Industrial Starches Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Market Size (2026) | USD 59.53 Billion |

| Market Size (2031) | USD 72.82 Billion |

| Growth Rate (2026 - 2031) | 4.11% CAGR |

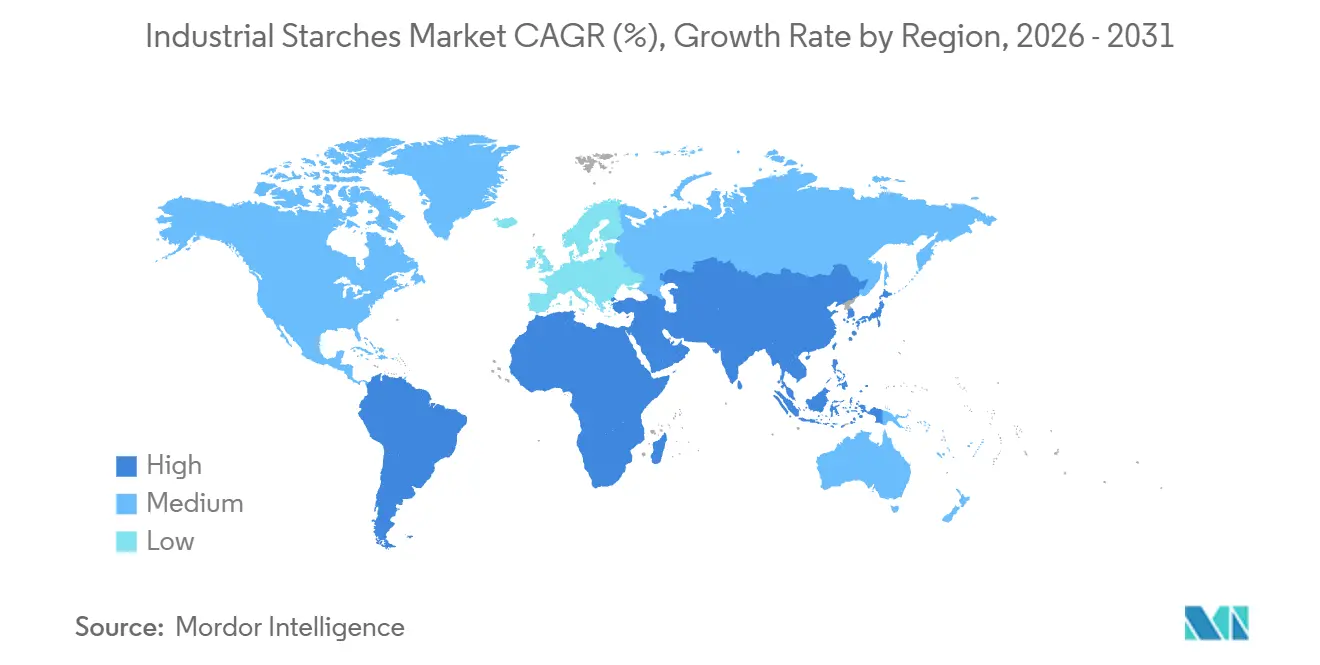

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

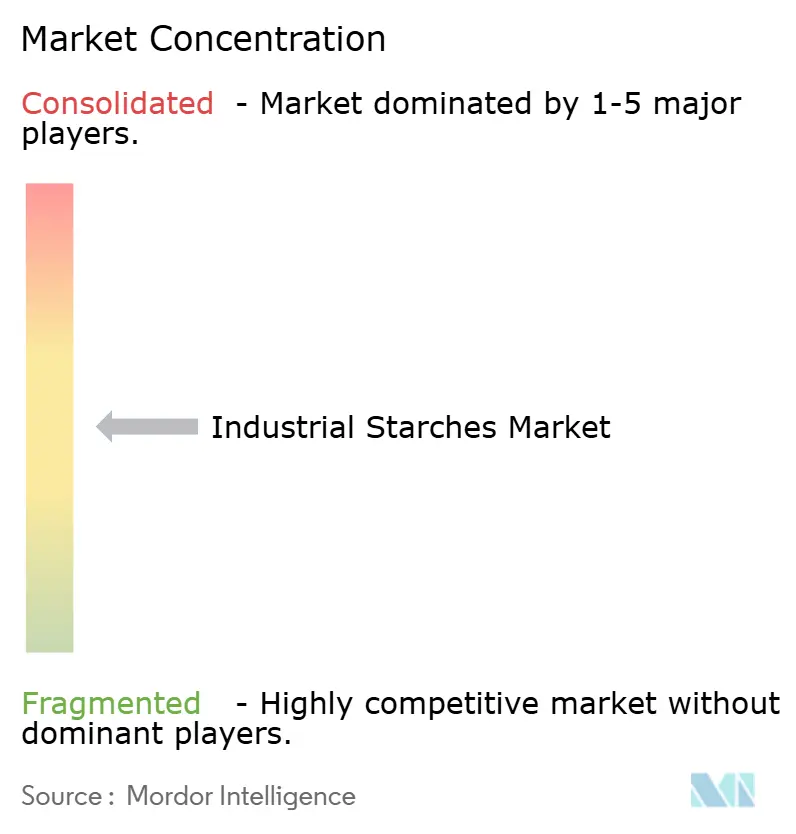

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Industrial Starches Market Analysis by Mordor Intelligence

The industrial starches market size was valued at USD 57.27 billion in 2025 and is estimated to grow from USD 59.53 billion in 2026 to reach USD 72.82 billion by 2031, at a CAGR of 4.11% during the forecast period (2026-2031). Corn-derived products are expected to dominate the market, contributing significantly to revenue in the year 2025. Meanwhile, cassava-based alternatives are witnessing steady growth, driven by their non-genetically modified organism (non-GMO) positioning, which aligns well with Europe’s labeling regulations. The demand for native starch is on the rise, particularly in clean-label bakery and dairy product formulations. At the same time, packaging converters are increasingly adopting starch-polymer blends to comply with extended-producer responsibility requirements set forth in California and the European Union. In the pharmaceutical industry, manufacturers are enhancing their use of modified starch grades that adhere to the standards of the United States Pharmacopeia and the European Pharmacopoeia, without necessitating allergen labeling. While North America continues to lead in terms of volume, the Asia-Pacific region is emerging as the fastest-growing market, supported by expansions in cassava production capacity in Thailand and a rise in tablet manufacturing in India.

Key Report Takeaways

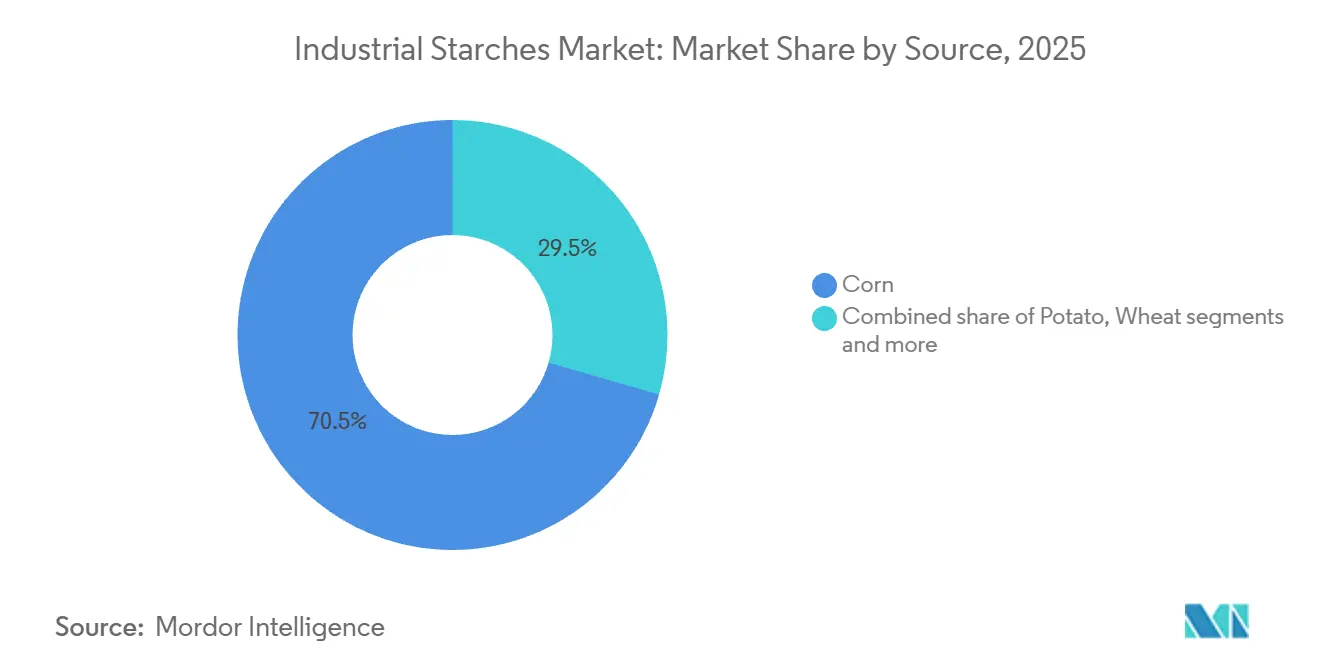

- By source, corn held 70.54% of industrial starch market share in 2025; tapioca is projected to grow at an 7.82% CAGR from 2026-2031.

- By type, native grades accounted for 66.98% of industrial starch market size in 2025, while modified variants are expected to post a 5.35% CAGR through 2031.

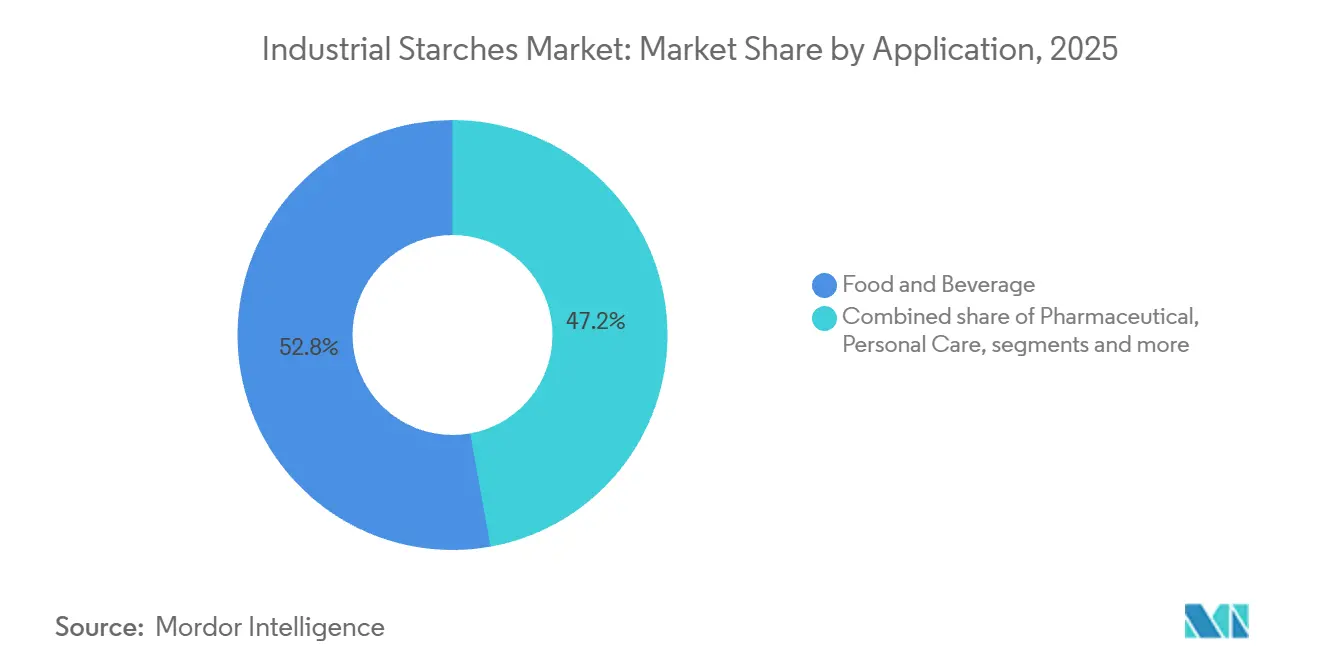

- By application, food and beverage led with 52.83% revenue share in 2025; pharmaceutical use is set to expand at a 6.62% CAGR to 2031.

- By geography, North America captured 30.56% of industrial starch market share in 2025, whereas Asia-Pacific is advancing at a 6.11% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Industrial Starches Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Increasing consumption of processed and convenience foods | +0.8% | Global, with concentration in North America, Europe, and urban Asia-Pacific | Medium term (2-4 years) |

| Shift toward clean-label and natural ingredients | +0.9% | North America and Europe lead; Asia-Pacific adoption accelerating | Short term (≤ 2 years) |

| Rise of plant-based and gluten-free product formulations | +0.6% | North America and Europe core; spillover to urban South America and Asia-Pacific | Medium term (2-4 years) |

| Expansion of pharmaceutical sector using starch as binder and disintegrant | +0.7% | Asia-Pacific (India, China), North America, Europe | Long term (≥ 4 years) |

| Widespread adoption of starches in paper, paperboard, and textile sizing/coating | +0.5% | Global, with mature demand in Europe and North America; growth in Asia-Pacific | Long term (≥ 4 years) |

| Growing demand for bio-based and biodegradable products in packaging | +0.8% | Europe (driven by EU regulations), North America (California), Asia-Pacific emerging | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Increasing consumption of processed and convenience foods

Urbanization and the increasing prevalence of dual-income households are significantly contributing to the growing consumption of ready-to-eat meals, bakery products, and shelf-stable sauces. These products heavily rely on starches to provide essential properties such as texture, viscosity, and freeze-thaw stability. According to the United States Department of Agriculture, processed food shipments in the Asia-Pacific region have experienced notable growth, with starch-intensive categories like instant noodles and frozen dumplings leading the way in terms of volume. Modified waxy-maize starches are being adopted as a replacement for guar gum in salad dressings due to their ability to endure high-shear mixing and acidic pH levels without causing syneresis, a technical advantage that clean-label brands emphasize in their front-of-pack claims. In Latin America, snack manufacturers are reformulating extruded products by incorporating tapioca starch to achieve a desirable crispness while reducing oil absorption. This approach not only lowers production costs but also aligns with consumer preferences for healthier product options. The shift from traditional home cooking to industrial food preparation has concentrated starch demand among a smaller number of larger buyers. This trend provides formulators with increased negotiating power but also raises expectations for consistent quality, a standard that only top-tier suppliers are equipped to meet effectively at scale.

Shift toward clean-label and natural ingredients

Retailers in North America and Europe are increasingly requiring ingredient lists with fewer than ten components, prompting brands to replace chemically modified starches with native or physically modified alternatives that consumers perceive as minimally processed. According to the annual report released by Ingredion for the year 2025, the demand for clean-label starches has shown remarkable growth, significantly surpassing the overall performance of the starch division. This shift is largely driven by bakery and dairy manufacturers reformulating their products to avoid E-number declarations, which are mandated by the labeling regulations of the European Union [1]Source: United States Department of Agriculture, “National Organic Program Document Cover Sheet,” ams.usda.gov. Native tapioca starch is increasingly being used as a substitute for acetylated and hydroxypropylated variants in organic yogurt production. This is because it complies with the certification requirements of the United States Department of Agriculture (USDA) National Organic Program without necessitating additional documentation, thereby streamlining supply chain audits. However, native starches come with certain limitations, such as narrower processing windows, the tendency to retrograde during refrigerated storage, and shear-thinning when subjected to high-speed mixing. These challenges often compel formulators to use higher quantities or combine them with hydrocolloids, which can negatively impact profit margins. Although the European Food Safety Authority conducted a re-evaluation of modified starches in 2024 and found no safety concerns, consumer skepticism remains strong. This ongoing sentiment continues to sustain the premium pricing for "clean" alternatives and drives the adoption of enzyme-based modification methods that do not involve chemical reagents [2]Source: European Food Safety Authority, “National Organic Program Document Cover Sheet,” efsa.europa.eu.

Rise of plant-based and gluten-free product formulations

Plant-based meat analogs and dairy-free desserts require starches that replicate the mouthfeel and water-binding capacity of animal proteins and fats. Pea and potato starches fulfill this functional requirement more effectively than corn starch because of their neutral flavor and fine granule size, which make them ideal for such applications. As highlighted in the sustainability report released by Oatly, the company utilizes potato starch in its barista-blend oat milk to achieve the desired microfoam stability required for espresso-based beverages. This is a performance specification that corn starch cannot meet without undergoing a chemical modification process known as acetylation. This example underscores the importance of carefully selecting starches that meet the functional, sensory, and performance demands of plant-based and dairy-free products. By making informed ingredient choices, companies can ensure their products consistently deliver the quality, texture, and overall experience that consumers expect in this dynamic and growing food category.

Expansion of pharmaceutical sector using starch as binder and disintegrant

Generic-drug manufacturers in India and China are significantly increasing tablet production to meet the growing healthcare demands driven by aging populations and the expansion of health insurance coverage. Starch-based excipients are widely chosen due to their excellent compressibility, affordability, and regulatory acceptance across multiple pharmacopeias. India's pharmaceutical exports have achieved remarkable growth in recent years, while the country's imports of starch-based excipients have also risen considerably, as domestic maize-starch production has not kept pace with the increasing installation of tablet-press machinery. Pregelatinized starches, which are processed through drum drying to enable direct compression without the need for wet granulation, are becoming increasingly popular. These starches help manufacturers streamline production by reducing batch cycle times and eliminating the requirement for drying ovens, which in turn significantly lowers energy costs per kilogram of finished tablets. The United States Food and Drug Administration (FDA) has introduced guidance for excipient traceability, requiring pharmaceutical starch suppliers to document the geographic origin of raw materials such as corn or potato. This regulation places a greater advantage on integrated producers with captive farms, as opposed to brokers who rely on sourcing spot cargoes. Furthermore, modified starches like sodium starch glycolate are extensively utilized as superdisintegrants in orally disintegrating tablets, a dosage form that is projected by the European Medicines Agency (EMA) to account for a growing share of new drug applications in the coming years.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Regulatory complexity and variations across food, pharma, and packaging standards | -0.4% | Global, with acute friction in cross-border trade between North America, Europe, and Asia-Pacific | Long term (≥ 4 years) |

| Stringent GMO restrictions on corn-based starches | -0.3% | Europe, parts of South America (Argentina, Brazil selective bans), and select Asia-Pacific markets | Medium term (2-4 years) |

| Variability in agricultural supply due to weather, droughts, and crop diseases | -0.5% | Global, with hotspots in Southeast Asia (cassava), South America (corn), and Europe (potato) | Short term (≤ 2 years) |

| Complex processing requirements for modified starches | -0.3% | Global, affecting smaller regional processors lacking capital for cleanroom and enzymatic modification infrastructure | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Regulatory complexity and variations across food, pharma, and packaging standards

Divergent definitions of "modified starch" create compliance challenges. The United States Food and Drug Administration (FDA) allows enzymatic hydrolysis under the "native" label, while the European Food Safety Authority (EFSA) classifies the same process as a modification requiring E-number disclosure [3]Source: Food and Drug Administration, “Foods Derived from Plants Produced Using Genome Editing: Guidance for Industry,”fda.gov. This discrepancy forces multinational brands to maintain separate formulations and packaging artwork for each market. India's Food Safety and Standards Authority (FSSAI) has introduced draft starch-purity standards that impose stricter heavy-metal residue limits compared to those set by Codex Alimentarius. This compels importers to source starch from mills equipped with ion-exchange purification, a capability available only at a limited number of global facilities. Pharmaceutical starch must comply with United States Pharmacopeia (USP) monograph specifications for microbial limits, residue on ignition, and pH. However, the European Pharmacopoeia enforces stricter tolerances on sulfur dioxide residues, requiring suppliers to either conduct dual production campaigns or forgo access to one of the markets. Additionally, packaging-film converters face uncertainty as the European Union's proposed Packaging and Packaging Waste Regulation deliberates whether starch-polyester blends qualify for composting certification. This decision will significantly influence capital investments in extrusion lines over the next several years.

Stringent GMO restrictions on corn-based starches

The European Union's zero-tolerance policy for unapproved genetically modified organism (GMO) events in food imports has resulted in the rejection of numerous United States corn-starch shipments since the year 2024. Even minimal detections of genetically modified maize have led to port rejections and forced re-exports, causing substantial financial losses for exporters. In September 2025, Reuters reported that several corn-starch containers intended for European bakery customers were denied entry at the port of Rotterdam. This decision was based on polymerase chain reaction testing, which identified the presence of genetically modified event MIR162, a strain that has not been authorized by the European Food Safety Authority. Argentina and Brazil have implemented selective bans on genetically modified organisms for organic and specialty food channels, further complicating South American starch supply chains. Exporters are now facing higher traceability costs as they are required to segregate non-GMO corn from general commodity flows. In Japan, labeling laws require the disclosure of genetically modified corn starch in products where starch exceeds a certain percentage of the formulation weight. This has prompted confectionery brands to source identity-preserved non-GMO starch, despite the associated cost premium. In response to these challenges, United States corn-starch producers are expanding non-GMO acreage through contract farming. However, non-GMO yields remain lower than those of genetically modified hybrids, which reduces profit margins and slows the pace at which non-GMO supply can grow.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Source: Cassava Gains on Corn Despite Infrastructure Gap

In 2025, corn accounted for 70.54% of industrial starch revenue, driven by the United States Midwest's long-established wet-milling infrastructure and corn's high amylose content, which is advantageous for film-forming applications. However, tapioca and cassava are experiencing the fastest growth among all source segments, with an annual growth rate of 7.82% projected through 2031. Thailand's cassava-starch exports reached 3.2 million metric tons in 2025, an 11% increase, as European food brands sought non-genetically modified organism (non-GMO) certification and a lower water footprint to diversify supply chains heavily reliant on United States corn. Potato starch, while ranking third in volume, commands a 20% to 30% price premium in pharmaceutical excipients due to its phosphate ester groups, which enhance tablet disintegration without chemical modification. This clean-label advantage is being leveraged by generic-drug manufacturers in India.

Wheat starch remains a niche product, primarily used in European paper-coating mills for its fine granule size and low gelatinization temperature. However, volatility in gluten co-product prices, as wheat gluten prices fluctuated by 40% in 2025, has discouraged capacity expansions. The growing preference for cassava is altering trade dynamics. In 2024, Vietnam commissioned two new tapioca-starch plants with a combined annual capacity of 180,000 metric tons, targeting pharmaceutical and biodegradable-film markets where corn's genetically modified organism (GMO) association poses a barrier to market access. Despite its growth, cassava's lower amylose-to-amylopectin ratio limits its application in high-clarity films and retort-stable sauces, where corn and potato starches maintain technical advantages.

By Type: Modified Starches Capture Pharmaceutical and Packaging Premiums

Native starches accounted for 66.98% of the projected 2025 volume, driven by clean-label requirements in the food and beverage industry. However, modified starches are experiencing an annual growth rate of 5.35%, fueled by demand from pharmaceutical tablet manufacturers and biodegradable-film producers for functional properties such as controlled viscosity, freeze-thaw stability, and acid resistance, which unmodified starches cannot provide. Acetylated starches, produced by esterifying hydroxyl groups with acetic anhydride, offer advantages such as preventing retrogradation in refrigerated sauces and dairy desserts. This performance benefit supports a price premium of 15% to 25% over native starches.

Hydroxypropylated starches are widely used in frozen food applications due to their ether linkages, which inhibit syneresis during freeze-thaw cycles, reducing purge loss in microwaveable meals by up to 40% compared to native corn starch. Cross-linked starches, created by reacting starch with phosphorus oxychloride or sodium trimetaphosphate, are capable of withstanding high shear and acidic pH conditions, making them suitable for canned soups and fruit fillings. However, the European Union's E-number labeling requirement (E1442 for acetylated cross-linked starch) has led to consumer skepticism, limiting adoption in organic and premium product categories.

By Application: Pharmaceutical Growth Outpaces Mature Food Segment

Food and beverage applications accounted for 52.83% of the industrial starch demand in 2025. However, pharmaceutical applications are projected to grow at an annual rate of 6.62% through 2031, marking the fastest growth among application segments. This growth is driven by the scaling of generic drug production in India, China, and Southeast Asia. In fiscal 2025, India's tablet production increased by 16%, with starch-based binders and disintegrants comprising 8% to 12% of the formulation weight in immediate-release dosage forms. Pregelatinized maize starch is the preferred excipient for direct-compression tablets due to its free-flowing and uniform compression properties, which eliminate the need for wet-granulation steps, thereby reducing batch cycle times by 24 to 48 hours. The United States Food and Drug Administration (FDA) 2024 drug-shortage task force identified the concentration of excipient supply as a systemic risk. This has led pharmaceutical buyers to adopt dual sourcing of starch from North American and European suppliers, despite a 10% to 15% cost increase.

In personal care applications, such as dry shampoos, face powders, and talc-free body powders, modified starches are increasingly used for their oil absorption properties and silky skin feel. This segment is expanding as talc faces regulatory scrutiny due to concerns over asbestos contamination. Paper, cardboard, and corrugated-board sizing consumed approximately 18% of the starch volume in 2025. This is a mature application where cationic and amphoteric starch modifications are replacing native starches to enhance wet-end retention and reduce freshwater consumption per ton of paper by 12% to 18%, aligning with International Organization for Standardization (ISO) 14001 environmental standards. Textile sizing for warp yarns in weaving mills remains a stable application. However, synthetic sizing agents, such as polyvinyl alcohol and acrylic copolymers, are increasingly used in high-speed looms, where starch's limited abrasion resistance can lead to thread breaks.

Geography Analysis

North America accounted for 30.56% of the industrial starch revenue in 2025, driven by the United States Corn Belt's integrated wet-milling complexes, which co-produce high-fructose corn syrup, corn oil, and animal-feed gluten. Ingredion's USD 50 million expansion in Cedar Rapids, completed in February 2025, added 120,000 metric tons of annual corn-starch capacity to cater to pharmaceutical and clean-label food markets, highlighting North America's shift toward higher-margin specialty starch grades. The United States Food and Drug Administration's 2024 excipient traceability guidance is increasing compliance costs for smaller starch producers, consolidating market share among the top four millers capable of investing in electronic batch-record systems and third-party audits. Canada's starch industry remains export-focused, with wheat-starch mills in Saskatchewan supplying United States paper-coating customers. However, the 2025 Canada-United States softwood lumber dispute indirectly impacted starch demand by reducing corrugated-box orders for construction materials.

The Asia-Pacific region is experiencing the fastest growth, with an annual rate of 6.11% projected through 2031. This growth is driven by cassava-starch capacity expansions in Thailand, Indonesia, and Vietnam, increased pharmaceutical tablet production in India, and the adoption of biodegradable packaging in China's e-commerce sector. Thailand's tapioca-starch exports reached 3.2 million metric tons in 2025, with non-GMO (non-genetically modified organism) certification enabling access to European and Japanese food markets that previously relied on United States corn starch. India's starch imports rose by 14% in fiscal 2025 as domestic maize-starch production struggled to meet pharmaceutical demand. The Food Safety and Standards Authority of India is drafting purity standards that could benefit domestic producers once implemented. In China, the biodegradable-packaging mandate, effective January 2025 in 46 cities, is driving the use of starch-polybutylene adipate terephthalate blends in food-delivery containers. However, cost premiums of 40% to 60% over polystyrene are limiting adoption beyond tier-one urban centers.

Europe's industrial starch market is balancing clean-label consumer preferences with the European Union's Packaging and Packaging Waste Regulation, which requires 65% recycled content in plastic packaging by 2030. This regulation is encouraging the use of starch-polyester blends that biodegrade in industrial composting. Germany's potato-starch production declined by 6% in 2025 due to late-blight issues, but the country remains the European Union's largest producer, with Emsland Group and Avebe controlling two-thirds of the region's capacity. The European Food Safety Authority's 2024 re-evaluation of modified starches found no safety concerns. However, clean-label claims on packaging continue to favor native and enzymatically modified starches, putting pressure on margins for acetylated and cross-linked variants.

Competitive Landscape

The industrial starch market demonstrates moderate concentration, with the top four global producers, Cargill, Ingredion, Tate and Lyle, and Roquette, controlling a significant portion of nameplate capacity. At the same time, regional cassava millers in Southeast Asia, potato-starch cooperatives in Europe, and specialty modifiers in North America account for the fragmented remainder. Leading players are adopting a dual strategy that includes backward integration into non-genetically modified organism (non-GMO) corn and cassava farming to secure clean-label feedstock, and forward integration into application-development laboratories to co-create formulations with pharmaceutical and packaging customers. This approach enables them to establish multi-year supply agreements that smaller commodity millers cannot replicate. For example, Ingredion's 2025 joint venture with Agrana to construct a specialty-starch facility in Romania combines Ingredion's expertise in modification with Agrana's European distribution network, targeting the region's bakery and pharmaceutical sectors.

White-space opportunities are emerging in starch-based biopolymers for flexible packaging. These applications, such as polybutylene adipate terephthalate (PBAT) blends, require advanced extrusion expertise that traditional wet-millers often lack. This gap creates opportunities for partnerships with chemical companies like BASF and Novamont. Technology is becoming a key differentiator for market leaders. Innovations such as enzymatic modification processes that avoid E-number labeling, continuous processing lines that reduce batch cycle times by 30 percent, and blockchain traceability platforms that meet pharmaceutical regulatory requirements are setting tier-one suppliers apart from regional commodity producers. An example of this is Tate and Lyle's patent filing for a cold-water-soluble starch produced via high-pressure homogenization, which eliminates the need for chemical cross-linking and protects margins in mature product categories.

Emerging disruptors include cassava-starch startups in Vietnam and Indonesia. These companies are bypassing traditional wet-milling processes by using mobile flash-drying units at farm gates, which reduce logistics costs and capture a larger share of the farm-to-factory value chain. However, maintaining quality consistency remains a challenge for pharmaceutical qualification. Compliance with International Organization for Standardization (ISO) 22000 food-safety management and ISO 14001 environmental standards is essential for multinational accounts. Yet, smaller mills in South America and Africa often lack the capital to undergo third-party audits, thereby losing high-value export opportunities to certified competitors.

Industrial Starches Industry Leaders

Cargill Inc.

Archer Daniels Midland Co.

Tate and Lyle PLC

Roquette Frères SA

Emsland Group

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- July 2025: Brenntag Specialties and Royal Avebe have extended their starch distribution partnership to the United States, introducing Dutch potato starches and derivatives to North American food and nutrition markets. This expansion focuses on the bakery, dairy, meat-alternative, and confectionery segments.

- December 2024: Tate & Lyle has announced a strategic partnership with BioHarvest Sciences to develop advanced plant-based ingredient molecules utilizing botanical synthesis technology. The collaboration will initially focus on botanical sweetening ingredients, with potential expansion into additional areas.

- November 2024: Tate & Lyle finalized a USD 1.8 billion merger with CP Kelco, forming a global specialty food and beverage solutions company. The combined entity employs approximately 5,000 individuals across 75 locations in 39 countries. This merger significantly enhances capabilities in pectin, specialty gums, and hydrocolloids, complementing the existing starch portfolio.

Global Industrial Starches Market Report Scope

Industrial starch is obtained from various natural sources, including wheat, corn, cassava, potato, and others. It is widely used in the paper industry, particularly in manufacturing and coating processes. The global industrial starch market is segmented by source into corn, tapioca or cassava, potato, wheat, and others. The market is further categorized by type into native starch and starch derivatives and sweeteners. Additionally, it is segmented by application into food and beverage, pharmaceutical, personal care, paper, cardboard, and corrugated board, textile, animal feed, and chemicals. The report also provides a comprehensive analysis of the industrial starch market across major economies in regions such as North America, Europe, Asia-Pacific, South America, and the Middle East and Africa. The market sizing has been done in value terms in USD and volume in Tonnes for all the abovementioned segments.

| Corn |

| Tapioca / Cassava |

| Potato |

| Wheat |

| Others |

| Native |

| Modified |

| Food and Beverage |

| Pharmaceutical |

| Personal Care |

| Paper, Cardboard, and Corrugated Board |

| Textile |

| Animal Feed |

| Chemicals |

| North America | United States |

| Canada | |

| Mexico | |

| Rest of North America | |

| Europe | Germany |

| United Kingdom | |

| Italy | |

| France | |

| Spain | |

| Netherlands | |

| Poland | |

| Belgium | |

| Sweden | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| Australia | |

| Indonesia | |

| South Korea | |

| Thailand | |

| Singapore | |

| Rest of Asia-Pacific | |

| South America | Brazil |

| Argentina | |

| Colombia | |

| Chile | |

| Peru | |

| Rest of South America | |

| Middle East and Africa | South Africa |

| Saudi Arabia | |

| United Arab Emirates | |

| Nigeria | |

| Egypt | |

| Morocco | |

| Turkey | |

| Rest of Middle East and Africa |

| By Source | Corn | |

| Tapioca / Cassava | ||

| Potato | ||

| Wheat | ||

| Others | ||

| By Type | Native | |

| Modified | ||

| By Application | Food and Beverage | |

| Pharmaceutical | ||

| Personal Care | ||

| Paper, Cardboard, and Corrugated Board | ||

| Textile | ||

| Animal Feed | ||

| Chemicals | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Rest of North America | ||

| Europe | Germany | |

| United Kingdom | ||

| Italy | ||

| France | ||

| Spain | ||

| Netherlands | ||

| Poland | ||

| Belgium | ||

| Sweden | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| Australia | ||

| Indonesia | ||

| South Korea | ||

| Thailand | ||

| Singapore | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Argentina | ||

| Colombia | ||

| Chile | ||

| Peru | ||

| Rest of South America | ||

| Middle East and Africa | South Africa | |

| Saudi Arabia | ||

| United Arab Emirates | ||

| Nigeria | ||

| Egypt | ||

| Morocco | ||

| Turkey | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

How large will the industrial starch market be by 2031?

The industrial starch market size is projected to reach USD 72.82 billion by 2031, expanding at a 4.11% CAGR from 2026 to 2031.

Which feedstock is growing fastest?

Cassava-based starch is expected to grow at a 7.82% CAGR through 2031 as non-GMO certification boosts demand in Europe and Asia-Pacific.

Why are pharmaceutical companies increasing starch usage?

Starch excipients support direct-compression tablets, meet multiple pharmacopeias, and enable orally disintegrating formats that regulators favor for pediatric and geriatric care.

What limits adoption of modified starch in clean-label foods?

EU E-number labeling and retailer ingredient-count caps make consumers skeptical of chemically modified grades, steering formulators toward native or enzyme-treated options.

Page last updated on: