Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

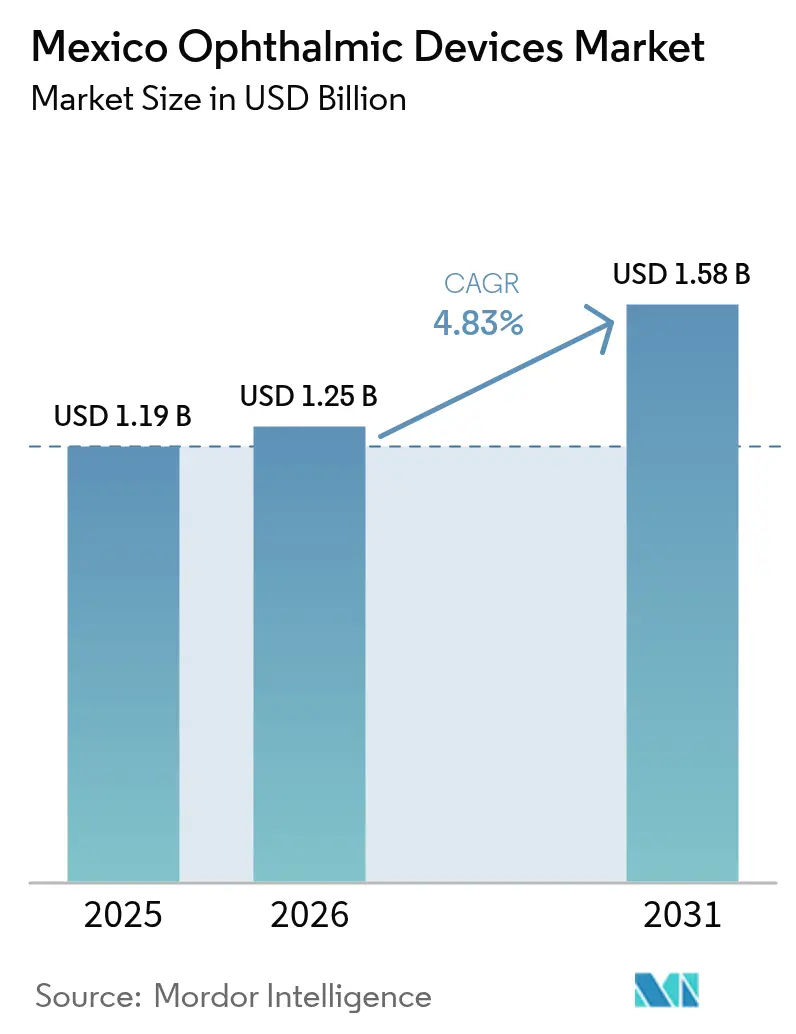

| Base Year Market Size (2025) | USD 1.19 Billion |

| Market Size (2026) | USD 1.25 Billion |

| Market Size (2031) | USD 1.58 Billion |

| Growth Rate (2026 - 2031) | 4.83% CAGR |

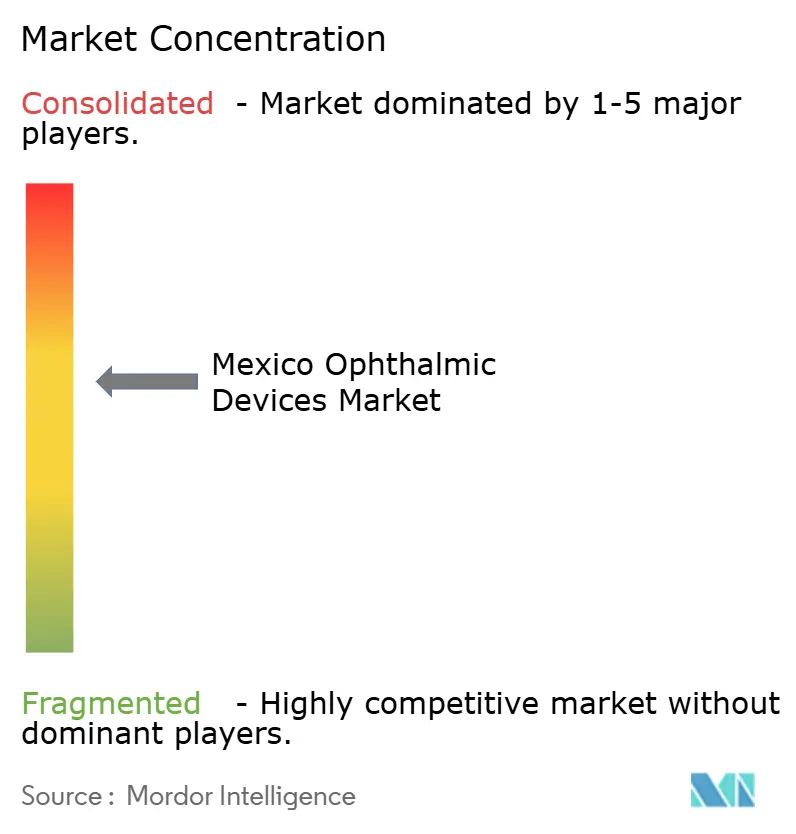

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Mexico Ophthalmic Devices Market Analysis by Mordor Intelligence

Mexico ophthalmic devices market size in 2026 is estimated at USD 1.25 billion, growing from 2025 value of USD 1.19 billion with 2031 projections showing USD 1.58 billion, growing at 4.83% CAGR over 2026-2031. Demand rises as nationwide diabetes screening uncovers sight-threatening complications, while new lens factories shorten import cycles for basic vision products. Refractive errors remain widespread, so retail chains expand fast-fit workshops that deliver prescription eyewear within hours. Artificial-intelligence modules embedded in diagnostic platforms raise reading speed and accuracy, pushing primary clinics to upgrade imaging suites. Urban hospital clusters anchor high-end surgical sales, yet many rural districts still operate below capacity because of limited infrastructure and clinical staff.

Key Report Takeaways

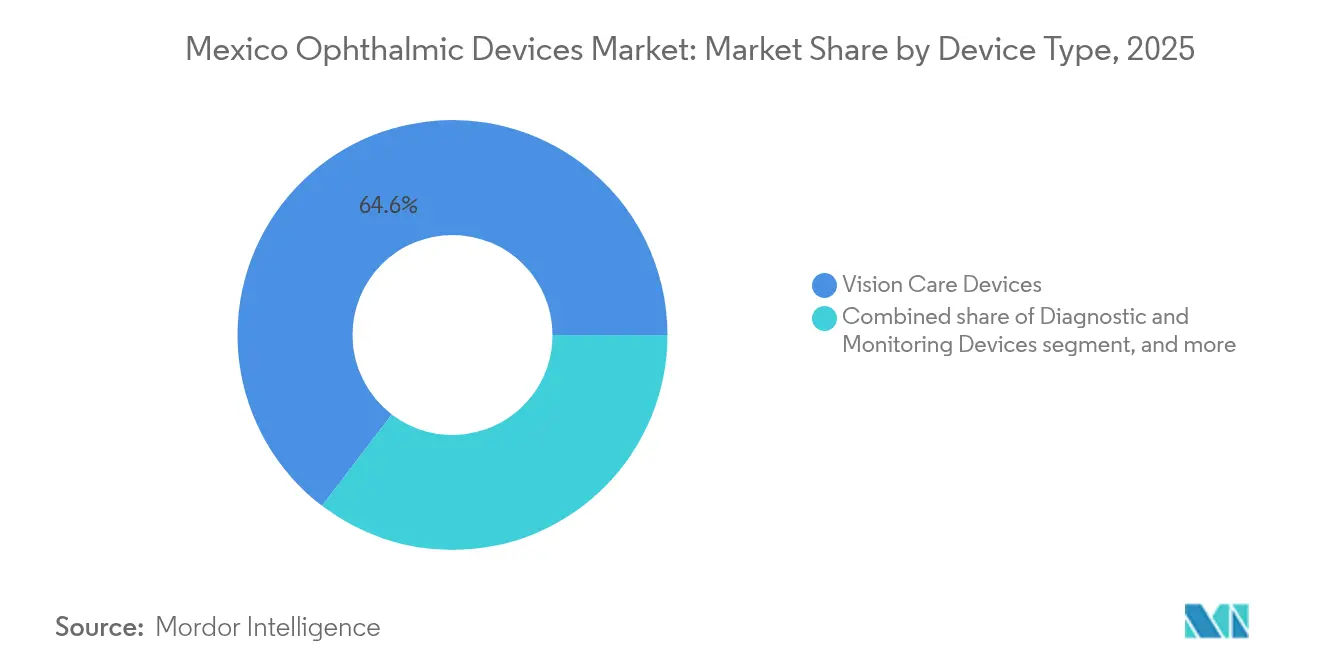

- By device type, vision care held 64.62% of the Mexico ophthalmic devices market share in 2025; diagnostic and monitoring devices are projected to grow at a 6.72% CAGR to 2031.

