Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

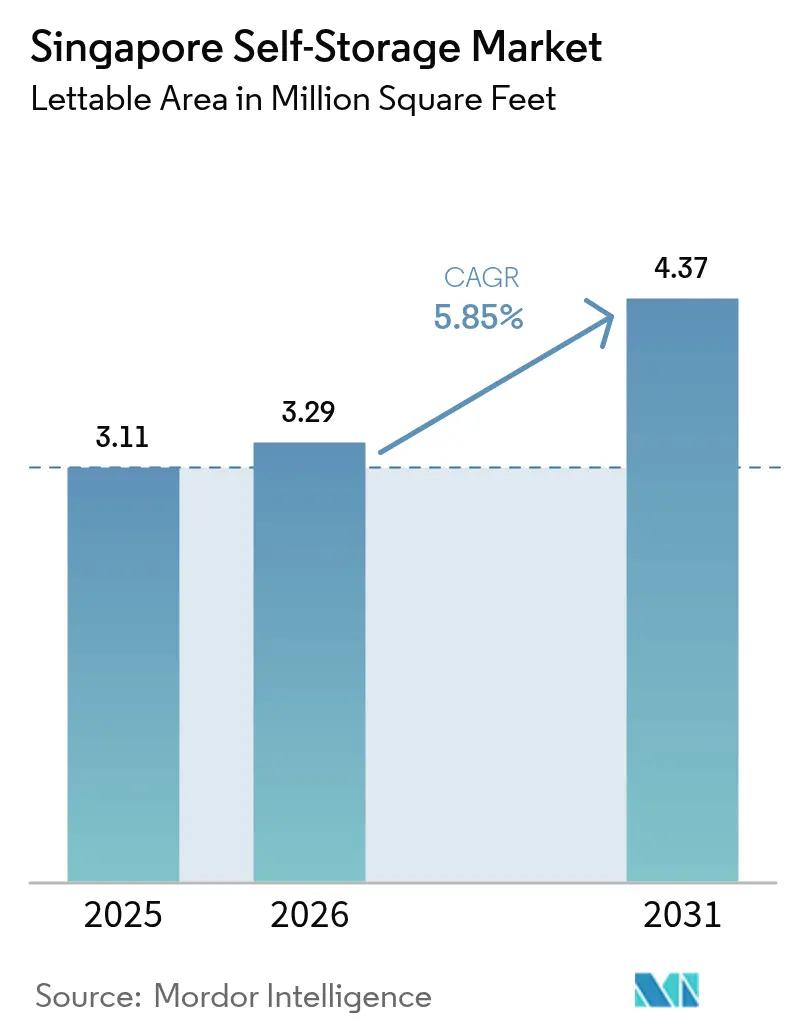

| Base Year Market Size (2025) | 3.11 Million square feet |

| Market Volume (2026) | 3.29 Million square feet |

| Market Volume (2031) | 4.37 Million square feet |

| Growth Rate (2026 - 2031) | 5.85% CAGR |

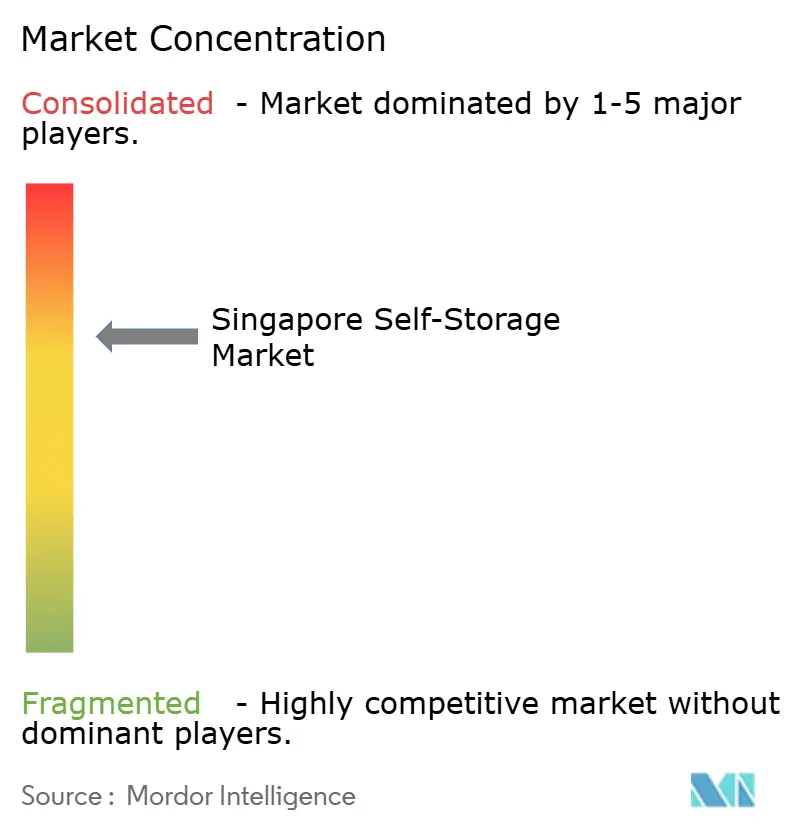

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Singapore Self-Storage Market Analysis by Mordor Intelligence

Singapore Self-Storage market size in 2026 is estimated at 3.29 million sq ft, growing from 2025 value of 3.11 million sq ft with 2031 projections showing 4.37 million sq ft, growing at 5.85% CAGR over 2026-2031. Robust population growth, an affluent consumer base, and intensifying e-commerce activity underpin the momentum. Demand is further reinforced by urban redevelopment that continually shrinks average flat sizes, while institutional capital entering the space accelerates construction of modern, climate-controlled facilities. The Singapore self-storage market also benefits from the government’s regional logistics ambitions, specifically the upcoming RTS Link and second airport logistics park that will expand cross-border flows. Competitive intensity remains moderate as high land costs and stringent Fire-Safety Code rules restrict new entrants, yet incumbents deploy technology and premium services to lift yields.

Key Report Takeaways

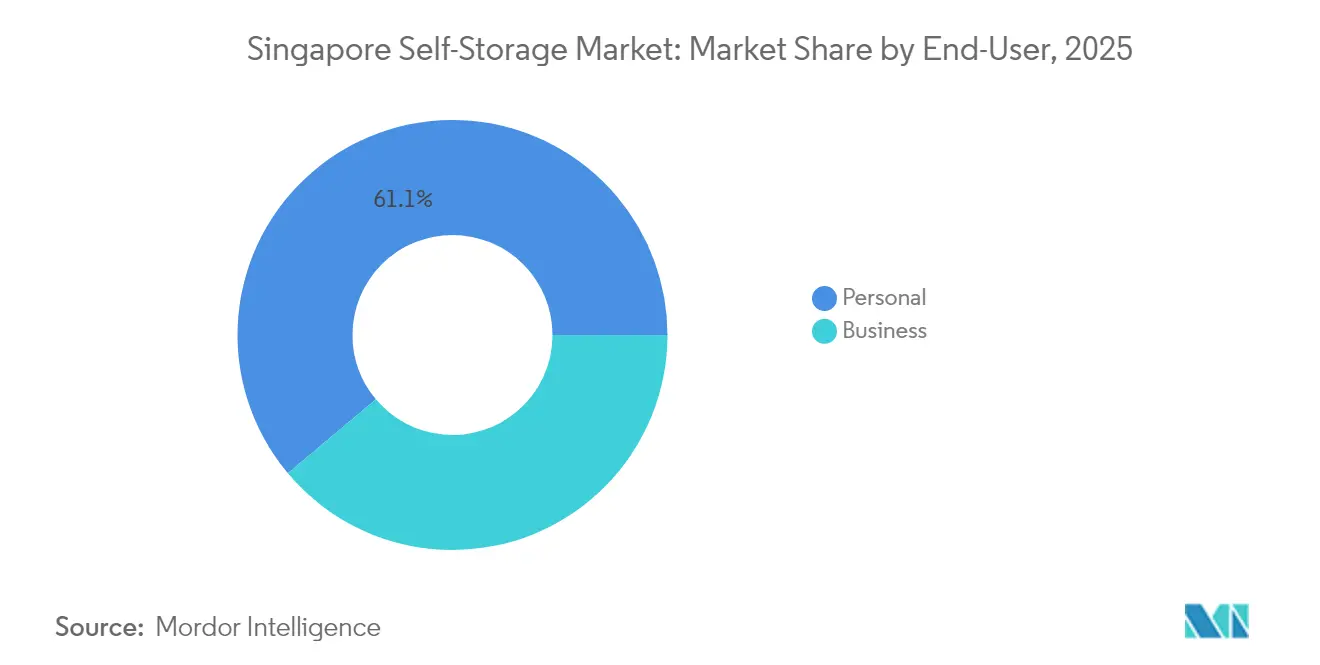

- By end-user, personal storage led with 61.12% of Singapore self-storage market share in 2025; business applications are projected to grow at 7.05% CAGR through 2031.

- By unit size, small and medium units (less than 40 sq ft) held 48.10% share of the Singapore self-storage market size in 2025, while large units (above 40 sq ft) expand fastest at 6.62% CAGR.

- By storage type, non-climate-controlled units accounted for 71.95% of the Singapore self-storage market size in 2025; climate-controlled offerings record the highest 7.19% CAGR.

- By ownership, leased facilities captured 57.30% of Singapore self-storage market share in 2025, whereas owned properties grow at 6.82% CAGR as institutional investors deepen exposure.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Singapore Self-Storage Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High population density and affluent demographics | +1.2% | Singapore national | Medium term (2-4 years) |

| Shrinking residential floor area | +1.5% | Central Region focus | Long term (≥ 4 years) |

| SME and e-commerce micro-fulfilment growth | +1.8% | National, Johor spill-over | Short term (≤ 2 years) |

| Institutional investors’ entry | +0.9% | National | Medium term (2-4 years) |

| Rise of cross-border digital nomads | +0.6% | Central Region | Short term (≤ 2 years) |

| Mandatory Green-Mark retrofit demand | +0.4% | National | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

High Population Density and Affluent Demographics Boost Discretionary Storage Demand

Singapore packs around 8,000 residents into each square kilometer, a figure unmatched in Asia outside of micro-states. Residents rank living-space constraints among their top stressors, and 50% admit shelving household items externally when feasible.[1]StorHub, “StorHub Evolves and Expands to Help Singaporeans Cope With Stress,” storhub.com.sg Rising household incomes support recurring rental fees, while a non-resident population that climbed 5% in 2024 values the flexibility to store possessions between relocations. Vertical city planning, exemplified by 50-storey public-housing blocks, concentrates living yet safeguards livability, indirectly pushing belongings into the Singapore self-storage market. Government programs such as GreenGov.SG further normalize “access over ownership,” nurturing structural demand for paid storage.[2]National Environment Agency, “Public Sector – Energy Efficiency,” nea.gov.sg

Shrinking Residential Floor Area from Urban Redevelopment Projects

Higher plot-ratio allowances in prime districts shrink flat sizes even as total housing stock rises. The 2019 Master Plan rezoning of Tanjong Rhu for 5,000 new homes exemplifies how redevelopment favors compact units. The 1H 2025 Government Land Sales program will introduce 8,505 private units, largely within integrated mixed-use projects.[3]Ministry of National Development, “Government Land Sales 1H 2025,” mnd.gov.sg As older estates undergo en bloc redevelopment, households downgrade in space and compensate by renting self-storage. This trend guarantees a long-run feedstock of consumers for the Singapore self-storage market.

SME and E-commerce Micro-Fulfilment Growth Needing Flexible Inventory Space

Singapore processed 300,000 parcels daily at SingPost’s regional hub after its SGD 30 million upgrade in 2025, triple 2024 capacity. Small sellers on platforms such as Shopee need space beyond home but short of full warehouses. Operators like Spaceship offer “co-warehouse” space bundled with pick-and-pack stations to serve this niche. The upcoming RTS Link will shorten Singapore-Johor turnaround times, prompting merchants to stock inventory in northern facilities for same-day cross-border delivery. These requirements push businesses toward larger, configurable units within the Singapore self-storage market, bolstering volumes and revenue yield.

Institutional Investors’ Entry Improving Funding Access and Build-Out Pace

CapitaLand Investment folded self-storage into its SGD 134 billion portfolio in 2024, validating the asset class for pension and sovereign funds. Deep-pocketed sponsors accelerate new-build pipelines and upgrade existing sites with solar roofs, automated access, and 24/7 surveillance. Cross-border acquisitions, such as StorHub’s AUD 110 million purchase of three Sydney sites, illustrate the scale possible when institutional money enters. Professional managers standardize safety compliance, marketing, and dynamic pricing, lifting overall sector professionalism.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High land costs inflating unit rental rates | -1.8% | Singapore National, acute in Central Region | Long term (≥ 4 years) |

| Limited supply of industrial-zoned land for new facilities | -1.1% | Singapore National | Long term (≥ 4 years) |

| Stringent Fire-Safety Code-2025 raising cap-ex for multilevel facilities | -0.7% | Singapore National | Medium term (2-4 years) |

| Concierge storage start-ups cannibalising traditional unit occupancy | -0.4% | Singapore National, concentrated in Central Region | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

High Land Costs Inflating Unit Rental Rates

Industrial land in core districts commands SGD 20–23 per sq m monthly, a baseline many operators exceed to secure sites JTC. While affluent users absorb higher fees, price-sensitive households may delay adoption or downgrade unit sizes. To maintain occupancy, leading brands offer promotional bundles, StorHub enables two months free rent alongside 30% discounts. Sustained rental inflation therefore tempers the Singapore self-storage market’s longer-term CAGR even as nominal revenue grows.

Limited Supply of Industrial-Zoned Land for New Facilities

Singapore’s land-use hierarchy prioritizes advanced manufacturing and logistics over self-storage. Developers must navigate Green-Mark reviews, environmental impact assessments, and Fire-Safety approvals that prolong timelines and inflate soft costs. Smaller operators lacking patient capital struggle to obtain sites, reinforcing market entry barriers. Adaptive-reuse of under-occupied business parks is a partial solution but often entails expensive retrofits to satisfy compartmentalization and sprinkler mandates. The constrained pipeline limits square-footage expansion even as demand climbs, capping potential supply-side response.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By End-User: Enterprise Adoption Outpaces Personal Uptake

The business segment contributes a 7.05% CAGR to the Singapore self-storage market while personal storage still commands 61.12% share in 2025. Companies favor climate-controlled units and 24/7 access, accepting premium tariffs that elevate revenue per square foot. E-commerce micro-sellers exploit facilities as mini-fulfillment nodes to shorten delivery lead times. Meanwhile, the personal cohort remains a stable volume anchor, driven by apartment downsizing and expatriate churn. Together they sustain broad occupancy, though enterprise clients set the pricing tone through higher service expectations. The Singapore self-storage market size allocated to business users is projected to approach 1.7 million sq ft by 2031, supported by RTS-enabled binational trade flows.

By Storage Size: Large-Unit Uptake Mirrors Logistics Maturity

Small and medium units still account for 48.10% of the Singapore self-storage market size, reflecting individual consumers’ need to stash household overflow. Yet units exceeding 40 sq ft post a 6.62% CAGR as merchants consolidate inventory nearer to end-customers. SingPost’s capacity upgrade lifts parcel volumes, encouraging sellers to stage stock downtown rather than at distant warehouses. Operators respond by reconfiguring upper floors into contiguous blocks that can be subdivided on demand. Large-unit penetration thus signals the market’s shift from pure personal-effects storage to hybrid inventory solutions aligned with omnichannel retail growth.

By Storage Type: Climate-Control Premium Gains Traction

Non-climate-controlled rooms supplied 71.95% of inventory in 2025, yet climate-controlled footprints grow 7.19% annually. Electronics, pharmaceuticals, art, and high-value collectibles deteriorate quickly in 80%+ humidity; enterprises and affluent collectors willingly pay a 15–20% rental premium for controlled environments. StorHub outfits newer sites with solar arrays and energy-efficient HVAC to mitigate power costs and meet Green-Mark targets, keeping margins intact. As climate-control gradually becomes table stakes, operators differentiate via humidity monitoring apps, insurance partnerships, and value-added packing services, embedding stickiness into the Singapore self-storage market.

By Ownership Pattern: Freehold Assets Attract Long-Term Capital

Leased facilities managed 57.30% of space in 2025, but owned properties expand at 6.82% CAGR thanks to institutional appetite. Controlling the underlying real estate shields operators from renewal risk and amplifies equity upside in land-scarce Singapore. CapitaLand’s endorsement has catalyzed similar moves by family offices and REITs seeking stable cash yields. Leasehold models persist for early-stage operators testing micro-markets or occupying upper levels of mixed industrial complexes. The evolution toward ownership deepens the Singapore self-storage industry’s capital pool and encourages higher-spec builds that comply with evolving fire-safety and sustainability codes.

Geography Analysis

The city-state’s compact 728 sq km footprint means every major operator can service the full addressable base, yet micro-location advantages remain decisive. Central Region sites near MRT lines command 20–25% higher rents but fill faster owing to proximity to CBD offices and expatriate enclaves. Suburban estates such as Tampines or Jurong offer larger land parcels, supporting multi-storey complexes with drive-up access. StorHub’s simultaneous roll-out in Serangoon, Tampines, Changi, and Jurong East illustrates a hub-and-spoke model that balances premium rates with volume play.

Northern nodes may experience demand uplift once the RTS Link launches in 2026, enabling 100,000 daily trips between Woodlands and Johor Bahru. SMEs straddling both economies could favor Singapore self-storage market options close to the checkpoint for cross-border inventory splits. Meanwhile, business park under-utilization, International Business Park occupancy stood at 64.4% in 2024, presents adaptive-reuse opportunities, albeit with retrofit costs. Government land-sale priorities will continue to densify residential clusters like Tanjong Rhu, compressing household space and localizing storage demand surges. The second airport logistics park scheduled for the 2030s will attract freight forwarders and e-commerce consolidators, likely lifting climate-controlled unit uptake in Changi precincts. Given uniform national codes, geographic differentiation stems more from access convenience and complementary land-use synergies than from regulatory arbitrage, yet operators adept at micro-site selection should sustain occupancy above 85% across the Singapore self-storage market.

Competitive Landscape

The market supports more than 20 operators, yet the top five collectively hold an estimated 65% share, signaling moderate concentration. StorHub leads on footprint and continuous product refresh, recently launching the Lifestyle brand with digital locks and concierge services. Storefriendly counters with robotics-enabled automated retrieval that compresses aisle width and lifts net lettable area by up to 30%. Spaceship differentiates through co-warehouse offerings that wrap in coworking desks, photography booths, and last-mile tie-ups, a blueprint that appeals to omnichannel merchants.

Institutional funding has triggered cross-border M&A, exemplified by StorHub’s AUD 110 million Wilson Storage purchase and Public Storage’s bid for Abacus Storage King. Capital heft enables portfolio diversification beyond traditional urban cores into mixed-industrial clusters. Barriers remain high: the SCDF Fire Code mandates compartmentalized designs and sprinklers, while BCA Green-Mark pushes energy-efficiency standards requiring upfront capex. Operators that internalize design-build expertise and advanced facility-management systems are best placed to navigate compliance while preserving margins in the Singapore self-storage market.

Technology is an emerging battlefield. App-based unit access, dynamic pricing algorithms, and AI-driven capacity planning differentiate leaders from commodity providers. Yet customer service, 24/7 call centers, multilingual support, integrated insurance, continues to influence tenant stickiness. Over the next five years, the Singapore self-storage industry is likely to witness selective consolidation around tech-forward brands with strong balance-sheets, while niche specialists focus on high-margin verticals such as wine, art, or pharmaceutical storage.

Singapore Self-Storage Industry Leaders

Store Friendly Management Pte Ltd

Spaceship Singapore (Astore Pte. Ltd.)

Store Room Pte Limited

StorHub Self Storage Pte Ltd

Work Plus Store Pte Ltd (“Work+Store”)

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- September 2025: StorHub Group acquired three Wilson Storage facilities in Sydney for AUD 110 million, adding 1,977 units across 1.1 million sq ft.

- June 2025: Public Storage and Ki Corporation issued a non-binding offer to acquire Abacus Storage King for AUD 1.47 per security, covering 126 properties.

- March 2025: SingPost invested SGD 30 million to triple daily parcel throughput to 300,000 at its Regional eCommerce Logistics Hub.

- March 2025: DFI Retail Group divested Cold Storage and Giant chains for SGD 125 million, freeing 2 distribution centers that may convert into storage.

Singapore Self-Storage Market Report Scope

Self-storage facilities give people access to space to rent and store any household or business possessions. Rental agreements for storage space, often known as storage units, are month-to-month agreements. Self-storage allows the user much greater control than full-service storage options, which restrict the customers' access to their possessions and depend on the storage provider to maintain and manage them. The study tracks the key market parameters, underlying growth influencers, and major vendors operating in the industry, which supports the market estimations and growth rates during the forecast period. The study tracks the total lettable area across Singapore. The study provides market trends along with key vendor profiles. The study analyzes the impact of COVID-19 on the ecosystem. The report offers market forecasts and size in volume (square feet) for all the above segments.

By End-User

| Personal |

| Business |

By Storage Size

| Small and Medium Units (less than 40 sq ft) |

| Large Units (above 40 sq ft) |

| Others (Lockers/Double-Stacked) |

By Storage Type

| Climate-Controlled |

| Non-Climate-Controlled |

By Ownership Pattern

| Owned Facilities |

| Leased Facilities |

| By End-User | Personal |

| Business | |

| By Storage Size | Small and Medium Units (less than 40 sq ft) |

| Large Units (above 40 sq ft) | |

| Others (Lockers/Double-Stacked) | |

| By Storage Type | Climate-Controlled |

| Non-Climate-Controlled | |

| By Ownership Pattern | Owned Facilities |

| Leased Facilities |

Key Questions Answered in the Report

How large is the Singapore self-storage market in 2026?

The Singapore self-storage market size stands at 3.29 million sq ft in 2026 and is forecast to reach 4.37 million sq ft by 2031.

What is the expected growth rate of self-storage space in Singapore?

Total rentable space is projected to expand at a 5.85% CAGR between 2026 and 2031.

Which end-user segment is growing fastest?

Business users, driven by SMEs and e-commerce sellers, are expanding at 7.05% CAGR, outpacing personal storage demand.

Why are climate-controlled units gaining popularity?

Singapore’s high humidity damages electronics, documents, and collectibles, so enterprises and affluent consumers pay premiums for controlled environments growing at 7.19% CAGR.

How do high land costs affect pricing?

Central sites incur SGD 20–23 per sq m monthly in baseline rents, forcing operators to charge higher unit fees and offer promotions to maintain occupancy.

Page last updated on: