Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

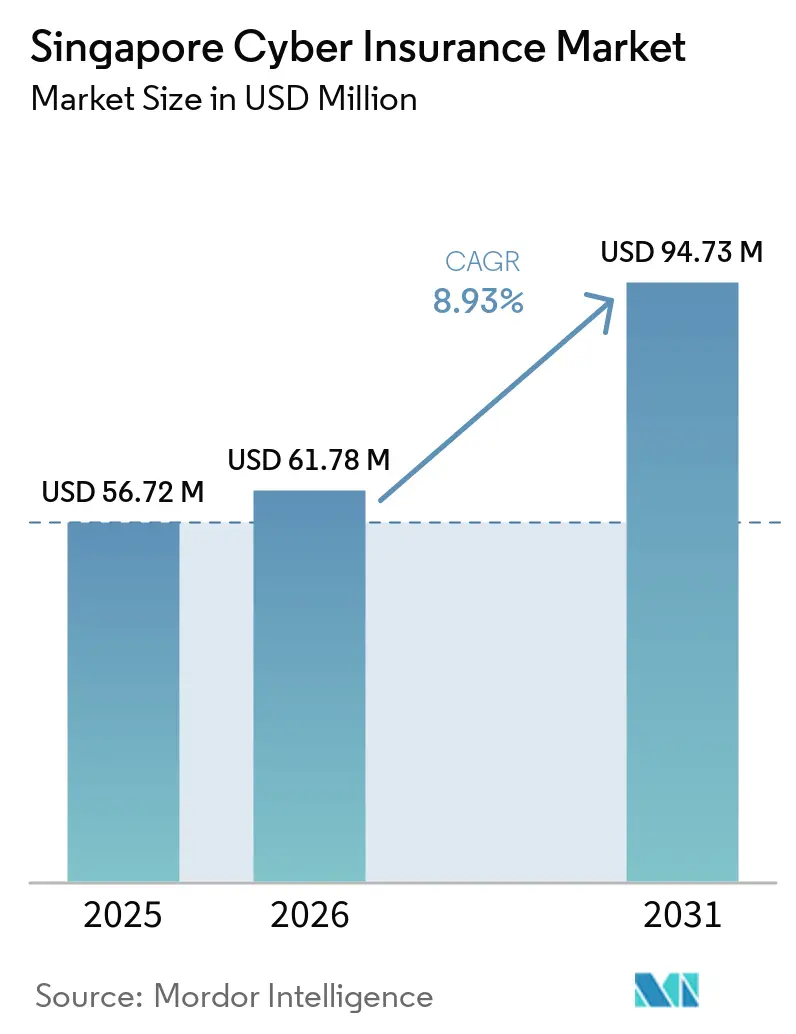

| Base Year Market Size (2025) | USD 56.72 Million |

| Market Size (2026) | USD 61.78 Million |

| Market Size (2031) | USD 94.73 Million |

| Growth Rate (2026 - 2031) | 8.93% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Singapore Cyber Insurance Market Analysis by Mordor Intelligence

The Singapore Cyber Insurance Market size is expected to grow from USD 56.72 million in 2025 to USD 61.78 million in 2026 and is forecast to reach USD 94.73 million by 2031 at 8.93% CAGR over 2026-2031.

Heightened regulatory scrutiny, growing ransomware losses, and the world-first ASEAN cyber-risk pool position Singapore as a regional test bed for innovative capacity expansion measures. The Shared Responsibility Framework that came into force in December 2024 imposes explicit anti-phishing duties on banks and telecom operators, pushing many firms to expand cover beyond traditional policies[1]Monetary Authority of Singapore, “Shared Responsibility Framework Consultation Paper,” mas.gov.sg. Fines totaling SGD 102,000 in May 2024 under the Personal Data Protection Act underscore the cost of non-compliance and increase the urgency of incident response coverage. Rising adoption of generative AI raises deepfake and data-poisoning exposures, prompting the government to commit SGD 20 million for detection technologies, which in turn fuels demand for bespoke policy wordings that address emerging threats.

Key Report Takeaways

- By product type, stand-alone policies held 53.65% of the Singapore cyber insurance market share in 2025, while the same segment is forecast to expand at 9.84% CAGR through 2031.

- By enterprise size, large enterprises accounted for 62.75% share of the Singapore cyber insurance market size in 2025; small and micro enterprises represent the fastest-growing band with a 9.46% CAGR to 2031.

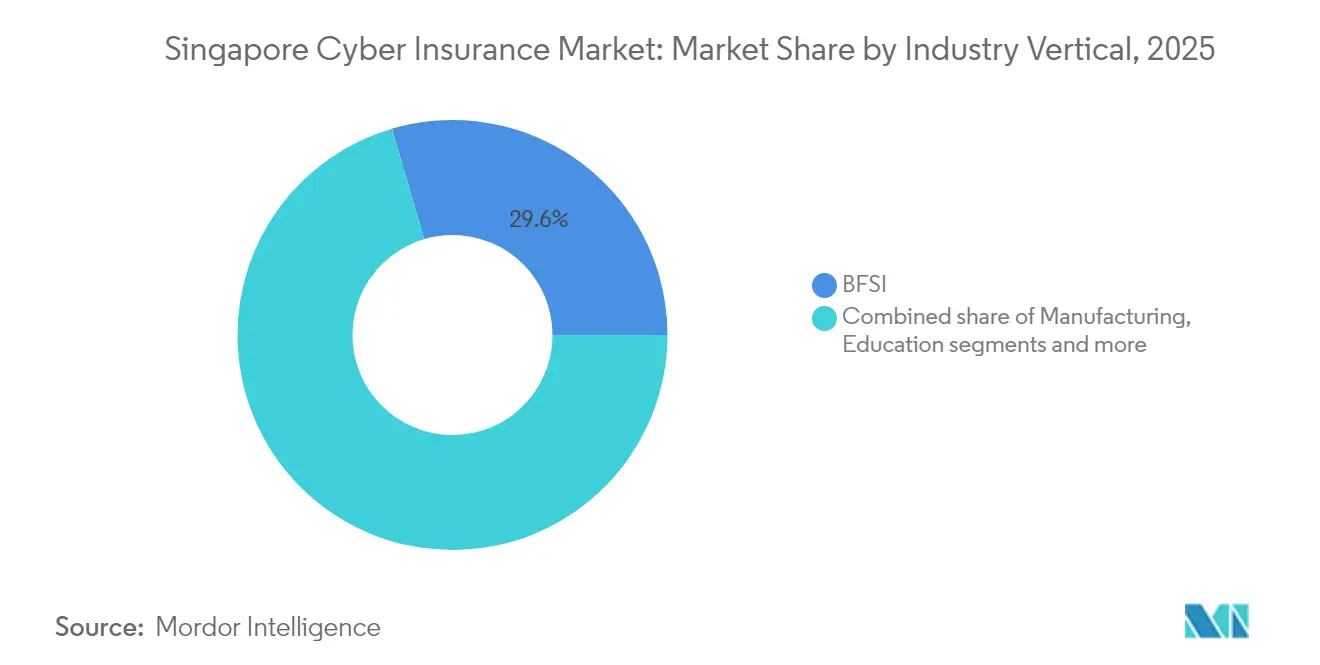

- By industry vertical, the BFSI sector led with 29.55% of the Singapore cyber insurance market share in 2025, whereas retail and e-commerce are projected to advance at a 10.22% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Singapore Cyber Insurance Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| PDPA & Cybersecurity Act breach-reporting mandates | +2.1% | Singapore with ASEAN spillover | Medium term (2-4 years) |

| Surge in ransomware frequency & costs | +1.8% | Global focus on Singapore finance | Short term (≤2 years) |

| SME cyber-hygiene programmes (Cyber Essentials, DEB) | +1.4% | Singapore pilot for region | Medium term (2-4 years) |

| Increasing capacity via Singapore Cyber-Risk Pool & ILS | +1.2% | ASEAN core, Singapore hub | Long term (≥4 years) |

| Gen-AI deepfake social-engineering escalation | +1.6% | Early impact on Singapore finance | Short term (≤2 years) |

| Government procurement cyber thresholds | +0.9% | Singapore influence on region | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

PDPA & Cybersecurity Act Breach-Reporting Mandates

Regulatory enforcement is a strong growth catalyst. The Personal Data Protection Commission can fine up to 10% of annual turnover, a ceiling that compels firms to treat cyber insurance as essential rather than discretionary[2]National Law Review Editors, “Singapore PDPC Enforcement Highlights,” natlawreview.com. Breach notification within three calendar days for incidents affecting 500 or more individuals creates operational urgency that aligns neatly with incident response endorsements. Amendments to the Cybersecurity Act widened the definition of critical information infrastructure, pulling more technology and logistics operators under direct supervision[3]Asia Insurance Review Staff, “CSA Records Rise in Ransomware Cases,” asiainsurancereview.com. Recent undertakings involving vendor lapses emphasize supply-chain diligence, a risk that underwriters now scrutinize during proposal assessment. Extraterritorial provisions extend to any entity processing Singapore residents’ data, broadening the potential client pool beyond domestic registrants. As penalties climb, firms increasingly seek policies that cover regulatory investigations, legal defense, and notification costs.

Surge in Ransomware Frequency & Costs

The Cyber Security Agency logged 132 ransomware cases in 2023, with double and triple extortion tactics now commonplace. The Toppan Next Tech breach spilled over to DBS Group and Bank of China customers, illustrating how a vendor incident can cascade across an entire financial ecosystem. Income Insurance’s DataPost event exposed personal details of 146 policyholders, underlining the persistence of supply-chain risk. QBE research predicts global incidents will double compared with 2020 levels, reinforcing premium momentum as loss ratios rise. Attackers commercialize ransomware-as-a-service kits, lowering technical barriers and expanding the pool of adversaries. This evolving threat landscape strengthens the value proposition of cyber insurance bundled with pre-breach security services.

SME Cyber-Hygiene Programmes (Cyber Essentials, DEB)

Government schemes cut adoption barriers for small firms. Cyber Essentials supplies step-by-step controls and partial funding, while the Digital Enterprise Blueprint frames broader digital-risk standards. The SME Policy Index places Singapore at the top end for digital readiness in Southeast Asia, signaling fertile ground for penetration growth. Delta Insurance partnered with Stone Forest to wrap affordable cover around managed security services in a bid to match underwriting with simplified risk scoring. Public procurement rules now require cybersecurity attestations, nudging suppliers toward insurance to back contractual obligations. QBE surveys show that one-third of local businesses still lack incident response playbooks, indicating untapped demand once awareness meets affordable premiums.

Increasing Capacity via Singapore Cyber-Risk Pool & ILS

The ASEAN cyber-risk pool pledges up to USD 1 billion, marrying traditional reinsurance with insurance-linked securities and providing headroom for systemic events. MS Amlin’s Phoenix Re sidecar climbed to USD 90 million for the 2025 treaty year, a sign of healthy investor appetite for Asian cyber risk. Cyber catastrophe bonds reached USD 575 million outstanding in 2024, with issuance supported by Singapore’s Special Purpose Reinsurance Vehicle regime and tax grants that run through 2025. Willis Towers Watson’s CyCore Asia facility allocates USD 15 million exclusively to Singapore and Hong Kong exposures, solidifying the city-state’s hub status. These initiatives temper price volatility by attracting capital markets capacity and enable broader wordings that cover cloud-outage and network-security failures.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High premiums & stringent underwriting for SMEs | -1.7% | Singapore and wider ASEAN SMEs | Medium term (2-4 years) |

| Limited local loss/claims data for actuarial pricing | -1.3% | Singapore with regional spillover | Long term (≥4 years) |

| Rate-softening threatens policy sustainability | -1.1% | Global with local competition | Short term (≤2 years) |

| War / systemic-event exclusions & supply-chain caps | -0.8% | Global geopolitical hotspots | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High Premiums & Stringent Underwriting for SMEs

Smaller firms often view cyber cover as too expensive relative to cash flow. Traditional underwriting protocols mirror enterprise-grade security checklists and insist on multi-factor authentication, patch cadence reports, and incident rehearsals that exceed SME resources. Cyber Sierra raised USD 4.3 million to automate assessments and lower acquisition cost, yet its SGD 232,000 2023 revenue shows market infancy[4]Tracxn Technologies, “Cyber Sierra Company Profile,” tracxn.com. Government vouchers partially defray costs, but sticker shock still delays purchase decisions.

Limited Local Loss/Claims Data for Actuarial Pricing

Insurers rely on global datasets that may overlook Singapore-specific nuances. The tightly connected financial and logistics sectors amplify cascade losses from a single vendor breach, yet few historical claims quantify such spillover. Lack of granular data forces underwriters to add safety-loadings, which in turn pushes rates upward and dampens demand. PDPC enforcement trends are still maturing, limiting predictive modeling of regulatory fines. Industry working groups are advocating anonymized loss sharing to improve rate adequacy without exposing sensitive client information.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Stand-Alone Policies Drive Sophisticated Coverage

Stand-alone covers commanded 53.65% of the Singapore cyber insurance market share in 2025 and are forecast to grow at a 9.84% CAGR, underscoring the shift toward bespoke wordings that address regulatory investigations, cloud outages, and AI-related liabilities. Enterprises favor these policies because packaged extensions rarely match the breadth of protection required for cross-border data flows. AXA XL’s 2024 Gen-AI endorsement, which protects against data poisoning and IP violations, exemplifies the innovation pace within the stand-alone space. Brokers report rising demand for supply-chain failure and reputational harm clauses that provide fixed payouts after defined triggers. This appetite accelerates as multinational clients integrate Singapore operations into global cyber towers.

Packaged add-ons, which held a 46.35% share, still appeal to smaller businesses entering the market for the first time. These buyers often transition to stand-alone forms once compliance audits highlight exclusion gaps. Over time, stand-alone penetration is expected to raise the overall Singapore cyber insurance market size by broadening coverage scopes and deepening policy limits. New parametric proposals tied to cloud downtime aim to simplify claims and are piloted within the stand-alone arena. Product designers also explore endorsements for quantum-resistant encryption failure, a forward-looking risk relevant to Singapore’s advanced tech ecosystem.

By Enterprise Size: Large Enterprises Lead, SMEs Accelerate

Large enterprises held 62.75% of the Singapore cyber insurance market size in 2025, reflecting their mature risk governance and mandatory compliance with sectoral regulations. These organizations purchase layered towers that bundle forensic services, PR support, and business interruption modules. Medium enterprises are increasingly adopting similar structures as digital value chains extend beyond headquarters, a dynamic that pushes underwriters to calibrate sub-limits to revenue scale. Government contractors must now demonstrate cyber readiness, a rule that converts many mid-market suppliers into first-time buyers.

Small and micro enterprises, while only a minority of premium today, represent the fastest-growing cohort at 9.46% CAGR through 2031. Programs such as Cyber Essentials lower technical thresholds and subsidize basic tooling, simplifying proposal completion. Insurtech platforms that embed questionnaires into accounting or HR software shorten the buying process and reduce distribution costs. Wider SME participation diversifies the risk pool and smooths premium swings for the Singapore cyber insurance market, an outcome welcomed by reinsurers seeking balanced portfolios.

By Industry Vertical: BFSI Dominance, Retail Acceleration

The BFSI sector accounted for 29.55% of the Singapore cyber insurance market share in 2025, driven by stringent MAS Technology Risk Management guidelines and high valuations of digital customer assets. Institutions often require limits that surpass USD 100 million and include broad social-engineering cover. The Shared Responsibility Framework that directs banks to absorb scam losses unless due diligence proofs shift liability is another tailwind for limit expansion. High-frequency penetration testing and zero-trust architecture enable insurers to differentiate pricing among banks based on observable controls.

Retail and e-commerce currently occupy a smaller slice but are the fastest-growing vertical at 10.22% CAGR. Escalating digital-payment usage and anti-fraud chargeback regulations mean merchants carry new liabilities that standard property or casualty products ignore. Underwriters now examine tokenization implementation, PCI-DSS compliance, and vendor access controls when rating this segment. Healthcare, manufacturing, and education clusters also contribute to the overall Singapore cyber insurance market size, but each poses unique threat pathways, such as connected medical devices or industrial IoT. Tailored endorsements and sector-specific breach coaches help insurers respond to these divergent needs.

Geography Analysis

Singapore anchors the domestic opportunity, and the city-state alone accounts for the entire USD 61.78 million Singapore cyber insurance market size in 2026, with buyers concentrated in finance, technology, and logistics. Mandatory breach-notification rules drive local uptake, while high-density digital infrastructure creates aggregation risk that underwriters model in far more detail than in neighboring markets. Because most headquarters share a single data-center corridor, insurers routinely cap single-site exposure and add sub-limits for cloud outages that could paralyze multiple clients at once. The Personal Data Protection Commission’s ability to levy fines up to 10% of turnover elevates regulatory-investigation cover to a core policy section rather than a bolt-on. These factors combine to produce higher per-policy limits than the regional average and explain why domestic premiums remain structurally above those in Malaysia or Indonesia.

The second growth vector stems from Singapore’s role as the regional service hub for multinationals that operate across ASEAN. Most large corporate towers written in Singapore extend cover to entities in Bangkok, Jakarta, and Ho Chi Minh City, effectively pulling cross-border premium into the local booking center. The world-first ASEAN cyber-risk pool pledges up to USD 1 billion of blended capacity, enabling carriers to write large, region-wide limits without breaching aggregation thresholds. Willis Towers Watson’s USD 15 million CyCore Asia facility focuses on Singapore and Hong Kong exposures, reflecting the two cities’ concentration of high-value data assets. As more regional regulators adopt Singapore-style breach laws, demand for unified contract language governed by Singapore law is expected to rise, reinforcing the city-state’s hub status.

Alternative capital cements Singapore’s geographic advantage. MS Amlin’s Phoenix Re sidecar expanded to USD 90 million for the 2025 renewal, showing fresh investor appetite for Asian cyber risk linked to the Singapore market share of global ILS flows. Cyber catastrophe bonds totaling USD 575 million in 2024 used the Special Purpose Reinsurance Vehicle framework, which offers tax incentives and expedited licensing that few other ASEAN jurisdictions can match. The Monetary Authority’s ILS grant, extended through 2025, reimburses up to 100% of issuance costs and draws sponsors seeking an Asian domicile for global cyber placements. These tools deepen available limits, stabilize pricing, and position Singapore as the natural capital gateway for any company seeking regional cyber cover.

Competitive Landscape

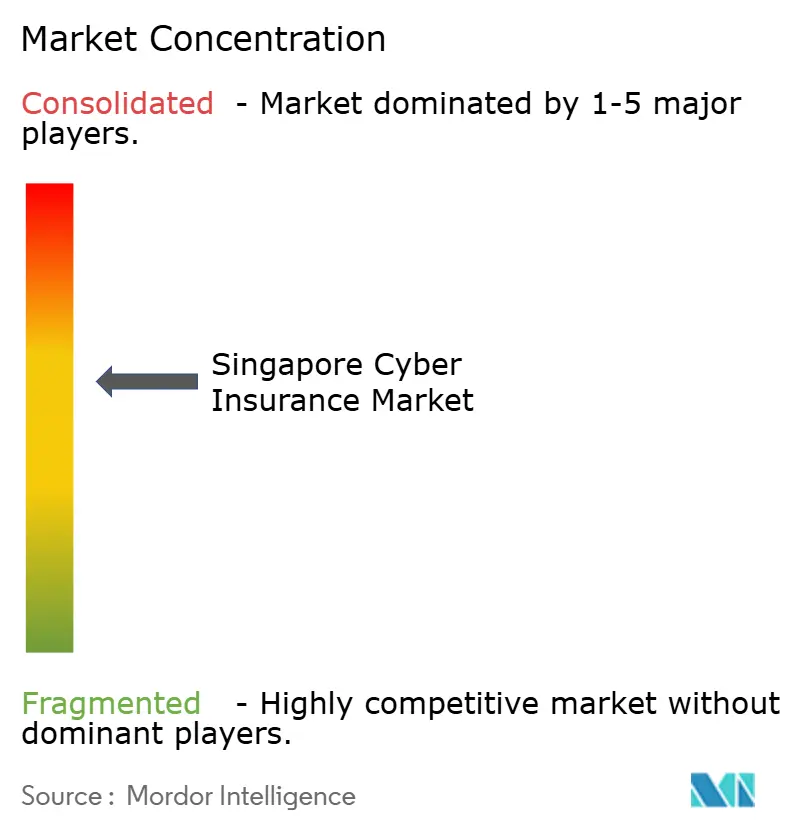

The Singapore cyber insurance market features moderate concentration, with the five largest players holding major market gross written premiums in 2025. Chubb, which wrote USD 573.6 million in global cyber premiums in 2023, leverages that scale to secure ample reinsurance and offer limits that smaller rivals cannot match locally. AXA XL differentiates through product innovation, as demonstrated by its October 2024 Gen-AI endorsement that covers data poisoning and AI IP breaches. AIG and Beazley round out the lead pack, each offering incident-response coaches and threat-intelligence feeds that appeal to regulated financial institutions. Price competition has intensified because global cyber rates softened 6-7% from 2022 peaks, prompting incumbents to add coinsurance clauses to protect profitability.

Specialist entrants have carved out profitable niches. Delta Insurance, the first Lloyd’s coverholder devoted to cyber and technology lines in Singapore, targets middle-market clients with policies that bundle pre-breach security audits. QBE advances an ecosystem strategy via QBE Ventures, investing in security analytics startups that feed telemetry directly into underwriting models for risk-based pricing. Beazley’s USD 300 million Quantum catastrophe bond shows how hybrid carrier-capital-markets structures can offload systemic risk and support higher line sizes on cloud-dependency covers. These moves sharpen competition and force traditional carriers to match service breadth rather than rely on balance-sheet depth alone.

Insurtech challengers pursue the underserved SME segment. Cyber Sierra raised USD 4.3 million to automate risk scoring and embed quotes inside accounting software, although its SGD 232,000 revenue in 2023 highlights the early stage of adoption. PolicyPal distributes micro-sized limits through mobile apps, positioning itself as an on-ramp for firms unable to meet enterprise-grade underwriting criteria. Brokers also adapt: Lockton Re openly supports government-backed risk pools to widen capacity for systemic events and reduce single-carrier accumulation. Over the next five years, market share shifts are likely to hinge on each player’s ability to pair preventive cyber-services with flexible balance-sheet solutions, while alternative capital exerts downward pressure on primary pricing.

Singapore Cyber Insurance Industry Leaders

Chubb

AIG

Beazley

Tokio Marine

Allianz

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2025: Lockton Re publicly supported government-backed cyber pools as a means to grow penetration and manage systemic exposures, spotlighting industry alignment on public-private cooperation.

- January 2025: MS Amlin expanded its Singapore-domiciled Phoenix Re sidecar to USD 90 million for 2025 renewals, a 12.5% capacity hike reflecting stronger investor appetite for Asian cyber risk.

- October 2024: AXA XL introduced a Gen-AI endorsement for CyberRiskConnect, covering data poisoning, usage-rights infringement, and AI regulation violations across global portfolios.

- September 2024: The PDPC accepted voluntary undertakings from KB Group Entities and MISC Group after breaches that exposed the personal data of more than 100,000 individuals, reinforcing enforcement vigor.

Singapore Cyber Insurance Market Report Scope

Cyber liability insurance or cyber insurance covers individuals and businesses in the event of a cyber-attack or data breach where the information of an individual and customer is impacted. It helps reduce the financial risk associated with doing business online in case of a data breach or any other online fraud in return for a certain premium to the insurer.

The Singapore cyber liability insurance market is segmented by end-users and by industry. By end-user, the market is sub-segmented into personal, SMEs, and corporates, and by industry, the market is sub-segmented into financial services, government bodies/agencies, healthcare, professional services, and other industries. The report offers the market sizes and forecast values (USD) for all the above segments.

By Product Type (Value)

| Packaged |

| Stand-alone |

By Enterprise Size (Value)

| Large Enterprises |

| Medium Enterprises |

| Small & Micro Enterprises |

By Industry Vertical (Value)

| BFSI |

| IT & Telecom |

| Retail & E-commerce |

| Healthcare & Life Sciences |

| Manufacturing |

| Government & Public Sector |

| Education |

| By Product Type (Value) | Packaged |

| Stand-alone | |

| By Enterprise Size (Value) | Large Enterprises |

| Medium Enterprises | |

| Small & Micro Enterprises | |

| By Industry Vertical (Value) | BFSI |

| IT & Telecom | |

| Retail & E-commerce | |

| Healthcare & Life Sciences | |

| Manufacturing | |

| Government & Public Sector | |

| Education |

Key Questions Answered in the Report

How large is the Singapore cyber insurance market in 2026?

The Singapore cyber insurance market size is USD 61.78 million in 2026 and is projected to reach USD 94.73 million by 2031.

What is the growth rate forecast for Singapore cyber cover?

The market is set to expand at a 8.93% CAGR from 2026 to 2031.

Which product type currently leads in Singapore?

Stand-alone policies hold 53.65% market share and are growing faster than packaged extensions.

Which enterprise segment is expanding the quickest?

Small and micro enterprises show the fastest uptake with a 9.46% CAGR, aided by Cyber Essentials and other government programs.

Why is the BFSI sector the largest buyer of cyber policies?

Strict Monetary Authority guidelines and high-value digital assets push financial institutions to purchase broad cyber limits and incident-response cover.

How does Singapore attract additional cyber capacity?

The Special Purpose Reinsurance Vehicle regime and ILS grant scheme encourage cyber catastrophe bond issuance and sidecar structures that add depth to available limits.

Page last updated on: