Global Single Cell Analysis Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

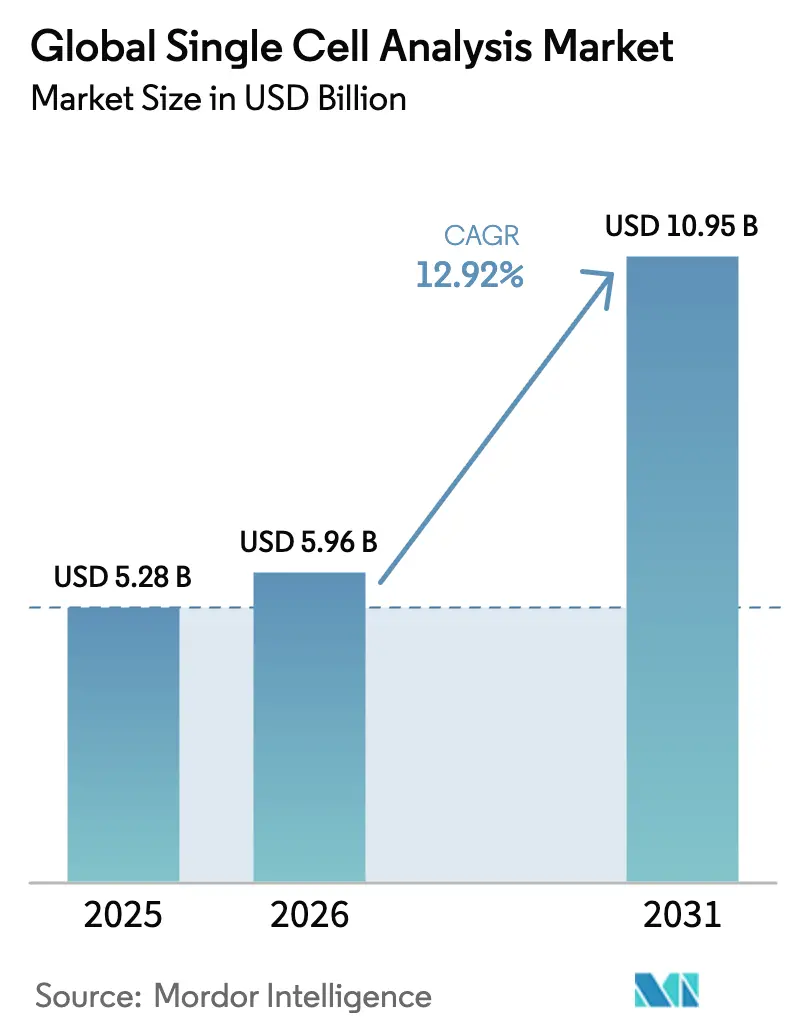

| Market Size (2026) | USD 5.96 Billion |

| Market Size (2031) | USD 10.95 Billion |

| Growth Rate (2026 - 2031) | 12.92% CAGR |

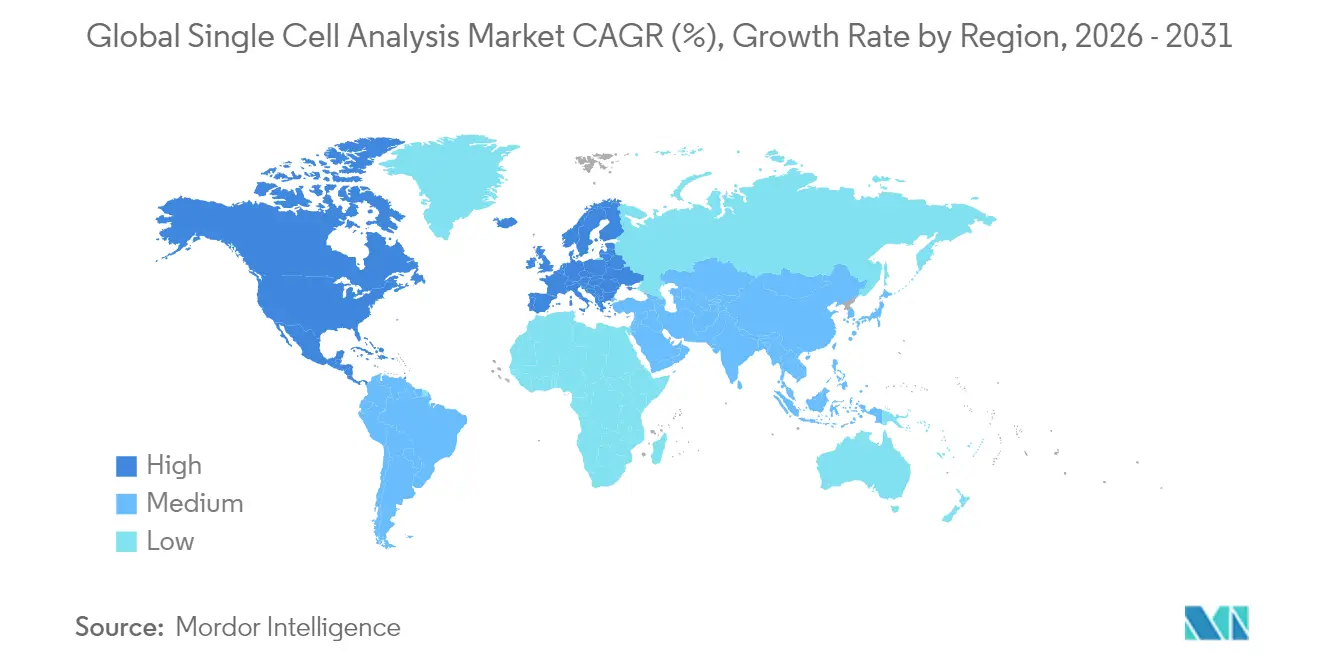

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Global Single Cell Analysis Market Analysis by Mordor Intelligence

The single cell analysis market size is expected to grow from USD 5.28 billion in 2025 to USD 5.96 billion in 2026 and is forecast to reach USD 10.95 billion by 2031 at 12.92% CAGR over 2026-2031. Expanding precision-medicine programs, a widening cancer and autoimmune disease burden, and active government and venture capital funding are sustaining double-digit growth. Rapid advances in single-cell multi-omics, AI-enabled bioinformatics, and spatial transcriptomics are opening new clinical and research use cases, while recurring consumables sales maintain predictable cash flows for suppliers. Strategic consolidation among large instrumentation firms and focused innovators is accelerating integrated workflow rollouts, and region-specific regulatory frameworks are beginning to accommodate diagnostic assays based on single-cell readouts.

Key Report Takeaways

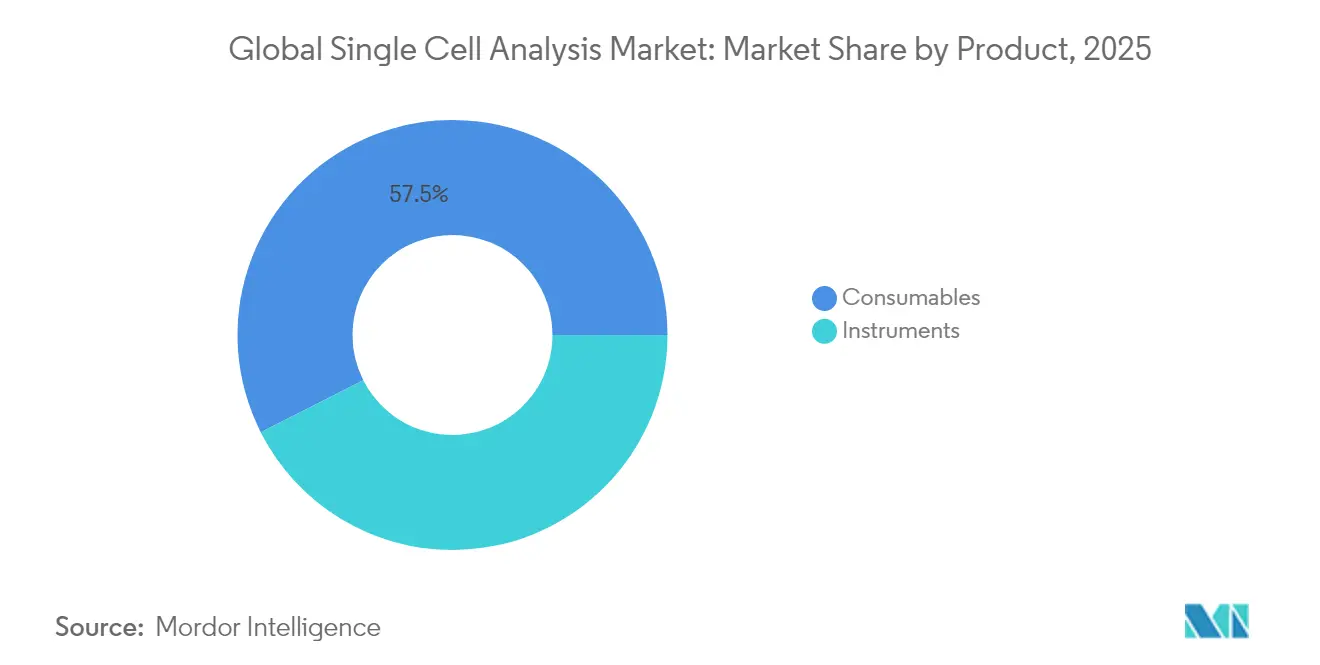

- By product, consumables led with 57.46% revenue share in 2025; instruments are projected to expand at 14.08% CAGR to 2031.

- By technique, flow cytometry captured 34.08% of single cell analysis market share in 2025, whereas next-generation sequencing is set to grow at a 13.35% CAGR through 2031.

- By cell type, human cells accounted for 60.74% share of the single cell analysis market size in 2025; microbial cells are advancing at a 13.94% CAGR to 2031.

- By workflow, the single-cell analysis step held 45.63% share in 2025, while data analysis and management is accelerating at 13.55% CAGR.

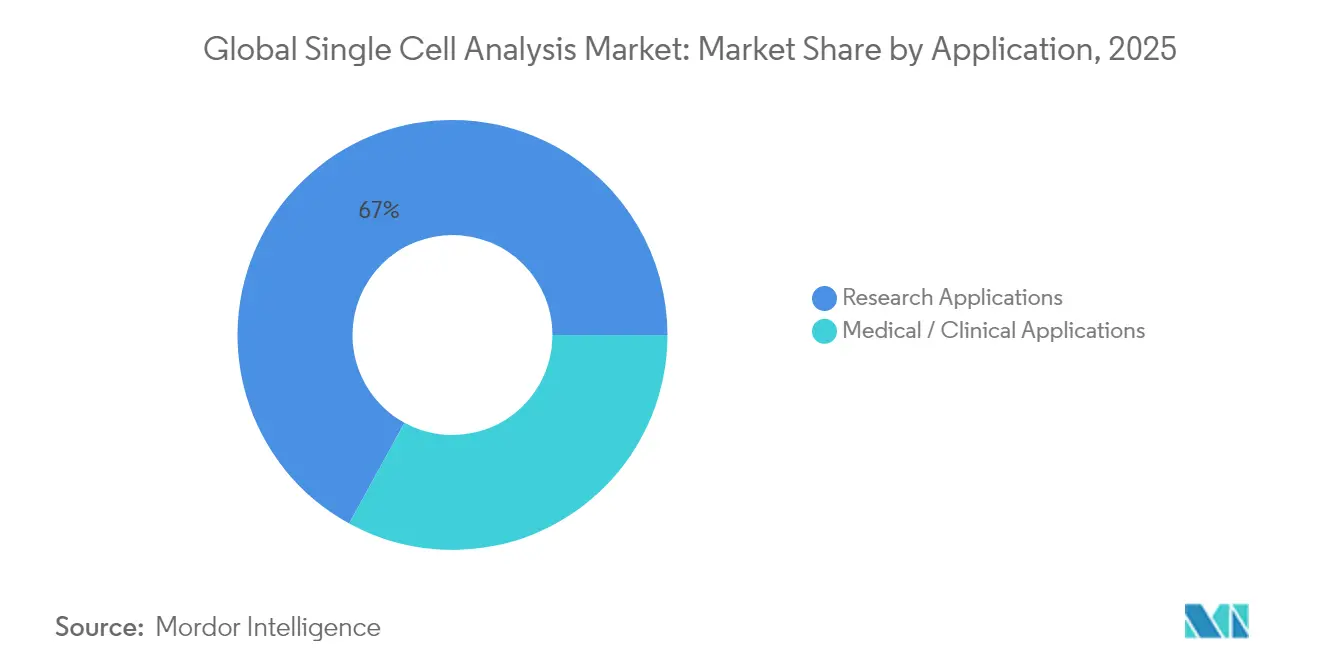

- By application, research commands 67.02% revenue share; medical and clinical use is expanding at a 13.82% CAGR to 2031.

- By end user, academic and research laboratories contributed 46.07% in 2025; biotechnology and pharmaceutical companies record the highest projected CAGR at 13.44%.

- By geography, North America dominated with 41.72% share in 2025, whereas Asia-Pacific is forecast to post a 14.12% CAGR between 2026-2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Single Cell Analysis Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Precision and personalized medicine adoption | +2.5% | North America, Europe, Global | Long term (≥ 4 years) |

| Multi-omics funding for precision oncology | +1.8% | North America, Europe, Emerging APAC | Medium term (2-4 years) |

| Rising cancer and immune-mediated disorders | +1.2% | Global, higher in aging regions | Long term (≥ 4 years) |

| Government and venture-capital investments | +1.5% | North America, Europe, China, Japan | Medium term (2-4 years) |

| AI-enabled bioinformatics platforms | +0.9% | Developed markets first, Global thereafter | Short term (≤ 2 years) |

| Spatial transcriptomics integration | +1.5% | North America, Europe, Advanced APAC | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Expanding Adoption of Precision and Personalized Medicine

Clinical programs increasingly rely on single-cell technologies to resolve cellular heterogeneity that limits bulk-omics approaches. Oncology illustrates the shift: single-cell RNA sequencing is identifying resistant tumor clones and refining immunotherapy selection, driving 35% gains in response-prediction accuracy [1]National Institutes of Health, “Single Cell Analysis Program,” nih.gov. Growing integration into routine workflows across major cancer centers positions the single cell analysis market for sustained long-term demand.

Surge in Single-Cell Multi-Omics Funding for Precision Oncology

Venture investment in startups that combine genomic, transcriptomic, and proteomic readouts at single-cell resolution surpassed USD 50 billion in 2024. Platforms delivering simultaneous DNA, RNA, and protein panels from a single cell are accelerating biomarker discovery and patient-stratification pipelines, reinforcing near-term commercial uptake.

Increasing Prevalence of Cancer and Immune-Mediated Disorders

Projected 47% growth in global cancer incidence by 2040 is magnifying demand for precise tumor profiling. Single-cell methods detect rare oncogenic or immune cell subpopulations that traditional diagnostics overlook, improving prognostic accuracy to 85% in melanoma cohorts.

Escalating Government and Venture-Capital Funding

More than USD 500 million in NIH grants and frequent USD 100 million-plus private rounds are accelerating product commercialization and broadening access to advanced platforms, mainly in North America, Europe, China, and Japan.

Introduction of AI-Enabled Bioinformatics Platforms

AI algorithms now automate cell-type annotation and trajectory inference, tackling terabyte-scale datasets that previously required specialized bioinformaticians. Early adopters report analysis-time cuts of up to 70% and reduced bottlenecks in clinical assay development.

Emergence of Spatial Transcriptomics Platforms Integrating Imaging + RNA-seq

Technologies that retain tissue context while mapping gene expression are illuminating tumor-microenvironment interactions, a critical factor in therapy design. Spatial workflows are gaining traction in oncology and neuroscience laboratories across the United States, Germany, Japan, and China.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High capital and maintenance costs | −1.5% | Emerging markets most affected | Medium term (2-4 years) |

| Shortage of trained bioinformaticians | −1.2% | APAC and MEA particularly | Short term (≤ 2 years) |

| Data-privacy compliance hurdles (GDPR, HIPAA) for cloud-based single-cell repositories | -0.9% | Europe and North America in the lead, global impact as cross-border projects grow | Short term (≤ 2 years) |

| Data-management, storage, and cybersecurity challenges | −0.8% | Global | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High Upfront Capital Expenditure and Maintenance Costs

Advanced spatial-omics instruments often list above USD 500,000, with annual service contracts adding 10-15% of ownership cost. High consumable prices, ranging USD 500–2,000 per sample, limit adoption outside well-funded centers, especially in Latin America, Africa, and parts of Southeast Asia [2]Oxford Nanopore Technologies, “Capital Markets Day 2023 Presentation,” storyblok.com.

Shortage of Trained Bioinformaticians for Giga-Scale Datasets

Two-thirds of research institutions report recruitment delays exceeding six months for data-science roles, hindering deployment of complex single-cell studies. Talent gaps are sharpest in emerging Asian and Middle-East hubs, prompting increased automation and online training initiatives [3]National Bioinformatics Infrastructure Sweden, “NBIS Strategic Plan 2025–2029,” nbis.se .

Data-Management, Storage, and Cybersecurity Challenges

Experiments profiling 10, 000 cells can generate 500 GB raw data. Institutions lacking robust IT infrastructure delay projects or scale back throughput, particularly when handling protected patient information. Cloud-native platforms are gaining favor but add subscription costs.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product: Consumables Sustain Recurring Revenue Streams

The consumables segment accounted for 57.46% of 2025 revenue as laboratories repeatedly purchase reagents, chips, and assay kits essential for routine workflows. Continuous demand for library-prep reagents anchors predictable income and lowers sensitivity to macroeconomic swings in instrumentation budgets. Instrument sales, although a smaller base, are projected to grow 14.08% CAGR owing to launches that combine multi-omic readouts in single runs. Automated liquid-handling and robotics modules that streamline high-throughput processing are also raising capital-equipment appeal.

Consumable manufacturers are pivoting toward integrated workflow bundles that pair reagents with software and technical support, deepening customer lock-in. Broad-portfolio firms capture cross-selling advantages, whereas niche reagent suppliers seek partnerships for full-solution offerings. The single cell analysis market size for instruments is set to expand rapidly as spatial-omics and combined DNA-RNA-protein analyzers move from prototype to commercial release.

By Technique: Next-Generation Sequencing Redefines Analytical Possibilities

Flow cytometry retained 34.08% revenue share in 2025 on the strength of established adoption in clinical immunology, transplantation, and blood-cancer labs. Continuous detector and fluorophore upgrades permit 40-plus-parameter panels, bolstering utility. Next-generation sequencing is the fastest-growing technique, forecast at 13.35% CAGR, as falling per-gigabase costs and cell-barcoding chemistries unlock high-content transcriptomic profiling. The single cell analysis market sees PCR, microscopy, mass spectrometry, microfluidics, and RNA-FISH occupying specialized niches. Mass-spectrometry-based single-cell proteomics is bridging transcript-to-protein gaps, while spatial transcriptomics combines imaging with sequencing to add microenvironment insights.

By Cell Type: Human Cells Dominate Clinical Research Applications

Human cells provided 60.74% of 2025 revenue, reflecting direct translational relevance. Oncology, neurology, and immunology depend heavily on patient-derived samples to capture disease heterogeneity. Microbial single-cell work, advancing at 13.94% CAGR, is unveiling microbiome functions in metabolic and inflammatory disorders. Animal models remain central to preclinical pipelines, and plant-cell studies, though smaller, are growing in agricultural biotech. Improved preservation and isolation protocols are expanding human clinical sample throughput, narrowing bench-to-bedside gaps. The single cell analysis market size attributed to microbial workflows is projected to swell as low-input chemistries overcome bacterial cell-wall hurdles.

By Workflow Step: Data Analysis Emerges as Critical Bottleneck

Single-cell analysis proper delivered 45.63% of 2025 revenue, covering cytometry, sequencing, and imaging. However, the data analysis and management segment is expanding at 13.55% CAGR as laboratories grapple with tera-scale datasets. Cloud-hosted platforms offering automated QC, clustering, and visualization are replacing home-grown pipelines. Sample-prep and cell-isolation advances are also pivotal; closed-cartridge systems now reduce hands-on time and variability, lifting reproducibility. Integrated end-to-end platforms are a competitive focal point, with co-developed solutions cutting total workflow time to under 10 hours.

By Application: Clinical Adoption Accelerates

Research dominated with 67.02% share in 2025, spanning oncology, stem-cell biology, immunology, and neuroscience. Clinical and medical uses are expanding at 13.82% CAGR as regulatory frameworks mature. Oncology diagnostics lead clinical uptake, driven by minimal residual disease detection and immunotherapy response monitoring. Prenatal screening and infectious-disease assays are burgeoning subsegments. AI-augmented interpretation is shortening the learning curve for pathologists evaluating complex multi-omic signatures. The single cell analysis market is thus shifting from exploratory science toward routine patient management.

By End User: Academic-Industry Partnerships Drive Innovation

Academic institutions held 46.07% revenue share in 2025, serving as early-adoption and innovation hubs. Biotech and pharmaceutical firms, growing at 13.44% CAGR, are integrating single-cell platforms into target discovery, lead-optimization, and patient-stratification studies. Diagnostic laboratories are gradually onboarding single-cell assays for clinical reporting, especially in hematologic malignancies. Contract research organizations are scaling capacity to deliver outsourced single-cell services, enabling smaller firms to access advanced capabilities without large capital spend.

Geography Analysis

North America contributed 41.72% revenue in 2025, supported by NIH funding, a dense network of cancer centers, and headquarters of global market leaders such as Thermo Fisher Scientific, Illumina, and 10x Genomics. FDA engagement with lab-developed single-cell diagnostics is fostering regulatory clarity. Regional collaborations between academic health systems and industry accelerate translational pipelines. The single cell analysis market size in North America is expected to keep expanding as reimbursements for molecular diagnostics broaden.

Asia-Pacific is forecast to post the fastest 14.12% CAGR through 2031. China’s precision-medicine initiatives, Japan’s engineering strengths, and India’s expanding biotech sector underpin demand. National research grants and favorable approval pathways for in-vitro tests are catalyzing local production of consumables and instruments. Regional governments are also investing in cloud infrastructure to cope with data-management demands.

Europe maintains a sizeable share led by Germany, the United Kingdom, and France. Horizon Europe grants fuel multi-center research, while the In-Vitro Diagnostic Regulation tightens performance-evidence requirements, influencing product designs. Smaller but growing adoption in the Middle East and South America reflects increasing healthcare modernization and genome-surveillance programs. Addressing cost barriers and workforce gaps will determine uptake pace across these emerging territories.

Mordor Intelligence provides coverage of the global single cell analysis market across other key regional markets, including Asia, each with their regulatory frameworks and demand patterns.

Regulatory Landscape

Regulation affecting single-cell analysis spans IVD oversight, advanced-therapy guidance, and data governance. In April 2026, the US FDA issued draft guidance on safety assessment of genome editing in human gene therapy products using next-generation sequencing, reinforcing expectations around assay performance, bioinformatics, and off-target assessment where single-cell and other NGS readouts support characterization. In parallel, the FDA signaled a more flexible chemistry, manufacturing, and control (CMC) posture for cell and gene therapies (January 2026), which increases the focus on robust analytical methods and release specifications, including sequencing-based approaches.

Standardization and traceability requirements are also tightening across global workflows. ISO published ISO 23494-1:2026 on provenance information management for biological material and data, and ISO/TC 276 is advancing ISO/DIS 25383 to define workflow and quality assessment requirements for scRNA-seq, pushing suppliers toward clearer QC metrics, documentation, and interoperable data handling. In the United States, legislative activity treating biological data as a strategic resource (for example, the Web of Biological Data Act of 2026 proposal) reinforces demand for compliant, auditable data pipelines that align with privacy and cross-border data-transfer constraints (for example, GDPR and HIPAA considerations for cloud repositories).

Value Chain Analysis

The single-cell analysis value chain starts with biological samples (human, animal, microbial, and plant) and upstream inputs such as enzymes, nucleotides, antibodies, microfluidic consumables, and assay kits. It then moves to instruments for isolation (sorting and microfluidics), measurement (NGS, cytometry, imaging, and emerging proteomics), and software for processing, storage, and interpretation. Consumables remain the recurring purchase engine (57.46% revenue share in 2025), while capital equipment purchases are increasingly paired with service contracts, workflow validation support, and bundled informatics to reduce total workflow time and improve reproducibility.

Downstream, distribution runs through direct sales to major academic centers, biopharma, and hospital laboratories, plus channel partners for broader geographic reach. Service delivery is also handled through CROs and core labs. Partnerships are increasingly used to integrate adjacent layers of the stack: 10x Genomics and Cleveland Clinic (June 2026) linked platforms (Flex Apex and Xenium) with clinical sample access for biomarker work, while ZEISS and EDGE Biotechnologies (April 2026) connected imaging hardware with AI analytics to support biopharma R&D workflows. Similar cross-vendor integration is visible in spatial transcriptomics workflows that combine Takara Bio USA and Illumina assays (presented February 2026), and in analytics-led alliances such as Waters and IMU Biosciences (June 2026) that join single-cell technologies with AI immune-mapping, underscoring informatics, automation, and clinical validation as key bottlenecks and differentiators.

Competitive Landscape

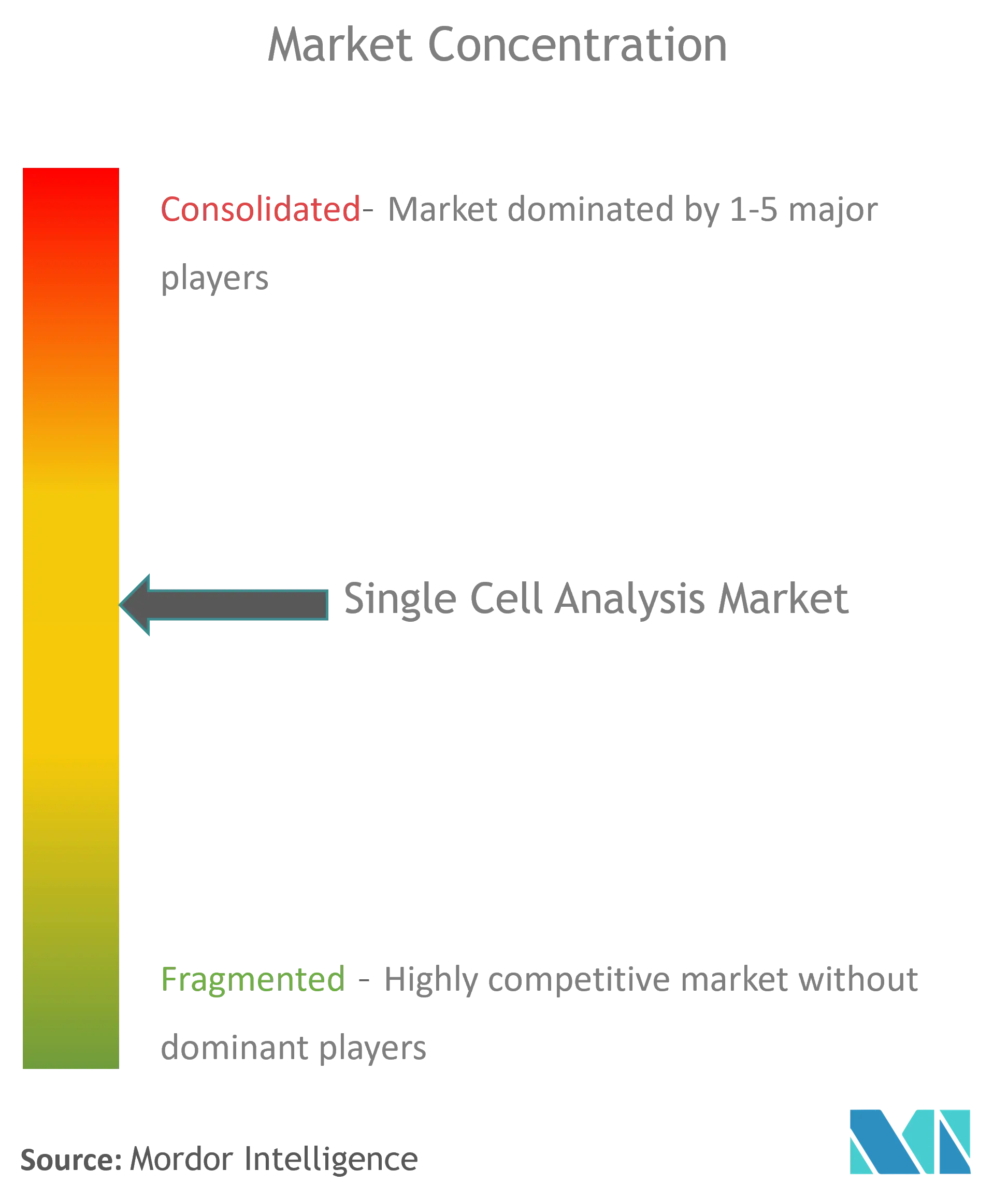

The single cell analysis market is moderately concentrated. Diversified instrument companies—Thermo Fisher Scientific, Becton Dickinson, and Illumina—combine broad portfolios with global distribution, while specialists such as 10x Genomics and Parse Biosciences focus on high-throughput multi-omic and spatial solutions.

Acquisition activity remains brisk; Qiagen’s 2023 purchase of Genoox expanded clinical-grade genomic capabilities. Competitive differentiation centers on integrated workflows covering sample prep to AI-assisted interpretation.

AI software developers and cloud providers are new entrants, partnering with assay vendors to tackle data bottlenecks. Opportunities persist for developers of cost-controlled, clinical-grade assays aimed at oncology and infectious-disease diagnostics.

Global Single Cell Analysis Industry Leaders

Bio-Rad Laboratories Inc.

Illumina Inc.

Beckman Coulter Inc. (Danaher Corporation)

Becton, Dickinson, and Company

Fluidigm Corporation

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

Clinical translation and workflow scale-up are creating clear whitespace in automated, standardized end-to-end offerings that reduce labor, turnaround time, and analysis burden. A concrete signal is the market shift toward massively scaled study designs enabled by automation-compatible formats, such as 10x Genomics next-generation Chromium Flex (October 2025), positioned around high-throughput profiling using plates and automation. This direction aligns with persistent constraints cited by end users, including trained bioinformatics shortages and data-management challenges, which supports opportunities for vendors that bundle instruments, consumables, and AI-assisted analysis in validated pipelines.

Regulatory and standards activity also supports commercialization of clinical-grade single-cell and spatial readouts, particularly where NGS and complex bioinformatics are central to claims. The FDA draft guidance on NGS-based safety assessment for genome editing in gene therapy products (April 2026) and ISO provenance and scRNA-seq standardization work (ISO 23494-1:2026 and ISO/DIS 25383 under ISO/TC 276) increase demand for traceable sample-to-result documentation, QC frameworks, and interoperable data handling. On the technology side, the market is moving toward multi-omics and spatial solutions with stronger software ecosystems, evidenced by launches such as Illumina Connected Multiomics (January 2026) and Illumina StrataMap Spatial Solution (June 2026), creating opportunity for platform providers and specialist software firms that can meet privacy, cybersecurity, and cross-site harmonization needs for multi-center translational programs.

Recent Industry Developments

- June 2026: Illumina launched the StrataMap Spatial Solution as an end-to-end sequencing-based spatial transcriptomics platform delivering single-cell resolution. The release strengthens Illumina's position in spatial workflows by pairing assays with an integrated ecosystem that can be scaled across research and translational settings.

- October 2025: Becton, Dickinson and Company entered a multi-year collaboration with Opentrons Labworks to integrate robotic liquid-handling into the BD Rhapsody HT Xpress System for automated single-cell multiomics workflows. The partnership targets higher throughput and standardization, reinforcing automation as a competitive requirement for large-scale single-cell programs.

- June 2024: Bio-Rad Laboratories launched the ddSEQ Single-Cell 3 RNA-Seq Kit alongside Omnition v1.1 analysis software for single-cell gene expression research. Bundling chemistry with analysis tools supports tighter workflow control and helps suppliers defend consumables pull-through as users expand sequencing-based single-cell studies.

Research Methodology Framework and Report Scope

Market Definition and Coverage

The single cell analysis market covers revenues from tools and workflows used to isolate, process, and measure biological signals at the individual cell level, across research and clinical use where applicable.

Scope exclusions: bulk or population-level assays that only report averaged signals across many cells without single-cell resolution are excluded.

Segmentation Overview

- By Product

- Consumables

- Instruments

- By Technique

- Flow Cytometry

- Next-Generation Sequencing

- Polymerase Chain Reaction (PCR)

- Microscopy

- Mass Spectrometry

- Microfluidics

- RNA-FISH

- Other Techniques

- By Cell Type

- Human Cells

- Animal Cells

- Microbial Cells

- Plant Cells

- By Workflow Step

- Sample Preparation

- Cell Isolation & Sorting

- Single-Cell Analysis

- Data Analysis & Management

- By Application

- Research Applications

- Stem Cell Research

- Neuroscience

- Immunology

- Oncology

- Microbiology

- Other Research Applications

- Medical / Clinical Applications

- Prenatal Testing

- In Vitro Fertilization

- Infectious Disease Diagnostics

- Oncology Diagnostics

- Research Applications

- By End User

- Academic & Research Laboratories

- Biotechnology & Pharmaceutical Companies

- Hospital & Diagnostic Laboratories

- Contract Research Organizations (CROs)

- By Geography

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Rest of Europe

- Asia-Pacific

- China

- Japan

- India

- South Korea

- Australia

- Rest of Asia-Pacific

- Middle East

- GCC

- South Africa

- Rest of Middle East

- South America

- Brazil

- Argentina

- Rest of South America

- North America

Data Sources, Market Sizing, and Validation

Desk Research

Desk research starts with mapping the installed research base and testing activity that drive demand for single-cell workflows. We reference public sources including the US National Institutes of Health (NIH) funding databases, the US FDA for relevant clinical and diagnostics context, the World Health Organization for disease burden signals, and OECD or World Bank indicators for R&D intensity and healthcare spending.

To translate activity into a practical demand pool, we review peer-reviewed journals in genomics and cell biology to understand technique adoption patterns, patents databases to track innovation cadence, and trade association or conference materials that summarize instrument placements and workflow trends. Company filings, investor presentations, and reputable press are also used to time major product cycles and pricing direction, supported by paid subscriptions for company financials and patent analytics where useful. These sources are illustrative, and additional public references were also used to collect, validate, and clarify inputs.

Primary Interviews and Surveys

Primary work is used to pressure-test adoption and pricing assumptions that are hard to infer from public data alone. We speak with tool manufacturers, reagent and consumables suppliers, software and service providers, and end users such as academic labs, biotech teams, and hospital-linked research groups across major regions. Afterward, we re-check any large variances before finalizing inputs.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 28% | CXOs: 14% | APAC: 48% |

| Mid tier: 55% | Functional/Unit leaders: 41% | EMEA: 30% |

| Smaller Players: 17% | Managers: 45% | Americas: 22% |

Market-Sizing & Forecasting

Sizing is built using a top-down approach where funding levels, testing intensity in high-need disease areas, and lab capacity indicators are used to reconstruct addressable demand for single-cell workflows by region. Once the demand pool is formed, we convert it into revenue using inputs such as instrument placement trends, average consumables pull-through per instrument, typical run volumes for key assays, and average selling price ranges by workflow type.

To keep the totals grounded, we corroborate results with selective bottom-up approximations, including sampled supplier revenue splits, channel feedback on annual unit movement, and ASP times volume checks for common consumables lines. When cross-checks show a consistent gap, the model is adjusted. For forecasting, scenario analysis is run around the main growth levers and is informed by interview-based consensus on adoption speed, pricing progression, and the pace of new workflow launches. Where the bottom-up view is incomplete for smaller countries or newer applications, we handle gaps using proxy indicators such as research spend, publication intensity, and installed base scaling.

Data Validation & Update Cycle

Outputs are validated through internal review rounds and cross-checks against independent signals, including funding direction, publication volume, and the pace of instrument-related announcements. If the model produces step-changes that do not align with these signals, assumptions are reopened and, when needed, experts are re-contacted to confirm whether a shift is real or timing-related.

Before sign-off, regional totals are checked for currency consistency, double counting across tools and consumables, and year-on-year movement that does not match adoption realities. Reports are refreshed annually, with interim updates when material events occur, such as major regulatory changes or large product cycle resets. Right before delivery, we do a final pass so clients receive an updated view.

Mordor Intelligence's Single Cell Analysis Market Size Versus Other Published Estimates

Published market values for single cell analysis can differ widely because studies do not always count the same revenue lines, and the base year and exchange rate assumptions can vary. Differences also come from how each model treats consumables pull-through, services, and software that sits inside broader life science tool budgets.

Evidence like the 2025 to 2026 step-up on the report page, plus region-level growth patterns that align with adoption and funding signals, is used to anchor Mordor Intelligence to a repeatable demand pool rather than broad life science spending totals.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 5.28 B (2025) | |

| Global Consultancy A | USD 4.89 B (2024) | Uses a different base year and growth window, and its scope appears to weight clinical and diagnostics usage more heavily, which can shift pricing and adoption assumptions versus a research-led demand build. |

| Industry Publisher B | USD 3.81 B (2025) | Narrower revenue capture in practice, since parts of software and services can be treated as optional or embedded under broader lab informatics and service categories, which reduces the counted total. |

The spread in values is mainly explained by scope boundaries and how each study converts activity into revenue, especially around consumables intensity and what is counted as stand-alone single-cell workflow spend. By keeping the demand drivers explicit and then cross-checking with supplier and channel reality checks, the final number stays traceable to inputs that can be reviewed and updated without reworking the full model.

Key Questions Answered in the Report

How big is the Global Single Cell Analysis Market?

The Global Single Cell Analysis Market size is expected to reach USD 5.96 billion in 2026 and grow at a CAGR of 12.92% to reach USD 10.95 billion by 2031.

What factors are driving the rapid growth of the single cell analysis market?

Precision-medicine adoption, rising cancer incidence, and sustained public- and private-sector funding are the primary growth catalysts, pushing the market toward a 12.92% CAGR through 2031.

Who are the key players in Global Single Cell Analysis Market?

Bio-Rad Laboratories Inc., Illumina Inc., Beckman Coulter Inc. (Danaher Corporation), Becton, Dickinson, and Company and Fluidigm Corporation are the major companies operating in the Global Single Cell Analysis Market.

Why is Asia-Pacific the fastest-growing regional market?

Large government precision-medicine programs, expanding research infrastructure, and favorable approval pathways are propelling Asia-Pacific at a projected 14.12% CAGR.

Which region has the biggest share in Global Single Cell Analysis Market?

In 2025, the North America accounts for the largest market share in Global Single Cell Analysis Market.

Page last updated on: