Single-Cell Genome Sequencing Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

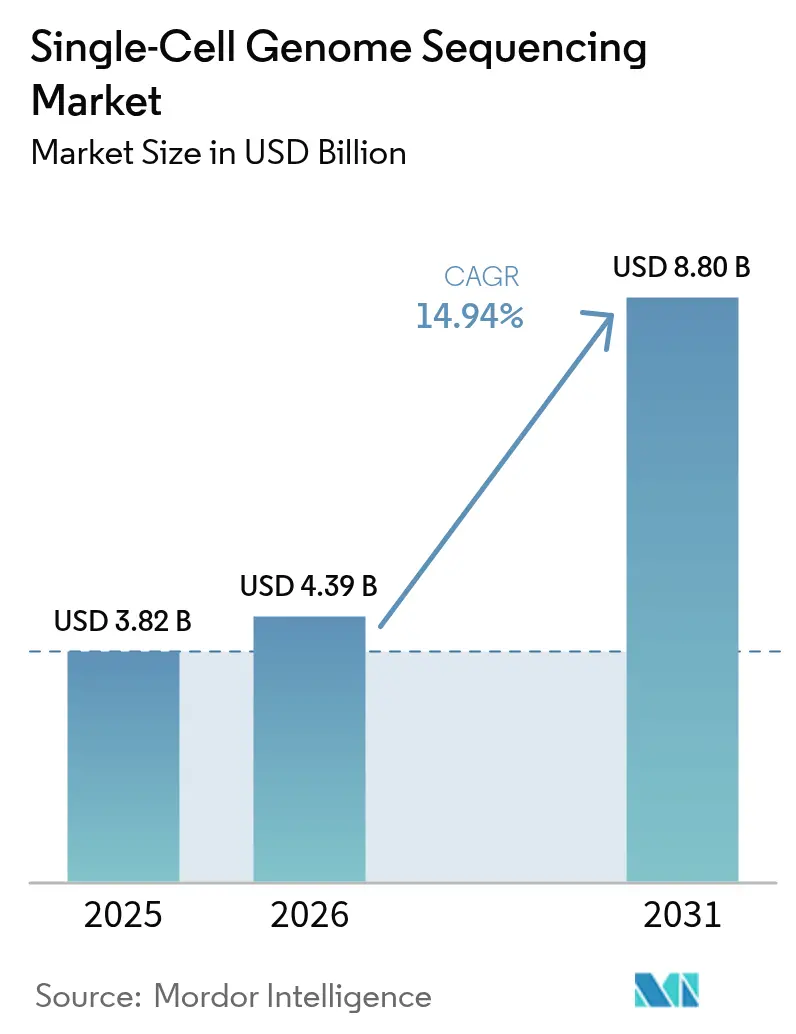

| Market Size (2026) | USD 4.39 Billion |

| Market Size (2031) | USD 8.8 Billion |

| Growth Rate (2026 - 2031) | 14.94% CAGR |

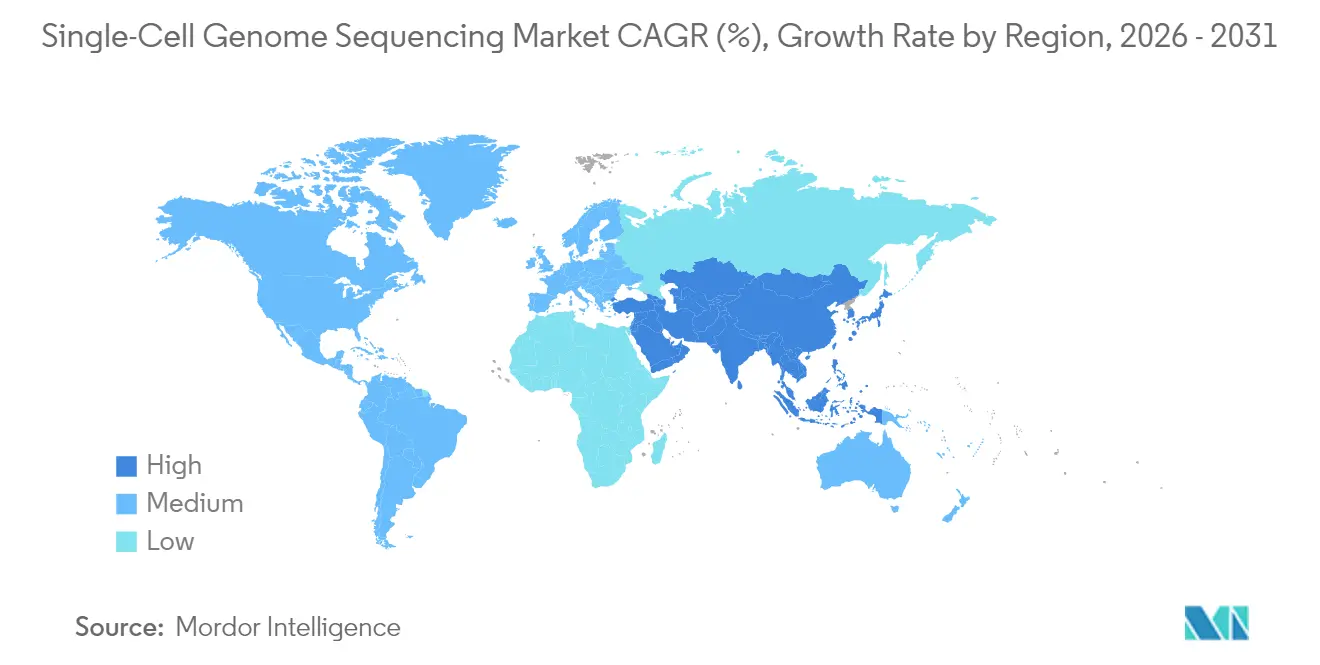

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

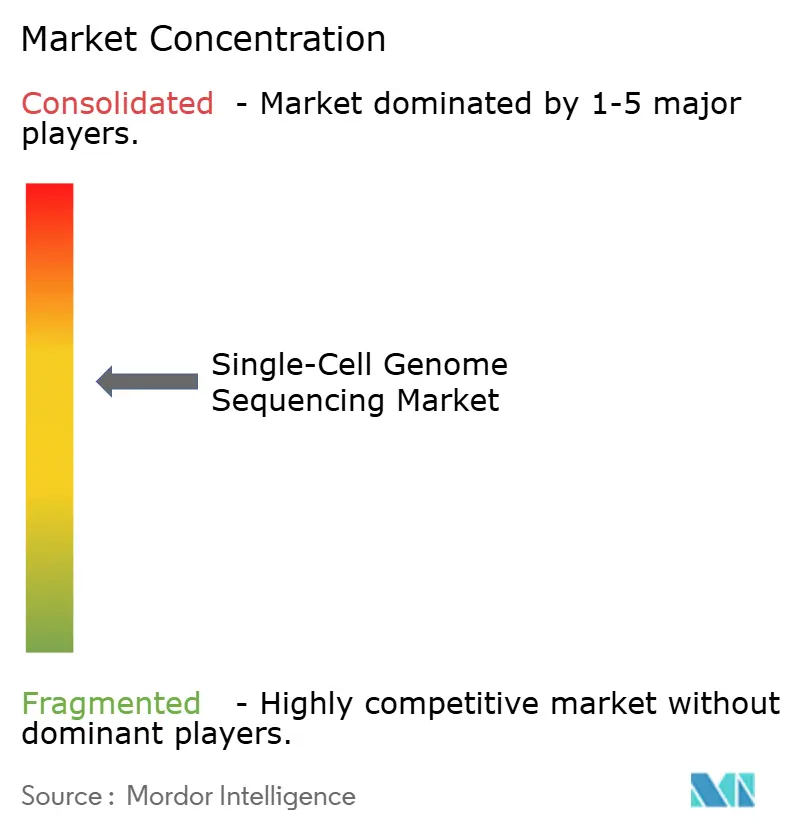

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Single-Cell Genome Sequencing Market Analysis by Mordor Intelligence

The single-cell genome sequencing market size was valued at USD 3.82 billion in 2025 and estimated to grow from USD 4.39 billion in 2026 to reach USD 8.8 billion by 2031, at a CAGR of 14.94% during the forecast period (2026-2031). This momentum is driven by fast-growing precision-oncology workflows, a steep fall in per-base sequencing prices, and chemistry refinements that lift data quality to clinical-grade benchmarks. Consumable demand remains sticky because proprietary microfluidic cartridges and barcoded library kits must be reordered for every run, while the instrument category is set for a capital refresh as benchtop long-read systems lower the entry bar for mid-tier laboratories. Regulatory tailwinds also support the single cell genome sequencing market, notably the U.S. FDA’s 2024 guidance that recommends orthogonal single-cell assays for genome-edited cell therapy characterization.[1]U.S. Food and Drug Administration, “Oncomine Dx Target Test Supplement Approval,” fda.gov Competitive positioning now hinges on end-to-end workflow ownership, with vendors racing to bundle isolation, amplification, sequencing, and bioinformatics into single-invoice offerings that shorten procurement cycles for hospital labs.

Key Report Takeaways

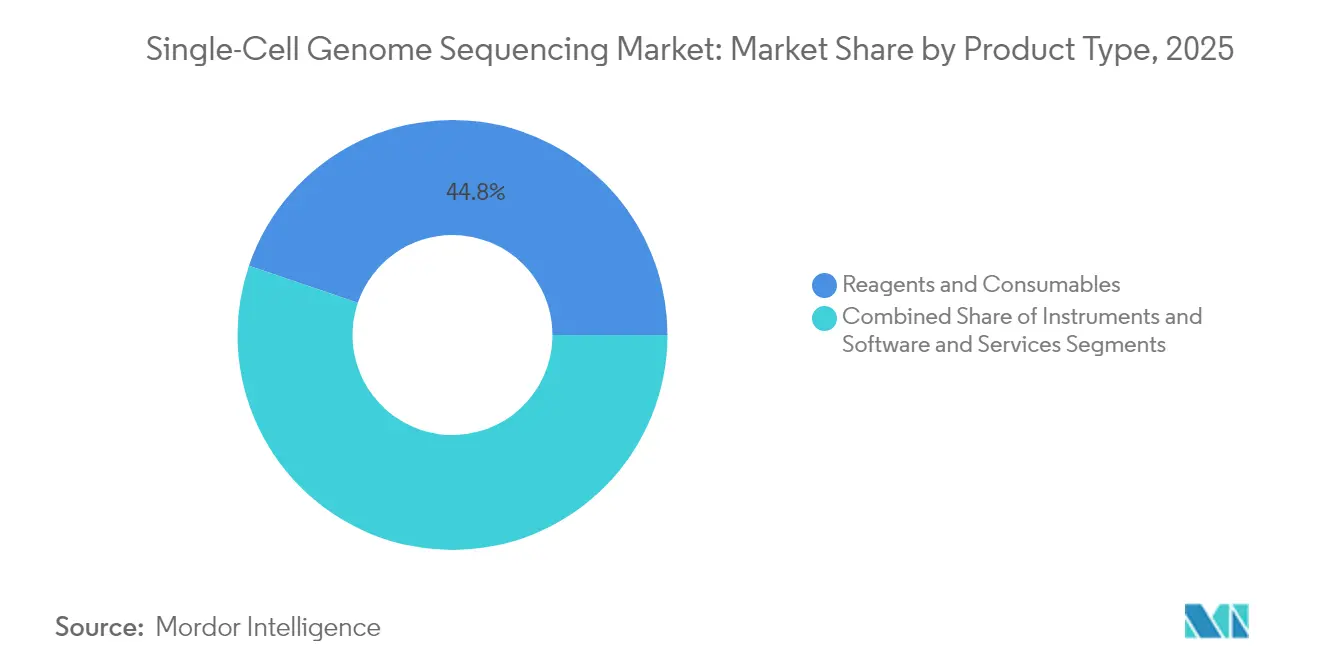

- By product type, reagents and consumables accounted for 44.78% of the single cell genome sequencing market share in 2025, while instruments are projected to register a 16.89% CAGR to 2031.

- By sequencing technology, short-read platforms retained 66.90% share of the single cell genome sequencing market size in 2025; long-read modalities are advancing at an 17.88% CAGR in the forecast window.

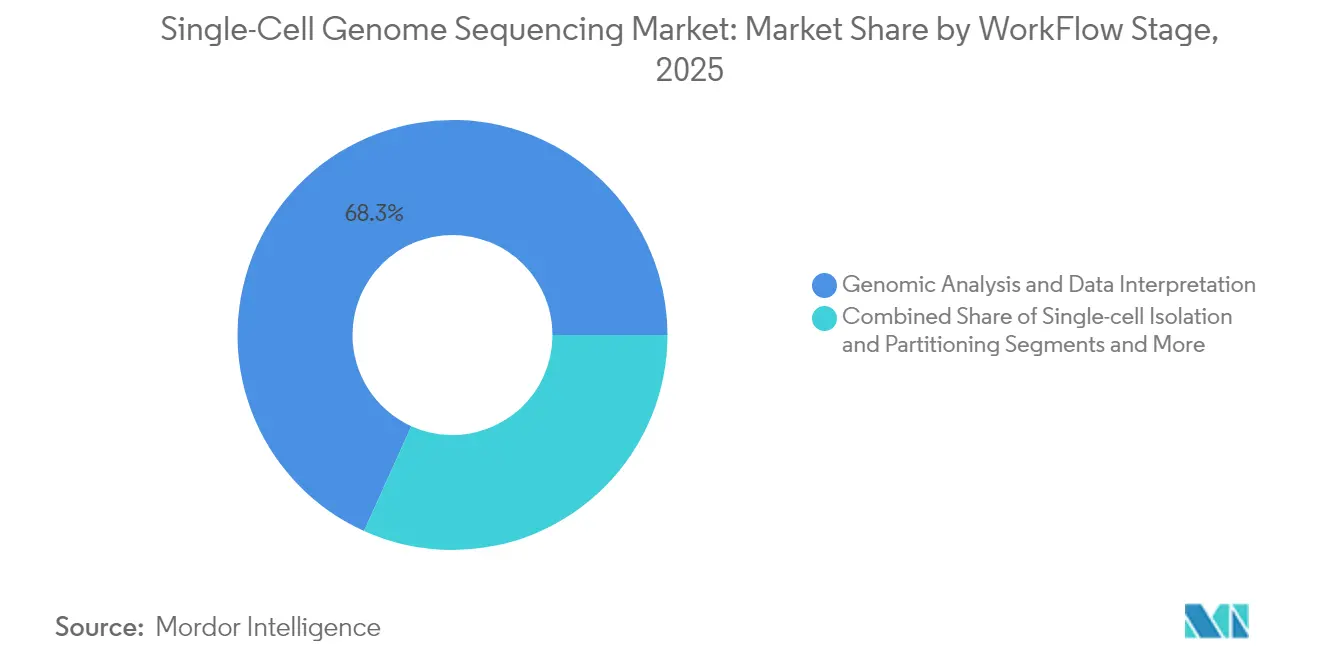

- By workflow stage, genomic analysis and data interpretation represented 68.25% of revenue in 2025 and are growing at a 17.21% CAGR through 2031.

- By application, oncology led with 39.10% revenue share in 2025; immunology and infectious disease are forecast to expand at an 18.05% CAGR through 2031.

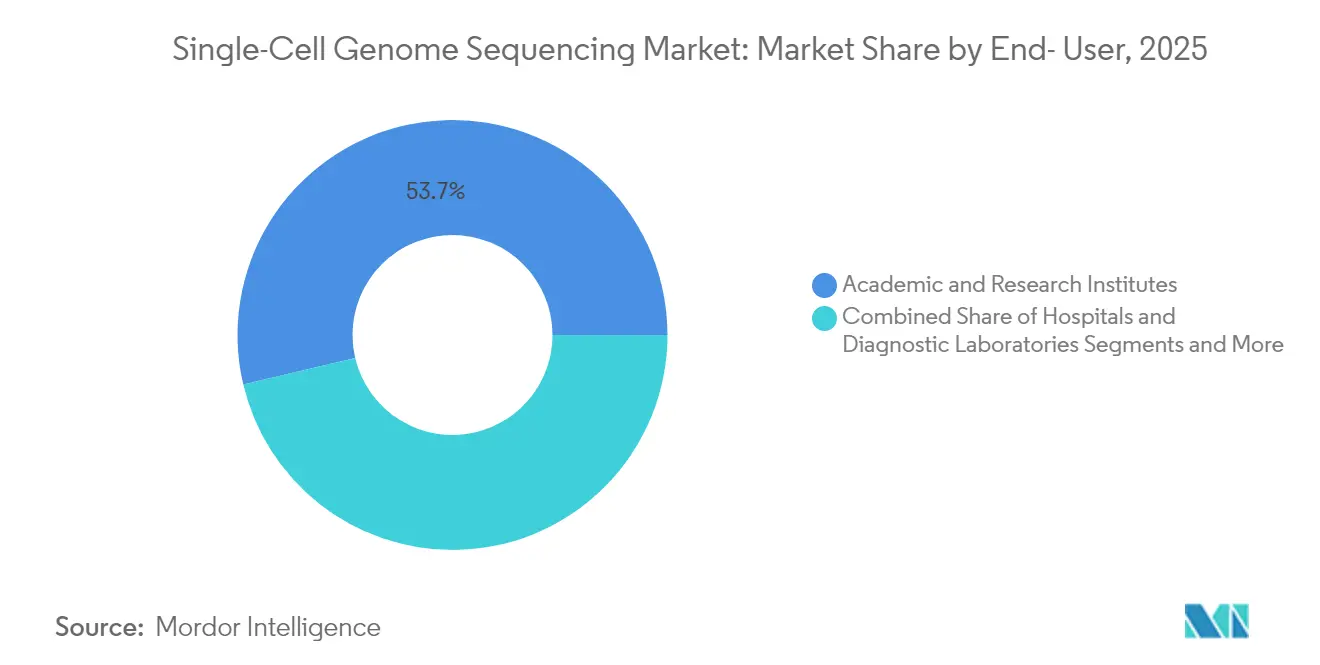

- By end user, pharmaceutical and biotechnology companies are projected to record a 17.12% CAGR through 2031, surpassing academic institutes in incremental spending.

- North America held 43.70% geographic share in 2025; Asia-Pacific is set to grow fastest at a 16.72% CAGR between 2026 and 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Single-Cell Genome Sequencing Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growth in Precision Oncology & Measurable Residual Disease (MRD) Workflows | 3.2% | Global, with early concentration in North America & Western Europe | Medium term (2-4 years) |

| Advances in Single-Cell WGA Chemistry Improving Data Quality | 2.1% | Global, with R&D leadership in North America, manufacturing scale in Asia-Pacific | Long term (≥4 years) |

| Declining Sequencing Costs and Availability of High-Throughput Platforms | 2.8% | Global, accelerated adoption in Asia-Pacific and Latin America | Short term (≤2 years) |

| Expansion of Cell-Atlas and Biobank Initiatives | 1.9% | North America & Europe core, expanding to Asia-Pacific | Long term (≥4 years) |

| Rising Tri-Omics Adoption in CGT Workflows and Translational Research | 2.4% | North America & Europe, with emerging traction in Asia-Pacific pharma hubs | Medium term (2-4 years) |

| Advances in Targeted Long-Read Single-Cell Protocols | 1.8% | Global, with early adopters in academic research institutes | Long term (≥4 years) |

| Source: Mordor Intelligence | |||

Growth in Precision Oncology and MRD Workflows

Minimal residual disease assays now use cell-level variant calling to detect malignant clones at frequencies below 0.01%, a sensitivity that bulk sequencing cannot match. Dana-Farber Cancer Institute and Memorial Sloan Kettering deployed Chromium platforms in 2024 to track clonal evolution in acute lymphoblastic leukemia cohorts, demonstrating clinical utility. FDA approval of a supplemental Oncomine Dx panel in October 2024 legitimized single-cell data in companion diagnostics, accelerating payer reimbursement and pharmaceutical trial adoption. Early MRD detection cuts relapse-associated costs and compresses oncology drug-development timelines, reinforcing spending momentum within the single cell genome sequencing market.

Advances in Single-Cell WGA Chemistry Improving Data Quality

Allelic dropout and GC bias historically limited clinical translation. Takara Bio’s 2024 PicoPLEX update achieved over 95% genome coverage at 30× depth, narrowing the fidelity gap with bulk methods.[2]Takara Bio, “PicoPLEX WGA Kit Performance,” takarabio.com BioSkryb’s primary-template-directed amplification reduced false structural calls by 60% versus legacy MDA kits.[3]BioSkryb Genomics, “Primary Template-Directed Amplification Technology,” bioskryb.com Regulators now reference uniformity metrics in submissions, favoring suppliers that document low-bias chemistries, and further fueling the single cell genome sequencing market.

Declining Sequencing Costs and Availability of High-Throughput Platforms

NHGRI tracked the fall of whole-genome prices below USD 600 in 2024. Illumina’s NovaSeq X Plus pushes 16 terabases per run at USD 2.40 per gigabase. PacBio’s USD 169,000 Vega benchtop system and Oxford Nanopore’s sub-USD 345 PromethION Plus genome target move long-read sequencing into hospital budgets. Lower prices expand the single cell genome sequencing market beyond elite core facilities.

Expansion of Cell-Atlas and Biobank Initiatives

The Human Cell Atlas released 13.5 million reference profiles in 2024, giving researchers baseline variant maps for comparative analyses Tabula Sapiens cataloged 500,000 single-cell genomes across 24 organs, revealing tissue-specific mutational signatures. National biobanks in the U.K., Japan, and South Korea now ensure new samples are single-cell ready, lowering marginal study costs and propelling the single cell genome sequencing market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Per-Sample and Instrument Costs | -1.8% | Global, with acute impact in price-sensitive Asia-Pacific and Latin America markets | Short term (≤2 years) |

| Complex Bioinformatics & Storage Burden | -1.3% | Global, particularly in regions with limited cloud infrastructure | Medium term (2-4 years) |

| Export/Procurement Restrictions Limit Platforms | -0.9% | China, Russia, and select Middle East markets under U.S. export controls | Short term (≤2 years) |

| IP Barriers and Licensing Constraints | -1.1% | Global, with concentrated impact in North America and Europe | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High Per-Sample and Instrument Costs

Per-sample outlays range from USD 500 to USD 2,000, while flagship sequencers list at USD 1 million, deterring smaller centers. Consumables remain pricey because of proprietary cartridge designs, and cloud bioinformatics adds USD 50 to USD 150 per sample. Cost remains a short-term drag on the single cell genome sequencing market.

Complex Bioinformatics and Storage Burden

Each single-cell genome at 30× coverage yields up to 120 gigabytes. Open-source pipelines such as Seurat need scarce expertise, and EU data-sovereignty rules inhibit economical cloud solutions. AWS’s Rainbow pipeline lowered analysis costs below USD 120 in 2024, yet cross-border data transfer constraints hamper universal uptake.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Recurring Consumables Anchor Revenue, Instruments See Capital Refresh

Reagents and consumables captured 44.78% of 2025 revenue, underscoring their recurring nature within the single cell genome sequencing market size context. Proprietary microfluidic cartridges tie every experiment to vendor-specific kits, creating predictable reorder cycles even as instrument placements mature. Instruments are projected to grow at 16.89% CAGR because benchtop long-read systems, like the USD 169,000 Vega, allow mid-cap institutes to buy rather than schedule core-facility time.

Install-base expansion sets a replacement wave in motion, especially in North America where early NovaSeq units near depreciation. Universal library kits from Takara Bio and QIAGEN aim to loosen consumable lock-in, but integrated vendors defend share through lease financing and bundled reagents. Software subscriptions monetize bioinformatics through per-sample fees instead of perpetual licenses, aligning revenue with throughput and supporting long-term cash flow visibility across the single cell genome sequencing market.

By Sequencing Technology: Short-Read Dominance Faces Long-Read Disruption

Short-read platforms held 66.90% share of the single cell genome sequencing market in 2025 on the back of NovaSeq and NextSeq economies. Long-read growth at 17.88% CAGR is fueled by structural-variant detection and haplotype phasing prowess, which short reads cannot match without complex assemblies.

Oxford Nanopore’s PromethION Plus promises sub-USD 345 genomes, while targeted capture methods eliminate whole-genome amplification, improving data fidelity for prenatal genetics and oncology. Regulatory frameworks still evolve for long reads, yet early clinical validations suggest escalating displacement potential within the single cell genome sequencing industry.

By Workflow Stage: Data Interpretation Captures the Greatest Value

Genomic analysis and data interpretation held 68.25% revenue in 2025 and will remain the profit core. Cloud pipelines like AWS Rainbow drop compute charges, but validated clinical software attracts premiums for lowering false-discovery rates.

Partitioning tools commoditize as patents expire, eroding margins for stand-alone cartridge vendors. Chemistry breakthroughs in whole-genome amplification, such as BioSkryb’s PTD protocol, translate directly into higher confidence variant calls and enlarge addressable clinical niches. These dynamics collectively underpin the high-value interpretation tier that defines profitability inside the single cell genome sequencing market.

By Application: Oncology Leads, Immunology Accelerates

Oncology maintained 39.10% revenue share in 2025, driven by MRD detection and clonal evolution tracking. Immunology is poised for an 18.05% CAGR as single-cell immune profiling gains traction in vaccine design and host-pathogen studies. Prenatal and embryo genetics leverage long reads for haplotype phasing without invasive parental sampling, delivering premium per-sample pricing and raising the overall single cell genome sequencing market size in this niche.

Neurology research expands steadily thanks to reference atlases, yet clinical adoption is gated by biopsy constraints. Metagenomics emerges as a precision-infection management tool, using cell-level genomes to select antibiotics when culture fails. Centers for Medicare and Medicaid Services extended coverage to certain single-cell oncology assays in 2024, reinforcing reimbursement foundations for expansion.

By End User: Pharma Outpaces Academia as CGT Workflows Embed Single-Cell QC

Academic institutes still held 53.70% share in 2025, but pharmaceutical and biotechnology users will grow faster at 17.12% CAGR, guided by FDA recommendations that embed orthogonal single-cell QC into gene-edited therapies CROs and CMOs adopt automated tri-omics prep to scale batch release, reinforcing vendor install bases.

Hospitals progress cautiously because bioinformatics staffing is thin, yet flagship centers such as Dana-Farber prove feasibility. Falling run costs coupled with cloud pipelines should lower the barrier, enlarging the clinical slice of the single cell genome sequencing market over the forecast horizon.

Geography Analysis

North America captured 43.70% of revenue in 2025, benefiting from NIH funding and the earliest clinical MRD implementations. The U.S. FDA’s October 2024 approval of single-cell variant calling within Oncomine Dx validated the technology for diagnostics and stimulated hospital procurement. Export controls risk parts shortages, but local manufacturing depth mitigates severe disruption.

Europe leverages cross-border consortia like Human Cell Atlas to share reference datasets, although GDPR hinders economical cloud storage. Spatial-omics adoption at Amsterdam UMC and Charité underscores innovation, yet on-premises compute investment slows roll-out.

Asia-Pacific is the fastest-growing territory at 16.72% CAGR, propelled by Chinese provincial precision-medicine budgets and Japanese pharma embedding single-cell QC in cell-therapy lines. Entity-List restrictions challenge Chinese buyers, motivating accelerated domestic instrument development by MGI Tech.

Middle East and Africa rely on sovereign wealth funding in Gulf states for genomics centers, while Latin American growth remains currency-sensitive. Brazil’s national biobank integrated single-cell protocols in 2024, future-proofing sample assets and broadening regional access to the single cell genome sequencing market.

Competitive Landscape

Illumina, 10x Genomics, and Thermo Fisher Scientific collectively control up to major share of global revenue, giving the single cell genome sequencing market a moderately concentrated profile. Ongoing patent litigation underscores the strategic importance of intellectual property, with 10x Genomics defending partitioning patents and Illumina contesting sequencing chemistry rivals.

Vertical integration shapes strategy: Illumina acquired Fluent BioSciences in July 2024 to internalize upstream library prep, while BioSkryb and Tecan combined automation with tri-omics chemistry in April 2025. Cloud providers now claim bioinformatics value pools; AWS delivers sub-USD 120 per-sample whole-genome analysis, decoupling interpretation from instrument franchises.

Niche specialists exploit white space. Mission Bio focuses on clonal hematopoiesis, and BioSkryb offers ultra-low input WGA for rare cells. Spatial-omics entrants add competitive pressure by retaining tissue context that dissociation loses. Overall differentiation is shifting toward workflow completeness and software ease rather than hardware throughput alone.

Single-Cell Genome Sequencing Industry Leaders

QIAGEN

Illumina, Inc.

F. Hoffmann-La Roche Ltd.

ThermoFisher Scientific, Inc.

Standard BioTools (Fluidigm)

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2025: BioSkryb Genomics and Tecan partnered to automate tri-omics library prep, trimming hands-on time to 90 minutes

- March 2025: Almac Diagnostic Services launched a single-cell RNA-seq offering to expand its biomarker portfolio.

- February 2025: Roche revealed sequencing-by-expansion chemistry that promises ultra-rapid runs for broad applications.

Global Single-Cell Genome Sequencing Market Report Scope

According to the scope, single-cell genome sequencing involves isolating a single cell, performing whole-genome amplification (WGA), constructing sequencing libraries, and then sequencing the DNA using a next-generation sequencer. The Single-cell Genome Sequencing Market is segmented by product type into reagents & consumables, instruments, software & services. By sequencing technology, the market is segmented into short-read NGS, long-read, PCR, microarray, and other enabling technologies. By workflow stage, the market is segmented into single-cell isolation & partitioning, whole genome amplification & library preparation, genomic analysis & data interpretation. By application, the market is segmented into oncology, immunology & infectious disease, prenatal/embryo genetics & reproductive health, neurology & somatic mosaicism, microbiology & metagenomics. By end user, the market is segmented into academic & research institutes, pharmaceutical & biotechnology companies, hospitals & diagnostic laboratories. By geography, the market is segmented into North America, Europe, Asia-Pacific, the Middle East & Africa, and South America. The market report also covers the estimated market sizes and trends for 17 countries across major global regions. The report offers the value (in USD million) for the above segments.

| Reagents & Consumables |

| Instruments |

| Software & Services |

| Short-read NGS |

| Long-read |

| PCR |

| Microarray |

| Other enabling technologies |

| Single-cell isolation & partitioning |

| Whole genome amplification (WGA) & library preparation |

| Genomic analysis & data interpretation |

| Oncology |

| Immunology & Infectious Disease |

| Prenatal/Embryo Genetics & Reproductive Health |

| Neurology & Somatic Mosaicism |

| Microbiology & Metagenomics |

| Academic & Research Institutes |

| Pharmaceutical & Biotechnology Companies |

| Hospitals & diagnostic laboratories |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| Australia | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East & Africa | GCC |

| South Africa | |

| Rest of Middle East & Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Product Type | Reagents & Consumables | |

| Instruments | ||

| Software & Services | ||

| By Sequencing Technology / Platform | Short-read NGS | |

| Long-read | ||

| PCR | ||

| Microarray | ||

| Other enabling technologies | ||

| By Workflow Stage | Single-cell isolation & partitioning | |

| Whole genome amplification (WGA) & library preparation | ||

| Genomic analysis & data interpretation | ||

| By Application | Oncology | |

| Immunology & Infectious Disease | ||

| Prenatal/Embryo Genetics & Reproductive Health | ||

| Neurology & Somatic Mosaicism | ||

| Microbiology & Metagenomics | ||

| By End User | Academic & Research Institutes | |

| Pharmaceutical & Biotechnology Companies | ||

| Hospitals & diagnostic laboratories | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| Australia | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East & Africa | GCC | |

| South Africa | ||

| Rest of Middle East & Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

How large is the single cell genome sequencing market in 2026?

The single cell genome sequencing market size stands at USD 4.39 billion in 2026.

What is the expected CAGR for single-cell sequencing through 2031?

The market is forecast to post a 14.94% CAGR between 2026 and 2031.

Which application is growing fastest?

Immunology and infectious disease applications are projected to grow at an 18.05% CAGR through 2031.

Why are long-read platforms gaining share?

Long reads resolve structural variants and phased haplotypes at single-cell resolution, driving an 17.88% CAGR for long-read technology.

What factor limits adoption in emerging markets?

High per-sample costs of USD 500 to USD 2,000 and capital equipment prices above USD 1 million constrain uptake in price-sensitive regions.

Which region will expand quickest?

Asia-Pacific is set to grow at a 16.72% CAGR thanks to precision-medicine investments in China and Japan.

Page last updated on: