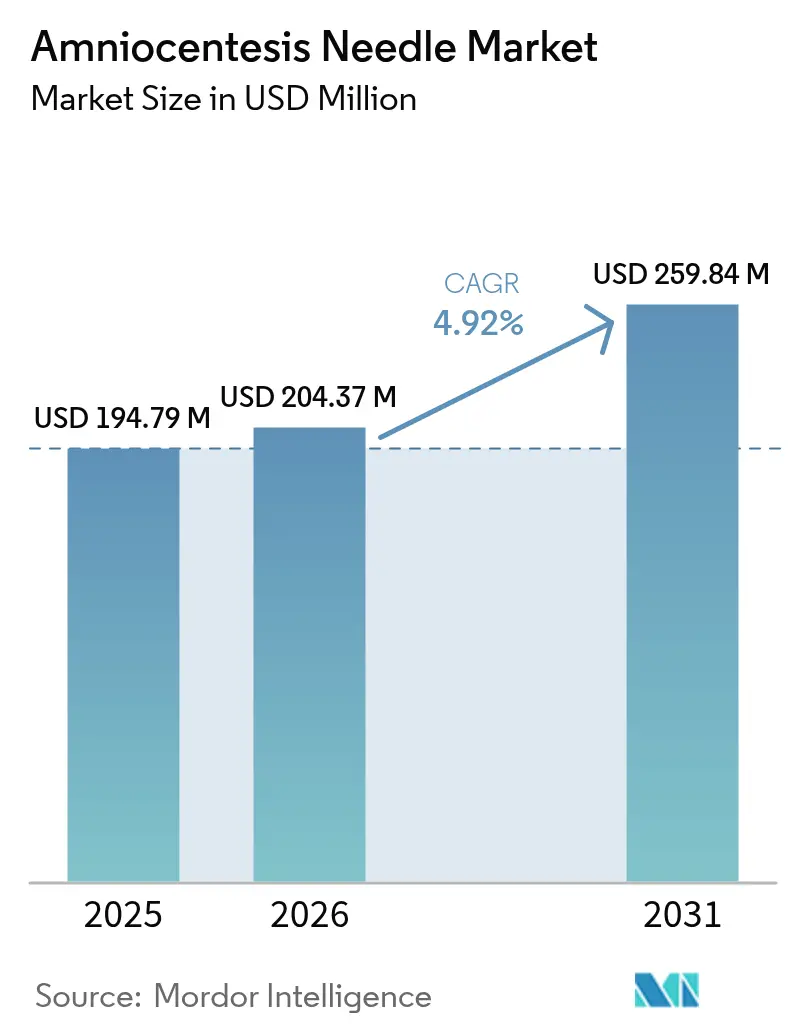

| Market Size (2026) | USD 204.37 Million |

| Market Size (2031) | USD 259.84 Million |

| Growth Rate (2026 - 2031) | 4.92% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

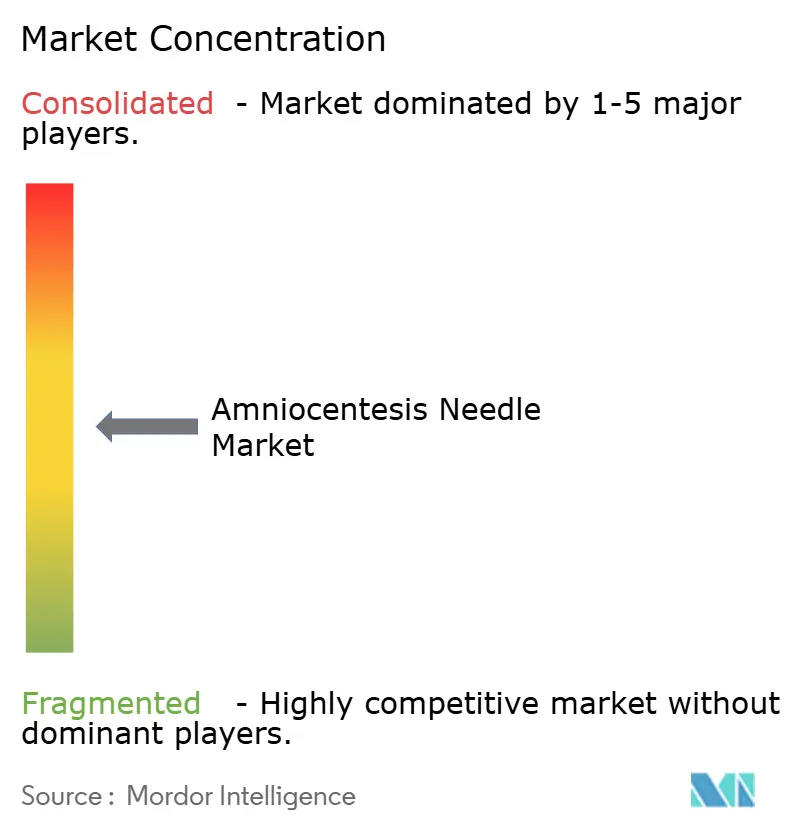

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Amniocentesis Needle Market Analysis by Mordor Intelligence

The amniocentesis needle market size is expected to grow from USD 194.79 million in 2025 to USD 204.37 million in 2026 and is forecast to reach USD 259.84 million by 2031 at 4.92% CAGR over 2026-2031. A steady yet deliberate expansion reflects the device’s indispensable role in amniocentesis, cordocentesis and fetal blood transfusion—procedures that still command definitive diagnostic accuracy despite the meteoric rise of non-invasive prenatal tests. Demand concentrates in high–risk pregnancies, where clinicians insist on highest-precision instrumentation to safeguard maternal and fetal outcomes. Uptake of premium products with enhanced ultrasound visibility and built-in safety stops is rising in tandem with population-level shifts toward older motherhood, greater use of assisted reproduction and widening prenatal screening mandates. While new reimbursement policies fuel procedure migration to outpatient settings, long-term growth remains anchored to hospitals and tertiary centers that can support complex fetal interventions.

Key Report Takeaways

- By needle length, the 100 – 150 mm category led with 53.48% of the amniocentesis needle market share in 2025; lengths above 150 mm are projected to grow at a 5.07% CAGR between 2026 – 2031.

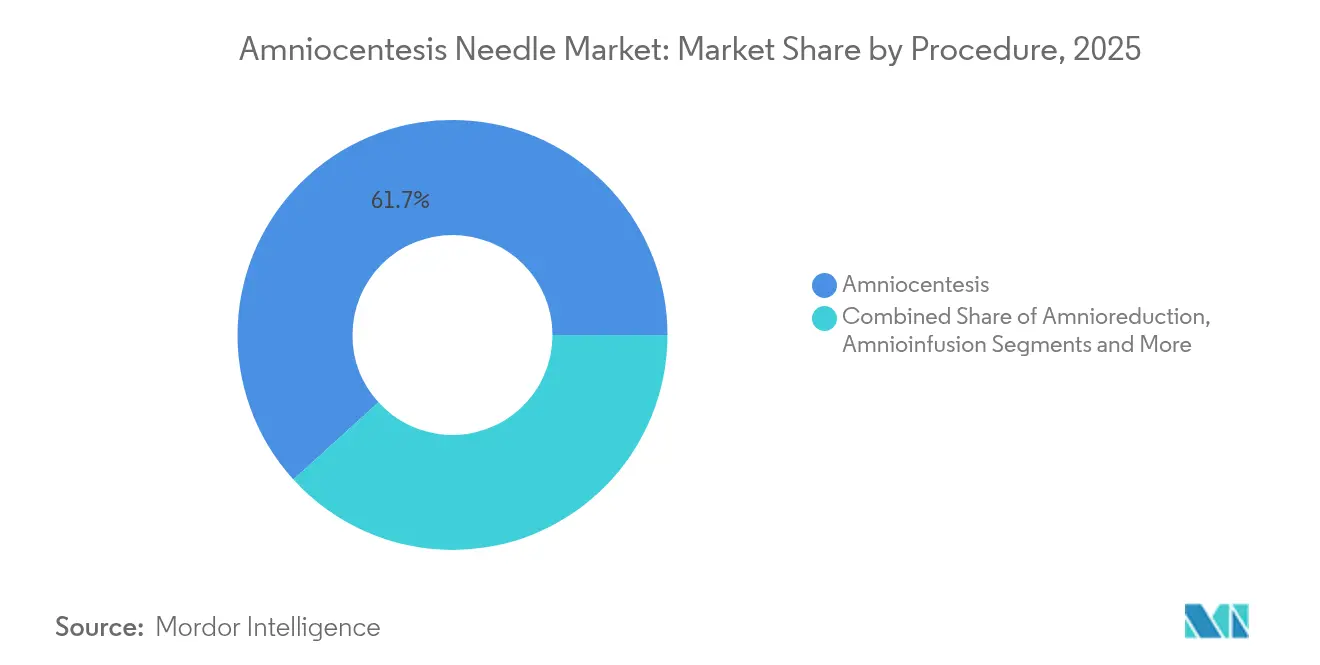

- By procedure, amniocentesis accounted for 61.74% revenue share in 2025, whereas cordocentesis is set to expand at a 5.78% CAGR through 2031.

- By end user, hospitals held 56.66% of the amniocentesis needle market size in 2025, while ambulatory surgical centers represent the fastest-growing care setting.

- By region, North America commanded 36.95% revenue in 2025; Asia-Pacific is forecast to post the quickest 6.44% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Amniocentesis Needle Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising Burden Of Genetic And Chromosomal Disorders | +1.2% | Global, with higher impact in developed regions | Long term (≥ 4 years) |

| Growing Maternal Age And Associated Pregnancy Risks | +1.5% | North America & EU, expanding to APAC | Medium term (2-4 years) |

| Growth In IVF-Related Multiple Pregnancies | +0.8% | Global, concentrated in urban centers | Medium term (2-4 years) |

| Rising Awareness And Government Support For Prenatal Genetic Testing And Screening Programs | +0.7% | APAC core, spill-over to MEA | Long term (≥ 4 years) |

| AI-Guided Ultrasound Improving Puncture Accuracy | +0.6% | North America & EU, early adoption in select APAC markets | Short term (≤ 2 years) |

| Availability Of Technological Advanced And Product Variety | +0.4% | Global | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rising Burden of Genetic and Chromosomal Disorders

Chromosomal abnormalities affect 0.6% of live births worldwide, with trisomy 21 incidence climbing sharply beyond maternal age 35.[1]Line Elmerdahl Frederiksen, “Maternal Age and the Risk of Fetal Aneuploidy: A Nationwide Cohort Study,” Acta Obstetricia et Gynecologica Scandinavica, obgyn.onlinelibrary.wiley.com As national screening programs cast a wider net, confirmatory invasive tests remain the clinical gold standard, keeping the amniocentesis needle market firmly embedded in prenatal pathways. Genetic counselors routinely underscore that screening cannot replace diagnostic certainty, sustaining demand for high-precision needles that reduce repeat insertions and procedure-related anxiety.

Growing Maternal Age and Associated Pregnancy Risks

In 2025, pregnancies in women ≥ 40 years carry a trisomy 21 risk of 1 in 98, versus 1 in 1,095 at age 29. This demographic reality, driven by career priorities and socioeconomic shifts, anchors a steady pool of patients for whom invasive diagnostics remain recommended irrespective of initial NIPT results. Device makers therefore continue to prioritize ergonomic hubs and echogenic tips that improve single-pass success in diverse maternal anatomies.

Growth in IVF-Related Multiple Pregnancies

IVF triples the twin-pregnancy rate, multiplying procedure complexity because non-invasive screens show higher false-positive rates in multiples.[2]Antenatal Results and Choices, “Prenatal Genetic Testing and Multiple Pregnancies,” arc-uk.org Multiple sacs often force steeper insertion angles and longer reach, steering customers toward the premium end of the amniocentesis needle market that provides superior ultrasound contrast and depth markings.

AI-Guided Ultrasound Improving Puncture Accuracy

Clinical pilots reveal that real-time AI overlay shortens puncture time and reduces redirections, encouraging hospitals to refresh inventories with needles optimized for enhanced echogenicity. Early adopters in the United States and Western Europe are already bundling AI-enabled scanners with proprietary needle kits, strengthening the market’s technology pull.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rapid Uptake Of CFDNA Screening | -1.8% | Global, particularly in developed markets | Short term (≤ 2 years) |

| Shortage Of Fetomaternal Medicine Specialists | -0.9% | North America & EU, emerging in APAC | Medium term (2-4 years) |

| Litigation Risk In Invasive Procedures | -0.6% | North America, expanding globally | Long term (≥ 4 years) |

| Supply Pinch In Surgical-Grade Stainless Steel | -0.3% | Global manufacturing hubs | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Rapid Uptake of cfDNA Screening

Professional-society endorsements have cut invasive diagnostic testing volumes by 44% within two years of NIPT rollout.[3]Sebastian Larion, “Changes in Prenatal Testing Trends After Introduction of Noninvasive Prenatal Testing,” Obstetrics & Gynecology, journals.lww.com With 98.6% of low-risk women declining invasive confirmation when cfDNA is negative, base-procedure volumes retreat even as remaining interventions skew toward higher-risk pregnancies that demand premium needles.

Shortage of Fetomaternal Medicine Specialists

OB-GYN workforce shortages have created maternity deserts where access to specialized invasive care is scarce, particularly in rural North America. Even when equipment is available, a lack of certified operators can delay or prevent procedures, tempering the growth trajectory of the amniocentesis needle market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Needle Length: Versatile Mid-Range Leads Yet Longer Formats Accelerate

The 100 – 150 mm class captured 53.48% of the amniocentesis needle market share in 2025, a position earned through its adaptability across routine amniocentesis and cordocentesis. User feedback highlights easier handling, consistent ultrasound visibility and lower maternal-discomfort scores, solidifying loyalty among high-volume obstetric units. Longer needles above 150 mm, however, are outpacing the category at a 5.07% CAGR as rising maternal BMI and late-gestation interventions demand deeper uterine reach. Needle innovators now coat shafts with micro-etching and embed stylets that lock once the amniotic cavity or umbilical vein is entered, minimizing the risk of over-penetration. Many hospitals adopt mixed-length trays so clinicians can select the optimal device per patient, a practice that expands overall procurement volume and underpins the amniocentesis needle market size for the segment.

Clinicians also report higher first-pass success when echogenic tip geometry is mated precisely to real-time AI visualization algorithms. Vendors, therefore, pair needle length with proprietary software presets, encouraging facilities to standardize on a single brand ecosystem. As software upgrades roll out over the air, customers feel compelled to refresh inventories to ensure maximum compatibility—an aftermarket dynamic that further supports the amniocentesis needle market.

By Procedure: Amniocentesis Dominates While Cordocentesis Gains Momentum

Amniocentesis procedures contributed 61.74% to 2025 revenue, cementing their role as the workhorse of fetal genetic diagnosis. The segment benefits from entrenched clinical guidelines, time-tested risk profiles and broad gestational windows, all of which assure predictable annual order volumes. Cordocentesis, though smaller, is poised for a 5.78% CAGR as practitioners broaden fetal therapy offerings, particularly intrauterine transfusions in red-cell alloimmunization. Hospitals investing in advanced doppler ultrasonography often refresh needle inventories simultaneously, which lifts the amniocentesis needle market size tied to cordocentesis kits.

Research showing safe amniocentesis beyond 24 weeks—once considered late for invasive sampling—adds new indications and prolongs the viable window for diagnosis. Likewise, AI-assisted trajectory mapping is shrinking total needle time inside the uterus, encouraging physicians previously hesitant about cordocentesis to adopt the procedure. As therapeutic and diagnostic lines blur, product managers increasingly market “dual-purpose” needles with interchangeable stylets, driving procurement synergies for facilities under budget scrutiny.

By End User: Hospitals Still Command but Outpatient Sites Rise

Hospitals retained 56.66% of 2025 revenue by leveraging 24/7 imaging, anesthesia backup and rapid neonatal care. High-risk referrals, emergency blood transfusions and complex multiple-sac pregnancies keep tertiary centers at the heart of the amniocentesis needle market. Nonetheless, outpatient specialty clinics are winning share owing to patient preference for shorter wait times and bundled prenatal packages; ambulatory surgical centers are meanwhile capitalizing on reimbursement parity for several invasive prenatal codes.

Value-based payment reforms reward lower complication rates, favoring facilities that deploy the latest echogenic-coated needles and AI-guided ultrasound to minimize needle passes. In turn, vendors bundle staff training modules and tele-mentoring, enabling mid-volume centers to safely perform more procedures. Over the forecast period, these shifts could redistribute demand without eroding overall amniocentesis needle market size, given persistent high-risk caseloads.

Geography Analysis

North America’s 36.95% revenue share in 2025 stems from universal insurance coverage of high-risk diagnostics and broad acceptance of prenatal genetics. The 2025 removal of prior authorization for cfDNA by a leading private payer streamlines testing pathways, yet does not eliminate the need for invasive confirmation in abnormal cases, keeping hospitals on a predictable purchasing cycle. Rural maternity deserts remain a concern, but tele-ultrasound partnerships push expertise into smaller units, indirectly bolstering equipment sales across the amniocentesis needle market.

Asia-Pacific is forecast to grow at 6.44% CAGR through 2031, propelled by urbanization, fertility-treatment uptake and delayed parenthood. Nations such as Japan and South Korea now document advanced-maternal-age pregnancy rates rivaling Western peers. Government-funded newborn-disorder initiatives align with this shift, enabling multi-year procurement contracts for fetal medicine devices. Local contract manufacturers have begun to supply stainless-steel cannulae, trimming cost layers and widening adoption of premium-coated needles.

Europe enjoys uniform prenatal guidelines and public-funded screening programs that guarantee baseline demand. Regional focus on cost containment, however, nudges providers toward outpatient settings—an evolution mirroring the United States. Harmonized Medical Device Regulation certification has lengthened market-entry timelines but also reassures clinicians of product safety, encouraging them to upgrade to AI-compatible devices over older stock. Consequently, refresh cycles for the amniocentesis needle market remain synchronized with ultrasound capital refresh programs.

Regulatory Landscape

In the United States, amniocentesis trays and related samplers that include needles are regulated by the FDA under 21 CFR 884.1550 as Class I devices subject to general controls and, under specified conditions, are generally exempt from 510(k) premarket notification. Even with a lighter premarket pathway, manufacturers still need to meet baseline compliance expectations, including establishment registration and device listing, and to operate within quality system and labeling requirements for sterile, single-use obstetrical diagnostic devices.

In Europe, access and ongoing compliance are shaped by the EU Medical Device Regulation (MDR), which has increased conformity assessment, technical documentation, and post-market obligations relative to legacy directives. On December 16, 2025, the European Commission published COM(2025) 1023 final, a legislative proposal to amend MDR and IVDR to reduce administrative burden, with adoption targeted in late 2026 to early 2027 pending negotiations. Across markets, technical standards such as ISO 80369-7:2021 for small-bore connectors and related needle and tubing standards remain a key design and interoperability anchor for amniocentesis needle kits used with syringes and accessory components.

Value Chain Analysis

The value chain starts with raw materials and components, led by medical-grade stainless steel cannula and stylet inputs and polymer hubs (commonly polycarbonate), followed by precision manufacturing steps such as tube drawing, forming, bevel grinding, and echogenic enhancement via laser marking or etching. Final assembly and sterile packaging convert these parts into single-use amniocentesis needles or complete trays (needle with stylet, syringe, and collection accessories) that meet clinical handling and ultrasound-visibility requirements.

Downstream, distribution is handled through direct hospital tenders and group purchasing routes, supported by regional distributor networks serving obstetrics and gynecology departments, and manufacturer-direct ordering platforms. Quality and compliance activities cut across the chain, including traceability, sterility assurance, and documentation aligned to major regulatory regimes (for example, FDA Class I general controls in the United States and MDR documentation expectations in Europe). Supply risk concentrates around consistent availability of surgical-grade stainless steel tubing and specialist machining and marking capabilities needed to deliver tight tolerances and reproducible echogenic performance.

Competitive Landscape

The amniocentesis needle market shows moderate concentration. Each fields broad portfolios, from mid-range 22-gauge needles to extra-long 20-gauge variants, fortified by global service networks and hospital contracts. New entrants face formidable regulatory and clinical-validation hurdles, yet selected regional firms are climbing the value chain by offering private-label production for Western OEMs.

Competition is shifting toward software-hardware convergence. Patents filed in 2024–25 spotlight algorithms that enhance needle echogenicity and lock onto cannula trajectories in real time. Larger players ink exclusivity deals with AI ultrasound start-ups, embedding proprietary visualization codes into their disposables. Meanwhile, stainless-steel supply constraints triggered by global alloy shortages incentivize OEMs to diversify material sources, prompting joint ventures with metal-tubing specialists in Southeast Asia.

Marketing strategies increasingly highlight total-cost-of-ownership. Firms bundle needles with ultrasound presets, puncture-practice simulators and cloud-based audit dashboards that document needle path accuracy for credentialing purposes. This integrated-solution pitch resonates with risk-averse hospitals seeking to mitigate litigation exposure, thus reinforcing lock-in and padding average selling prices across the amniocentesis needle market.

Amniocentesis Needle Industry Leaders

-

Cook Medical Incorporated

-

RI.MOS. srl

-

BD

-

CooperSurgical

-

Smiths Medical

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

Product differentiation around ultrasound visibility and procedure safety remains a clear whitespace, especially as providers adopt AI-guided ultrasound overlays that reward higher echogenic contrast and consistent shaft calibration. Suppliers are therefore pairing needle design changes (tip geometry, micro-etching, depth markings, and safety stops) with standardized kits used in hospitals and outpatient settings, which supports higher-value procurement relative to commodity needles.

On market access, the United States regulatory framework offers a comparatively accessible on-ramp for compliant new offerings because amniotic fluid samplers and trays are Class I under 21 CFR 884.1550 and are generally exempt from 510(k) under applicable conditions. This shifts competitive focus toward manufacturing quality, sterility assurance, and distribution reach rather than lengthy premarket submissions. In Europe, the European Commission proposal published on December 16, 2025 (COM(2025) 1023 final) to reduce MDR and IVDR administrative burden creates a visible policy pathway that manufacturers are monitoring while keeping MDR-grade technical documentation and post-market readiness. Vendors that can sustain that documentation load while expanding kit and training support are positioned to compete for higher-complexity provider accounts.

Recent Industry Developments

- April 2026: RI.MOS. announced its participation in ExpoSalud 2026 in Chile, positioning its Made in Italy disposable portfolio for obstetrics and gynecology in front of regional buyers. The communication highlighted export-facing commercialization activity rather than a single product update, reinforcing competitive pressure on pricing and distribution in Latin America. For amniocentesis needle suppliers, this type of channel-building supports broader tender access and distributor relationships in emerging procurement markets.

- May 2025: The Thalassemia and Sickle Cell Society partnered with Fernandez Hospital to launch carrier-screening-linked prenatal diagnosis in Hyderabad. Linking screening to confirmatory prenatal diagnosis strengthens clinical pathways where invasive sampling remains necessary after a positive or high-risk screen. Over time, structured programs like this tend to concentrate demand in equipped centers that standardize procedure kits and consumables.

- March 2024: MIT researchers reported amniotic-fluid organoid culture work that enables fetal-stage disease modeling using amniotic fluid rather than direct fetal contact. This broadens the perceived downstream utility of amniotic fluid beyond karyotyping, supporting continued clinical and research interest in high-quality sample acquisition. The development also highlights the importance of reliable, contamination-minimizing collection tools in advanced diagnostic workflows.

Research Methodology Framework and Report Scope

Market Definition and Coverage

This market covers revenues from amniocentesis needles used in ultrasound guided procedures to collect amniotic fluid for prenatal diagnostic or therapeutic purposes, across hospitals, specialty clinics, and ambulatory surgical centers.

Scope exclusions: The sizing excludes needles primarily designed and sold for chorionic villus sampling and general biopsy uses.

Segmentation Overview

-

By Needle Length

- < 100 mm

- 100 – 150 mm

- > 150 mm

-

By Procedure

- Amniocentesis

- Amnioreduction

- Fetal Blood Transfusion

- Amnioinfusion

- Cordocentesis

-

By End User

- Hospitals

- Specialty Clinics

- Ambulatory Surgical Centers

-

By Geography

-

North America

- United States

- Canada

- Mexico

-

Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Rest of Europe

-

Asia-Pacific

- China

- Japan

- India

- Australia

- South Korea

- Rest of Asia-Pacific

-

Middle East and Africa

- GCC

- South Africa

- Rest of Middle East and Africa

-

South America

- Brazil

- Argentina

- Rest of South America

-

North America

Data Sources, Market Sizing, and Validation

Desk Research

Desk research started by mapping the clinical context and the demand pool, then aligning it with the device scope that is being priced and shipped. We relied on public sources to ground the model, including national health statistics on births and maternal age, disease surveillance and pregnancy risk indicators from the CDC and WHO, and method guidance and clinical practice documents from ACOG.

We also reviewed peer reviewed obstetrics and fetal medicine journals to track how amniocentesis usage is shifting versus non invasive prenatal testing, and to understand procedure timing patterns by gestational week. Supporting checks were added using import-export trade classifications where available, regulatory and recall databases for device signals, and company filings and investor decks for product and regional commentary. Select paid subscriptions were used only for company financials, news screening, and patent lookups. The sources listed here are illustrative, and many other public references were used for data collection, validation, and clarification.

Primary Interviews and Surveys

Primary interviews focused on validating procedure volumes, typical replacement behavior, and price bands by geography, because these details often do not appear cleanly in public tables. We spoke with clinicians involved in fetal medicine, procurement and sterile supplies teams, and distribution side contacts, with coverage balanced across APAC, EMEA, and the Americas to reduce single region bias.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 37% | CXOs: 17% | APAC: 45% |

| Mid tier: 43% | Functional/Unit leaders: 38% | EMEA: 31% |

| Smaller Players: 20% | Managers: 45% | Americas: 24% |

Market-Sizing & Forecasting

The core build uses a top down demand pool approach where pregnancy volumes and the share of pregnancies routed to invasive prenatal diagnosis are translated into expected amniocentesis procedures. Those procedure totals are then converted into needle demand and value using region specific pricing.

To keep the model realistic, we cross checked the top down results through selective bottom up approximations, including sampled price lists and channel checks, and then adjusted when the two views disagreed.

Key inputs in this market include total births and the maternal age mix, high risk pregnancy indicators, the amniocentesis rate per 1,000 pregnancies, average needles used per procedure (including re attempts in complex cases), and regional price dispersion driven by procurement practices and distribution margins. Forecasting uses scenario based trend projection supported by exponential smoothing on procedure intensity, since adoption changes are gradual and influenced by clinical guidelines and substitution from non invasive testing. Where country level procedure data is sparse, gaps are handled by proxying from comparable health system peers, then revalidated in interviews before finalizing the run.

Data Validation & Update Cycle

Outputs are triangulated against independent signals, such as procedure volume discussions in journals, birth and maternal age trends, and any visible device supply disruptions from public safety notices. Outliers are flagged early, assumptions are rechecked, and we apply a second analyst review so the final numbers are not tied to one person's judgment.

The study is refreshed each year, and interim updates are triggered when a material event changes procedure patterns or pricing. Examples in scope include guideline changes, reimbursement shifts, and major supply constraints. Before delivery, we do a fresh pass on key inputs like exchange rates, inflation effects on device pricing, and the latest pregnancy and screening statistics.

Mordor Intelligence's Amniocentesis Needle Market Size Compared With Other Published Estimates

Published market values for amniocentesis needles can vary even when the product name sounds the same. The included procedures, pricing layers, and base year choices are often not consistent across sources.

In this study, the main differences typically come from whether adjacent invasive prenatal needles are bundled into the same bucket, whether prices reflect hospital purchase levels or fully loaded channel prices, and how quickly procedure volumes are assumed to change as non invasive prenatal testing expands. Another common driver is refresh cadence. In smaller medical device markets, procedure and procurement timing can shift when one region changes guideline usage, and those changes do not get captured evenly, which is why the scope and validation choices applied by Mordor Intelligence matter.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 204.37 M (2026) | |

| Global Research Publisher A | USD 170.50 M (2024) | Uses an earlier base year and appears to size a broader set of invasive fetal procedures in some sections, which can shift the implied needle count per pregnancy and dampen near term value when converted to a single needle category. |

| Industry Research Publisher B | USD 174.40 M (2025) | States a 2025 base value with limited visible scope notes, so differences can come from pricing level (manufacturer level versus channel price), currency timing, and how quickly procedure substitution from non invasive screening is modeled. |

Taken together, the spread is mainly explained by base year selection, what is counted as an eligible procedure for an amniocentesis needle, and whether pricing is captured at a hospital purchase level or at a distribution included level. By tying the totals back to births, high risk pregnancy share, procedure intensity, and region specific price checks, the final number stays traceable and repeatable even when public data is uneven.

Key Questions Answered in the Report

What is the current value of the amniocentesis needle market?

The market is valued at USD 204.37 million in 2026 and is projected to reach USD 259.84 million by 2031.

Why do invasive procedures persist despite non-invasive prenatal tests?

CfDNA screening identifies risk, but definitive diagnosis often still requires amniotic-fluid or fetal-blood sampling for karyotyping, sustaining demand for high-precision needles.

Which needle length is most popular with clinicians?

Devices measuring 100 – 150 mm account for 53.48% of revenue because they balance reach with control across varied maternal anatomies.

Which region is expanding fastest in this market?

Asia-Pacific is forecast to grow at 6.44% CAGR through 2031 thanks to delayed parenthood, IVF uptake and improving healthcare infrastructure.

How is AI influencing product design?

AI-guided ultrasound overlays demand needles with higher echogenic contrast and consistent shaft calibration, pushing manufacturers to integrate software and hardware for one-pass accuracy.

Page last updated on: