Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

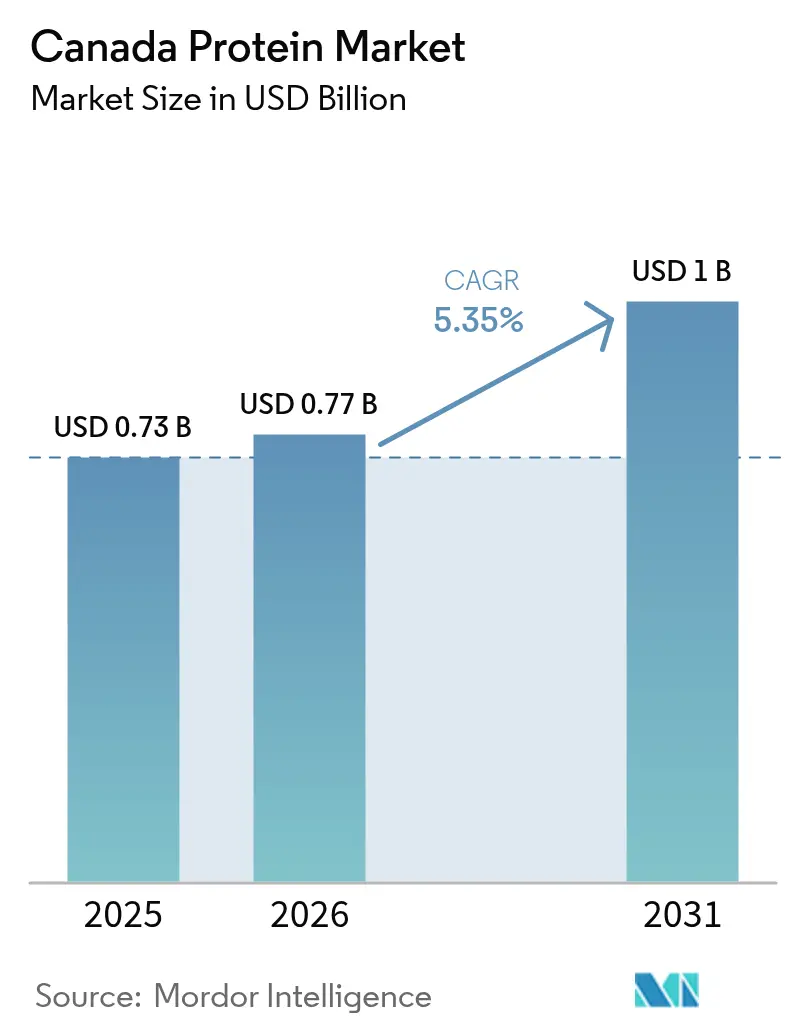

| Base Year Market Size (2025) | USD 0.73 Billion |

| Market Size (2026) | USD 0.77 Billion |

| Market Size (2031) | USD 1 Billion |

| Growth Rate (2026 - 2031) | 5.35% CAGR |

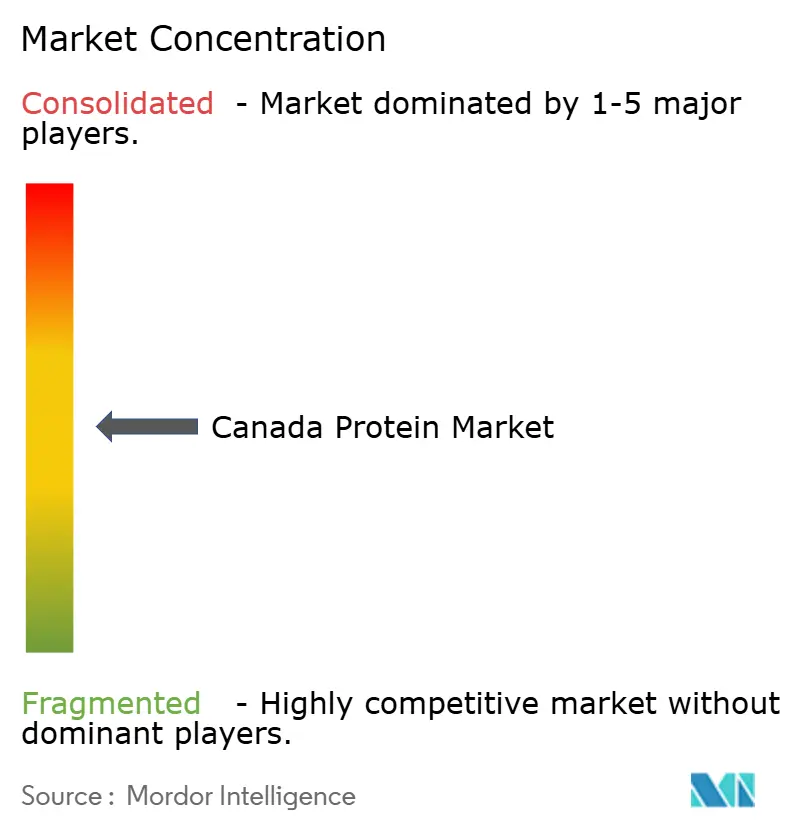

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Canada Protein Market Analysis by Mordor Intelligence

The Canada protein market size is projected to be USD 0.73 billion in 2025, USD 0.77 billion in 2026, and reach USD 1.00 billion by 2031, growing at a CAGR of 5.35% from 2026 to 2031. Federal super-cluster funding, large-scale Prairie processing hubs, and a nationwide shift toward flexitarian eating habits are steering demand toward plant and microbial proteins. Multinational ingredient suppliers are scaling Prairie facilities to capitalize on low-carbon hydroelectric power and direct rail access to export terminals, while regional innovators license proprietary extraction technologies to compete on functionality rather than volume. Traded-goods dynamics are equally important: processors hedge currency and crop-price swings through long-term grower contracts and diversified protein portfolios, thereby buffering earnings against drought-induced volatility in pea and lentil prices. Regulatory clarity for novel proteins and rising scrutiny of Scope 3 emissions among global buyers further strengthen Canada’s competitive edge in low-carbon, traceable protein ingredients.

Key Report Takeaways

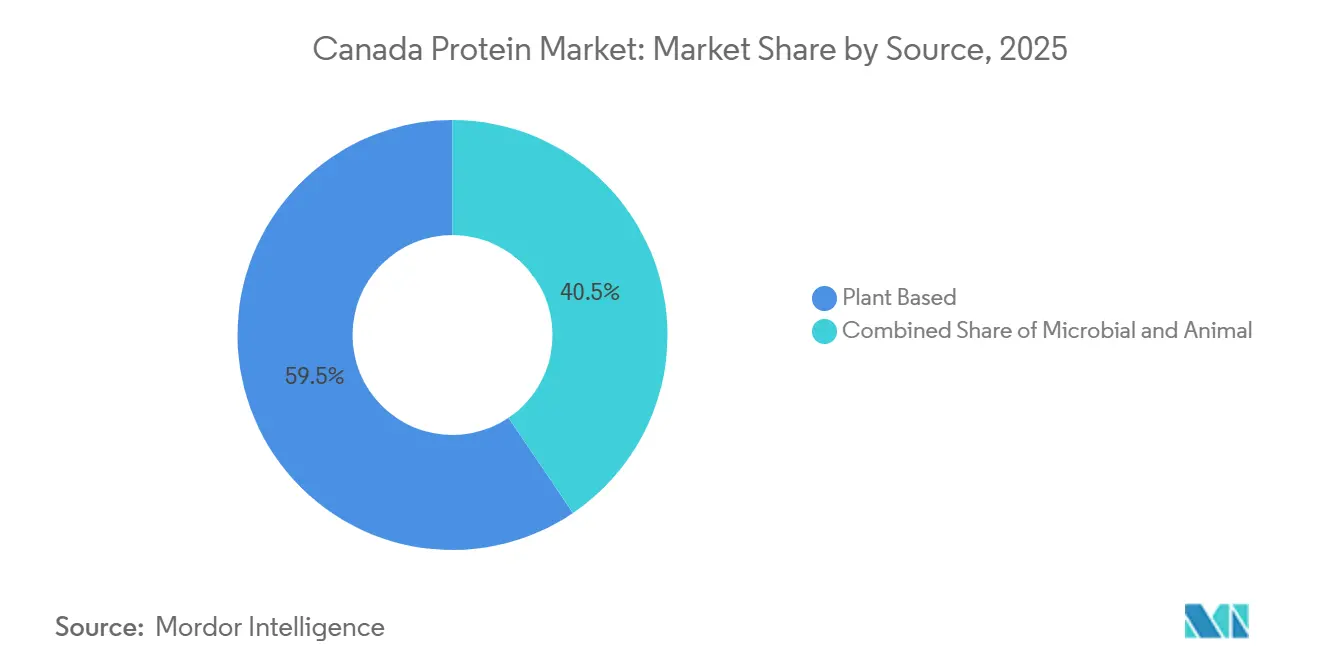

- By source, plant proteins led with 59.48% of Canada's protein market share in 2025, whereas microbial proteins are set to log the fastest growth at a 6.99% CAGR through 2031.

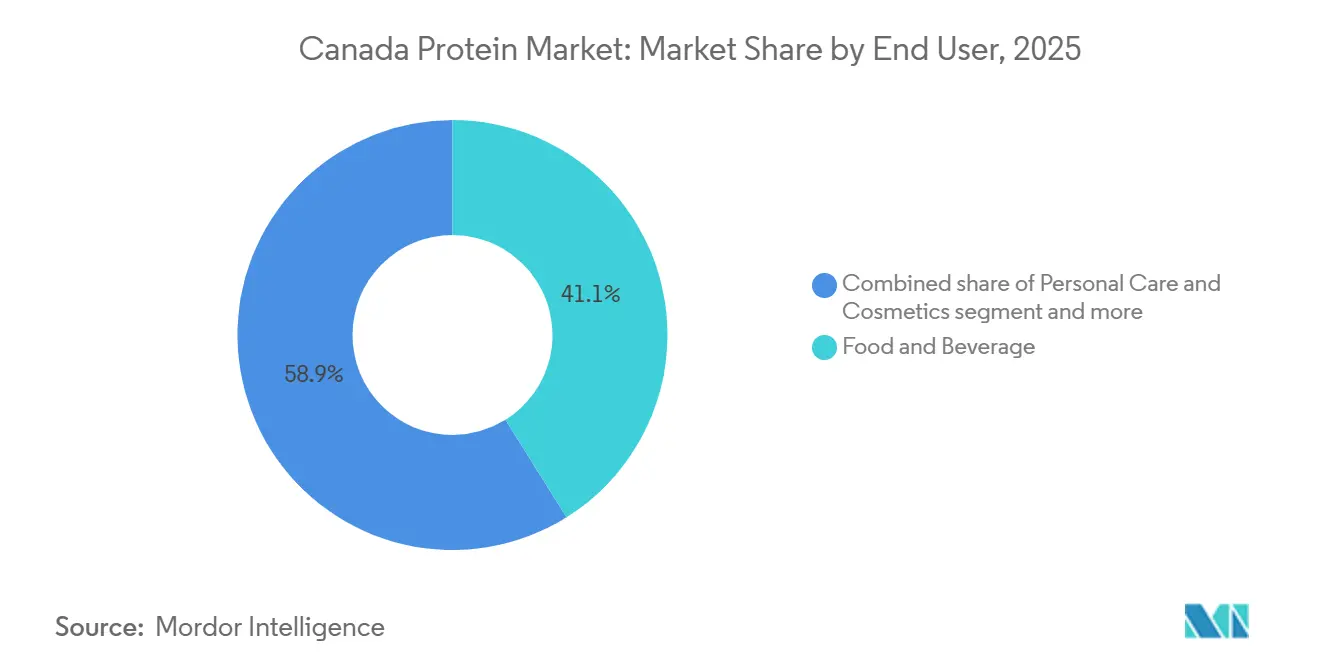

- By end user, food and beverages accounted for 41.05% of Canada's protein market size in 2025, while animal feed is projected to register a 5.75% CAGR over 2026-2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Canada Protein Market Trends and Insights

Drivers Impact Analysis*

| Driver | ( ~ ) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising demand for high-protein health and wellness foods | +1.2% | National, with concentration in urban centers (Toronto, Vancouver, Montreal) | Medium term (2-4 years) |

| Growth of plant-based and flexitarian diets | +1.5% | National, strongest in British Columbia and Ontario | Medium term (2-4 years) |

| Federal super-cluster funding (Protein Industries Canada) | +0.9% | Prairie provinces (Manitoba, Saskatchewan, Alberta) | Long term (≥ 4 years) |

| Prairie mega-facilities lowering production cost | +1.0% | Manitoba and Saskatchewan, export benefits national | Long term (≥ 4 years) |

| Canola and fava protein process breakthroughs | +0.6% | National production, global market access | Long term (≥ 4 years) |

| Low-carbon provincial energy advantage (e.g., Manitoba hydro) | +0.4% | Manitoba, competitive advantage for export-oriented facilities | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising demand for high-protein health and wellness foods

Health-conscious Canadians are embedding protein into everyday parts, from breakfast cereals fortified with pea isolate to ready-to-drink beverages delivering 20 grams per serving, a shift that food manufacturers are monetizing through premium pricing. The 2025 Dalhousie University survey revealed that 51% of Canadians are willing to reduce meat intake, with protein quality and satiety driving purchase decisions over calorie count alone[1]Source: Dalhousie University, “Canadian Consumer Food Trends Survey 2025,” dal.ca. This behavioral change is most pronounced among millennials and Gen Z consumers, who view protein as a functional ingredient rather than a macronutrient, prompting brands to reformulate snacks, condiments, and dairy alternatives with 8-12 gram protein claims. Regulatory frameworks under Health Canada's Food and Drug Regulations permit protein content claims when products meet minimum thresholds, enabling manufacturers to differentiate on-pack messaging and command shelf premiums in competitive categories. The convergence of aging demographics, seniors seeking muscle-preserving nutrition, and athletic populations pursuing performance gains is expanding addressable markets beyond traditional sports supplements into elderly nutrition and medical foods, segments where whey and casein proteins retain functional advantages despite plant-based competition.

Growth of plant-based and flexitarian diets

Flexitarianism is outpacing veganism as the dominant dietary trend in Canada, creating sustained demand for hybrid products that blend animal and plant proteins to optimize taste, texture, and cost. Approximately 15% of Canadians now follow plant-based diets, yet the larger opportunity lies in the 40% who identify as flexitarian, purchasing plant-based meat alternatives 2-3 times per month while maintaining omnivorous habits, according to the study by Dalhousie University. This dual consumption pattern is reshaping product development: dairy processors like Saputo and Agropur are launching blended yogurts that combine whey with pea protein to retain creaminess while lowering saturated fat, a formulation strategy that appeals to health-focused consumers unwilling to sacrifice sensory experience. The flexitarian cohort is less price-sensitive than value shoppers but more demanding of ingredient transparency, pushing brands to source non-GMO, organic-certified proteins and to disclose country of origin on labels, a trend that favors Canadian-grown pulses over imported soy, according to the Canadian Food Inspection Agency.

Federal super-cluster funding (Protein Industries Canada)

Canada's federal funding prioritizes projects that integrate canola crushing, pulse fractionation, and fermentation under single-site operations, reducing inter-facility logistics and enabling co-product valorization. Canola meal, for instance, is now being upgraded into protein concentrates rather than sold as low-margin animal feed. Co-funded initiatives include Merit Functional Foods' CAD 310 million (USD 232 million) canola and pea protein plant in Winnipeg, which achieved commercial production in 2024 and is targeting 20,000 tonnes of annual output by 2026. The super-cluster model also funds pre-competitive research at universities and government labs, accelerating process innovations, such as dry fractionation and membrane filtration, that lower water and energy consumption per kilogram of protein produced, a critical factor as carbon pricing rises under federal climate policy. By clustering investments in Manitoba and Saskatchewan, the program is creating regional ecosystems where ingredient suppliers, equipment manufacturers, and contract research organizations collaborate, reducing time-to-market for novel proteins from 5-7 years to 3-4 years.

Prairie mega-facilities lowering production cost

Large-scale fractionation plants are achieving unit economics that make Canadian pea and canola proteins cost-competitive with imported soy isolates, a threshold that unlocks mass-market adoption in price-sensitive categories like bakery and snacks. Roquette's Portage la Prairie facility, which began doubling capacity in 2024 to reach 250,000 tonnes annually, benefits from automation and continuous processing that reduce labor costs per tonne by 35% compared to batch operations. Louis Dreyfus Company's Yorkton plant, commissioned in 2025 with 75,000 tonnes of pea protein capacity, integrates starch recovery and fiber valorization, generating revenue from three product streams instead of one and improving overall plant profitability. These mega-facilities also negotiate long-term contracts with pulse growers, locking in feedstock prices and reducing exposure to spot-market volatility, a strategy that proved essential during the 2024 drought, when pea prices spiked 18% in Saskatchewan according to Statistics Canada. Proximity to Prairie acreage minimizes inbound freight, while export-oriented operators ship protein isolates in bulk tankers to U.S. and Asian customers, avoiding the margin dilution of small-pack retail distribution. The cost advantage is most pronounced in Manitoba, where hydroelectric power delivers industrial rates 25% below Alberta's natural-gas-dependent grid, a differential that compounds over multi-decade plant lifespans.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| CFIA labelling and novel food approvals complexity | -0.5% | National, affects all novel protein sources | Medium term (2-4 years) |

| Climate-driven pulse-crop price volatility | -0.7% | Prairie provinces (Saskatchewan, Alberta, Manitoba) | Short term (≤ 2 years) |

| Rail-capacity bottlenecks from Prairies to ports | -0.4% | Manitoba, Saskatchewan, Alberta (export-dependent facilities) | Short term (≤ 2 years) |

| Cultural taste barriers for insect/microbial proteins | -0.3% | National, strongest resistance in rural and older demographics | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

CFIA labelling and novel food approvals complexity

The Canadian Food Inspection Agency's novel food approval process requires extensive safety dossiers and can extend 18-24 months from submission to clearance, delaying market entry for microbial and insect proteins that lack a history of safe use in Canada. CFIA classifies proteins derived from precision fermentation, algae cultivation, and insect larvae as novel foods under Division 28 of the Food and Drug Regulations, triggering pre-market notification and toxicological assessment, a pathway that conventional plant proteins like pea and soy bypass because they are derived from foods with established safety records[2]Source: Canadian Food Inspection Agency, “Novel Foods,” inspection.canada.ca. This regulatory asymmetry disadvantages innovators: Enterra Corporation spent 3 years securing CFIA approval for black soldier fly larvae protein in aquaculture feed, a timeline that consumed working capital and allowed U.S. competitors to capture early-mover share in North American markets. Labeling requirements add complexity; CFIA mandates that novel proteins be identified by their source organism on ingredient panels, which can deter consumers unfamiliar with terms like "Aspergillus oryzae mycoprotein" or "Spirulina platensis protein," forcing brands to invest in consumer education and reformulation to mask novel ingredients within blends. The supplemented foods framework under Division 29 further restricts protein fortification levels in certain categories, capping the amount of added protein in beverages and snacks to prevent misleading nutrition claims, a rule that limits formulation flexibility for brands seeking to differentiate on high-protein positioning.

Climate-driven pulse-crop price volatility

Saskatchewan and Alberta experienced a 15% decline in pea yields during the 2024 growing season due to drought and heat stress, triggering spot-price spikes that compressed processor margins and forced some plants to source higher-cost pulses from Montana and North Dakota. Pulse crops, peas, lentils, and chickpeas are sensitive to moisture stress during flowering, and climate models project increased frequency of multi-year droughts across the Canadian Prairies, introducing structural volatility into feedstock costs. Processors with fixed-price supply contracts to food manufacturers cannot pass through input cost inflation, eroding profitability; Roquette and Louis Dreyfus mitigate this risk by contracting directly with grower cooperatives for multi-year deliveries at formula-based pricing, but smaller operators lack the balance-sheet strength to offer such terms. The 2024 drought also reduced protein content in harvested peas from typical levels of 21-23% to 19-20%, requiring processors to blend multiple lots to meet customer specifications and increasing handling costs, according to Agriculture and Agri-Food Canada. Crop insurance programs administered by provincial governments provide partial income protection to growers but do not stabilize prices for downstream processors, creating a mismatch between risk-sharing mechanisms and value-chain exposure. Long-term adaptation strategies include breeding drought-tolerant pea and fava varieties through public-private partnerships funded by Protein Industries Canada, though commercial deployment of such cultivars will not occur until 2027-2028.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Source: Plant Proteins Anchor Market, Microbial Segment Accelerates

Plant proteins held 59.48% market share in 2025, with pea protein dominating due to Prairie processing capacity that now exceeds 200,000 tonnes annually across Roquette, Louis Dreyfus, and Merit Functional Foods facilities. Burcon NutraScience's enzymatic extraction platform is enabling canola protein to challenge pea in sports nutrition formulations, where neutral flavor and hypoallergenic profiles justify premium pricing despite lower market penetration. Soy protein retains a foothold in bakery and meat alternatives, though Canadian production is limited and most supply is imported from U.S. Midwest crushers, creating a strategic vulnerability as trade frictions periodically disrupt cross-border flows. Wheat protein, primarily gluten extracted from flour milling, serves niche applications in baked goods and pet food but faces flat demand as gluten-free trends erode its addressable market. Hemp protein is emerging in organic and natural channels, supported by Health Canada's 2018 regulatory changes that legalized hemp food ingredients, yet production remains small-scale, and pricing is 2-3 times higher than pea, limiting mass-market adoption. Rice protein, sourced largely from Asian suppliers, occupies a minor share in hypoallergenic infant formulas and medical nutrition, where its low allergenicity offsets higher landed costs.

Microbial proteins, algae and mycoprotein, are expanding at 6.99% CAGR through 2031, the fastest rate among source segments, driven by precision fermentation platforms that produce complete proteins with amino acid profiles superior to most plant sources. Algae protein, particularly from Spirulina and Chlorella, is gaining traction in sports supplements and functional beverages, where its high leucine content supports muscle protein synthesis more effectively than pea or rice. Canadian startups are piloting closed-loop photobioreactor systems that eliminate seasonal variability and enable year-round production, though capital intensity remains a barrier to scale. Mycoprotein, derived from fungal fermentation, is being commercialized by international players with limited Canadian production to date, though CFIA's 2024 approval of Fusarium venenatum mycoprotein as a novel food ingredient opens the door for domestic manufacturing. Animal proteins, whey, casein, egg, collagen, gelatin, collectively represent a significant share, with dairy cooperatives like Agropur and Saputo investing in whey protein concentrate and isolate capacity to serve sports nutrition and infant formula markets; Agropur's CAD 200 million (USD 150 million) Lethbridge plant expansion, completed in 2025, added 15,000 tonnes of whey protein isolate capacity. Insect protein, led by Enterra Corporation's black soldier fly larvae, is approved for aquaculture feed and poultry rations, with limited human food applications due to cultural acceptance barriers, though regulatory pathways are clearer in feed than food.

By End User: Animal Feed Outpaces Food and Beverage Growth

Food and beverage applications commanded 41.05% market share in 2025, yet animal feed is projected to grow at 5.75% CAGR through 2031, outpacing all other end-user segments as livestock and aquaculture producers seek cost-effective, sustainable protein sources. Within food and beverages, dairy and dairy alternative products are the largest sub-segment, fueled by plant-based milk, yogurt, and cheese formulations that blend pea, oat, and almond proteins to optimize taste and texture; Saputo and Agropur are both launching hybrid dairy products that combine whey with pea protein to retain creaminess while lowering saturated fat. Meat, poultry, seafood, and meat alternative products represent the second-largest application, with plant-based burger and sausage brands sourcing pea and fava proteins from Canadian processors to meet clean-label and non-GMO claims. Aquaculture operators are substituting 30-40% of fishmeal with insect larvae protein and pulse concentrates, a shift driven by sustainability certifications like the Aquaculture Stewardship Council, which penalize reliance on wild-caught forage fish. Bakery applications, bread, muffins, and protein bars use wheat gluten and pea protein to boost protein content and improve dough strength, though formulation challenges around moisture retention and shelf life persist. Beverages, including ready-to-drink shakes and protein waters, demand highly soluble isolates with neutral flavor, a specification that favors canola and rice proteins over pea. Breakfast cereals, snacks, and RTE/RTC food products are incorporating protein to capture health-conscious consumers, with brands reformulating to achieve 8-12 gram protein claims that trigger front-of-pack callouts.

Supplements, encompassing sports nutrition, elderly nutrition, and infant formula, are a high-margin segment where whey and casein proteins retain functional advantages, though plant-based alternatives are gaining share among vegan and lactose-intolerant consumers. Sports and performance nutrition products favor whey protein isolate for its rapid digestion and high leucine content, yet pea and rice protein blends are capturing 25-30% of the segment by offering comparable amino acid profiles at lower price points. Elderly nutrition and medical nutrition products require proteins with high digestibility and low allergenicity, driving demand for hydrolyzed whey and rice proteins that meet clinical nutrition standards. Baby food and infant formula represent a tightly regulated sub-segment where dairy proteins dominate due to established safety profiles, though CFIA's approval of novel plant proteins for infant use could open opportunities for hypoallergenic formulations by 2027. Personal care and cosmetics applications use collagen, gelatin, and hydrolyzed proteins for hair and skin conditioning, a niche segment with limited growth potential but stable demand from premium beauty brands. Animal feed, the fastest-growing end user, benefits from CFIA's 2024 approval of insect protein for poultry and swine rations, expanding the addressable market beyond aquaculture; Enterra Corporation is scaling production to meet demand from integrators seeking to reduce reliance on soybean meal imports.

Geography Analysis

Canada's protein market is geographically concentrated in the Prairie provinces, Manitoba, Saskatchewan, and Alberta, which collectively host processing capacity due to proximity to pulse acreage and access to low-cost energy, yet Ontario and Quebec remain critical demand centers where 60% of end-user consumption occurs. Manitoba's 97% renewable electricity grid has attracted CAD 1.4 billion (USD 1.05 billion) in protein processing investments since 2020, including Roquette's pea protein complex in Portage la Prairie and Merit Functional Foods' canola and pea plant in Winnipeg, both of which market low-carbon credentials to European and North American buyers facing Scope 3 emissions targets. Saskatchewan leads in pulse crop production, supplying 50% of Canada's pea and lentil harvest, and hosts Louis Dreyfus Company's CAD 500 million (USD 375 million) Yorkton plant, which began commercial production in 2025 and is targeting Asian export markets where Canadian pulses command premiums for non-GMO and pesticide-residue compliance. Alberta's protein sector is smaller but diversifying, with Phytokana's proposed CAD 225 million (USD 169 million) pea protein facility in Strathmore receiving a CAD 10 million grant from Emissions Reduction Alberta, signaling provincial support for value-added agriculture. British Columbia and Ontario are net importers of protein ingredients, with demand driven by food and beverage manufacturers in Metro Vancouver and the Greater Toronto Area; these provinces also host research institutions like the University of British Columbia and University of Guelph that are advancing protein extraction and functionalization technologies through partnerships with Protein Industries Canada.

Export dynamics are reshaping regional growth trajectories: Canadian pea protein isolates are displacing European and Chinese suppliers in U.S. sports nutrition and plant-based meat markets, where buyers prioritize traceability and non-GMO sourcing. The Port of Vancouver handles 70% of Canada's protein ingredient exports, with bulk shipments to Japan, South Korea, and Taiwan, while Thunder Bay serves as the gateway for European-bound cargoes via Great Lakes and St. Lawrence Seaway routes[3]Source: Port of Vancouver, “Cargo Statistics,” portvancouver.com. Rail capacity constraints during harvest seasons periodically delay protein shipments, forcing processors to build larger inventories and increasing working capital requirements; CN Rail and CP Kansas City are investing CAD 500 million annually in Prairie corridor upgrades, though bottlenecks persist at key junctions near Winnipeg and Saskatoon. Quebec's dairy protein sector, anchored by Agropur and Saputo, is pivoting toward high-value whey protein isolates and hydrolysates for infant formula and clinical nutrition, markets where regulatory barriers to entry and technical specifications limit competition from plant proteins. Atlantic Canada remains a minor player in protein production, though Cooke Inc.'s aquaculture operations in New Brunswick are driving demand for insect and pulse proteins as fishmeal substitutes, creating localized opportunities for feed ingredient suppliers. The federal government's 2024 AgriInnovate program allocated CAD 75 million to support protein processing expansions in underserved regions, targeting Ontario and Quebec to reduce dependence on Prairie supply chains and improve food security according to the Agriculture and Agri-Food Canada.

Provincial policy divergence is creating competitive asymmetries: Manitoba offers capital tax credits for protein processing investments, Saskatchewan provides royalty holidays on Crown land leases for pulse growers, and Alberta's Technology Innovation and Emissions Reduction fund co-finances low-carbon processing equipment. These incentives, combined with federal super-cluster funding, are clustering investments in the Prairies and widening the gap with central and eastern provinces, where higher energy costs and limited feedstock availability constrain competitiveness. Ontario's food processing sector is lobbying for comparable support, arguing that proximity to 40% of Canada's population justifies domestic protein production to reduce transportation emissions and improve supply-chain resilience, a debate that will shape federal agricultural policy through 2027. The geographic concentration of processing capacity in Manitoba and Saskatchewan creates single-point-of-failure risks: a prolonged rail strike or severe drought could disrupt national supply, highlighting the strategic case for distributed capacity across multiple provinces.

Competitive Landscape

The Canada protein market exhibits moderate fragmentation, with the top five players, Agropur Dairy Cooperative, Archer Daniels Midland, Saputo, Roquette Frères, and Lactalis, collectively accounting for the majority market share, leaving substantial room for regional specialists and technology-driven disruptors to capture niche segments through proprietary extraction platforms and vertical integration strategies. Multinational ingredient suppliers are deploying capital-intensive mega-facilities to achieve unit-cost advantages, while Canadian-born innovators like Burcon NutraScience and AGT Food & Ingredients are licensing novel fractionation technologies to contract manufacturers, effectively monetizing intellectual property without bearing operational risk. Dairy cooperatives are defending whey and casein franchises by investing in ultrafiltration and hydrolysis capabilities that produce high-purity isolates for infant formula and clinical nutrition markets, where plant proteins face regulatory and functional barriers. Agropur's CAD 200 million (USD 150 million) Lethbridge expansion, completed in 2025, exemplifies this defensive strategy.

White-space opportunities are emerging in microbial proteins, where precision fermentation platforms can produce complete proteins with tailored amino acid profiles, yet capital requirements of CAD 100-200 million per plant and multi-year CFIA approval timelines deter all but the most capitalized entrants. Competitive intensity is highest in commodity pea protein, where Roquette, Louis Dreyfus, and Merit Functional Foods are competing on cost and carbon footprint, driving margin compression that favors scale and operational efficiency over differentiation. Technology adoption is becoming a decisive factor: Roquette's deployment of AI-driven process optimization at its Portage la Prairie plant reduced energy consumption per kilogram of protein by 12% in 2024, a gain that translates to CAD 3 million in annual savings and strengthens its position against lower-cost Asian suppliers.

Emerging disruptors include Enterra Corporation, which holds patents on black soldier fly larvae rearing systems that convert food waste into protein, creating a circular-economy narrative that resonates with sustainability-focused buyers; the company's 2025 capacity expansion to 10,000 tonnes annually positions it as a credible alternative to soybean meal in aquaculture and poultry feed. Smaller contenders like Avena Foods and Nutri-Pea are targeting organic and non-GMO segments, where certification premiums offset higher production costs and limited scale, though market size constraints cap revenue potential below CAD 50 million annually. Regulatory compliance is a competitive moat: companies that navigate CFIA's novel food approval process efficiently gain 18-24 month first-mover advantages, a dynamic that favors well-capitalized players with in-house regulatory affairs teams over underfunded startups reliant on consultants.

Canada Protein Industry Leaders

Agropur Dairy Cooperative

Archer Daniels Midland Company

Saputo Inc.

Roquette Frères

Lactalis Group

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2025: Hiton Foods bolstered its market presence with a USD 192 million investment in a food processing facility located in Brantford. This expansion is anticipated to strengthen the company's production capabilities and meet the rising demand for processed food products in the region.

- April 2024: Wamame Foods joined forces with AGT Food to craft high-protein meat alternatives in Canada, targeting global markets and leveraging new Canadian protein ingredients. This partnership aims to address the growing demand for sustainable and plant-based protein products worldwide.

- February 2024: Louis Dreyfus Company unveiled plans for an SK pea protein isolate plant, slated for a late 2025 debut, emphasizing high functionality and taste neutrality. The facility is expected to enhance the company's product portfolio and cater to the increasing consumer preference for plant-based protein solutions.

- April 2023: Sunnydale Foods, a Canadian company, announced significant progress in its product development efforts, particularly in the creation of high-protein pulse-based ingredients. They proudly introduced a faba bean protein concentrate with a protein content of 65% and are actively pursuing further enhancements to reach protein levels of up to 80%.

Canada Protein Market Report Scope

Protein is an essential macronutrient that plays a crucial role in the body, including building and repairing tissues, producing hormones and enzymes, and supporting immune function. The Canada Protein market is segmented by source and end-user. Based on the source, the market is segmented by animal, microbial, and plant. Based on animal sources, the market is further segmented into casein and caseinates, collagen, egg protein, gelatin, insect protein, milk protein, whey protein, and other animal protein. Based on microbial sources, the market is further segmented into algae protein and mycoprotein. Based on plant sources, the market is further segmented into hemp protein, oat protein, pea protein, potato protein, rice protein, soy protein, wheat protein, and other plant proteins. Based on end-users, the market is segmented into animal feed, personal care and cosmetics, food and beverages, and supplements. The end-user food and beverages segment is further sub-segmented into the bakery, beverages, breakfast cereals, condiments/sauces, confectionery, dairy and dairy alternative products, meat/poultry/seafood and meat alternative products, RTE/RTC food products, and snacks. The end-user supplements segment is further sub-segmented into baby food and infant formula, elderly nutrition and medical nutrition, and sport/performance nutrition. For each segment, the report provides market size in value (USD) and volume (tons).

By Source

| Animal | Casein and Caseinates |

| Collagen | |

| Egg Protein | |

| Gelatin | |

| Insect Protein | |

| Milk Protein | |

| Whey Protein | |

| Other Animal Proteins | |

| Microbial | Algae Protein |

| Mycoprotein | |

| Plant | Hemp Protein |

| Pea Protein | |

| Rice Protein | |

| Soy Protein | |

| Wheat Protein | |

| Other Plant Proteins |

By End User

| Food and Beverages | Bakery |

| Beverages | |

| Breakfast Cereals | |

| Condiments/Sauces | |

| Confectionery | |

| Dairy and Dairy Alternative Products | |

| Meat/Poultry/Seafood and Meat Alternative Products | |

| RTE/RTC Food Products | |

| Snacks | |

| Other Food and Beverage Applications | |

| Personal Care and Cosmetics | |

| Animal Feed | |

| Supplements | Baby Food and Infant Formula |

| Elderly Nutrition and Medical Nutrition | |

| Sport/Performance Nutrition |

| By Source | Animal | Casein and Caseinates |

| Collagen | ||

| Egg Protein | ||

| Gelatin | ||

| Insect Protein | ||

| Milk Protein | ||

| Whey Protein | ||

| Other Animal Proteins | ||

| Microbial | Algae Protein | |

| Mycoprotein | ||

| Plant | Hemp Protein | |

| Pea Protein | ||

| Rice Protein | ||

| Soy Protein | ||

| Wheat Protein | ||

| Other Plant Proteins | ||

| By End User | Food and Beverages | Bakery |

| Beverages | ||

| Breakfast Cereals | ||

| Condiments/Sauces | ||

| Confectionery | ||

| Dairy and Dairy Alternative Products | ||

| Meat/Poultry/Seafood and Meat Alternative Products | ||

| RTE/RTC Food Products | ||

| Snacks | ||

| Other Food and Beverage Applications | ||

| Personal Care and Cosmetics | ||

| Animal Feed | ||

| Supplements | Baby Food and Infant Formula | |

| Elderly Nutrition and Medical Nutrition | ||

| Sport/Performance Nutrition | ||

Key Questions Answered in the Report

How big is the Canada protein market today?

It is valued at USD 0.77 billion in 2026 and is forecast to reach USD 1.00 billion by 2031.

Which protein source leads Canadian production?

Plant proteins, mainly pea and canola, held 59.48% share in 2025.

What is the fastest-growing protein source segment?

Microbial proteins, including algae and mycoprotein, are projected to grow at 6.99% CAGR through 2031.

Why are Prairie provinces central to processing?

Proximity to pulse acreage, low-carbon hydro power, and rail links create cost and sustainability advantages.

Which end-user segment will grow fastest?

Animal feed, driven by aquaculture and poultry, is set to expand at a 5.75% CAGR over 2026-2031.

What hinders novel protein commercialization?

Lengthy CFIA approval timelines and labeling requirements slow speed-to-market for microbial and insect proteins.

Page last updated on: