Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

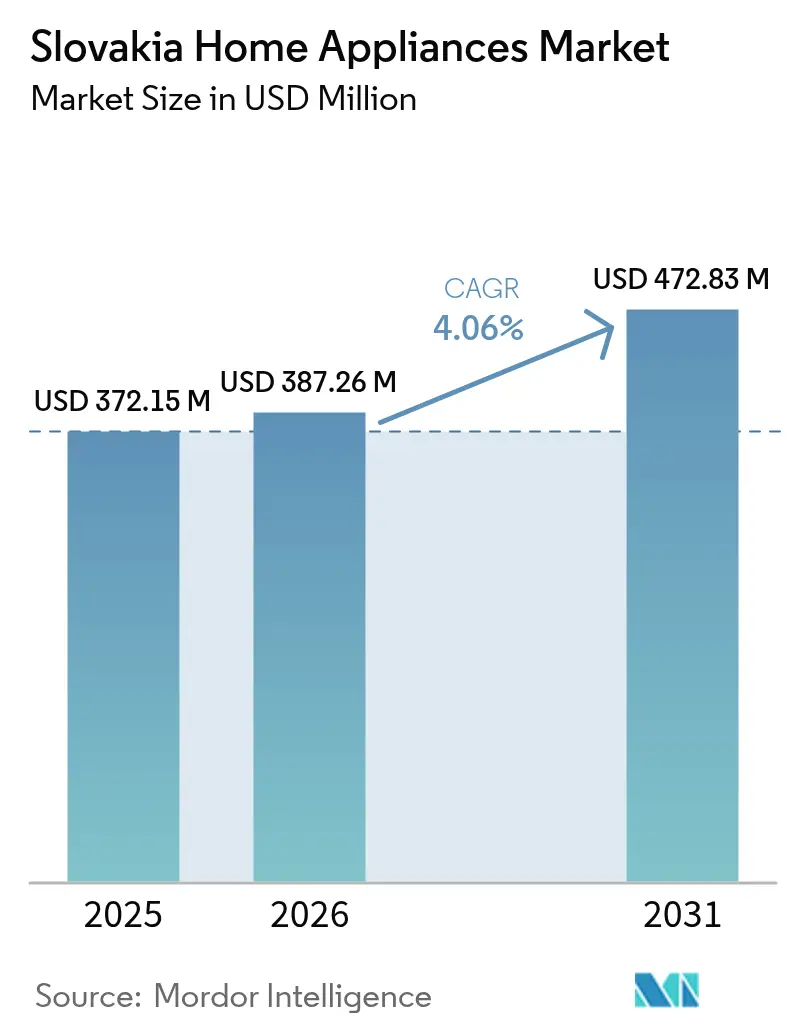

| Base Year Market Size (2025) | USD 372.15 Million |

| Market Size (2026) | USD 387.26 Million |

| Market Size (2031) | USD 472.83 Million |

| Growth Rate (2026 - 2031) | 4.06% CAGR |

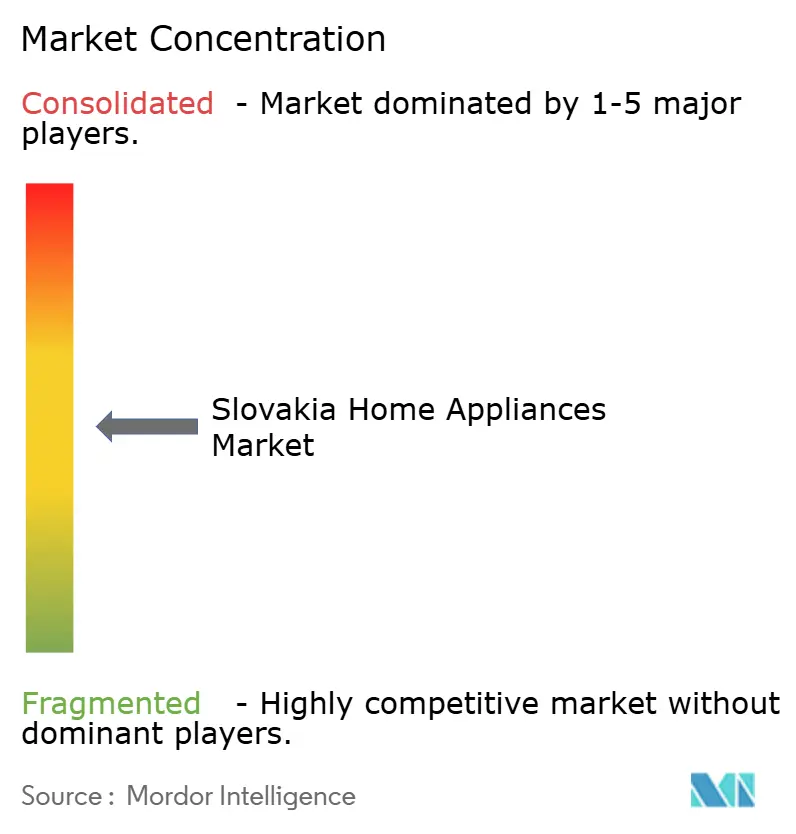

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Slovakia Home Appliances Market Analysis by Mordor Intelligence

The Slovakia home appliances market size in 2026 is estimated at USD 387.26 million, growing from 2025 value of USD 372.15 million with 2031 projections showing USD 472.83 million, growing at 4.06% CAGR over 2026-2031. Moderate inflation easing to 4.2% in early 2025 and real wage growth of 2.6% in 2024 have broadened household budgets, allowing consumers to replace aging equipment with energy-efficient models. EU-wide efficiency rules, a sturdy digital infrastructure, and government subsidy vouchers worth more than EUR 47 million are further directing demand toward A-class products and connected devices. Simultaneously, global suppliers are learning to price around a 23% VAT rate that took effect in January 2025 while balancing volatile component costs tied to lingering supply-chain disruptions.

Key Report Takeaways

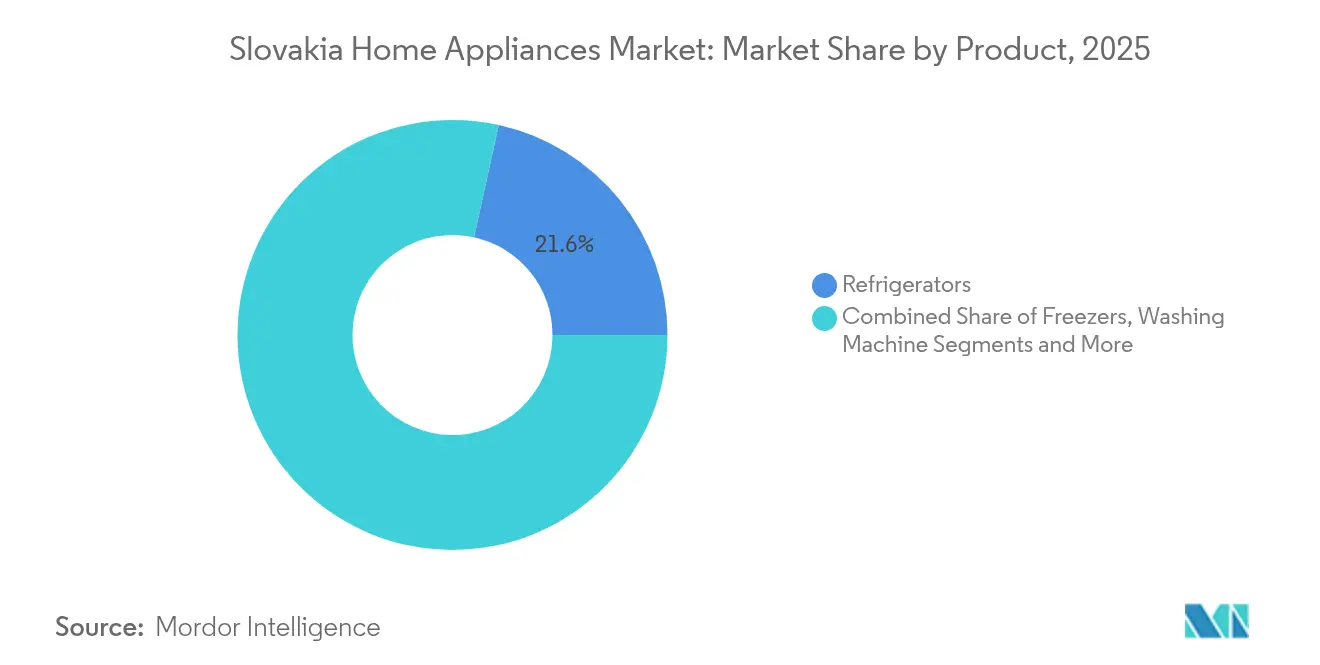

- By product category, refrigerators led with 21.55% of the Slovakia home appliances market share in 2025; air fryers are projected to expand at a 10.02% CAGR to 2031.

- By distribution channel, multi-brand stores held 42.20% of the Slovakia home appliances market in 2025, whereas online sales are set to climb at 9.28% CAGR through 2031.

- By geography, Western Slovakia commanded 37.65% revenue share of the Slovakia home appliances market in 2025; Eastern Slovakia is expected to post the fastest 5.95% CAGR between 2026 and 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Slovakia Home Appliances Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising disposable income & premiumisation | +1.2% | National, strongest in Bratislava & Western regions | Medium term (2–4 years) |

| EU energy-efficiency regulations | +0.9% | National, linked to EU-wide policy | Long term (≥4 years) |

| Expansion of online & retail ecosystems | +0.8% | National, urban focus | Short term (≤2 years) |

| Growing demand for smart connected devices | +0.7% | Western & Central, gradually moving eastward | Medium term (2–4 years) |

| Replacement and home-renovation uptick | +0.6% | National, higher in Western Slovakia | Medium term (2–4 years) |

| Source: Mordor Intelligence | |||

Rising Disposable Income & Premiumisation Trend

Disposable income reached EUR 19.44 billion in Q1 2025, reinforcing the appeal of higher-spec appliances that promise lower running costs over a longer lifecycle. Parallel convergence toward EU consumption norms now places Slovak household expenditure at 77% of the EU average, compared with far lower levels a decade ago[1]OECD, “Regional Economic Disparities in Slovakia 2024,” oecd.org. As unemployment stabilises near 5.3%, vendors offering energy-saving or design-oriented models see stronger volume growth, particularly in Bratislava and its commuter belt, where purchasing power is highest. Manufacturers are responding by broadening mid-to-premium portfolios in refrigeration, laundry, and built-in cooking. Voucher-funded upgrades through the “Zelená domácnostiam” programme reinforce the premium shift as households seize subsidies to offset upfront prices.

EU Energy-Efficiency Regulations Accelerating Replacement Cycle

Revised EU energy labels triggered a jump in A-rated market penetration across core appliance lines, compressing the payback period on replacements and anchoring predictable demand for the next decade. Slovakia’s Act No. 321/2014 obliges routine energy audits for large businesses, moving institutional buyers toward best-in-class equipment[2]International Energy Agency, “Slovakia: Energy Policies Review 2024,” iea.org. With renewable energy targeted at 25% of generation by 2030, households increasingly view efficient appliances as a means to maximise solar and heat-pump investments. The national subsidy cap of 90% on qualifying units accelerates scrappage of pre-label appliances, smoothing market visibility for OEMs through 2030.

Expansion of Online & Retail Ecosystems

More than half of Slovaks now buy goods online, and the furniture-and-appliances category alone registered USD 213 million in 2024 internet sales[3]U.S. Department of Commerce, “Slovakia eCommerce Market Guide 2024,” trade.gov. Leading platforms such as Alza.sk secured USD 412.6 million revenue in 2024 by marrying next-day delivery with extended warranty bundles, convincing consumers to purchase large-ticket white goods digitally. Pure-play channels have, in turn, forced chain retailers such as DATART to launch click-and-collect counters, keeping store traffic relevant for product demos. With median mobile download speeds above 60 Mbps, smartphone-led shopping is routine in the capital and spreading into regional cities. The combination of high internet penetration and competitive fulfilment costs positions e-commerce as the fastest contributor to Slovakia's home appliances market revenue over the next two years.

Growing Demand for Smart and Connected Home Devices

Interoperability breakthroughs such as the Matter 1.4 protocol are resolving earlier brand-lock concerns, encouraging households to view refrigerators, washers, and HVAC units as integrated energy nodes rather than stand-alone machines. Leveraging fixed broadband speeds around 90 Mbps, vendors now embed Wi-Fi modules even in mid-price models, allowing users to schedule cycles during off-peak tariffs or monitor consumption in real time. Adoption remains highest in Western Slovakia, yet demand is gradually filtering eastward as component prices normalise and utility bills incentivise precise load management. Local appliance assemblers already deploy industrial AI for predictive maintenance, shortening the learning curve for household acceptance. Collectively, these shifts inject a technology premium into average selling prices and lift value growth ahead of volume gains for the Slovakia home appliances market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Persistent inflation & VAT-led price jumps | -0.8% | National, stronger in Eastern Slovakia | Short term (≤2 years) |

| Global supply-chain volatility | -0.6% | National, across all channels | Medium term (2–4 years) |

| Growing second-hand & refurbished channels | -0.4% | Urban centres nationwide | Long term (≥4 years) |

| Source: Mordor Intelligence | |||

Persistent Inflation Pressuring Household Budgets

Although headline inflation fell from 15% in early 2023, the new 23% VAT rate that began in 2025 makes large-ticket goods visibly dearer. Eastern Slovakia, with unemployment above 10%, sees the sharpest demand pull-back as families prioritise essentials over premium white goods. Low savings buffers—Slovak households average EUR 21,000 in financial assets, the EU’s second-lowest—reinforce cautious spending. Budget models, therefore, gain share even as A-class penetration rises, causing a short-term mix shift that suppresses average revenue per unit across the Slovakia home appliances market.

Global Supply-Chain Volatility Raising Lead-Times & Costs

Smart appliance launches depend on stable semiconductor flows, yet chip capacity remains stretched as automotive, telecoms, and consumer-electronics buyers compete for the same wafers. Energy-intensive manufacturing also contends with price swings in imported gas, a legacy of the war in Ukraine. BSH Hausgeräte reported a 7% turnover drop in 2023 as material and freight costs spiked, illustrating how even scale players endure squeezed margins. Longer lead times push retailers to carry extra stock, raising working-capital needs and ultimately shelf prices.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product: Air Fryers Drive Small Appliance Revolution

Air fryers are forecast to grow at 10.02% CAGR to 2031, outpacing every other small appliance category as households experiment with oil-free cooking that suits compact kitchens of the Slovakia home appliances market. Refrigerators, while mature, continue to anchor 21.55% of 2025 revenue thanks to mandatory efficiency upgrades under EU labelling. Major brands are refreshing fridge portfolios with inverter compressors and recyclable insulation panels, capturing subsidy-eligible sales in both Western and Eastern Slovakia. Washing machines tap into rising urban apartment stock, with leading producers adding steam-refresh cycles that reduce water use, a feature favoured by subsidy guidelines. Dishwasher and oven demand rise steadily as Slovaks adopt Western consumption patterns in meal preparation and cleanup. The Slovakia home appliances market size for air fryers will therefore post the most pronounced growth, whereas refrigerators will reach the highest absolute value. Health-oriented design is spreading to blenders, coffee makers, and food processors, strengthening cross-selling opportunities in the countertop segment. Large appliances now integrate Wi-Fi modules for remote diagnostics, positioning vendors ahead of repairs-as-a-service regulations expected after 2026. Government vouchers covering up to 90% of eligible energy-efficient units are accelerating turnover of ageing refrigerators, washing machines, and dishwashers, thereby enlarging the Slovakia home appliances market size across premium-leaning categories.

By Distribution Channel: Online Growth Reshapes Retail Dynamics

Multi-brand stores retained a 42.20% slice of the Slovakia home appliances market in 2025 by offering side-by-side comparisons and same-day carry-out, features prized for bulky goods. The Slovakia home appliances market size for online sales is on course to expand at 9.28% CAGR amid 91.8% internet penetration and an advanced parcel-locker network. Alza.sk leverages predictive analytics to optimise next-day routes, boosting repeat purchases in categories such as vacuum cleaners and countertop ovens. Omnichannel hybrids are emerging: pure-play sites now run pop-up experience zones where consumers can test dishwashers or induction hobs before ordering online. Traditional retailers are introducing same-day click-and-collect to protect footfall. Online platforms also experiment with subscription bundles that spread appliance costs over 36 months, an approach that alleviates inflation worries and keeps the Slovakia home appliances market on an upward trajectory.

Geography Analysis

Western Slovakia dominates sales through higher incomes, a vibrant expatriate community, and property-led renovation cycles. The region’s proximity to Vienna and Brno exposes shoppers to cutting-edge smart refrigerators and washer-dryers that integrate with energy dashboards, reinforcing a habit of early adoption. Second-home ownership around the Small Carpathians further drives duplicate purchases of basic appliances for weekend lodges.Central Slovakia blends industrial employment with a price-sensitive consumer psyche, creating strong mid-segment churn in laundry and cooking. As regional cities like Žilina reinforce logistics corridors, appliance makers utilise the area as a distribution backbone, ensuring two-day reach to most population centres.Eastern Slovakia benefits from EU-funded insulation schemes that require A-label replacements, funnelling subsidies toward refrigerators, heat-pump dryers, and induction cookers. Rising connectivity brings e-commerce access to rural households, while new automotive campuses near Košice lift disposable wages. These overlapping forces position the region as the prime volume growth pocket for the wider Slovakia home appliances market.

Regulatory Landscape

Slovakia's home appliances regulatory framework is closely aligned with EU rules on product safety, ecodesign, and energy labeling. Act No. 83/2025 Z. z. on general product safety supports the EU General Product Safety Regulation (EU) 2023/988 and applies from December 13, 2024. It tightens obligations for placing non-food consumer products on the market and reinforces recall and traceability expectations across retail and e-commerce channels.

Market surveillance and compliance oversight sit mainly with the Ministry of Economy of the Slovak Republic, while the Slovak Trade Inspection (Slovenska obchodna inspekcia) enforces point-of-sale requirements such as energy label display and broader consumer-product compliance. Technical standardization and conformity assessment are coordinated by the Office for Standards, Metrology and Testing of the Slovak Republic, and Government Regulation 148/2016 Z. z. governs technical safety requirements for electrical equipment within specified voltage limits. Energy efficiency policy linkages also run through Act No. 321/2014 Z. z. on Energy Efficiency (consolidated as of 1 August 2024), which shapes procurement and institutional buying behavior through energy-efficiency related requirements.

Value Chain Analysis

The Slovakia home appliances value chain combines import-led brand portfolios with regional manufacturing and component production integrated into Central European industrial corridors. Upstream inputs include compressors, electronic control systems, motors, steel enclosures, and plastics. The supply mix relies on cross-border sourcing, for example control systems from Germany and steel enclosures from Poland, alongside Asian-sourced components such as compressors.

Midstream activities include assembly (historically including Whirlpool's production presence in Poprad) and quality or compliance processes tied to EU-harmonized standards. Downstream distribution is shaped by multi-brand retailers and fast-growing online platforms, supported by parcel-locker density and next-day delivery models in major cities. Industry coordination and advocacy are supported by APPLiA Slovakia, which represents manufacturers in discussions on regulation and standard-setting, while retailers increasingly add take-back and recycling services that affect brand selection, merchandising, and aftersales commitments.

Competitive Landscape

Competition remains moderately fragmented. European incumbents—BSH, Electrolux, and Whirlpool—share shelves with South Korean challengers Samsung and LG, while Hisense and Midea use aggressive pricing and fast feature rollouts to win first-time smart buyers. BSH generated EUR 15.3 billion global turnover in 2024, allocating 5.5% to R&D that prioritises AI-enabled diagnostics and recyclable materials. Whirlpool is scaling induction hob capacity in Poland to shorten freight lanes to Slovak warehouses, shaving lead-times by two weeks.

Retail-centric partnerships are critical. LG and Samsung have negotiated extended-term exclusivity slots on Alza.sk’s landing pages during peak campaigns, leveraging high click-through rates for flagship refrigerator launches. DATART’s in-store ‘eco-corner’ awards floor space to any brand offering take-back and recycling commitments, a move BSH and Electrolux embraced early to consolidate premium mindshare.

Refurbishment upstarts such as Back Market are slicing into mid-segment volumes by certifying second-hand washers and refrigerators, pushing incumbents to pilot factory-grade remanufacturing lines within Slovakia. Smart-device interoperability remains the new battleground: Siemens, Bosch, and LG already ensure Matter 1.4 compatibility, while Whirlpool plans firmware upgrades by 2026. Taken together, innovation pace and channel agility will decide share shifts within the Slovakia home appliances market.

Slovakia Home Appliances Industry Leaders

Hisense Group Co., Ltd.

Electrolux AB

BSH Hausgeräte GmbH

Whirlpool Corporation

Samsung Electronics Co., Ltd.

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

Regulatory-driven replacement and premium mix upgrades create whitespace for manufacturers and retailers that can operationalize compliance, labeling clarity, and energy-led merchandising at scale. Slovakia's alignment with EU ecodesign and energy labeling rules, reinforced by national energy-efficiency policy under Act No. 321/2014 Z. z., supports assortment strategies centered on high-efficiency models and clearer in-store and online product information. In 2025, specific inflection points include new mandatory EU energy-label requirements from June 20, 2025 (covering tumble dryers, alongside other labeled product groups) and updated ecodesign requirements for local space heaters from July 1, 2025. These changes raise the bar for products placed on the market and increase the value of compliance-ready portfolios.

Smart-connected appliances and serviceability also represent an opportunity layer. Interoperability improvements, such as Matter 1.4 referenced across connected-device positioning, can lower barriers to multi-brand households and shift competition toward software features, diagnostics, and aftersales performance. Retailers with strong e-commerce execution, for example Alza.sk's next-day delivery model cited in-market, can expand attachment of warranties, installation, and take-back services. Brands that invest in repair networks and parts availability may benefit as right-to-repair style requirements move into implementation through Slovak consumer-protection updates. In eastern Slovakia, manufacturing and component investments tied to heating and hot-water equipment build out supplier and logistics capabilities, supporting faster replenishment and a broader locally supported service footprint for adjacent appliance categories.

Recent Industry Developments

- June 2026: Vaillant reconfirmed the operational status of its heat pump mega-factory in Senica, Slovakia, a 100,000-square-metre site that reached full operational status in 2023 with stated capacity of 500,000 units annually. The scale strengthens Slovakia's role in European electrification and HVAC-adjacent manufacturing, with spillovers into supplier capability, service networks, and distribution infrastructure relevant to energy-related home equipment.

- September 2025: BSH Home Appliances Group announced a global strategic partnership with ECOVACS ROBOTICS to co-develop smart floor-cleaning robots, including a planned Bosch-branded integrated robotic vacuum-mop system for European retail launch in spring 2026. The collaboration raises competitive intensity in connected small appliances and pushes channel partners to differentiate on ecosystem integration, software updates, and aftersales support.

- October 2024: The Slovak government approved investment aid of about EUR 19.6 million for BDR Thermea Kosice to build a new plant in Vranov nad Toplou focused on heat pumps and stainless-steel tanks, with a commitment of up to 750 new jobs in the Presov region by 2028. The investment deepens the local manufacturing base for energy-efficient home equipment and adds momentum to eastern Slovakia's industrial ecosystem that supports adjacent appliance supply chains.

Research Methodology Framework and Report Scope

Market Definition and Coverage

For this study, the Slovakia home appliances market is defined as the annual value of new appliances sold in the country, covering large and small household appliances used for cooking, cleaning, cooling, laundry, and home comfort.

Scope exclusions: We exclude refurbished or second-hand appliance sales and appliance rentals to reduce double counting of the same unit across channels.

Segmentation Overview

- By Product

- Major Home Appliances

- Refrigerators

- Freezers

- Washing Machines

- Dishwashers

- Ovens (Incl. Combi & Microwave)

- Air Conditioners

- Other Major Home Appliances

- Small Home Appliances

- Coffee Makers

- Food Processors

- Grills & Roasters

- Electric Kettles

- Juicers & Blenders

- Air Fryers

- Vacuum Cleaners

- Toasters

- Countertop Ovens

- Other Small Home Appliances

- Major Home Appliances

- By Distribution Channel

- Multi-Brand Stores

- Exclusive Brand Outlets

- Online

- Other Distribution Channels

- By Geography

- Western Slovakia

- Central Slovakia

- Eastern Slovakia

Data Sources, Market Sizing, and Validation

Desk Research

Desk research is used to map demand drivers and set practical guardrails around units, pricing, and trade flows for Slovakia. We typically rely on public statistics and official references such as Eurostat, the Statistical Office of the Slovak Republic, European Commission energy labeling and Ecodesign documentation, UN Comtrade customs data, and OECD macro indicators, which help frame household formation, consumption, and import reliance.

To make the model realistic, we also review annual reports and investor presentations of relevant manufacturers and retailers, along with association websites and reputed press for updates on regulation and pricing conditions. Where it improves consistency, paid database subscriptions are used for company financials and intelligence, news and financials, and import and export shipment-level checks to spot abnormal swings. These examples are illustrative and not exhaustive, and other references were also used for collection, validation, and clarification.

Primary Interviews and Surveys

Primary work focuses on validating what secondary data cannot fully explain, especially category mix changes, promotion intensity, and realistic price movement in a given year. We spoke with a balanced mix of manufacturers, distributors, retailers, service partners, and category specialists across Slovakia to sanity-check volumes, replacement cycles, and how energy-efficiency rules are influencing purchasing decisions.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 29% | CXOs: 12% | APAC: 49% |

| Mid tier: 53% | Functional/Unit leaders: 40% | EMEA: 31% |

| Smaller Players: 18% | Managers: 48% | Americas: 20% |

Market-Sizing & Forecasting

Sizing starts with a top-down build where national consumption is reconstructed using a demand pool view that is anchored to household counts, appliance replacement cycles, and import and export patterns for key product groups. After that, totals are corroborated with selective bottom-up approximations, such as rolling up a sample of supplier and channel revenues and testing the implied average selling price (ASP) against observed retail price bands, and then the final value is adjusted where mismatches persist.

Key inputs that materially shape the model include the split of major versus small appliances, the mix shift toward higher-efficiency models, the share of promotional sales, and the trend in freight and energy-related cost pass-through that affects ASP. In Slovakia, housing turnover and renovation activity are also treated as practical demand signals because they tend to pull forward replacements for large appliances. Forecasting is handled through scenario analysis supported by simple multivariate relationships, where macro indicators and category-level replacement behavior are stress-tested with interview feedback, and gaps are handled by using conservative carry-forward assumptions until a consistent signal is confirmed.

Data Validation & Update Cycle

Outputs are triangulated against independent indicators, including import value trends, category-level pricing signals, and the implied per-household spend pattern, which helps keep results within plausible bounds. When a variance looks unusual, drivers are rechecked, assumptions are reopened, and follow-up outreach is triggered with interviewees who are closest to that category or channel.

Each report goes through multi-step analyst review before sign-off, including logic checks for unit consistency, currency conversion timing, and year-over-year step changes that may need explanation. Reports are refreshed annually, and interim updates are made when material events occur, such as tax changes, regulation updates, or sudden price shocks. Right before delivery, a fresh pass is completed so clients receive the latest view based on the most recent available information.

Mordor Intelligence's Slovakia Home Appliances Market Size Compared Against Other Published Estimates

Published market values for Slovakia home appliances can look far apart because the timing and mechanics behind the numbers are not always aligned. Differences usually come from which appliance categories are counted, whether the sizing uses retail or factory-level pricing, and how currency conversion is applied for a given year.

When exchange-rate windows, promotion-driven ASP swings, and trade-value cross-checks are refreshed on a predictable cadence, the size tends to stay closer to the real purchase cycle seen in the country, and that refresh-led discipline is built into Mordor Intelligence for this market.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 387.26 M (2026) | |

| Regional Consultancy A | USD 745.00 M (2024) | May apply a broader retail-value lens that blends appliances with adjacent categories or attach services, and it can also differ on whether re-sold units are removed, which can lift the total. |

| Industry Publisher B | USD 1.80 B (2026) | May include a wider end-user base beyond households and assume higher ASP levels across categories, and it may also apply a different currency conversion timing, which can expand the USD value for the same year. |

Across the three figures, the main takeaway is that scope choices and refresh timing for price and currency assumptions can move the number materially. By keeping the model tied to visible demand signals and then checking them against trade and channel reality, the result stays more repeatable when clients want to re-run the logic with updated inputs.

Key Questions Answered in the Report

What is the current value of the Slovakia home appliances market?

The market is valued at USD 387.26 million in 2026 and is projected to reach USD 472.83 million by 2031.

Which product segment holds the largest share?

Refrigerators lead with 21.55% revenue share in 2025, driven by mandatory efficiency upgrades.

Why are air fryers growing so quickly?

Air fryers align with health-focused cooking and compact kitchen trends, supporting a 10.02% CAGR forecast to 2031.

How fast are online appliance sales increasing?

Online channels are expected to expand at 9.28% CAGR, underpinned by 91.8% internet penetration and efficient logistics.

Which region will grow the fastest?

Eastern Slovakia is projected to register a 5.95% CAGR between 2026 and 2031 as EU-funded renovations accelerate appliance demand.

What policy changes most affect the market?

EU energy-efficiency rules and Slovakia’s 23% VAT rate shape pricing strategies and replacement cycles across the sector.

Page last updated on: