Market Overview

| Study Period | 2021 - 2031 |

|---|---|

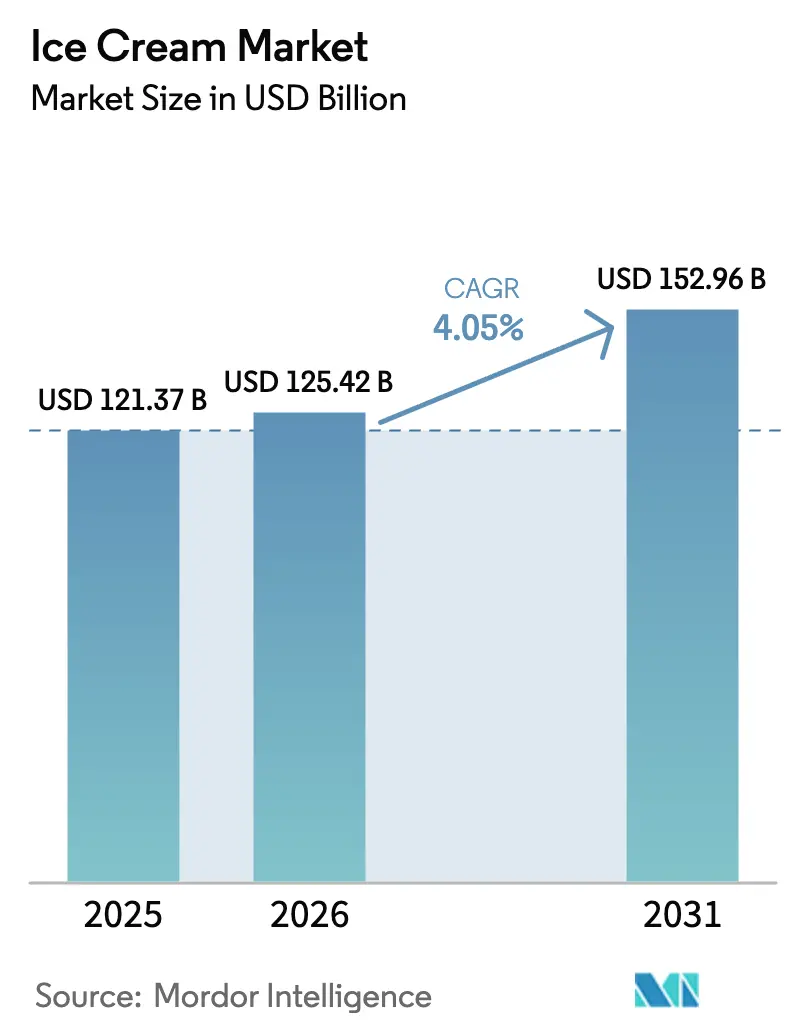

| Market Size (2026) | USD 125.42 Billion |

| Market Size (2031) | USD 152.96 Billion |

| Growth Rate (2026 - 2031) | 4.05% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Ice Cream Market Analysis by Mordor Intelligence

The Ice Cream Market is expected to grow from USD 121.37 billion in 2025 to USD 125.42 billion in 2026 and is forecasted to reach USD 152.96 billion by 2031 at 4.05% CAGR over 2026-2031. Standard variants continue to account for the majority of sales volume; however, premium, artisan, and functional products are gaining shelf space and increasing average unit prices. Growth in the ice cream market is also being driven by rapid flavor innovation, plant-based product development, and the expansion of quick-commerce platforms that shorten delivery times and promote impulse purchases. Health-focused reformulations, such as GLP-1-friendly and high-protein recipes, are shifting product portfolios toward premium offerings, despite higher ingredient costs. Brands that meet clean-label standards and provide verifiable sustainability credentials are securing retailer support and building consumer loyalty. While North America remains the largest regional market, Asia-Pacific is the fastest-growing region, supported by rising disposable incomes and the modernization of organized retail channels.

Key Report Takeaways

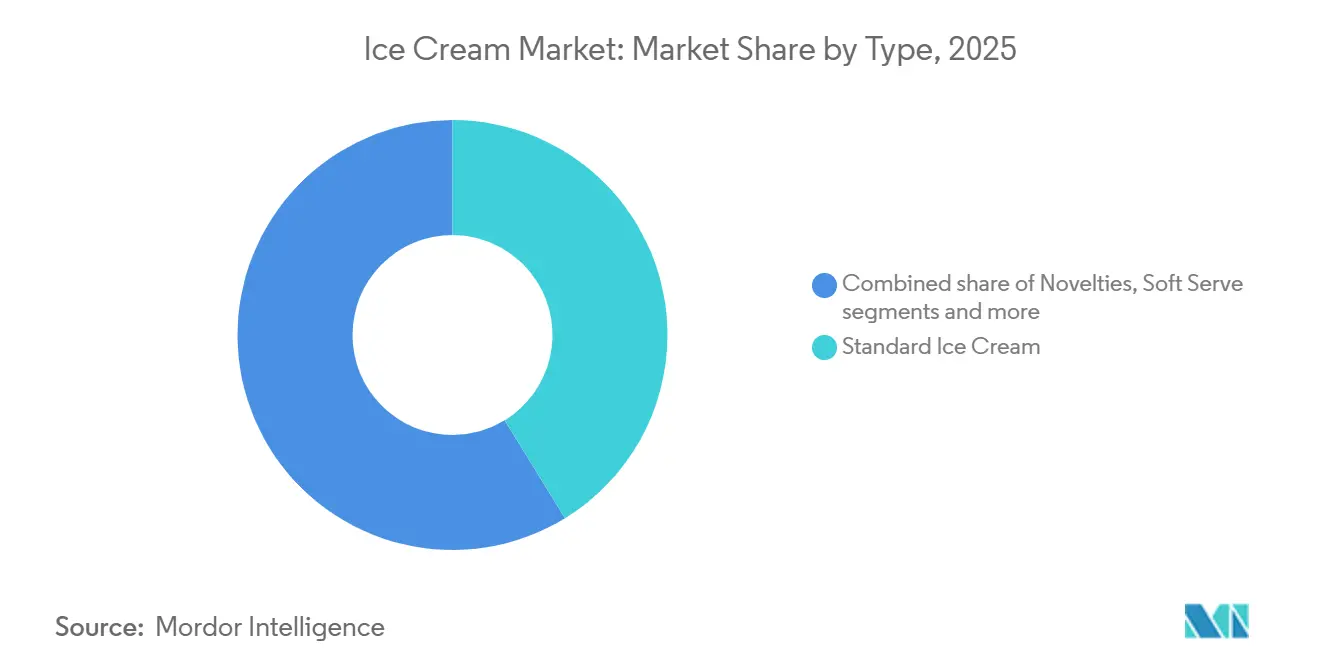

- By type, standard formats accounted for 41.23% of the 2025 value, whereas specialty and artisanal products are set to post a 4.55% CAGR through 2031.

- By category, the dairy segment accounted for 81.23% of the revenue in 2025, while the non-dairy segment is projected to grow at a CAGR of 5.43% through 2031.

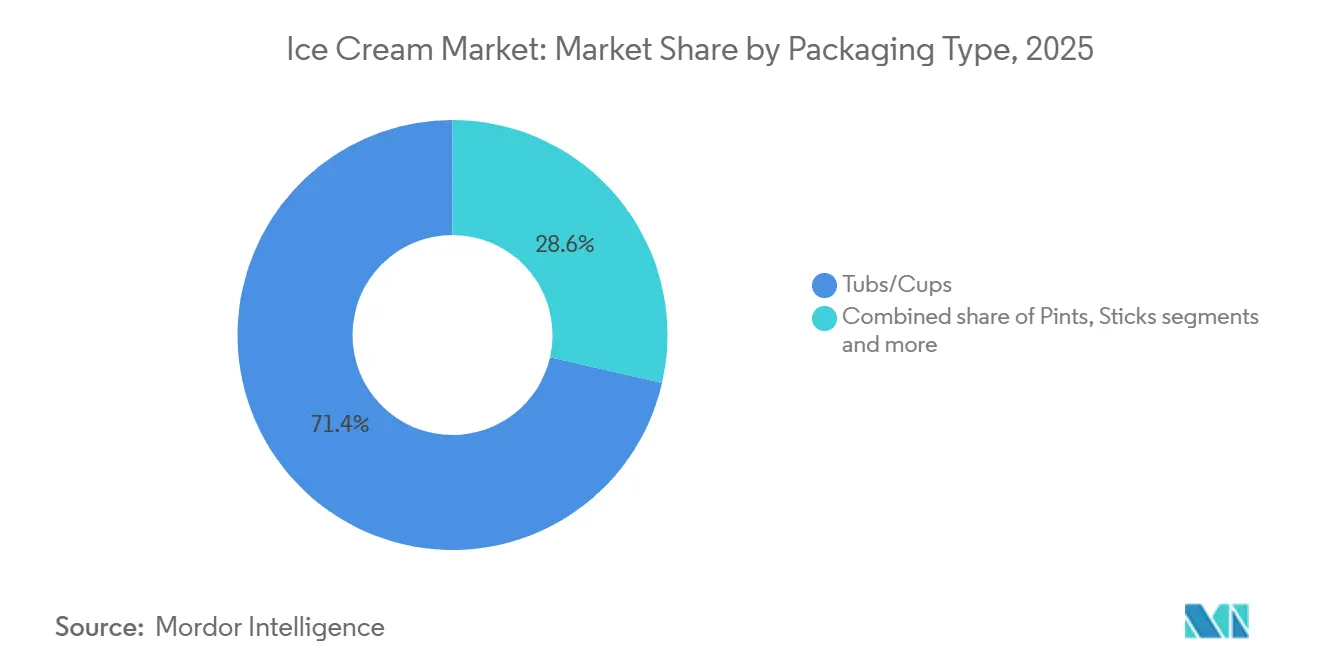

- By packaging, tubs and cups commanded 72.13% of the 2025 value, while pints are projected to expand at a 4.98% CAGR through 2031.

- By distribution channel, the off-trade maintained a 78.71% share in 2025; however, on-trade venues are expected to grow at a 5.66% CAGR over the same horizon.

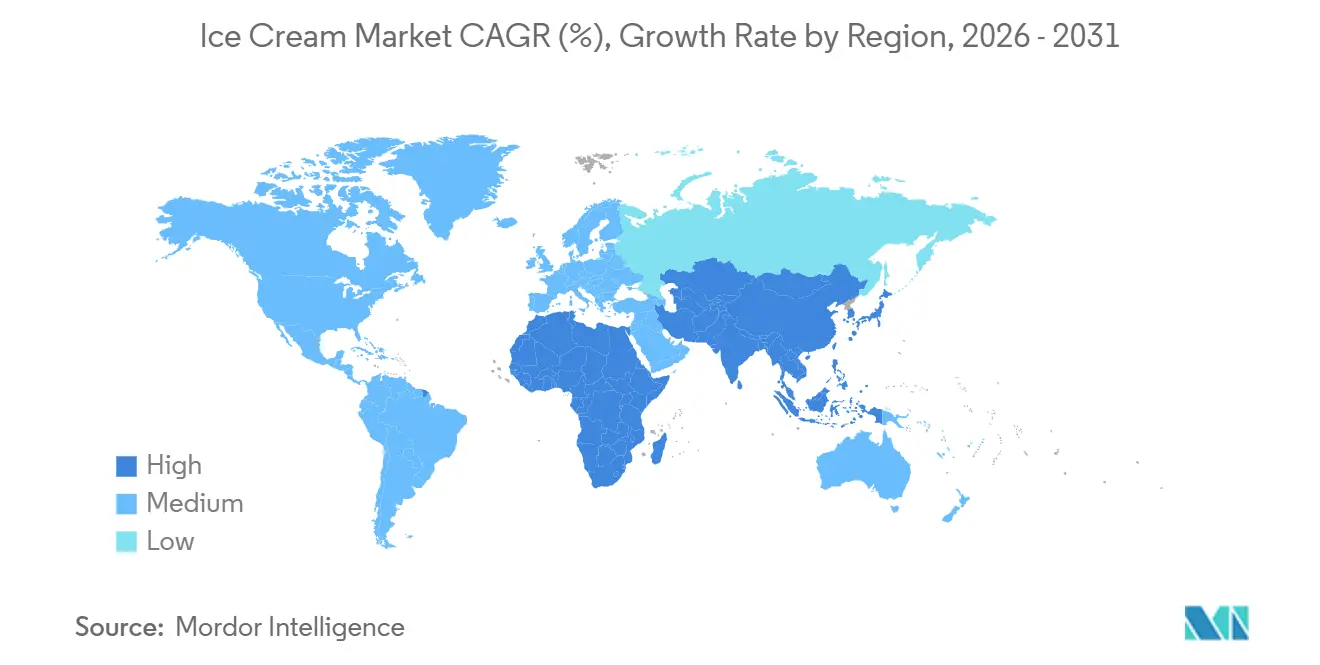

- By geography, North America held the largest revenue share, at 30.87%, in 2025. The Asia-Pacific region is expected to record the fastest CAGR of 6.15% through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Ice Cream Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Increasing demand for health-focused ice creams | +1.2% | Global, with early adoption in North America and Europe | Medium term (2-4 years) |

| Preference for clean-label and natural ingredients | +0.8% | North America, Europe, Asia-Pacific urban centers | Short term (≤ 2 years) |

| Innovation in products and flavor experimentation | +0.9% | Global, particularly strong in Asia-Pacific and North America | Short term (≤ 2 years) |

| Growing demand for premium, high-end, and artisan ice cream products | +1.1% | North America, Europe, Asia-Pacific affluent segments | Medium term (2-4 years) |

| Trends in customization and experiential consumption | +0.7% | North America, Europe, Asia-Pacific urban markets | Medium term (2-4 years) |

| Focus on sustainability and ethical sourcing | +0.6% | Europe, North America, select Asia-Pacific markets | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Increasing demand for health-focused ice creams

Functional reformulation is reshaping product portfolios as brands aim to attract health-conscious consumers without compromising indulgence. In 2025, Two Spoons and Oppo Pro introduced GLP-1 (Glucagon-Like Peptide-1)-friendly ice creams containing 30 to 40 grams of protein per pint, targeting consumers on weight-management medications who seek satiating desserts with minimal blood-sugar impact. In 2024, Smearcase launched a cottage cheese-based formulation delivering 20 grams of protein per serving while maintaining a creamy texture, aligning with the high-protein trend influencing yogurt and snack categories. Low-sugar variants utilizing allulose, a rare sugar with minimal glycemic impact, are gaining traction, particularly in North America and Europe, where diabetes prevalence and obesity rates remain high. This trend is compressing margins for standard formulations and compelling incumbents to invest in ingredient research and development as well as clinical validation to support health claims. The growing demand for such products reflects a broader shift in consumer preferences, with a focus on health benefits and nutritional value, as brands strive to meet the needs of a population increasingly aware of the impact of diet on overall well-being.

Preference for clean-label and natural ingredients

Consumer scrutiny of ingredient lists has increased, prompting brands to replace artificial colors, flavors, and preservatives with recognizable, minimally processed alternatives. The European Food Safety Authority's proposed restrictions on titanium dioxide, a whitening agent used in certain ice cream formulations, led to reformulations across multiple stock-keeping units (SKUs) in 2024. While this shift raised ingredient costs, it aligned with consumer preferences for natural additives. Natural alternatives, such as beet juice for color, vanilla extract for flavor, and guar gum for stabilization, often cost 20% to 30% more than synthetic options and may affect shelf stability, posing formulation challenges for manufacturers. Clean-label positioning has emerged as a competitive advantage, with brands that transparently disclose ingredient sourcing and processing methods commanding premium pricing and fostering consumer trust. This trend is particularly significant among millennial and Generation Z consumers, who prioritize transparency and are willing to pay a premium for products that reflect their values. Regulatory frameworks, including Food and Drug Administration labeling requirements and European Union Regulation No. 1169/2011, mandate detailed ingredient disclosure, increasing compliance costs but ensuring accountability across the category [1]Source: European Commission, "Food information to consumers - legislation," food.ec.europa.eu.

Innovation in products and flavor experimentation

Exotic and fusion flavors are transitioning from niche parlors to mass retail, driven by younger consumers' demand for novelty and social media appeal. Flavors such as matcha, ube, pandan, and baklava-inspired variants gained popularity in 2025, particularly in urban markets across Asia-Pacific and North America, as brands aim to diversify beyond traditional options like vanilla and chocolate. Dessert-inspired crossovers, including tiramisu, churro, and s'mores, combine familiar flavor profiles with added textural complexity through inclusions and swirls. A consumer survey revealed that 75% of respondents view trying unique flavors as an enjoyable experience, while 68% express a preference for nostalgic sweet treats. This creates a dual challenge for innovation teams to balance novelty with comfort. Brand collaborations further support this trend: for instance, Ben & Jerry's partnered with musician Noah Kahan in 2025 to release a limited-edition flavor, and Ore-Ida collaborated with goodpop to develop potato-inspired frozen treats, blurring traditional category boundaries and generating earned media. While this experimentation cycle shortens product life spans and increases SKU proliferation costs, it also maintains consumer engagement and encourages trial rates.

Growing demand for premium, high-end, and artisan ice cream products

Premiumization is no longer limited to specialty stores, as mainstream retailers are allocating more shelf space to artisan brands that command 30% to 50% price premiums over standard products. The share of frozen novelties in the North American market increased from 45% in 2018 to a projected 53% by 2025. Dollar sales in this segment are expected to grow by 10% between 2024 and 2028, surpassing volume growth and indicating consumers' willingness to pay for innovation and quality. Small-batch producers, such as Van Leeuwen and Jeni's Splendid Ice Creams, have expanded their distribution into national grocery chains, capitalizing on Instagram-driven brand equity and limited-edition collaborations. For instance, Häagen-Dazs partnered with the "Emily in Paris" television series in 2024 to launch co-branded flavors, which sold out within weeks. This trend is creating a bifurcated market: value-oriented players compete on price and volume, while premium brands emphasize storytelling, ingredient provenance, and sensory differentiation. Consequently, the middle tier faces margin compression, and undifferentiated brands encounter higher barriers to entry.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Dependence on cold chain and storage limitations | -0.9% | Global, particularly acute in South Asia, Africa, Latin America | Short term (≤ 2 years) |

| High sensitivity to temperature fluctuations | -0.5% | Global, with greater impact in regions with unreliable power infrastructure | Short term (≤ 2 years) |

| Short shelf life compared to ambient desserts | -0.4% | Global, especially challenging in rural and remote markets | Medium term (2-4 years) |

| Regulatory scrutiny on additives and labeling | -0.6% | North America, Europe, select Asia-Pacific markets | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Dependence on cold chain and storage limitations

Infrastructure limitations in emerging markets restrict distribution reach and increase logistics costs, creating a structural barrier to volume growth. Ice cream requires consistent storage temperatures between -18°C and -23°C throughout the supply chain, as even brief temperature rises above -12°C can lead to ice-crystal formation, negatively impacting texture and consumer satisfaction. In India, where the organized ice cream market is growing at double-digit rates, insufficient cold-chain infrastructure in tier-2 and tier-3 cities hampers brand penetration. Quick-commerce platforms, which enable delivery within 60 minutes by consolidating demand, partially address this issue but are limited to urban areas. Last-mile delivery remains the most expensive segment, accounting for up to 40% of total logistics costs in markets with fragmented retail networks. Manufacturers are increasingly adopting Internet of Things (IoT)-enabled temperature sensors and smart freezers to ensure real-time compliance monitoring. However, adoption rates remain low among independent retailers due to limited capital for equipment upgrades. Additionally, energy costs further compound the challenge, as maintaining sub-zero temperatures in tropical climates can double refrigeration expenses compared to temperate regions. This significantly reduces profitability for regional manufacturers.

High sensitivity to temperature fluctuations

Even slight deviations from optimal storage conditions can cause irreversible quality degradation, posing operational risks throughout the supply chain. For instance, ice cream stored above -12°C for just 30 minutes undergoes ice-crystal growth, resulting in a grainy texture that reduces consumer satisfaction, potentially leading to product returns and brand reputation damage. Power outages in regions with unreliable electricity infrastructure—common in sub-Saharan Africa, parts of South Asia, and rural Latin America—often force retailers to discard inventory, increasing shrinkage rates and reducing profit margins. Transportation delays caused by heat waves or equipment failures can compromise entire shipments, especially on long-haul routes where refrigerated trucks must maintain precise temperatures for 12 to 48 hours. To address these challenges, manufacturers are investing in phase-change materials and advanced insulation to enhance temperature stability; however, these solutions increase packaging costs by 10 to 15%. Additionally, climate change is intensifying these issues, as rising ambient temperatures heighten cooling demands, increase energy consumption, and strain aging cold-chain infrastructure in both developed and emerging markets, creating a persistent structural challenge for volume growth.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Type: Specialty Formats Gain Share Despite Standard Dominance

In 2025, standard ice cream held a significant 41.23% share of the global ice cream market, underscoring its position as the most widely consumed and commercially stable format. This dominance is attributed to its widespread acceptance across various age groups, driven by familiar flavors such as vanilla, chocolate, strawberry, and traditional regional variants that consistently maintain high consumption levels. Standard ice cream benefits from mass production scalability and formulation stability, enabling manufacturers to produce large volumes while ensuring consistent taste, texture, and shelf life across different markets. Its strong presence in both on-trade (sales through restaurants, cafes, and similar establishments) and off-trade (sales through retail outlets) channels enhances visibility and accessibility, fostering repeat purchases and habitual consumption.

Specialty and artisanal ice cream formats are projected to grow at a compound annual growth rate (CAGR) of 4.55% through 2031, reflecting a gradual shift in consumer preferences toward premium, experiential, and unique products. This growth is supported by rising demand for craft-style production, small-batch formulations, and innovative flavor profiles, including ethnic desserts, gourmet inclusions, and seasonal or limited-edition offerings. Consumers increasingly prioritize authenticity, ingredient transparency, and sensory appeal, positioning artisanal ice creams as indulgent treats rather than mass-market desserts. The segment's growth is further bolstered by the proliferation of boutique parlors, specialty dessert outlets, and premium retail spaces, enabling brands to achieve higher profit margins while enhancing brand differentiation and storytelling.

By Category: Plant-Based Gains Share Despite Taste Gaps

Dairy-based ice cream formats accounted for 81.23% of the global ice cream market in 2025, highlighting their continued dominance and essential role within the category. These products remain deeply ingrained in consumer preferences due to their rich texture, superior creaminess, and familiar sensory appeal. While plant-based alternatives aim to replicate these attributes, they have not yet achieved the same level of widespread acceptance. The extensive availability of dairy-based products across standard, novelty, soft-serve, and premium segments further strengthens their market leadership. This variety allows manufacturers to cater to a broad range of consumption occasions, from everyday family desserts to spontaneous indulgences.

Non-dairy ice cream alternatives are projected to grow at a compound annual growth rate (CAGR) of 5.43% through 2031, reflecting a consistent shift toward plant-based and dairy-free consumption patterns within the frozen dessert category. This growth is primarily driven by increasing consumer awareness of lactose intolerance, milk allergies, and digestive sensitivities, along with a rising interest in vegan and flexitarian diets. Advances in plant-based formulation technologies, using bases such as almond, oat, coconut, soy, and pea, have significantly improved taste, texture, and creaminess. These developments have narrowed the sensory gap with traditional dairy ice cream, enhancing the mainstream appeal of non-dairy options to a broader audience.

By Packaging Type: Pints Gain as Households Shrink

Tubs and cups collectively accounted for a significant 72.13% share of the global ice cream market in 2025, underscoring their position as the primary and most versatile packaging formats across retail and foodservice channels. This dominance is attributed to their suitability for take-home, family consumption, and portion-controlled single-serve usage, catering to a wide range of consumer needs. Tubs are particularly preferred for multi-serve and value-oriented purchases, while cups effectively address individual indulgence, on-the-go consumption, and controlled serving sizes, thereby maintaining their volume leadership. Their adaptability across various consumer occasions further solidifies their importance in the market.

Pint packaging formats are projected to grow at a CAGR of 4.98% through 2031, reflecting their increasing relevance as a premium, portion-controlled, and indulgence-focused packaging option in the global ice cream market. This growth is closely linked to premiumization trends, with brands leveraging this format to highlight high-quality ingredients, dense textures, and innovative flavor profiles. Pints are especially popular for single-serve or shared indulgence occasions, appealing to consumers seeking convenience and a treat-oriented experience without committing to larger family-sized packs. Furthermore, the format's ability to cater to evolving consumer preferences for premium, artisanal, and innovative ice cream offerings enhances its growth potential, making it a key driver in the market's premium segment.

By Distribution Channel: On-Trade Margins Lure Investment

Off-trade channels accounted for a dominant 78.71% of global ice cream sales in 2025, underscoring their critical role as the primary route to market for ice cream consumption worldwide. This dominance is largely driven by the strong penetration of supermarkets, hypermarkets, convenience stores, and increasingly online retail platforms, which offer consumers greater accessibility, variety, and purchase flexibility compared to on-trade formats. Off-trade channels are particularly well suited to take-home and multi-serve consumption, aligning closely with the popularity of tubs, cups, and pint formats that support family and repeat usage occasions. Additionally, the adaptability of off-trade channels to evolving consumer demands, their ability to provide competitive pricing, and the convenience of bulk purchasing further reinforce their position as the leading choice for ice cream distribution globally.

On-trade venues are projected to grow at a CAGR of 5.66% through 2031, reflecting a steady recovery and structural growth in out-of-home ice cream consumption across foodservice formats. This growth is driven by the increasing popularity of ice cream parlors, cafés, quick-service restaurants (QSRs), casual dining chains, and dessert-focused outlets. In these settings, ice cream is positioned as an experiential and premium product rather than a commodity. On-trade channels allow brands to offer freshly served, customizable, and visually appealing formats such as soft serve, scoops, sundaes, and specialty desserts, enhancing consumer engagement and supporting higher price points. For example, according to the United States Department of Agriculture (USDA), food sales at foodservice outlets in the United States reached USD 1.52 trillion in 2024, underscoring the significant consumption base and traffic potential available to ice cream manufacturers through on-trade partnerships [2]Source: United States Department of Agriculture (USDA), "Food Service Industry", ers.usda.gov. As foodservice operators continue to expand dessert menus with seasonal flavors, premium toppings, and limited-time ice cream offerings, ice cream is increasingly recognized as a high-margin add-on item.

Geography Analysis

North America is expected to maintain a dominant position in the global ice cream market, accounting for 30.87% of revenue in 2025. This dominance is driven by deeply ingrained consumer habits and well-established distribution networks. According to the International Dairy Foods Association (IDFA), 73% of consumers consumed ice cream at least once per week in 2024, with two out of three preferring to indulge in the evening [3]Source: International Dairy Foods Association (IDFA), "Ice Cream Sales & Trends", idfa.org. This highlights ice cream's role as a staple comfort food across various demographics. Frequent consumption, coupled with innovations in premium flavors, plant-based alternatives, and novelty formats, sustains strong demand. In the United States, parlor culture and seasonal promotions further reinforce the region's market leadership.

The Asia-Pacific region is projected to grow at a compound annual growth rate (CAGR) of 6.15% through 2031, making it the fastest-growing market. This growth is driven by rapid urbanization, changing lifestyles, and increasing per-capita consumption in emerging markets such as China and India. Urban consumers in densely populated cities are seeking convenient and indulgent treats to fit their busy schedules, boosting demand for novelties and soft-serve ice creams. The expansion of foodservice outlets and e-commerce platforms further supports this growth. Localization of flavors, incorporating tropical fruits and fusion elements, caters to diverse consumer preferences. Additionally, investments in cold-chain logistics are addressing infrastructure challenges, positioning the region for accelerated development.

Europe continues to experience steady growth in the ice cream market, operating within a stringent regulatory framework that emphasizes food safety, clean labeling, and sustainability standards. While these regulations present challenges, they also drive refinement in product offerings. Countries such as Germany, Italy, and the Netherlands focus on artisanal and dairy-based ice creams, supported by premiumization and seasonal tourism. South America and the Middle East and Africa face challenges due to underdeveloped cold-chain infrastructure, which increases spoilage risks and limits off-trade penetration. Despite these obstacles, rising health trends and growing imports in urban centers such as Brazil and the United Arab Emirates present opportunities for market growth. These regions show potential for development as infrastructure improves and consumer preferences evolve.

Competitive Landscape

The ice cream industry exhibits moderate consolidation, with a few multinational corporations dominating the market. Companies such as Nestlé S.A., General Mills, Inc., Blue Bell Creameries LP, Wells Enterprises Inc., and Lotte Corporation leverage extensive distribution networks, strong brand equity, and economies of scale to secure significant market shares. These major players maintain their leadership through diversified product portfolios, encompassing standard, novelty, and premium segments. Competition is driven by strategies such as aggressive marketing, seasonal campaigns, and acquisitions of regional brands. Meanwhile, smaller artisanal producers focus on niche specialty offerings to differentiate themselves in the market.

Significant growth opportunities exist in the plant-based and non-dairy ice cream segments, where established players face competition from agile startups and vegan-focused innovators. These challengers are disrupting the traditional dairy market. Companies like Nestlé and General Mills have introduced products such as plant-based pints and low-sugar novelties to address this trend. However, gaps remain in scalable and affordable options, particularly in vegan soft-serve and artisanal blends designed for lactose-intolerant consumers in high-growth regions like Asia-Pacific. The rapid expansion of this segment provides entry points for new players, emphasizing clean-label and allergen-free innovations. This shift in consumer preferences toward sustainable and health-conscious indulgence is pressuring major companies to increase their Research and Development investments.

Technological advancements are intensifying competition within the ice cream industry. Leading companies are adopting AI-driven flavor development, automated cold-chain monitoring, and precision manufacturing to improve efficiency and product quality. For instance, Wells Enterprises and Mars are utilizing blockchain technology to enhance traceability in ethical sourcing. Additionally, digital tools are enabling personalized e-commerce experiences and advanced data analytics for demand forecasting, providing these companies with a competitive edge over fragmented local players. Emerging technologies, such as 3D-printed custom ice creams and lab-grown dairy alternatives, are shaping the future of the industry. These innovations are prompting established players to collaborate with or acquire startups to maintain their market positions and meet evolving consumer demands for transparency and novelty.

Ice Cream Industry Leaders

-

Nestlé S.A.

-

General Mills, Inc.

-

Blue Bell Creameries LP

-

Wells Enterprises Inc.

-

Lotte Corporation

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2025: Oppo Brothers has expanded its range of low-calorie ice creams with the introduction of Oppo Refreshed, a vegan ice cream sorbet line. This range features Sicilian Lemon & Strawberry, Alphonso Mango & Passionfruit, and Raspberry Coulis Swirl flavors.

- April 2025: Kwality Wall’s has introduced a new brand, The Dairy Factory, offering a range of slow-churned ice creams. The product line includes four popular variants: Vanilla, Butterscotch, Mango, and Chocolate, available in party packs and tubs.

- March 2025: Havmor Ice Cream has partnered with Swiggy Instamart to introduce a limited-edition Thandai Ice Cream family pack, available exclusively on Swiggy Instamart.

- July 2024: Snoop Dogg introduced two new flavors to his Dr. Bombay Ice Cream line: Baked Blueberry Muffin and Peanut Butter Jelly Time. These flavors join the existing Strawberry Cream Dream option.

Global Ice Cream Market Report Scope

Ice cream is a sweetened frozen food typically eaten as a snack or dessert. The global ice cream market is segmented by product type, category, packaging type, distribution channel, and geography. By product type, the market is segmented into standard ice cream, novelties, soft serve, and specialty/artisanal ice cream. By category, the market is segmented into dairy and non-dairy. By packaging type, the market is segmented by pints, tubs/cups, sticks, and others. By distribution channel, the market is segmented into on-trade and off-trade. Off-trade is further sub-segmented into convenience stores, specialist retailers, supermarkets/hypermarkets, online retail stores, and other distribution channels. By geography, the market is segmented into North America, Europe, Asia-Pacific, South America, and the Middle East and Africa. The report provides market size and forecasts in both value (USD) and volume (Liters) for all the mentioned segments.

By Type

| Standard Ice Cream |

| Novelties |

| Soft Serve |

| Specialty/Artisanal Ice Cream |

By Category

| Dairy |

| Non-Dairy |

By Packaging Type

| Pints |

| Tubs/Cups |

| Sticks |

| Others |

By Distribution Channel

| On-trade | |

| Off-trade | Convenience Stores |

| Specialist Retailers | |

| Supermarkets and Hypermarkets | |

| On-line Retail | |

| Others |

By Geography

| North America | United States |

| Canada | |

| Mexico | |

| Rest of North America | |

| Europe | Germany |

| United Kingdom | |

| Italy | |

| France | |

| Spain | |

| Netherlands | |

| Poland | |

| Belgium | |

| Sweden | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| Australia | |

| Indonesia | |

| South Korea | |

| Thailand | |

| Singapore | |

| Rest of Asia-Pacific | |

| South America | Brazil |

| Argentina | |

| Colombia | |

| Chile | |

| Peru | |

| Rest of South America | |

| Middle East and Africa | South Africa |

| Saudi Arabia | |

| United Arab Emirates | |

| Nigeria | |

| Egypt | |

| Morocco | |

| Turkey | |

| Rest of Middle East and Africa |

| By Type | Standard Ice Cream | |

| Novelties | ||

| Soft Serve | ||

| Specialty/Artisanal Ice Cream | ||

| By Category | Dairy | |

| Non-Dairy | ||

| By Packaging Type | Pints | |

| Tubs/Cups | ||

| Sticks | ||

| Others | ||

| By Distribution Channel | On-trade | |

| Off-trade | Convenience Stores | |

| Specialist Retailers | ||

| Supermarkets and Hypermarkets | ||

| On-line Retail | ||

| Others | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Rest of North America | ||

| Europe | Germany | |

| United Kingdom | ||

| Italy | ||

| France | ||

| Spain | ||

| Netherlands | ||

| Poland | ||

| Belgium | ||

| Sweden | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| Australia | ||

| Indonesia | ||

| South Korea | ||

| Thailand | ||

| Singapore | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Argentina | ||

| Colombia | ||

| Chile | ||

| Peru | ||

| Rest of South America | ||

| Middle East and Africa | South Africa | |

| Saudi Arabia | ||

| United Arab Emirates | ||

| Nigeria | ||

| Egypt | ||

| Morocco | ||

| Turkey | ||

| Rest of Middle East and Africa | ||

Market Definition

- Butter - Butter is a yellow-to-white solid emulsion of fat globules, water, and inorganic salts produced by churning the cream from cows’ milk

- Dairy - Dairy product include milk and any of the foods made from milk, including butter, cheese, ice cream, yogurt, and condensed and dried milk.

- Frozen Desserts - Frozen dairy dessert means and includes products containing milk or cream and other ingredients which are frozen or semi-frozen prior to consumption, such as ice milk or sherbet, including frozen dairy desserts for special dietary purposes, and sorbet

- Sour Milk Drinks - Sour milk is thick, curdled milk, with a sour taste, obtained from the fermentation of milk. Sour milk drinks such as kefir, laban, buttermilk have been considered in the study

| Keyword | Definition |

|---|---|

| Cultured Butter | Cultured butter is prepared by having the raw butter go through chemical processing and has been added with certain emulsifiers and foreign ingredients. |

| Uncultured Butter | This type of butter is one which has not been processed in any way |

| Natural Cheese | The type of cheese in its most natural form. It is made from natural and simple products and ingredients, including fresh and natural salts, natural colors, enzymes, and high-quality milk. |

| Processed Cheese | Processed cheese undergoes the same processes as natural cheese; however, it requires more steps and many different forms of ingredients. Making processed cheese involves melting natural cheese, emulsifying it, and adding preservatives and other artificial ingredients or colorings. |

| Single Cream | Single cream contains around 18% fat. It’s a single layer of cream that appears over boiled milk. |

| Double Cream | Double cream contains 48% fat, more than double the amount of fat of single cream. It’s heavier and thicker than single cream |

| Whipping Cream | This has a much higher fat percentage than single cream (36%). Used to top cakes, pies, and puddings and as a thickener for sauces, soups, and fillings. |

| Frozen Desserts | Desserts that are meant to be eaten in frozen condition. E.g., sherbets, sorbets, frozen yogurts |

| UHT Milk (Ultra-high temperature milk) | Milk heated at a very high temperature. Ultra-high-temperature processing (UHT) of milk involves heating for 1–8 sec at 135–154°C. which kills the spore-forming pathogenic microorganism, resulting in a product with a shelf-life of several months. |

| Non-dairy butter/Plant-based butter | Butter made from plant-derived oil such as coconut, palm, etc. |

| Non-dairy Yogurt | Yogurt made from typically made from nuts, like almonds, cashews, coconuts, and even other foods like soybeans, plantains, oats, and peas |

| On-trade | It refers to restaurants, QSRs, and bars. |

| Off-trade | It refers to supermarkets, hypermarkets, on-line channels, etc. |

| Neufchatel cheese | One of the oldest kinds of cheese in France. It is a soft, slightly crumbly, mold-ripened, bloomy-rind cheese made in the Neufchâtel-en-Bray region of Normandy. |

| Flexitarian | It refers to a consumer preferring a semi-vegetarian diet, that is centered on plant foods with limited or occasional inclusion of meat. |

| Lactose Intolerance | Lactose intolerance is a reaction in digestive system to lactose, the sugar in milk. It causes uncomfortable symptoms in response to the consumption of dairy products. |

| Cream Cheese | Cream cheese is a soft and creamy fresh cheese with a tangy taste made from milk and cream. |

| Sorbets | Sorbet is a frozen dessert made using ice combined with fruit juice, fruit purée, or other ingredients, such as wine, liqueur, or honey. |

| Sherbet | Sherbet is a sweetened frozen dessert made with fruit and some sort of dairy product such as milk or cream. |

| Shelf stable | Foods that can be safely stored at room temperature, or "on the shelf," for at least one year and do not have to be cooked or refrigerated to eat safely. |

| DSD | Direct Store Delivery is the process in supply chain management wherein the product is delivered from manufacturing plant directly to the retailer. |

| OU Kosher | Orthodox Union Kosher is a kosher certification agency based in New York City. |

| Gelato | Gelato is a frozen creamy dessert made with milk, heavy cream and sugar. |

| Grass-fed Cows | Grass-fed cows are allowed to graze in pastures, where they eat a variety of grasses and clover. |

Research Methodology

Mordor Intelligence follows a four-step methodology in all our reports.

- Step-1: Identify Key Variables: In order to build a robust forecasting methodology, the variables and factors identified in Step 1 are tested against available historical market numbers. Through an iterative process, the variables required for market forecast are set, and the model is built on the basis of these variables.

- Step-2: Build a Market Model: Market-size estimations for the forecast years are in nominal terms. Inflation is not a part of the pricing, and the average selling price (ASP) is kept constant throughout the forecast period for each country.

- Step-3: Validate and Finalize: In this important step, all market numbers, variables, and analyst calls are validated through an extensive network of primary research experts from the market studied. The respondents are selected across levels and functions to generate a holistic picture of the market studied.

- Step-4: Research Outputs: Syndicated Reports, Custom Consulting Assignments, Databases & Subscription Platforms