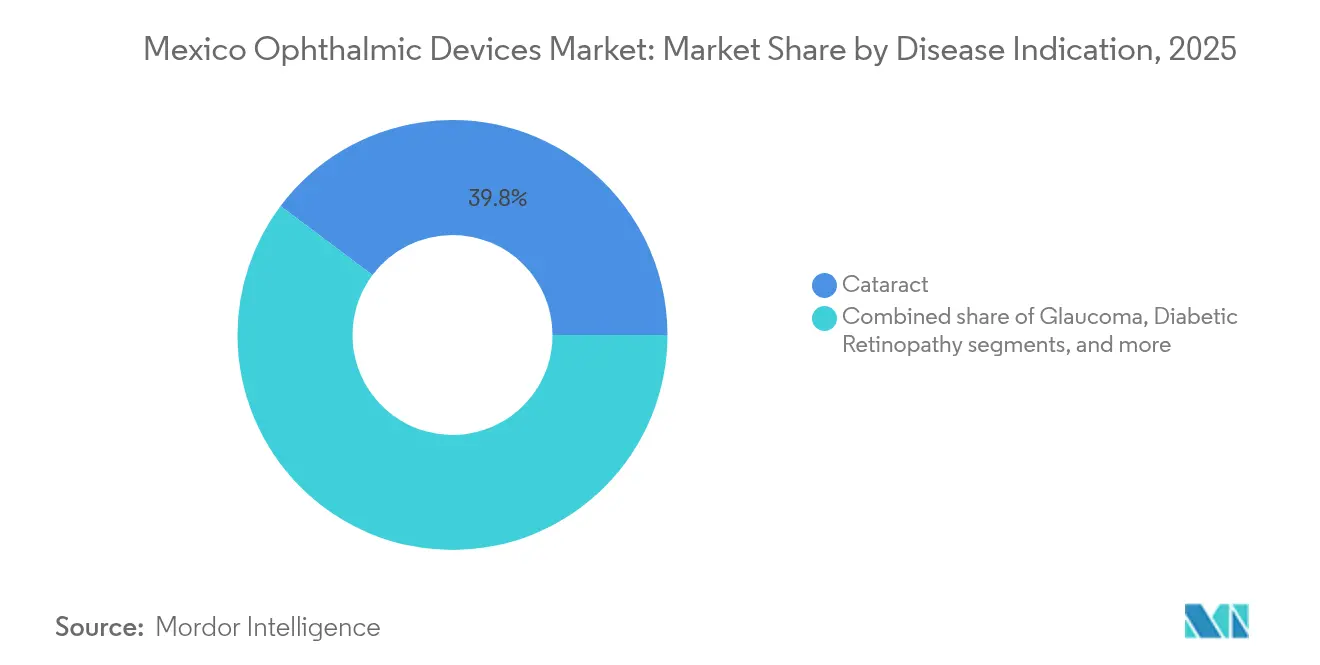

- By disease indication, cataract accounted for a 39.76% share of the Mexico ophthalmic devices market size in 2025, while diabetic retinopathy is set to expand at a 5.93% CAGR through 2031.

- By end-user, hospitals dominated with 45.85% revenue in 2025, whereas ambulatory surgery centers are expected to post a 5.76% CAGR between 2026 and 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Mexico Ophthalmic Devices Market Trends and Insights

Driver Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising prevalence of diabetic retinopathy & age-related cataract | +1.2% | Nationwide | Long term (≥ 4 years) |

| Government “Salud Visual” program boosting surgical volumes | +1.0% | Nationwide | Medium term (2-4 years) |

| Expansion of private ophthalmology chains in urban hubs | +0.8% | Mexico City, Guadalajara, Monterrey | Medium term (2-4 years) |

| Smartphone-driven myopia surge among Mexican youth | +0.6% | Urban school districts | Long term (≥ 4 years) |

| Adoption of femtosecond & SLT lasers post-COFEPRIS approvals | +0.5% | Major surgical centers | Short term (≤ 2 years) |

| Medical-tourism demand for premium IOLs in border states | +0.4% | Baja California, Nuevo León | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Escalating Diabetic Retinopathy Burden

One in three Mexican adults with type 2 diabetes shows retinal damage that requires routine optical coherence tomography and fundus photography[1]Silvia Silva-Tinoco, “Prevalence of Diabetic Retinopathy in Mexican Adults with Type 2 Diabetes,” Investigación Clínica, investigacionclinica.org. Screening efficiency is high, with one positive case detected for every three patients evaluated, a ratio that justifies large equipment orders for public hospitals.

Federal “Salud Visual” and MAS-Bienestar Programs

The national health platform offers free primary eye care, while the “Vive Saludable, Vive Feliz” initiative screens 11 million schoolchildren for refractive errors. Mandatory electronic health records route patients to accredited centers, prompting procurement of interoperable autorefractors and pediatric diagnostic kits.

Expansion of High-Volume Private Ophthalmology Chains

salaUno and similar networks adopt standardized surgical lines that shorten cataract procedure times. High throughput raises demand for phaco machines, microscopes, and single-use consumables, though growth concentrates in urban hubs where disposable incomes are higher.

Smartphone-Related Myopia Surge among Youth

Long daily screen exposure correlates with faster axial length growth, pushing families toward specialty lenses that slow progression. Portable autorefractors accompany school outreach teams, introducing children to on-site vision testing.

Restraints Impact Analysis*

| Restraints Impact Analysis | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Limited reimbursement for premium IOLs & refractive procedures | −0.7% | Nationwide | Medium term (2-4 years) |

| Shortage of trained ophthalmic surgeons in rural regions | −0.5% | Southern & central states | Long term (≥ 4 years) |

| Import tariffs & lengthy COFEPRIS registration timelines | −0.4% | Nationwide | Short term (≤ 2 years) |

| Peso depreciation inflates cost of imported equipment | −0.3% | Nationwide | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Limited Reimbursement for Premium IOLs

Public insurance excludes multifocal and light-adjustable lenses, so patients finance upgrades themselves. A standard cataract intervention costs USD 1,045, which is a heavy burden for many households.

Shortage of Trained Ophthalmic Surgeons

Mexico averages fewer than 10 ophthalmologists per 100,000 inhabitants, with most practicing in major cities[2]Serge Resnikoff, “Global Distribution of Ophthalmologists,” World Health Organization, who.int. Rural hospitals often run modern equipment below capacity because certified specialists are unavailable every day.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Device Type: Vision Care Retains Scale, Diagnostics Gains Speed

Vision care generated 64.62% of overall revenue in 2025 as domestic factories supply low-cost spectacles and contact lenses. EssilorLuxottica’s USD 172 million Tijuana complex fabricates 10 million pairs annually, positioning the plant as a regional export hub Essilorluxottica.com. The Mexico ophthalmic devices market size for vision care is projected at USD 1.01 billion by 2031 alongside a steady replacement cycle.

Diagnostic and monitoring devices record the fastest trajectory with a 6.72% CAGR through 2031. Artificial-intelligence modules inside OCT scanners boost reading accuracy to 88.6%, surpassing early-career clinicians. Government diabetes initiatives add community clinics to the upgrade roster, pushing the Mexico ophthalmic devices market to install compact fundus cameras that upload images to cloud repositories.

By Disease Indication: Cataract Commands Volume, Diabetic Retinopathy Accelerates

Cataract interventions captured 39.76% of 2025 sales, supported by nonprofit caravans that yield 12 pesos in social value for every peso invested. Consumable kits tailored to mobile theaters ensure surgeries proceed despite unstable power supply.

Diabetic retinopathy is the fastest-growing segment with a 5.93% CAGR, reflecting the 33.6% prevalence among adults with type 2 diabetes. Intravitreal anti-VEGF therapy achieves marked visual gains, so demand rises for injectors and high-definition angiography modules.

By End-User: Hospitals Dominate, ASCs Scale Rapidly

Hospitals delivered 45.85% of 2025 revenue because multidisciplinary settings house complex vitreoretinal suites. MAS-Bienestar coverage lifts patient flow, boosting purchases of interoperable slit lamps and ultrasound biometers.

Ambulatory surgery centers grow at a 5.76% CAGR by offering bundled pricing and short waiting lists. Compact, touch-screen phaco consoles fit smaller theaters, allowing quick turnover. Private specialty clinics use cross-subsidy pricing to keep basic cataract fees low while funding premium upgrades.

Competitive Landscape

The Mexico ophthalmic devices market features moderate concentration; the five largest suppliers hold roughly 55% of revenue. EssilorLuxottica enjoys vertical integration across lens blanks, coatings, and retail distribution, ensuring stable margins even in price-sensitive tiers. Alcon posts 12% vision-care and 5% surgical growth for 2024, underpinned by the CENTURION phaco system and DAILIES contact lenses. Johnson & Johnson Vision differentiates through the iDesign Refractive Studio, which fuses topography and wavefront analysis to improve LASIK accuracy.

Specialist chains such as salaUno replicate lean surgical lines inspired by India’s Aravind model, achieving high cataract throughput while maintaining affordable fee structures. Domestic assemblers supply value-priced slit lamps and autorefractors to independent optometrists, rebranding Chinese OEM hardware under local trademarks. Venture capital activity signals future consolidation, with enterprise contracts likely to shift procurement toward cloud-linked inventory hubs.

Technology partnerships matter more each year. AI developers align with imaging firms to integrate on-device analytics that flag pathology in real time, shortening reading cycles in busy clinics. Training alliances between equipment makers and teaching hospitals supply fellowships and simulation labs that familiarize residents with proprietary platforms early in their careers.

Mexico Ophthalmic Devices Industry Leaders

Alcon Inc

Nidek Co. Ltd

Johnson & Johnson

Essilor International SA

Carl Zeiss Meditec AG

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2025: Alcon released its 2024 Sustainability and Social Impact Report highlighting USD 9.8 billion net sales and seven upcoming device innovations.

- March 2025: IMSS launched “Vive Saludable, Vive Feliz,” screening 11 million schoolchildren and tendering portable vision screeners.

- October 2024: The American Academy of Ophthalmology presented study results showing USD 1 cost 3-D-printed adjustable eyeglasses improved vision for children in Ensenada.

- January 2024: EssilorLuxottica inaugurated USD 172 million lens facilities in Tijuana, adding 2,000 jobs and 10 million extra pairs of annual capacity.

Mexico Ophthalmic Devices Market Report Scope

The term 'ophthalmic devices' refers to devices used in ophthalmic diagnostics, monitoring, and ophthalmic surgeries, along with devices used for vision correction, such as contact lenses. The Mexico Ophthalmic Devices Market is segmented by Devices (Surgical Devices (Glaucoma Drainage Devices, Glaucoma Stents and Implants, Intraocular Lenses, Lasers, and Other Surgical Devices), Diagnostic and Monitoring Devices (Autorefractors and Keratometers, Corneal Topography Systems, Ophthalmic Ultrasound Imaging Systems, Ophthalmoscopes, Optical Coherence Tomography Scanners, and Other Diagnostic & Monitoring Devices), Vision Correction Devices (Spectacles and Contact Lenses). The report offers the value (In USD Million) for the above segments.

By Device Type

| Diagnostic & Monitoring Devices | OCT Scanners |

| Fundus & Retinal Cameras | |

| Autorefractors & Keratometers | |

| Corneal Topography Systems | |

| Ultrasound Imaging Systems | |

| Perimeters & Tonometers | |

| Other Diagnostic & Monitoring Devices | |

| Surgical Devices | Cataract Surgical Devices |

| Vitreoretinal Surgical Devices | |

| Refreactive Surgical Devices | |

| Glaucoma Surgical Devices | |

| Other Surgical Devices | |

| Vision Care Devices | Spectacles Frames & Lenses |

| Contact Lenses |

By Disease Indication

| Cataract |

| Glaucoma |

| Diabetic Retinopathy |

| Other Disease Indications |

By End-user

| Hospitals |

| Specialty Ophthalmic Clinics |

| Ambulatory Surgery Centers (ASCs) |

| Other End-users |

| By Device Type | Diagnostic & Monitoring Devices | OCT Scanners |

| Fundus & Retinal Cameras | ||

| Autorefractors & Keratometers | ||

| Corneal Topography Systems | ||

| Ultrasound Imaging Systems | ||

| Perimeters & Tonometers | ||

| Other Diagnostic & Monitoring Devices | ||

| Surgical Devices | Cataract Surgical Devices | |

| Vitreoretinal Surgical Devices | ||

| Refreactive Surgical Devices | ||

| Glaucoma Surgical Devices | ||

| Other Surgical Devices | ||

| Vision Care Devices | Spectacles Frames & Lenses | |

| Contact Lenses | ||

| By Disease Indication | Cataract | |

| Glaucoma | ||

| Diabetic Retinopathy | ||

| Other Disease Indications | ||

| By End-user | Hospitals | |

| Specialty Ophthalmic Clinics | ||

| Ambulatory Surgery Centers (ASCs) | ||

| Other End-users | ||

Key Questions Answered in the Report

What is the current value of the Mexico ophthalmic devices market?

The market stands at USD 1.25 billion in 2026 and is forecast to reach USD 1.58 billion by 2031 at a 4.83% CAGR.

Which device category leads revenue?

Vision care devices contribute 64.62% of 2025 revenue, buoyed by high demand for cost-effective spectacles and contact lenses.

Why is diabetic retinopathy an important growth area?

A 33.6% prevalence among adults with type 2 diabetes drives sustained demand for OCT scanners, fundus cameras, and intravitreal therapy systems.

How are government programs influencing demand?

MAS-Bienestar and IMSS school screenings enlarge patient pipelines, pushing hospitals and clinics to acquire diagnostic and pediatric devices.

What limits adoption of premium intraocular lenses?

Public insurance excludes multifocal and light-adjustable lenses, so high out-of-pocket costs confine uptake to affluent urban patients.

Where are investment opportunities strongest?

Diagnostic devices with AI support, ambulatory surgery centers, and rural outreach platforms offer the fastest growth potential through 2030.

Page last updated on: