Single-cell Omics Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

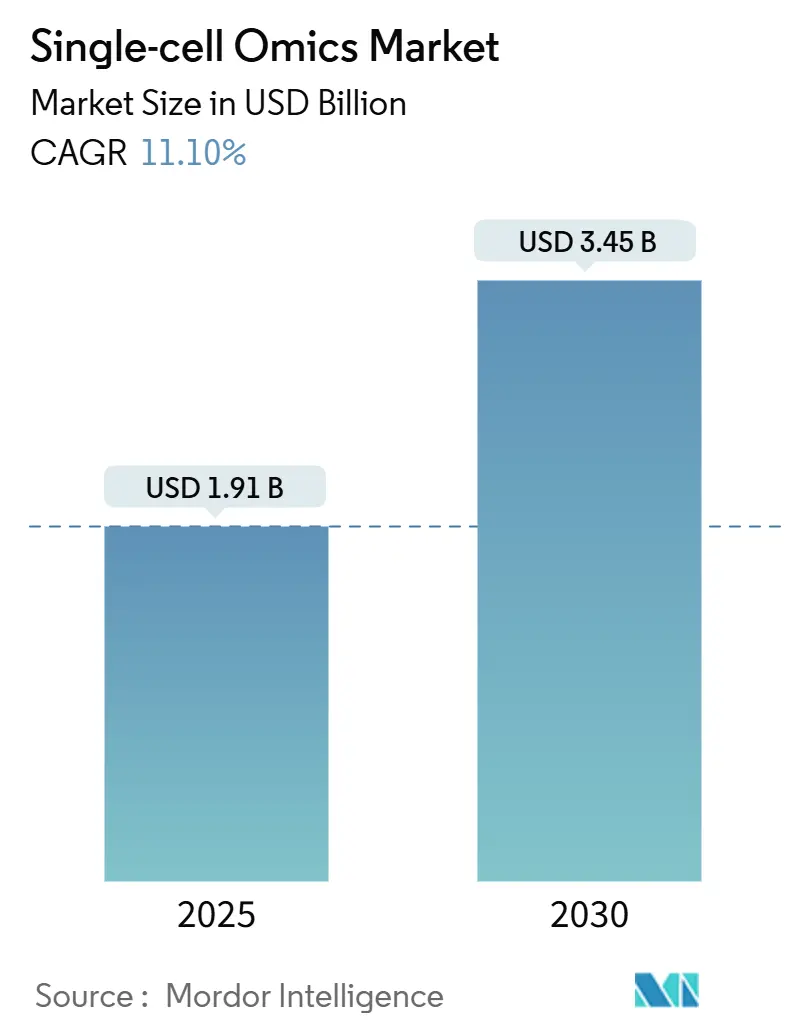

| Market Size (2025) | USD 1.91 Billion |

| Market Size (2030) | USD 3.45 Billion |

| Growth Rate (2025 - 2030) | 11.10% CAGR |

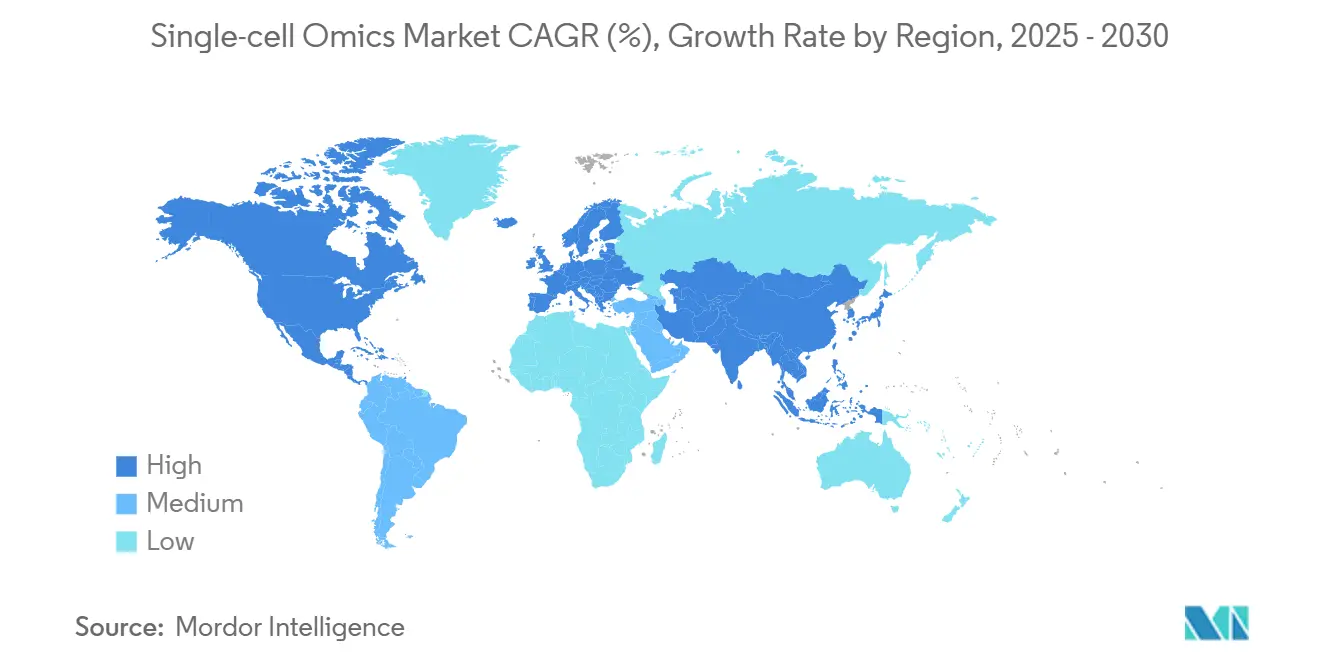

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Single-cell Omics Market Analysis by Mordor Intelligence

The Single-Cell Omics market size was valued at USD 1.9 billion in 2025 and is forecast to climb to USD 3.45 billion by 2030, reflecting an 11.1% CAGR over the period. Momentum stems from rapid price declines in droplet-based sequencing, where per-cell costs have fallen to USD 0.01 for high-throughput assays, enabling analysis of millions of cells per study. This cost compression, combined with precision-medicine mandates, has shifted purchasing priorities toward platforms that support multi-omic integration and scalable computational pipelines. Regional dynamics add further impetus: North America holds 38.7% revenue share on the strength of entrenched research infrastructure. In comparison, Asia Pacific delivers an 11.5% CAGR on aggressive public-sector genomics investment, such as India’s 10,000-genome initiative. Competitive intensity is rising as incumbents absorb specialized innovators, illustrated by Bruker’s USD 392 million purchase of NanoString’s spatial biology assets and Illumina’s acquisition of Fluent BioSciences to simplify single-cell workflows. Meanwhile, tighter U.S. laboratory-developed-test rules introduce both opportunity and compliance cost, even as AI-enabled reference mapping projects such as the Billion Cells Project promise to streamline data interpretation.

Key Report Takeaways

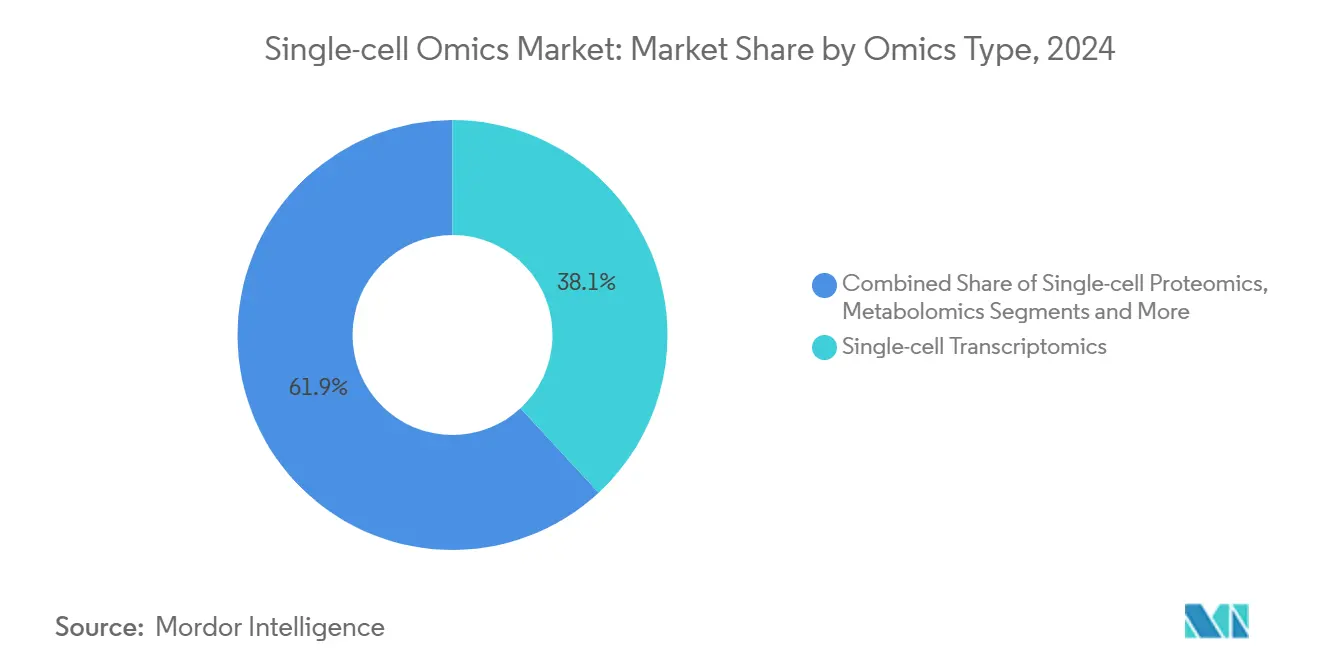

- By omics type, single-cell transcriptomics led with 38.1% revenue share in 2024, while integrated multi-omics is projected to expand at a 15.4% CAGR through 2030.

- By workflow component, consumables and reagents accounted for 46.5% of 2024 revenue; software and services show the fastest momentum at 11.6% CAGR to 2030.

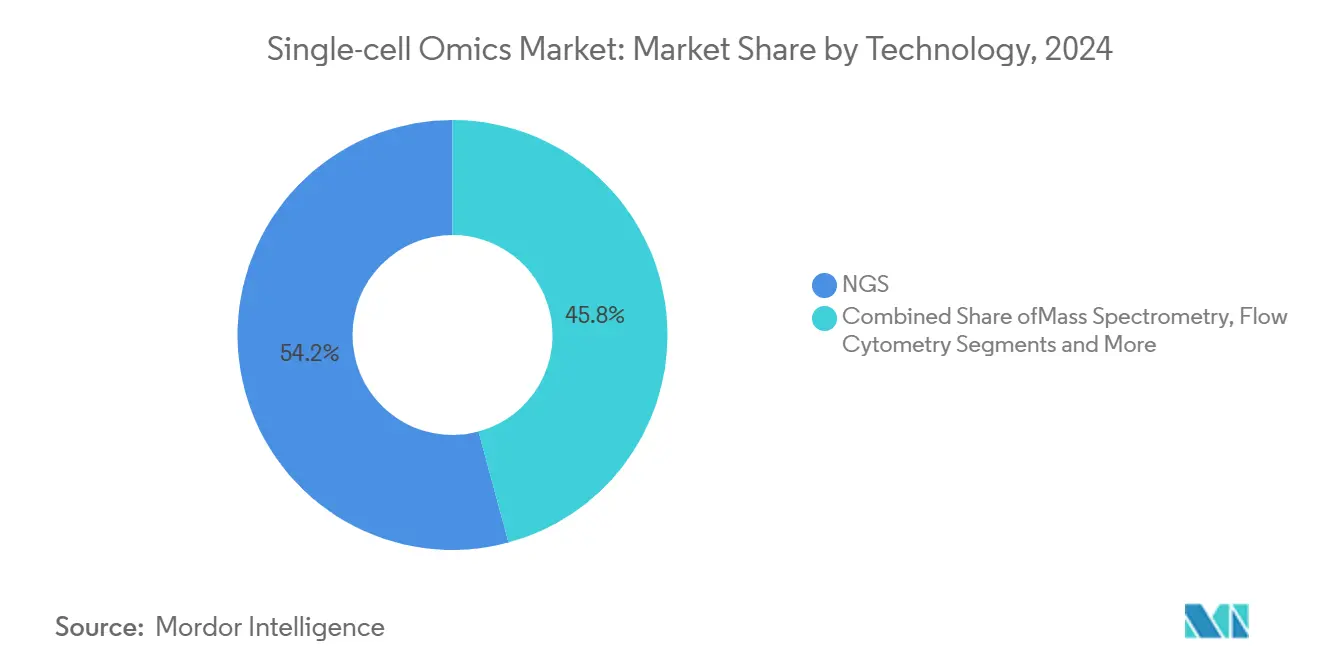

- By technology platform, next-generation sequencing commanded 54.2% share in 2024, whereas spatial transcriptomics records a 13.2% CAGR through 2030.

- By application, oncology captured 42.1% share in 2024; stem-cell and developmental biology is advancing at a 10.1% CAGR through 2030.

- By end user, academic and research institutes controlled 57.3% of 2024 revenue; pharmaceutical and biotechnology companies register the highest projected CAGR at 12.3% to 2030.

- By geography, North America held 38.7% revenue share in 2024; Asia Pacific posts the quickest regional growth at 11.5% CAGR through 2030.

Global Single-cell Omics Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rapid Adoption Of Single-Cell Sequencing In Oncology Precision Medicine | +3.20% | Global, with concentration in North America & Europe | Medium term (2-4 years) |

| Declining Cost Of NGS And Microfluidic Platforms | +2.80% | Global, accelerated in Asia Pacific | Short term (≤ 2 years) |

| Growing Investments And Grants For Single-Cell Research | +2.10% | North America & Europe primary, expanding to Asia Pacific | Long term (≥ 4 years) |

| Advancements In Multi-Omics Integration Software | +1.90% | Global | Medium term (2-4 years) |

| Emergence Of Spatial Single-Cell Multi-Omics Pipelines | +1.60% | North America & Europe, emerging in Asia Pacific | Long term (≥ 4 years) |

| Demand From Cell & Gene Therapy Process Analytics | +1.40% | North America & Europe | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rapid Adoption of Single-Cell Sequencing in Oncology Precision Medicine

Clinical oncology now relies on single-cell resolution to uncover tumor heterogeneity, detect minimal residual disease, and fine-tune treatment regimens. The myeloMATCH trial, a collaboration between Thermo Fisher Scientific and the U.S. National Cancer Institute, exemplifies real-time patient stratification based on cell-level biomarkers. FDA approval of TruSight-based companion diagnostics validates single-cell assays for clinical use and accelerates hospital adoption. Pharmaceutical pipelines increasingly incorporate multi-omic tumor profiling during early target-identification phases, shortening development cycles. Venture capital continues to flow to start-ups tackling liquid-biopsy applications, confirming the segment’s commercial appeal. Competitive advantage now hinges on delivering clinically annotated data sets at scale rather than raw sequencing throughput alone.

Declining Cost of NGS and Microfluidic Platforms

Ten years ago, single-cell assays cost hundreds of dollars per cell; today, droplet microfluidics pushes that figure to USD 0.01, widening global access. Standardized chip fabrication and barcoding chemistry produce economies of scale that compress consumable pricing without sacrificing read depth. New kit-based approaches eliminate bulky instruments, allowing smaller labs in emerging economies to enter the field. As academic barriers fall, population-level studies become feasible, opening new grant opportunities and fostering consortium-based investigations into complex diseases. Lower costs also stimulate demand for high-capacity data-analysis software, encouraging platform vendors to bundle cloud-based pipelines with reagent sales to secure recurring revenue.

Growing Investments and Grants for Single-Cell Research

Public and private funding peaked in 2025 as large-scale programs such as the Billion Cells Project pledged to profile vast cell repertoires with AI-ready metadata. India’s Genome India Project proves emerging markets can mobilize resources for comprehensive population studies. Venture capital backs translational ventures like OneCell Diagnostics, which secured USD 16 million to scale liquid-biopsy testing. The influx of capital feeds infrastructure build-outs, including biobanks and high-performance computing clusters, that form the backbone of sustainable multi-omic research ecosystems. Continuous funding also nurtures talent pipelines, mitigating the bioinformatics skills gap that has constrained adoption.

Advancements in Multi-Omics Integration Software

Data heterogeneity once created analytic bottlenecks; new machine-learning frameworks such as SpatialGlue and probabilistic integrators like MIDAS now reconcile genomics, transcriptomics, proteomics, and metabolomics within unified matrices.[1]Nature Methods, “A Machine Learning Tool for Spatial Multi-Omics,” nature.comCloud-native platforms, exemplified by NanoString’s AtoMx Spatial Informatics suite, extend enterprise-class analysis to mid-size labs without local servers. Algorithms capable of imputing missing modalities lower experimental cost by reducing redundant assays. Open-source communities speed feature upgrades and provide peer-reviewed validation, fostering trust in emerging computational standards. These software advances convert raw cell counts into actionable biological insights, thereby unlocking downstream diagnostic and therapeutic value.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Capital & Operational Costs Of Single-Cell Platforms | -2.40% | Global, particularly impacting emerging markets | Short term (≤ 2 years) |

| Data-Analysis Complexity & Lack Of Standard Pipelines | -1.80% | Global | Medium term (2-4 years) |

| Sample-Throughput Bottlenecks In Clinical-Grade Workflows | -1.50% | North America & Europe, expanding to Asia Pacific | Medium term (2-4 years) |

| Ethical & Privacy Concerns Around Cell-Level Genomic Data | -1.20% | Global, with heightened focus in Europe & North America | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High Capital & Operational Costs of Single-Cell Platforms

Although per-cell reagent expenses are dropping, high-end instruments still cost more than USD 500,000, placing them out of reach for many hospitals and universities. Annual maintenance contracts, specialized staff, and data-storage infrastructure add recurring overhead that can exceed initial capital outlay. Multi-omics requires parallel platforms, multiplying expenditure. Emerging-market institutions struggle most, widening the global research gap. Vendors address affordability through pay-per-run service models, yet budget constraints remain a near-term drag on adoption.

Data-Analysis Complexity and Lack of Standard Pipelines

Single-cell datasets often contain millions of observations per experiment, demanding bioinformatics expertise rare outside top centers. A fragmented software landscape leads to inconsistent preprocessing methods, hampering reproducibility. Regulatory agencies have yet to define validation standards, adding uncertainty for diagnostic developers. Cloud solutions lower computational burden but introduce security compliance tasks that smaller labs must navigate. Community-driven standards are forming, but time is required before plug-and-play analytics become ubiquitous.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Omics Type: Multi-Omics Integration Drives Growth

Integrated approaches underscore where the single-cell omics market is heading. Single-cell transcriptomics delivered 38.1% revenue share in 2024, underscoring its maturity; however, integrated multi-omics posts a 15.4% CAGR to 2030, making it the clear growth engine. Pharmaceutical companies now demand comprehensive cellular portraits that merge genomic, RNA, protein, and metabolic layers in one workflow. MIDAS integration software exemplifies how missing modalities can be imputed to retain biological fidelity.[2]Nature, “Mosaic Integration with MIDAS,” nature.com The outcome is faster target validation and richer biomarker panels that elevate clinical-trial precision.

The leap toward multi-omic concurrency expands total assay spend per sample, which enlarges the Single-Cell Omics market size for technology vendors. Although single-cell proteomics and metabolomics are nascent, advances in mass-spectrometry sensitivity and microfluidic isolation lift feasibility. Cross-platform convergence also compounds bioinformatic complexity, bolstering demand for cloud analytics. Combined, these forces reinforce the structural shift from single-modality dominance to holistic cellular interrogation.

By Workflow Component: Software Services Accelerate

Consumables and reagents generated 46.5% of 2024 revenue, reflecting the constant need for barcoded beads, sequencing kits, and microfluidic chips. Yet software and services grow fastest at 11.6% CAGR, confirming a pivot toward data-centric value extraction. Subscription-based informatics suites offer predictable margins and high customer stickiness, making them strategic for vendors aiming to diversify beyond instrument sales. Automated systems such as the Chromium-Beckman solution cut hands-on time to under thirty minutes, highlighting workflow industrialization.

Service bureaus armed with cloud pipelines can now deliver full turnkey projects, lowering entry barriers for labs lacking internal bioinformatics. As platform differentiation narrows, analytics usability becomes the decision factor. Vendors that pair consumables with end-to-end data interpretation stand to capture recurring revenue, enlarging their portion of the Single-Cell Omics market share.

By Technology Platform: Spatial Transcriptomics Leads Innovation

Next-generation sequencing remains the revenue anchor at 54.2% share in 2024, bolstered by economies of scale and standardized chemistry. Spatial transcriptomics however logs 13.2% CAGR, portraying it as the innovation frontier. Visium HD’s 2-micrometer tissue maps unlock cell-to-cell interaction insights previously unobtainable. The addition of CosMx by Bruker unifies spatial RNA and protein detection within one imaging platform.

Spatial capability raises the Single-Cell Omics market size within translational research by tying molecular events to histological context. Flow cytometry, PCR, and microfluidics remain indispensable for targeted or rapid assays, yet their growth trails spatial modalities. Vendors consequently bundle NGS back-end reading with front-end imaging to position themselves for comprehensive tissue-context solutions.

By Application: Stem Cell Biology Shows Promise

Oncology accounted for 42.1% of revenue in 2024 due to heavy precision medicine investment. Still, stem-cell and developmental biology deliver a 10.1% CAGR through 2030 as regenerative medicine research scales. Single-cell readouts reveal lineage trajectories and reprogramming efficiencies that bulk assays overlook. Immunology follows close behind, with spatial multi-omics clarifying cell-cell signaling within inflamed tissues, aiding biologic drug design.[3]Yahui Long et al., “The Spatial Multi-Omics Revolution in Cancer Therapy: Precision Redefined,” Cancer Communications, sciencedirect.com

Microbiology applications gain importance as pathogen surveillance embraces single-cell resolution for antimicrobial resistance tracking. Neurology labs leverage spatial transcriptomics to map neuronal circuits lost in degenerative disease. Each application growth vector feeds aggregate demand, guaranteeing the Single-Cell Omics market remains diversified across therapeutic areas.

By End User: Pharma Biotech Gains Momentum

Academic and research institutes led 2024 spending with 57.3% share, reflecting historical strengths in grant-funded discovery programs. Pharmaceutical and biotechnology companies, though, post a 12.3% CAGR as they internalize single-cell workflows for pipeline acceleration. Companies such as OneCell Diagnostics illustrate commercial momentum by integrating single-cell liquid biopsy into oncology trials.

Contract research organizations absorb overflow demand, especially for regulated bioanalysis. Diagnostic labs begin to adopt single-cell assays once companion-diagnostic approvals set analytical precedence. This diffusion into clinical organisms broadens total addressable demand, reinforcing growth across the Single-Cell Omics industry ecosystem.

Geography Analysis

North America captured 38.7% revenue in 2024, supported by NIH funding, early adopter pharmaceutical firms, and a dense cluster of platform vendors. FDA guidance on companion diagnostics clarifies regulatory pathways, encouraging hospital deployments. Despite leadership, growth moderates as market penetration deepens and capital budgets plateau. Continued investment in flagship initiatives such as the Billion Cells Project keeps innovation flowing and sustains the Single-Cell Omics market within the region.

Asia Pacific registers an 11.5% CAGR through 2030, the fastest globally. China’s BGI and MGI Tech launch turnkey single-cell platforms, while Japan and South Korea contribute precision instrumentation. India’s Genome India Project demonstrates capacity for nationwide cohort studies, signaling rising domestic demand. Lower production costs enable regional manufacturers to export competitively priced consumables, expanding the Single-Cell Omics market footprint into price-sensitive territories.

Europe maintains significant share through robust academic consortia and supportive data-sharing frameworks. GDPR compliance fosters advanced privacy-preserving analytics, an attractive feature for clinical partners. Horizon Europe grants fund cross-border multi-omic projects, enhancing technology uptake. Latin America, the Middle East, and Africa remain nascent but benefit from declining consumable costs and training initiatives. As regional centers of excellence emerge, these markets provide long-term expansion corridors.

Competitive Landscape

Competition balances scale and specialization. 10x Genomics, Illumina, and Thermo Fisher Scientific leverage broad portfolios, integrated consumable-software stacks, and entrenched customer bases. Bruker’s acquisition of NanoString’s spatial assets elevates its standing in tissue-context analysis. Illumina strengthens front-end simplicity via Fluent BioSciences’ PIPseq technology. These moves consolidate intellectual property and expand compatible chemistries across single-cell and spatial workflows.

Emerging entrants chase niche performance gains. BioSkryb Genomics targets whole-genome fidelity, while Scale Biosciences pushes ultra-high-throughput capacities that process 2 million cells per run. Deepcell applies generative AI to morphologically guided cell isolation, indicating a shift toward intelligent automation. Competition now centers on lowering the total cost of ownership, improving analysis usability, and securing clinical evidence. Partnership networks between platform vendors, pharmaceutical firms, and AI startups accelerate end-to-end solution development, raising barriers for latecomers but fostering rapid technology dissemination.

Single-cell Omics Industry Leaders

10x Genomics

Illumina

Thermo Fisher Scientific

BGI Group

Oxford Nanopore Technologies

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2025: Chan Zuckerberg Initiative unveiled the Billion Cells Project with 10x Genomics and Ultima Genomics to integrate AI and large-scale single-cell mapping.

- April 2025: Arc Institute partnered with 10x Genomics and Ultima Genomics to build the Arc Virtual Cell Atlas, holding 300 million single-cell measurements

- April 2025: Takara Bio rolled out the Shasta Single-Cell System scaling runs to 1,500 cells.

Global Single-cell Omics Market Report Scope

| Single-cell Genomics |

| Single-cell Transcriptomics |

| Single-cell Proteomics |

| Single-cell Metabolomics |

| Integrated Multi-omics |

| Instruments |

| Consumables & Reagents |

| Software & Services |

| Next-Generation Sequencing (NGS) |

| Mass Spectrometry |

| Flow Cytometry & FACS |

| Microfluidics |

| PCR & qPCR |

| Oncology |

| Immunology |

| Neurology |

| Stem-cell & Developmental Biology |

| Microbiology & Infectious Diseases |

| Academic & Research Institutes |

| Pharmaceutical & Biotechnology Companies |

| Clinical & Diagnostic Laboratories |

| Contract Research Organizations (CROs) |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia Pacific | China |

| Japan | |

| India | |

| South Korea | |

| Australia | |

| Rest of Asia Pacific | |

| Middle East & Africa | GCC |

| South Africa | |

| Rest of Middle East & Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Omics Type | Single-cell Genomics | |

| Single-cell Transcriptomics | ||

| Single-cell Proteomics | ||

| Single-cell Metabolomics | ||

| Integrated Multi-omics | ||

| By Workflow Component | Instruments | |

| Consumables & Reagents | ||

| Software & Services | ||

| By Technology Platform | Next-Generation Sequencing (NGS) | |

| Mass Spectrometry | ||

| Flow Cytometry & FACS | ||

| Microfluidics | ||

| PCR & qPCR | ||

| By Application | Oncology | |

| Immunology | ||

| Neurology | ||

| Stem-cell & Developmental Biology | ||

| Microbiology & Infectious Diseases | ||

| By End User | Academic & Research Institutes | |

| Pharmaceutical & Biotechnology Companies | ||

| Clinical & Diagnostic Laboratories | ||

| Contract Research Organizations (CROs) | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Australia | ||

| Rest of Asia Pacific | ||

| Middle East & Africa | GCC | |

| South Africa | ||

| Rest of Middle East & Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

How large is the Single-Cell Omics market in 2025?

The Single-Cell Omics market size stands at USD 1.9 billion in 2025.

What CAGR is expected for Single-Cell Omics between 2025 and 2030?

Revenue is projected to rise at an 11.1% CAGR through 2030.

Which region grows fastest in Single-Cell Omics?

Asia Pacific posts the highest regional CAGR of 11.5% due to strong public-sector genomics investment.

Which omics segment records the quickest growth?

Integrated multi-omics leads with a 15.4% CAGR as researchers seek holistic cellular insights.

Why are software services gaining share?

Cloud-based analytics and subscription models expand margins and reduce entry barriers, driving an 11.6% CAGR for software and services.

What is driving spatial transcriptomics adoption?

Subcellular resolution enables tissue-context mapping, pushing spatial transcriptomics to a 13.2% CAGR.

Page last updated on: